MPA105 - Financial Accounting & Reporting: IFRS 16 Leases Analysis

VerifiedAdded on 2023/06/13

|10

|1947

|210

Report

AI Summary

This report provides a comprehensive analysis of IFRS 16 Leases, a new standard introduced by IASB for lease accounting, effective from January 1, 2019, replacing IAS 17. It delves into the rationale behind the standard, highlighting the shortcomings of IAS 17 in accurately representing lease transactions and the economic reality. The report discusses the implications of IFRS 16 on both lessors and lessees, noting a significant impact on lessees due to the elimination of the operating and finance lease classification. It also identifies the industries most likely to be affected, including retail, telecommunications, banking, metal and mining, transport, oil & gas and insurance companies, and concludes that IFRS 16 aims to provide more accurate and transparent information about lease transactions, enhancing the reliability of financial statements.

RUNNING HEAD: FINANCIAL ACCOUNTING AND REPORTING

IFRS 16 leases

IFRS 16 leases

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial accounting and reporting 1

Contents

Introduction...........................................................................................................................................2

IFRS 16 Leases......................................................................................................................................2

Rationale behind the standard................................................................................................................3

Implications...........................................................................................................................................4

Lessor................................................................................................................................................4

Lessee................................................................................................................................................4

Companies most likely to be affected....................................................................................................5

Conclusion.............................................................................................................................................7

References.............................................................................................................................................8

Contents

Introduction...........................................................................................................................................2

IFRS 16 Leases......................................................................................................................................2

Rationale behind the standard................................................................................................................3

Implications...........................................................................................................................................4

Lessor................................................................................................................................................4

Lessee................................................................................................................................................4

Companies most likely to be affected....................................................................................................5

Conclusion.............................................................................................................................................7

References.............................................................................................................................................8

Financial accounting and reporting 2

Introduction

A new standard for lease accounting has been developed by IASB named as IFRS 16 Leases.

It provides guidelines for lease accounting and state that the data reported must show the

accurate information about the lease transactions. The standard will come into effect from

January 1, 2019 and once applicable it will replace the old standard IAS 17 (Iasplus.com.

2018). The reports contains detailed information about IFRS 16, its implications on lessor

and lessee and the reasons behind introducing it. In the later part, it also discussed about the

companies which are likely to be affected by this.

IFRS 16 Leases

IASB published a new standard for lease reporting in January 2016, which will be in effect

from January 2019. It was introduced by IASB as part of joint project with FASB. It deals

with the new principles for disclosure and measurement of leases. A single lessee model was

established which requires a lessee to take into account all the liabilities and assets for the

leases that have a term period of more than 1 year (Deloitte UK. 2018). Under IFRS 16, lease

is defined as a contract in which customer (“lessee”) get a right to use an asset for a specified

period of time in exchange of some consideration (accaglobal.com. 2018). The introduction

of new standard will definitely impact several industries and also the accounting requirements

of lessee and lessor. The sectors which mainly get affected are retail, telecommunications,

banking, metal and mining, insurance and oil and gas entities.

However, entities that has applied for IFRS 15 Revenue from Contracts with Customers can

apply IFRS 16 in its lease accounting before its effective date. The main motive of bringing

this was to enhance the reporting of leases by eliminating their classification as financial and

operating lease. This elimination will enable the lessees to show all the leases on its balance

sheet so that true and fair picture can be represented (Ifrs.org. 2016).

Introduction

A new standard for lease accounting has been developed by IASB named as IFRS 16 Leases.

It provides guidelines for lease accounting and state that the data reported must show the

accurate information about the lease transactions. The standard will come into effect from

January 1, 2019 and once applicable it will replace the old standard IAS 17 (Iasplus.com.

2018). The reports contains detailed information about IFRS 16, its implications on lessor

and lessee and the reasons behind introducing it. In the later part, it also discussed about the

companies which are likely to be affected by this.

IFRS 16 Leases

IASB published a new standard for lease reporting in January 2016, which will be in effect

from January 2019. It was introduced by IASB as part of joint project with FASB. It deals

with the new principles for disclosure and measurement of leases. A single lessee model was

established which requires a lessee to take into account all the liabilities and assets for the

leases that have a term period of more than 1 year (Deloitte UK. 2018). Under IFRS 16, lease

is defined as a contract in which customer (“lessee”) get a right to use an asset for a specified

period of time in exchange of some consideration (accaglobal.com. 2018). The introduction

of new standard will definitely impact several industries and also the accounting requirements

of lessee and lessor. The sectors which mainly get affected are retail, telecommunications,

banking, metal and mining, insurance and oil and gas entities.

However, entities that has applied for IFRS 15 Revenue from Contracts with Customers can

apply IFRS 16 in its lease accounting before its effective date. The main motive of bringing

this was to enhance the reporting of leases by eliminating their classification as financial and

operating lease. This elimination will enable the lessees to show all the leases on its balance

sheet so that true and fair picture can be represented (Ifrs.org. 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial accounting and reporting 3

Rationale behind the standard

The main reason behind introducing IFRS 16 was to amend the approach stated under IAS

17, related to the classification of leases. IAS 17 was focused on distinguishing between the

two types of leases. Under it, the lease that transfers all the risk and reward of asset

ownership is termed as financial lease and apart from this all other leases are known as

operating leases. However, the classification set out in IAS 17 was subjective which provides

a clear benefit to the people who prepare financial statements of lessee. They can argue about

the fact that leases should be presented as operating in order to avoid the presentation of

leased assets and liabilities on the balance sheet (accaglobal.com. 2018). It was for this

reason that IASB brings new lease standard IFRS 16.

Also according to the IASB Chairman, the former lease standard does not reflect the

economic reality. As per him, more than 85% leases are recognized as operating and are not

shown on the balance sheet. As a result of which, they contribute in creating real liabilities

which may prove to be difficult for the major sectors like retail industry to cope up with the

situation of financial crisis. In addition to this, under IAS 17, companies were allowed to be

discrete about their operating leases. This led to the false and unfair representation of

company’s financial position and performance. As a result, investors find it difficult to

measure and compare the economic condition of different entities due to the faulty and

unreliable data provided by the balance sheet. In a nutshell, former standard does not reflect

economic reality which led to the introduction of IFRS 16 (Ifrs.org. 2016).

Implications

Lessor

The impact on the lessors will be minor as the requirement for them will remain unchanged.

They are required to classify the leases in the same way as it was mentioned in IAS 17.

Rationale behind the standard

The main reason behind introducing IFRS 16 was to amend the approach stated under IAS

17, related to the classification of leases. IAS 17 was focused on distinguishing between the

two types of leases. Under it, the lease that transfers all the risk and reward of asset

ownership is termed as financial lease and apart from this all other leases are known as

operating leases. However, the classification set out in IAS 17 was subjective which provides

a clear benefit to the people who prepare financial statements of lessee. They can argue about

the fact that leases should be presented as operating in order to avoid the presentation of

leased assets and liabilities on the balance sheet (accaglobal.com. 2018). It was for this

reason that IASB brings new lease standard IFRS 16.

Also according to the IASB Chairman, the former lease standard does not reflect the

economic reality. As per him, more than 85% leases are recognized as operating and are not

shown on the balance sheet. As a result of which, they contribute in creating real liabilities

which may prove to be difficult for the major sectors like retail industry to cope up with the

situation of financial crisis. In addition to this, under IAS 17, companies were allowed to be

discrete about their operating leases. This led to the false and unfair representation of

company’s financial position and performance. As a result, investors find it difficult to

measure and compare the economic condition of different entities due to the faulty and

unreliable data provided by the balance sheet. In a nutshell, former standard does not reflect

economic reality which led to the introduction of IFRS 16 (Ifrs.org. 2016).

Implications

Lessor

The impact on the lessors will be minor as the requirement for them will remain unchanged.

They are required to classify the leases in the same way as it was mentioned in IAS 17.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial accounting and reporting 4

Fundamentally, the requirements of lessor accounting has not changed under IFRS 16.

However, lessors will have new disclosure requirements. The new standard contains a

specific exemption for lessors related to the valuation of investment properties at fair value.

Some new requirements related to sales and lease back transactions are also provided by

IFRS 16. Apart from these, there is no such significant impact on the lessors (KPMG. 2016).

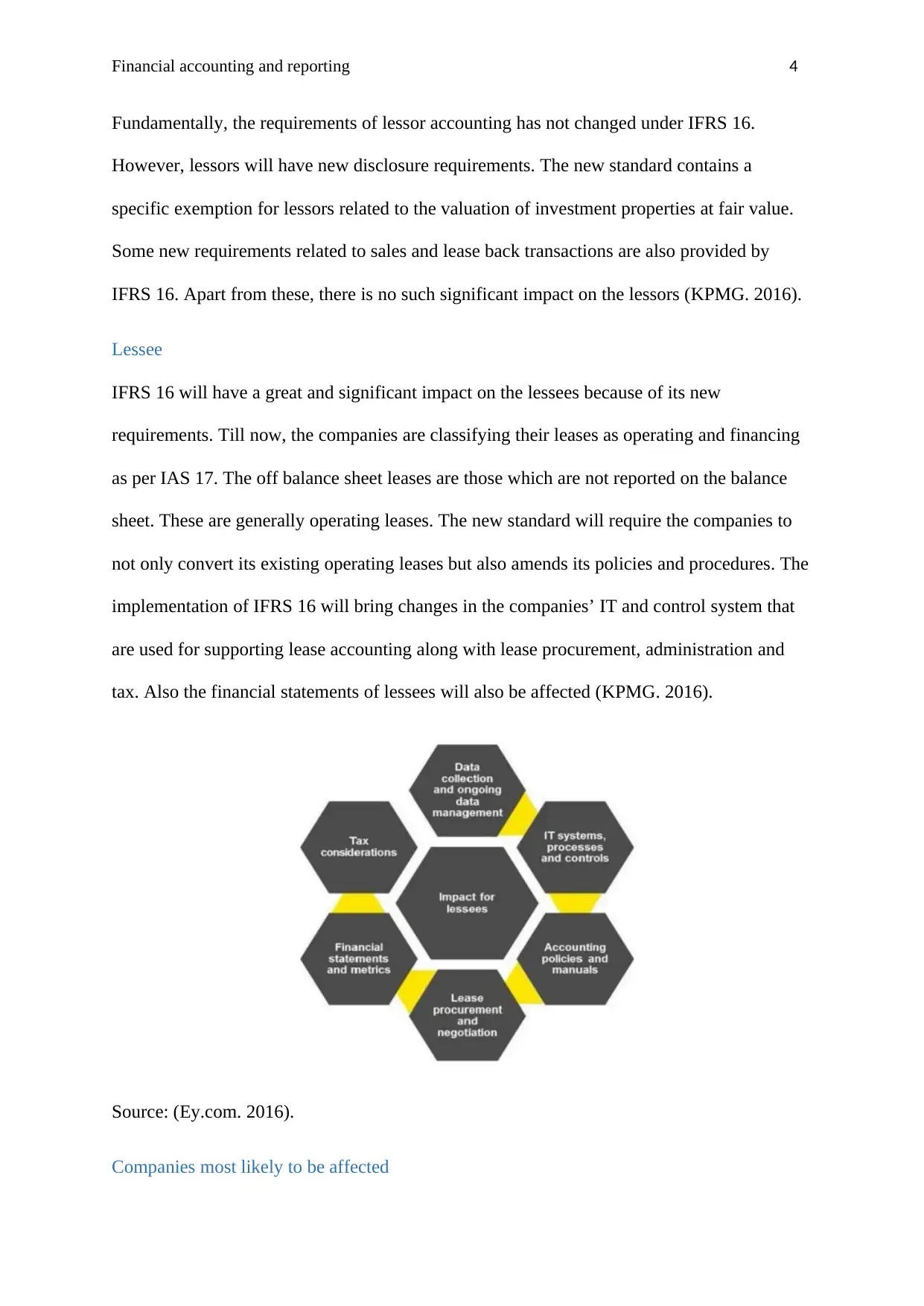

Lessee

IFRS 16 will have a great and significant impact on the lessees because of its new

requirements. Till now, the companies are classifying their leases as operating and financing

as per IAS 17. The off balance sheet leases are those which are not reported on the balance

sheet. These are generally operating leases. The new standard will require the companies to

not only convert its existing operating leases but also amends its policies and procedures. The

implementation of IFRS 16 will bring changes in the companies’ IT and control system that

are used for supporting lease accounting along with lease procurement, administration and

tax. Also the financial statements of lessees will also be affected (KPMG. 2016).

Source: (Ey.com. 2016).

Companies most likely to be affected

Fundamentally, the requirements of lessor accounting has not changed under IFRS 16.

However, lessors will have new disclosure requirements. The new standard contains a

specific exemption for lessors related to the valuation of investment properties at fair value.

Some new requirements related to sales and lease back transactions are also provided by

IFRS 16. Apart from these, there is no such significant impact on the lessors (KPMG. 2016).

Lessee

IFRS 16 will have a great and significant impact on the lessees because of its new

requirements. Till now, the companies are classifying their leases as operating and financing

as per IAS 17. The off balance sheet leases are those which are not reported on the balance

sheet. These are generally operating leases. The new standard will require the companies to

not only convert its existing operating leases but also amends its policies and procedures. The

implementation of IFRS 16 will bring changes in the companies’ IT and control system that

are used for supporting lease accounting along with lease procurement, administration and

tax. Also the financial statements of lessees will also be affected (KPMG. 2016).

Source: (Ey.com. 2016).

Companies most likely to be affected

Financial accounting and reporting 5

The changes in the lease accounting has affected many companies and also their financial

metrics. However, the impact is measured as per the facts and circumstances related to each

entity. The main entities or industries that get affected by IFRS 16 are:

Retail and Customer: This sector is expected to be majorly impacted by the change

in lease requirements. It is especially in the case where leasing the retail space is the

business of the entity. Moreover, manufacturing companies also need to look at all the

major contracts that includes rental of plant and equipment, distribution centre and

fleet arrangements. As an effect of the changes, retailers need to check the renewal

options, estimate and remeasure the variable payments that are linked to a spot rate or

an index. In addition to this, they are also required to separate the service charges

from the lease elements (Pwc.com. 2016).

Telecommunications companies: These entities lease a vast number of big ticket

items that includes cell towers, network equipment, fibre optical cables and satellite

transponders. According to the new requirements they need to consider the new

definition of lease for identifying the arrangements that contain lease. In addition to

this, these companies need to analyse the contracts where the equipment are provided

to the customers. Identification of the lease and the method of lease payments is

required to be done by the telecommunication entities (Ey.com. 2016).

Banking and Financial institutions: Banks have many branch networks and large

call centres and administration that require them to consider the lease arrangements

carefully. Moreover contracts related to the ATMs and the space used by them are

required to be assessed as per the requirements of the new lease standard. Financial

institutions can make use of the data storage facilities and these arrangements can

cover under the scope of IFRS 16. As per the changes, financial service entities need

to determine the treatment of right-of-use assets for regulatory capital requirements.

The changes in the lease accounting has affected many companies and also their financial

metrics. However, the impact is measured as per the facts and circumstances related to each

entity. The main entities or industries that get affected by IFRS 16 are:

Retail and Customer: This sector is expected to be majorly impacted by the change

in lease requirements. It is especially in the case where leasing the retail space is the

business of the entity. Moreover, manufacturing companies also need to look at all the

major contracts that includes rental of plant and equipment, distribution centre and

fleet arrangements. As an effect of the changes, retailers need to check the renewal

options, estimate and remeasure the variable payments that are linked to a spot rate or

an index. In addition to this, they are also required to separate the service charges

from the lease elements (Pwc.com. 2016).

Telecommunications companies: These entities lease a vast number of big ticket

items that includes cell towers, network equipment, fibre optical cables and satellite

transponders. According to the new requirements they need to consider the new

definition of lease for identifying the arrangements that contain lease. In addition to

this, these companies need to analyse the contracts where the equipment are provided

to the customers. Identification of the lease and the method of lease payments is

required to be done by the telecommunication entities (Ey.com. 2016).

Banking and Financial institutions: Banks have many branch networks and large

call centres and administration that require them to consider the lease arrangements

carefully. Moreover contracts related to the ATMs and the space used by them are

required to be assessed as per the requirements of the new lease standard. Financial

institutions can make use of the data storage facilities and these arrangements can

cover under the scope of IFRS 16. As per the changes, financial service entities need

to determine the treatment of right-of-use assets for regulatory capital requirements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial accounting and reporting 6

Metals and Mining: After the implementation of IFRS 16, companies operating in

metals and mining sector needs to consider all the major arrangements they have

made such as mining equipment, land and buildings as well as vehicles. Such

arrangements may give rise to on balance sheet leases accounting under new standard.

Likewise, construction companies also have to consider all the arrangements made

related to equipment, vehicle and land and buildings leasing which may give rise to

on balance sheet leases (Ey.com. 2016).

Transport and logistics sector: Firms operating in this industries often lease items

such as trains, ships, aircraft, real estate and also other vehicles. They also required to

decide about the renewal options and identify the lease as a service or operating lease.

Along with this, they need to separate the service elements from the leased equipment

(Pwc.com. 2016).

Oil & Gas entities and insurance companies: They are least affected and are may be

impacted by the arrangements done in respect of vehicles, equipment and land and

buildings along with those that contain a lease (Ey.com. 2016).

So, all the above sectors or industries will be majorly impacted by the changes in the lease

accounting standard. Once IFRS 16 become effective, the companies are required to report

their leases as per the new requirements and comply with the changes made in their policies

and procedures.

Conclusion

From the above report, it can be concluded that introduction of new lease standard IFRS 16

will change the procedure for lease accounting, specifically for operating leases. It will lay

down some certain requirements that are to be followed by the companies and as a result of

which their financial statements will be highly affected. IFRS 16 will eliminate the need of

Metals and Mining: After the implementation of IFRS 16, companies operating in

metals and mining sector needs to consider all the major arrangements they have

made such as mining equipment, land and buildings as well as vehicles. Such

arrangements may give rise to on balance sheet leases accounting under new standard.

Likewise, construction companies also have to consider all the arrangements made

related to equipment, vehicle and land and buildings leasing which may give rise to

on balance sheet leases (Ey.com. 2016).

Transport and logistics sector: Firms operating in this industries often lease items

such as trains, ships, aircraft, real estate and also other vehicles. They also required to

decide about the renewal options and identify the lease as a service or operating lease.

Along with this, they need to separate the service elements from the leased equipment

(Pwc.com. 2016).

Oil & Gas entities and insurance companies: They are least affected and are may be

impacted by the arrangements done in respect of vehicles, equipment and land and

buildings along with those that contain a lease (Ey.com. 2016).

So, all the above sectors or industries will be majorly impacted by the changes in the lease

accounting standard. Once IFRS 16 become effective, the companies are required to report

their leases as per the new requirements and comply with the changes made in their policies

and procedures.

Conclusion

From the above report, it can be concluded that introduction of new lease standard IFRS 16

will change the procedure for lease accounting, specifically for operating leases. It will lay

down some certain requirements that are to be followed by the companies and as a result of

which their financial statements will be highly affected. IFRS 16 will eliminate the need of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial accounting and reporting 7

classifying the lease as operating and finance and will provide a single accounting model for

lease reporting. The report also states that lessees will be more impacted than lessors, as they

have to change their method of lease accounting in order to comply with the new

requirements. Overall, it can be said that IFRS 16 will help in providing accurate information

about the lease transaction of the companies.

classifying the lease as operating and finance and will provide a single accounting model for

lease reporting. The report also states that lessees will be more impacted than lessors, as they

have to change their method of lease accounting in order to comply with the new

requirements. Overall, it can be said that IFRS 16 will help in providing accurate information

about the lease transaction of the companies.

Financial accounting and reporting 8

References

Iasplus.com. (2018). IFRS 16 — Leases. Retrieved from

https://www.iasplus.com/en/standards/ifrs/ifrs-16

Deloitte UK. (2018). IFRS 16 Leases: new financial reporting standard Potential implications

for lenders. Retrieved from https://www2.deloitte.com/uk/en/pages/audit/articles/ifrs-

16-leases.html

Ey.com. (2016). Leases a summary of IFRS 16 and its effects. Retrieved from

http://www.ey.com/Publication/vwLUAssets/ey-leases-a-summary-of-ifrs-16/$FILE/

ey-leases-a-summary-of-ifrs-16.pdf

Pwc.com. (2016). IFRS 16: The leases standard is changing. Retrieved from

https://www.pwc.com/gx/en/services/audit-assurance/assets/ifrs-16-new-leases.pdf

Ifrs.org. (2016). IFRS 16 Leases. Retrieved from

http://www.ifrs.org/-/media/project/leases/ifrs/published-documents/ifrs16-effects-

analysis.pdf

accaglobal.com. (2018). IFRS 16, Leases. Retrieved from

http://www.accaglobal.com/sg/en/student/exam-support-resources/fundamentals-

exams-study-resources/f7/technical-articles/ifrs16.html

Ifrs.org. (2016). Introductory comments to the European Parliament. Retrieved from

http://www.ifrs.org/-/media/feature/news/speeches/hans-hoogervorst-introductory-

comments-to-the-european-parliament-jan-2016.pdf

KPMG. (2016). IFRS 16 Leases. Retrieved from

https://home.kpmg.com/content/dam/kpmg/pdf/2016/01/leases-first-impressions-

2016.pdf

References

Iasplus.com. (2018). IFRS 16 — Leases. Retrieved from

https://www.iasplus.com/en/standards/ifrs/ifrs-16

Deloitte UK. (2018). IFRS 16 Leases: new financial reporting standard Potential implications

for lenders. Retrieved from https://www2.deloitte.com/uk/en/pages/audit/articles/ifrs-

16-leases.html

Ey.com. (2016). Leases a summary of IFRS 16 and its effects. Retrieved from

http://www.ey.com/Publication/vwLUAssets/ey-leases-a-summary-of-ifrs-16/$FILE/

ey-leases-a-summary-of-ifrs-16.pdf

Pwc.com. (2016). IFRS 16: The leases standard is changing. Retrieved from

https://www.pwc.com/gx/en/services/audit-assurance/assets/ifrs-16-new-leases.pdf

Ifrs.org. (2016). IFRS 16 Leases. Retrieved from

http://www.ifrs.org/-/media/project/leases/ifrs/published-documents/ifrs16-effects-

analysis.pdf

accaglobal.com. (2018). IFRS 16, Leases. Retrieved from

http://www.accaglobal.com/sg/en/student/exam-support-resources/fundamentals-

exams-study-resources/f7/technical-articles/ifrs16.html

Ifrs.org. (2016). Introductory comments to the European Parliament. Retrieved from

http://www.ifrs.org/-/media/feature/news/speeches/hans-hoogervorst-introductory-

comments-to-the-european-parliament-jan-2016.pdf

KPMG. (2016). IFRS 16 Leases. Retrieved from

https://home.kpmg.com/content/dam/kpmg/pdf/2016/01/leases-first-impressions-

2016.pdf

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial accounting and reporting 9

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.