Finance for Decision Makers: M&S Financial Performance Report

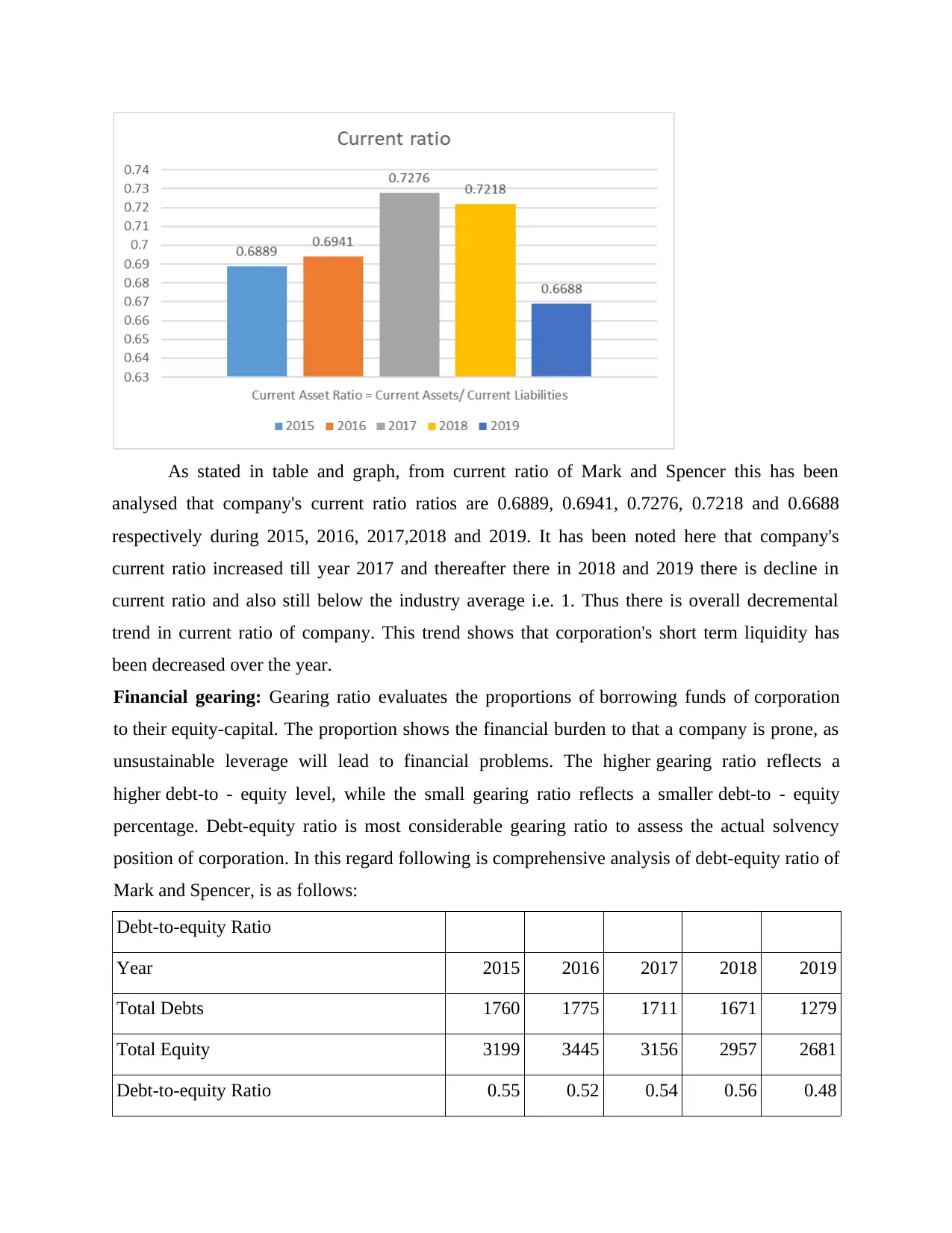

VerifiedAdded on 2023/01/10

|15

|3824

|31

Report

AI Summary

This report provides a comprehensive financial analysis of Mark and Spencer (M&S), evaluating its performance through ratio analysis, including profitability, efficiency, liquidity, and financial gearing ratios from 2015 to 2019. The analysis reveals trends in gross profit margin, asset turnover, current ratio, and debt-to-equity ratio, offering recommendations to improve profitability and financial stability. Furthermore, the report assesses investment alternatives using Net Present Value (NPV) and Internal Rate of Return (IRR) methods, evaluating a potential project's viability. The NPV calculation yields a positive result, while the IRR is calculated, indicating the project's attractiveness. The report also touches on the concept of potential acquisition, providing a holistic view of financial decision-making for the company.

Finance

for

Decision Makers

for

Decision Makers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

1. Evaluation of financial performance:.......................................................................................3

2. Investment appraisal:...............................................................................................................9

3. Potential acquisition:..............................................................................................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

1. Evaluation of financial performance:.......................................................................................3

2. Investment appraisal:...............................................................................................................9

3. Potential acquisition:..............................................................................................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

In the companies, decision making is one of the crucial process which needs to be

considered in an effective manner. Especially financial decisions need lot of time and data for

making correct judgement. The term, financial decision making can be defined as a process of

analysing need of funds in a company and allocating funds into different activities. The project

report is based on a company that is Mark and Spencer. This company is located in London,

United Kingdom and it was founded in year 1884. The company mainly engaged in selling a

range of products such as clothing, food, home products etc. The senior management team of this

company wants a detailed report which needs to include information about financial performance

of company. As well as analysis of investment alternatives by help of various method of

investment appraisal. The end part of report includes information about acquisition in which

Mark and Spencer will acquire a target company.

MAIN BODY

1. Evaluation of financial performance:

Ratio analysis- This is defined as a kind of approach or method which is used by companies in

order to evaluate their financial performance. Under it, different kinds of ratios are calculated

and analysed in order to compare current performance with past years’ performance. This

technique is suitable for companies because it consumes lack of time and cost in financial

analysis as compared to other techniques. There are some advantages and disadvantages of ratio

analysis technique that are as follows:

Advantages:

One of the key benefit of this technique is that by help of it, a company can easily make

compare their financial performance with competitive companies and industries.

This technique highlights the problem areas in which company needs to improve. As well

as managers of companies become able to know the concern area or activity in which

they need to take action.

The ratio analysis makes complex financial statements easier to understand. This

becomes possible because under it, all type of financial data of statements is included in

ratios.

In the companies, decision making is one of the crucial process which needs to be

considered in an effective manner. Especially financial decisions need lot of time and data for

making correct judgement. The term, financial decision making can be defined as a process of

analysing need of funds in a company and allocating funds into different activities. The project

report is based on a company that is Mark and Spencer. This company is located in London,

United Kingdom and it was founded in year 1884. The company mainly engaged in selling a

range of products such as clothing, food, home products etc. The senior management team of this

company wants a detailed report which needs to include information about financial performance

of company. As well as analysis of investment alternatives by help of various method of

investment appraisal. The end part of report includes information about acquisition in which

Mark and Spencer will acquire a target company.

MAIN BODY

1. Evaluation of financial performance:

Ratio analysis- This is defined as a kind of approach or method which is used by companies in

order to evaluate their financial performance. Under it, different kinds of ratios are calculated

and analysed in order to compare current performance with past years’ performance. This

technique is suitable for companies because it consumes lack of time and cost in financial

analysis as compared to other techniques. There are some advantages and disadvantages of ratio

analysis technique that are as follows:

Advantages:

One of the key benefit of this technique is that by help of it, a company can easily make

compare their financial performance with competitive companies and industries.

This technique highlights the problem areas in which company needs to improve. As well

as managers of companies become able to know the concern area or activity in which

they need to take action.

The ratio analysis makes complex financial statements easier to understand. This

becomes possible because under it, all type of financial data of statements is included in

ratios.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

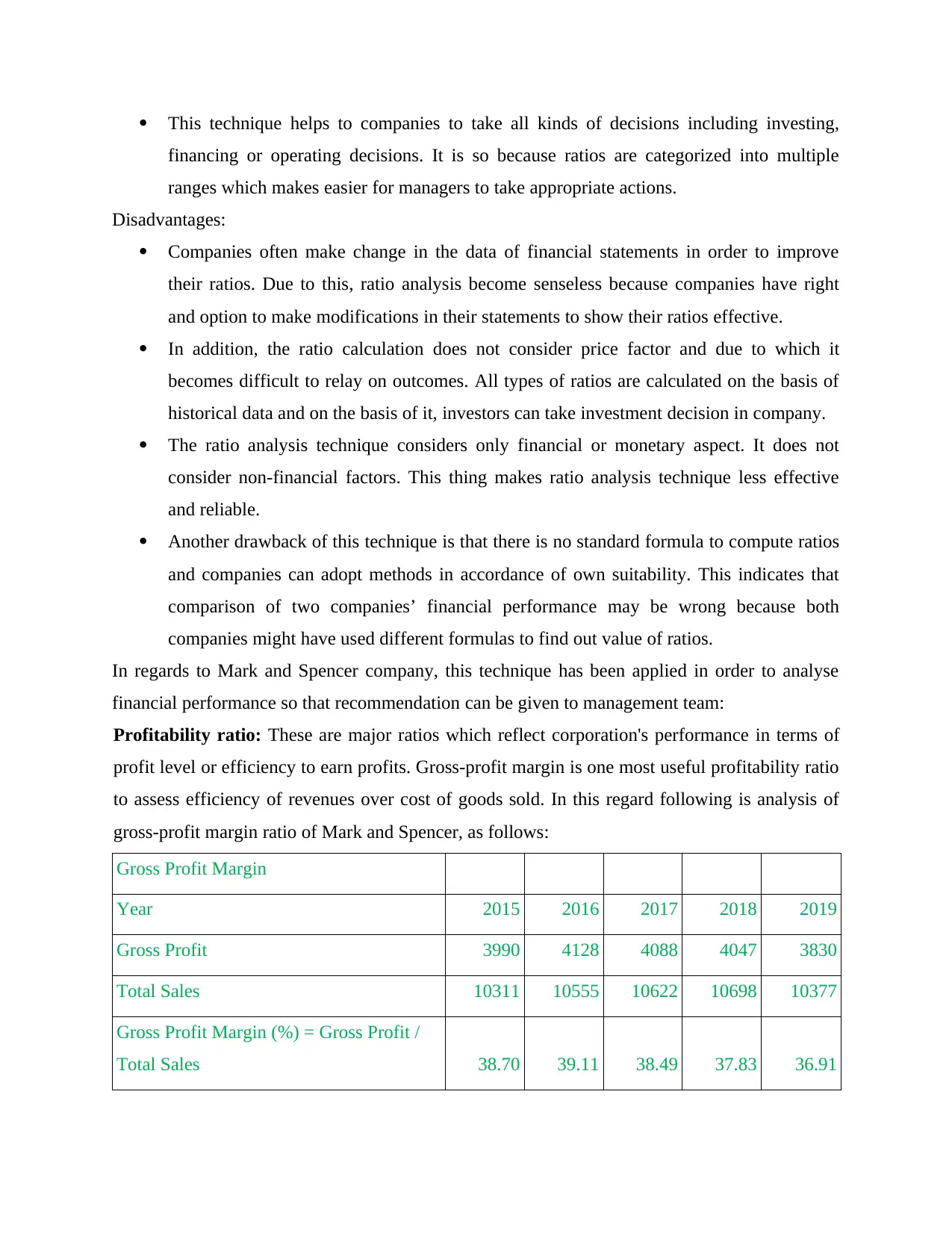

This technique helps to companies to take all kinds of decisions including investing,

financing or operating decisions. It is so because ratios are categorized into multiple

ranges which makes easier for managers to take appropriate actions.

Disadvantages:

Companies often make change in the data of financial statements in order to improve

their ratios. Due to this, ratio analysis become senseless because companies have right

and option to make modifications in their statements to show their ratios effective.

In addition, the ratio calculation does not consider price factor and due to which it

becomes difficult to relay on outcomes. All types of ratios are calculated on the basis of

historical data and on the basis of it, investors can take investment decision in company.

The ratio analysis technique considers only financial or monetary aspect. It does not

consider non-financial factors. This thing makes ratio analysis technique less effective

and reliable.

Another drawback of this technique is that there is no standard formula to compute ratios

and companies can adopt methods in accordance of own suitability. This indicates that

comparison of two companies’ financial performance may be wrong because both

companies might have used different formulas to find out value of ratios.

In regards to Mark and Spencer company, this technique has been applied in order to analyse

financial performance so that recommendation can be given to management team:

Profitability ratio: These are major ratios which reflect corporation's performance in terms of

profit level or efficiency to earn profits. Gross-profit margin is one most useful profitability ratio

to assess efficiency of revenues over cost of goods sold. In this regard following is analysis of

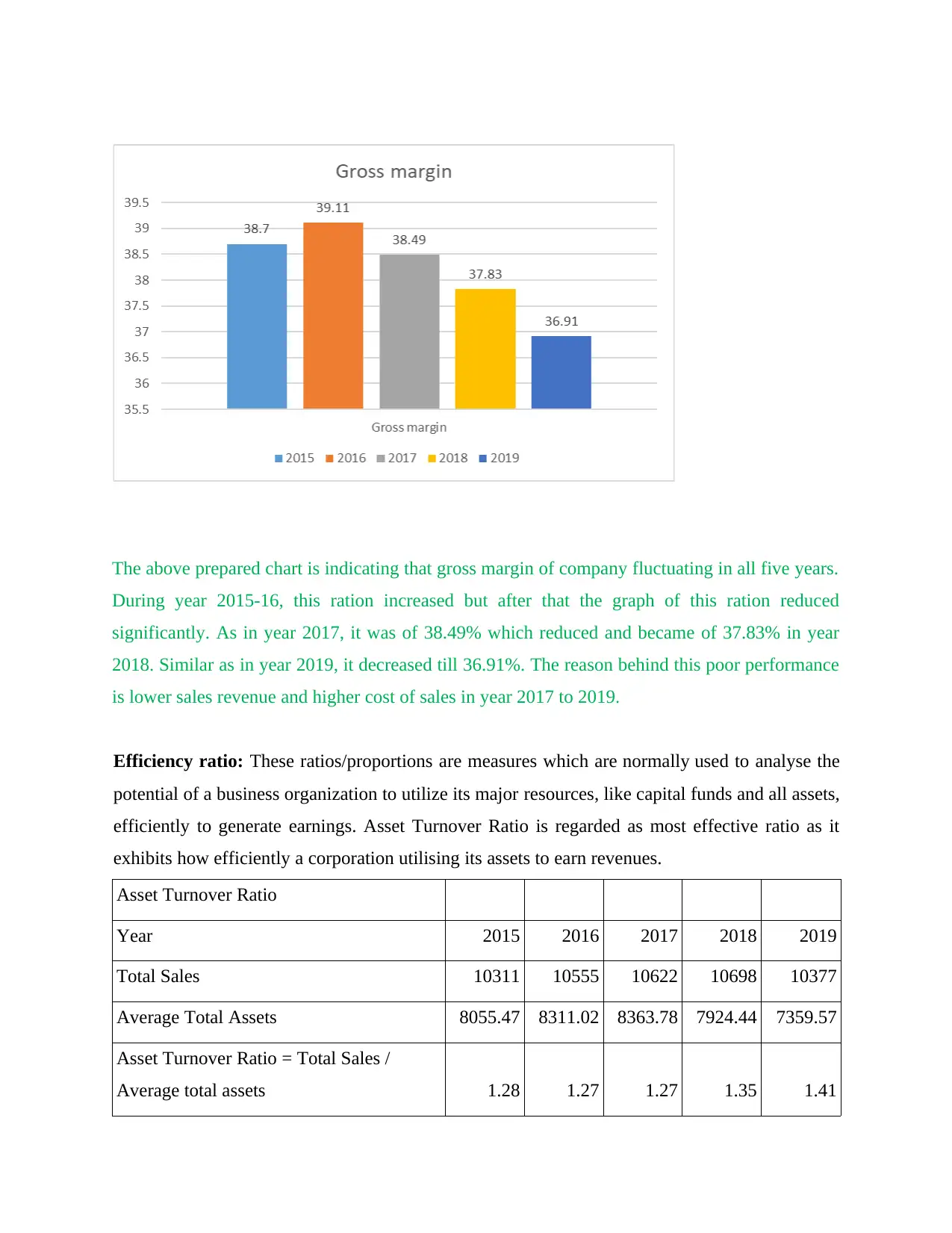

gross-profit margin ratio of Mark and Spencer, as follows:

Gross Profit Margin

Year 2015 2016 2017 2018 2019

Gross Profit 3990 4128 4088 4047 3830

Total Sales 10311 10555 10622 10698 10377

Gross Profit Margin (%) = Gross Profit /

Total Sales 38.70 39.11 38.49 37.83 36.91

financing or operating decisions. It is so because ratios are categorized into multiple

ranges which makes easier for managers to take appropriate actions.

Disadvantages:

Companies often make change in the data of financial statements in order to improve

their ratios. Due to this, ratio analysis become senseless because companies have right

and option to make modifications in their statements to show their ratios effective.

In addition, the ratio calculation does not consider price factor and due to which it

becomes difficult to relay on outcomes. All types of ratios are calculated on the basis of

historical data and on the basis of it, investors can take investment decision in company.

The ratio analysis technique considers only financial or monetary aspect. It does not

consider non-financial factors. This thing makes ratio analysis technique less effective

and reliable.

Another drawback of this technique is that there is no standard formula to compute ratios

and companies can adopt methods in accordance of own suitability. This indicates that

comparison of two companies’ financial performance may be wrong because both

companies might have used different formulas to find out value of ratios.

In regards to Mark and Spencer company, this technique has been applied in order to analyse

financial performance so that recommendation can be given to management team:

Profitability ratio: These are major ratios which reflect corporation's performance in terms of

profit level or efficiency to earn profits. Gross-profit margin is one most useful profitability ratio

to assess efficiency of revenues over cost of goods sold. In this regard following is analysis of

gross-profit margin ratio of Mark and Spencer, as follows:

Gross Profit Margin

Year 2015 2016 2017 2018 2019

Gross Profit 3990 4128 4088 4047 3830

Total Sales 10311 10555 10622 10698 10377

Gross Profit Margin (%) = Gross Profit /

Total Sales 38.70 39.11 38.49 37.83 36.91

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The above prepared chart is indicating that gross margin of company fluctuating in all five years.

During year 2015-16, this ration increased but after that the graph of this ration reduced

significantly. As in year 2017, it was of 38.49% which reduced and became of 37.83% in year

2018. Similar as in year 2019, it decreased till 36.91%. The reason behind this poor performance

is lower sales revenue and higher cost of sales in year 2017 to 2019.

Efficiency ratio: These ratios/proportions are measures which are normally used to analyse the

potential of a business organization to utilize its major resources, like capital funds and all assets,

efficiently to generate earnings. Asset Turnover Ratio is regarded as most effective ratio as it

exhibits how efficiently a corporation utilising its assets to earn revenues.

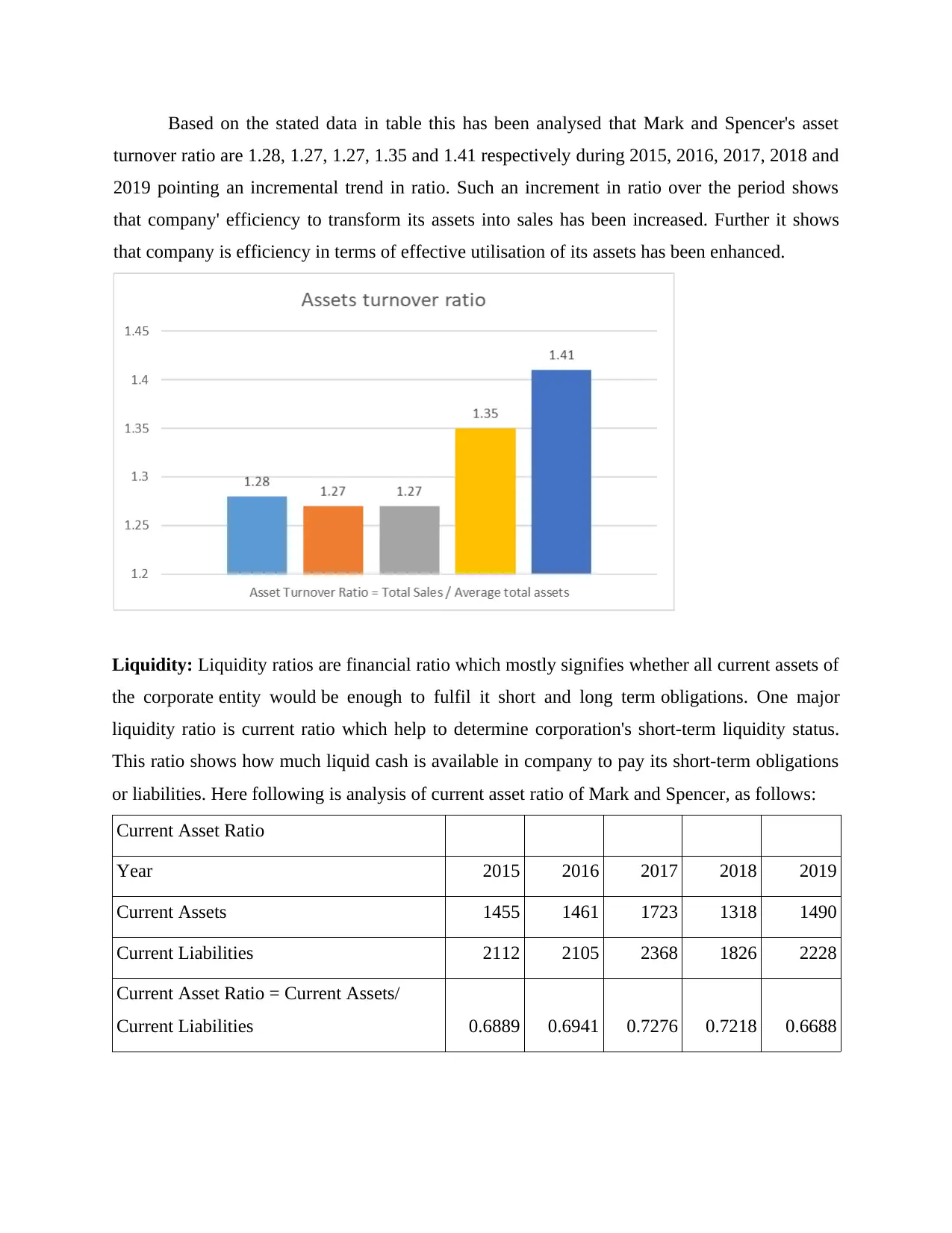

Asset Turnover Ratio

Year 2015 2016 2017 2018 2019

Total Sales 10311 10555 10622 10698 10377

Average Total Assets 8055.47 8311.02 8363.78 7924.44 7359.57

Asset Turnover Ratio = Total Sales /

Average total assets 1.28 1.27 1.27 1.35 1.41

During year 2015-16, this ration increased but after that the graph of this ration reduced

significantly. As in year 2017, it was of 38.49% which reduced and became of 37.83% in year

2018. Similar as in year 2019, it decreased till 36.91%. The reason behind this poor performance

is lower sales revenue and higher cost of sales in year 2017 to 2019.

Efficiency ratio: These ratios/proportions are measures which are normally used to analyse the

potential of a business organization to utilize its major resources, like capital funds and all assets,

efficiently to generate earnings. Asset Turnover Ratio is regarded as most effective ratio as it

exhibits how efficiently a corporation utilising its assets to earn revenues.

Asset Turnover Ratio

Year 2015 2016 2017 2018 2019

Total Sales 10311 10555 10622 10698 10377

Average Total Assets 8055.47 8311.02 8363.78 7924.44 7359.57

Asset Turnover Ratio = Total Sales /

Average total assets 1.28 1.27 1.27 1.35 1.41

Based on the stated data in table this has been analysed that Mark and Spencer's asset

turnover ratio are 1.28, 1.27, 1.27, 1.35 and 1.41 respectively during 2015, 2016, 2017, 2018 and

2019 pointing an incremental trend in ratio. Such an increment in ratio over the period shows

that company' efficiency to transform its assets into sales has been increased. Further it shows

that company is efficiency in terms of effective utilisation of its assets has been enhanced.

Liquidity: Liquidity ratios are financial ratio which mostly signifies whether all current assets of

the corporate entity would be enough to fulfil it short and long term obligations. One major

liquidity ratio is current ratio which help to determine corporation's short-term liquidity status.

This ratio shows how much liquid cash is available in company to pay its short-term obligations

or liabilities. Here following is analysis of current asset ratio of Mark and Spencer, as follows:

Current Asset Ratio

Year 2015 2016 2017 2018 2019

Current Assets 1455 1461 1723 1318 1490

Current Liabilities 2112 2105 2368 1826 2228

Current Asset Ratio = Current Assets/

Current Liabilities 0.6889 0.6941 0.7276 0.7218 0.6688

turnover ratio are 1.28, 1.27, 1.27, 1.35 and 1.41 respectively during 2015, 2016, 2017, 2018 and

2019 pointing an incremental trend in ratio. Such an increment in ratio over the period shows

that company' efficiency to transform its assets into sales has been increased. Further it shows

that company is efficiency in terms of effective utilisation of its assets has been enhanced.

Liquidity: Liquidity ratios are financial ratio which mostly signifies whether all current assets of

the corporate entity would be enough to fulfil it short and long term obligations. One major

liquidity ratio is current ratio which help to determine corporation's short-term liquidity status.

This ratio shows how much liquid cash is available in company to pay its short-term obligations

or liabilities. Here following is analysis of current asset ratio of Mark and Spencer, as follows:

Current Asset Ratio

Year 2015 2016 2017 2018 2019

Current Assets 1455 1461 1723 1318 1490

Current Liabilities 2112 2105 2368 1826 2228

Current Asset Ratio = Current Assets/

Current Liabilities 0.6889 0.6941 0.7276 0.7218 0.6688

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

As stated in table and graph, from current ratio of Mark and Spencer this has been

analysed that company's current ratio ratios are 0.6889, 0.6941, 0.7276, 0.7218 and 0.6688

respectively during 2015, 2016, 2017,2018 and 2019. It has been noted here that company's

current ratio increased till year 2017 and thereafter there in 2018 and 2019 there is decline in

current ratio and also still below the industry average i.e. 1. Thus there is overall decremental

trend in current ratio of company. This trend shows that corporation's short term liquidity has

been decreased over the year.

Financial gearing: Gearing ratio evaluates the proportions of borrowing funds of corporation

to their equity-capital. The proportion shows the financial burden to that a company is prone, as

unsustainable leverage will lead to financial problems. The higher gearing ratio reflects a

higher debt-to - equity level, while the small gearing ratio reflects a smaller debt-to - equity

percentage. Debt-equity ratio is most considerable gearing ratio to assess the actual solvency

position of corporation. In this regard following is comprehensive analysis of debt-equity ratio of

Mark and Spencer, is as follows:

Debt-to-equity Ratio

Year 2015 2016 2017 2018 2019

Total Debts 1760 1775 1711 1671 1279

Total Equity 3199 3445 3156 2957 2681

Debt-to-equity Ratio 0.55 0.52 0.54 0.56 0.48

analysed that company's current ratio ratios are 0.6889, 0.6941, 0.7276, 0.7218 and 0.6688

respectively during 2015, 2016, 2017,2018 and 2019. It has been noted here that company's

current ratio increased till year 2017 and thereafter there in 2018 and 2019 there is decline in

current ratio and also still below the industry average i.e. 1. Thus there is overall decremental

trend in current ratio of company. This trend shows that corporation's short term liquidity has

been decreased over the year.

Financial gearing: Gearing ratio evaluates the proportions of borrowing funds of corporation

to their equity-capital. The proportion shows the financial burden to that a company is prone, as

unsustainable leverage will lead to financial problems. The higher gearing ratio reflects a

higher debt-to - equity level, while the small gearing ratio reflects a smaller debt-to - equity

percentage. Debt-equity ratio is most considerable gearing ratio to assess the actual solvency

position of corporation. In this regard following is comprehensive analysis of debt-equity ratio of

Mark and Spencer, is as follows:

Debt-to-equity Ratio

Year 2015 2016 2017 2018 2019

Total Debts 1760 1775 1711 1671 1279

Total Equity 3199 3445 3156 2957 2681

Debt-to-equity Ratio 0.55 0.52 0.54 0.56 0.48

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

As table shows Mark and Spencer's debt-to-equity ratios are 0.55, 0.52, 0.54, 0.56 and

0.48 respectively in year 2015, 2016, 2017, 2018 and 2019 reflecting a declining trend i.e.

favourable indication. This decline in ratio shows that company's reliability upon debt financing

has been decreased. Although here it is also notable aspect is that company's equity funds has

also been decreased over the period and below the industry's average level i.e. around 1.

Decrease in dependence upon debt-financing shows that corporation's long term liquidity

position is quite good.

Recommendation to management team: Here based on the above ratios analysis it has been

recommended to managerial team that corporation's profitability status is continuously declined

and expected to be decline thus they have to focus towards this area. In attempt to increase net

profit margin company has to improve their controlling over costs and expenditures. Further to

increase the overall sales company has to modify or adapt new promotional strategy. Also there

is just slight improvement in financial gearing while liquidity ratio is decline in last two year

there here advisable to them to restructure their debts and focus towards equity funding instead

debt financing. Moreover, company should list out all those aspects or influences which are

impacting corporation's financial performance within industry and put efforts to minimise the

effects of such aspects.

0.48 respectively in year 2015, 2016, 2017, 2018 and 2019 reflecting a declining trend i.e.

favourable indication. This decline in ratio shows that company's reliability upon debt financing

has been decreased. Although here it is also notable aspect is that company's equity funds has

also been decreased over the period and below the industry's average level i.e. around 1.

Decrease in dependence upon debt-financing shows that corporation's long term liquidity

position is quite good.

Recommendation to management team: Here based on the above ratios analysis it has been

recommended to managerial team that corporation's profitability status is continuously declined

and expected to be decline thus they have to focus towards this area. In attempt to increase net

profit margin company has to improve their controlling over costs and expenditures. Further to

increase the overall sales company has to modify or adapt new promotional strategy. Also there

is just slight improvement in financial gearing while liquidity ratio is decline in last two year

there here advisable to them to restructure their debts and focus towards equity funding instead

debt financing. Moreover, company should list out all those aspects or influences which are

impacting corporation's financial performance within industry and put efforts to minimise the

effects of such aspects.

2. Investment appraisal:

Investment appraisal is an analysis conducted to determine the viability of investment

made over asset's existence including feasibility and strategic alliance considerations. It is a way

a company can determine the feasibility of future investments or ventures centred on results from

many various methods of capital-budgeting and funding. This is a sort of basic evaluation for

traders because this could help recognize longer-term patterns and the expected profitability

level of a business. Investment appraisal can be regarded as an input to investment decision that

is sponsor and governing board 's decision who determines/defines investment in a portfolio,

proposal and project (Ndanyenbah, T.Y. and Zakaria, A., 2019). This offers the basis and

reasoning for investing scarce capital and focuses on a comprehensive investment evaluation.

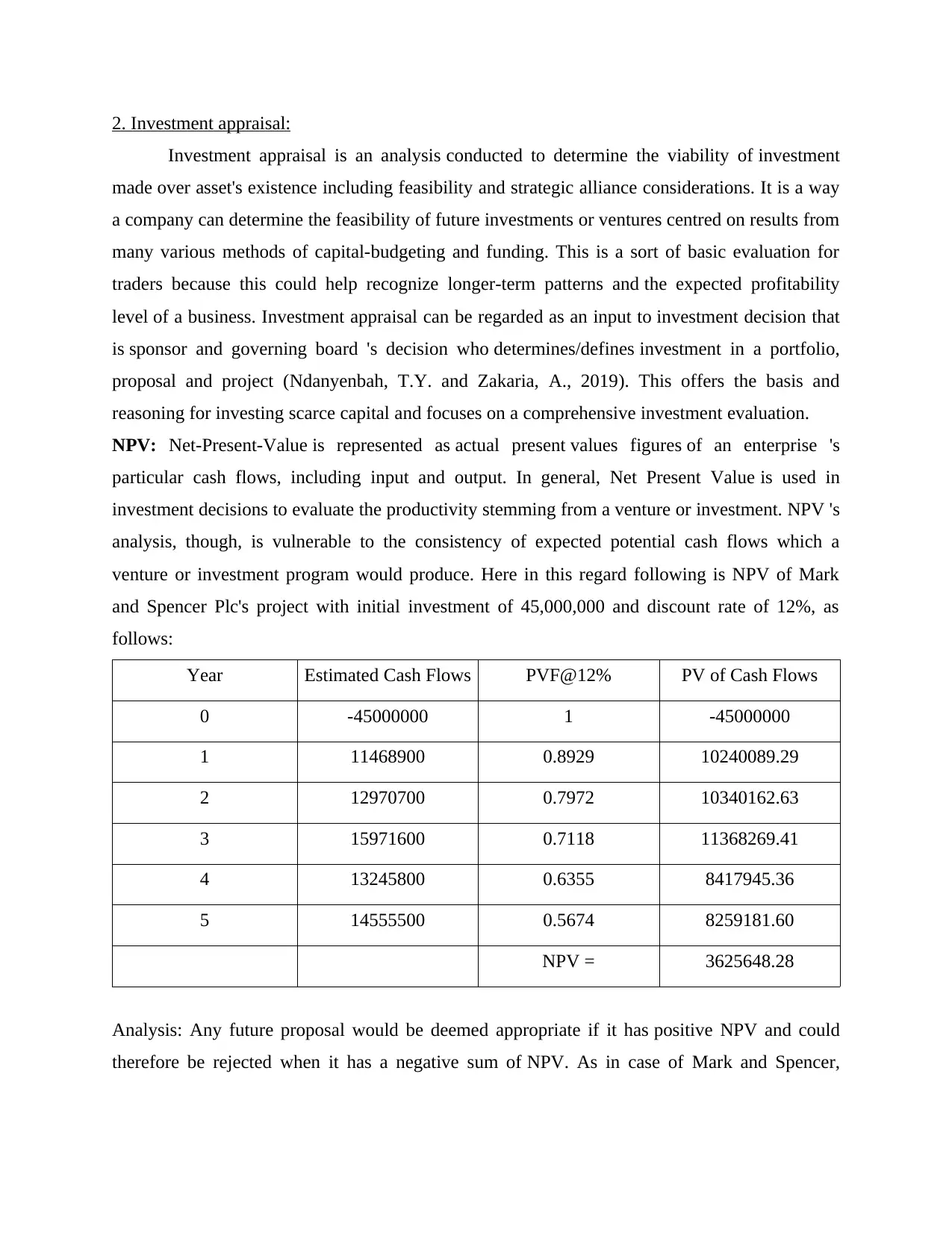

NPV: Net-Present-Value is represented as actual present values figures of an enterprise 's

particular cash flows, including input and output. In general, Net Present Value is used in

investment decisions to evaluate the productivity stemming from a venture or investment. NPV 's

analysis, though, is vulnerable to the consistency of expected potential cash flows which a

venture or investment program would produce. Here in this regard following is NPV of Mark

and Spencer Plc's project with initial investment of 45,000,000 and discount rate of 12%, as

follows:

Year Estimated Cash Flows PVF@12% PV of Cash Flows

0 -45000000 1 -45000000

1 11468900 0.8929 10240089.29

2 12970700 0.7972 10340162.63

3 15971600 0.7118 11368269.41

4 13245800 0.6355 8417945.36

5 14555500 0.5674 8259181.60

NPV = 3625648.28

Analysis: Any future proposal would be deemed appropriate if it has positive NPV and could

therefore be rejected when it has a negative sum of NPV. As in case of Mark and Spencer,

Investment appraisal is an analysis conducted to determine the viability of investment

made over asset's existence including feasibility and strategic alliance considerations. It is a way

a company can determine the feasibility of future investments or ventures centred on results from

many various methods of capital-budgeting and funding. This is a sort of basic evaluation for

traders because this could help recognize longer-term patterns and the expected profitability

level of a business. Investment appraisal can be regarded as an input to investment decision that

is sponsor and governing board 's decision who determines/defines investment in a portfolio,

proposal and project (Ndanyenbah, T.Y. and Zakaria, A., 2019). This offers the basis and

reasoning for investing scarce capital and focuses on a comprehensive investment evaluation.

NPV: Net-Present-Value is represented as actual present values figures of an enterprise 's

particular cash flows, including input and output. In general, Net Present Value is used in

investment decisions to evaluate the productivity stemming from a venture or investment. NPV 's

analysis, though, is vulnerable to the consistency of expected potential cash flows which a

venture or investment program would produce. Here in this regard following is NPV of Mark

and Spencer Plc's project with initial investment of 45,000,000 and discount rate of 12%, as

follows:

Year Estimated Cash Flows PVF@12% PV of Cash Flows

0 -45000000 1 -45000000

1 11468900 0.8929 10240089.29

2 12970700 0.7972 10340162.63

3 15971600 0.7118 11368269.41

4 13245800 0.6355 8417945.36

5 14555500 0.5674 8259181.60

NPV = 3625648.28

Analysis: Any future proposal would be deemed appropriate if it has positive NPV and could

therefore be rejected when it has a negative sum of NPV. As in case of Mark and Spencer,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

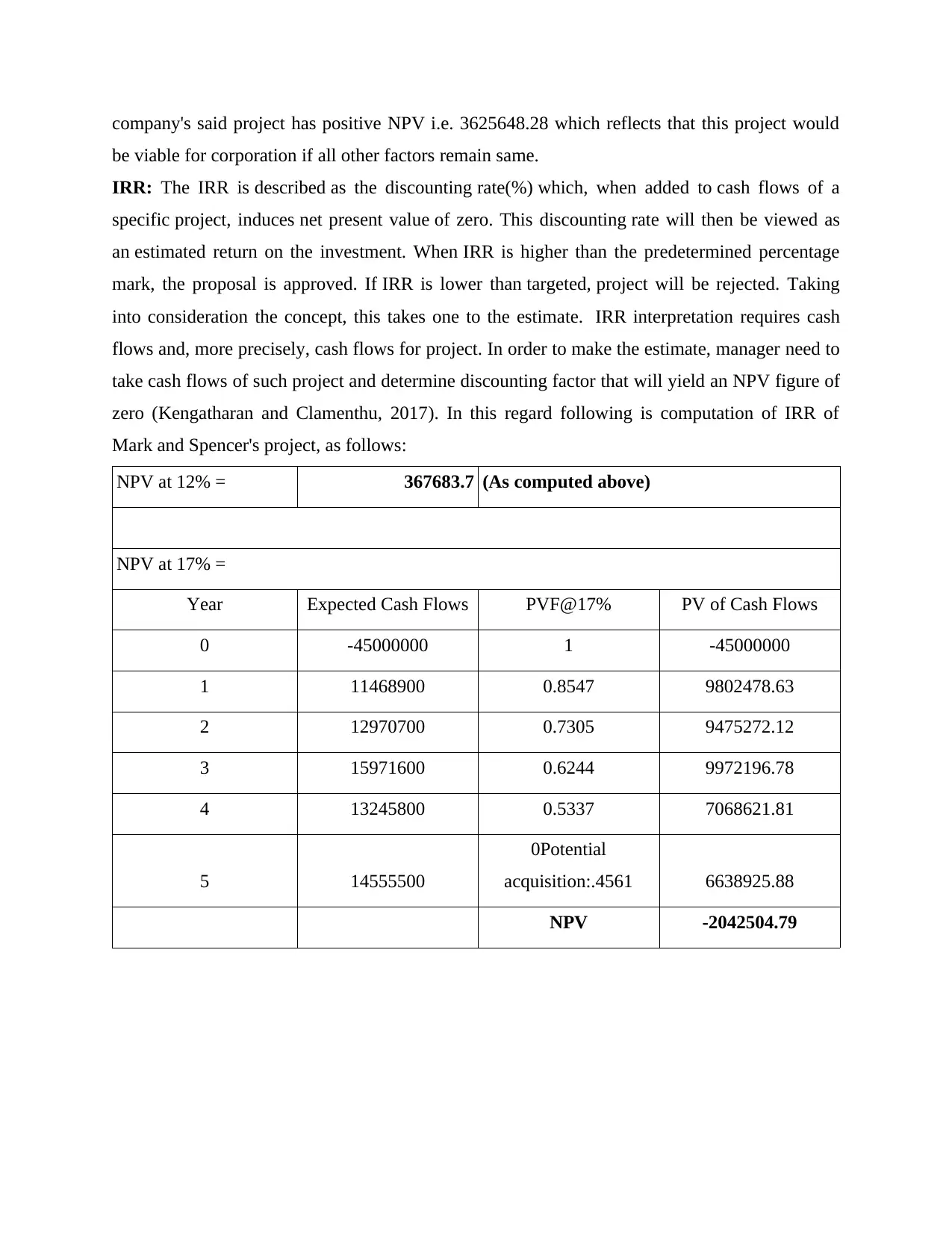

company's said project has positive NPV i.e. 3625648.28 which reflects that this project would

be viable for corporation if all other factors remain same.

IRR: The IRR is described as the discounting rate(%) which, when added to cash flows of a

specific project, induces net present value of zero. This discounting rate will then be viewed as

an estimated return on the investment. When IRR is higher than the predetermined percentage

mark, the proposal is approved. If IRR is lower than targeted, project will be rejected. Taking

into consideration the concept, this takes one to the estimate. IRR interpretation requires cash

flows and, more precisely, cash flows for project. In order to make the estimate, manager need to

take cash flows of such project and determine discounting factor that will yield an NPV figure of

zero (Kengatharan and Clamenthu, 2017). In this regard following is computation of IRR of

Mark and Spencer's project, as follows:

NPV at 12% = 367683.7 (As computed above)

NPV at 17% =

Year Expected Cash Flows PVF@17% PV of Cash Flows

0 -45000000 1 -45000000

1 11468900 0.8547 9802478.63

2 12970700 0.7305 9475272.12

3 15971600 0.6244 9972196.78

4 13245800 0.5337 7068621.81

5 14555500

0Potential

acquisition:.4561 6638925.88

NPV -2042504.79

be viable for corporation if all other factors remain same.

IRR: The IRR is described as the discounting rate(%) which, when added to cash flows of a

specific project, induces net present value of zero. This discounting rate will then be viewed as

an estimated return on the investment. When IRR is higher than the predetermined percentage

mark, the proposal is approved. If IRR is lower than targeted, project will be rejected. Taking

into consideration the concept, this takes one to the estimate. IRR interpretation requires cash

flows and, more precisely, cash flows for project. In order to make the estimate, manager need to

take cash flows of such project and determine discounting factor that will yield an NPV figure of

zero (Kengatharan and Clamenthu, 2017). In this regard following is computation of IRR of

Mark and Spencer's project, as follows:

NPV at 12% = 367683.7 (As computed above)

NPV at 17% =

Year Expected Cash Flows PVF@17% PV of Cash Flows

0 -45000000 1 -45000000

1 11468900 0.8547 9802478.63

2 12970700 0.7305 9475272.12

3 15971600 0.6244 9972196.78

4 13245800 0.5337 7068621.81

5 14555500

0Potential

acquisition:.4561 6638925.88

NPV -2042504.79

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

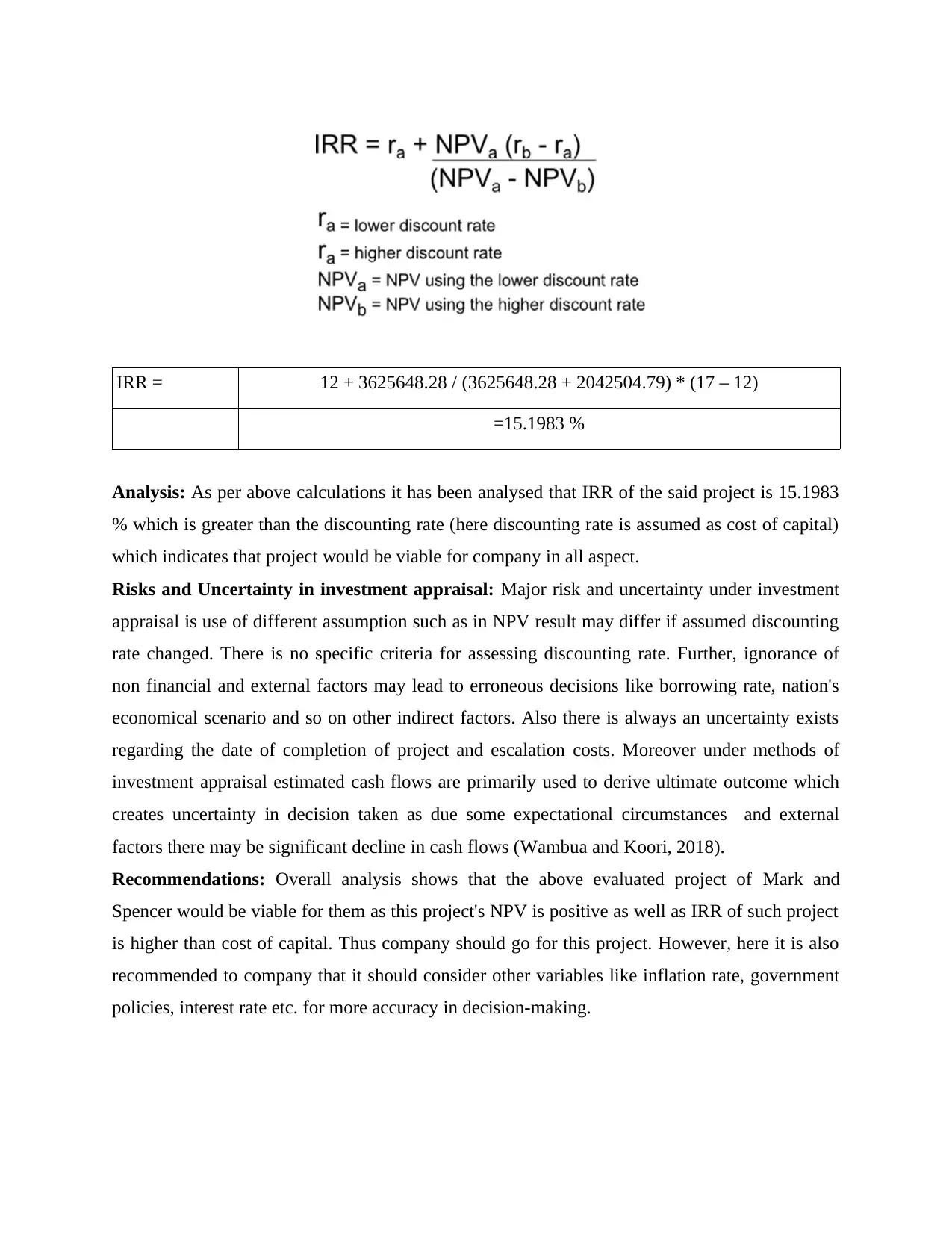

IRR = 12 + 3625648.28 / (3625648.28 + 2042504.79) * (17 – 12)

=15.1983 %

Analysis: As per above calculations it has been analysed that IRR of the said project is 15.1983

% which is greater than the discounting rate (here discounting rate is assumed as cost of capital)

which indicates that project would be viable for company in all aspect.

Risks and Uncertainty in investment appraisal: Major risk and uncertainty under investment

appraisal is use of different assumption such as in NPV result may differ if assumed discounting

rate changed. There is no specific criteria for assessing discounting rate. Further, ignorance of

non financial and external factors may lead to erroneous decisions like borrowing rate, nation's

economical scenario and so on other indirect factors. Also there is always an uncertainty exists

regarding the date of completion of project and escalation costs. Moreover under methods of

investment appraisal estimated cash flows are primarily used to derive ultimate outcome which

creates uncertainty in decision taken as due some expectational circumstances and external

factors there may be significant decline in cash flows (Wambua and Koori, 2018).

Recommendations: Overall analysis shows that the above evaluated project of Mark and

Spencer would be viable for them as this project's NPV is positive as well as IRR of such project

is higher than cost of capital. Thus company should go for this project. However, here it is also

recommended to company that it should consider other variables like inflation rate, government

policies, interest rate etc. for more accuracy in decision-making.

=15.1983 %

Analysis: As per above calculations it has been analysed that IRR of the said project is 15.1983

% which is greater than the discounting rate (here discounting rate is assumed as cost of capital)

which indicates that project would be viable for company in all aspect.

Risks and Uncertainty in investment appraisal: Major risk and uncertainty under investment

appraisal is use of different assumption such as in NPV result may differ if assumed discounting

rate changed. There is no specific criteria for assessing discounting rate. Further, ignorance of

non financial and external factors may lead to erroneous decisions like borrowing rate, nation's

economical scenario and so on other indirect factors. Also there is always an uncertainty exists

regarding the date of completion of project and escalation costs. Moreover under methods of

investment appraisal estimated cash flows are primarily used to derive ultimate outcome which

creates uncertainty in decision taken as due some expectational circumstances and external

factors there may be significant decline in cash flows (Wambua and Koori, 2018).

Recommendations: Overall analysis shows that the above evaluated project of Mark and

Spencer would be viable for them as this project's NPV is positive as well as IRR of such project

is higher than cost of capital. Thus company should go for this project. However, here it is also

recommended to company that it should consider other variables like inflation rate, government

policies, interest rate etc. for more accuracy in decision-making.

3. Potential acquisition:

Rationale for selecting Ocado Retail Ltd (Target Company): Ocado Retail Ltd is an

active corporation with registered office situated in the Hatfield, Hertfordshire, formed on

11th November 1999. Ocado Retail operating for 20 years. Mark and Spencer is expecting

around significant synergy to be generated due to this acquisition as the target company has 20

year experience in the sector as well as have popular web platform for online selling of products.

Main rationale for selecting this company is that company is planning to expand their online

selling through the online web platform of Ocado Retail. Also company is planning to expand

their business in clothing sector (Ocado: About us. 2020).

Synergistic gain of the acquisition: Synergistic gain of around GBP 70 million is expected by

Mark and Spencer due to this acquisition. This would benefit from a acquisition of increased

purchasing volume, enhanced procurement economics of M&S direct brand and marketed

products, and substantial decrease in product research cost and production costs. The new

collaboration could lead to the distribution of clothes alongside grocery stores, and although

Ocado's logistics were not currently structured to distribute clothes, they stored products like

Pretty Polly tights and knickers, suggesting "possibility to use it very rapidly". The acquisition

would see Marks & Spencer providing first-time online grocery delivery platform and will be

able to sell more than 6,500 food products through Ocado 's website.

Proposed deal value and finance of the acquisition: Here in the proposed deal Mark and

Spencer and Ocado will enter into a joint venture arrangement, whereby M&S will acquire 50

percent of share in Ocado's UK retail business. Under terms of this joint venture, as portion

of five-year strategy to "unlocking growth" inside its food sector, M&S is to buy a 50 per cent

share of the Ocado for GBP 750 million. Ocado will keep trading under its original title, but it

will sell M&S goods from Sep 2020 at latest after its existing Waitrose deal is terminated.

Completion of the deal is scheduled in third quarter of year 2019. A major portion of finance for

this acquisition will be arranged by company through long term loans from bank (M&S

ACQUIRES 50% OF OCADO. 2019). Potential implications of this acquisition on organization's

performance: A major implication of the said acquisition will be: prices for consumers may be

at lower Credit. M&S Food adherents would be enabled to purchase the items online. Prior

experiments at retailer of in-house delivery services proved uneconomic, preventing a complete

rolled-out. As per chief executive Steve Rowe, this was a potential owing to the expected cost

Rationale for selecting Ocado Retail Ltd (Target Company): Ocado Retail Ltd is an

active corporation with registered office situated in the Hatfield, Hertfordshire, formed on

11th November 1999. Ocado Retail operating for 20 years. Mark and Spencer is expecting

around significant synergy to be generated due to this acquisition as the target company has 20

year experience in the sector as well as have popular web platform for online selling of products.

Main rationale for selecting this company is that company is planning to expand their online

selling through the online web platform of Ocado Retail. Also company is planning to expand

their business in clothing sector (Ocado: About us. 2020).

Synergistic gain of the acquisition: Synergistic gain of around GBP 70 million is expected by

Mark and Spencer due to this acquisition. This would benefit from a acquisition of increased

purchasing volume, enhanced procurement economics of M&S direct brand and marketed

products, and substantial decrease in product research cost and production costs. The new

collaboration could lead to the distribution of clothes alongside grocery stores, and although

Ocado's logistics were not currently structured to distribute clothes, they stored products like

Pretty Polly tights and knickers, suggesting "possibility to use it very rapidly". The acquisition

would see Marks & Spencer providing first-time online grocery delivery platform and will be

able to sell more than 6,500 food products through Ocado 's website.

Proposed deal value and finance of the acquisition: Here in the proposed deal Mark and

Spencer and Ocado will enter into a joint venture arrangement, whereby M&S will acquire 50

percent of share in Ocado's UK retail business. Under terms of this joint venture, as portion

of five-year strategy to "unlocking growth" inside its food sector, M&S is to buy a 50 per cent

share of the Ocado for GBP 750 million. Ocado will keep trading under its original title, but it

will sell M&S goods from Sep 2020 at latest after its existing Waitrose deal is terminated.

Completion of the deal is scheduled in third quarter of year 2019. A major portion of finance for

this acquisition will be arranged by company through long term loans from bank (M&S

ACQUIRES 50% OF OCADO. 2019). Potential implications of this acquisition on organization's

performance: A major implication of the said acquisition will be: prices for consumers may be

at lower Credit. M&S Food adherents would be enabled to purchase the items online. Prior

experiments at retailer of in-house delivery services proved uneconomic, preventing a complete

rolled-out. As per chief executive Steve Rowe, this was a potential owing to the expected cost

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.