Comprehensive Analysis of M&S Financial Reporting Under IFRS Framework

VerifiedAdded on 2020/06/06

|15

|3498

|34

Report

AI Summary

This report provides a comprehensive analysis of financial reporting, focusing on the application of International Financial Reporting Standards (IFRS) to the financial performance of M&S. It begins with an introduction to the context and purpose of financial reporting, emphasizing its role in providing useful information to stakeholders for decision-making. The report then delves into the conceptual and regulatory framework of financial reporting, outlining its purpose and principles. A key aspect of the report is the identification of primary stakeholders of M&S and the benefits they derive from financial reporting. The value of financial reporting in meeting organizational goals is also explored. The analysis includes a detailed examination of various financial statements, such as the statement of profit and loss, the statement of equity, and the statement of financial position, along with the interpretation of M&S's financial performance through ratio analysis. The report also differentiates between IFRS and IAS, highlighting the benefits of IFRS adoption and identifying varying degrees of compliance with IFRS. The analysis includes calculations and interpretations of key financial metrics, providing a thorough understanding of M&S's financial position and performance. The report concludes with a summary of the key findings and implications of the financial reporting analysis.

International Financial

Reporting

Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

1.Context and purpose of financial reporting:........................................................................1

2. Purpose and principles of Conceptual and regulatory framework.....................................2

Q3: Determination of primary stakeholders of M&S and their benefits:...............................3

Q4: Value of financial reporting for meeting organisation goals...........................................4

Q5: Various financial statement analysis...............................................................................5

A: Statement of profit and loss:..............................................................................................5

B: Statement of equity:...........................................................................................................6

C: Statement of financial position:.........................................................................................7

Q6: Interpretation of financial performance of M&S.............................................................8

Q7. Difference between IFRS and IAS..................................................................................9

Q8. Benefits of IFRS............................................................................................................10

Q9: Identification of the varying degrees of compliance with IFRS....................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

1.Context and purpose of financial reporting:........................................................................1

2. Purpose and principles of Conceptual and regulatory framework.....................................2

Q3: Determination of primary stakeholders of M&S and their benefits:...............................3

Q4: Value of financial reporting for meeting organisation goals...........................................4

Q5: Various financial statement analysis...............................................................................5

A: Statement of profit and loss:..............................................................................................5

B: Statement of equity:...........................................................................................................6

C: Statement of financial position:.........................................................................................7

Q6: Interpretation of financial performance of M&S.............................................................8

Q7. Difference between IFRS and IAS..................................................................................9

Q8. Benefits of IFRS............................................................................................................10

Q9: Identification of the varying degrees of compliance with IFRS....................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Every firm’s performance is measure by making and analysing the financial and

management accounting. As this is the tool which is used by the investors and other stakeholders

for taking their rational decisions. The performance of the business is totally relied upon the

performance of the company. Financial statement is made by financial experts which helps to the

investors for taking their rational decisions (Shah, Liang and Akbar, 2013). Financial reporting

assumes a great role in international economies. Its main aim is to render appropriate and helpful

information to the business owners and other stakeholders so that they could take their decisions.

1.Context and purpose of financial reporting:

Financial reporting plays an important role for making the business objectives sustainable

and reliable. The main aim for making the financial reporting is to render a useful and justifiable

information to the diverse stakeholders. This occurs mostly in public limited companies, where

share capital is traded to the general public via stock exchange (Walton, 2012). With the help of

financial reporting, annual reporting is made and it plays an important role for making their

business objectives in an effective manner. With the help of annual return, owners can make

strategy for long term and short term. The owner gets an annual statement which main aim is to

summarise the performance and position of their firm.

Without this reporting system, investors will be lower inclined to part with their capital as

they are going to have no way of monitoring how efficient being run by the directors. The chosen

interns of the company are assuming to be the operating in the best interests of the shareholders.

For satiating the requirements of the users of the financial statements, organisations are

required to applied accounting systems which renders the information related requirement. This

is likewise crucial that financial reporting system is regulated in order to ensure that the

information rendered to the users is in an effective manner and that it is implemented to their

informational needs.

The main purpose of financial reports is to track the financial performance of the business.

As this will help out for knowing about the profit amount is making. the main aim of the

financial reporting is to render this information to the lenders of the business.

1

Every firm’s performance is measure by making and analysing the financial and

management accounting. As this is the tool which is used by the investors and other stakeholders

for taking their rational decisions. The performance of the business is totally relied upon the

performance of the company. Financial statement is made by financial experts which helps to the

investors for taking their rational decisions (Shah, Liang and Akbar, 2013). Financial reporting

assumes a great role in international economies. Its main aim is to render appropriate and helpful

information to the business owners and other stakeholders so that they could take their decisions.

1.Context and purpose of financial reporting:

Financial reporting plays an important role for making the business objectives sustainable

and reliable. The main aim for making the financial reporting is to render a useful and justifiable

information to the diverse stakeholders. This occurs mostly in public limited companies, where

share capital is traded to the general public via stock exchange (Walton, 2012). With the help of

financial reporting, annual reporting is made and it plays an important role for making their

business objectives in an effective manner. With the help of annual return, owners can make

strategy for long term and short term. The owner gets an annual statement which main aim is to

summarise the performance and position of their firm.

Without this reporting system, investors will be lower inclined to part with their capital as

they are going to have no way of monitoring how efficient being run by the directors. The chosen

interns of the company are assuming to be the operating in the best interests of the shareholders.

For satiating the requirements of the users of the financial statements, organisations are

required to applied accounting systems which renders the information related requirement. This

is likewise crucial that financial reporting system is regulated in order to ensure that the

information rendered to the users is in an effective manner and that it is implemented to their

informational needs.

The main purpose of financial reports is to track the financial performance of the business.

As this will help out for knowing about the profit amount is making. the main aim of the

financial reporting is to render this information to the lenders of the business.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Purpose and principles of Conceptual and regulatory framework

This is used to elaborates the nature and aim of the financial accounting and reporting within the

business context. This covers the diverse theories and conceptual factors that are implemented in

the firm’s context. This covers the theories and conceptual factors that are implemented in the

financial reporting. This is a system which helps the layout of the accounting standards and

principles. This is a systematic format of forming information and reflecting in the report format.

This is assuming to the statement of forming of GAAP which renders a layout of assessment of

current accounting and financial practices. Information that are given under conceptual layout

which is based on the theories and practices. Information which are rendered according to the

conceptual framework which is formed as per the theories and concepts (Walton, 2012). This

assists in forming decisions, strategies, assessment of economic layout.

There is a contingency plan which is found in considering conceptual frameworks to

emerge specific information related to the financial statements. Conceptual framework is needed

to form financial reports and standards in the absence of this framework diverse defects could be

emerged. Some of them are mentioned hereunder:

There is an inner inconsistency found among the diverse concepts which influence the

transactions and income statement.

There are various chances of misrepresentation of reports subject to financial position

statements, financial position statements.

Few of the standards constant biased according to the nature of transactions which

covers the direction of standards and quality of reporting standards.

According to International Accounting Standards Board, conceptual framework is needed to

up-to date and relevant to the financial records.

Purpose of conceptual and regulatory framework:

Emergence of ethical layout of firm in respect of financial reporting and accounting

standards are the key objective of this concept.

This helps to emerge IFRS and assist IFRS and likewise stimulate mandatory

accounting regulations and standards implemented in financial accounting.

Conceptual framework is a planned layout handle discipline in accounting practice.

This main aim is to renders a path to auditors, financial managers, investors and

stakeholders to assess the financial layout of a firm.

2

This is used to elaborates the nature and aim of the financial accounting and reporting within the

business context. This covers the diverse theories and conceptual factors that are implemented in

the firm’s context. This covers the theories and conceptual factors that are implemented in the

financial reporting. This is a system which helps the layout of the accounting standards and

principles. This is a systematic format of forming information and reflecting in the report format.

This is assuming to the statement of forming of GAAP which renders a layout of assessment of

current accounting and financial practices. Information that are given under conceptual layout

which is based on the theories and practices. Information which are rendered according to the

conceptual framework which is formed as per the theories and concepts (Walton, 2012). This

assists in forming decisions, strategies, assessment of economic layout.

There is a contingency plan which is found in considering conceptual frameworks to

emerge specific information related to the financial statements. Conceptual framework is needed

to form financial reports and standards in the absence of this framework diverse defects could be

emerged. Some of them are mentioned hereunder:

There is an inner inconsistency found among the diverse concepts which influence the

transactions and income statement.

There are various chances of misrepresentation of reports subject to financial position

statements, financial position statements.

Few of the standards constant biased according to the nature of transactions which

covers the direction of standards and quality of reporting standards.

According to International Accounting Standards Board, conceptual framework is needed to

up-to date and relevant to the financial records.

Purpose of conceptual and regulatory framework:

Emergence of ethical layout of firm in respect of financial reporting and accounting

standards are the key objective of this concept.

This helps to emerge IFRS and assist IFRS and likewise stimulate mandatory

accounting regulations and standards implemented in financial accounting.

Conceptual framework is a planned layout handle discipline in accounting practice.

This main aim is to renders a path to auditors, financial managers, investors and

stakeholders to assess the financial layout of a firm.

2

Qualitative characteristic related to financial information:

This assist to determine the objective of financial statements.

Helps producer of publishing the financial reports.

This forms reliable information and records to the people of a firm.

This assist to segregate assets, liabilities, income and expenditure. All these

standards and policies are elaborated under regulatory and conceptual framework

constant relevant to capital and revenue maintained.

Q3: Determination of primary stakeholders of M&S and their benefits:

Stakeholders are required to recognised as independent bodies those are accountable for firm’s

decision-making process (Shah, Liang and Akbar, 2013). They could influence by diverse firms’

policies and objectives. Some of the crucial stakeholders are creditors, members, government

and supplier from which complete operation of business draws its resources. There are main

party of a company those are having few common interest in it. They could influence by

decision- making those are required to be completed by M&S for emerging better brand image in

the market. In addition to this, the modern theory goes beyond this primary notion to oversee

additional stakeholders like government.

They could form direct or indirect effect on the work execution of M&S. As, internal

stakeholders are having curiosity in the firm as this emerge via direct relation. While on the other

hand, external stakeholders are the outsiders and they do not perform actively in the company’s

operations but they are connected to the company in some point by actions and consequences

(Pelger, 2016). Each stakeholder is accountable forming enhancing competence and productivity

of M&S. They are advantages for them to have each information regarding capital invested and

profits they are getting from total investment. They are advantageous for them to have each

information related to capital invested and return they are achieved from total investment. They

implement to assess diverse financial reports.

Advantages to company:

Stakeholders helps the firm to make transparency in the company which would further

help out to look the growth of the firm.

They are linked with decision making process and to eliminate the process and also

eliminate the risk which emerge in a firm because of not implementing appropriate

measures.

3

This assist to determine the objective of financial statements.

Helps producer of publishing the financial reports.

This forms reliable information and records to the people of a firm.

This assist to segregate assets, liabilities, income and expenditure. All these

standards and policies are elaborated under regulatory and conceptual framework

constant relevant to capital and revenue maintained.

Q3: Determination of primary stakeholders of M&S and their benefits:

Stakeholders are required to recognised as independent bodies those are accountable for firm’s

decision-making process (Shah, Liang and Akbar, 2013). They could influence by diverse firms’

policies and objectives. Some of the crucial stakeholders are creditors, members, government

and supplier from which complete operation of business draws its resources. There are main

party of a company those are having few common interest in it. They could influence by

decision- making those are required to be completed by M&S for emerging better brand image in

the market. In addition to this, the modern theory goes beyond this primary notion to oversee

additional stakeholders like government.

They could form direct or indirect effect on the work execution of M&S. As, internal

stakeholders are having curiosity in the firm as this emerge via direct relation. While on the other

hand, external stakeholders are the outsiders and they do not perform actively in the company’s

operations but they are connected to the company in some point by actions and consequences

(Pelger, 2016). Each stakeholder is accountable forming enhancing competence and productivity

of M&S. They are advantages for them to have each information regarding capital invested and

profits they are getting from total investment. They are advantageous for them to have each

information related to capital invested and return they are achieved from total investment. They

implement to assess diverse financial reports.

Advantages to company:

Stakeholders helps the firm to make transparency in the company which would further

help out to look the growth of the firm.

They are linked with decision making process and to eliminate the process and also

eliminate the risk which emerge in a firm because of not implementing appropriate

measures.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Stakeholders by taking help of financial statements, can create the portfolio on the basis

of them. There are various objectives that can be achieved by using diverse tools.

Being an effective role model for employees, they are ever ready to enhance the moral of

workers and other people.

As per the financial report, they could emerge future investment decision. This would

assist M&S firm to monitor their functions in a most prominent manner.

By the help of financial reporting, stakeholders could identify existing position of the

nation for facing the competitors those are selling in the similar business line.

They are the person which can participate in the firm’s general meeting and could

determine capital structure of the firm.

Q4: Value of financial reporting for meeting organisation goals

Accounting report is considering as one of the indispensable section of an enterprise because it

keeps the records of entire expenditure whatever is incurring in an association which is helpful in

decision making process (Navarro Galera and Rodríguez Bolívar, 2011). In fact, department of

report is significant for management team as it aids while planning and during allocation of

resources. However, it plays a crucial role in making strategies, policies designing as well as

selection of optimum alternatives for development and growth of an association. Therefore, it

includes various essential statements such as; cash flow statements, financial positioning, income

statements, expense incurred in an enterprise, factory account, profit and loss account. Thus, all

these significant statements are concluded in single format in order to design summary of entire

project. For instance, accounting statements of selected form highlight the entire turnover of a

company and return on investment. Along with this, it aids managers while summarising the data

and designing a conclusive project with the consideration of necessary terms (Markelevich,

Shaw and Weihs, 2011). Additionally, it supports an enterprise in evaluating the recent financial

status or capital overview by which accounting team get succeeded in identifying the financial

strength in order to repay future debts or liabilities. Mainly, these statements are appropriate for

accountants, company auditors, stakeholder and various other members invested in an

association. Hence, three necessary statements are described as follows: Cash flow statement: - It shows the overview of flowing cash internally and externally in

an enterprise into three main segments such as; operating, investing and financial

4

of them. There are various objectives that can be achieved by using diverse tools.

Being an effective role model for employees, they are ever ready to enhance the moral of

workers and other people.

As per the financial report, they could emerge future investment decision. This would

assist M&S firm to monitor their functions in a most prominent manner.

By the help of financial reporting, stakeholders could identify existing position of the

nation for facing the competitors those are selling in the similar business line.

They are the person which can participate in the firm’s general meeting and could

determine capital structure of the firm.

Q4: Value of financial reporting for meeting organisation goals

Accounting report is considering as one of the indispensable section of an enterprise because it

keeps the records of entire expenditure whatever is incurring in an association which is helpful in

decision making process (Navarro Galera and Rodríguez Bolívar, 2011). In fact, department of

report is significant for management team as it aids while planning and during allocation of

resources. However, it plays a crucial role in making strategies, policies designing as well as

selection of optimum alternatives for development and growth of an association. Therefore, it

includes various essential statements such as; cash flow statements, financial positioning, income

statements, expense incurred in an enterprise, factory account, profit and loss account. Thus, all

these significant statements are concluded in single format in order to design summary of entire

project. For instance, accounting statements of selected form highlight the entire turnover of a

company and return on investment. Along with this, it aids managers while summarising the data

and designing a conclusive project with the consideration of necessary terms (Markelevich,

Shaw and Weihs, 2011). Additionally, it supports an enterprise in evaluating the recent financial

status or capital overview by which accounting team get succeeded in identifying the financial

strength in order to repay future debts or liabilities. Mainly, these statements are appropriate for

accountants, company auditors, stakeholder and various other members invested in an

association. Hence, three necessary statements are described as follows: Cash flow statement: - It shows the overview of flowing cash internally and externally in

an enterprise into three main segments such as; operating, investing and financial

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Income statement: - Operating and administration expenses are falls under this category.

Thus, high level of income over expenditures are considered as profit and vice versa.

Financial position statement or balance sheet: - Amount of company assets and

liabilities are falls under this statement which is further bifurcated into two different

parts. Therefore, recent or fixed assets are falling under assets side of balance sheet

whereas current liabilities are on other side.

Q5: Various financial statement analysis

A: Statement of profit and loss:

Particular Amount

Sales 285100

Less: COGS 191700

Gross profits 93400

Rental income 1600

Loss on revaluation of investment

property 3300

Loss on sale of inventory 400

Operating expenses 43100

Profit from operation 44600

Bank interest 1030

Preference dividend 1330

PBT 42240

Tax expenses 12000

Profit after tax for equity shareholders 30240

Working note:

Calculation of Depreciation: Amount

On Land and property:

Property 4000

Plant and equipment 48000-22400*12.5% 3200

Total 7200

5

Thus, high level of income over expenditures are considered as profit and vice versa.

Financial position statement or balance sheet: - Amount of company assets and

liabilities are falls under this statement which is further bifurcated into two different

parts. Therefore, recent or fixed assets are falling under assets side of balance sheet

whereas current liabilities are on other side.

Q5: Various financial statement analysis

A: Statement of profit and loss:

Particular Amount

Sales 285100

Less: COGS 191700

Gross profits 93400

Rental income 1600

Loss on revaluation of investment

property 3300

Loss on sale of inventory 400

Operating expenses 43100

Profit from operation 44600

Bank interest 1030

Preference dividend 1330

PBT 42240

Tax expenses 12000

Profit after tax for equity shareholders 30240

Working note:

Calculation of Depreciation: Amount

On Land and property:

Property 4000

Plant and equipment 48000-22400*12.5% 3200

Total 7200

5

Charged to cost of sales 3600

Charged to operating expenses 3600

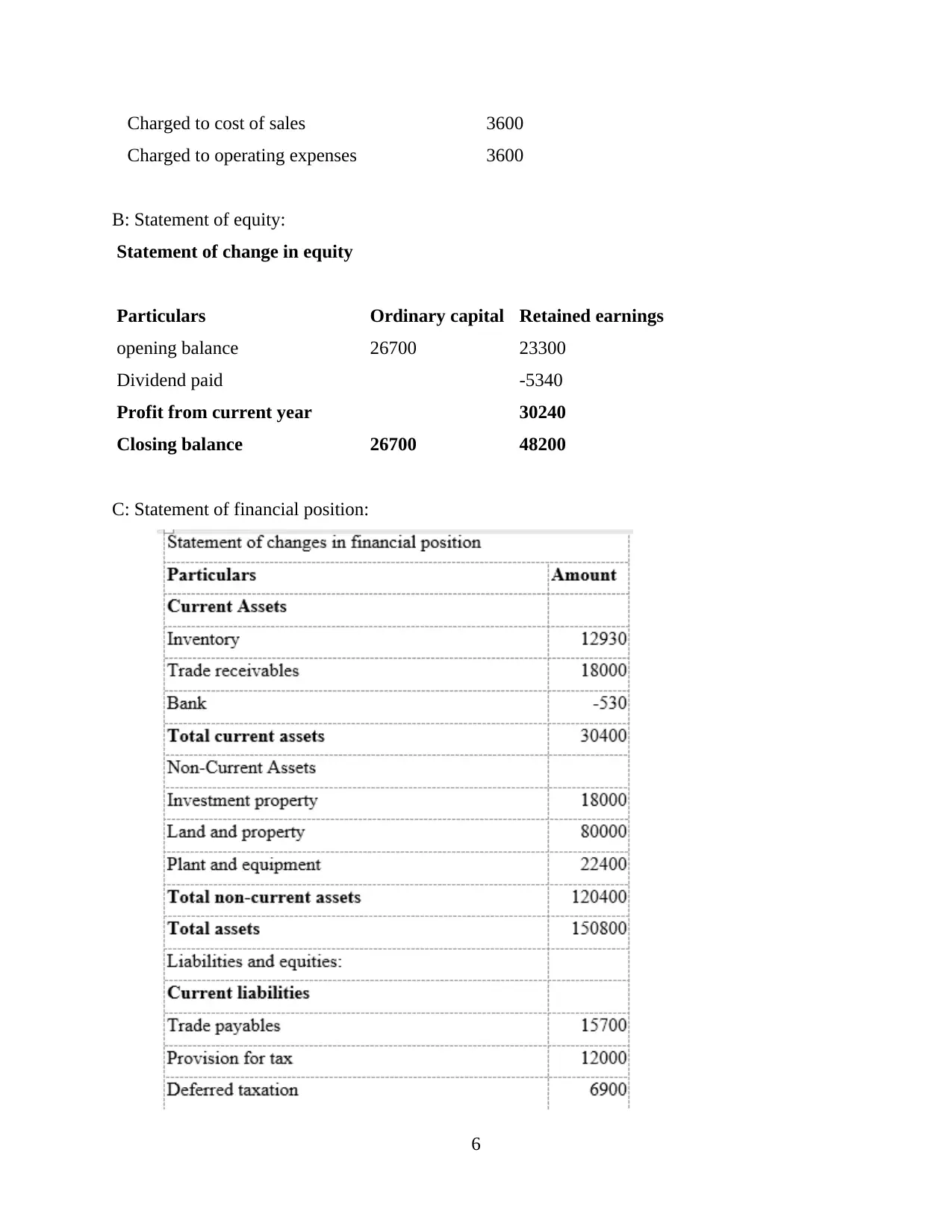

B: Statement of equity:

Statement of change in equity

Particulars Ordinary capital Retained earnings

opening balance 26700 23300

Dividend paid -5340

Profit from current year 30240

Closing balance 26700 48200

C: Statement of financial position:

6

Charged to operating expenses 3600

B: Statement of equity:

Statement of change in equity

Particulars Ordinary capital Retained earnings

opening balance 26700 23300

Dividend paid -5340

Profit from current year 30240

Closing balance 26700 48200

C: Statement of financial position:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

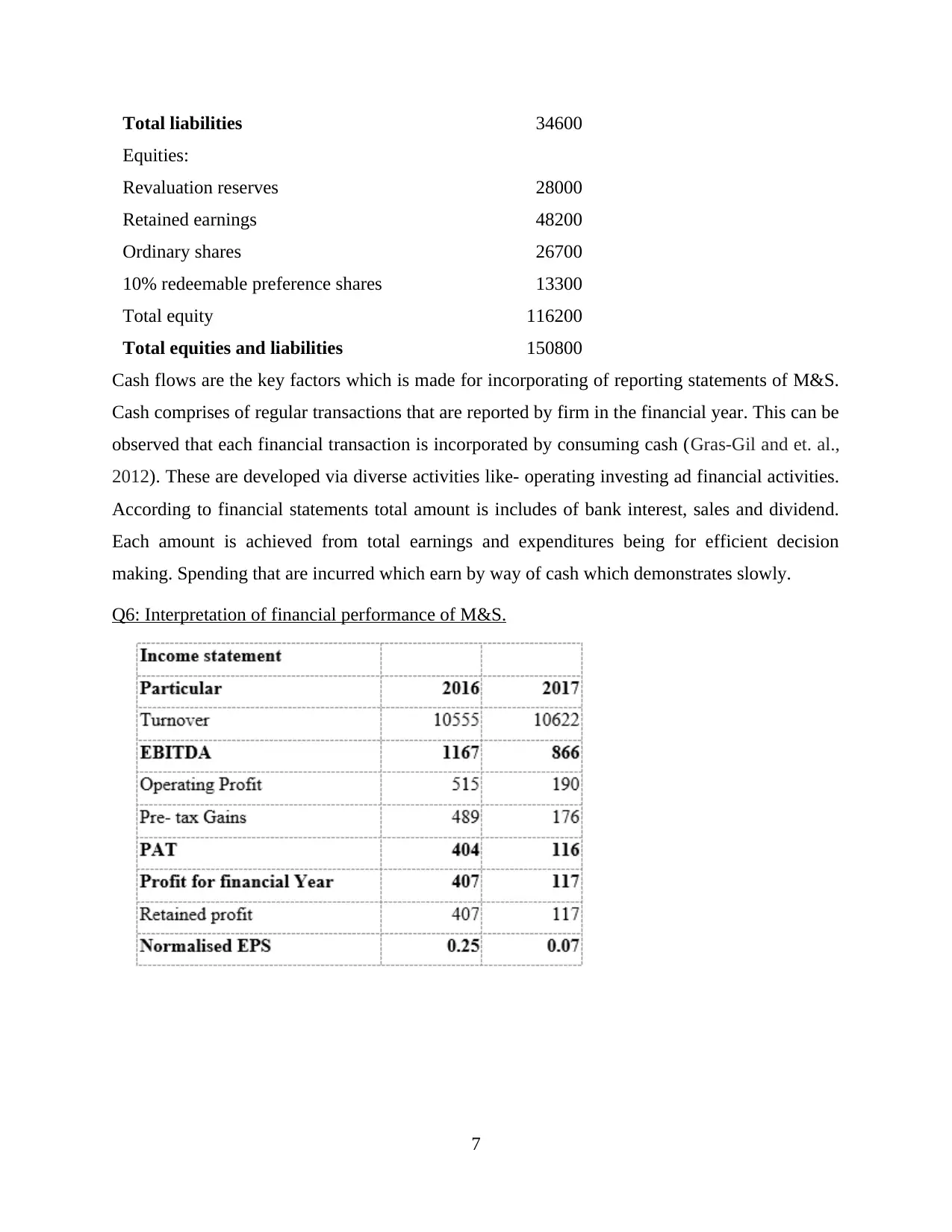

Total liabilities 34600

Equities:

Revaluation reserves 28000

Retained earnings 48200

Ordinary shares 26700

10% redeemable preference shares 13300

Total equity 116200

Total equities and liabilities 150800

Cash flows are the key factors which is made for incorporating of reporting statements of M&S.

Cash comprises of regular transactions that are reported by firm in the financial year. This can be

observed that each financial transaction is incorporated by consuming cash (Gras-Gil and et. al.,

2012). These are developed via diverse activities like- operating investing ad financial activities.

According to financial statements total amount is includes of bank interest, sales and dividend.

Each amount is achieved from total earnings and expenditures being for efficient decision

making. Spending that are incurred which earn by way of cash which demonstrates slowly.

Q6: Interpretation of financial performance of M&S.

7

Equities:

Revaluation reserves 28000

Retained earnings 48200

Ordinary shares 26700

10% redeemable preference shares 13300

Total equity 116200

Total equities and liabilities 150800

Cash flows are the key factors which is made for incorporating of reporting statements of M&S.

Cash comprises of regular transactions that are reported by firm in the financial year. This can be

observed that each financial transaction is incorporated by consuming cash (Gras-Gil and et. al.,

2012). These are developed via diverse activities like- operating investing ad financial activities.

According to financial statements total amount is includes of bank interest, sales and dividend.

Each amount is achieved from total earnings and expenditures being for efficient decision

making. Spending that are incurred which earn by way of cash which demonstrates slowly.

Q6: Interpretation of financial performance of M&S.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

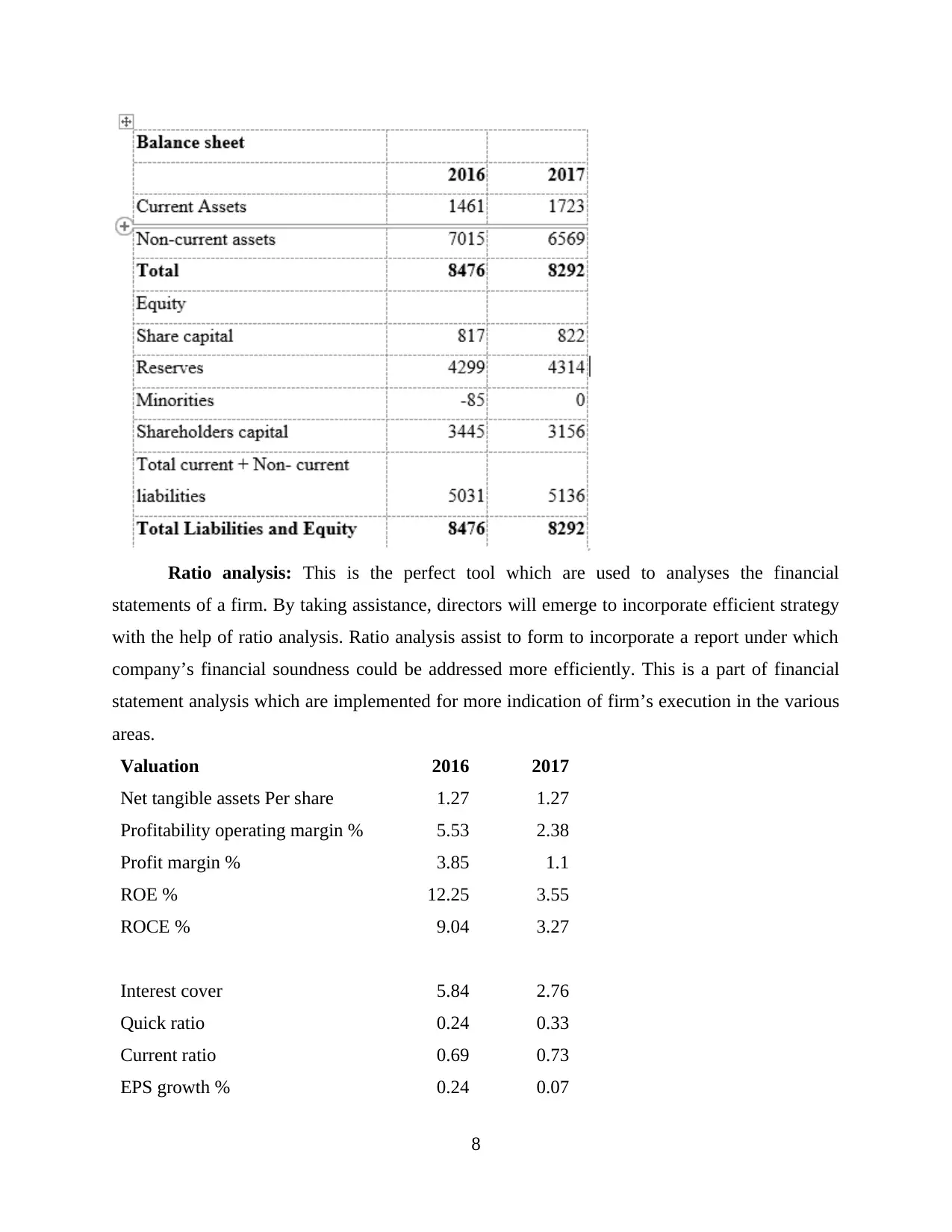

Ratio analysis: This is the perfect tool which are used to analyses the financial

statements of a firm. By taking assistance, directors will emerge to incorporate efficient strategy

with the help of ratio analysis. Ratio analysis assist to form to incorporate a report under which

company’s financial soundness could be addressed more efficiently. This is a part of financial

statement analysis which are implemented for more indication of firm’s execution in the various

areas.

Valuation 2016 2017

Net tangible assets Per share 1.27 1.27

Profitability operating margin % 5.53 2.38

Profit margin % 3.85 1.1

ROE % 12.25 3.55

ROCE % 9.04 3.27

Interest cover 5.84 2.76

Quick ratio 0.24 0.33

Current ratio 0.69 0.73

EPS growth % 0.24 0.07

8

statements of a firm. By taking assistance, directors will emerge to incorporate efficient strategy

with the help of ratio analysis. Ratio analysis assist to form to incorporate a report under which

company’s financial soundness could be addressed more efficiently. This is a part of financial

statement analysis which are implemented for more indication of firm’s execution in the various

areas.

Valuation 2016 2017

Net tangible assets Per share 1.27 1.27

Profitability operating margin % 5.53 2.38

Profit margin % 3.85 1.1

ROE % 12.25 3.55

ROCE % 9.04 3.27

Interest cover 5.84 2.76

Quick ratio 0.24 0.33

Current ratio 0.69 0.73

EPS growth % 0.24 0.07

8

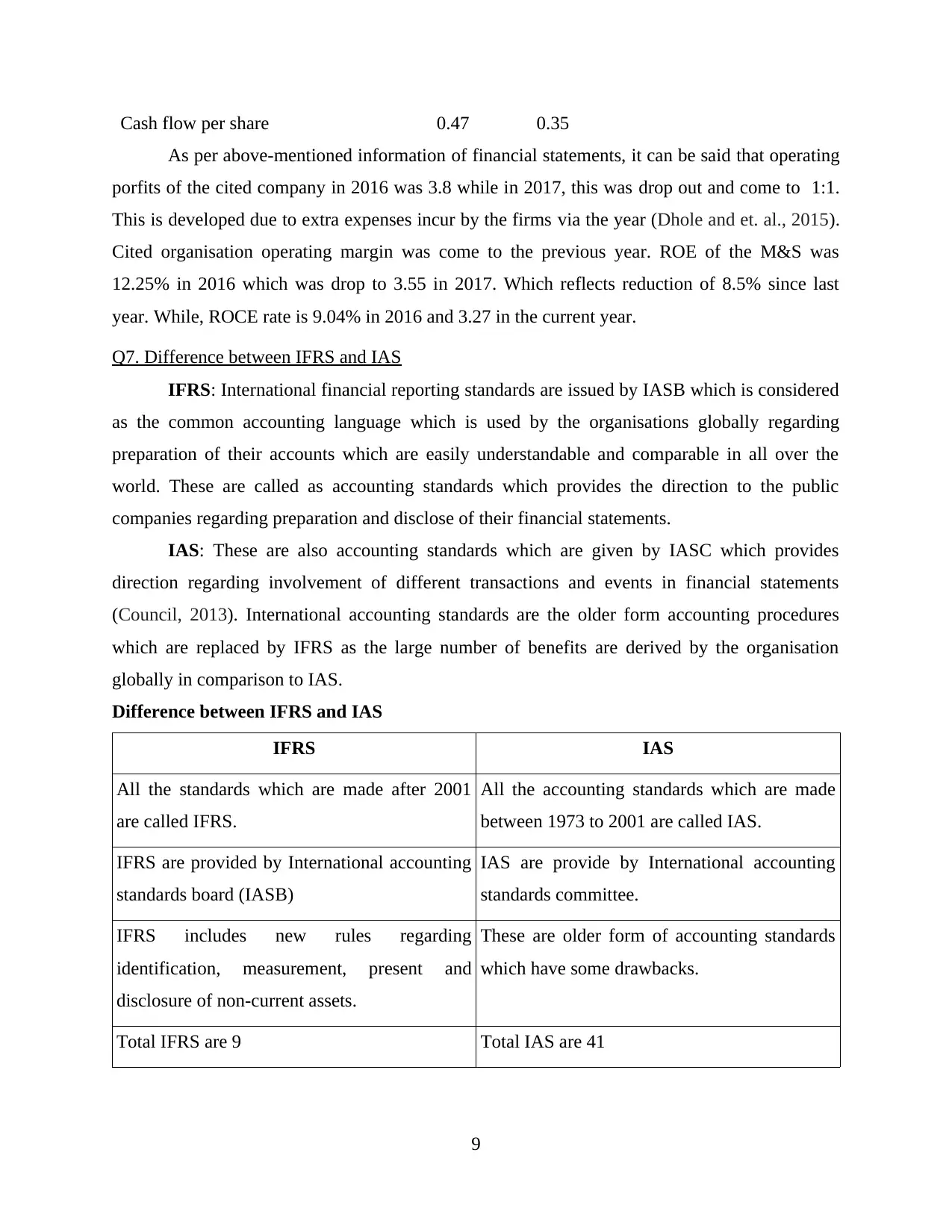

Cash flow per share 0.47 0.35

As per above-mentioned information of financial statements, it can be said that operating

porfits of the cited company in 2016 was 3.8 while in 2017, this was drop out and come to 1:1.

This is developed due to extra expenses incur by the firms via the year (Dhole and et. al., 2015).

Cited organisation operating margin was come to the previous year. ROE of the M&S was

12.25% in 2016 which was drop to 3.55 in 2017. Which reflects reduction of 8.5% since last

year. While, ROCE rate is 9.04% in 2016 and 3.27 in the current year.

Q7. Difference between IFRS and IAS

IFRS: International financial reporting standards are issued by IASB which is considered

as the common accounting language which is used by the organisations globally regarding

preparation of their accounts which are easily understandable and comparable in all over the

world. These are called as accounting standards which provides the direction to the public

companies regarding preparation and disclose of their financial statements.

IAS: These are also accounting standards which are given by IASC which provides

direction regarding involvement of different transactions and events in financial statements

(Council, 2013). International accounting standards are the older form accounting procedures

which are replaced by IFRS as the large number of benefits are derived by the organisation

globally in comparison to IAS.

Difference between IFRS and IAS

IFRS IAS

All the standards which are made after 2001

are called IFRS.

All the accounting standards which are made

between 1973 to 2001 are called IAS.

IFRS are provided by International accounting

standards board (IASB)

IAS are provide by International accounting

standards committee.

IFRS includes new rules regarding

identification, measurement, present and

disclosure of non-current assets.

These are older form of accounting standards

which have some drawbacks.

Total IFRS are 9 Total IAS are 41

9

As per above-mentioned information of financial statements, it can be said that operating

porfits of the cited company in 2016 was 3.8 while in 2017, this was drop out and come to 1:1.

This is developed due to extra expenses incur by the firms via the year (Dhole and et. al., 2015).

Cited organisation operating margin was come to the previous year. ROE of the M&S was

12.25% in 2016 which was drop to 3.55 in 2017. Which reflects reduction of 8.5% since last

year. While, ROCE rate is 9.04% in 2016 and 3.27 in the current year.

Q7. Difference between IFRS and IAS

IFRS: International financial reporting standards are issued by IASB which is considered

as the common accounting language which is used by the organisations globally regarding

preparation of their accounts which are easily understandable and comparable in all over the

world. These are called as accounting standards which provides the direction to the public

companies regarding preparation and disclose of their financial statements.

IAS: These are also accounting standards which are given by IASC which provides

direction regarding involvement of different transactions and events in financial statements

(Council, 2013). International accounting standards are the older form accounting procedures

which are replaced by IFRS as the large number of benefits are derived by the organisation

globally in comparison to IAS.

Difference between IFRS and IAS

IFRS IAS

All the standards which are made after 2001

are called IFRS.

All the accounting standards which are made

between 1973 to 2001 are called IAS.

IFRS are provided by International accounting

standards board (IASB)

IAS are provide by International accounting

standards committee.

IFRS includes new rules regarding

identification, measurement, present and

disclosure of non-current assets.

These are older form of accounting standards

which have some drawbacks.

Total IFRS are 9 Total IAS are 41

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.