MSc Professional Accounting Report: M&A Advisory and Factors

VerifiedAdded on 2021/05/31

|26

|7708

|18

Report

AI Summary

This report, prepared for an MSc in Professional Accounting, delves into the realm of mergers and acquisitions (M&A). It begins with an introduction that highlights the increasing significance of M&A in the corporate world, citing statistics on global deal volumes and the growing role of M&A advisory firms. The report provides an overview of M&A, defining mergers and acquisitions, and distinguishing between different types such as horizontal, vertical, and conglomerate mergers, as well as friendly and hostile takeovers. It then examines the factors influencing the choice of M&A advisory firms, emphasizing the benefits of intermediaries, such as efficiency gains in information gathering and partner searching. The report also explores critical success factors for target companies and project success criteria, defining these terms and highlighting their importance in determining project outcomes. Furthermore, it discusses the critical factors that lead to spotting winning mergers and concludes by summarizing the key findings and providing references for further study. The report aims to provide a comprehensive understanding of M&A activities, the roles of advisory firms, and the critical elements that contribute to successful outcomes.

Running head: MSC PROFESSIONAL ACCOUNTING

MSc Professional Accounting

Name of the Student

Name of the University

Author’s Note

MSc Professional Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MSC PROFESSIONAL ACCOUNTING

Table of Contents

Section 1..............................................................................................................................2

Introduction..........................................................................................................................2

Mergers and Acquisition Overview.....................................................................................3

Factors affecting merger and acquisition advisory choice..................................................6

Critical Success Factors for the target company..................................................................8

Project Success Criteria.......................................................................................................9

Critical success factors......................................................................................................12

Critical success factors for projects...................................................................................12

Spotting Winning Mergers’ Critical Characteristics.........................................................13

Conclusion.........................................................................................................................14

References for Section 1....................................................................................................16

Section 2............................................................................................................................19

Reflective Essay.................................................................................................................19

References for Section 2....................................................................................................23

Table of Contents

Section 1..............................................................................................................................2

Introduction..........................................................................................................................2

Mergers and Acquisition Overview.....................................................................................3

Factors affecting merger and acquisition advisory choice..................................................6

Critical Success Factors for the target company..................................................................8

Project Success Criteria.......................................................................................................9

Critical success factors......................................................................................................12

Critical success factors for projects...................................................................................12

Spotting Winning Mergers’ Critical Characteristics.........................................................13

Conclusion.........................................................................................................................14

References for Section 1....................................................................................................16

Section 2............................................................................................................................19

Reflective Essay.................................................................................................................19

References for Section 2....................................................................................................23

2MSC PROFESSIONAL ACCOUNTING

Section 1

Introduction

As discussed by El-Khatib, Fogel and Jandik (2015), the corporate mergers and

acquisitions have received a lot of publicity in the academic as well as corporate world. In 2005,

Thompson Financial reports were seen to announce a worldwide deal volume of US $ 2.7 trillion

which is an increase of more than 38% from $ 2 trillion in 2004. In compared to this, the value of

the deal increased by 33.3% to USD 1.1 trillion an announced in 2005. Additionally, the Europe

deal volume also went up by 37% to US $ 1.2 trillion and additionally the Asian deal volume

also experienced a surge of 64% to USD to 280 million. Several corporations around the world

considered M&A strategies for realizing the cost synergies as for the increased competition,

product mix, pricing pressures and concentration of the asset.

In the recent times, as the number of M&A transactions keeps on increasing, the advisory

entities of M&A as those opposed to the global investment banking have been benefited from

this trend. The global investment banking and brokerage industry is depicted to generate total

revenue of USD 57.5 billion in 2005 in which USD 19 billion was as a result of M&A activities.

Additionally, it is also not common for the company’s especially small and medium companies

with insufficient expertise to manage thine house M&A activities. It is more common for the

large corporations for establishing the in-house financial and corporate deployment departments

for employing the advisory services and utilizing the valuable content network and efficient use

of client personal close to monitor the transactions (Products 2015).

The main purpose of the study inside discussing the fact that shareholders in “target

company gain more in the short-term and medium-term compared to the shareholders in the

Section 1

Introduction

As discussed by El-Khatib, Fogel and Jandik (2015), the corporate mergers and

acquisitions have received a lot of publicity in the academic as well as corporate world. In 2005,

Thompson Financial reports were seen to announce a worldwide deal volume of US $ 2.7 trillion

which is an increase of more than 38% from $ 2 trillion in 2004. In compared to this, the value of

the deal increased by 33.3% to USD 1.1 trillion an announced in 2005. Additionally, the Europe

deal volume also went up by 37% to US $ 1.2 trillion and additionally the Asian deal volume

also experienced a surge of 64% to USD to 280 million. Several corporations around the world

considered M&A strategies for realizing the cost synergies as for the increased competition,

product mix, pricing pressures and concentration of the asset.

In the recent times, as the number of M&A transactions keeps on increasing, the advisory

entities of M&A as those opposed to the global investment banking have been benefited from

this trend. The global investment banking and brokerage industry is depicted to generate total

revenue of USD 57.5 billion in 2005 in which USD 19 billion was as a result of M&A activities.

Additionally, it is also not common for the company’s especially small and medium companies

with insufficient expertise to manage thine house M&A activities. It is more common for the

large corporations for establishing the in-house financial and corporate deployment departments

for employing the advisory services and utilizing the valuable content network and efficient use

of client personal close to monitor the transactions (Products 2015).

The main purpose of the study inside discussing the fact that shareholders in “target

company gain more in the short-term and medium-term compared to the shareholders in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MSC PROFESSIONAL ACCOUNTING

acquiring company”. This discussion is further supported with various types of assessments

which are associated to the process of conducting is business combination activities.

Additionally, the project’s success criteria are also measured from the merger and acquisition of

advisory firms (Belleflamme, Lambert and Schwienbacher 2014).

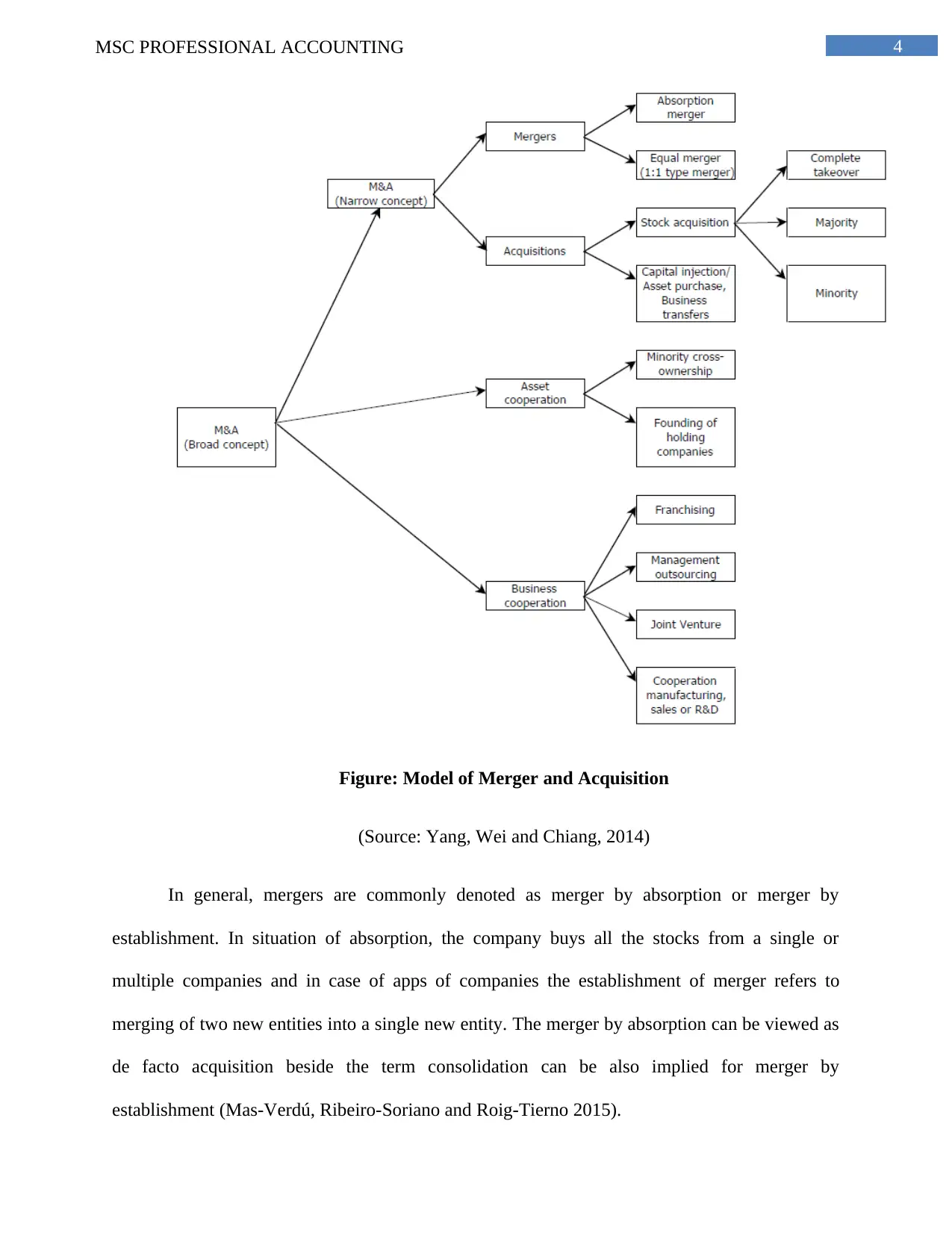

Mergers and Acquisition Overview

The topic of merger and activity is gaining increasing importance in the last two decades

with response to more and more merger and activities being increasingly complex in terms of

transactions involved. In a broad sense, M&A activity implies the total number of different

transactions which ranges from a number of purchase and sales activity is concentrated between

the joint ventures, alliances and undertakings for ensuring independence of business. There are

several explanations to this theory which leads to confusion and misunderstanding due to the

strategic alliances. Merger is identified as a combination between two entities for creating a

separate entity. Acquisition is the act of purchasing assets or shares of another company for

achieving managerial influence which may not be or maybe in the mutual agreement (Kansal and

Chandani 2014). The model of M&A has been depicted below as follows

acquiring company”. This discussion is further supported with various types of assessments

which are associated to the process of conducting is business combination activities.

Additionally, the project’s success criteria are also measured from the merger and acquisition of

advisory firms (Belleflamme, Lambert and Schwienbacher 2014).

Mergers and Acquisition Overview

The topic of merger and activity is gaining increasing importance in the last two decades

with response to more and more merger and activities being increasingly complex in terms of

transactions involved. In a broad sense, M&A activity implies the total number of different

transactions which ranges from a number of purchase and sales activity is concentrated between

the joint ventures, alliances and undertakings for ensuring independence of business. There are

several explanations to this theory which leads to confusion and misunderstanding due to the

strategic alliances. Merger is identified as a combination between two entities for creating a

separate entity. Acquisition is the act of purchasing assets or shares of another company for

achieving managerial influence which may not be or maybe in the mutual agreement (Kansal and

Chandani 2014). The model of M&A has been depicted below as follows

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MSC PROFESSIONAL ACCOUNTING

Figure: Model of Merger and Acquisition

(Source: Yang, Wei and Chiang, 2014)

In general, mergers are commonly denoted as merger by absorption or merger by

establishment. In situation of absorption, the company buys all the stocks from a single or

multiple companies and in case of apps of companies the establishment of merger refers to

merging of two new entities into a single new entity. The merger by absorption can be viewed as

de facto acquisition beside the term consolidation can be also implied for merger by

establishment (Mas-Verdú, Ribeiro-Soriano and Roig-Tierno 2015).

Figure: Model of Merger and Acquisition

(Source: Yang, Wei and Chiang, 2014)

In general, mergers are commonly denoted as merger by absorption or merger by

establishment. In situation of absorption, the company buys all the stocks from a single or

multiple companies and in case of apps of companies the establishment of merger refers to

merging of two new entities into a single new entity. The merger by absorption can be viewed as

de facto acquisition beside the term consolidation can be also implied for merger by

establishment (Mas-Verdú, Ribeiro-Soriano and Roig-Tierno 2015).

5MSC PROFESSIONAL ACCOUNTING

During the acquisition of companies, the buying company may pursue a significant share

of the stocks of a target company. Similarly, there are important forms of acquisition, namely

share acquisition and asset acquisitions. In a share acquisition, the company is depicted to

purchase certain percentage of stocks of the target company for influencing the management.

Whereas, during asset acquisition the company buys all parts of the target company’s assets and

the target sustains as a legal entity. Based on the significance of shares of stocks, the company

acquisitions are further categorized into three types. This includes: “complete take over (100%

of target’s issued shares)”, “majority (50-99%)”, and “minority (less than 50%)” (Yilmaz and

Tanyeri 2016). In addition to this, the merger and acquisition are depicted as to separate from the

actions which have several consequences based on the legal obligations, tax liabilities and

procedure of acquisition. Despite of this, in general the final outcome of M&A transactions

considered in which two or more companies are seen to combine their business affords and we

do not make an effort to separate this merger transaction from acquisition ones. In such a

situation, M&A is treated as a corporate finance service which provides M&A advice to the

firms (Ferris, Houston and Javakhadze 2016).

In context of classification of mergers and acquisitions, the main perspective of value

chain for M&A is categorized as horizontal, vertical or conglomerate. In case of horizontal

M&A, the target companies and the acquiring companies are depicted as competing in the same

industry. In addition to this, in horizontal business combination process the restructuring in

business occurs as a result of technological changes and liberalization. This particular trade is

evident in industries related to petroleum, the mobile and pharmaceuticals (Yılmaz and Tanyeri

2016). A similar example of this can be seen with the merger of two US giants namely Glaxo

and SmithKline Beecham with a total value of USD 76 billion. Based on the statement of the

former CEO of SmithKline Beecham the main aim of combination of two companies was

depicted with research and development synergies to drive the revenues and explore enormous

During the acquisition of companies, the buying company may pursue a significant share

of the stocks of a target company. Similarly, there are important forms of acquisition, namely

share acquisition and asset acquisitions. In a share acquisition, the company is depicted to

purchase certain percentage of stocks of the target company for influencing the management.

Whereas, during asset acquisition the company buys all parts of the target company’s assets and

the target sustains as a legal entity. Based on the significance of shares of stocks, the company

acquisitions are further categorized into three types. This includes: “complete take over (100%

of target’s issued shares)”, “majority (50-99%)”, and “minority (less than 50%)” (Yilmaz and

Tanyeri 2016). In addition to this, the merger and acquisition are depicted as to separate from the

actions which have several consequences based on the legal obligations, tax liabilities and

procedure of acquisition. Despite of this, in general the final outcome of M&A transactions

considered in which two or more companies are seen to combine their business affords and we

do not make an effort to separate this merger transaction from acquisition ones. In such a

situation, M&A is treated as a corporate finance service which provides M&A advice to the

firms (Ferris, Houston and Javakhadze 2016).

In context of classification of mergers and acquisitions, the main perspective of value

chain for M&A is categorized as horizontal, vertical or conglomerate. In case of horizontal

M&A, the target companies and the acquiring companies are depicted as competing in the same

industry. In addition to this, in horizontal business combination process the restructuring in

business occurs as a result of technological changes and liberalization. This particular trade is

evident in industries related to petroleum, the mobile and pharmaceuticals (Yılmaz and Tanyeri

2016). A similar example of this can be seen with the merger of two US giants namely Glaxo

and SmithKline Beecham with a total value of USD 76 billion. Based on the statement of the

former CEO of SmithKline Beecham the main aim of combination of two companies was

depicted with research and development synergies to drive the revenues and explore enormous

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MSC PROFESSIONAL ACCOUNTING

opportunities for revenue creation. The vertical merger and acquisition are common with firms in

buyer and seller relationship and client supplier relationship. Many companies often seek to

reduce uncertainties of the transaction costs by considering the downstream and upstream

“linkages in the value chain” in order to benefit from economies of scope. Finally, several

companies that tend to diversify the risk and attain economies of scope by engaging in

conglomerate merger and acquisition transaction in which the business are operating as unrelated

entities. For instance, the vertical merger and acquisition is clear with the business combination

of General foods and Philip Morris in a deal of USD 5.6 billion (Porter and Heppelmann 2015).

The last category of merger and acquisition needs to be depicted with friendly and hostile

mergers. In situations when the target company agrees to the transaction then it is known as

friendly merger. On the other hand, if the board refuses an offer in several situations, the

acquiring company offers wishes against the target company. Finally, M&A transaction can also

take place either with cross-border or domestic transaction. In case of cross-border M&A

activity, the two forms located in different economies are depicted to operate in a single

economy but belong to two different countries.

Factors affecting merger and acquisition advisory choice

Comprehensive discussion on the various benefits in acquiring the target firm is often

seen with enjoying the result of employing M&A advisory firm. It needs to be further understood

that there are two prominent advantages of the advisory M & A firms. Firstly, the intermediaries

of M&A are able to deliver a certain level of anonymity to the target and acquiring forms which

is of significant importance due to the initial discussions prior to the start of merger and

acquisition negotiations. Secondly, the intermediaries may have certain specialized knowledge

on the particular characteristics of a form which includes the information on the upmarket

potential and financial potential with that wearers may not have. Additionally, the employment

opportunities for revenue creation. The vertical merger and acquisition are common with firms in

buyer and seller relationship and client supplier relationship. Many companies often seek to

reduce uncertainties of the transaction costs by considering the downstream and upstream

“linkages in the value chain” in order to benefit from economies of scope. Finally, several

companies that tend to diversify the risk and attain economies of scope by engaging in

conglomerate merger and acquisition transaction in which the business are operating as unrelated

entities. For instance, the vertical merger and acquisition is clear with the business combination

of General foods and Philip Morris in a deal of USD 5.6 billion (Porter and Heppelmann 2015).

The last category of merger and acquisition needs to be depicted with friendly and hostile

mergers. In situations when the target company agrees to the transaction then it is known as

friendly merger. On the other hand, if the board refuses an offer in several situations, the

acquiring company offers wishes against the target company. Finally, M&A transaction can also

take place either with cross-border or domestic transaction. In case of cross-border M&A

activity, the two forms located in different economies are depicted to operate in a single

economy but belong to two different countries.

Factors affecting merger and acquisition advisory choice

Comprehensive discussion on the various benefits in acquiring the target firm is often

seen with enjoying the result of employing M&A advisory firm. It needs to be further understood

that there are two prominent advantages of the advisory M & A firms. Firstly, the intermediaries

of M&A are able to deliver a certain level of anonymity to the target and acquiring forms which

is of significant importance due to the initial discussions prior to the start of merger and

acquisition negotiations. Secondly, the intermediaries may have certain specialized knowledge

on the particular characteristics of a form which includes the information on the upmarket

potential and financial potential with that wearers may not have. Additionally, the employment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MSC PROFESSIONAL ACCOUNTING

of M&A intermediaries has the scope of exploiting the various benefits as a result of

comparative advantages (Mnih et al. 2015). Some of the lesser-known facts of engaging in

business combination activities are any moderated as follows:

Efficiency Gains Based On Information Cost

In situations when the form is to not hire any intermediaries for merger and acquisition,

they are particularly seen to see for potential partners by themselves. The information gathering

process takes place with those partners will cause the cost of the firms. In case, there is any

potential of failing to materialize information, it is considered as a waste from society’s point of

view as the intermediaries would create an updated database for potential M&A partners and

utilize the same with various types of engagements. Due to this, the intermediaries of M&A are

often seen to provide the insurance for any scope of sampling error which may seek the firms to

adopt merger and acquisition activities without any advisory assistance. Therefore, the

intermediaries with merger and acquisition market have more efficiency than the ones which

does not have (Ouyang and Hilsenrath 2017).

Efficiency gains as per searching of potential partners

In various situations the forms incline to search for information about the potential

partners only when they are in need for M&A assistance. However, it is to be seen that the

advisory firms continue the searching process of M&A on a continuous basis thereby enabling

that writers for suggesting potential partners to their clients in several conditions thereby

reducing sampling errors.

of M&A intermediaries has the scope of exploiting the various benefits as a result of

comparative advantages (Mnih et al. 2015). Some of the lesser-known facts of engaging in

business combination activities are any moderated as follows:

Efficiency Gains Based On Information Cost

In situations when the form is to not hire any intermediaries for merger and acquisition,

they are particularly seen to see for potential partners by themselves. The information gathering

process takes place with those partners will cause the cost of the firms. In case, there is any

potential of failing to materialize information, it is considered as a waste from society’s point of

view as the intermediaries would create an updated database for potential M&A partners and

utilize the same with various types of engagements. Due to this, the intermediaries of M&A are

often seen to provide the insurance for any scope of sampling error which may seek the firms to

adopt merger and acquisition activities without any advisory assistance. Therefore, the

intermediaries with merger and acquisition market have more efficiency than the ones which

does not have (Ouyang and Hilsenrath 2017).

Efficiency gains as per searching of potential partners

In various situations the forms incline to search for information about the potential

partners only when they are in need for M&A assistance. However, it is to be seen that the

advisory firms continue the searching process of M&A on a continuous basis thereby enabling

that writers for suggesting potential partners to their clients in several conditions thereby

reducing sampling errors.

8MSC PROFESSIONAL ACCOUNTING

When it comes to M&A of the advisory firms, two important empirical studies have a

significant role to play. A sample of acquisition collected from over a period of 1981-1992

shows the assessment of three hypotheses namely “transaction costs, asymmetric information,

and contracting hypotheses”. These empirical researches have shown that the advisory firm of

M&A in the banking industry have depicted several implications on investment bank -assisted

transaction which is more often taken over by hostile means and less likely to be all-cash

financed. In addition to this, when they acquirer is not seen as the first bidder then it is more

likely that the investment bank will take its part. In terms of the contracting hypotheses there are

several studies which showed that investment banks have it reducing tendency of the agency

costs in terms of acquiring the firms which certifies the value of acquisition. Additionally, the

acquiring forms are also more likely to use the investment bank while purchasing of publicly

traded companies (Dimopoulos and Sacchetto 2017).

Critical Success Factors for the target company

As stated by Kruglova and Zubkov (2017), some of the main critical success factors for

the merger and acquisition activities needs to be taken into consideration with the description of

project success standards for M&A projects from different viewpoints and advisory firms. The

second aim of this section identifies the critical factors for merger and acquisition projects.

Before stating the review of the literature it is important to note that terminologies namely

critical success factors and project success criteria have control in determining the review the

party “who gains” and “who loses” in the short, medium and longer terms and whether the gains,

if they exist, are found in all cases (Piper and Schneider 2015).

Critical accomplishment factors are identified as “the set of circumstances, facts, or

influences which contribute to the project outcomes”. Secondly, the success criteria of a project

is set out with the standards of principles through which success in the project can be brought.

When it comes to M&A of the advisory firms, two important empirical studies have a

significant role to play. A sample of acquisition collected from over a period of 1981-1992

shows the assessment of three hypotheses namely “transaction costs, asymmetric information,

and contracting hypotheses”. These empirical researches have shown that the advisory firm of

M&A in the banking industry have depicted several implications on investment bank -assisted

transaction which is more often taken over by hostile means and less likely to be all-cash

financed. In addition to this, when they acquirer is not seen as the first bidder then it is more

likely that the investment bank will take its part. In terms of the contracting hypotheses there are

several studies which showed that investment banks have it reducing tendency of the agency

costs in terms of acquiring the firms which certifies the value of acquisition. Additionally, the

acquiring forms are also more likely to use the investment bank while purchasing of publicly

traded companies (Dimopoulos and Sacchetto 2017).

Critical Success Factors for the target company

As stated by Kruglova and Zubkov (2017), some of the main critical success factors for

the merger and acquisition activities needs to be taken into consideration with the description of

project success standards for M&A projects from different viewpoints and advisory firms. The

second aim of this section identifies the critical factors for merger and acquisition projects.

Before stating the review of the literature it is important to note that terminologies namely

critical success factors and project success criteria have control in determining the review the

party “who gains” and “who loses” in the short, medium and longer terms and whether the gains,

if they exist, are found in all cases (Piper and Schneider 2015).

Critical accomplishment factors are identified as “the set of circumstances, facts, or

influences which contribute to the project outcomes”. Secondly, the success criteria of a project

is set out with the standards of principles through which success in the project can be brought.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MSC PROFESSIONAL ACCOUNTING

The various types of critical factors can be also perceived as a result of impeding conditions

which effect the project result whereas the project success criteria are viewed as a result of

measurement agreed among the stakeholders for assessment of project outcomes. In addition to

this, there are several researchers who have observed the critical success factors in the recent

times to be categorized as dependent variables. In other words, the critical success factors can

significantly have a positive impact on the project outcomes which will be conducive for

assessment of measurement factors as specified in the project success criteria (Abbott et al.

2016). Moreover, the issues associated to project success criteria are stated as follows:

Project Success Criteria

in the past, several early researchers have identified the success criteria is such as “iron

triangle of time, budget and required quality”. However, in the recent corporate environment

these measures are unlikely to fetch the desired outcome. There have been several claims made

that if a project is measured with variables of the time, scope and cost, it suggests that project

management is only serving in a tactical way and not in a strategic way. Based on several types

of literature review it has been explained that the development of criteria leading the success of

the project is based on internal aspects since the external aspects are particularly complicated and

generally included in the handover phase (Bowers, Hall and Srinivasan 2017). Nevertheless, the

recent researchers have included several external aspects which are critical in including

stakeholder community benefits, organizational benefits and achievement of business goals. This

is viewed with in a modern merger acquisition transaction of “Qantas Holidays, Qantas

Business Travel” and the “Jetset Travelworld Retail Group”, merging with “Stella Travel

Services PTY. LTD” (Airline Business 2015).

Some of the other successful mergers and acquisition activities in the country has been

depicted with Hanesbrands Inc. acquisition of Pacific Brand Ltd. in a deal of $ 1.1 billion. “HBI

The various types of critical factors can be also perceived as a result of impeding conditions

which effect the project result whereas the project success criteria are viewed as a result of

measurement agreed among the stakeholders for assessment of project outcomes. In addition to

this, there are several researchers who have observed the critical success factors in the recent

times to be categorized as dependent variables. In other words, the critical success factors can

significantly have a positive impact on the project outcomes which will be conducive for

assessment of measurement factors as specified in the project success criteria (Abbott et al.

2016). Moreover, the issues associated to project success criteria are stated as follows:

Project Success Criteria

in the past, several early researchers have identified the success criteria is such as “iron

triangle of time, budget and required quality”. However, in the recent corporate environment

these measures are unlikely to fetch the desired outcome. There have been several claims made

that if a project is measured with variables of the time, scope and cost, it suggests that project

management is only serving in a tactical way and not in a strategic way. Based on several types

of literature review it has been explained that the development of criteria leading the success of

the project is based on internal aspects since the external aspects are particularly complicated and

generally included in the handover phase (Bowers, Hall and Srinivasan 2017). Nevertheless, the

recent researchers have included several external aspects which are critical in including

stakeholder community benefits, organizational benefits and achievement of business goals. This

is viewed with in a modern merger acquisition transaction of “Qantas Holidays, Qantas

Business Travel” and the “Jetset Travelworld Retail Group”, merging with “Stella Travel

Services PTY. LTD” (Airline Business 2015).

Some of the other successful mergers and acquisition activities in the country has been

depicted with Hanesbrands Inc. acquisition of Pacific Brand Ltd. in a deal of $ 1.1 billion. “HBI

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MSC PROFESSIONAL ACCOUNTING

Australian Acquisition Co. Pty Ltd” was identified a fully subsidiary under Hanesbrands Inc.

Some of the main form of proceeding of the deal can be identified with the offering of an all cash

bid of $ 1.15 per share for 100% of the company. The price was further depicted to be segregated

into a purchase of $ 1.056 and a $ 0.0094 fully franked special dividend per share. The total

transaction has been depicted to be equated with an overall price of $ 1.1 billion.

The Genesee & Wyoming acquisition of Glencore Plc is identified as another important

M&A activity which is worth $1.14 billion. The Glencore involved an asset for the sale program

to reduce the pile of the overall debt. The M&A activity was conducive for the reducing the $ 50

billion debt. The program further led to several types of the issues which are seen to be

associated to the right to transport 40 million of the coal to the Port of Newcastle in each year. In

their complex deal RBC capital ran the Glencore’s auction and Glencore was able to obtain the

legal advice by the “Bank of America Merrill Lynch, and Allens” who was responsible for their

legal work.

The M&A activity of Baring Private Equity and SAI Global Ltd took place in 2016 is

also considered to be significantly important. The $ 1billion was considered as an all cash offer

which was accepted in September for $ 4.75 per share and 34% of the premium was adjusted as

per the weight of the average price at the time of acquisition (The Typewriter 2016).

This merger can directly be viewed as a short-term and medium-term gains for Qantas

group as the main intention of entering into M&A activity was depicted with including

stakeholder community benefits, organizational benefits and fulfilment of business goals of

Qantas. Additionally, there are several other measurements to assess the outcomes of project

which includes different perspectives of viewing the project manager’s opinion and public

opinion in general. These explain why the same project is perceived as a success by a one group

and failure by other. For instance, one project might be identified as successful as per the client,

Australian Acquisition Co. Pty Ltd” was identified a fully subsidiary under Hanesbrands Inc.

Some of the main form of proceeding of the deal can be identified with the offering of an all cash

bid of $ 1.15 per share for 100% of the company. The price was further depicted to be segregated

into a purchase of $ 1.056 and a $ 0.0094 fully franked special dividend per share. The total

transaction has been depicted to be equated with an overall price of $ 1.1 billion.

The Genesee & Wyoming acquisition of Glencore Plc is identified as another important

M&A activity which is worth $1.14 billion. The Glencore involved an asset for the sale program

to reduce the pile of the overall debt. The M&A activity was conducive for the reducing the $ 50

billion debt. The program further led to several types of the issues which are seen to be

associated to the right to transport 40 million of the coal to the Port of Newcastle in each year. In

their complex deal RBC capital ran the Glencore’s auction and Glencore was able to obtain the

legal advice by the “Bank of America Merrill Lynch, and Allens” who was responsible for their

legal work.

The M&A activity of Baring Private Equity and SAI Global Ltd took place in 2016 is

also considered to be significantly important. The $ 1billion was considered as an all cash offer

which was accepted in September for $ 4.75 per share and 34% of the premium was adjusted as

per the weight of the average price at the time of acquisition (The Typewriter 2016).

This merger can directly be viewed as a short-term and medium-term gains for Qantas

group as the main intention of entering into M&A activity was depicted with including

stakeholder community benefits, organizational benefits and fulfilment of business goals of

Qantas. Additionally, there are several other measurements to assess the outcomes of project

which includes different perspectives of viewing the project manager’s opinion and public

opinion in general. These explain why the same project is perceived as a success by a one group

and failure by other. For instance, one project might be identified as successful as per the client,

11MSC PROFESSIONAL ACCOUNTING

on the other hand the same project may not be finished within timeframe and be considered

unsuccessful in the aspect of project management (Obokata et al. 2014).

With particular relevance to M&A projects, the advisory Council of the firms often take

control of the Central advisory role on client’s behalf. In several situations, the project team

forms its own member of personal with varying nature of expertise is and the stakeholders either

in the target form or acquiring form. In other situations, the key stakeholders are considered as its

clients either in the target form or acquiring firm. In situations, then there is requirement for

several advisers, the M&A advisory firm especially the investment banks take his role is as a

coordinator.

On the other hand, there are several understandings from other excerpts states that forms

engage in different types of M&A activities which can bring successful fulfilment of the firm’s

motives. In case, the merger and acquisition deal is initiated the manager toward their own

individual benefits are allowed to maximize the same. In majority of the cases, the motives can

be realized once the deal is closed. In general, M&A advisory firm are normally seen to be

engaged in several stages towards the closure. In these cases, a major concern is seen with the

significant influence. This points to the concurrence of one finding from an empirical study

stated that the benefit of choosing high-quality investment banker using a sample of 114 U.S.-

based deals of M&A obtained out of the 600 completed deals reported by Mergers &

Acquisitions. The study showed that the investment bank acted as an intermediary and did not

create wealth which underlies the main motives of M&A advisor choice. The main findings of

the study further revealed that the absolute and relative wealth were not related to each other and

there was a possibility of negative correlation with the reputation of the advisor and bidder. This

has raised several questions about the doubts concerned with merger and acquisition projects.

on the other hand the same project may not be finished within timeframe and be considered

unsuccessful in the aspect of project management (Obokata et al. 2014).

With particular relevance to M&A projects, the advisory Council of the firms often take

control of the Central advisory role on client’s behalf. In several situations, the project team

forms its own member of personal with varying nature of expertise is and the stakeholders either

in the target form or acquiring form. In other situations, the key stakeholders are considered as its

clients either in the target form or acquiring firm. In situations, then there is requirement for

several advisers, the M&A advisory firm especially the investment banks take his role is as a

coordinator.

On the other hand, there are several understandings from other excerpts states that forms

engage in different types of M&A activities which can bring successful fulfilment of the firm’s

motives. In case, the merger and acquisition deal is initiated the manager toward their own

individual benefits are allowed to maximize the same. In majority of the cases, the motives can

be realized once the deal is closed. In general, M&A advisory firm are normally seen to be

engaged in several stages towards the closure. In these cases, a major concern is seen with the

significant influence. This points to the concurrence of one finding from an empirical study

stated that the benefit of choosing high-quality investment banker using a sample of 114 U.S.-

based deals of M&A obtained out of the 600 completed deals reported by Mergers &

Acquisitions. The study showed that the investment bank acted as an intermediary and did not

create wealth which underlies the main motives of M&A advisor choice. The main findings of

the study further revealed that the absolute and relative wealth were not related to each other and

there was a possibility of negative correlation with the reputation of the advisor and bidder. This

has raised several questions about the doubts concerned with merger and acquisition projects.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.