MSIN0001 Corporate Finance Sample Paper: Detailed Solutions & Analysis

VerifiedAdded on 2023/06/12

|8

|1074

|338

Homework Assignment

AI Summary

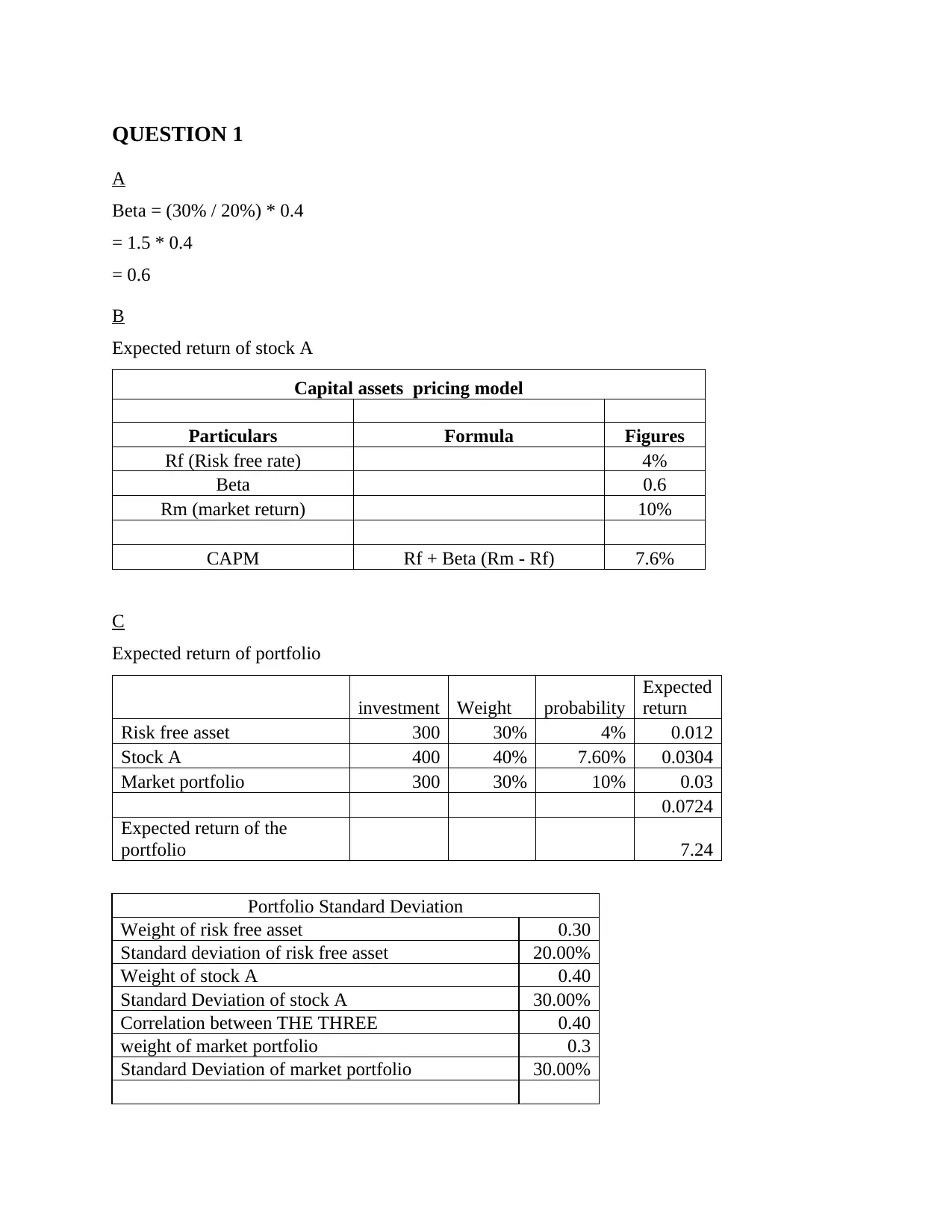

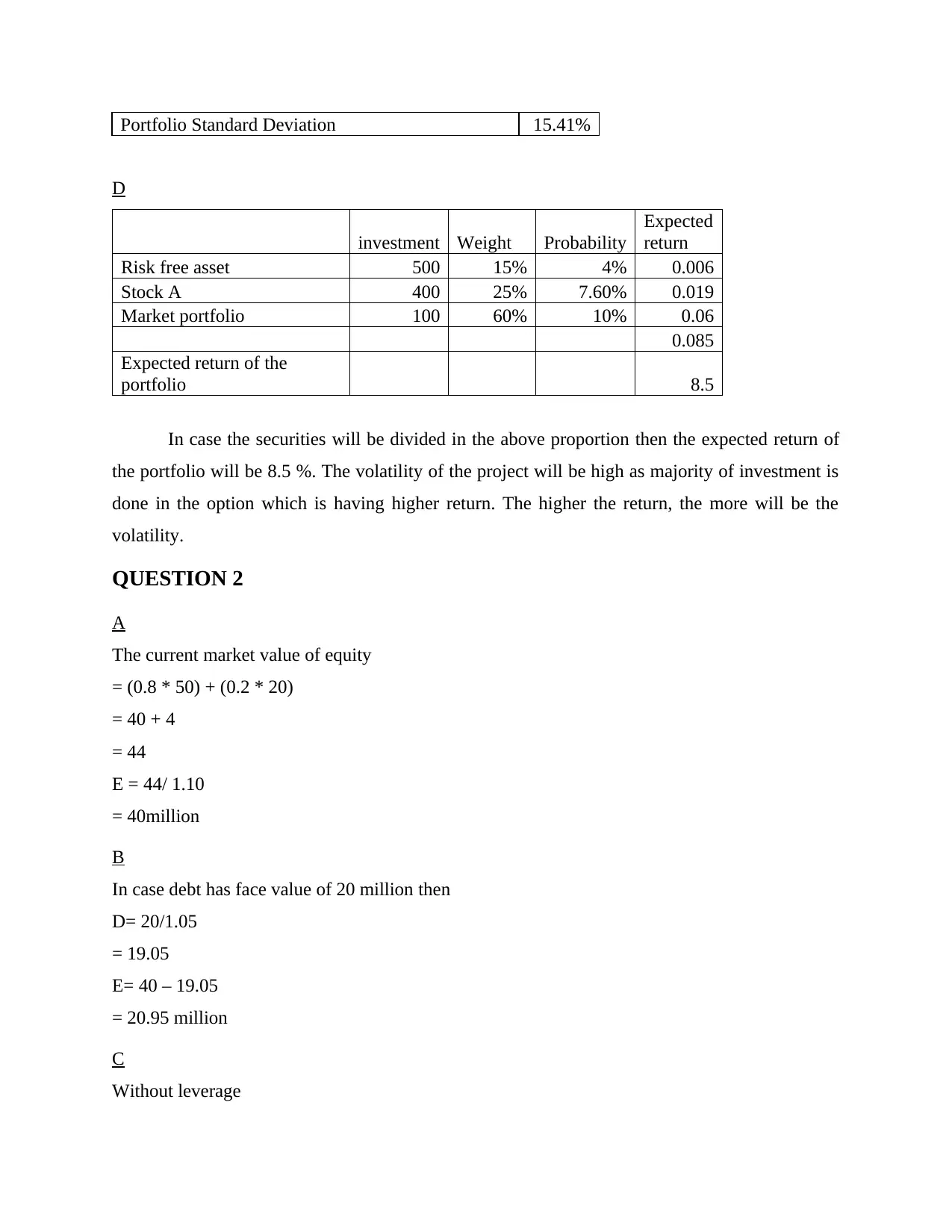

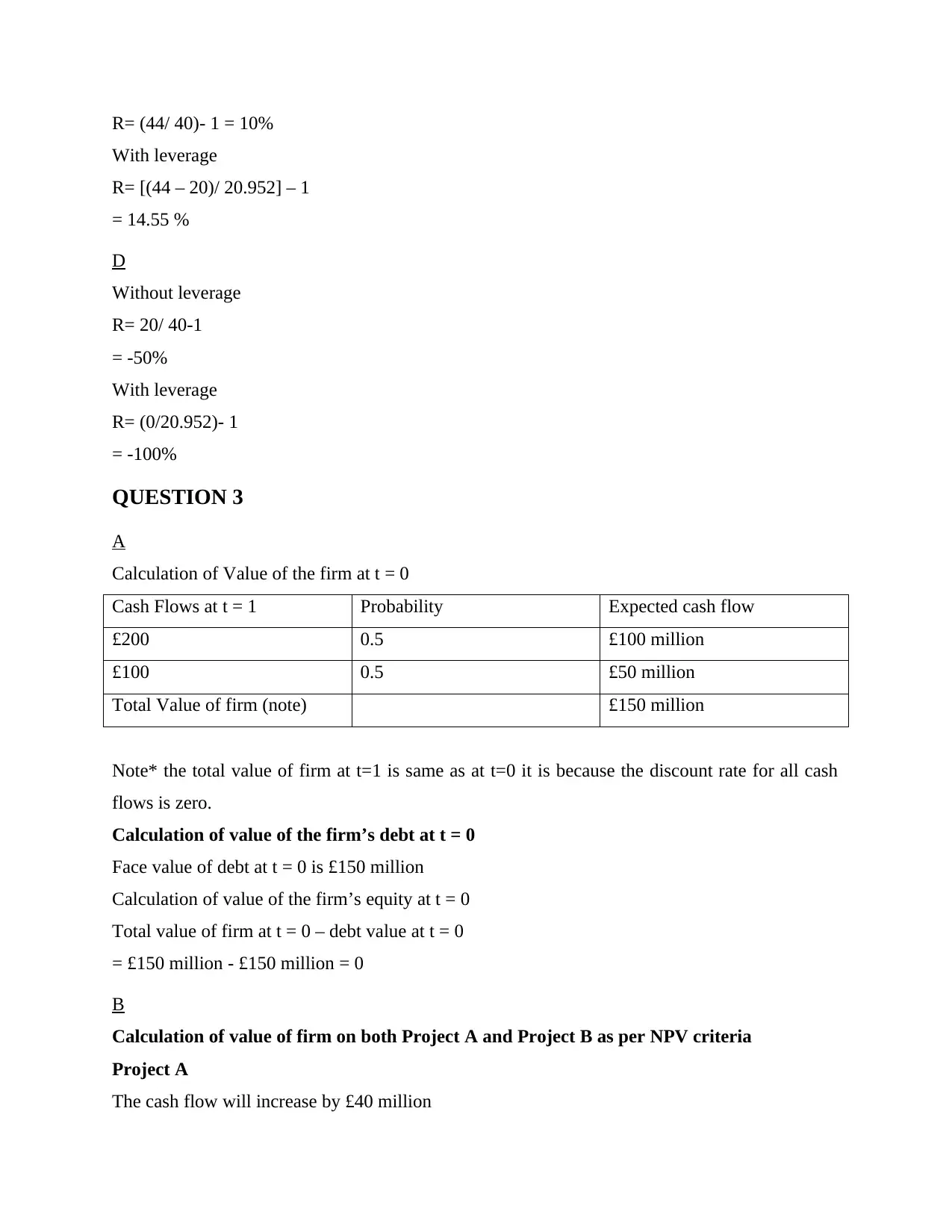

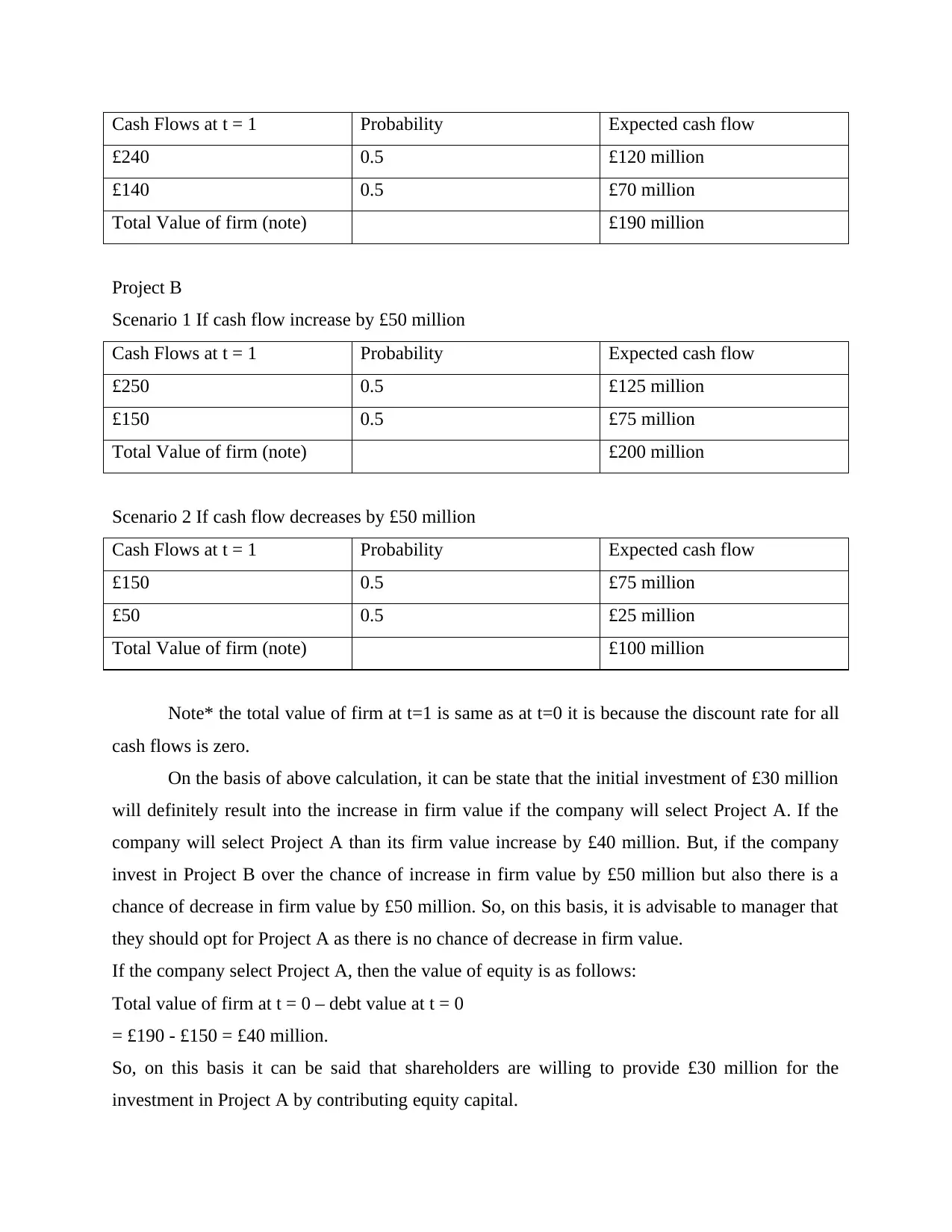

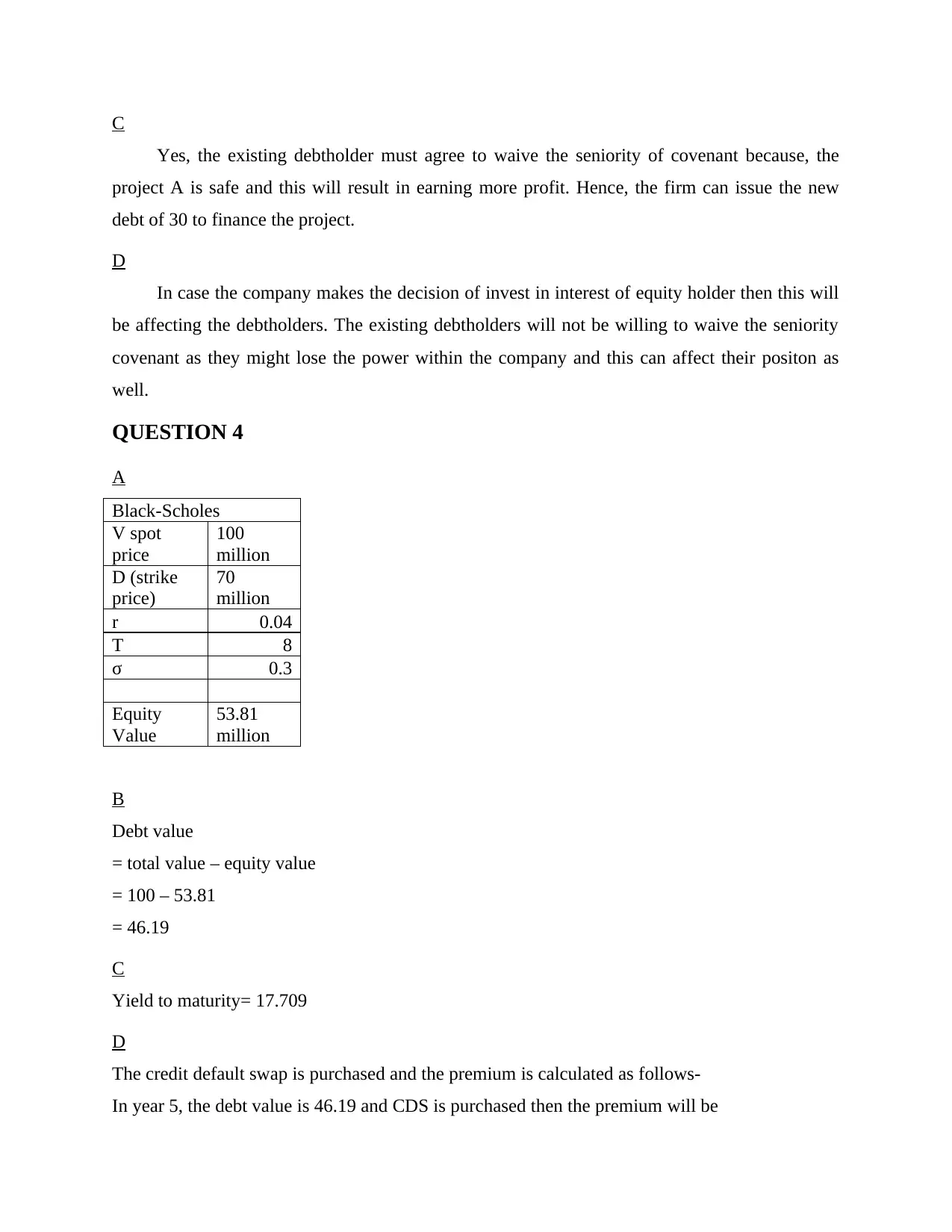

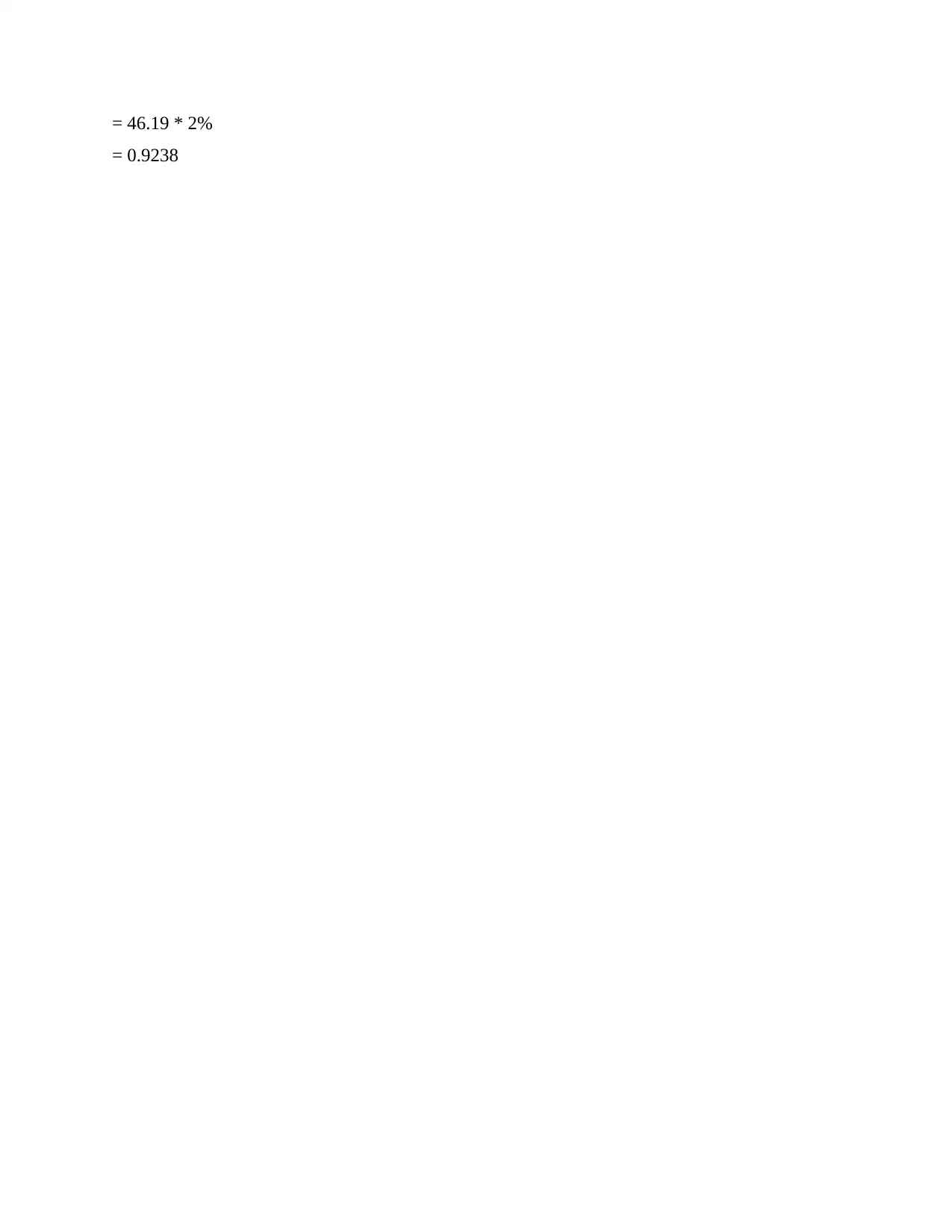

This document presents solutions to a Corporate Finance sample paper, covering topics such as Capital Asset Pricing Model (CAPM), Net Present Value (NPV), Black-Scholes model, and debt/equity valuation. The solutions include calculations for expected returns, portfolio standard deviation, firm valuation under different scenarios, and analysis of investment decisions. The paper also examines the impact of leverage, the implications of investment choices on debt and equity holders, and the calculation of credit default swap premiums. Project A is recommended based on NPV calculations.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.