Analysis of US Real GDP Determinants Using Regression Models

VerifiedAdded on 2023/05/30

|7

|1718

|55

Project

AI Summary

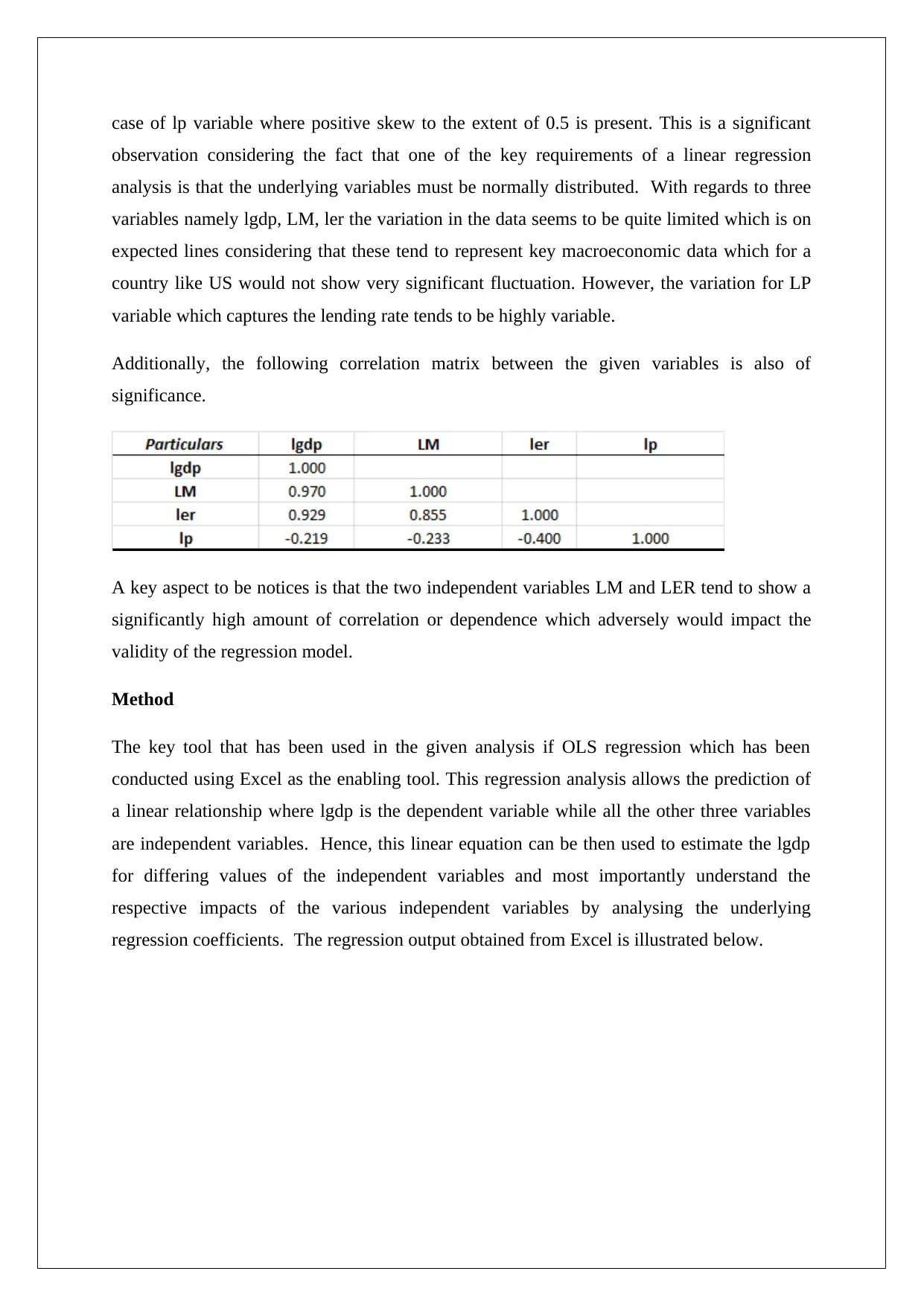

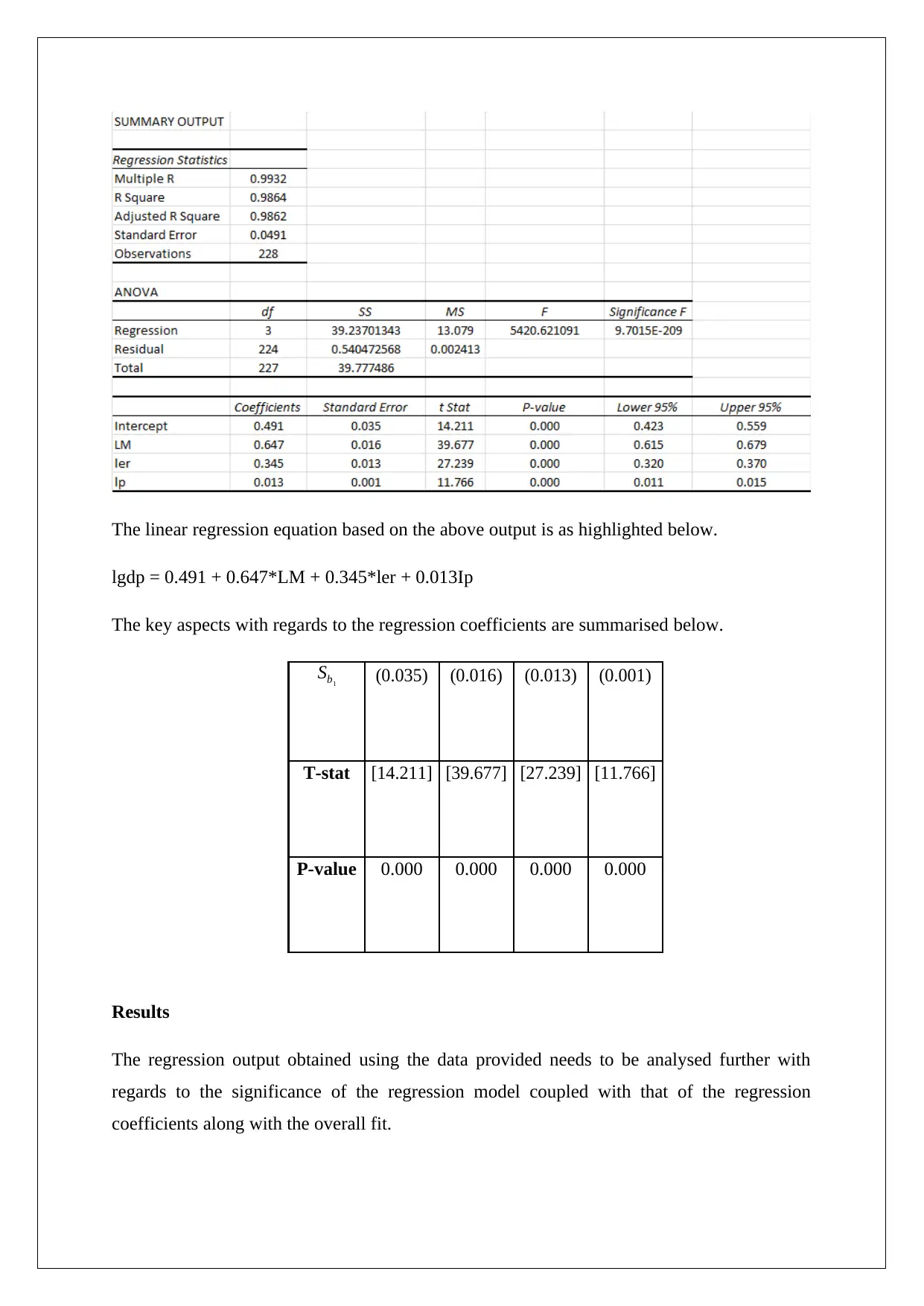

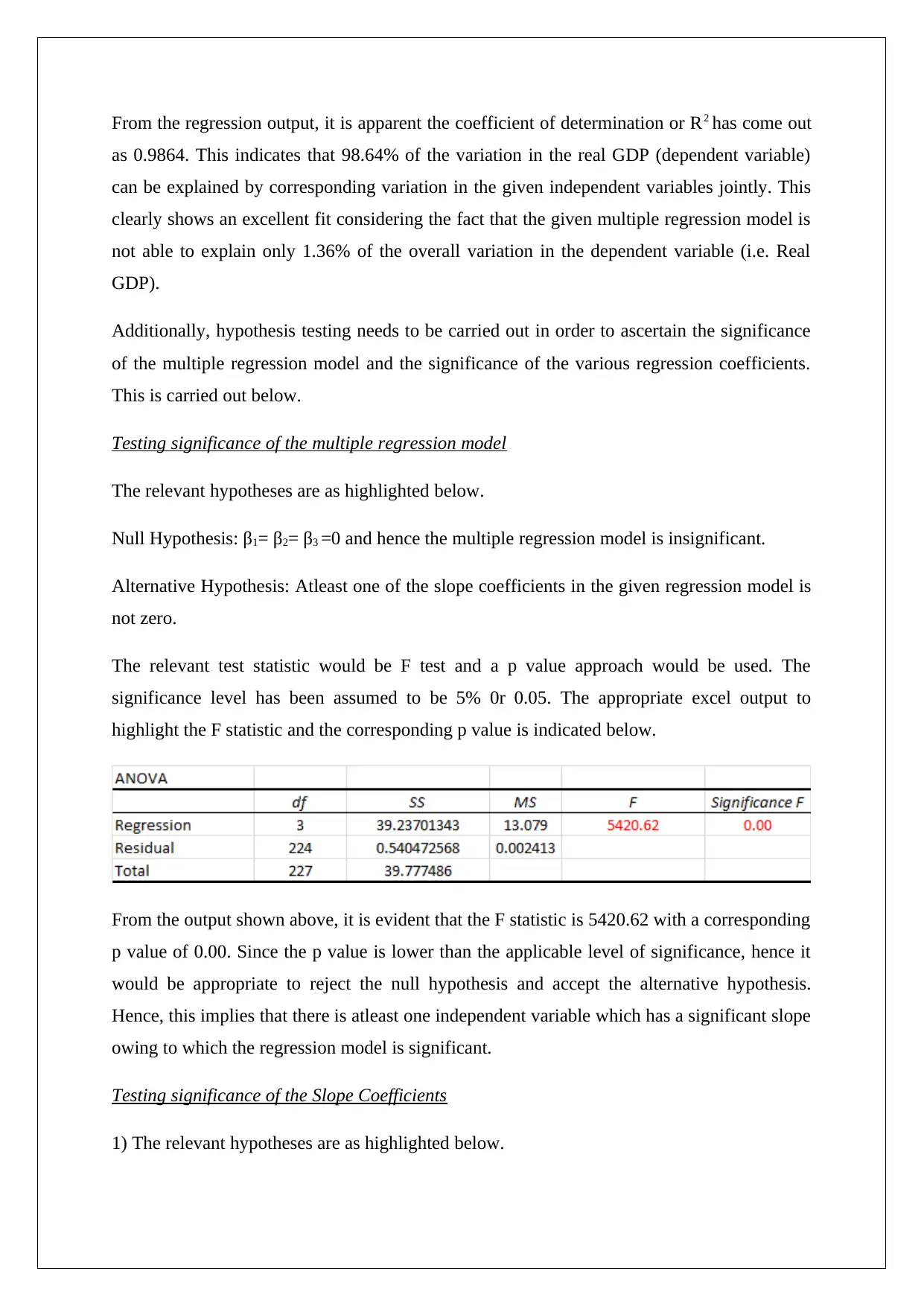

This project presents a multiple regression analysis to examine the relationship between US real GDP and three independent variables: lending rate, nominal effective exchange rate, and money supply. The analysis, conducted using Excel, reveals a significant and well-fitting model with a high coefficient of determination, indicating that nearly all variation in real GDP can be explained by the independent variables. All slope coefficients are statistically significant and positive, suggesting that higher values of these variables correlate with increased real GDP. However, the study acknowledges the high correlation between money supply and nominal effective exchange rate, which may impact the model's validity. The findings underscore the importance of considering these factors for sustainable economic recovery and stability, particularly for the Federal Reserve's decision-making. The project includes descriptive statistics, correlation analysis, and hypothesis testing to validate the model's significance and the significance of individual regression coefficients. The results suggest that the lending rate, money supply, and exchange rate are crucial determinants of real GDP, with implications for monetary policy and business decisions. This project is available on Desklib, a platform providing students with AI-based study tools, including past papers and solved assignments.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.