Finance Portfolio Management Report: Mutual Fund Evaluation

VerifiedAdded on 2022/10/17

|7

|1263

|14

Report

AI Summary

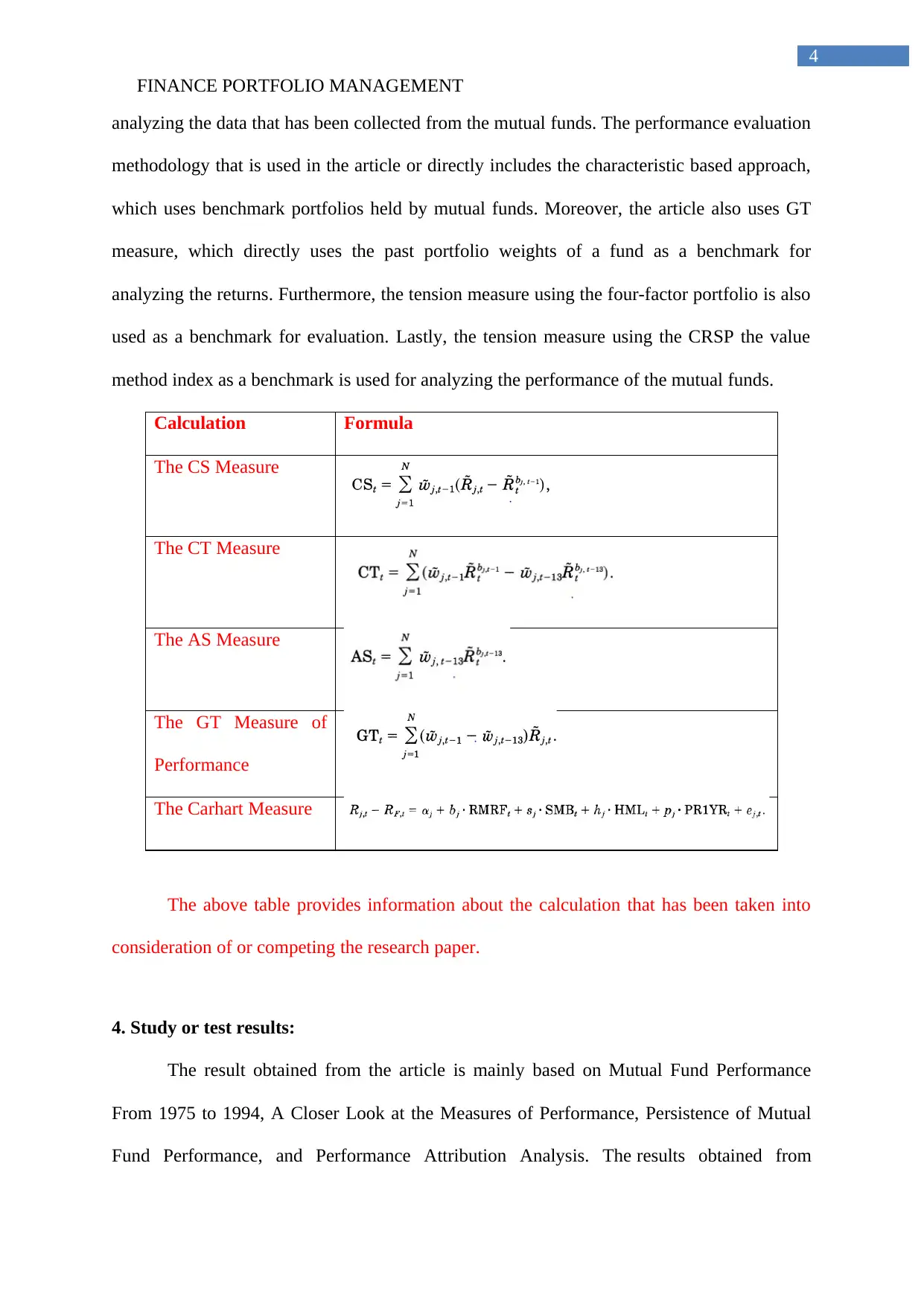

This report analyzes mutual fund performance by utilizing characteristic-based benchmarks, focusing on equity funds from 1975 to 1994. It evaluates the performance of portfolios based on stock characteristics, including market capitalization, book-to-market ratio, and prior-year returns. The research employs various methodologies, such as Characteristic-Based Performance Measures, CS Measure, CT Measure, AS Measure, GT Measure of Performance, and the Carhart Measure, to assess the return generation capabilities of mutual funds. The findings indicate that aggressive growth funds exhibit some selectivity ability, but there is no evidence of characteristic timing ability. The report also highlights the implications for investors in identifying and measuring mutual funds' performance to generate higher returns. The analysis suggests that while fund managers may change investment styles to increase returns, this can reduce the performance of mutual fund managers. The report concludes that the selective measures assigned for investment purposes have no significant abnormal performance and would not provide higher returns to the investors in the mechanical characteristic-based strategy.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.