MP212 Financial Accounting: Myer Holdings Ltd Impairment Report

VerifiedAdded on 2023/06/03

|10

|2263

|484

Report

AI Summary

This report assesses the necessity of asset impairment testing for Myer Holdings Ltd in accordance with AASB 136, prompted by an ASIC media release. It identifies internal and external factors indicating potential impairment, outlines the processes for determining necessary asset impairments, and specifies the information required for such determinations. The report also addresses management's flexibility in impairment decisions, emphasizing adherence to accounting standards for accurate financial reporting. It concludes that Myer Holdings Ltd has appropriately addressed asset impairment in its financial reporting, ensuring a transparent view for stakeholders. Desklib offers a range of solved assignments and past papers for students.

impairment test

Financial accounting

Impairment testing

Name of the author

University Name-

Financial accounting

Impairment testing

Name of the author

University Name-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

With the ramified business changes, every company needs to establish proper

harmonization in it international and domestic accounting frameworks. Nowadays, every

company is dealing with an issue of asset impairment that becomes a major issue for a company

when they want to keep the true and fair view of the recorded assets to its stakeholders. This

report focuses on the company named Myer Holding ltd which is a departmental structural

company worked as store chains.

With the ramified business changes, every company needs to establish proper

harmonization in it international and domestic accounting frameworks. Nowadays, every

company is dealing with an issue of asset impairment that becomes a major issue for a company

when they want to keep the true and fair view of the recorded assets to its stakeholders. This

report focuses on the company named Myer Holding ltd which is a departmental structural

company worked as store chains.

Table of Contents

EXECUTIVE SUMMARY.........................................................................................................................1

INTRODUCTION.......................................................................................................................................2

ANNOUNCEMENT OF ASIC REGARDING IMPAIRMENT.................................................................2

EVIDENCES THAT STATES THAT IMPAIRMENT TESTING OF ASSETS IS NECESSARY............3

THE PROCESS REQUIRED TO BE ADDRESSED IN DETERMINING ANY ASSET IMPAIRMENTS

THAT MIGHT BE NECESSARY..............................................................................................................5

INFORMATION REQUIRED TO DETERMINE THE IMPAIRMENT OF ASSETS...............................6

MANAGEMENT'S FLEXIBILITY WHEN IT COMES TO IMPAIRMENT DECISION.........................7

Conclusion...................................................................................................................................................7

References...................................................................................................................................................8

EXECUTIVE SUMMARY.........................................................................................................................1

INTRODUCTION.......................................................................................................................................2

ANNOUNCEMENT OF ASIC REGARDING IMPAIRMENT.................................................................2

EVIDENCES THAT STATES THAT IMPAIRMENT TESTING OF ASSETS IS NECESSARY............3

THE PROCESS REQUIRED TO BE ADDRESSED IN DETERMINING ANY ASSET IMPAIRMENTS

THAT MIGHT BE NECESSARY..............................................................................................................5

INFORMATION REQUIRED TO DETERMINE THE IMPAIRMENT OF ASSETS...............................6

MANAGEMENT'S FLEXIBILITY WHEN IT COMES TO IMPAIRMENT DECISION.........................7

Conclusion...................................................................................................................................................7

References...................................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Impairment of assets is a substantial accounting reconciliation as it is an important part of

a company to identify the true recoverable value of the assets and liabilities recorded in the

financial statement of company. According to AASB 136, Impairment of Assets, impairment

means falling down in the value of assets whether indefinite or irrevocable of fixed assets

including both tangible and non-tangible assets. It occurs due to the overvaluation of assets in the

books of accounts from its versatile value, that simply means if the assets are to be sold that may

recover less amount as compare to the amount shown in the books of accounts due to

overvaluation of assets. This report simply composed for a motive of an announcement through

the media that the ASIC (Australian Securities and Investment commissions) has to be done in

last of May 2018. This accouchement is shared with the media with an intention to pass the

information among all the companies that the financial statements off company would follow all

the rules and regulations given in AASB 136 to identify the true recoverable value of the assets

and liabilities recorded in the financial statement of company. The AASB 136 covers all the

accounting treatment of impairment of assets of financial assets and liabilities of Myer Holding

Ltd.

The announcement regarding the impairment of assets clearly declare that this would be

the important part of accounting treatment that a firm has to do, as testing of assets that should be

impairment mentioned in the financial report of company. The report declares the complete

information regarding the importance of the impairment of the assets for the transparent view

point of the assets.

ANNOUNCEMENT OF ASIC REGARDING IMPAIRMENT

According to the announcement done by ASIC the directors and the auditor are

responsible for the same terms regarding that, they are as follows:

The directors and auditor make sure that the company's speculation regarding the cash flow of

assets must be appropriate that shown in the books of accounts. All the directors needs to

evaluate their financial statements and recorded accounts as per AASB 136 so that they could

keep the business more transparent towards the stakeholders.

Impairment of assets is a substantial accounting reconciliation as it is an important part of

a company to identify the true recoverable value of the assets and liabilities recorded in the

financial statement of company. According to AASB 136, Impairment of Assets, impairment

means falling down in the value of assets whether indefinite or irrevocable of fixed assets

including both tangible and non-tangible assets. It occurs due to the overvaluation of assets in the

books of accounts from its versatile value, that simply means if the assets are to be sold that may

recover less amount as compare to the amount shown in the books of accounts due to

overvaluation of assets. This report simply composed for a motive of an announcement through

the media that the ASIC (Australian Securities and Investment commissions) has to be done in

last of May 2018. This accouchement is shared with the media with an intention to pass the

information among all the companies that the financial statements off company would follow all

the rules and regulations given in AASB 136 to identify the true recoverable value of the assets

and liabilities recorded in the financial statement of company. The AASB 136 covers all the

accounting treatment of impairment of assets of financial assets and liabilities of Myer Holding

Ltd.

The announcement regarding the impairment of assets clearly declare that this would be

the important part of accounting treatment that a firm has to do, as testing of assets that should be

impairment mentioned in the financial report of company. The report declares the complete

information regarding the importance of the impairment of the assets for the transparent view

point of the assets.

ANNOUNCEMENT OF ASIC REGARDING IMPAIRMENT

According to the announcement done by ASIC the directors and the auditor are

responsible for the same terms regarding that, they are as follows:

The directors and auditor make sure that the company's speculation regarding the cash flow of

assets must be appropriate that shown in the books of accounts. All the directors needs to

evaluate their financial statements and recorded accounts as per AASB 136 so that they could

keep the business more transparent towards the stakeholders.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The difference between the actual value and the value that shown in the books are evaluated

adequately and in a proper manner by considering adequate cash flows regarding the assets of

company.

For doing the evaluation of impairment of assets in Myer Holding Company no speculative data

of cash flow considered, only adequate and actual cash flow is considered while evaluating the

impairment of assets.

The test of impairment of assets of Myer Holding Company contains the reassessed value of

assets and liabilities that might be influenced by the internal and external forces that leads to the

adverse or different result of testing.

The risk included in the assets and the places where it deemed to be occurring must decide

before deciding the discount rates on risks of Myer Holding Company. The discounted rates are

related with the different activities allied with different profit producing activities under different

type of risks included.

The cost of issuance must be adequate and affordable in nature regarding to the assets.

The actual value of assets and liabilities that has to be mentioned in the accounting books must

be resolute. The process of costing must be ratified through cost drivers1.

EVIDENCES THAT STATES THAT IMPAIRMENT TESTING OF ASSETS IS

NECESSARY

Evidences of testing of impairment of Myer Holding Company refers to the situation

where the company are supposed to be think about the testing of impairment of assets considered

in the books of accounts in consequential manner. The evidence may be based on external or

internal aspects that lead to the impairment of assets. The evidence that considered is as follows:

INTERNAL EVIDENCES

It includes any substantial harm that perceive in the Myer Holding Company recently.

All the assets of Myer Holding Company are not operated according to the performance set for

them.

1 Kabir, Humayun, and Asheq Rahman. "The role of corporate governance in accounting discretion under

IFRS: Goodwill impairment in Australia." Journal of Contemporary Accounting & Economics 12.3 (2016):

290-308.

adequately and in a proper manner by considering adequate cash flows regarding the assets of

company.

For doing the evaluation of impairment of assets in Myer Holding Company no speculative data

of cash flow considered, only adequate and actual cash flow is considered while evaluating the

impairment of assets.

The test of impairment of assets of Myer Holding Company contains the reassessed value of

assets and liabilities that might be influenced by the internal and external forces that leads to the

adverse or different result of testing.

The risk included in the assets and the places where it deemed to be occurring must decide

before deciding the discount rates on risks of Myer Holding Company. The discounted rates are

related with the different activities allied with different profit producing activities under different

type of risks included.

The cost of issuance must be adequate and affordable in nature regarding to the assets.

The actual value of assets and liabilities that has to be mentioned in the accounting books must

be resolute. The process of costing must be ratified through cost drivers1.

EVIDENCES THAT STATES THAT IMPAIRMENT TESTING OF ASSETS IS

NECESSARY

Evidences of testing of impairment of Myer Holding Company refers to the situation

where the company are supposed to be think about the testing of impairment of assets considered

in the books of accounts in consequential manner. The evidence may be based on external or

internal aspects that lead to the impairment of assets. The evidence that considered is as follows:

INTERNAL EVIDENCES

It includes any substantial harm that perceive in the Myer Holding Company recently.

All the assets of Myer Holding Company are not operated according to the performance set for

them.

1 Kabir, Humayun, and Asheq Rahman. "The role of corporate governance in accounting discretion under

IFRS: Goodwill impairment in Australia." Journal of Contemporary Accounting & Economics 12.3 (2016):

290-308.

The operating cost of company increases unexpectedly at an uncertain level of the firm.

Assets of Myer Holding Company are to be superannuated according to the requirement of the

firm as per the plans set previously. In the annual report, these ideas are to be considered for the

business2.

The performance of Myer Holding Company is not up to mark that is estimated and making

unexpected increase in the cost.

EXTERNAL EVIDENCES

There are some of the external factors of Myer Holding Company which might evidence the

impairment testing need.

The unexpected increment in the interest rates in the market affect the discount rates which make

an adverse fall in the value of the assets that are to be used in the firm.

New technology, procedures, rules or economy introduced in the market that leads to the new

expansion in the assets that already in use of the firm3.

It includes for putting the carry forward value of assets on the excessive side in the balance sheet

over the market capitalization value of Myer Holding Ltd.

2 André, Paul, Dionysia Dionysiou, and Ioannis Tsalavoutas. ‘Mandated disclosures under IAS 36

Impairment of Assets and IAS 38 Intangible Assets: value relevance and impact on analysts’

forecasts50(7) (2018).’ Applied Economics : 707-725.

3 Bepari, Md Khokan, Sheikh F. Rahman, and Abu Taher Mollik. ‘Firms' compliance with the disclosure

requirements of IFRS for goodwill impairment testing: Effect of the global financial crisis and other firm

characteristics. 10(1) (2014)’ Journal of Accounting and Organizational Change ): 116-149.

Assets of Myer Holding Company are to be superannuated according to the requirement of the

firm as per the plans set previously. In the annual report, these ideas are to be considered for the

business2.

The performance of Myer Holding Company is not up to mark that is estimated and making

unexpected increase in the cost.

EXTERNAL EVIDENCES

There are some of the external factors of Myer Holding Company which might evidence the

impairment testing need.

The unexpected increment in the interest rates in the market affect the discount rates which make

an adverse fall in the value of the assets that are to be used in the firm.

New technology, procedures, rules or economy introduced in the market that leads to the new

expansion in the assets that already in use of the firm3.

It includes for putting the carry forward value of assets on the excessive side in the balance sheet

over the market capitalization value of Myer Holding Ltd.

2 André, Paul, Dionysia Dionysiou, and Ioannis Tsalavoutas. ‘Mandated disclosures under IAS 36

Impairment of Assets and IAS 38 Intangible Assets: value relevance and impact on analysts’

forecasts50(7) (2018).’ Applied Economics : 707-725.

3 Bepari, Md Khokan, Sheikh F. Rahman, and Abu Taher Mollik. ‘Firms' compliance with the disclosure

requirements of IFRS for goodwill impairment testing: Effect of the global financial crisis and other firm

characteristics. 10(1) (2014)’ Journal of Accounting and Organizational Change ): 116-149.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

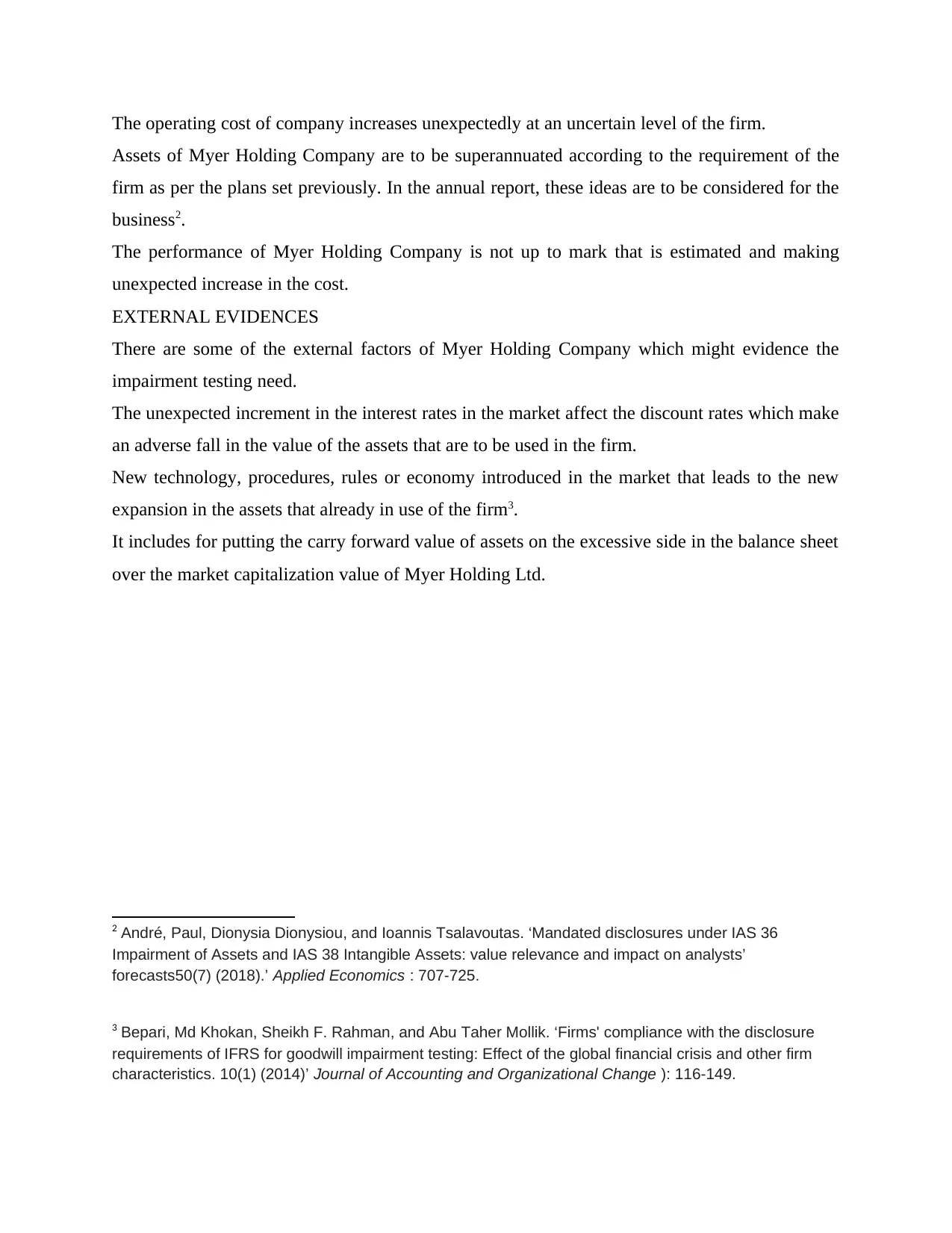

THE PROCESS REQUIRED TO BE ADDRESSED IN DETERMINING ANY ASSET

IMPAIRMENTS THAT MIGHT BE NECESSARY

Due to rapid changes, decreasing in the valuation of assets, impairment testing helps the

company to find out or evaluating the actual value of assets that are to be mentioned in the books

of accounts of a company. Determining the evidences is not only the way to cure the problem,

the company may determine by certain processes whether the impairment test is to be done or

not. The following steps are to be included to find out whether the impairment test is necessary

or not4:

In the first step, we should check the evidences as they are as much compatible and

strong enough that on the basis of them the impairment tests of assets are to be done related to

the cash flow of assets.

The second step consist that the company may evaluate various required elements related to this,

that considered the impulsive value of tangible and non-tangible assets are doing the comparison

between the value of using at present and future after sale value.

4 Biancone, Paolo Pietro. ’ Italian Experience on Impairment Test of Goodwill’ International

2(1) (2014). Journal of Advances in Management Science , 162-176.

IMPAIRMENTS THAT MIGHT BE NECESSARY

Due to rapid changes, decreasing in the valuation of assets, impairment testing helps the

company to find out or evaluating the actual value of assets that are to be mentioned in the books

of accounts of a company. Determining the evidences is not only the way to cure the problem,

the company may determine by certain processes whether the impairment test is to be done or

not. The following steps are to be included to find out whether the impairment test is necessary

or not4:

In the first step, we should check the evidences as they are as much compatible and

strong enough that on the basis of them the impairment tests of assets are to be done related to

the cash flow of assets.

The second step consist that the company may evaluate various required elements related to this,

that considered the impulsive value of tangible and non-tangible assets are doing the comparison

between the value of using at present and future after sale value.

4 Biancone, Paolo Pietro. ’ Italian Experience on Impairment Test of Goodwill’ International

2(1) (2014). Journal of Advances in Management Science , 162-176.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The third step, considered whether the valued amount of assets that shown in the books of

accounts is less than the impulsive amount of assets that should be determined before.

After determining, whether the assets are to be impaired or not, the company needs to maintain a

separate account of losses in profit and loss account that occur during the impairment of assets5.

INFORMATION REQUIRED TO DETERMINE THE IMPAIRMENT OF ASSETS

The following information is to be determined in the impairment of assets:

Myer holding's evidences declared that there is the requirement of impairment of assets in their

company.

The real impulsive value of assets shows the market situations.

Real value and the value that use in books of accounts is required for determine the actual

impulsive value of the assets.

The impairment of assets is to be compared with the previous impairment, and the valuation of

impairment should be analyzed.

5 Bond, David, Brett Govendir, and Peter Wells. . ‘An evaluation of asset impairments by Australian firms

and whether they were impacted by AASB 136.’ 56.1 (2016): Accounting & Finance 259-288

accounts is less than the impulsive amount of assets that should be determined before.

After determining, whether the assets are to be impaired or not, the company needs to maintain a

separate account of losses in profit and loss account that occur during the impairment of assets5.

INFORMATION REQUIRED TO DETERMINE THE IMPAIRMENT OF ASSETS

The following information is to be determined in the impairment of assets:

Myer holding's evidences declared that there is the requirement of impairment of assets in their

company.

The real impulsive value of assets shows the market situations.

Real value and the value that use in books of accounts is required for determine the actual

impulsive value of the assets.

The impairment of assets is to be compared with the previous impairment, and the valuation of

impairment should be analyzed.

5 Bond, David, Brett Govendir, and Peter Wells. . ‘An evaluation of asset impairments by Australian firms

and whether they were impacted by AASB 136.’ 56.1 (2016): Accounting & Finance 259-288

It also considered that the clients of the company are having updated knowledge regarding the

records of assets and liabilities6.

MANAGEMENT'S FLEXIBILITY WHEN IT COMES TO IMPAIRMENT DECISION

The management has the right to gather information from any source or any aspects that

is to be needed in the impairment of assets. Wherever, the evidenced collected by the

administration regarding the impairment of assets must determine whether the impairment is

necessary or not, if there is no requirement then the administration have no right to take a

decision regarding this. Only the firm will do impairment of assets if it is needed to be done. The

administration cannot back step of doing impairment of assets when it is necessary under the rule

AASB 36, Impairment of assets. This will allow the firm to maintain the records of assets and

liabilities that may help the shareholders for taking the further decisions. But, if the management

is in profit then the impulsive amount is calculated by using market value rather than using real

value and all this is manipulated and make approachable afterwards.

Conclusion

Hence, if the assets of the organization needs to impaired then there is no other option

that will resolve this situation rather than impairment of assets. After evaluating the annual report

of company, it is inferred that all the accounting treatment regarding the impairment of assets is

done by Myer Holding. As per the accounting rules issued by the Australian Securities and

Investment Commissions (ASIC), Myer has prepared an attentive and subjective report of

financial information to identify the true recoverable value of the assets and liabilities recorded

in the financial statement of company.

6 Wen C, Pervin K. Shroff, and Ivy Z. ‘Fair value accounting: Consequences of booking market-driven

goodwill impairment 25(1) (2017) International Journal of Accounting & Information Management : 44-79.

records of assets and liabilities6.

MANAGEMENT'S FLEXIBILITY WHEN IT COMES TO IMPAIRMENT DECISION

The management has the right to gather information from any source or any aspects that

is to be needed in the impairment of assets. Wherever, the evidenced collected by the

administration regarding the impairment of assets must determine whether the impairment is

necessary or not, if there is no requirement then the administration have no right to take a

decision regarding this. Only the firm will do impairment of assets if it is needed to be done. The

administration cannot back step of doing impairment of assets when it is necessary under the rule

AASB 36, Impairment of assets. This will allow the firm to maintain the records of assets and

liabilities that may help the shareholders for taking the further decisions. But, if the management

is in profit then the impulsive amount is calculated by using market value rather than using real

value and all this is manipulated and make approachable afterwards.

Conclusion

Hence, if the assets of the organization needs to impaired then there is no other option

that will resolve this situation rather than impairment of assets. After evaluating the annual report

of company, it is inferred that all the accounting treatment regarding the impairment of assets is

done by Myer Holding. As per the accounting rules issued by the Australian Securities and

Investment Commissions (ASIC), Myer has prepared an attentive and subjective report of

financial information to identify the true recoverable value of the assets and liabilities recorded

in the financial statement of company.

6 Wen C, Pervin K. Shroff, and Ivy Z. ‘Fair value accounting: Consequences of booking market-driven

goodwill impairment 25(1) (2017) International Journal of Accounting & Information Management : 44-79.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Bepari, Md Khokan, and Abu Taher Mollik. "Regime change in the accounting for goodwill:

goodwill write-offs and the value relevance of older goodwill." International Journal of

Accounting & Information Management 25(1) (2017): 43-69.

Chen, Wen, Pervin K. Shroff, and Ivy Zhang. Fair value accounting: Consequences of booking

market-driven goodwill impairment 25(1) (2017) International Journal of Accounting &

Information Management : 44-79

David , Bond, , Brett G., and Peter W. ‘An evaluation of asset impairments by Australian firms

and whether they were impacted by AASB 136.’ 56.1 (2016): Accounting & Finance 259-288.

Humayun K , and Asheq R. ‘The role of corporate governance in accounting discretion under

IFRS: Goodwill impairment in Australia.’ 12(3) (2016): Journal of Contemporary Accounting &

Economics 290-308.

Md Khokan B, , Sheikh F. Rahman, and Abu, T M. ‘Firms' compliance with the disclosure

requirements of IFRS for goodwill impairment testing: Effect of the global financial crisis and

other firm characteristics. 10(1) (2014)’ Journal of Accounting and Organizational Change ):

116-149.

Paolo P, B,. "IFRS:’ Italian Experience on Impairment Test of Goodwill’ International 2(1)

(2014). Journal of Advances in Management Science , 162-176.

Paul A, Dionysia D, and Ioannis T. ‘Mandated disclosures under IAS 36 Impairment of Assets

and IAS 38 Intangible Assets: value relevance and impact on analysts’ forecasts50(7)

(2018).’ Applied Economics : 707-725.

Bepari, Md Khokan, and Abu Taher Mollik. "Regime change in the accounting for goodwill:

goodwill write-offs and the value relevance of older goodwill." International Journal of

Accounting & Information Management 25(1) (2017): 43-69.

Chen, Wen, Pervin K. Shroff, and Ivy Zhang. Fair value accounting: Consequences of booking

market-driven goodwill impairment 25(1) (2017) International Journal of Accounting &

Information Management : 44-79

David , Bond, , Brett G., and Peter W. ‘An evaluation of asset impairments by Australian firms

and whether they were impacted by AASB 136.’ 56.1 (2016): Accounting & Finance 259-288.

Humayun K , and Asheq R. ‘The role of corporate governance in accounting discretion under

IFRS: Goodwill impairment in Australia.’ 12(3) (2016): Journal of Contemporary Accounting &

Economics 290-308.

Md Khokan B, , Sheikh F. Rahman, and Abu, T M. ‘Firms' compliance with the disclosure

requirements of IFRS for goodwill impairment testing: Effect of the global financial crisis and

other firm characteristics. 10(1) (2014)’ Journal of Accounting and Organizational Change ):

116-149.

Paolo P, B,. "IFRS:’ Italian Experience on Impairment Test of Goodwill’ International 2(1)

(2014). Journal of Advances in Management Science , 162-176.

Paul A, Dionysia D, and Ioannis T. ‘Mandated disclosures under IAS 36 Impairment of Assets

and IAS 38 Intangible Assets: value relevance and impact on analysts’ forecasts50(7)

(2018).’ Applied Economics : 707-725.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.