Detailed Analysis of MYOB's Financial Performance: Cash Flow, OCI, Tax

VerifiedAdded on 2024/06/03

|9

|2320

|371

Report

AI Summary

This report provides a detailed financial analysis of MYOB, a software solutions company, focusing on its cash flow statement, other comprehensive income (OCI), and corporate income tax for the period 2015-2017. The cash flow analysis examines operating, investing, and financing activities, highlighting the company's increasing cash flow from operations and significant investments in new product development and company acquisitions. The OCI analysis identifies foreign currency translation reserves as the primary item. The corporate income tax analysis reconciles the calculated tax based on net income with the actual tax paid, accounting for variations due to items excluded in tax computations. The report uses data from MYOB's annual reports to provide a comprehensive overview of the company's financial performance.

Table of Contents

Introduction.................................................................................................................................................2

Critical analysis of Cash flow statement......................................................................................................2

Critical analysis of OCI...............................................................................................................................5

Computation of Corporate Income tax........................................................................................................6

References...................................................................................................................................................9

Introduction.................................................................................................................................................2

Critical analysis of Cash flow statement......................................................................................................2

Critical analysis of OCI...............................................................................................................................5

Computation of Corporate Income tax........................................................................................................6

References...................................................................................................................................................9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

The main purpose of the assignment is to analyse in detail the annual report of a company and

provide comparative analysis on the cash flow statement for the 3 year period from 2015 to

2017. The student then analyse the other comprehensive income aspect of the company, the

various particulars included in the OCI of the annual report and last part is to perform a detailed

analysis on the corporate income tax paid by the company. The organisation which is considered

for the analysis is MYOB, a primary software solutions company which is involved in offering

software solutions to the small and medium sized enterprises on the various area which includes

taxation, accounting system, payroll maintenance etc. The company main clients are the small

and medium sized enterprises which are located in Australia, New Zealand and other Asian

countries. The company offers solutions to its clients through cloud computing and other

software soutions like MYOB Advanaced module, Payroll MYOB, Direct Pay, the company also

offers various other services like taxation filing, payroll management of the employees, GST

computation, record management system of key financial and non-financial information.

Critical analysis of Cash flow statement

.

The cash flow statement shall be considered as a complete account of changes in the accounts

and balance sheet. Attention is primarily focused on money in these sectors. The cash flow

statement can be classified into categories such as cash flow from operations, cash flow from

investing activities, cash flow from financial operations and cash flow operations. train. The

main purpose of the cash flow statement is to provide more information and information on total

revenues and payments over a certain period of time, usually one year. This statement helps the

company understand the company's total liquidity, assesses the solvency from time to time,

predicts future cash flows and seeks resources. The most important components of the cash flow

statement are mainly based on the accounting capabilities that the company has to determine

when comparing revenues and costs. It should be noted that the cash flow statement contains

only the funds and funds that were released. These statements generally exclude a transaction

that does not include money

From the critical analysis of cash flow statement of MYOB it is noted that the cash flow from the

beginning of the period were 61,434,000 in 2017 but in the year 2016 it stood at 36,384,000 and

5,044,000 in 2015. This shows that the cash flow of the business is consistently increasing over

the period of time.

Analysis of cash flow based on the operating activities:

The main purpose of the assignment is to analyse in detail the annual report of a company and

provide comparative analysis on the cash flow statement for the 3 year period from 2015 to

2017. The student then analyse the other comprehensive income aspect of the company, the

various particulars included in the OCI of the annual report and last part is to perform a detailed

analysis on the corporate income tax paid by the company. The organisation which is considered

for the analysis is MYOB, a primary software solutions company which is involved in offering

software solutions to the small and medium sized enterprises on the various area which includes

taxation, accounting system, payroll maintenance etc. The company main clients are the small

and medium sized enterprises which are located in Australia, New Zealand and other Asian

countries. The company offers solutions to its clients through cloud computing and other

software soutions like MYOB Advanaced module, Payroll MYOB, Direct Pay, the company also

offers various other services like taxation filing, payroll management of the employees, GST

computation, record management system of key financial and non-financial information.

Critical analysis of Cash flow statement

.

The cash flow statement shall be considered as a complete account of changes in the accounts

and balance sheet. Attention is primarily focused on money in these sectors. The cash flow

statement can be classified into categories such as cash flow from operations, cash flow from

investing activities, cash flow from financial operations and cash flow operations. train. The

main purpose of the cash flow statement is to provide more information and information on total

revenues and payments over a certain period of time, usually one year. This statement helps the

company understand the company's total liquidity, assesses the solvency from time to time,

predicts future cash flows and seeks resources. The most important components of the cash flow

statement are mainly based on the accounting capabilities that the company has to determine

when comparing revenues and costs. It should be noted that the cash flow statement contains

only the funds and funds that were released. These statements generally exclude a transaction

that does not include money

From the critical analysis of cash flow statement of MYOB it is noted that the cash flow from the

beginning of the period were 61,434,000 in 2017 but in the year 2016 it stood at 36,384,000 and

5,044,000 in 2015. This shows that the cash flow of the business is consistently increasing over

the period of time.

Analysis of cash flow based on the operating activities:

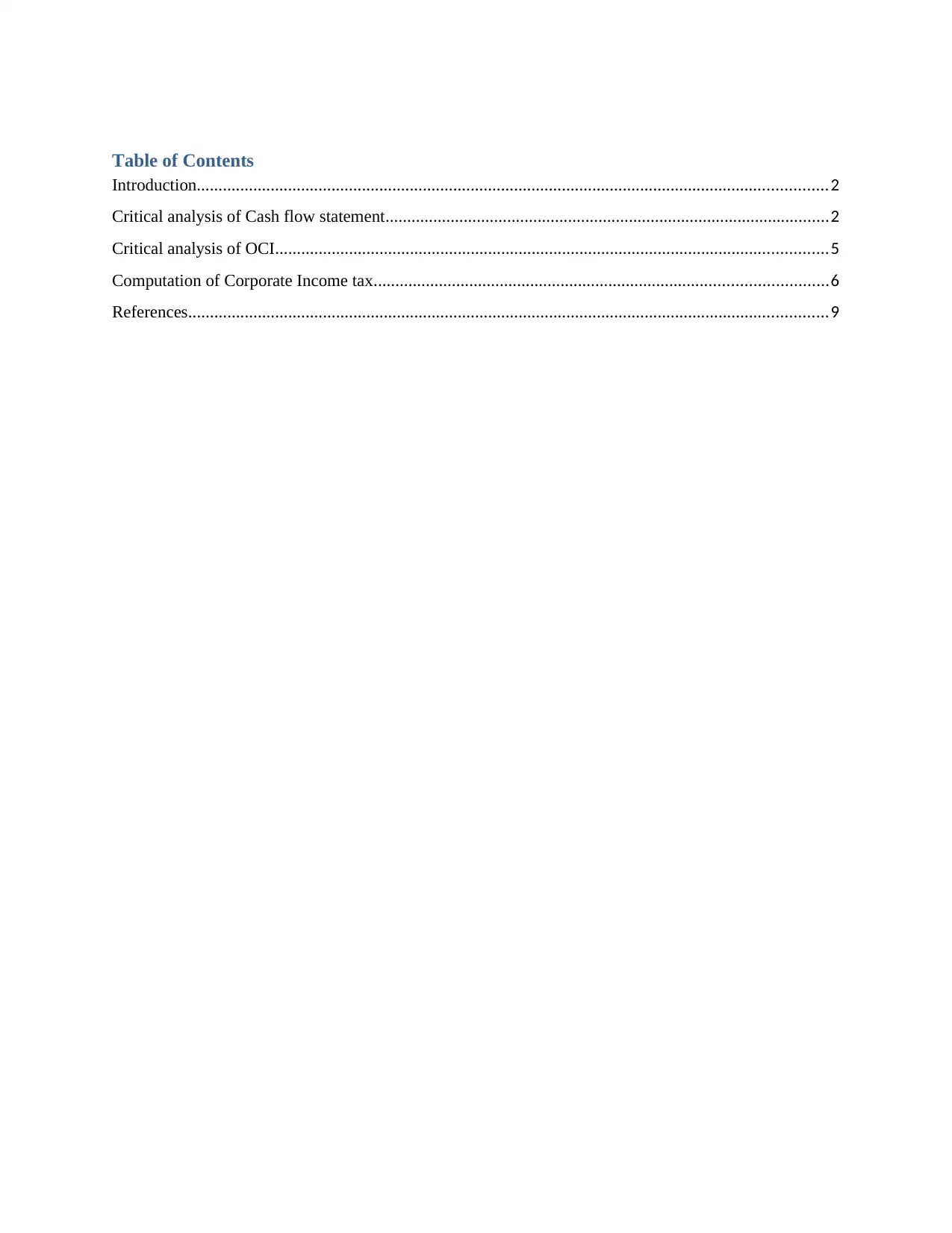

From the annual report of the company it is noted that the net cash flow based on the operating

process was 97,860,000 in 2015 whereas it was 145,833,000 in 2016 and it has grown to

163,919,000 in 2017. This shows that the business has grown to a larger extent in the past three

years.

The cash receipts of the company were at 362,211,000 in 2015, but this has significantly

increased to 406,711,000 in 2016 and 414,224,000 in 2017. Similarly the payments to the

suppliers and others has been made to a level of 213,879,000 in 2015, and this has increased to

246,153,000 in 2016 but due to continuous effort of the management the expenses has been

reduced to 233,781,000 in 2017. The net cash flow from the operating activities were at

97,860,000 in 2015, increased significantly in 2016 and stood at 145,833,000 in 2016 and

increased even further to 163,919,000 in 2017.

2015 2016 2017

Net cash from operating

activities

97,86

0

145,83

3

163,91

9

2015 2016 2017

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

Net cash from operating activities

Net cash from operating

activities

Analysis of investment activities of MYOB: This section is mainly involved in understanding the

various investment activities which has been carried out by the company during the period 2015

to 2017, The company made a major investment in creating new product development in 2015

for this purpose 13,822,000 has been invested in 2015, whereas in 2016 the new product

development was capitalised to a level of 26,879,000 in 2016 nd this has increased to 35,288,000

process was 97,860,000 in 2015 whereas it was 145,833,000 in 2016 and it has grown to

163,919,000 in 2017. This shows that the business has grown to a larger extent in the past three

years.

The cash receipts of the company were at 362,211,000 in 2015, but this has significantly

increased to 406,711,000 in 2016 and 414,224,000 in 2017. Similarly the payments to the

suppliers and others has been made to a level of 213,879,000 in 2015, and this has increased to

246,153,000 in 2016 but due to continuous effort of the management the expenses has been

reduced to 233,781,000 in 2017. The net cash flow from the operating activities were at

97,860,000 in 2015, increased significantly in 2016 and stood at 145,833,000 in 2016 and

increased even further to 163,919,000 in 2017.

2015 2016 2017

Net cash from operating

activities

97,86

0

145,83

3

163,91

9

2015 2016 2017

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

Net cash from operating activities

Net cash from operating

activities

Analysis of investment activities of MYOB: This section is mainly involved in understanding the

various investment activities which has been carried out by the company during the period 2015

to 2017, The company made a major investment in creating new product development in 2015

for this purpose 13,822,000 has been invested in 2015, whereas in 2016 the new product

development was capitalised to a level of 26,879,000 in 2016 nd this has increased to 35,288,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

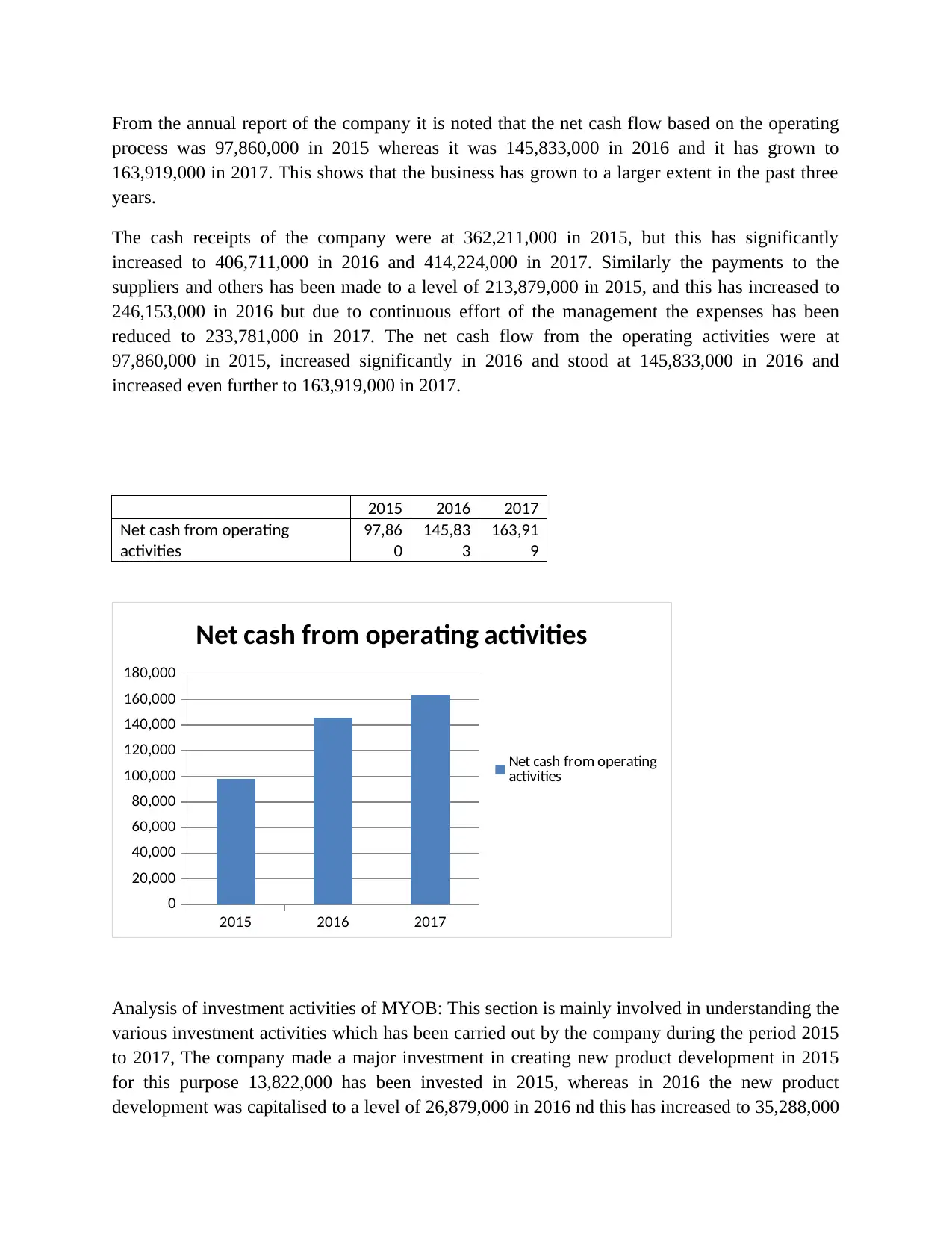

in 2017. Furthermore the company paid 13,160,000 in 2015 for the purchase of new company,

whereas in 2016 the purchase of new companies was 22,820,000 and in 2017 the value of

investment was at 47,545,000 in 2017.

The overall investment made by the company in the year 2015 was 54,605,000, whereas in the

year 2016 it was around 59,031,000 but in 2017 the investment has increased significantly and

was around 101,680,000.

2015 2016 2017

Net cash in investment activities

54,60

5

59,03

1

101,68

0

2015 2016 2017

0

20,000

40,000

60,000

80,000

100,000

120,000

Net cash in investment activities

Net cash in investment

activities

Analysis of financing sources of the company: Based on the annual reports of the company, it is

identified that the company raised the capital through the issue of shares at 828,062,000 in 2015,

whereas the proceeds generated through the treasury shares were at 3,456,000 in 2017. The

company made a repayment of borrowing 1,048,176,000 in 2015, however the repayment of

financial liabilities were 410,000 in 2017. The overall financing aspects of the company were at -

11,878,000 in 2015, whereas it reduced to -62,453,000 in 2016 and -69,525,000 in 2017.

2015 2016 2017

Net cash in financing activities

11,87

8

62,54

3

69,52

5

whereas in 2016 the purchase of new companies was 22,820,000 and in 2017 the value of

investment was at 47,545,000 in 2017.

The overall investment made by the company in the year 2015 was 54,605,000, whereas in the

year 2016 it was around 59,031,000 but in 2017 the investment has increased significantly and

was around 101,680,000.

2015 2016 2017

Net cash in investment activities

54,60

5

59,03

1

101,68

0

2015 2016 2017

0

20,000

40,000

60,000

80,000

100,000

120,000

Net cash in investment activities

Net cash in investment

activities

Analysis of financing sources of the company: Based on the annual reports of the company, it is

identified that the company raised the capital through the issue of shares at 828,062,000 in 2015,

whereas the proceeds generated through the treasury shares were at 3,456,000 in 2017. The

company made a repayment of borrowing 1,048,176,000 in 2015, however the repayment of

financial liabilities were 410,000 in 2017. The overall financing aspects of the company were at -

11,878,000 in 2015, whereas it reduced to -62,453,000 in 2016 and -69,525,000 in 2017.

2015 2016 2017

Net cash in financing activities

11,87

8

62,54

3

69,52

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2015 2016 2017

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Net cash in financing activities

Net cash in financing

activities

A comparative analysis was made for a period of 2015 to 2017, the following table shows the

various aspects pertaining to the cash flow of the business.

2015 2016 2017

Net cash from operating

activities

97,86

0

145,83

3

163,91

9

Net cash in investment

activities

54,60

5 59,031

101,68

0

Net cash in financing activities

11,87

8 62,543 69,525

Net cash flow

36,38

4 61,434 54,779

Net cash from

operating

activities

Net cash in

investment

activities

Net cash in

financing

activities

Net cash flow

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

2015

2016

2017

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Net cash in financing activities

Net cash in financing

activities

A comparative analysis was made for a period of 2015 to 2017, the following table shows the

various aspects pertaining to the cash flow of the business.

2015 2016 2017

Net cash from operating

activities

97,86

0

145,83

3

163,91

9

Net cash in investment

activities

54,60

5 59,031

101,68

0

Net cash in financing activities

11,87

8 62,543 69,525

Net cash flow

36,38

4 61,434 54,779

Net cash from

operating

activities

Net cash in

investment

activities

Net cash in

financing

activities

Net cash flow

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

2015

2016

2017

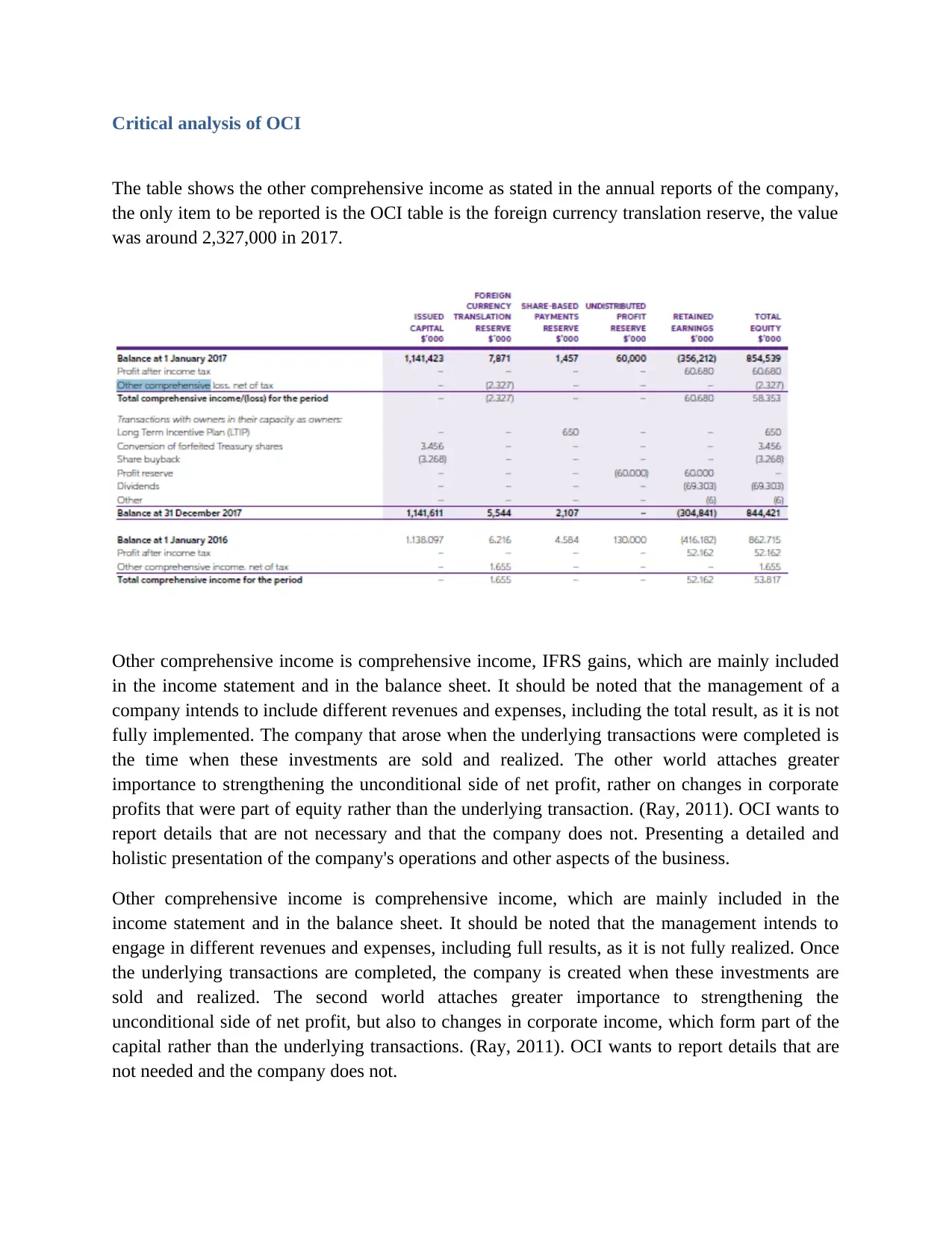

Critical analysis of OCI

The table shows the other comprehensive income as stated in the annual reports of the company,

the only item to be reported is the OCI table is the foreign currency translation reserve, the value

was around 2,327,000 in 2017.

Other comprehensive income is comprehensive income, IFRS gains, which are mainly included

in the income statement and in the balance sheet. It should be noted that the management of a

company intends to include different revenues and expenses, including the total result, as it is not

fully implemented. The company that arose when the underlying transactions were completed is

the time when these investments are sold and realized. The other world attaches greater

importance to strengthening the unconditional side of net profit, rather on changes in corporate

profits that were part of equity rather than the underlying transaction. (Ray, 2011). OCI wants to

report details that are not necessary and that the company does not. Presenting a detailed and

holistic presentation of the company's operations and other aspects of the business.

Other comprehensive income is comprehensive income, which are mainly included in the

income statement and in the balance sheet. It should be noted that the management intends to

engage in different revenues and expenses, including full results, as it is not fully realized. Once

the underlying transactions are completed, the company is created when these investments are

sold and realized. The second world attaches greater importance to strengthening the

unconditional side of net profit, but also to changes in corporate income, which form part of the

capital rather than the underlying transactions. (Ray, 2011). OCI wants to report details that are

not needed and the company does not.

The table shows the other comprehensive income as stated in the annual reports of the company,

the only item to be reported is the OCI table is the foreign currency translation reserve, the value

was around 2,327,000 in 2017.

Other comprehensive income is comprehensive income, IFRS gains, which are mainly included

in the income statement and in the balance sheet. It should be noted that the management of a

company intends to include different revenues and expenses, including the total result, as it is not

fully implemented. The company that arose when the underlying transactions were completed is

the time when these investments are sold and realized. The other world attaches greater

importance to strengthening the unconditional side of net profit, rather on changes in corporate

profits that were part of equity rather than the underlying transaction. (Ray, 2011). OCI wants to

report details that are not necessary and that the company does not. Presenting a detailed and

holistic presentation of the company's operations and other aspects of the business.

Other comprehensive income is comprehensive income, which are mainly included in the

income statement and in the balance sheet. It should be noted that the management intends to

engage in different revenues and expenses, including full results, as it is not fully realized. Once

the underlying transactions are completed, the company is created when these investments are

sold and realized. The second world attaches greater importance to strengthening the

unconditional side of net profit, but also to changes in corporate income, which form part of the

capital rather than the underlying transactions. (Ray, 2011). OCI wants to report details that are

not needed and the company does not.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Computation of Corporate Income tax

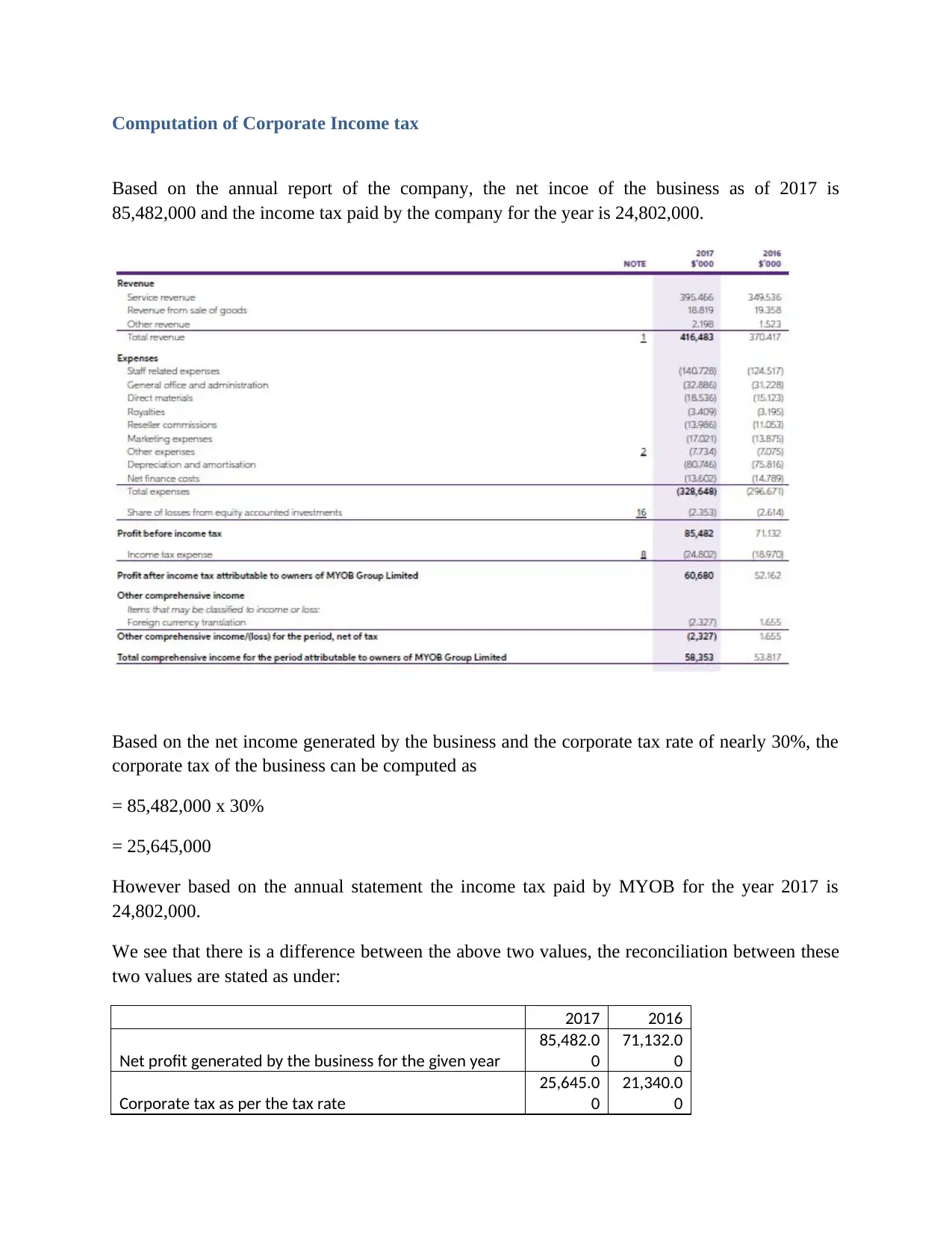

Based on the annual report of the company, the net incoe of the business as of 2017 is

85,482,000 and the income tax paid by the company for the year is 24,802,000.

Based on the net income generated by the business and the corporate tax rate of nearly 30%, the

corporate tax of the business can be computed as

= 85,482,000 x 30%

= 25,645,000

However based on the annual statement the income tax paid by MYOB for the year 2017 is

24,802,000.

We see that there is a difference between the above two values, the reconciliation between these

two values are stated as under:

2017 2016

Net profit generated by the business for the given year

85,482.0

0

71,132.0

0

Corporate tax as per the tax rate

25,645.0

0

21,340.0

0

Based on the annual report of the company, the net incoe of the business as of 2017 is

85,482,000 and the income tax paid by the company for the year is 24,802,000.

Based on the net income generated by the business and the corporate tax rate of nearly 30%, the

corporate tax of the business can be computed as

= 85,482,000 x 30%

= 25,645,000

However based on the annual statement the income tax paid by MYOB for the year 2017 is

24,802,000.

We see that there is a difference between the above two values, the reconciliation between these

two values are stated as under:

2017 2016

Net profit generated by the business for the given year

85,482.0

0

71,132.0

0

Corporate tax as per the tax rate

25,645.0

0

21,340.0

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

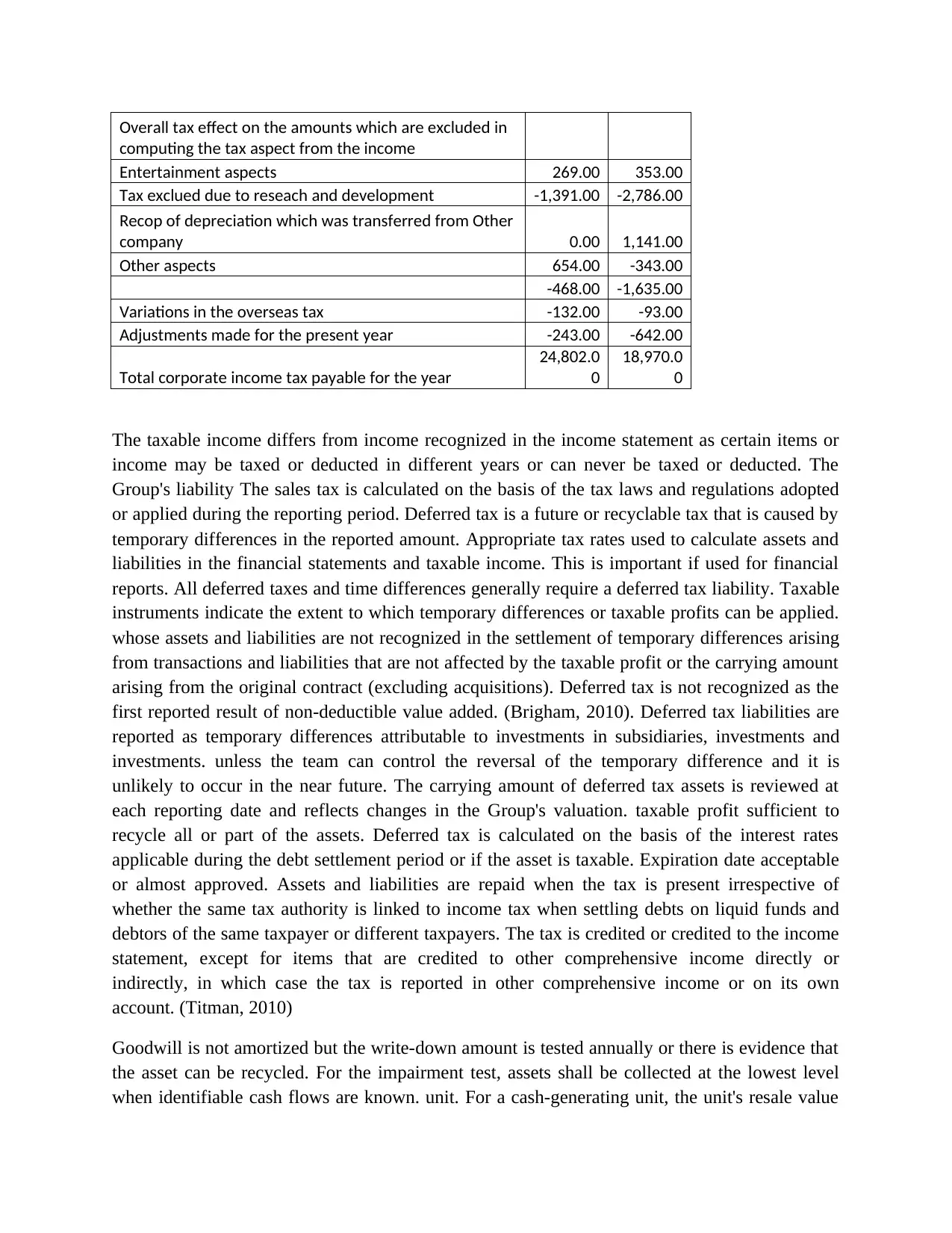

Overall tax effect on the amounts which are excluded in

computing the tax aspect from the income

Entertainment aspects 269.00 353.00

Tax exclued due to reseach and development -1,391.00 -2,786.00

Recop of depreciation which was transferred from Other

company 0.00 1,141.00

Other aspects 654.00 -343.00

-468.00 -1,635.00

Variations in the overseas tax -132.00 -93.00

Adjustments made for the present year -243.00 -642.00

Total corporate income tax payable for the year

24,802.0

0

18,970.0

0

The taxable income differs from income recognized in the income statement as certain items or

income may be taxed or deducted in different years or can never be taxed or deducted. The

Group's liability The sales tax is calculated on the basis of the tax laws and regulations adopted

or applied during the reporting period. Deferred tax is a future or recyclable tax that is caused by

temporary differences in the reported amount. Appropriate tax rates used to calculate assets and

liabilities in the financial statements and taxable income. This is important if used for financial

reports. All deferred taxes and time differences generally require a deferred tax liability. Taxable

instruments indicate the extent to which temporary differences or taxable profits can be applied.

whose assets and liabilities are not recognized in the settlement of temporary differences arising

from transactions and liabilities that are not affected by the taxable profit or the carrying amount

arising from the original contract (excluding acquisitions). Deferred tax is not recognized as the

first reported result of non-deductible value added. (Brigham, 2010). Deferred tax liabilities are

reported as temporary differences attributable to investments in subsidiaries, investments and

investments. unless the team can control the reversal of the temporary difference and it is

unlikely to occur in the near future. The carrying amount of deferred tax assets is reviewed at

each reporting date and reflects changes in the Group's valuation. taxable profit sufficient to

recycle all or part of the assets. Deferred tax is calculated on the basis of the interest rates

applicable during the debt settlement period or if the asset is taxable. Expiration date acceptable

or almost approved. Assets and liabilities are repaid when the tax is present irrespective of

whether the same tax authority is linked to income tax when settling debts on liquid funds and

debtors of the same taxpayer or different taxpayers. The tax is credited or credited to the income

statement, except for items that are credited to other comprehensive income directly or

indirectly, in which case the tax is reported in other comprehensive income or on its own

account. (Titman, 2010)

Goodwill is not amortized but the write-down amount is tested annually or there is evidence that

the asset can be recycled. For the impairment test, assets shall be collected at the lowest level

when identifiable cash flows are known. unit. For a cash-generating unit, the unit's resale value

computing the tax aspect from the income

Entertainment aspects 269.00 353.00

Tax exclued due to reseach and development -1,391.00 -2,786.00

Recop of depreciation which was transferred from Other

company 0.00 1,141.00

Other aspects 654.00 -343.00

-468.00 -1,635.00

Variations in the overseas tax -132.00 -93.00

Adjustments made for the present year -243.00 -642.00

Total corporate income tax payable for the year

24,802.0

0

18,970.0

0

The taxable income differs from income recognized in the income statement as certain items or

income may be taxed or deducted in different years or can never be taxed or deducted. The

Group's liability The sales tax is calculated on the basis of the tax laws and regulations adopted

or applied during the reporting period. Deferred tax is a future or recyclable tax that is caused by

temporary differences in the reported amount. Appropriate tax rates used to calculate assets and

liabilities in the financial statements and taxable income. This is important if used for financial

reports. All deferred taxes and time differences generally require a deferred tax liability. Taxable

instruments indicate the extent to which temporary differences or taxable profits can be applied.

whose assets and liabilities are not recognized in the settlement of temporary differences arising

from transactions and liabilities that are not affected by the taxable profit or the carrying amount

arising from the original contract (excluding acquisitions). Deferred tax is not recognized as the

first reported result of non-deductible value added. (Brigham, 2010). Deferred tax liabilities are

reported as temporary differences attributable to investments in subsidiaries, investments and

investments. unless the team can control the reversal of the temporary difference and it is

unlikely to occur in the near future. The carrying amount of deferred tax assets is reviewed at

each reporting date and reflects changes in the Group's valuation. taxable profit sufficient to

recycle all or part of the assets. Deferred tax is calculated on the basis of the interest rates

applicable during the debt settlement period or if the asset is taxable. Expiration date acceptable

or almost approved. Assets and liabilities are repaid when the tax is present irrespective of

whether the same tax authority is linked to income tax when settling debts on liquid funds and

debtors of the same taxpayer or different taxpayers. The tax is credited or credited to the income

statement, except for items that are credited to other comprehensive income directly or

indirectly, in which case the tax is reported in other comprehensive income or on its own

account. (Titman, 2010)

Goodwill is not amortized but the write-down amount is tested annually or there is evidence that

the asset can be recycled. For the impairment test, assets shall be collected at the lowest level

when identifiable cash flows are known. unit. For a cash-generating unit, the unit's resale value

reduces the write-down, mainly decreases the book value of goodwill associated with the

company, and then gives the entity access to other assets. The impairment loss recognized in

goodwill can not be changed in subsequent periods. The recoverable amount is the actual value,

the sale cost and the value in use. Estimated future cash flows reflecting current money market

and risk assessments at discounted discount rates before tax in current valuations are special

tools for which future cash flow analyzes have not been modified.

References

Bragg, Steven. (2007). Throughput Accounting: A Guide to Constraint Management. 1st edition.

Wiley & Sons

Brigham, E. F. (2010). Financial Management: Theory & Practice. 5th edition. Cengage

Learning.

Brooks, R. M. (2012). Financial Management. 4th edition. Prentice Hall.

Kaplan, R. S., & Young, M. S. (2011). Management Accounting. 3rd edition. Prentice Hall.

MYOB. (2017). Annual report of MYOB

Ray, G., & Eric, N. (2011). Managerial Accounting. McGraw-Hill/Irwin.

Titman, S. J. (2010). Financial Management. Prentice Hall.

Weygandt. (2011). Managerial Accounting: Tools for Business Decision Making (6th ed.).

Wiley.

company, and then gives the entity access to other assets. The impairment loss recognized in

goodwill can not be changed in subsequent periods. The recoverable amount is the actual value,

the sale cost and the value in use. Estimated future cash flows reflecting current money market

and risk assessments at discounted discount rates before tax in current valuations are special

tools for which future cash flow analyzes have not been modified.

References

Bragg, Steven. (2007). Throughput Accounting: A Guide to Constraint Management. 1st edition.

Wiley & Sons

Brigham, E. F. (2010). Financial Management: Theory & Practice. 5th edition. Cengage

Learning.

Brooks, R. M. (2012). Financial Management. 4th edition. Prentice Hall.

Kaplan, R. S., & Young, M. S. (2011). Management Accounting. 3rd edition. Prentice Hall.

MYOB. (2017). Annual report of MYOB

Ray, G., & Eric, N. (2011). Managerial Accounting. McGraw-Hill/Irwin.

Titman, S. J. (2010). Financial Management. Prentice Hall.

Weygandt. (2011). Managerial Accounting: Tools for Business Decision Making (6th ed.).

Wiley.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.