Dividend Pay-Out Recommendation: A Report on Nam Cheong Limited

VerifiedAdded on 2023/06/03

|10

|2981

|207

Report

AI Summary

This report provides an analysis of dividend payout strategies, focusing on OCBC Group, a company listed on the Singapore Exchange. The analysis includes a review of the company's historical financial performance from 2013 to 2017, examining key financial and non-financial factors affecting its performance. It discusses the impact of dividend policy on these factors, provides a critical review of the company's dividend policy in light of the Modigliani and Miller approach, and forecasts the company's revenue for the next financial year. The report concludes with a recommendation for the next year's dividend payout, suggesting a potential increase based on positive prospects and historical emphasis on reinvestment for future earnings. The student also reflects on their contribution to the report and its relevance to their future employability. Desklib provides this assignment as an example of student work.

PREPARED BY

NAME:

STUDENT ID:

NAME:

STUDENT ID:

1

A Brief Report onA Brief Report on

thethe

Dividend pay-outDividend pay-out

of theof the

Nam CheongNam Cheong

LimitedLimited

NAME:

STUDENT ID:

NAME:

STUDENT ID:

1

A Brief Report onA Brief Report on

thethe

Dividend pay-outDividend pay-out

of theof the

Nam CheongNam Cheong

LimitedLimited

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

Though there are numerous theories suggested by various scholars from time to time, but its

ultimate application is completely dependent on the rational judgment considering the various

financial and non-financial factors associated with the company at a given circumstances. The

main purpose of our report is to suggest how to decide the next year’s dividend pay-out for

which we have selected the OCBC Group, a Bank listed in the FTSE ST ALL Share index on the

Singapore Exchange.

2

Though there are numerous theories suggested by various scholars from time to time, but its

ultimate application is completely dependent on the rational judgment considering the various

financial and non-financial factors associated with the company at a given circumstances. The

main purpose of our report is to suggest how to decide the next year’s dividend pay-out for

which we have selected the OCBC Group, a Bank listed in the FTSE ST ALL Share index on the

Singapore Exchange.

2

Table of Contents

Executive Summary.....................................................................................................................................2

Introduction.................................................................................................................................................4

Background..................................................................................................................................................4

Key Indices...................................................................................................................................................4

Analysis of the company’s historical performance..................................................................................4

Discussion on the effect of dividend policy on above key factors...........................................................6

Critical discussion on the company’s dividend policy..................................................................................6

Discussion on company’s next financial year’s forecasted Revenue...........................................................7

Advice what should the next year dividend pay-out...................................................................................7

Conclusion with personal contribution........................................................................................................8

References...................................................................................................................................................8

3

Executive Summary.....................................................................................................................................2

Introduction.................................................................................................................................................4

Background..................................................................................................................................................4

Key Indices...................................................................................................................................................4

Analysis of the company’s historical performance..................................................................................4

Discussion on the effect of dividend policy on above key factors...........................................................6

Critical discussion on the company’s dividend policy..................................................................................6

Discussion on company’s next financial year’s forecasted Revenue...........................................................7

Advice what should the next year dividend pay-out...................................................................................7

Conclusion with personal contribution........................................................................................................8

References...................................................................................................................................................8

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Our report is intended to provide the suggestion on how to decide the future year’s dividend pay-

out for the company based on our study and evaluation of the financial data of one of the

company listed in the FTSE ST ALL Share index on the Singapore Exchange naming OCBC

group (Belton, 2017). Our study begins with the historical performance of the company for last

five years along with the various key factors and measures both financial and non-financial as

well affecting the performance. Before suggesting on future year’s dividend pay-out with the

rationale behind the decision we have undergone a critical discussion on its existing dividend

policy together with the estimation of future year’s revenue forecast. Finally at the end,

individual contribution towards this report along with the relevance of this report in changing the

individual approach for further assignments and enhancing individual employability have been

briefly elaborated along with suggestion for the policy on future year’s dividend pay-out

(Alexander, 2016).

Background

The dividend policy of a firm demands a critical judgment to be made by the Board of directors

as it requires a proper balance between meeting shareholders expectation to get a share out of the

earnings available for distribution to them and setting aside a part of the same in form of retained

earnings that shall be utilized as a source for future reinvestment to be made by the company.

Key Indices

Analysis of the company’s historical performance

For the purpose of making a detailed study of historical performance of the OCBC group we

have covered the last five years annual income statement starting from the year 2013 and ending

on 2017. The following table clearly reflects the historical performance of the company in last

five years (Bromwich & Scapens, 2016).

Income statement (Figure in S$) (Singapore Dollar)

Particulars 2013 2014 2015 2016 2017

Total income 6621 8340 8722 8489 9636

Operating

Expenses

2784 3258 3664 3788 4034

Operating

Profit before

Allowances

3837 5082 5058 4701 5602

Net Profit

Attributable

to

Shareholders

2768 3842 3903 3473 4146

4

Our report is intended to provide the suggestion on how to decide the future year’s dividend pay-

out for the company based on our study and evaluation of the financial data of one of the

company listed in the FTSE ST ALL Share index on the Singapore Exchange naming OCBC

group (Belton, 2017). Our study begins with the historical performance of the company for last

five years along with the various key factors and measures both financial and non-financial as

well affecting the performance. Before suggesting on future year’s dividend pay-out with the

rationale behind the decision we have undergone a critical discussion on its existing dividend

policy together with the estimation of future year’s revenue forecast. Finally at the end,

individual contribution towards this report along with the relevance of this report in changing the

individual approach for further assignments and enhancing individual employability have been

briefly elaborated along with suggestion for the policy on future year’s dividend pay-out

(Alexander, 2016).

Background

The dividend policy of a firm demands a critical judgment to be made by the Board of directors

as it requires a proper balance between meeting shareholders expectation to get a share out of the

earnings available for distribution to them and setting aside a part of the same in form of retained

earnings that shall be utilized as a source for future reinvestment to be made by the company.

Key Indices

Analysis of the company’s historical performance

For the purpose of making a detailed study of historical performance of the OCBC group we

have covered the last five years annual income statement starting from the year 2013 and ending

on 2017. The following table clearly reflects the historical performance of the company in last

five years (Bromwich & Scapens, 2016).

Income statement (Figure in S$) (Singapore Dollar)

Particulars 2013 2014 2015 2016 2017

Total income 6621 8340 8722 8489 9636

Operating

Expenses

2784 3258 3664 3788 4034

Operating

Profit before

Allowances

3837 5082 5058 4701 5602

Net Profit

Attributable

to

Shareholders

2768 3842 3903 3473 4146

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Core

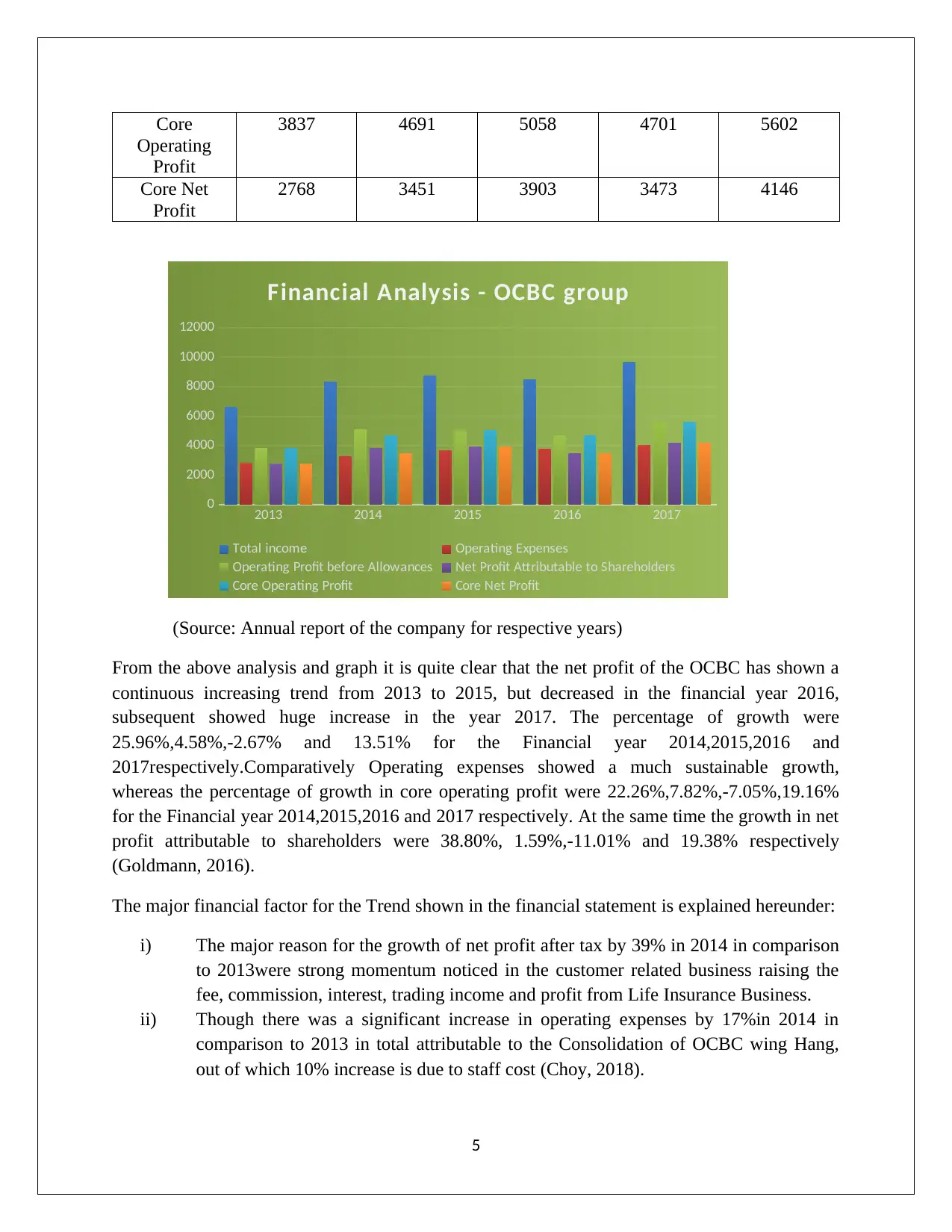

Operating

Profit

3837 4691 5058 4701 5602

Core Net

Profit

2768 3451 3903 3473 4146

2013 2014 2015 2016 2017

0

2000

4000

6000

8000

10000

12000

Financial Analysis - OCBC group

Total income Operating Expenses

Operating Profit before Allowances Net Profit Attributable to Shareholders

Core Operating Profit Core Net Profit

(Source: Annual report of the company for respective years)

From the above analysis and graph it is quite clear that the net profit of the OCBC has shown a

continuous increasing trend from 2013 to 2015, but decreased in the financial year 2016,

subsequent showed huge increase in the year 2017. The percentage of growth were

25.96%,4.58%,-2.67% and 13.51% for the Financial year 2014,2015,2016 and

2017respectively.Comparatively Operating expenses showed a much sustainable growth,

whereas the percentage of growth in core operating profit were 22.26%,7.82%,-7.05%,19.16%

for the Financial year 2014,2015,2016 and 2017 respectively. At the same time the growth in net

profit attributable to shareholders were 38.80%, 1.59%,-11.01% and 19.38% respectively

(Goldmann, 2016).

The major financial factor for the Trend shown in the financial statement is explained hereunder:

i) The major reason for the growth of net profit after tax by 39% in 2014 in comparison

to 2013were strong momentum noticed in the customer related business raising the

fee, commission, interest, trading income and profit from Life Insurance Business.

ii) Though there was a significant increase in operating expenses by 17%in 2014 in

comparison to 2013 in total attributable to the Consolidation of OCBC wing Hang,

out of which 10% increase is due to staff cost (Choy, 2018).

5

Operating

Profit

3837 4691 5058 4701 5602

Core Net

Profit

2768 3451 3903 3473 4146

2013 2014 2015 2016 2017

0

2000

4000

6000

8000

10000

12000

Financial Analysis - OCBC group

Total income Operating Expenses

Operating Profit before Allowances Net Profit Attributable to Shareholders

Core Operating Profit Core Net Profit

(Source: Annual report of the company for respective years)

From the above analysis and graph it is quite clear that the net profit of the OCBC has shown a

continuous increasing trend from 2013 to 2015, but decreased in the financial year 2016,

subsequent showed huge increase in the year 2017. The percentage of growth were

25.96%,4.58%,-2.67% and 13.51% for the Financial year 2014,2015,2016 and

2017respectively.Comparatively Operating expenses showed a much sustainable growth,

whereas the percentage of growth in core operating profit were 22.26%,7.82%,-7.05%,19.16%

for the Financial year 2014,2015,2016 and 2017 respectively. At the same time the growth in net

profit attributable to shareholders were 38.80%, 1.59%,-11.01% and 19.38% respectively

(Goldmann, 2016).

The major financial factor for the Trend shown in the financial statement is explained hereunder:

i) The major reason for the growth of net profit after tax by 39% in 2014 in comparison

to 2013were strong momentum noticed in the customer related business raising the

fee, commission, interest, trading income and profit from Life Insurance Business.

ii) Though there was a significant increase in operating expenses by 17%in 2014 in

comparison to 2013 in total attributable to the Consolidation of OCBC wing Hang,

out of which 10% increase is due to staff cost (Choy, 2018).

5

iii) On 30th September, 2014 because the bank increased its stake in the Bank of Ningbo,

hence that significantly increased in share of earning from the associated company.

iv) The major reason behind increase in net profit after tax by 13% in 2015 in

comparison to 2014 excluding one-off gain was attributable to rise in trading and

investment income, fee, commission and net interest income.

v) The rate of growth of operating expenses in the year 2015 is 12% more in

comparison to 2014 after taking into account the full years effect of consolidation of

OCBC Wing hang, though excluding this consolidation it was only 5% mainly

attributable to the increase in staff strength resulting into higher staff cost.

vi) The net profit after tax for the year 2016 decreased by 11% in comparison to 2015

due to the significant reduction in trading and Insurance income and increase in net

allowances (Mahapatra, Levental, & Narasimhan, 2017).

vii) The net profit after tax increased by 19% in 2017 in comparison to 2016 attributable

to the growth momentum noticed by wealth management, insurance business and

Banking, whereas the major reason for rise of 6% in operating expenses were

business expansion and staff cost.

The major non- financial factor for the Trend shown in the financial statement is explained

hereunder:

i) The soundness of long term corporate strategy chosen and the strength and resilience

shown in the diversified business for the financial year 2017’s performance.

ii) The adverse global operational environment brought down the profit of the year 2016.

iii) The initiative to adopt the new model of banking business with new technological up

gradation known as Fin tech is a factor for growth in the year 2015.

iv) The strong growth with expansion strategy is the major reason for growth in the year

2014 (Linden & Freeman, 2017).

Discussion on the effect of dividend policy on above key factors

It is clearly evident from the study of the dividend payout of the OCBC group as reflected

through the annual reports of the aforesaid years that as the adoption of a steady and predictable

dividend pay-out policy had been preferred hence there dividend policy of the company has no

effect on anyone of the key factors and measures discussed above (Lavassani & Movahedi,

2017).

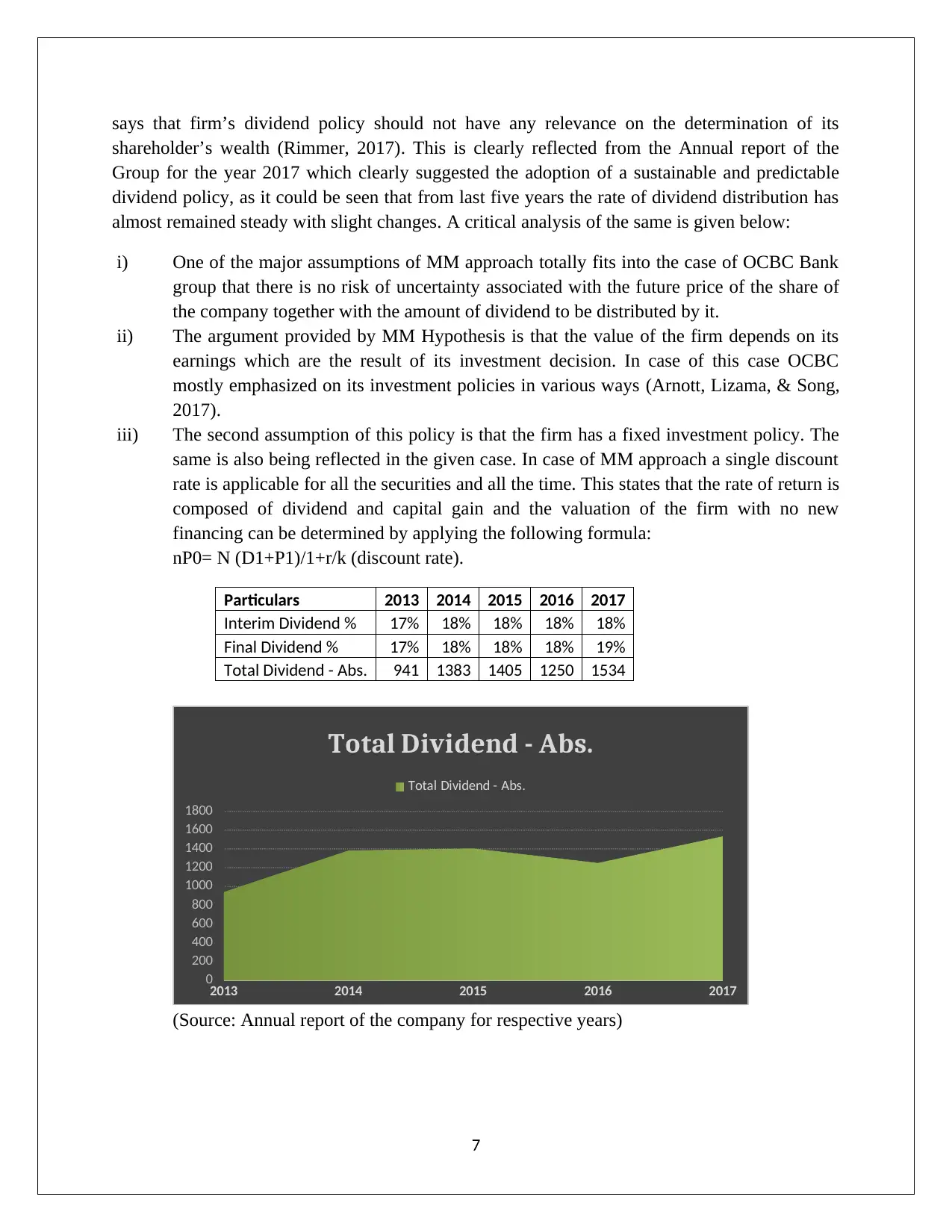

Critical discussion on the company’s dividend policy

In case of OCBC Bank group it is clearly evident from the study of annual reports of last five

years that the Modigliani and Miller approach for dividend distribution has been adopted, which

6

hence that significantly increased in share of earning from the associated company.

iv) The major reason behind increase in net profit after tax by 13% in 2015 in

comparison to 2014 excluding one-off gain was attributable to rise in trading and

investment income, fee, commission and net interest income.

v) The rate of growth of operating expenses in the year 2015 is 12% more in

comparison to 2014 after taking into account the full years effect of consolidation of

OCBC Wing hang, though excluding this consolidation it was only 5% mainly

attributable to the increase in staff strength resulting into higher staff cost.

vi) The net profit after tax for the year 2016 decreased by 11% in comparison to 2015

due to the significant reduction in trading and Insurance income and increase in net

allowances (Mahapatra, Levental, & Narasimhan, 2017).

vii) The net profit after tax increased by 19% in 2017 in comparison to 2016 attributable

to the growth momentum noticed by wealth management, insurance business and

Banking, whereas the major reason for rise of 6% in operating expenses were

business expansion and staff cost.

The major non- financial factor for the Trend shown in the financial statement is explained

hereunder:

i) The soundness of long term corporate strategy chosen and the strength and resilience

shown in the diversified business for the financial year 2017’s performance.

ii) The adverse global operational environment brought down the profit of the year 2016.

iii) The initiative to adopt the new model of banking business with new technological up

gradation known as Fin tech is a factor for growth in the year 2015.

iv) The strong growth with expansion strategy is the major reason for growth in the year

2014 (Linden & Freeman, 2017).

Discussion on the effect of dividend policy on above key factors

It is clearly evident from the study of the dividend payout of the OCBC group as reflected

through the annual reports of the aforesaid years that as the adoption of a steady and predictable

dividend pay-out policy had been preferred hence there dividend policy of the company has no

effect on anyone of the key factors and measures discussed above (Lavassani & Movahedi,

2017).

Critical discussion on the company’s dividend policy

In case of OCBC Bank group it is clearly evident from the study of annual reports of last five

years that the Modigliani and Miller approach for dividend distribution has been adopted, which

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

says that firm’s dividend policy should not have any relevance on the determination of its

shareholder’s wealth (Rimmer, 2017). This is clearly reflected from the Annual report of the

Group for the year 2017 which clearly suggested the adoption of a sustainable and predictable

dividend policy, as it could be seen that from last five years the rate of dividend distribution has

almost remained steady with slight changes. A critical analysis of the same is given below:

i) One of the major assumptions of MM approach totally fits into the case of OCBC Bank

group that there is no risk of uncertainty associated with the future price of the share of

the company together with the amount of dividend to be distributed by it.

ii) The argument provided by MM Hypothesis is that the value of the firm depends on its

earnings which are the result of its investment decision. In case of this case OCBC

mostly emphasized on its investment policies in various ways (Arnott, Lizama, & Song,

2017).

iii) The second assumption of this policy is that the firm has a fixed investment policy. The

same is also being reflected in the given case. In case of MM approach a single discount

rate is applicable for all the securities and all the time. This states that the rate of return is

composed of dividend and capital gain and the valuation of the firm with no new

financing can be determined by applying the following formula:

nP0= N (D1+P1)/1+r/k (discount rate).

Particulars 2013 2014 2015 2016 2017

Interim Dividend % 17% 18% 18% 18% 18%

Final Dividend % 17% 18% 18% 18% 19%

Total Dividend - Abs. 941 1383 1405 1250 1534

2013 2014 2015 2016 2017

0

200

400

600

800

1000

1200

1400

1600

1800

Total Dividend - Abs.

Total Dividend - Abs.

(Source: Annual report of the company for respective years)

7

shareholder’s wealth (Rimmer, 2017). This is clearly reflected from the Annual report of the

Group for the year 2017 which clearly suggested the adoption of a sustainable and predictable

dividend policy, as it could be seen that from last five years the rate of dividend distribution has

almost remained steady with slight changes. A critical analysis of the same is given below:

i) One of the major assumptions of MM approach totally fits into the case of OCBC Bank

group that there is no risk of uncertainty associated with the future price of the share of

the company together with the amount of dividend to be distributed by it.

ii) The argument provided by MM Hypothesis is that the value of the firm depends on its

earnings which are the result of its investment decision. In case of this case OCBC

mostly emphasized on its investment policies in various ways (Arnott, Lizama, & Song,

2017).

iii) The second assumption of this policy is that the firm has a fixed investment policy. The

same is also being reflected in the given case. In case of MM approach a single discount

rate is applicable for all the securities and all the time. This states that the rate of return is

composed of dividend and capital gain and the valuation of the firm with no new

financing can be determined by applying the following formula:

nP0= N (D1+P1)/1+r/k (discount rate).

Particulars 2013 2014 2015 2016 2017

Interim Dividend % 17% 18% 18% 18% 18%

Final Dividend % 17% 18% 18% 18% 19%

Total Dividend - Abs. 941 1383 1405 1250 1534

2013 2014 2015 2016 2017

0

200

400

600

800

1000

1200

1400

1600

1800

Total Dividend - Abs.

Total Dividend - Abs.

(Source: Annual report of the company for respective years)

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The above graph and table shows the amount distributed as dividend in the company. Both the

interim and final dividend have been taken into consideration.

Discussion on company’s next financial year’s forecasted Revenue

In order to make a rationale projection for the projected earning s of 2018 for the OCBC group

we have taken the help of various media reports, various reports published in media etc.

i) OCBC group is in the process of finalizing the process of divestment through the sale

of Great Eastern Life Malaysia and as per the report published in the Business

Singapore dated 5th day of June, 2018, thereby planning to achieve the level of its

core earnings at the rate lying between 10-12% return on its total assets and 6%to 7%

of RWA (Trieu, 2017).

ii) As per the CEO of the OCBC after the announcement of the Q2 ,2018 results of the

Bank in the forthcoming quarter it will observe the gradual increase in the net interest

margins in spite of the present resilience experienced by few Home buyers for which

some property cooling measures have also been taken by it.

iii) As the OCBC management has already set a target rate of seven to eight percent

finding the year to date growth rate of 5.5% that shall increase its asset quality base.

iv) In the forthcoming year if the Bank wants to gain the competitive advantage from the

viewpoint of its lender than the digital transformation would be a necessity for the

Bank to raise its earnings and retain its customers. Hence without proper approach for

this transformation may significantly affect the future earnings of the bank. Hence it

has targeted to achieve the cost to ratio rate of 40% by 2023 through its tried and

tested digital transformational platform (Dichev, 2017).

Advice what should the next year dividend pay-out

It is quite clear from the study of dividend pay-out history of the history of the OCBC group, that

it always tried to prove its faith on the MM Hypothesis of dividend distribution by clearly stating

that an investor should always be able to predict the future earnings in form of dividend for

which stability and sustainability are the two key requirements (Dumay & Baard, 2017). Hence

from the Annual report of 2017 in which the dividend was 19 percent per share was declared in

the forthcoming year of 2018 it may be expected that due to its positive prospect of achieving

higher net profit after tax in the forthcoming financial year it may raise the rate by 1%, thereby

making it 20%.

The second reason for this is that from its history it is quite evident that it has always emphasized

on the policy to raise its investment for raising future earnings and using the same earning for

future investment. Again adopting this approach proved successful for it in last few years too,

hence there remains very low scope that it should hardly bring a drastic change in its dividend

distribution policy for the year 2018 (Mun, 2018).

8

interim and final dividend have been taken into consideration.

Discussion on company’s next financial year’s forecasted Revenue

In order to make a rationale projection for the projected earning s of 2018 for the OCBC group

we have taken the help of various media reports, various reports published in media etc.

i) OCBC group is in the process of finalizing the process of divestment through the sale

of Great Eastern Life Malaysia and as per the report published in the Business

Singapore dated 5th day of June, 2018, thereby planning to achieve the level of its

core earnings at the rate lying between 10-12% return on its total assets and 6%to 7%

of RWA (Trieu, 2017).

ii) As per the CEO of the OCBC after the announcement of the Q2 ,2018 results of the

Bank in the forthcoming quarter it will observe the gradual increase in the net interest

margins in spite of the present resilience experienced by few Home buyers for which

some property cooling measures have also been taken by it.

iii) As the OCBC management has already set a target rate of seven to eight percent

finding the year to date growth rate of 5.5% that shall increase its asset quality base.

iv) In the forthcoming year if the Bank wants to gain the competitive advantage from the

viewpoint of its lender than the digital transformation would be a necessity for the

Bank to raise its earnings and retain its customers. Hence without proper approach for

this transformation may significantly affect the future earnings of the bank. Hence it

has targeted to achieve the cost to ratio rate of 40% by 2023 through its tried and

tested digital transformational platform (Dichev, 2017).

Advice what should the next year dividend pay-out

It is quite clear from the study of dividend pay-out history of the history of the OCBC group, that

it always tried to prove its faith on the MM Hypothesis of dividend distribution by clearly stating

that an investor should always be able to predict the future earnings in form of dividend for

which stability and sustainability are the two key requirements (Dumay & Baard, 2017). Hence

from the Annual report of 2017 in which the dividend was 19 percent per share was declared in

the forthcoming year of 2018 it may be expected that due to its positive prospect of achieving

higher net profit after tax in the forthcoming financial year it may raise the rate by 1%, thereby

making it 20%.

The second reason for this is that from its history it is quite evident that it has always emphasized

on the policy to raise its investment for raising future earnings and using the same earning for

future investment. Again adopting this approach proved successful for it in last few years too,

hence there remains very low scope that it should hardly bring a drastic change in its dividend

distribution policy for the year 2018 (Mun, 2018).

8

Conclusion with personal contribution

At the outset I would like to add some lines to the fact that how this study helped me to bring

some positive dynamic change by making myself more capable to accept the similar types of

assignment. Overall the capital structure and dividend policy has a lot to do with the final

performance of the company through the year end. Some of the key points noted in this regard

are as follows:

1. This study provides me the opportunity to have a deep rooted analysis of the critical

factors that are to be kept in mind while deciding about the dividend policy of the

company.

2. Again it makes us aware of the fact that how a very liberal policy towards dividend

distribution may fail to achieve the growth of the company as without making further

investment there is no scope of higher future earnings.

3. Again in this assignment my individual contribution was the collection of the relevant

facts and figures reflected through the report, hence it enhanced my analytical capability

as well as ability to select the relevant facts related to the report.

References

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-

431.

Arnott, D., Lizama, F., & Song, Y. (2017). Patterns of business intelligence systems use in organizations.

Decision Support Systems, 97(2), 58-68.

Belton, P. (2017). Competitive Strategy: Creating and Sustaining Superior Performance. London: Macat

International ltd.

Bromwich, M., & Scapens, R. (2016). Management Accounting Research: 25 years on. Management

Accounting Research, 31(1), 1-9.

Choy, Y. K. (2018). Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 145. doi:https://doi.org/10.1016/j.ecolecon.2017.08.005

9

At the outset I would like to add some lines to the fact that how this study helped me to bring

some positive dynamic change by making myself more capable to accept the similar types of

assignment. Overall the capital structure and dividend policy has a lot to do with the final

performance of the company through the year end. Some of the key points noted in this regard

are as follows:

1. This study provides me the opportunity to have a deep rooted analysis of the critical

factors that are to be kept in mind while deciding about the dividend policy of the

company.

2. Again it makes us aware of the fact that how a very liberal policy towards dividend

distribution may fail to achieve the growth of the company as without making further

investment there is no scope of higher future earnings.

3. Again in this assignment my individual contribution was the collection of the relevant

facts and figures reflected through the report, hence it enhanced my analytical capability

as well as ability to select the relevant facts related to the report.

References

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-

431.

Arnott, D., Lizama, F., & Song, Y. (2017). Patterns of business intelligence systems use in organizations.

Decision Support Systems, 97(2), 58-68.

Belton, P. (2017). Competitive Strategy: Creating and Sustaining Superior Performance. London: Macat

International ltd.

Bromwich, M., & Scapens, R. (2016). Management Accounting Research: 25 years on. Management

Accounting Research, 31(1), 1-9.

Choy, Y. K. (2018). Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 145. doi:https://doi.org/10.1016/j.ecolecon.2017.08.005

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Dichev, I. (2017). On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), 617-632. doi:https://doi.org/10.1080/00014788.2017.1299620

Dumay, J., & Baard, V. (2017). An introduction to interventionist research in accounting. The Routledge

Companion to Qualitative Accounting Research Methods, 265. Retrieved from

https://books.google.co.in/books?

hl=en&lr=&id=PzQlDwAAQBAJ&oi=fnd&pg=PA265&dq=Dumay,+J.,+%26+Baard,+V.+(2017).

+An+introduction+to+interventionist+research+in+accounting.

+The+Routledge+Companion+to+Qualitative+Accounting+Research+Methods,

+265.&ots=ta1isTHB

Goldmann, K. (2016). Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4(3), 103-112.

Lavassani, K., & Movahedi, B. (2017). Applications Driven Information Systems: Beyond Networks toward

Business Ecosystems. International Journal of Innovation in the Digital Economy, 8(1), 61-75.

Linden, B., & Freeman, R. (2017). Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), 353-379. doi:https://doi.org/10.1017/beq.2017.1

Mahapatra, S., Levental, S., & Narasimhan, R. (2017). Market price uncertainty, risk aversion and

procurement: Combining contracts and open market sourcing alternatives. International Journal

of Production Economics, 33(1), 34-51.

Mun, K. a. (2018). A close look at the role of regulatory fit in consumers’ responses to unethical firms.

Korea: PROCEEDINGS OF THE INTERNATIONAL CRISIS AND RISK COMMUNICATION

CONFERENCE. doi:https://doi.org/10.30658/icrcc.2018.13

Rimmer, M. (2017). The Trans-Pacific Partnership: Intellectual property, public health, and access to

essential medicines. . Intellectual Property Journal, 29(2), 277.

Trieu, V. (2017). Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, 93(1), 111-124.

10

Research, 47(6), 617-632. doi:https://doi.org/10.1080/00014788.2017.1299620

Dumay, J., & Baard, V. (2017). An introduction to interventionist research in accounting. The Routledge

Companion to Qualitative Accounting Research Methods, 265. Retrieved from

https://books.google.co.in/books?

hl=en&lr=&id=PzQlDwAAQBAJ&oi=fnd&pg=PA265&dq=Dumay,+J.,+%26+Baard,+V.+(2017).

+An+introduction+to+interventionist+research+in+accounting.

+The+Routledge+Companion+to+Qualitative+Accounting+Research+Methods,

+265.&ots=ta1isTHB

Goldmann, K. (2016). Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4(3), 103-112.

Lavassani, K., & Movahedi, B. (2017). Applications Driven Information Systems: Beyond Networks toward

Business Ecosystems. International Journal of Innovation in the Digital Economy, 8(1), 61-75.

Linden, B., & Freeman, R. (2017). Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), 353-379. doi:https://doi.org/10.1017/beq.2017.1

Mahapatra, S., Levental, S., & Narasimhan, R. (2017). Market price uncertainty, risk aversion and

procurement: Combining contracts and open market sourcing alternatives. International Journal

of Production Economics, 33(1), 34-51.

Mun, K. a. (2018). A close look at the role of regulatory fit in consumers’ responses to unethical firms.

Korea: PROCEEDINGS OF THE INTERNATIONAL CRISIS AND RISK COMMUNICATION

CONFERENCE. doi:https://doi.org/10.30658/icrcc.2018.13

Rimmer, M. (2017). The Trans-Pacific Partnership: Intellectual property, public health, and access to

essential medicines. . Intellectual Property Journal, 29(2), 277.

Trieu, V. (2017). Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, 93(1), 111-124.

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.