Auditing and Ethics Report: National Australia Bank Financial Analysis

VerifiedAdded on 2023/02/01

|9

|3044

|86

Report

AI Summary

This report presents a comprehensive financial analysis of the National Australia Bank (NAB). It begins with a background on the company, followed by a detailed discussion of materiality calculations, considering various bases like interest income, total assets, and equity, with a focus on the rationale behind the chosen criteria. The report then delves into an analytical review of NAB's financial performance from 2015 to 2018, utilizing key ratio analysis to assess profitability, efficiency, and capital ratios. It examines relevant audit assertions and outlines corresponding audit procedures. The cash flow statement is analyzed, highlighting significant inflows and outflows, non-cash activities, and the implications for the company's going concern assumption. Finally, the report analyzes the audit report issued by EY, addressing key audit matters and providing insights into the overall audit process and findings, including the calculation of provisions for credit impairment on loans.

Auditing and ethics in australia

NATIONAL AUSTRALIAN BANK

Student’s Name

[Email address]

NATIONAL AUSTRALIAN BANK

Student’s Name

[Email address]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Background..................................................................................................................................................2

Discussion and Analysis...............................................................................................................................3

Introduction to the company...................................................................................................................3

Section 1: Level of Materiality.................................................................................................................3

Section 2: Analytical Review, Assertions and Audit procedures..............................................................4

Section 3: Cash flow analysis...................................................................................................................5

Audit Report analysis...............................................................................................................................6

References...................................................................................................................................................7

Background..................................................................................................................................................2

Discussion and Analysis...............................................................................................................................3

Introduction to the company...................................................................................................................3

Section 1: Level of Materiality.................................................................................................................3

Section 2: Analytical Review, Assertions and Audit procedures..............................................................4

Section 3: Cash flow analysis...................................................................................................................5

Audit Report analysis...............................................................................................................................6

References...................................................................................................................................................7

Background

A following is a report on the financial analysis of one of the companies listed on Australian Stock

exchange named National Australian Bank. The report shows the calculation of materiality to be

considered during the audit of the company and how the same is arrived at using different bases. The

quantitative estimate and the rationale behind the same has been shown. The draft notes and the

disclosures have been studied and those which are significant from audit perspective has been

highlighted. Preliminary analytical review for last 4 years has also been done to establish the

relationship between the trend, the market and the company’s business. Relevant audit assertion and

related audit procedure for same has also been stated. In the final section, the company’s cash flow

statement has been studied w.r.t. cash inflows and outflows, non-cash activities and investing and

financing activities as well. The audit report has been studied and the relevant audit issues have been

highlighted in report.

A following is a report on the financial analysis of one of the companies listed on Australian Stock

exchange named National Australian Bank. The report shows the calculation of materiality to be

considered during the audit of the company and how the same is arrived at using different bases. The

quantitative estimate and the rationale behind the same has been shown. The draft notes and the

disclosures have been studied and those which are significant from audit perspective has been

highlighted. Preliminary analytical review for last 4 years has also been done to establish the

relationship between the trend, the market and the company’s business. Relevant audit assertion and

related audit procedure for same has also been stated. In the final section, the company’s cash flow

statement has been studied w.r.t. cash inflows and outflows, non-cash activities and investing and

financing activities as well. The audit report has been studied and the relevant audit issues have been

highlighted in report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

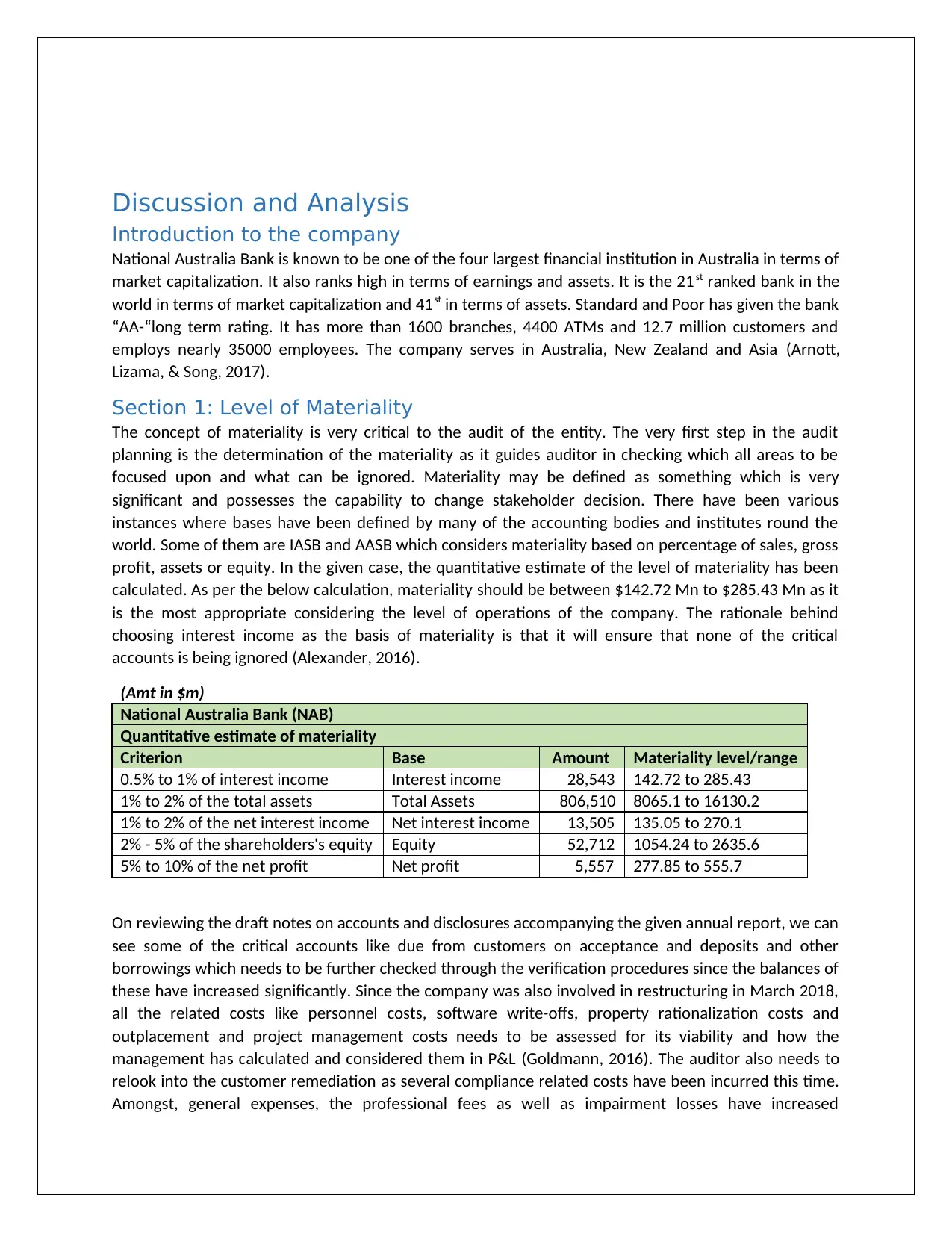

Discussion and Analysis

Introduction to the company

National Australia Bank is known to be one of the four largest financial institution in Australia in terms of

market capitalization. It also ranks high in terms of earnings and assets. It is the 21st ranked bank in the

world in terms of market capitalization and 41st in terms of assets. Standard and Poor has given the bank

“AA-“long term rating. It has more than 1600 branches, 4400 ATMs and 12.7 million customers and

employs nearly 35000 employees. The company serves in Australia, New Zealand and Asia (Arnott,

Lizama, & Song, 2017).

Section 1: Level of Materiality

The concept of materiality is very critical to the audit of the entity. The very first step in the audit

planning is the determination of the materiality as it guides auditor in checking which all areas to be

focused upon and what can be ignored. Materiality may be defined as something which is very

significant and possesses the capability to change stakeholder decision. There have been various

instances where bases have been defined by many of the accounting bodies and institutes round the

world. Some of them are IASB and AASB which considers materiality based on percentage of sales, gross

profit, assets or equity. In the given case, the quantitative estimate of the level of materiality has been

calculated. As per the below calculation, materiality should be between $142.72 Mn to $285.43 Mn as it

is the most appropriate considering the level of operations of the company. The rationale behind

choosing interest income as the basis of materiality is that it will ensure that none of the critical

accounts is being ignored (Alexander, 2016).

(Amt in $m)

National Australia Bank (NAB)

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of interest income Interest income 28,543 142.72 to 285.43

1% to 2% of the total assets Total Assets 806,510 8065.1 to 16130.2

1% to 2% of the net interest income Net interest income 13,505 135.05 to 270.1

2% - 5% of the shareholders's equity Equity 52,712 1054.24 to 2635.6

5% to 10% of the net profit Net profit 5,557 277.85 to 555.7

On reviewing the draft notes on accounts and disclosures accompanying the given annual report, we can

see some of the critical accounts like due from customers on acceptance and deposits and other

borrowings which needs to be further checked through the verification procedures since the balances of

these have increased significantly. Since the company was also involved in restructuring in March 2018,

all the related costs like personnel costs, software write-offs, property rationalization costs and

outplacement and project management costs needs to be assessed for its viability and how the

management has calculated and considered them in P&L (Goldmann, 2016). The auditor also needs to

relook into the customer remediation as several compliance related costs have been incurred this time.

Amongst, general expenses, the professional fees as well as impairment losses have increased

Introduction to the company

National Australia Bank is known to be one of the four largest financial institution in Australia in terms of

market capitalization. It also ranks high in terms of earnings and assets. It is the 21st ranked bank in the

world in terms of market capitalization and 41st in terms of assets. Standard and Poor has given the bank

“AA-“long term rating. It has more than 1600 branches, 4400 ATMs and 12.7 million customers and

employs nearly 35000 employees. The company serves in Australia, New Zealand and Asia (Arnott,

Lizama, & Song, 2017).

Section 1: Level of Materiality

The concept of materiality is very critical to the audit of the entity. The very first step in the audit

planning is the determination of the materiality as it guides auditor in checking which all areas to be

focused upon and what can be ignored. Materiality may be defined as something which is very

significant and possesses the capability to change stakeholder decision. There have been various

instances where bases have been defined by many of the accounting bodies and institutes round the

world. Some of them are IASB and AASB which considers materiality based on percentage of sales, gross

profit, assets or equity. In the given case, the quantitative estimate of the level of materiality has been

calculated. As per the below calculation, materiality should be between $142.72 Mn to $285.43 Mn as it

is the most appropriate considering the level of operations of the company. The rationale behind

choosing interest income as the basis of materiality is that it will ensure that none of the critical

accounts is being ignored (Alexander, 2016).

(Amt in $m)

National Australia Bank (NAB)

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of interest income Interest income 28,543 142.72 to 285.43

1% to 2% of the total assets Total Assets 806,510 8065.1 to 16130.2

1% to 2% of the net interest income Net interest income 13,505 135.05 to 270.1

2% - 5% of the shareholders's equity Equity 52,712 1054.24 to 2635.6

5% to 10% of the net profit Net profit 5,557 277.85 to 555.7

On reviewing the draft notes on accounts and disclosures accompanying the given annual report, we can

see some of the critical accounts like due from customers on acceptance and deposits and other

borrowings which needs to be further checked through the verification procedures since the balances of

these have increased significantly. Since the company was also involved in restructuring in March 2018,

all the related costs like personnel costs, software write-offs, property rationalization costs and

outplacement and project management costs needs to be assessed for its viability and how the

management has calculated and considered them in P&L (Goldmann, 2016). The auditor also needs to

relook into the customer remediation as several compliance related costs have been incurred this time.

Amongst, general expenses, the professional fees as well as impairment losses have increased

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

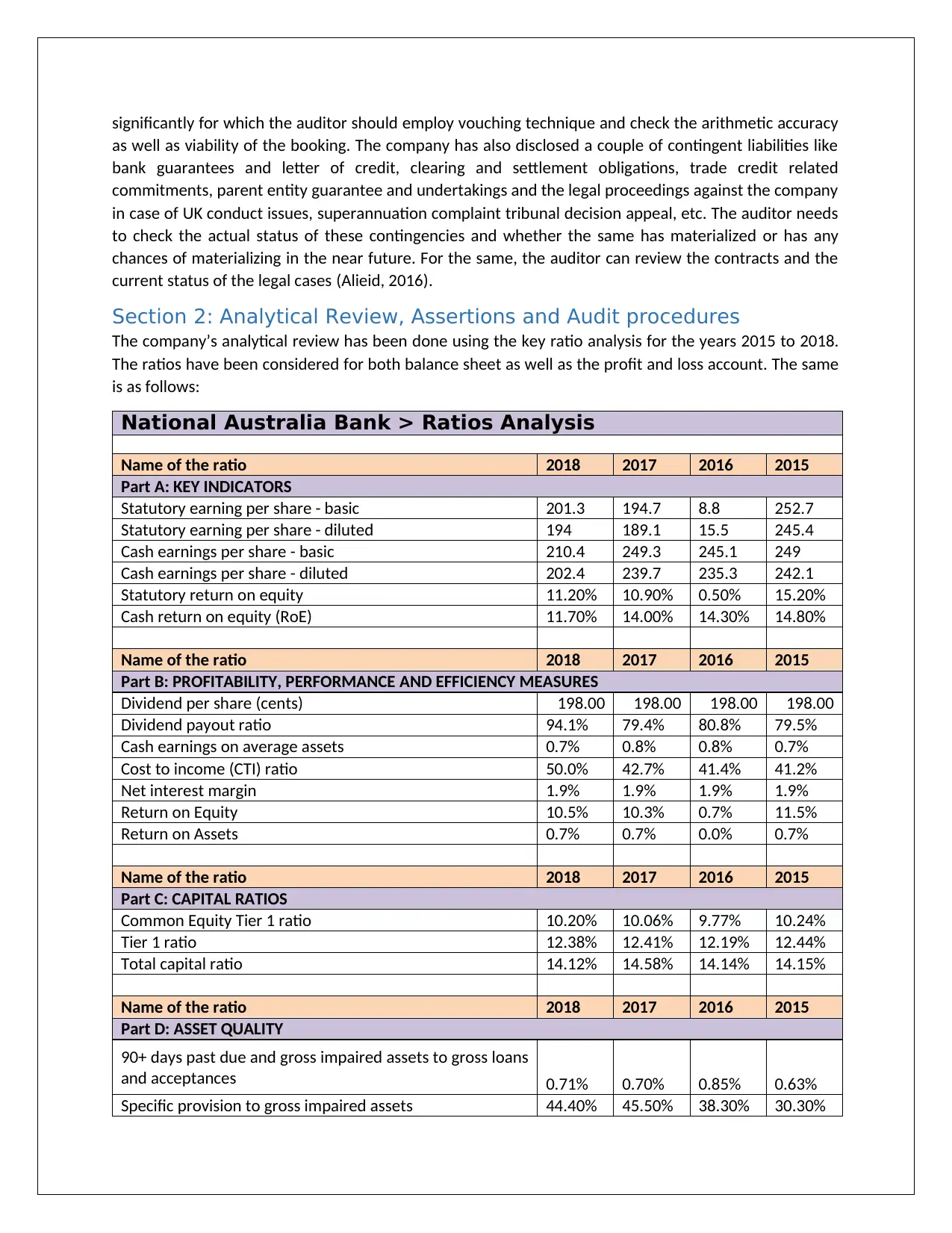

significantly for which the auditor should employ vouching technique and check the arithmetic accuracy

as well as viability of the booking. The company has also disclosed a couple of contingent liabilities like

bank guarantees and letter of credit, clearing and settlement obligations, trade credit related

commitments, parent entity guarantee and undertakings and the legal proceedings against the company

in case of UK conduct issues, superannuation complaint tribunal decision appeal, etc. The auditor needs

to check the actual status of these contingencies and whether the same has materialized or has any

chances of materializing in the near future. For the same, the auditor can review the contracts and the

current status of the legal cases (Alieid, 2016).

Section 2: Analytical Review, Assertions and Audit procedures

The company’s analytical review has been done using the key ratio analysis for the years 2015 to 2018.

The ratios have been considered for both balance sheet as well as the profit and loss account. The same

is as follows:

National Australia Bank > Ratios Analysis

Name of the ratio 2018 2017 2016 2015

Part A: KEY INDICATORS

Statutory earning per share - basic 201.3 194.7 8.8 252.7

Statutory earning per share - diluted 194 189.1 15.5 245.4

Cash earnings per share - basic 210.4 249.3 245.1 249

Cash earnings per share - diluted 202.4 239.7 235.3 242.1

Statutory return on equity 11.20% 10.90% 0.50% 15.20%

Cash return on equity (RoE) 11.70% 14.00% 14.30% 14.80%

Name of the ratio 2018 2017 2016 2015

Part B: PROFITABILITY, PERFORMANCE AND EFFICIENCY MEASURES

Dividend per share (cents) 198.00 198.00 198.00 198.00

Dividend payout ratio 94.1% 79.4% 80.8% 79.5%

Cash earnings on average assets 0.7% 0.8% 0.8% 0.7%

Cost to income (CTI) ratio 50.0% 42.7% 41.4% 41.2%

Net interest margin 1.9% 1.9% 1.9% 1.9%

Return on Equity 10.5% 10.3% 0.7% 11.5%

Return on Assets 0.7% 0.7% 0.0% 0.7%

Name of the ratio 2018 2017 2016 2015

Part C: CAPITAL RATIOS

Common Equity Tier 1 ratio 10.20% 10.06% 9.77% 10.24%

Tier 1 ratio 12.38% 12.41% 12.19% 12.44%

Total capital ratio 14.12% 14.58% 14.14% 14.15%

Name of the ratio 2018 2017 2016 2015

Part D: ASSET QUALITY

90+ days past due and gross impaired assets to gross loans

and acceptances 0.71% 0.70% 0.85% 0.63%

Specific provision to gross impaired assets 44.40% 45.50% 38.30% 30.30%

as well as viability of the booking. The company has also disclosed a couple of contingent liabilities like

bank guarantees and letter of credit, clearing and settlement obligations, trade credit related

commitments, parent entity guarantee and undertakings and the legal proceedings against the company

in case of UK conduct issues, superannuation complaint tribunal decision appeal, etc. The auditor needs

to check the actual status of these contingencies and whether the same has materialized or has any

chances of materializing in the near future. For the same, the auditor can review the contracts and the

current status of the legal cases (Alieid, 2016).

Section 2: Analytical Review, Assertions and Audit procedures

The company’s analytical review has been done using the key ratio analysis for the years 2015 to 2018.

The ratios have been considered for both balance sheet as well as the profit and loss account. The same

is as follows:

National Australia Bank > Ratios Analysis

Name of the ratio 2018 2017 2016 2015

Part A: KEY INDICATORS

Statutory earning per share - basic 201.3 194.7 8.8 252.7

Statutory earning per share - diluted 194 189.1 15.5 245.4

Cash earnings per share - basic 210.4 249.3 245.1 249

Cash earnings per share - diluted 202.4 239.7 235.3 242.1

Statutory return on equity 11.20% 10.90% 0.50% 15.20%

Cash return on equity (RoE) 11.70% 14.00% 14.30% 14.80%

Name of the ratio 2018 2017 2016 2015

Part B: PROFITABILITY, PERFORMANCE AND EFFICIENCY MEASURES

Dividend per share (cents) 198.00 198.00 198.00 198.00

Dividend payout ratio 94.1% 79.4% 80.8% 79.5%

Cash earnings on average assets 0.7% 0.8% 0.8% 0.7%

Cost to income (CTI) ratio 50.0% 42.7% 41.4% 41.2%

Net interest margin 1.9% 1.9% 1.9% 1.9%

Return on Equity 10.5% 10.3% 0.7% 11.5%

Return on Assets 0.7% 0.7% 0.0% 0.7%

Name of the ratio 2018 2017 2016 2015

Part C: CAPITAL RATIOS

Common Equity Tier 1 ratio 10.20% 10.06% 9.77% 10.24%

Tier 1 ratio 12.38% 12.41% 12.19% 12.44%

Total capital ratio 14.12% 14.58% 14.14% 14.15%

Name of the ratio 2018 2017 2016 2015

Part D: ASSET QUALITY

90+ days past due and gross impaired assets to gross loans

and acceptances 0.71% 0.70% 0.85% 0.63%

Specific provision to gross impaired assets 44.40% 45.50% 38.30% 30.30%

From the ratio analysis shown above, we see the sharp decline in profitability of the company for the

year 2016 and the main reason for the same was 2 major events of discontinued business. The company

sold 80% of the NAB’s life insurance business as well as initiated IPO as well as demerger of CYBG Group

in the same year, which resulted in 2 separate discontinued operations and lower profitability for the

group (Werner, 2017). Apart from that one time event, the company has delivered positive results in

terms of shareholder’s expectation as earnings per share has increased gradually over the years. The

cash earnings per share however has declined implying lesser inflow of cash for shareholders. The

statutory return on equity has improved whereas the cash return on equity has again declined implying

declined returns to shareholders. With respect to profitability and performance, the dividend payout has

improved constantly implying consistency in approach by company (Visinescu, Jones, & Sidorova, 2017).

The cost to income ratio has increased due to increase in expenses and that is a cause of worry for the

management. The net interest margin which is very critical aspect in banks and financial institutions has

almost been constant at 1.9% and therefore it indicates that the difference between the interest income

from the borrowers and interest payment to the lenders has not changed much.

In terms of capital ratios, NAB has comparatively less risk as its common equity tier 1 ratio which

indicates the proportion of common stock held by the bank has been more than the minimum

requirement of 4.50% for most of the years. It shows that the company has less risk of default (Grenier,

2017). Similarly, the Tier 1 ratio which is the ratio of equity capital and reserves to the risk weighted

assets has also been more or less constant near 10%. In terms of asset quality as well, 90+ days past

dues and gross impaired assets has come down from 0.85% to 0.71% over the years which is a positive

indicator. On the other hand, the specific provision to gross impaired assets ratio has increased

considerably from meagre 30% to 44% which indicates the increase in quality of assets (Jefferson, 2017).

Some of the relevant assertions include:

1. Accuracy in the provisions and if the completeness has been considered in taking relevant

provision for expenses and losses. The same can be checked by random sampling and vouching

and verification.

2. The auditor also needs to verify on cut-off date considered for each of the reporting and

accounting and if the classification of incomes and expenses and its presentation is done in

compliance with the Australian Accounting standards and the local GAAP. It can be checked by

reviewing the appropriateness of disclosures and notes to accounts and whether the supporting

evidences have been produced (Knechel & Salterio, 2016).

3. The company has also used a number of valuation techniques and particularly fair valuation in

case of financial instruments and therefore the auditor should use services of the expert to do

the audit for valuation appropriateness.

Section 3: Cash flow analysis

In terms of the cash flow statement, the greatest category in terms of cash inflows was financing activity

whereas the greatest contributor in terms of cash outflow was operating activities (Fukukawa & Mock,

2011).

year 2016 and the main reason for the same was 2 major events of discontinued business. The company

sold 80% of the NAB’s life insurance business as well as initiated IPO as well as demerger of CYBG Group

in the same year, which resulted in 2 separate discontinued operations and lower profitability for the

group (Werner, 2017). Apart from that one time event, the company has delivered positive results in

terms of shareholder’s expectation as earnings per share has increased gradually over the years. The

cash earnings per share however has declined implying lesser inflow of cash for shareholders. The

statutory return on equity has improved whereas the cash return on equity has again declined implying

declined returns to shareholders. With respect to profitability and performance, the dividend payout has

improved constantly implying consistency in approach by company (Visinescu, Jones, & Sidorova, 2017).

The cost to income ratio has increased due to increase in expenses and that is a cause of worry for the

management. The net interest margin which is very critical aspect in banks and financial institutions has

almost been constant at 1.9% and therefore it indicates that the difference between the interest income

from the borrowers and interest payment to the lenders has not changed much.

In terms of capital ratios, NAB has comparatively less risk as its common equity tier 1 ratio which

indicates the proportion of common stock held by the bank has been more than the minimum

requirement of 4.50% for most of the years. It shows that the company has less risk of default (Grenier,

2017). Similarly, the Tier 1 ratio which is the ratio of equity capital and reserves to the risk weighted

assets has also been more or less constant near 10%. In terms of asset quality as well, 90+ days past

dues and gross impaired assets has come down from 0.85% to 0.71% over the years which is a positive

indicator. On the other hand, the specific provision to gross impaired assets ratio has increased

considerably from meagre 30% to 44% which indicates the increase in quality of assets (Jefferson, 2017).

Some of the relevant assertions include:

1. Accuracy in the provisions and if the completeness has been considered in taking relevant

provision for expenses and losses. The same can be checked by random sampling and vouching

and verification.

2. The auditor also needs to verify on cut-off date considered for each of the reporting and

accounting and if the classification of incomes and expenses and its presentation is done in

compliance with the Australian Accounting standards and the local GAAP. It can be checked by

reviewing the appropriateness of disclosures and notes to accounts and whether the supporting

evidences have been produced (Knechel & Salterio, 2016).

3. The company has also used a number of valuation techniques and particularly fair valuation in

case of financial instruments and therefore the auditor should use services of the expert to do

the audit for valuation appropriateness.

Section 3: Cash flow analysis

In terms of the cash flow statement, the greatest category in terms of cash inflows was financing activity

whereas the greatest contributor in terms of cash outflow was operating activities (Fukukawa & Mock,

2011).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Furthermore, the majority of cash receipt comes from interest receipt, net trading income, proceeds

from the disposals and maturities and inflow from bond issue, notes and subordinate debts. On the

other hand, the primary cash payments included interest payments, the operating expenses and the

income tax, the loans repayment, the purchases of the debt instruments, purchase of PPE and software.

It also included repayment of the bonds, notes and subordinate debts and also the dividend repayments

(Linden & Freeman, 2017).

The main non cash financial and investing activities included investment in the dividend reinvestment

plan and subordinated medium term notes reinvestment offer, the non-cash collateral amounts which

were either received or pledged, changes in the fair value of hedges, foreign currency translation and

other related adjustments. These where the major non cash transactions and therefore does not finds a

place in the cash flow statements (Dichev, 2017).

Based on the cash flow status of the company, the going concern assumption holds good for the entity

as it has had positive business in the past and is also having positive cash flow impact from operating

activities and financing activities. However, still in order to be sure, the auditor should check and employ

procedures for reviewing the liquidity and solvency position of company, the negative trend in the

operating cash flow category, whether the loans and advances are realizable and is there any long term

commitment by the company (Raiborn, Butler, & Martin, 2016).

Audit Report analysis

The audit of National Australia Bank has been conducted by EY and they have given a clear opinion on

the set of financial statements. They have mentioned that the company has complied with Corporation

Act 2001 while preparation and presentation of financial statements and it gives true and fair view and

has also complied with the Australian Accounting Standards. They also do believe that the audit

evidence found were sufficient and appropriate in establishing such an opinion.

There were some key audit issues which has been highlighted in a separate section in Audit report under

KAM. Some of them included

1. calculation of provision for credit impairment on loans at amortized costs – its quantum and

timing – for this the auditors specifically checked the expected credit loss model of the

company, effectiveness of relevant controls, sample checking, significant modelling

assumptions, processes used to identify it and the sufficiency and adequacy of the same

(Mubako & O'Donnell, 2018).

2. Restructuring Provision: this was significant in terms of measurement, recognition and

disclosure – the same was assessed by auditor by analyzing the restructuring plan of the

company, assessing the key assumptions and selecting a sample for restructuring costs

(Kangarluie & Aalizadeh, 2017).

3. Information technology systems and controls over financial reporting: since the process is

heavily reliant on the IT controls and the automated processes in the company – This was

checked by auditors with the help of IT specialists.

Conclusion

The extensive analysis of the annual report of the company was done and it was found that the

company has had sharp decline in 2016 but since then the company has improved. The auditors have

issued clean report but there are a few issues which needs to be assessed and checked further. The cash

from the disposals and maturities and inflow from bond issue, notes and subordinate debts. On the

other hand, the primary cash payments included interest payments, the operating expenses and the

income tax, the loans repayment, the purchases of the debt instruments, purchase of PPE and software.

It also included repayment of the bonds, notes and subordinate debts and also the dividend repayments

(Linden & Freeman, 2017).

The main non cash financial and investing activities included investment in the dividend reinvestment

plan and subordinated medium term notes reinvestment offer, the non-cash collateral amounts which

were either received or pledged, changes in the fair value of hedges, foreign currency translation and

other related adjustments. These where the major non cash transactions and therefore does not finds a

place in the cash flow statements (Dichev, 2017).

Based on the cash flow status of the company, the going concern assumption holds good for the entity

as it has had positive business in the past and is also having positive cash flow impact from operating

activities and financing activities. However, still in order to be sure, the auditor should check and employ

procedures for reviewing the liquidity and solvency position of company, the negative trend in the

operating cash flow category, whether the loans and advances are realizable and is there any long term

commitment by the company (Raiborn, Butler, & Martin, 2016).

Audit Report analysis

The audit of National Australia Bank has been conducted by EY and they have given a clear opinion on

the set of financial statements. They have mentioned that the company has complied with Corporation

Act 2001 while preparation and presentation of financial statements and it gives true and fair view and

has also complied with the Australian Accounting Standards. They also do believe that the audit

evidence found were sufficient and appropriate in establishing such an opinion.

There were some key audit issues which has been highlighted in a separate section in Audit report under

KAM. Some of them included

1. calculation of provision for credit impairment on loans at amortized costs – its quantum and

timing – for this the auditors specifically checked the expected credit loss model of the

company, effectiveness of relevant controls, sample checking, significant modelling

assumptions, processes used to identify it and the sufficiency and adequacy of the same

(Mubako & O'Donnell, 2018).

2. Restructuring Provision: this was significant in terms of measurement, recognition and

disclosure – the same was assessed by auditor by analyzing the restructuring plan of the

company, assessing the key assumptions and selecting a sample for restructuring costs

(Kangarluie & Aalizadeh, 2017).

3. Information technology systems and controls over financial reporting: since the process is

heavily reliant on the IT controls and the automated processes in the company – This was

checked by auditors with the help of IT specialists.

Conclusion

The extensive analysis of the annual report of the company was done and it was found that the

company has had sharp decline in 2016 but since then the company has improved. The auditors have

issued clean report but there are a few issues which needs to be assessed and checked further. The cash

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

flow status of the company was also analyzed and found that the company is a going concern based on

the same.

References

Annual Report (2018), National Australia Bank.

Annual Report (2017), National Australia Bank.

Annual Report (2016), National Australia Bank.

Annual Report (2015), National Australia Bank.

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-

431.

Alieid, E. E. (2016). The Role of Accounting Information Systems in Making Investment Decisions.

Internal Auditing & Risk Management, 11(2), 233-242.

Arnott, D., Lizama, F., & Song, Y. (2017). Patterns of business intelligence systems use in organizations.

Decision Support Systems, 97, 58-68.

Dichev, I. (2017). On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), 617-632. doi:https://doi.org/10.1080/00014788.2017.1299620

Fukukawa, H., & Mock, T. (2011). Audit risk assessments using belief versus probability. Auditing: A

Journal of Practice & Theory, 30(1), 75-99.

Goldmann, K. (2016). Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4(3), 103-112.

Grenier, J. (2017). Encouraging Professional Skepticism in the Industry Specialization Era. Journal of

Business Ethics, 142(2), 241-256.

Jefferson, M. (2017). Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland .

Technological Forecasting and Social Change, 353-354.

Kangarluie, S., & Aalizadeh, A. (2017). 'The expectation gap in auditing. Accounting, 3(1), 19-22.

Knechel, W., & Salterio, S. (2016). Auditing:Assurance and Risk (4th ed.). New York: Routledge.

Linden, B., & Freeman, R. (2017). Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), 353-379. Retrieved from https://doi.org/10.1017/beq.2017.1

Mubako, G., & O'Donnell, E. (2018). Effect of fraud risk assessments on auditor skepticism: Unintended

consequences on evidence evaluation. International Journal of Auditing, 22(1), 55-64.

the same.

References

Annual Report (2018), National Australia Bank.

Annual Report (2017), National Australia Bank.

Annual Report (2016), National Australia Bank.

Annual Report (2015), National Australia Bank.

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-

431.

Alieid, E. E. (2016). The Role of Accounting Information Systems in Making Investment Decisions.

Internal Auditing & Risk Management, 11(2), 233-242.

Arnott, D., Lizama, F., & Song, Y. (2017). Patterns of business intelligence systems use in organizations.

Decision Support Systems, 97, 58-68.

Dichev, I. (2017). On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), 617-632. doi:https://doi.org/10.1080/00014788.2017.1299620

Fukukawa, H., & Mock, T. (2011). Audit risk assessments using belief versus probability. Auditing: A

Journal of Practice & Theory, 30(1), 75-99.

Goldmann, K. (2016). Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4(3), 103-112.

Grenier, J. (2017). Encouraging Professional Skepticism in the Industry Specialization Era. Journal of

Business Ethics, 142(2), 241-256.

Jefferson, M. (2017). Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland .

Technological Forecasting and Social Change, 353-354.

Kangarluie, S., & Aalizadeh, A. (2017). 'The expectation gap in auditing. Accounting, 3(1), 19-22.

Knechel, W., & Salterio, S. (2016). Auditing:Assurance and Risk (4th ed.). New York: Routledge.

Linden, B., & Freeman, R. (2017). Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), 353-379. Retrieved from https://doi.org/10.1017/beq.2017.1

Mubako, G., & O'Donnell, E. (2018). Effect of fraud risk assessments on auditor skepticism: Unintended

consequences on evidence evaluation. International Journal of Auditing, 22(1), 55-64.

Raiborn, C., Butler, J., & Martin, K. (2016). The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), 10-21.

Visinescu, L., Jones, M., & Sidorova, A. (2017). Improving Decision Quality: The Role of Business

Intelligence. Journal of Computer Information Systems, 57(1), 58-66.

Werner, M. (2017). Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, 25(1), 57-80.

Governance. Journal of Corporate Accounting and Finance, 28(2), 10-21.

Visinescu, L., Jones, M., & Sidorova, A. (2017). Improving Decision Quality: The Role of Business

Intelligence. Journal of Computer Information Systems, 57(1), 58-66.

Werner, M. (2017). Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, 25(1), 57-80.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.