Analysis of NAB's Dividend Cut: Financial Performance Report

VerifiedAdded on 2023/04/19

|5

|1454

|135

Report

AI Summary

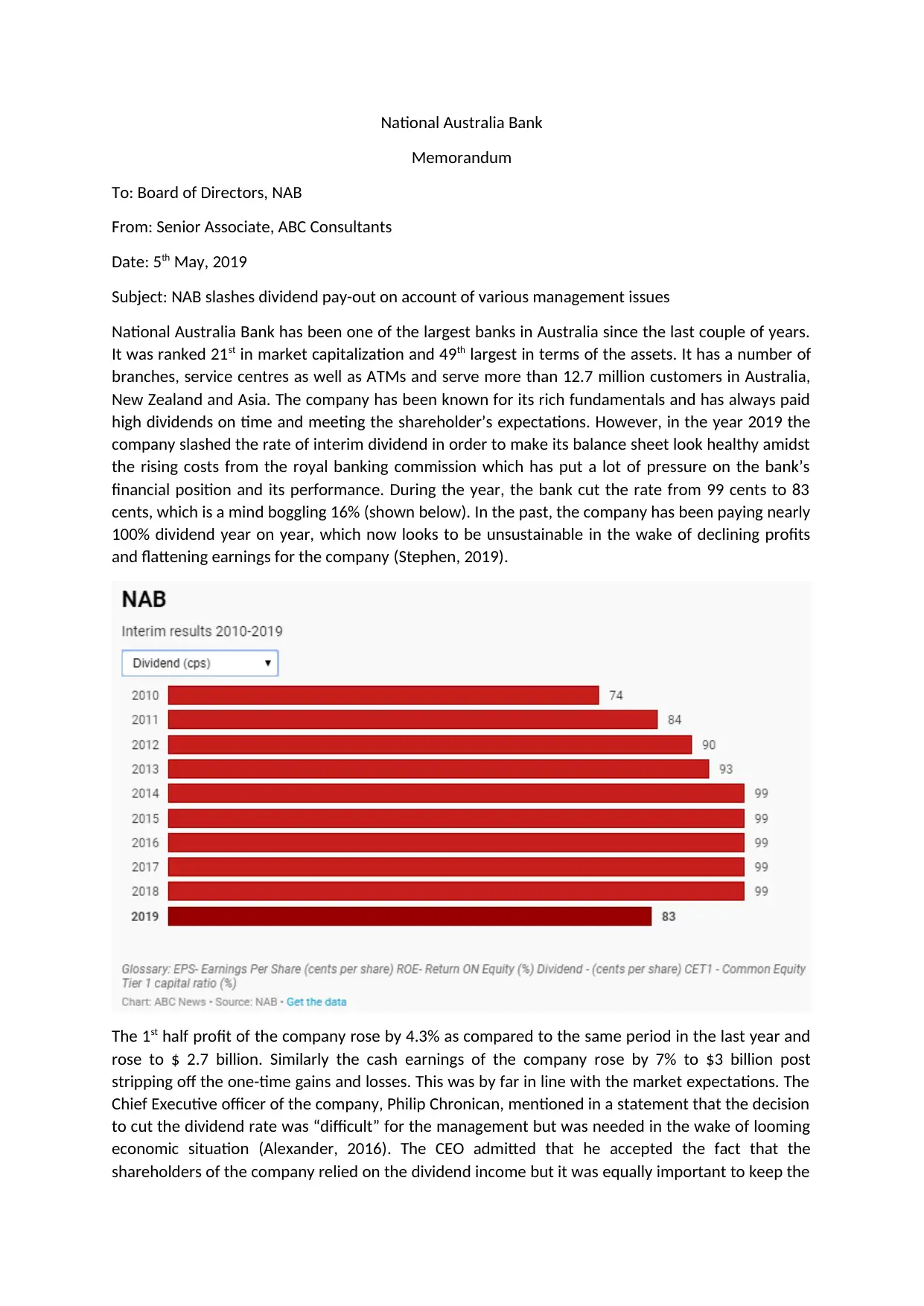

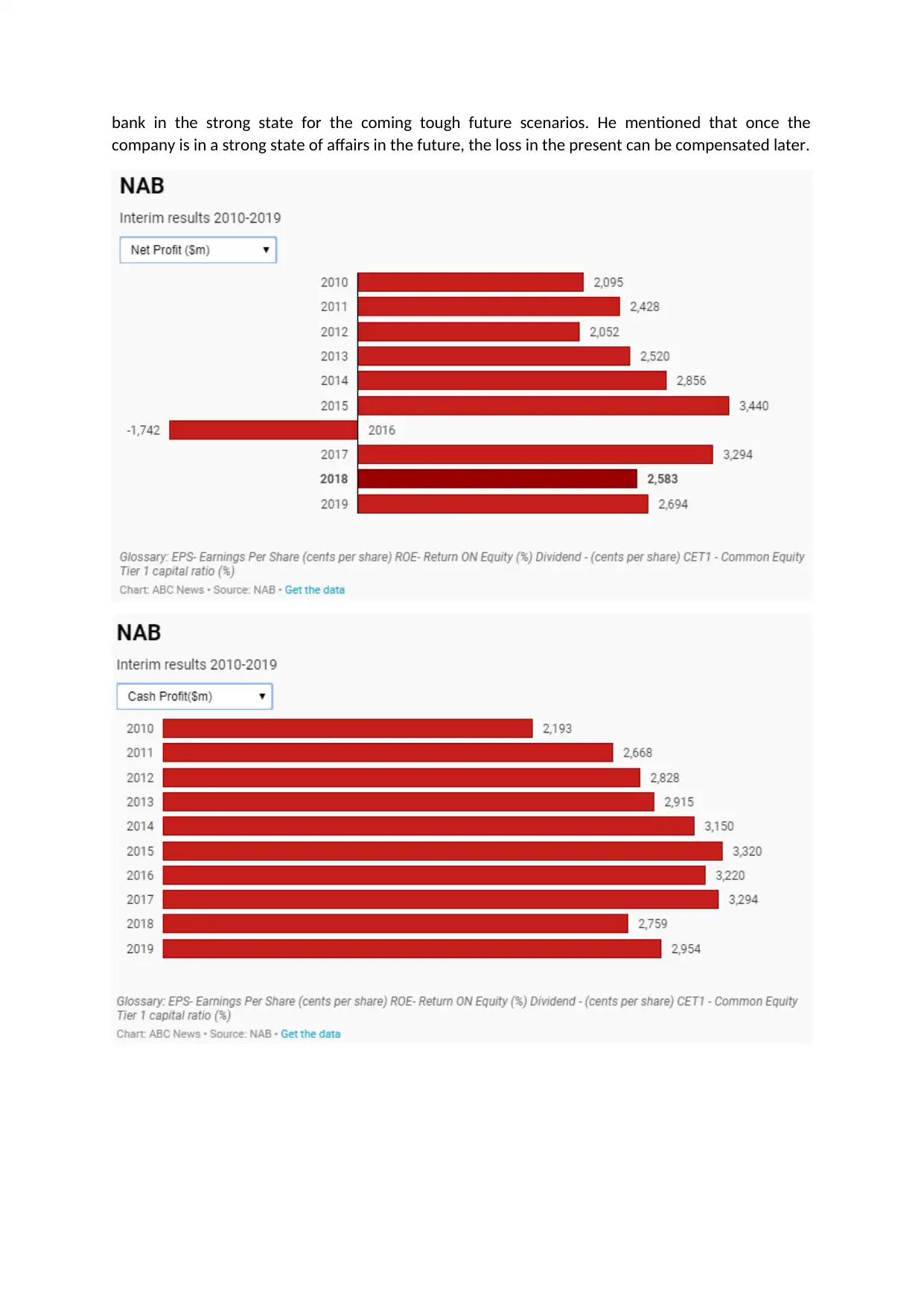

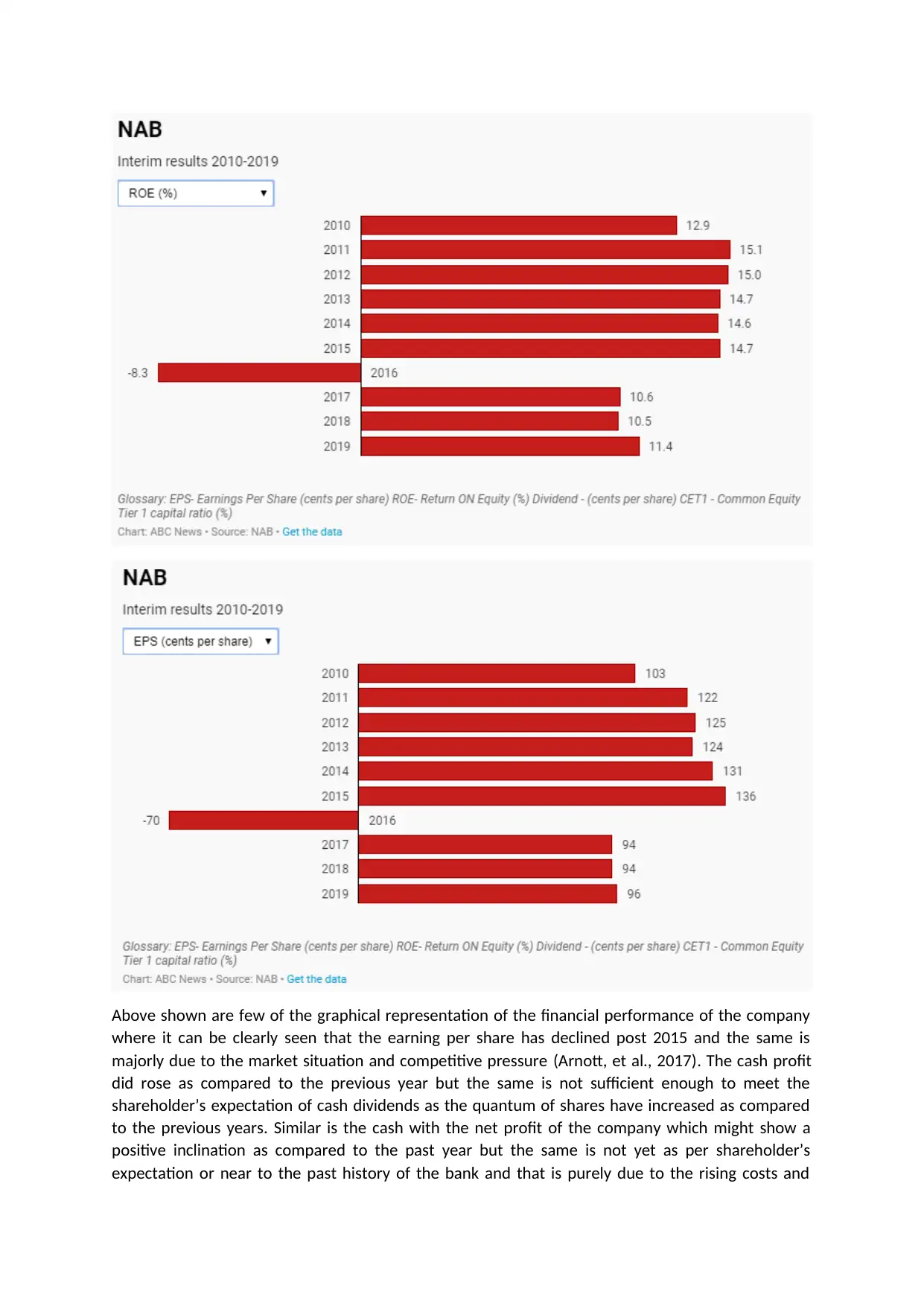

This report analyzes the decision of the National Australia Bank (NAB) to slash its dividend payout in 2019. The memorandum, addressed to the Board of Directors, highlights various management issues contributing to this decision. Key factors include rising costs from the Royal Banking Commission, declining profits, and flattening earnings. The bank's CEO cited the need to strengthen the balance sheet amidst a challenging economic environment. The report details the decline in earnings per share, rising impairment charges due to mortgage delinquencies, and falling housing prices. It also discusses the impact of past financial scandals and the need for accurate cost estimation and strategic revisions. Despite these challenges, NAB's performance remains relatively strong compared to its peers. The report concludes by emphasizing the importance of prudent financial management in navigating current market conditions.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.