Detailed Analysis of Tax Policy: Negative Gearing and CGT Reforms

VerifiedAdded on 2023/06/07

|8

|2121

|216

Report

AI Summary

This report analyzes the implications of Australia's tax policy on negative gearing, focusing on the Labor Party's proposal to limit negative gearing to new housing and halve the capital gains tax discount. The report examines the significance of the policy issue, key stakeholders (investors, homeowners, government, and the economy), and identifies winners (small-time investors, lower-income investors, and the government) and losers (landlords, high-earners). It further explores the implications for accounting and taxation, including changes to imputation credits and depreciation, and the impact on the Australian Taxation Office (ATO), particularly regarding the analysis of the effective limitations on negative gearing and communication with investors. The report references various sources to support its analysis and provides insights into the potential effects of the proposed tax reforms on the housing market, government revenue, and intergenerational equality.

TAX POLICY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Task 1: Significance of the Tax Policy Issue...............................................................................................1

Task 2: Key Stakeholders of the Policy and Impact on them.......................................................................1

Task 3: Winner and Losers..........................................................................................................................2

Task 4: Implications for accounting and taxation........................................................................................3

Task 5: Impact on ATO...............................................................................................................................3

References...................................................................................................................................................5

Task 1: Significance of the Tax Policy Issue...............................................................................................1

Task 2: Key Stakeholders of the Policy and Impact on them.......................................................................1

Task 3: Winner and Losers..........................................................................................................................2

Task 4: Implications for accounting and taxation........................................................................................3

Task 5: Impact on ATO...............................................................................................................................3

References...................................................................................................................................................5

Task 1: Significance of the Tax Policy Issue

This tax policy issue is significant because it is important to make sure that Australia’s tax

system is sustainable, just and aimed at growth and jobs. Negative gearing and Capital Gains Tax

(CGT) discount encourage real-estate investors (housing) to take debt. This reduces the stability

of the housing market and crowds out 1st house purchasers. Limiting the negative gearing

deductions on just purchased rental housing will place comparatively modest downward pressure

on prices of the house. These loopholes in taxation and concessions benefit the rich (Dixon,

2018). Hence this issue is critical in terms of greater fiscal repair in the country.

Task 2: Key Stakeholders of the Policy and Impact on them

Investors and homeowners – The main benefit of the tax reform would be for any

individual/group purchasing already-built properties. The proposal is probably to take some of

the heat from the competition for established houses as investors turn their focus toward off-the-

plan properties. Younger Australians are likely to get the greatest benefits. First home purchasers

will not have to contend with investors for established homes any more. Australians belonging to

the age group 45 and above will be the most negatively geared. Home builders and property

developers can also reap some benefits from the plan (Yardney, 2018). With investors removed

from the market for established homes, new stock will be in greater demand. This can lead to

higher investment in greenfield property development. Further, decreasing the discount on

capital gains tax will result in higher income people paying greater CGT. This will decrease the

variance between the tax paid by lower and higher income rental investors. Thus, this would

alleviate inequalities in the existing system. A steady and staged transition will have little effect

on average Australians, but it would enhance access to suitable, safe and affordable housing.

This will benefit the Australian community’s well-being (Grattan, 2016).

Government and the economy – A reduced CGT discount for investors implies more tax payable.

This means more tax revenue for the government, which can be re-employed toward education,

welfare and housing initiatives. Reform of negative gearing can save the government A$1.7bn

from the yearly AUS$3.04bn cost of negative gearing deductions, without damaging “mum and

dad investors.” The key is incremental transformation. Steady reform over 10 years or more

reduces the burden on government budgets (Tacadena, 2018). In the long-run, setting-up an

1

This tax policy issue is significant because it is important to make sure that Australia’s tax

system is sustainable, just and aimed at growth and jobs. Negative gearing and Capital Gains Tax

(CGT) discount encourage real-estate investors (housing) to take debt. This reduces the stability

of the housing market and crowds out 1st house purchasers. Limiting the negative gearing

deductions on just purchased rental housing will place comparatively modest downward pressure

on prices of the house. These loopholes in taxation and concessions benefit the rich (Dixon,

2018). Hence this issue is critical in terms of greater fiscal repair in the country.

Task 2: Key Stakeholders of the Policy and Impact on them

Investors and homeowners – The main benefit of the tax reform would be for any

individual/group purchasing already-built properties. The proposal is probably to take some of

the heat from the competition for established houses as investors turn their focus toward off-the-

plan properties. Younger Australians are likely to get the greatest benefits. First home purchasers

will not have to contend with investors for established homes any more. Australians belonging to

the age group 45 and above will be the most negatively geared. Home builders and property

developers can also reap some benefits from the plan (Yardney, 2018). With investors removed

from the market for established homes, new stock will be in greater demand. This can lead to

higher investment in greenfield property development. Further, decreasing the discount on

capital gains tax will result in higher income people paying greater CGT. This will decrease the

variance between the tax paid by lower and higher income rental investors. Thus, this would

alleviate inequalities in the existing system. A steady and staged transition will have little effect

on average Australians, but it would enhance access to suitable, safe and affordable housing.

This will benefit the Australian community’s well-being (Grattan, 2016).

Government and the economy – A reduced CGT discount for investors implies more tax payable.

This means more tax revenue for the government, which can be re-employed toward education,

welfare and housing initiatives. Reform of negative gearing can save the government A$1.7bn

from the yearly AUS$3.04bn cost of negative gearing deductions, without damaging “mum and

dad investors.” The key is incremental transformation. Steady reform over 10 years or more

reduces the burden on government budgets (Tacadena, 2018). In the long-run, setting-up an

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

extensive property tax is fairer and more effective than state governments relying on stamp duty

forever. Yearly tax rates in the 1st year of the change differ from AUS$47 in Tasmania to

AUS$129 in NSW which will finance a 10% reduction in stamp duties. To completely finance

the removal of stamp duty, the yearly property tax will need to rise to AUS$472 in Tasmania and

AUS$1,293 in NSW over ten years. For the government, this will be income neutral, but the

inclusive tax-burden will move from new home buyers to the ones who already have houses

(AHURI, 2018). This will not just enhance intergenerational equality but will offer a more stable

income for the state governments. However, real-estate is among the main sectors propelling the

Australian economy. Any apparent risk to profitability may witness investors fleeing the market.

this can have grave economic implications.

Task 3: Winner and Losers

Small-time and lower income investors plus the government will emerge as the winner of this

reformed policy. Around 3 quarters of the country’s families will be better off if negative gearing

is limited. Owner-occupiers and renters are winners, but landlords, particularly high-earners lose.

Improvements in the rate of home-ownership will largely be among middle-aged and young

families who are comparatively poor (Doherty, 2018).

There are worries that revising negative gearing will hamper the economic wellbeing of small-

time investors. However, employing data on the distribution of income and property renders it

plausible to differentiate between wealthy and poor investors, enabling the government to target

the restructurings to cushion the blow for low-income investors. Given this change will be less

likely to harm lower-income investors, they will be less likely to move away from the rental

market as opposed to if negative gearing was altogether removed. This will also alleviate the

effect of negative gearing changes on renters (Schlesinger, 2016).

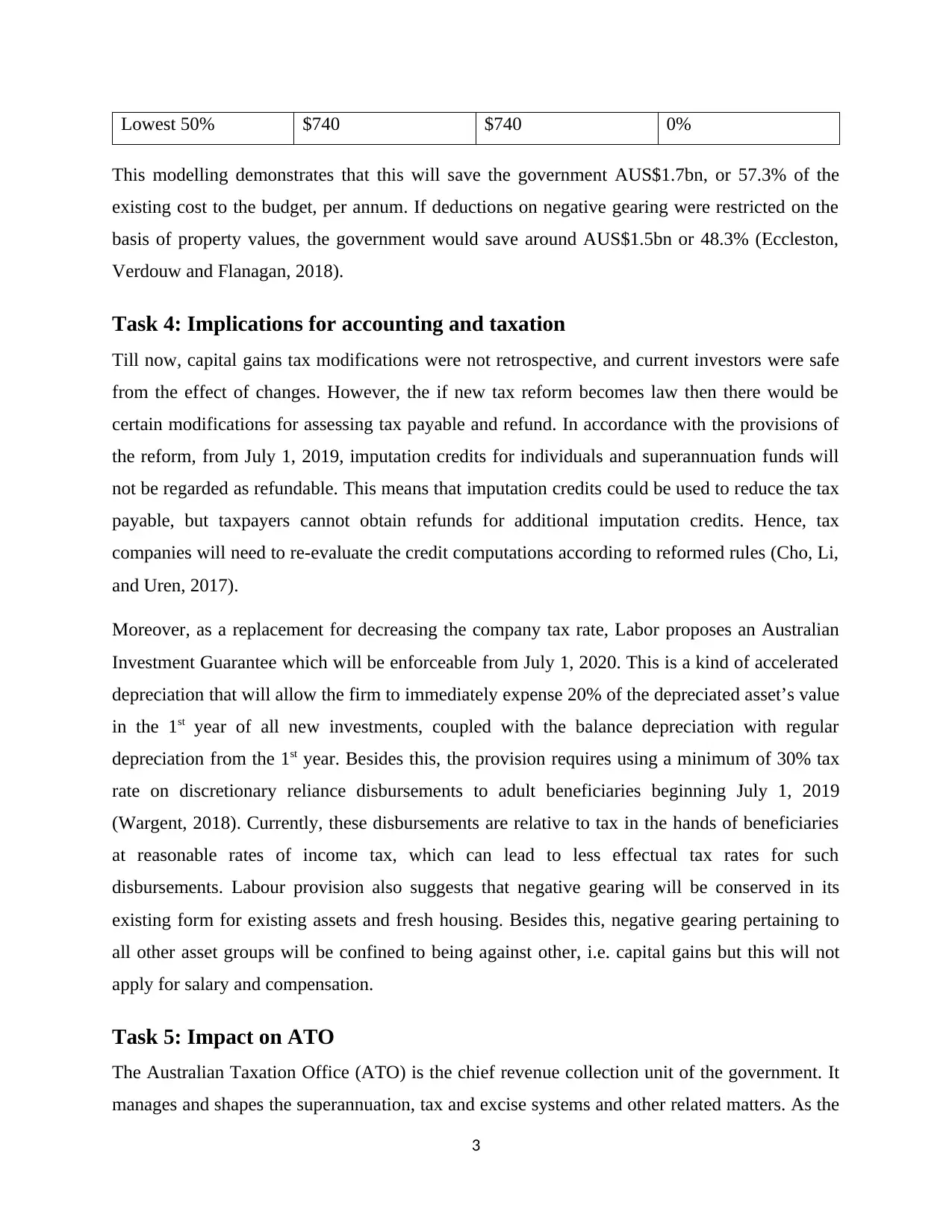

The government will also surface as a winner of this policy. Modelling of a proposed scenario is

shown below:

Income percentile Existing tax savings Tax savings post

changes

% change in tax

savings

Highest 25% $3,150 $0 -100%

50-75% $2,360 $1,200 -.49.15%

2

forever. Yearly tax rates in the 1st year of the change differ from AUS$47 in Tasmania to

AUS$129 in NSW which will finance a 10% reduction in stamp duties. To completely finance

the removal of stamp duty, the yearly property tax will need to rise to AUS$472 in Tasmania and

AUS$1,293 in NSW over ten years. For the government, this will be income neutral, but the

inclusive tax-burden will move from new home buyers to the ones who already have houses

(AHURI, 2018). This will not just enhance intergenerational equality but will offer a more stable

income for the state governments. However, real-estate is among the main sectors propelling the

Australian economy. Any apparent risk to profitability may witness investors fleeing the market.

this can have grave economic implications.

Task 3: Winner and Losers

Small-time and lower income investors plus the government will emerge as the winner of this

reformed policy. Around 3 quarters of the country’s families will be better off if negative gearing

is limited. Owner-occupiers and renters are winners, but landlords, particularly high-earners lose.

Improvements in the rate of home-ownership will largely be among middle-aged and young

families who are comparatively poor (Doherty, 2018).

There are worries that revising negative gearing will hamper the economic wellbeing of small-

time investors. However, employing data on the distribution of income and property renders it

plausible to differentiate between wealthy and poor investors, enabling the government to target

the restructurings to cushion the blow for low-income investors. Given this change will be less

likely to harm lower-income investors, they will be less likely to move away from the rental

market as opposed to if negative gearing was altogether removed. This will also alleviate the

effect of negative gearing changes on renters (Schlesinger, 2016).

The government will also surface as a winner of this policy. Modelling of a proposed scenario is

shown below:

Income percentile Existing tax savings Tax savings post

changes

% change in tax

savings

Highest 25% $3,150 $0 -100%

50-75% $2,360 $1,200 -.49.15%

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Lowest 50% $740 $740 0%

This modelling demonstrates that this will save the government AUS$1.7bn, or 57.3% of the

existing cost to the budget, per annum. If deductions on negative gearing were restricted on the

basis of property values, the government would save around AUS$1.5bn or 48.3% (Eccleston,

Verdouw and Flanagan, 2018).

Task 4: Implications for accounting and taxation

Till now, capital gains tax modifications were not retrospective, and current investors were safe

from the effect of changes. However, the if new tax reform becomes law then there would be

certain modifications for assessing tax payable and refund. In accordance with the provisions of

the reform, from July 1, 2019, imputation credits for individuals and superannuation funds will

not be regarded as refundable. This means that imputation credits could be used to reduce the tax

payable, but taxpayers cannot obtain refunds for additional imputation credits. Hence, tax

companies will need to re-evaluate the credit computations according to reformed rules (Cho, Li,

and Uren, 2017).

Moreover, as a replacement for decreasing the company tax rate, Labor proposes an Australian

Investment Guarantee which will be enforceable from July 1, 2020. This is a kind of accelerated

depreciation that will allow the firm to immediately expense 20% of the depreciated asset’s value

in the 1st year of all new investments, coupled with the balance depreciation with regular

depreciation from the 1st year. Besides this, the provision requires using a minimum of 30% tax

rate on discretionary reliance disbursements to adult beneficiaries beginning July 1, 2019

(Wargent, 2018). Currently, these disbursements are relative to tax in the hands of beneficiaries

at reasonable rates of income tax, which can lead to less effectual tax rates for such

disbursements. Labour provision also suggests that negative gearing will be conserved in its

existing form for existing assets and fresh housing. Besides this, negative gearing pertaining to

all other asset groups will be confined to being against other, i.e. capital gains but this will not

apply for salary and compensation.

Task 5: Impact on ATO

The Australian Taxation Office (ATO) is the chief revenue collection unit of the government. It

manages and shapes the superannuation, tax and excise systems and other related matters. As the

3

This modelling demonstrates that this will save the government AUS$1.7bn, or 57.3% of the

existing cost to the budget, per annum. If deductions on negative gearing were restricted on the

basis of property values, the government would save around AUS$1.5bn or 48.3% (Eccleston,

Verdouw and Flanagan, 2018).

Task 4: Implications for accounting and taxation

Till now, capital gains tax modifications were not retrospective, and current investors were safe

from the effect of changes. However, the if new tax reform becomes law then there would be

certain modifications for assessing tax payable and refund. In accordance with the provisions of

the reform, from July 1, 2019, imputation credits for individuals and superannuation funds will

not be regarded as refundable. This means that imputation credits could be used to reduce the tax

payable, but taxpayers cannot obtain refunds for additional imputation credits. Hence, tax

companies will need to re-evaluate the credit computations according to reformed rules (Cho, Li,

and Uren, 2017).

Moreover, as a replacement for decreasing the company tax rate, Labor proposes an Australian

Investment Guarantee which will be enforceable from July 1, 2020. This is a kind of accelerated

depreciation that will allow the firm to immediately expense 20% of the depreciated asset’s value

in the 1st year of all new investments, coupled with the balance depreciation with regular

depreciation from the 1st year. Besides this, the provision requires using a minimum of 30% tax

rate on discretionary reliance disbursements to adult beneficiaries beginning July 1, 2019

(Wargent, 2018). Currently, these disbursements are relative to tax in the hands of beneficiaries

at reasonable rates of income tax, which can lead to less effectual tax rates for such

disbursements. Labour provision also suggests that negative gearing will be conserved in its

existing form for existing assets and fresh housing. Besides this, negative gearing pertaining to

all other asset groups will be confined to being against other, i.e. capital gains but this will not

apply for salary and compensation.

Task 5: Impact on ATO

The Australian Taxation Office (ATO) is the chief revenue collection unit of the government. It

manages and shapes the superannuation, tax and excise systems and other related matters. As the

3

chief revenue collection wing of the government, ATO levies an income tax, GST and other

federal taxes. The reformed tax policy will have a significant impact on the work of ATO. Its

liability will increase pertaining to analysis of the effectual limitation on negative gearing

(Pawson, 2018).

A decline in the CGT discount will affect rental investors of the high-income group to a great

extent as compared to low-income investors. This will bridge the gap in user cost pressures

which higher and lower income rental investors bear. Due to such variance between dollar value

effect and percentage, the new policy will have to be cautiously communicated to prevent

confusion that the effect of the CGT amendment is probable to be regressive in context of its

likely impact on rental investors’ incomes. Hence, the ATO will be accountable for

communicating to the investors about the changes in a manner that confine the threat of a shock

to the market, if investors decide to leave the housing market (AHURI, 2018). Till now,

policymakers have shown reluctance in modifying the core set of the tax system, but ATO will

have to do it in a manner that reduces the effect on lower-income investors.

The chief goal of the ATO is to help people comprehend their rights and duties, besides offering

ease of compliance and access to benefits pertaining to abidance of law. Hence, ATO will give

hands-on guidelines for taxpayers to help them take relevant decisions. Besides this, the agency

will also need to counsel about the administrative approach pertaining to specific changes. For

e.g., as in the current case, the explanation needs to be given that losses from new stock

investments and current properties can apply for adjustments against tax liabilities.

4

federal taxes. The reformed tax policy will have a significant impact on the work of ATO. Its

liability will increase pertaining to analysis of the effectual limitation on negative gearing

(Pawson, 2018).

A decline in the CGT discount will affect rental investors of the high-income group to a great

extent as compared to low-income investors. This will bridge the gap in user cost pressures

which higher and lower income rental investors bear. Due to such variance between dollar value

effect and percentage, the new policy will have to be cautiously communicated to prevent

confusion that the effect of the CGT amendment is probable to be regressive in context of its

likely impact on rental investors’ incomes. Hence, the ATO will be accountable for

communicating to the investors about the changes in a manner that confine the threat of a shock

to the market, if investors decide to leave the housing market (AHURI, 2018). Till now,

policymakers have shown reluctance in modifying the core set of the tax system, but ATO will

have to do it in a manner that reduces the effect on lower-income investors.

The chief goal of the ATO is to help people comprehend their rights and duties, besides offering

ease of compliance and access to benefits pertaining to abidance of law. Hence, ATO will give

hands-on guidelines for taxpayers to help them take relevant decisions. Besides this, the agency

will also need to counsel about the administrative approach pertaining to specific changes. For

e.g., as in the current case, the explanation needs to be given that losses from new stock

investments and current properties can apply for adjustments against tax liabilities.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

AHURI. 2018. Modelling negative gearing and capital gains tax reforms. [pdf]. Available

through: <https://www.ahuri.edu.au/__data/assets/pdf_file/0027/16488/PES-004-Modelling-

negative-gearing-and-capital-gains-tax-reforms.pdf>. [Accessed on 11 September 2018].

Cho, Y., Li, S. and Uren, L., 2017. Negative Gearing and Welfare: A Quantitative Study for the

Australian Housing Market. Monash University.

Dixon, D., 2018. Prepare for changes to negative gearing and capital gains tax. The Sydney

Morning Herald. [Online]. Available through: <https://www.smh.com.au/money/prepare-for-

changes-to-negative-gearing-and-capital-gains-tax-20180126-h0otyp.html>. [Accessed on 11

September 2018].

Doherty, B., 2018. Home ownership would rise if negative gearing is scrapped, study says. The

Guardian. [Online]. Available through:

<https://www.theguardian.com/australia-news/2018/jan/13/australian-house-prices-will-fall-if-

negative-gearing-goes-study-says>. [Accessed on 11 September 2018].

Eccleston, R., Verdouw, J. and Flanagan, K., 2018. Gradual reform to capital gains, negative

gearing and stamp duty will make housing more affordable. [Online]. Available through:

<https://theconversation.com/gradual-reform-to-capital-gains-negative-gearing-and-stamp-duty-

will-make-housing-more-affordable-98933>. [Accessed on 11 September 2018].

Grattan, M., 2016. Shorten policy hits tax breaks for negative gearing and capital gains.

[Online]. Available through: <https://theconversation.com/shorten-policy-hits-tax-breaks-for-

negative-gearing-and-capital-gains-54700>. [Accessed on 11 September 2018].

Pawson, I., 2018. Reframing Australia's housing affordability problem: The politics and

economics of negative gearing. Journal of Australian Political Economy, The, (81), p.121.

Schlesinger, L., 2016. What negative gearing changes could mean to you. [Online]. Available

through: <https://www.afr.com/personal-finance/what-negative-gearing-changes-could-mean-to-

you-20160218-gmxe7v>. [Accessed on 11 September 2018].

Tacadena, G., 2018. Why the federal government needs to consider reforming negative gearing

policies. [Online]. Available through: <https://www.yourmortgage.com.au/mortgage-news/why-

the-federal-government-needs-to-consider-reforming-negative-gearing-policies/247472/>.

[Accessed on 11 September 2018].

Wargent, P., 2018. Impacts of Labor’s proposed negative gearing and CGT reforms. [Online].

Available through: <https://www.livewiremarkets.com/wires/impacts-of-labor-s-proposed-

negative-gearing-and-cgt-reforms>. [Accessed on 11 September 2018].

Yardney, M., 2018. The possible impacts of Labor’s proposed negative gearing and CGT

changes. [Online]. Available through:

5

AHURI. 2018. Modelling negative gearing and capital gains tax reforms. [pdf]. Available

through: <https://www.ahuri.edu.au/__data/assets/pdf_file/0027/16488/PES-004-Modelling-

negative-gearing-and-capital-gains-tax-reforms.pdf>. [Accessed on 11 September 2018].

Cho, Y., Li, S. and Uren, L., 2017. Negative Gearing and Welfare: A Quantitative Study for the

Australian Housing Market. Monash University.

Dixon, D., 2018. Prepare for changes to negative gearing and capital gains tax. The Sydney

Morning Herald. [Online]. Available through: <https://www.smh.com.au/money/prepare-for-

changes-to-negative-gearing-and-capital-gains-tax-20180126-h0otyp.html>. [Accessed on 11

September 2018].

Doherty, B., 2018. Home ownership would rise if negative gearing is scrapped, study says. The

Guardian. [Online]. Available through:

<https://www.theguardian.com/australia-news/2018/jan/13/australian-house-prices-will-fall-if-

negative-gearing-goes-study-says>. [Accessed on 11 September 2018].

Eccleston, R., Verdouw, J. and Flanagan, K., 2018. Gradual reform to capital gains, negative

gearing and stamp duty will make housing more affordable. [Online]. Available through:

<https://theconversation.com/gradual-reform-to-capital-gains-negative-gearing-and-stamp-duty-

will-make-housing-more-affordable-98933>. [Accessed on 11 September 2018].

Grattan, M., 2016. Shorten policy hits tax breaks for negative gearing and capital gains.

[Online]. Available through: <https://theconversation.com/shorten-policy-hits-tax-breaks-for-

negative-gearing-and-capital-gains-54700>. [Accessed on 11 September 2018].

Pawson, I., 2018. Reframing Australia's housing affordability problem: The politics and

economics of negative gearing. Journal of Australian Political Economy, The, (81), p.121.

Schlesinger, L., 2016. What negative gearing changes could mean to you. [Online]. Available

through: <https://www.afr.com/personal-finance/what-negative-gearing-changes-could-mean-to-

you-20160218-gmxe7v>. [Accessed on 11 September 2018].

Tacadena, G., 2018. Why the federal government needs to consider reforming negative gearing

policies. [Online]. Available through: <https://www.yourmortgage.com.au/mortgage-news/why-

the-federal-government-needs-to-consider-reforming-negative-gearing-policies/247472/>.

[Accessed on 11 September 2018].

Wargent, P., 2018. Impacts of Labor’s proposed negative gearing and CGT reforms. [Online].

Available through: <https://www.livewiremarkets.com/wires/impacts-of-labor-s-proposed-

negative-gearing-and-cgt-reforms>. [Accessed on 11 September 2018].

Yardney, M., 2018. The possible impacts of Labor’s proposed negative gearing and CGT

changes. [Online]. Available through:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

<https://www.smartcompany.com.au/industries/property/impacts-of-labors-proposed-negative-

gearing-and-cgt-changes/>. [Accessed on 11 September 2018].

6

gearing-and-cgt-changes/>. [Accessed on 11 September 2018].

6

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.