Nelson College, HND Business, Management Accounting Report Analysis

VerifiedAdded on 2022/12/28

|14

|3966

|58

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their application within a business context, using a case study scenario of Marshalls. It explores the requirements of different management accounting systems, including cost accounting, inventory management, job costing, and price optimization, highlighting their advantages and disadvantages. The report also details various types of management accounting reports, such as budget reports, cost reports, and performance reports, illustrating their significance in monitoring and evaluating a company's financial performance. Furthermore, the report includes an income statement comparing marginal and absorption costing methods, offering insights into their impact on profit calculation. Finally, the report examines the advantages and disadvantages of planning tools used for budgetary control and discusses how organizations adapt their management accounting systems to address financial challenges.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

P1 Management accounting requirements of different types of management accounting

systems.........................................................................................................................................3

P2 Different types of management accounting reports................................................................6

P3 Prepare an income statement using marginal and absorption costs.......................................7

P4 Advantages and disadvantages of planning tools used for budgetary control........................9

P5 How organisations are adapting management accounting systems to respond to financial

problems....................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

P1 Management accounting requirements of different types of management accounting

systems.........................................................................................................................................3

P2 Different types of management accounting reports................................................................6

P3 Prepare an income statement using marginal and absorption costs.......................................7

P4 Advantages and disadvantages of planning tools used for budgetary control........................9

P5 How organisations are adapting management accounting systems to respond to financial

problems....................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES................................................................................................................................1

INTRODUCTION

Management accounting (MA) perform series of functions defined as identification,,

analysing, recording and presenting financial information to the management for decision

making, planning and controlling functions. The present report is based on case study scenario

which explain about the various strategies pertaining to MA systems and their requirement in

business. The report will also discuss about the various kinds of management reports and

advantages of it. Further the project will highlight the marginal and absorption techniques of

costing. In addition to this it will also outline advantages and disadvantages of budgetary control

tools used for planning. At last comparison of management accounting system used for solving

financial problem will be undertaken.

MAIN BODY

P1 Necessity of management accounting in various types of accounting systems

MA refers to identification, analysis, interpretation and presentation of accounting

information in order to take decision for management of business (Abdusalomova, 2019). It

helps managers in the preparation of rules, policy, regulations and decision making process in

day to day dealings of company.

Role and Principle of management accounting

Relevance: the information on which management accounting is based must be relevant

and accurate (Ameen, Ahmed and Abd Hafez, 2018.). Management accounting take into

account accurate information relating to enterprise which assist in improving the quality

of decision making by management.

Influence: in management accounting emphasis is laid over communicating financial

information to managers and if there will be any issue then this will affect decision

making. Hence, the communication of information affects the working of management

accounting to a great extent.

Credibility: Management accounting experts are being ethical, responsible and aware

about the rules and regulations of corporate governance. If this is present, then the

information will be credible and can be used in taking effective decision.

Various kind of management accounting system

Management accounting (MA) perform series of functions defined as identification,,

analysing, recording and presenting financial information to the management for decision

making, planning and controlling functions. The present report is based on case study scenario

which explain about the various strategies pertaining to MA systems and their requirement in

business. The report will also discuss about the various kinds of management reports and

advantages of it. Further the project will highlight the marginal and absorption techniques of

costing. In addition to this it will also outline advantages and disadvantages of budgetary control

tools used for planning. At last comparison of management accounting system used for solving

financial problem will be undertaken.

MAIN BODY

P1 Necessity of management accounting in various types of accounting systems

MA refers to identification, analysis, interpretation and presentation of accounting

information in order to take decision for management of business (Abdusalomova, 2019). It

helps managers in the preparation of rules, policy, regulations and decision making process in

day to day dealings of company.

Role and Principle of management accounting

Relevance: the information on which management accounting is based must be relevant

and accurate (Ameen, Ahmed and Abd Hafez, 2018.). Management accounting take into

account accurate information relating to enterprise which assist in improving the quality

of decision making by management.

Influence: in management accounting emphasis is laid over communicating financial

information to managers and if there will be any issue then this will affect decision

making. Hence, the communication of information affects the working of management

accounting to a great extent.

Credibility: Management accounting experts are being ethical, responsible and aware

about the rules and regulations of corporate governance. If this is present, then the

information will be credible and can be used in taking effective decision.

Various kind of management accounting system

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting system used by different types of organisations in day to day

operations of business. MA systems and their role pertaining to organisational process belongs

to Marshall are discussed below:

Cost Accounting System: This system assists the firm in identification, estimation of

price of product, for valuation of stock, profitability and cost control (Jbarah, 2018). This

accounting system will individually measure and record the cost then comparing it with actual

results and prepare reports to assist the management of company. This system is the main key of

managerial accounting because it helps in analysing the tools like budgetary control and others

which are used for correct ascertainment cost of product. The chosen firm uses job based costing

and transportation costing system for measuring equipment, structural assessment of its cost of

product. The direct and indirect cost related to the manufacturing needs to be considered by the

accountant in this system. The benefit of using this system is find out per unit cost of product of

Marshall and based on its price can be set.

Advantages Disadvantages

It eliminates wastages and losses.

It helps in reduction of cost

It assist in control

Complex system

It requires additional step for checking

accuracy

Involved huge cost as it requires highly

skilled accountants

Inventory Management System: It refers to a process of ordering, storing of raw

material, WIP and producing finished goods and assure that right stock is produced at the right

place and time. Organisational process integrated by Marshall can be achieving by efficient and

effective flow of inventory in the firm. The main objective inventory system for Marshall is to

understand the present inventory level and minimize over and under stocks situations. The main

functions of inventory management system for Marshall is to request purchase orders, receiving

that order then relocating and adjusting inventory and at last disposing of inventory. This system

is using different methods for valuation of inventory like FIFO, LIFO, and AVCO.

Advantages Disadvantages

It integrates with accounting system It reduced physical audits

operations of business. MA systems and their role pertaining to organisational process belongs

to Marshall are discussed below:

Cost Accounting System: This system assists the firm in identification, estimation of

price of product, for valuation of stock, profitability and cost control (Jbarah, 2018). This

accounting system will individually measure and record the cost then comparing it with actual

results and prepare reports to assist the management of company. This system is the main key of

managerial accounting because it helps in analysing the tools like budgetary control and others

which are used for correct ascertainment cost of product. The chosen firm uses job based costing

and transportation costing system for measuring equipment, structural assessment of its cost of

product. The direct and indirect cost related to the manufacturing needs to be considered by the

accountant in this system. The benefit of using this system is find out per unit cost of product of

Marshall and based on its price can be set.

Advantages Disadvantages

It eliminates wastages and losses.

It helps in reduction of cost

It assist in control

Complex system

It requires additional step for checking

accuracy

Involved huge cost as it requires highly

skilled accountants

Inventory Management System: It refers to a process of ordering, storing of raw

material, WIP and producing finished goods and assure that right stock is produced at the right

place and time. Organisational process integrated by Marshall can be achieving by efficient and

effective flow of inventory in the firm. The main objective inventory system for Marshall is to

understand the present inventory level and minimize over and under stocks situations. The main

functions of inventory management system for Marshall is to request purchase orders, receiving

that order then relocating and adjusting inventory and at last disposing of inventory. This system

is using different methods for valuation of inventory like FIFO, LIFO, and AVCO.

Advantages Disadvantages

It integrates with accounting system It reduced physical audits

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

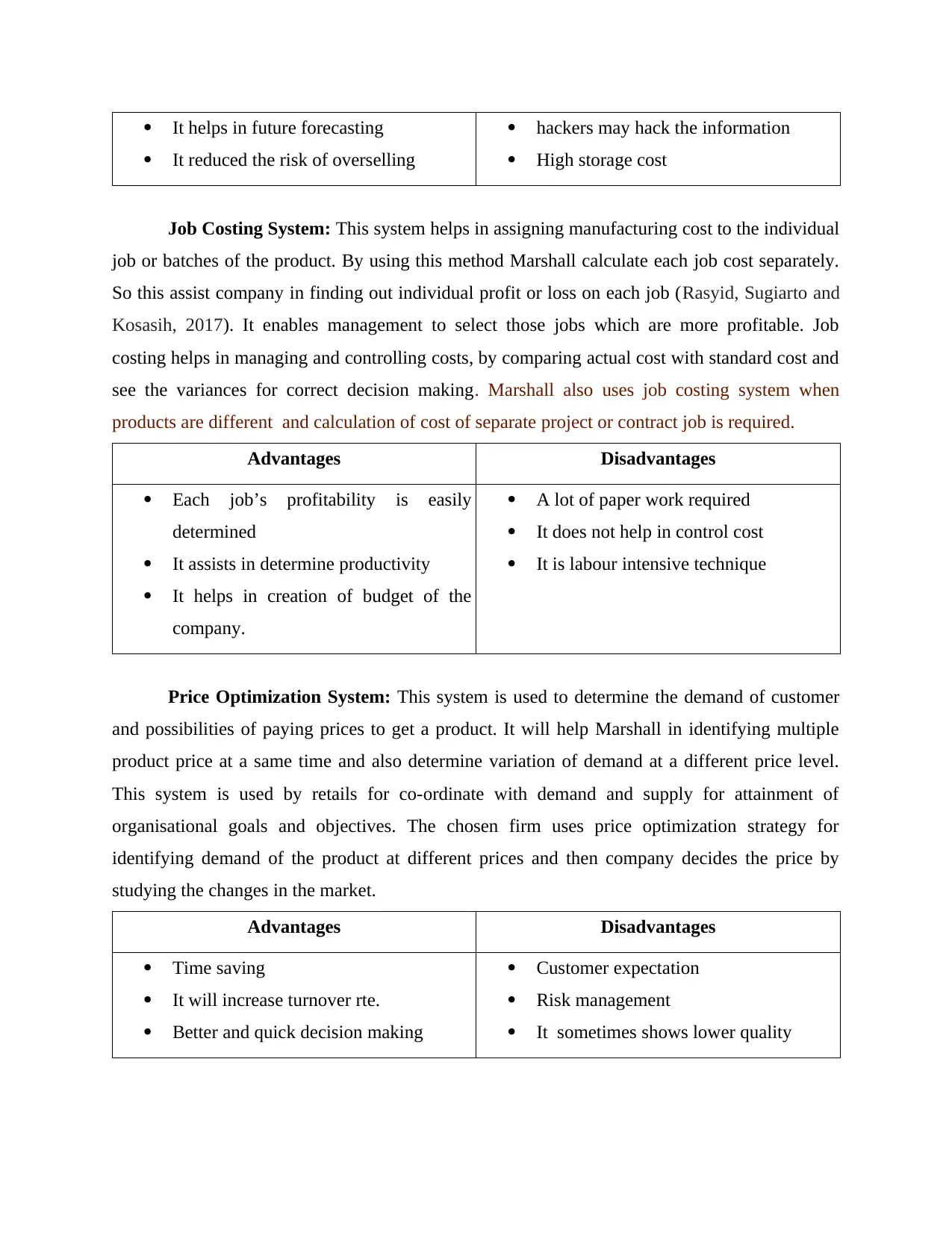

It helps in future forecasting

It reduced the risk of overselling

hackers may hack the information

High storage cost

Job Costing System: This system helps in assigning manufacturing cost to the individual

job or batches of the product. By using this method Marshall calculate each job cost separately.

So this assist company in finding out individual profit or loss on each job (Rasyid, Sugiarto and

Kosasih, 2017). It enables management to select those jobs which are more profitable. Job

costing helps in managing and controlling costs, by comparing actual cost with standard cost and

see the variances for correct decision making. Marshall also uses job costing system when

products are different and calculation of cost of separate project or contract job is required.

Advantages Disadvantages

Each job’s profitability is easily

determined

It assists in determine productivity

It helps in creation of budget of the

company.

A lot of paper work required

It does not help in control cost

It is labour intensive technique

Price Optimization System: This system is used to determine the demand of customer

and possibilities of paying prices to get a product. It will help Marshall in identifying multiple

product price at a same time and also determine variation of demand at a different price level.

This system is used by retails for co-ordinate with demand and supply for attainment of

organisational goals and objectives. The chosen firm uses price optimization strategy for

identifying demand of the product at different prices and then company decides the price by

studying the changes in the market.

Advantages Disadvantages

Time saving

It will increase turnover rte.

Better and quick decision making

Customer expectation

Risk management

It sometimes shows lower quality

It reduced the risk of overselling

hackers may hack the information

High storage cost

Job Costing System: This system helps in assigning manufacturing cost to the individual

job or batches of the product. By using this method Marshall calculate each job cost separately.

So this assist company in finding out individual profit or loss on each job (Rasyid, Sugiarto and

Kosasih, 2017). It enables management to select those jobs which are more profitable. Job

costing helps in managing and controlling costs, by comparing actual cost with standard cost and

see the variances for correct decision making. Marshall also uses job costing system when

products are different and calculation of cost of separate project or contract job is required.

Advantages Disadvantages

Each job’s profitability is easily

determined

It assists in determine productivity

It helps in creation of budget of the

company.

A lot of paper work required

It does not help in control cost

It is labour intensive technique

Price Optimization System: This system is used to determine the demand of customer

and possibilities of paying prices to get a product. It will help Marshall in identifying multiple

product price at a same time and also determine variation of demand at a different price level.

This system is used by retails for co-ordinate with demand and supply for attainment of

organisational goals and objectives. The chosen firm uses price optimization strategy for

identifying demand of the product at different prices and then company decides the price by

studying the changes in the market.

Advantages Disadvantages

Time saving

It will increase turnover rte.

Better and quick decision making

Customer expectation

Risk management

It sometimes shows lower quality

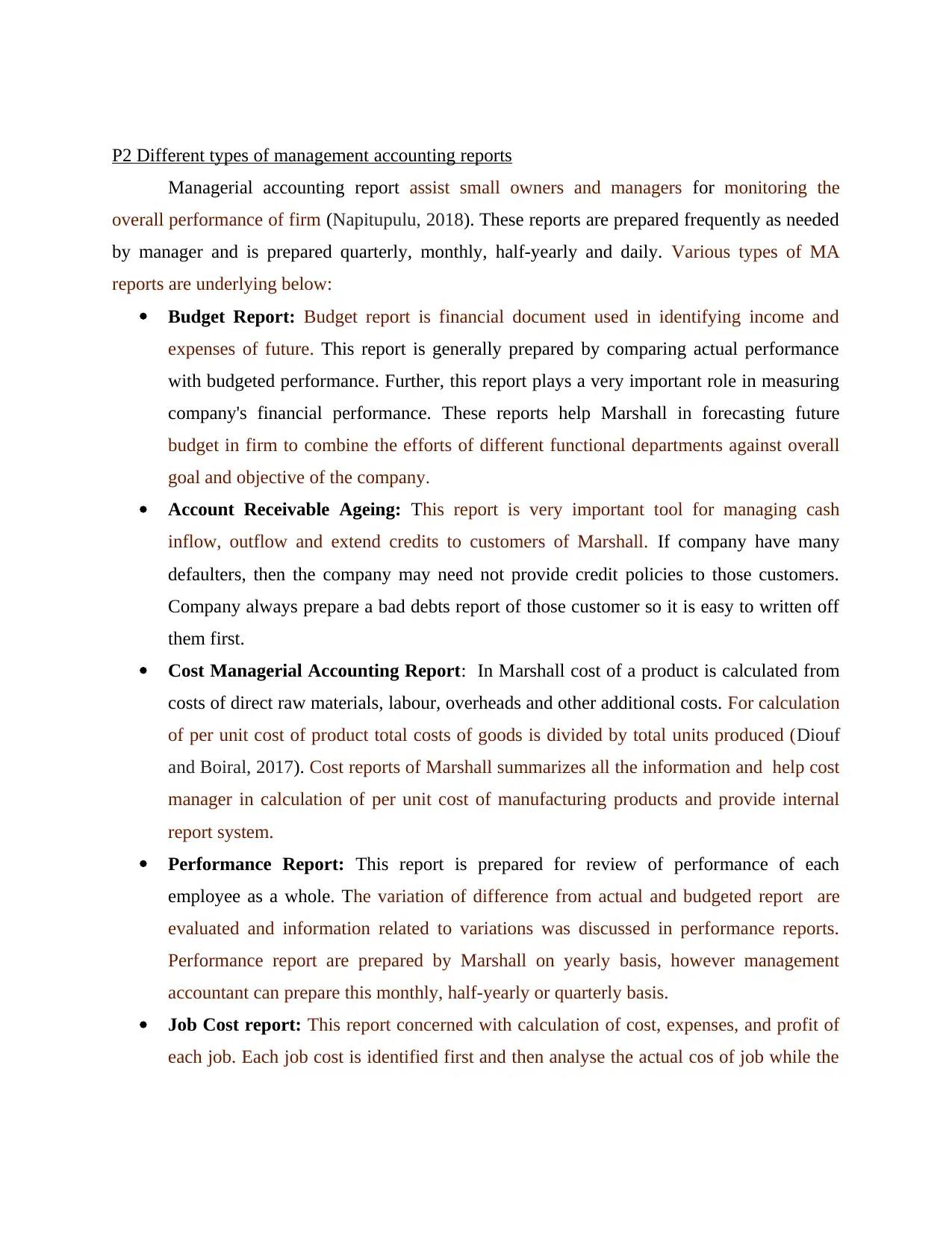

P2 Different types of management accounting reports

Managerial accounting report assist small owners and managers for monitoring the

overall performance of firm (Napitupulu, 2018). These reports are prepared frequently as needed

by manager and is prepared quarterly, monthly, half-yearly and daily. Various types of MA

reports are underlying below:

Budget Report: Budget report is financial document used in identifying income and

expenses of future. This report is generally prepared by comparing actual performance

with budgeted performance. Further, this report plays a very important role in measuring

company's financial performance. These reports help Marshall in forecasting future

budget in firm to combine the efforts of different functional departments against overall

goal and objective of the company.

Account Receivable Ageing: This report is very important tool for managing cash

inflow, outflow and extend credits to customers of Marshall. If company have many

defaulters, then the company may need not provide credit policies to those customers.

Company always prepare a bad debts report of those customer so it is easy to written off

them first.

Cost Managerial Accounting Report: In Marshall cost of a product is calculated from

costs of direct raw materials, labour, overheads and other additional costs. For calculation

of per unit cost of product total costs of goods is divided by total units produced (Diouf

and Boiral, 2017). Cost reports of Marshall summarizes all the information and help cost

manager in calculation of per unit cost of manufacturing products and provide internal

report system.

Performance Report: This report is prepared for review of performance of each

employee as a whole. The variation of difference from actual and budgeted report are

evaluated and information related to variations was discussed in performance reports.

Performance report are prepared by Marshall on yearly basis, however management

accountant can prepare this monthly, half-yearly or quarterly basis.

Job Cost report: This report concerned with calculation of cost, expenses, and profit of

each job. Each job cost is identified first and then analyse the actual cos of job while the

Managerial accounting report assist small owners and managers for monitoring the

overall performance of firm (Napitupulu, 2018). These reports are prepared frequently as needed

by manager and is prepared quarterly, monthly, half-yearly and daily. Various types of MA

reports are underlying below:

Budget Report: Budget report is financial document used in identifying income and

expenses of future. This report is generally prepared by comparing actual performance

with budgeted performance. Further, this report plays a very important role in measuring

company's financial performance. These reports help Marshall in forecasting future

budget in firm to combine the efforts of different functional departments against overall

goal and objective of the company.

Account Receivable Ageing: This report is very important tool for managing cash

inflow, outflow and extend credits to customers of Marshall. If company have many

defaulters, then the company may need not provide credit policies to those customers.

Company always prepare a bad debts report of those customer so it is easy to written off

them first.

Cost Managerial Accounting Report: In Marshall cost of a product is calculated from

costs of direct raw materials, labour, overheads and other additional costs. For calculation

of per unit cost of product total costs of goods is divided by total units produced (Diouf

and Boiral, 2017). Cost reports of Marshall summarizes all the information and help cost

manager in calculation of per unit cost of manufacturing products and provide internal

report system.

Performance Report: This report is prepared for review of performance of each

employee as a whole. The variation of difference from actual and budgeted report are

evaluated and information related to variations was discussed in performance reports.

Performance report are prepared by Marshall on yearly basis, however management

accountant can prepare this monthly, half-yearly or quarterly basis.

Job Cost report: This report concerned with calculation of cost, expenses, and profit of

each job. Each job cost is identified first and then analyse the actual cos of job while the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

project is in progress. Hence, Marshall can assess those areas of waste and eliminate it

may bring forth more profits with minimum waste at a same time.

Order Information Report: This report will assist management of Marshall to know

about current trends and changes in their business efficiently and effectively. In order

information report different types of report are prepare which help Marshall in decision

making for achieve low cost on placing of orders.

Manufacturing Report: Marshall prepare this report and it assist in easy calculation of

manufacturing and inventory cost. These report includes labour and overheads cost and

wastage material cost of inventory through which managers can easily differentiate each

assembly lines cost on their particular department.

Special Report: Management find difficulties in decision making and other reports not

give actual information to handle all problems. Under this circumstances, special reports

are prepared. These reports are needed for special purposes only as per the need of

situation. If available accounting information may not be sufficient, then special data will

be collected. It may needed put extra staff for compiling these reports and also involve

co-ordination of different departments and levels of management.

P3 Income statement using marginal and absorption costs.

Income statement (Marginal costing)

For the month October 2019

Particulars Amount(£)

Sales Revenue (25 per unit x40000 units) 10,00,000

(-) Marginal cost of sales

Direct material cost (10 per unit x40,000 units)) 4,00,000

Direct labour cost (30x40000 units) / 60) x 8 1,60,000

Variable production Overhead cost (2 per unit x40,000 units)) 80000

variable selling expense cost (4 per unit x40,000 units)) 1,60,000

Contribution 2,00,000

may bring forth more profits with minimum waste at a same time.

Order Information Report: This report will assist management of Marshall to know

about current trends and changes in their business efficiently and effectively. In order

information report different types of report are prepare which help Marshall in decision

making for achieve low cost on placing of orders.

Manufacturing Report: Marshall prepare this report and it assist in easy calculation of

manufacturing and inventory cost. These report includes labour and overheads cost and

wastage material cost of inventory through which managers can easily differentiate each

assembly lines cost on their particular department.

Special Report: Management find difficulties in decision making and other reports not

give actual information to handle all problems. Under this circumstances, special reports

are prepared. These reports are needed for special purposes only as per the need of

situation. If available accounting information may not be sufficient, then special data will

be collected. It may needed put extra staff for compiling these reports and also involve

co-ordination of different departments and levels of management.

P3 Income statement using marginal and absorption costs.

Income statement (Marginal costing)

For the month October 2019

Particulars Amount(£)

Sales Revenue (25 per unit x40000 units) 10,00,000

(-) Marginal cost of sales

Direct material cost (10 per unit x40,000 units)) 4,00,000

Direct labour cost (30x40000 units) / 60) x 8 1,60,000

Variable production Overhead cost (2 per unit x40,000 units)) 80000

variable selling expense cost (4 per unit x40,000 units)) 1,60,000

Contribution 2,00,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

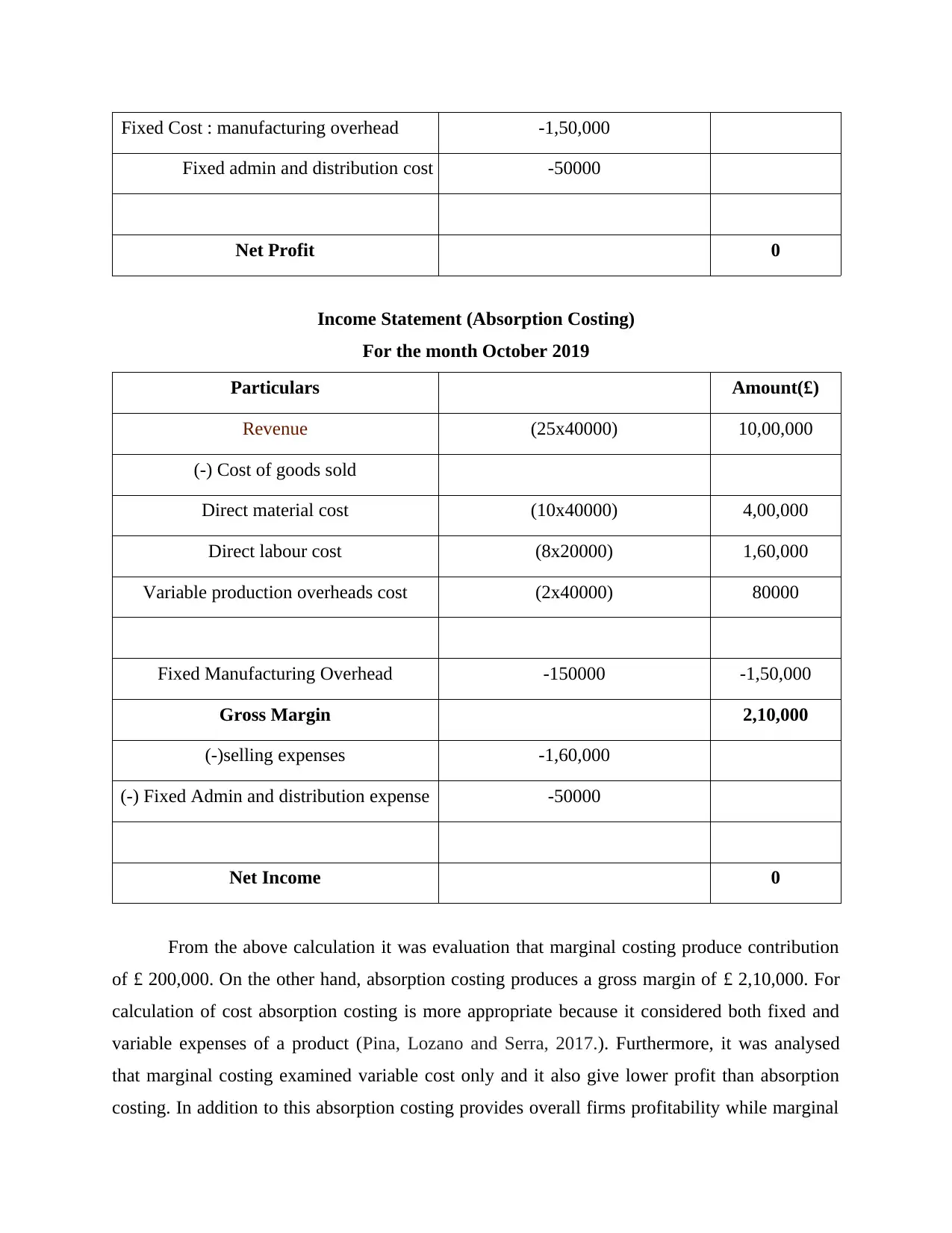

Fixed Cost : manufacturing overhead -1,50,000

Fixed admin and distribution cost -50000

Net Profit 0

Income Statement (Absorption Costing)

For the month October 2019

Particulars Amount(£)

Revenue (25x40000) 10,00,000

(-) Cost of goods sold

Direct material cost (10x40000) 4,00,000

Direct labour cost (8x20000) 1,60,000

Variable production overheads cost (2x40000) 80000

Fixed Manufacturing Overhead -150000 -1,50,000

Gross Margin 2,10,000

(-)selling expenses -1,60,000

(-) Fixed Admin and distribution expense -50000

Net Income 0

From the above calculation it was evaluation that marginal costing produce contribution

of £ 200,000. On the other hand, absorption costing produces a gross margin of £ 2,10,000. For

calculation of cost absorption costing is more appropriate because it considered both fixed and

variable expenses of a product (Pina, Lozano and Serra, 2017.). Furthermore, it was analysed

that marginal costing examined variable cost only and it also give lower profit than absorption

costing. In addition to this absorption costing provides overall firms profitability while marginal

Fixed admin and distribution cost -50000

Net Profit 0

Income Statement (Absorption Costing)

For the month October 2019

Particulars Amount(£)

Revenue (25x40000) 10,00,000

(-) Cost of goods sold

Direct material cost (10x40000) 4,00,000

Direct labour cost (8x20000) 1,60,000

Variable production overheads cost (2x40000) 80000

Fixed Manufacturing Overhead -150000 -1,50,000

Gross Margin 2,10,000

(-)selling expenses -1,60,000

(-) Fixed Admin and distribution expense -50000

Net Income 0

From the above calculation it was evaluation that marginal costing produce contribution

of £ 200,000. On the other hand, absorption costing produces a gross margin of £ 2,10,000. For

calculation of cost absorption costing is more appropriate because it considered both fixed and

variable expenses of a product (Pina, Lozano and Serra, 2017.). Furthermore, it was analysed

that marginal costing examined variable cost only and it also give lower profit than absorption

costing. In addition to this absorption costing provides overall firms profitability while marginal

costing outlined each product contribution. It also reflects that cost per unit remains same either

in change of production level in marginal costing. In contradictory side in absorption costing due

to the fixed expenses cost per unit decrease when production level increase.

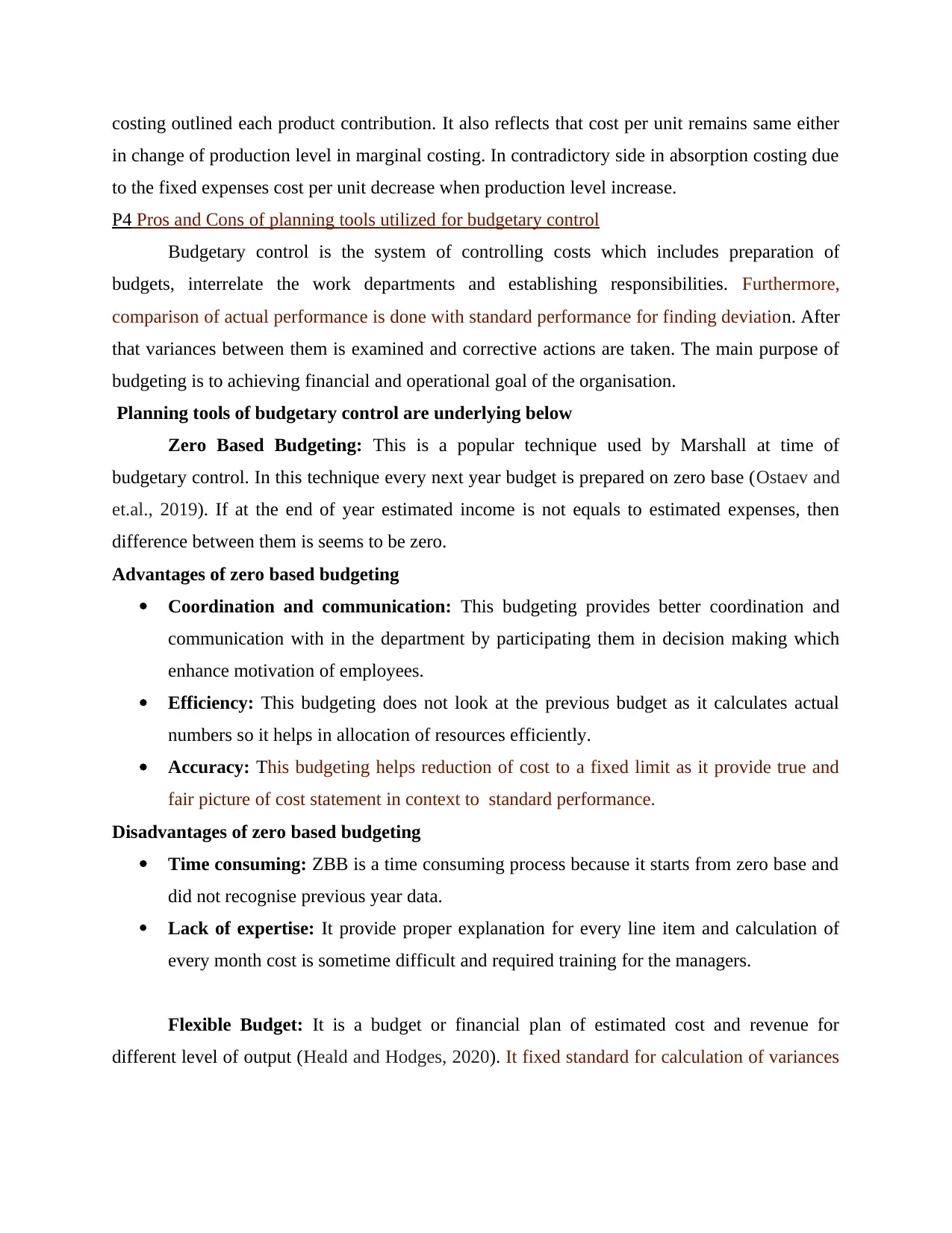

P4 Pros and Cons of planning tools utilized for budgetary control

Budgetary control is the system of controlling costs which includes preparation of

budgets, interrelate the work departments and establishing responsibilities. Furthermore,

comparison of actual performance is done with standard performance for finding deviation. After

that variances between them is examined and corrective actions are taken. The main purpose of

budgeting is to achieving financial and operational goal of the organisation.

Planning tools of budgetary control are underlying below

Zero Based Budgeting: This is a popular technique used by Marshall at time of

budgetary control. In this technique every next year budget is prepared on zero base (Ostaev and

et.al., 2019). If at the end of year estimated income is not equals to estimated expenses, then

difference between them is seems to be zero.

Advantages of zero based budgeting

Coordination and communication: This budgeting provides better coordination and

communication with in the department by participating them in decision making which

enhance motivation of employees.

Efficiency: This budgeting does not look at the previous budget as it calculates actual

numbers so it helps in allocation of resources efficiently.

Accuracy: This budgeting helps reduction of cost to a fixed limit as it provide true and

fair picture of cost statement in context to standard performance.

Disadvantages of zero based budgeting

Time consuming: ZBB is a time consuming process because it starts from zero base and

did not recognise previous year data.

Lack of expertise: It provide proper explanation for every line item and calculation of

every month cost is sometime difficult and required training for the managers.

Flexible Budget: It is a budget or financial plan of estimated cost and revenue for

different level of output (Heald and Hodges, 2020). It fixed standard for calculation of variances

in change of production level in marginal costing. In contradictory side in absorption costing due

to the fixed expenses cost per unit decrease when production level increase.

P4 Pros and Cons of planning tools utilized for budgetary control

Budgetary control is the system of controlling costs which includes preparation of

budgets, interrelate the work departments and establishing responsibilities. Furthermore,

comparison of actual performance is done with standard performance for finding deviation. After

that variances between them is examined and corrective actions are taken. The main purpose of

budgeting is to achieving financial and operational goal of the organisation.

Planning tools of budgetary control are underlying below

Zero Based Budgeting: This is a popular technique used by Marshall at time of

budgetary control. In this technique every next year budget is prepared on zero base (Ostaev and

et.al., 2019). If at the end of year estimated income is not equals to estimated expenses, then

difference between them is seems to be zero.

Advantages of zero based budgeting

Coordination and communication: This budgeting provides better coordination and

communication with in the department by participating them in decision making which

enhance motivation of employees.

Efficiency: This budgeting does not look at the previous budget as it calculates actual

numbers so it helps in allocation of resources efficiently.

Accuracy: This budgeting helps reduction of cost to a fixed limit as it provide true and

fair picture of cost statement in context to standard performance.

Disadvantages of zero based budgeting

Time consuming: ZBB is a time consuming process because it starts from zero base and

did not recognise previous year data.

Lack of expertise: It provide proper explanation for every line item and calculation of

every month cost is sometime difficult and required training for the managers.

Flexible Budget: It is a budget or financial plan of estimated cost and revenue for

different level of output (Heald and Hodges, 2020). It fixed standard for calculation of variances

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

from actual performance of the company. It is a kind of variable budget that predicts the actual

manufacture activities in business entity

Advantages of Flexible budgeting

This budgets act as a standard by setting expenditures at different level of activity and

also identify variable expenses.

It helps in better control and correction by glorifying operational inefficiency and error

It is good tool for analysing the performance of managers as it closely aligns to

expectations at any level of activities.

This budget is more flexible than static budget because it can be easily modified

according to market situation and environment.

Disadvantages of Flexible budgeting

It requires more planning to identify expenses because all expenses are figure out at one

place.

For formulation of flexible budget expert workers required and availableness of that

workers become a challenge for the organisations.

It depends upon a forecast of the past business and if any error or mistakes in the

previous books of accounts then it does not show correct results.

Fixed and flexible cost ascertainment held on arbitrary basis, hence flexible costs are less

relatable for find out actual budget cost.

Fixed Budget: It is a financial document which remains constant throughout a financial

period either changes taken place in the volume of sales, revenue, no of units produced. It does

not vary with the change in actual output, and it prepared for single level of activity.

Advantages of Fixed Budget:

Easy implementation: It is easy to implement this budget in organisations because it

allows the company to compare its expenses and revenue and implement the strategies in

future.

Helps in measure profits: It helps in measure both short and long term profits because it

allocates the same amount of money for necessities on a regular basis. So profit

measurement is easy in this case as everything remains unchanged.

Helps in future planning: By using previous records of this budget mangers plan their

budget proposal which helps in future planning and forecasting.

manufacture activities in business entity

Advantages of Flexible budgeting

This budgets act as a standard by setting expenditures at different level of activity and

also identify variable expenses.

It helps in better control and correction by glorifying operational inefficiency and error

It is good tool for analysing the performance of managers as it closely aligns to

expectations at any level of activities.

This budget is more flexible than static budget because it can be easily modified

according to market situation and environment.

Disadvantages of Flexible budgeting

It requires more planning to identify expenses because all expenses are figure out at one

place.

For formulation of flexible budget expert workers required and availableness of that

workers become a challenge for the organisations.

It depends upon a forecast of the past business and if any error or mistakes in the

previous books of accounts then it does not show correct results.

Fixed and flexible cost ascertainment held on arbitrary basis, hence flexible costs are less

relatable for find out actual budget cost.

Fixed Budget: It is a financial document which remains constant throughout a financial

period either changes taken place in the volume of sales, revenue, no of units produced. It does

not vary with the change in actual output, and it prepared for single level of activity.

Advantages of Fixed Budget:

Easy implementation: It is easy to implement this budget in organisations because it

allows the company to compare its expenses and revenue and implement the strategies in

future.

Helps in measure profits: It helps in measure both short and long term profits because it

allocates the same amount of money for necessities on a regular basis. So profit

measurement is easy in this case as everything remains unchanged.

Helps in future planning: By using previous records of this budget mangers plan their

budget proposal which helps in future planning and forecasting.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Disadvantages of fixed budgets:

It is based on previous data so new firms face many problems whole implementing fixed

budget

Fixed budget is recognised as an unproductive tool of cost control because it is not

considered changes.

P5 Adoption of management accounting systems for respond financial problems.

Financial problem is a situation in which firm is not able to meet its requirement in terms

of money. It can also be defined as issues or problem faced in managing and allocating money

within company. Some financial problems which are faced by small businesses are lack of

working capital, debt repayment, inconsistent cash flow, access to funding etc.

For instance, Lack of Working Capital is a problem faced by small businesses. If any firm is

facing problem of insufficient working capital, then it shows inability of company to meet out its

financial obligation (Abd, Ramli and Abdul, 2020.). It is necessary for the organisation to meet

out its short term obligation on time maintaining good creditworthiness in the society.

Management accounting systems used for respond financial problems

Benchmarking: It is the process of comparing business products, services and processes

to its competitors for finding out key differences. It also identifies gaps in an organisation

process in order to achieve competitive advantages. Marshall use benchmarking for determining

the capabilities of its products or services in comparison with its competitors. After that

evaluation of variances is done in order to improve its performance by making different

strategies.

Variance Analysis: It is a quantitative technique of finding out deviation between actual

and budgeted performance of an organisation. When existing results are higher than standard, a

favourable variance arise (Heald and Hodges, 2020.). On the other side when they are not up-to

standard an adverse variance arises It helps Marshall in understanding why fluctuation arise and

what should be done to reduce the adverse variance. Marshall use this technique which helps its

managers in making efficient and forward budgetary decisions. This would enable management

to fix the responsibilities to the right person at a right time. this in turn will help company in

solving financial problem with efficiency.

Key Performance Indicator (KPI): It measure and indicate how effectively firm

achieving main organisation objectives. KPIs focus on the overall financial performance of the

It is based on previous data so new firms face many problems whole implementing fixed

budget

Fixed budget is recognised as an unproductive tool of cost control because it is not

considered changes.

P5 Adoption of management accounting systems for respond financial problems.

Financial problem is a situation in which firm is not able to meet its requirement in terms

of money. It can also be defined as issues or problem faced in managing and allocating money

within company. Some financial problems which are faced by small businesses are lack of

working capital, debt repayment, inconsistent cash flow, access to funding etc.

For instance, Lack of Working Capital is a problem faced by small businesses. If any firm is

facing problem of insufficient working capital, then it shows inability of company to meet out its

financial obligation (Abd, Ramli and Abdul, 2020.). It is necessary for the organisation to meet

out its short term obligation on time maintaining good creditworthiness in the society.

Management accounting systems used for respond financial problems

Benchmarking: It is the process of comparing business products, services and processes

to its competitors for finding out key differences. It also identifies gaps in an organisation

process in order to achieve competitive advantages. Marshall use benchmarking for determining

the capabilities of its products or services in comparison with its competitors. After that

evaluation of variances is done in order to improve its performance by making different

strategies.

Variance Analysis: It is a quantitative technique of finding out deviation between actual

and budgeted performance of an organisation. When existing results are higher than standard, a

favourable variance arise (Heald and Hodges, 2020.). On the other side when they are not up-to

standard an adverse variance arises It helps Marshall in understanding why fluctuation arise and

what should be done to reduce the adverse variance. Marshall use this technique which helps its

managers in making efficient and forward budgetary decisions. This would enable management

to fix the responsibilities to the right person at a right time. this in turn will help company in

solving financial problem with efficiency.

Key Performance Indicator (KPI): It measure and indicate how effectively firm

achieving main organisation objectives. KPIs focus on the overall financial performance of the

company which provides information about expenses, profit, cash flows, and sales, in order to

achieve financial goals and objectives of the business. The chosen firm use this KPIs for

calculating financial performance of the business. Every financial professional needs to know

about these KPIs i.e. GP, NP, Current and quick ratio, return on assets and equity ratio etc. By

using this KPIs firm evaluate the overall financial growth and performance of the company.

under this Marshall uses a specific indicator and measure the performance against that indicator

in order to solve financial problem.

Marshall Sustonable

For solving financial problem Marshall use

benchmarking for determining the capabilities

of its good and services from its competitors.

This assist Marshall in finding out differences

which needs to improve by the firm

For solving financial problem Sustainable use

specific key performance indicator through

which measure the performance. Sustainable

sets an indicator and comparing its actual

performance against that indicator

CONCLUSION

From the above report it was summarised that management accounting is defined as a

process of recording, identifying, Summarising accounting information in order to take

managerial decision in business. Current report was based on Case scenario of Marshall which

defines about different accounting systems like cost accounting and inventory management

system. The above study reflected that budgetary report, performances report are various types of

accounting report used by the company. With assistance of above report income statement was

prepared by using techniques of marginal and absorption costing. Further it was highlighted that

different tools of planning are ZBB, fixed and others. At last the report outlined different

methods of solving financial problems like benchmarking and variance analysis.

achieve financial goals and objectives of the business. The chosen firm use this KPIs for

calculating financial performance of the business. Every financial professional needs to know

about these KPIs i.e. GP, NP, Current and quick ratio, return on assets and equity ratio etc. By

using this KPIs firm evaluate the overall financial growth and performance of the company.

under this Marshall uses a specific indicator and measure the performance against that indicator

in order to solve financial problem.

Marshall Sustonable

For solving financial problem Marshall use

benchmarking for determining the capabilities

of its good and services from its competitors.

This assist Marshall in finding out differences

which needs to improve by the firm

For solving financial problem Sustainable use

specific key performance indicator through

which measure the performance. Sustainable

sets an indicator and comparing its actual

performance against that indicator

CONCLUSION

From the above report it was summarised that management accounting is defined as a

process of recording, identifying, Summarising accounting information in order to take

managerial decision in business. Current report was based on Case scenario of Marshall which

defines about different accounting systems like cost accounting and inventory management

system. The above study reflected that budgetary report, performances report are various types of

accounting report used by the company. With assistance of above report income statement was

prepared by using techniques of marginal and absorption costing. Further it was highlighted that

different tools of planning are ZBB, fixed and others. At last the report outlined different

methods of solving financial problems like benchmarking and variance analysis.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.