Feasibility of Activity Based Budgeting Implementation - Neon Tech

VerifiedAdded on 2023/06/04

|14

|4005

|108

Report

AI Summary

This report assesses the feasibility of implementing Activity Based Budgeting (ABB) at Neon Innovative Tech Private Limited. Commissioned by the company's CEO after a seminar on ABB, the report, prepared by ABC Managements consultants, analyzes the current budgeting process and potential improvements through ABB. It details Neon Innovative Tech's operations, including its service offerings and associated activities and costs. The report defines ABB, outlines its features, and differentiates it from traditional budgeting systems. Key aspects covered include identifying cost drivers, linking organizational strategy to activities, and determining capacity management. The report also contrasts ABB with traditional budgeting, highlighting the limitations of the latter and the benefits of ABB in managing overheads and aligning with organizational goals. The ultimate aim is to provide Neon Innovative Tech with a clear understanding of the suitability and potential impact of transitioning to an ABB system.

55 Falcon Street, Crows Nest, N.S.W 2065

Phone : 011-42442685, Fax : 011-42442686

A FEASIBILITY REPORT

ON THE IMPLEMENTATION OF THE

ACTIVITY BASED BUDGETING

PREPARED FOR

NEON INNOVATIVE TECH PRIVATE LIMITED

PREPARED BY

STUDENT

STUDENT ID

STUDENT

STUDENT ID

STUDENT

STUDENT ID

CLIENT’S CONTACT: NAME

DESIGNATION: CHIEF EXECUTIVE OFFICER

PHONE ; 022-2286523,FAX : 022-2286522

ADDRESS : 24/2, 2ND FLOOR, CORPORATE CENTRE

XXXXX, XXXXX- 400071

1 | P a g e

Phone : 011-42442685, Fax : 011-42442686

A FEASIBILITY REPORT

ON THE IMPLEMENTATION OF THE

ACTIVITY BASED BUDGETING

PREPARED FOR

NEON INNOVATIVE TECH PRIVATE LIMITED

PREPARED BY

STUDENT

STUDENT ID

STUDENT

STUDENT ID

STUDENT

STUDENT ID

CLIENT’S CONTACT: NAME

DESIGNATION: CHIEF EXECUTIVE OFFICER

PHONE ; 022-2286523,FAX : 022-2286522

ADDRESS : 24/2, 2ND FLOOR, CORPORATE CENTRE

XXXXX, XXXXX- 400071

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Background and Abstract.................................................................................................................................................... 3

Introduction.............................................................................................................................................................................. 3

Key Points.................................................................................................................................................................................. 3

A brief description of the Client Company............................................................................................................... 3

Description of ABB and its features............................................................................................................................ 4

Features of ABB................................................................................................................................................................... 6

Difference between ABB and Traditional Budgeting system............................................................................6

Discussion on the Suitability of ABB........................................................................................................................ 11

Conclusion............................................................................................................................................................................... 12

References............................................................................................................................................................................... 13

2 | P a g e

Background and Abstract.................................................................................................................................................... 3

Introduction.............................................................................................................................................................................. 3

Key Points.................................................................................................................................................................................. 3

A brief description of the Client Company............................................................................................................... 3

Description of ABB and its features............................................................................................................................ 4

Features of ABB................................................................................................................................................................... 6

Difference between ABB and Traditional Budgeting system............................................................................6

Discussion on the Suitability of ABB........................................................................................................................ 11

Conclusion............................................................................................................................................................................... 12

References............................................................................................................................................................................... 13

2 | P a g e

BACKGROUND AND ABSTRACT

Neon Innovations Private Limited has engaged a team of management consultants from the

leadership ABC Managements consultants to assist with the feasibility of the implementation of

Activity Based Budgeting for which an in-depth analysis of the existing organizational

environment along with the prospective challenges and opportunities associated with its

implementation has been carried out by an expert team (Arnott, et al., 2017).

Based on the recommendations and guidelines provided in this report, the next step for the Neon

Innovative Tech Private Limited is to develop and implement the ABB.

INTRODUCTION

Neon Innovative Tech Private Limited is presently under the process for evaluation of the

feasibility of the current budgeting process along with prospect of the further scope of

improvement. During this process the CEO of the company has attended a seminar on Activity

Based Budgeting subsequent to which finding it a better option to adopt the same, it has asked

the ABC Managements consultants to submit a brief report on the feasibility of transition to

ABB for the company in the current scenario (Belton, 2017).

KEY POINTS

A BRIEF DESCRIPTION OF THE CLIENT COMPANY

Neon Innovative Tech Private Limited is a multinational IT company engaged as a service

provider providing services in terms of Consulting, Business process outsourcing, IT

Infrastructure services, Engineering and Industrial services, Application development and

maintenance, asset leverage solution and assurance services etc., which are preformed through

the help of a number of value added activities like Recruitment and training, document creation,

Communication, Rent, travelling and Conveyance, functional requirement analysis, marketing

support, supervision and administration, services of equipment’s and programmers etc. with the

associated cost drivers like programming hours, percentage increase in sales, number of visits

and facilities, requirements, number of units, number of calls and space provided etc. (Bromwich

& Scapens, 2016) . A number of Non- value added activities related drivers of rework and idle

time can also be found because of the client delays, resource unavailability, and lack of skills,

scope creep or Non conformances to proceed further or any other reason. Our client has mainly

incurred cost in terms of resource investment for enhanced employee remuneration and

functional requirement analysis together with operational support. During the past few years

company could earn only the marginal profits due to the resources allocated for the

aforementioned activities. But in last few years it has also been noticed that due to the delay in

3 | P a g e

Neon Innovations Private Limited has engaged a team of management consultants from the

leadership ABC Managements consultants to assist with the feasibility of the implementation of

Activity Based Budgeting for which an in-depth analysis of the existing organizational

environment along with the prospective challenges and opportunities associated with its

implementation has been carried out by an expert team (Arnott, et al., 2017).

Based on the recommendations and guidelines provided in this report, the next step for the Neon

Innovative Tech Private Limited is to develop and implement the ABB.

INTRODUCTION

Neon Innovative Tech Private Limited is presently under the process for evaluation of the

feasibility of the current budgeting process along with prospect of the further scope of

improvement. During this process the CEO of the company has attended a seminar on Activity

Based Budgeting subsequent to which finding it a better option to adopt the same, it has asked

the ABC Managements consultants to submit a brief report on the feasibility of transition to

ABB for the company in the current scenario (Belton, 2017).

KEY POINTS

A BRIEF DESCRIPTION OF THE CLIENT COMPANY

Neon Innovative Tech Private Limited is a multinational IT company engaged as a service

provider providing services in terms of Consulting, Business process outsourcing, IT

Infrastructure services, Engineering and Industrial services, Application development and

maintenance, asset leverage solution and assurance services etc., which are preformed through

the help of a number of value added activities like Recruitment and training, document creation,

Communication, Rent, travelling and Conveyance, functional requirement analysis, marketing

support, supervision and administration, services of equipment’s and programmers etc. with the

associated cost drivers like programming hours, percentage increase in sales, number of visits

and facilities, requirements, number of units, number of calls and space provided etc. (Bromwich

& Scapens, 2016) . A number of Non- value added activities related drivers of rework and idle

time can also be found because of the client delays, resource unavailability, and lack of skills,

scope creep or Non conformances to proceed further or any other reason. Our client has mainly

incurred cost in terms of resource investment for enhanced employee remuneration and

functional requirement analysis together with operational support. During the past few years

company could earn only the marginal profits due to the resources allocated for the

aforementioned activities. But in last few years it has also been noticed that due to the delay in

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

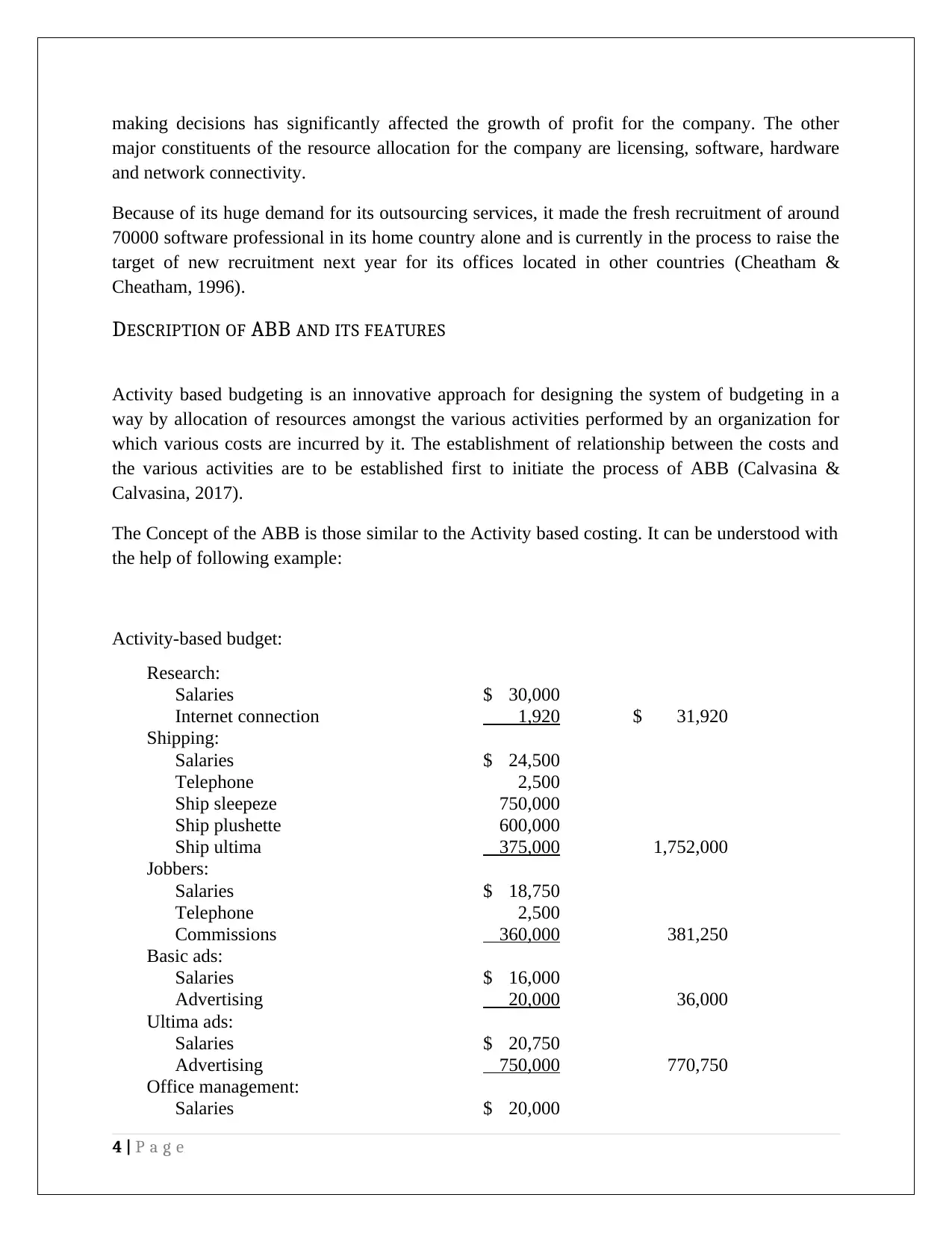

making decisions has significantly affected the growth of profit for the company. The other

major constituents of the resource allocation for the company are licensing, software, hardware

and network connectivity.

Because of its huge demand for its outsourcing services, it made the fresh recruitment of around

70000 software professional in its home country alone and is currently in the process to raise the

target of new recruitment next year for its offices located in other countries (Cheatham &

Cheatham, 1996).

DESCRIPTION OF ABB AND ITS FEATURES

Activity based budgeting is an innovative approach for designing the system of budgeting in a

way by allocation of resources amongst the various activities performed by an organization for

which various costs are incurred by it. The establishment of relationship between the costs and

the various activities are to be established first to initiate the process of ABB (Calvasina &

Calvasina, 2017).

The Concept of the ABB is those similar to the Activity based costing. It can be understood with

the help of following example:

Activity-based budget:

Research:

Salaries $ 30,000

Internet connection 1,920 $ 31,920

Shipping:

Salaries $ 24,500

Telephone 2,500

Ship sleepeze 750,000

Ship plushette 600,000

Ship ultima 375,000 1,752,000

Jobbers:

Salaries $ 18,750

Telephone 2,500

Commissions 360,000 381,250

Basic ads:

Salaries $ 16,000

Advertising 20,000 36,000

Ultima ads:

Salaries $ 20,750

Advertising 750,000 770,750

Office management:

Salaries $ 20,000

4 | P a g e

major constituents of the resource allocation for the company are licensing, software, hardware

and network connectivity.

Because of its huge demand for its outsourcing services, it made the fresh recruitment of around

70000 software professional in its home country alone and is currently in the process to raise the

target of new recruitment next year for its offices located in other countries (Cheatham &

Cheatham, 1996).

DESCRIPTION OF ABB AND ITS FEATURES

Activity based budgeting is an innovative approach for designing the system of budgeting in a

way by allocation of resources amongst the various activities performed by an organization for

which various costs are incurred by it. The establishment of relationship between the costs and

the various activities are to be established first to initiate the process of ABB (Calvasina &

Calvasina, 2017).

The Concept of the ABB is those similar to the Activity based costing. It can be understood with

the help of following example:

Activity-based budget:

Research:

Salaries $ 30,000

Internet connection 1,920 $ 31,920

Shipping:

Salaries $ 24,500

Telephone 2,500

Ship sleepeze 750,000

Ship plushette 600,000

Ship ultima 375,000 1,752,000

Jobbers:

Salaries $ 18,750

Telephone 2,500

Commissions 360,000 381,250

Basic ads:

Salaries $ 16,000

Advertising 20,000 36,000

Ultima ads:

Salaries $ 20,750

Advertising 750,000 770,750

Office management:

Salaries $ 20,000

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

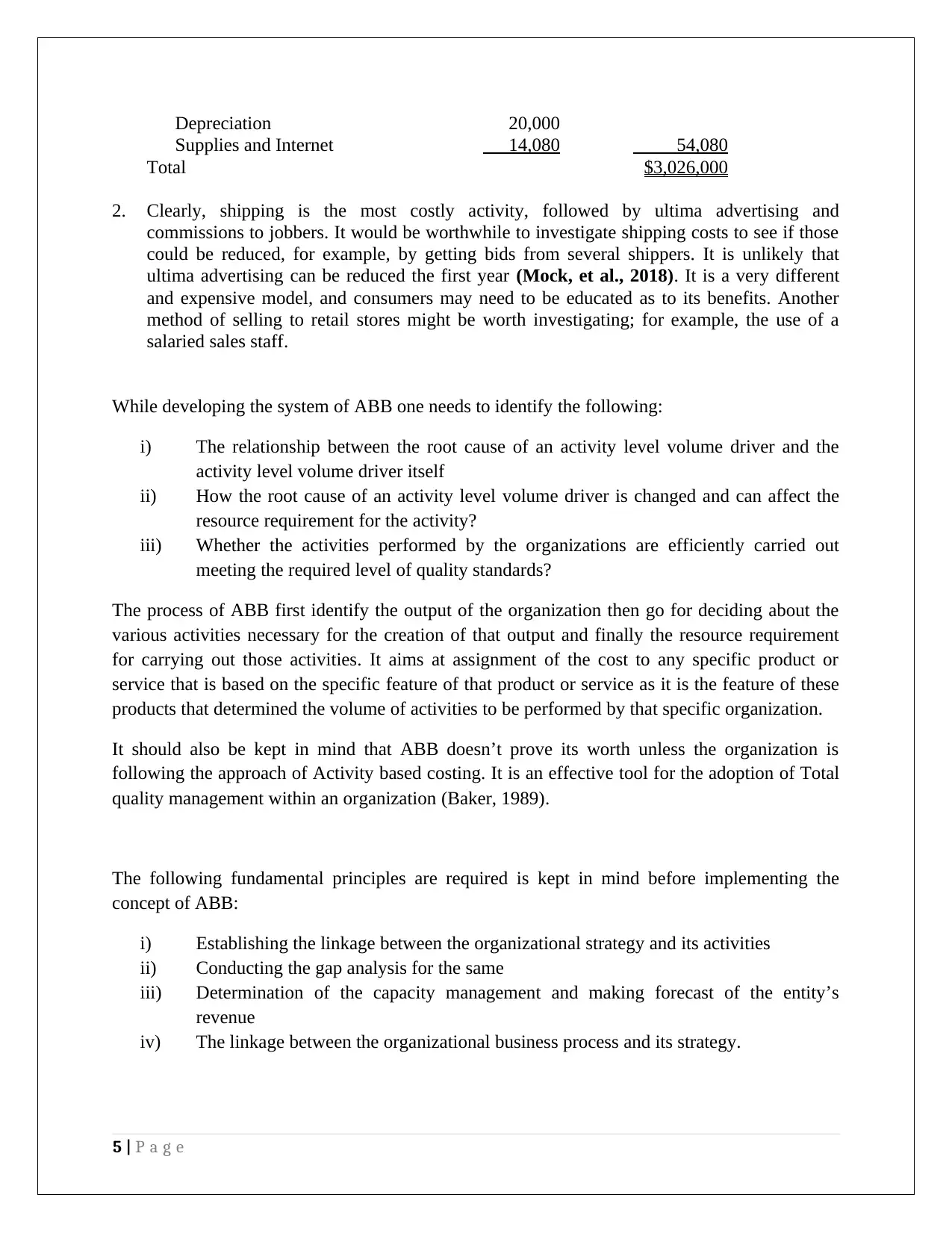

Depreciation 20,000

Supplies and Internet 14,080 54,080

Total $3,026,000

2. Clearly, shipping is the most costly activity, followed by ultima advertising and

commissions to jobbers. It would be worthwhile to investigate shipping costs to see if those

could be reduced, for example, by getting bids from several shippers. It is unlikely that

ultima advertising can be reduced the first year (Mock, et al., 2018). It is a very different

and expensive model, and consumers may need to be educated as to its benefits. Another

method of selling to retail stores might be worth investigating; for example, the use of a

salaried sales staff.

While developing the system of ABB one needs to identify the following:

i) The relationship between the root cause of an activity level volume driver and the

activity level volume driver itself

ii) How the root cause of an activity level volume driver is changed and can affect the

resource requirement for the activity?

iii) Whether the activities performed by the organizations are efficiently carried out

meeting the required level of quality standards?

The process of ABB first identify the output of the organization then go for deciding about the

various activities necessary for the creation of that output and finally the resource requirement

for carrying out those activities. It aims at assignment of the cost to any specific product or

service that is based on the specific feature of that product or service as it is the feature of these

products that determined the volume of activities to be performed by that specific organization.

It should also be kept in mind that ABB doesn’t prove its worth unless the organization is

following the approach of Activity based costing. It is an effective tool for the adoption of Total

quality management within an organization (Baker, 1989).

The following fundamental principles are required is kept in mind before implementing the

concept of ABB:

i) Establishing the linkage between the organizational strategy and its activities

ii) Conducting the gap analysis for the same

iii) Determination of the capacity management and making forecast of the entity’s

revenue

iv) The linkage between the organizational business process and its strategy.

5 | P a g e

Supplies and Internet 14,080 54,080

Total $3,026,000

2. Clearly, shipping is the most costly activity, followed by ultima advertising and

commissions to jobbers. It would be worthwhile to investigate shipping costs to see if those

could be reduced, for example, by getting bids from several shippers. It is unlikely that

ultima advertising can be reduced the first year (Mock, et al., 2018). It is a very different

and expensive model, and consumers may need to be educated as to its benefits. Another

method of selling to retail stores might be worth investigating; for example, the use of a

salaried sales staff.

While developing the system of ABB one needs to identify the following:

i) The relationship between the root cause of an activity level volume driver and the

activity level volume driver itself

ii) How the root cause of an activity level volume driver is changed and can affect the

resource requirement for the activity?

iii) Whether the activities performed by the organizations are efficiently carried out

meeting the required level of quality standards?

The process of ABB first identify the output of the organization then go for deciding about the

various activities necessary for the creation of that output and finally the resource requirement

for carrying out those activities. It aims at assignment of the cost to any specific product or

service that is based on the specific feature of that product or service as it is the feature of these

products that determined the volume of activities to be performed by that specific organization.

It should also be kept in mind that ABB doesn’t prove its worth unless the organization is

following the approach of Activity based costing. It is an effective tool for the adoption of Total

quality management within an organization (Baker, 1989).

The following fundamental principles are required is kept in mind before implementing the

concept of ABB:

i) Establishing the linkage between the organizational strategy and its activities

ii) Conducting the gap analysis for the same

iii) Determination of the capacity management and making forecast of the entity’s

revenue

iv) The linkage between the organizational business process and its strategy.

5 | P a g e

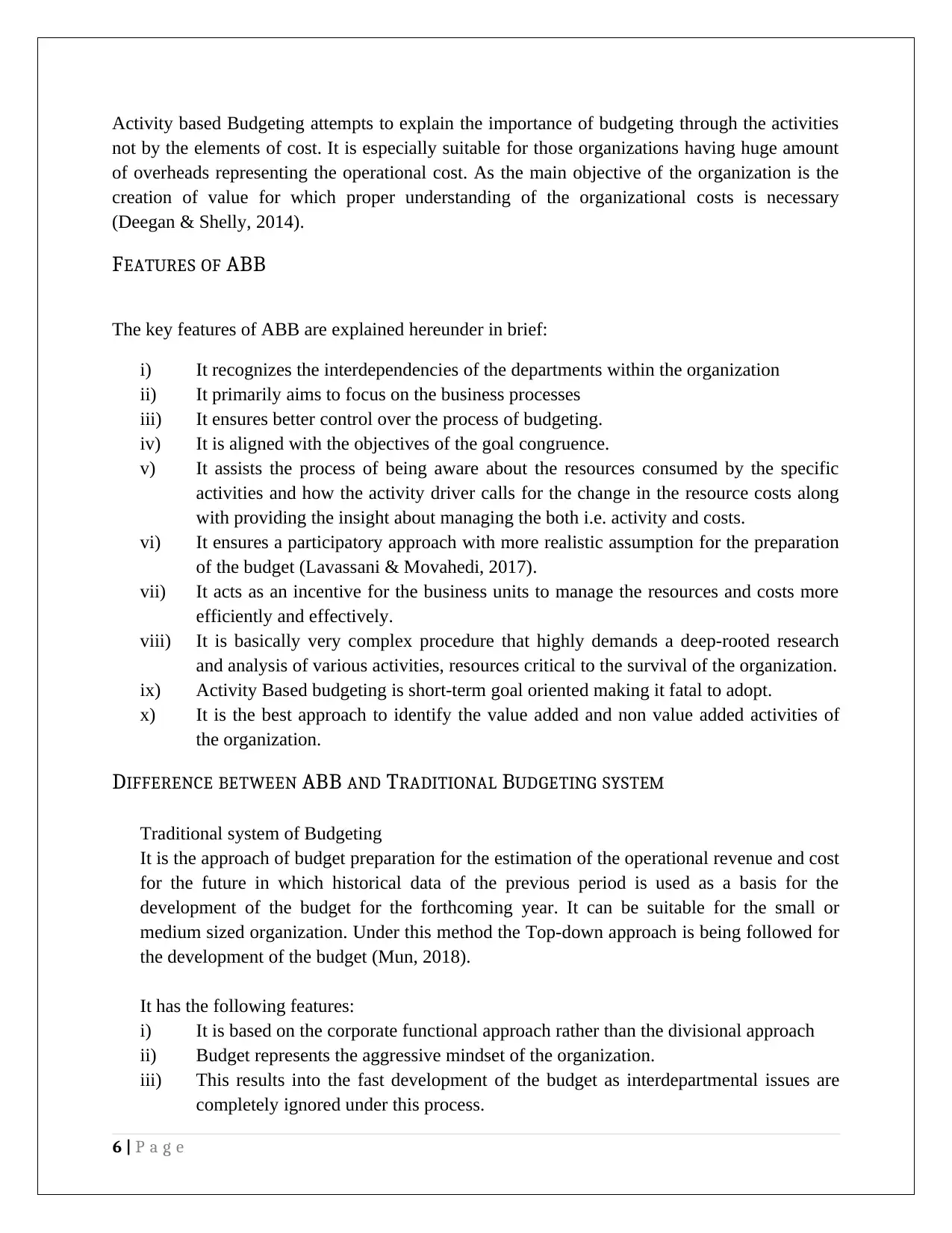

Activity based Budgeting attempts to explain the importance of budgeting through the activities

not by the elements of cost. It is especially suitable for those organizations having huge amount

of overheads representing the operational cost. As the main objective of the organization is the

creation of value for which proper understanding of the organizational costs is necessary

(Deegan & Shelly, 2014).

FEATURES OF ABB

The key features of ABB are explained hereunder in brief:

i) It recognizes the interdependencies of the departments within the organization

ii) It primarily aims to focus on the business processes

iii) It ensures better control over the process of budgeting.

iv) It is aligned with the objectives of the goal congruence.

v) It assists the process of being aware about the resources consumed by the specific

activities and how the activity driver calls for the change in the resource costs along

with providing the insight about managing the both i.e. activity and costs.

vi) It ensures a participatory approach with more realistic assumption for the preparation

of the budget (Lavassani & Movahedi, 2017).

vii) It acts as an incentive for the business units to manage the resources and costs more

efficiently and effectively.

viii) It is basically very complex procedure that highly demands a deep-rooted research

and analysis of various activities, resources critical to the survival of the organization.

ix) Activity Based budgeting is short-term goal oriented making it fatal to adopt.

x) It is the best approach to identify the value added and non value added activities of

the organization.

DIFFERENCE BETWEEN ABB AND TRADITIONAL BUDGETING SYSTEM

Traditional system of Budgeting

It is the approach of budget preparation for the estimation of the operational revenue and cost

for the future in which historical data of the previous period is used as a basis for the

development of the budget for the forthcoming year. It can be suitable for the small or

medium sized organization. Under this method the Top-down approach is being followed for

the development of the budget (Mun, 2018).

It has the following features:

i) It is based on the corporate functional approach rather than the divisional approach

ii) Budget represents the aggressive mindset of the organization.

iii) This results into the fast development of the budget as interdepartmental issues are

completely ignored under this process.

6 | P a g e

not by the elements of cost. It is especially suitable for those organizations having huge amount

of overheads representing the operational cost. As the main objective of the organization is the

creation of value for which proper understanding of the organizational costs is necessary

(Deegan & Shelly, 2014).

FEATURES OF ABB

The key features of ABB are explained hereunder in brief:

i) It recognizes the interdependencies of the departments within the organization

ii) It primarily aims to focus on the business processes

iii) It ensures better control over the process of budgeting.

iv) It is aligned with the objectives of the goal congruence.

v) It assists the process of being aware about the resources consumed by the specific

activities and how the activity driver calls for the change in the resource costs along

with providing the insight about managing the both i.e. activity and costs.

vi) It ensures a participatory approach with more realistic assumption for the preparation

of the budget (Lavassani & Movahedi, 2017).

vii) It acts as an incentive for the business units to manage the resources and costs more

efficiently and effectively.

viii) It is basically very complex procedure that highly demands a deep-rooted research

and analysis of various activities, resources critical to the survival of the organization.

ix) Activity Based budgeting is short-term goal oriented making it fatal to adopt.

x) It is the best approach to identify the value added and non value added activities of

the organization.

DIFFERENCE BETWEEN ABB AND TRADITIONAL BUDGETING SYSTEM

Traditional system of Budgeting

It is the approach of budget preparation for the estimation of the operational revenue and cost

for the future in which historical data of the previous period is used as a basis for the

development of the budget for the forthcoming year. It can be suitable for the small or

medium sized organization. Under this method the Top-down approach is being followed for

the development of the budget (Mun, 2018).

It has the following features:

i) It is based on the corporate functional approach rather than the divisional approach

ii) Budget represents the aggressive mindset of the organization.

iii) This results into the fast development of the budget as interdepartmental issues are

completely ignored under this process.

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

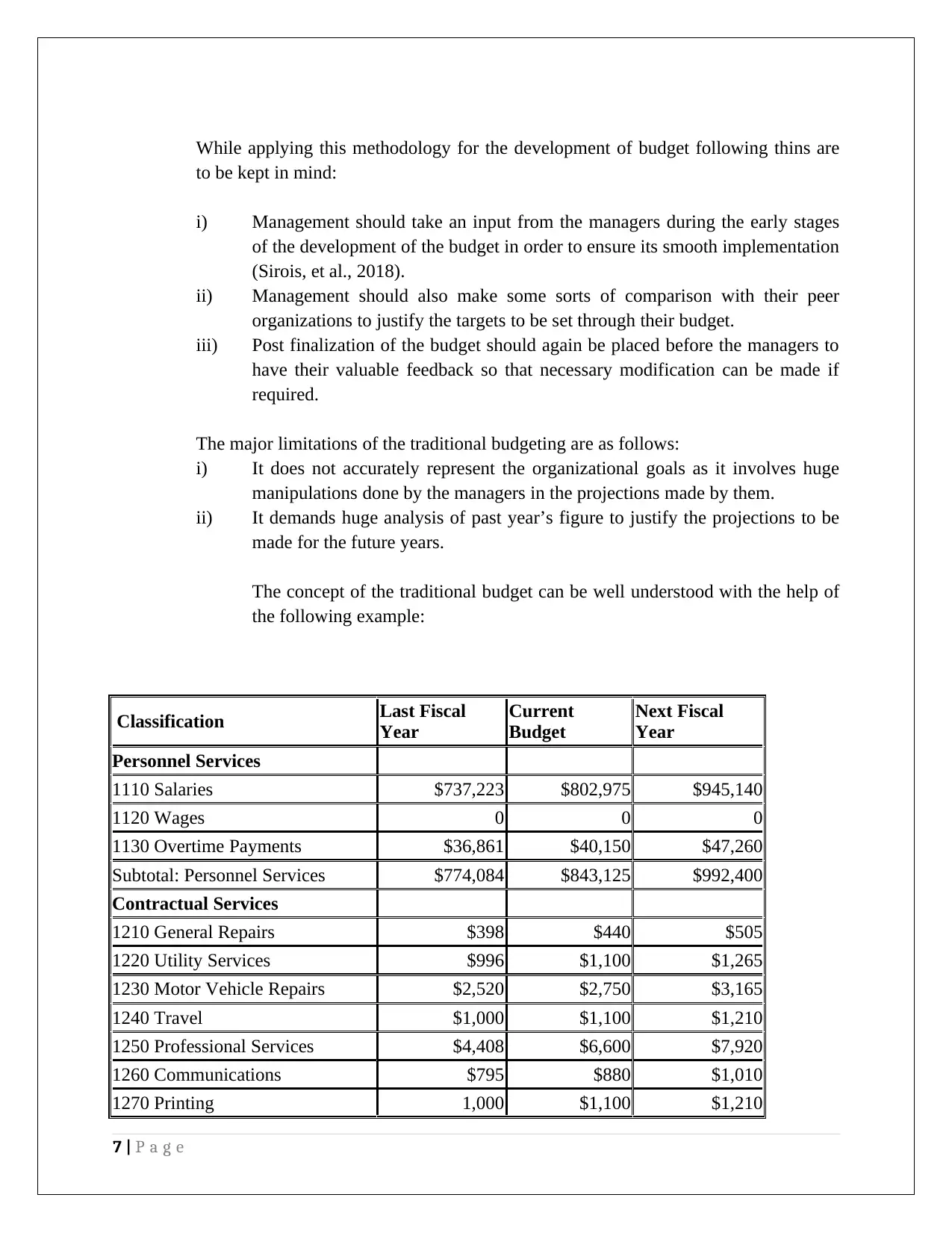

While applying this methodology for the development of budget following thins are

to be kept in mind:

i) Management should take an input from the managers during the early stages

of the development of the budget in order to ensure its smooth implementation

(Sirois, et al., 2018).

ii) Management should also make some sorts of comparison with their peer

organizations to justify the targets to be set through their budget.

iii) Post finalization of the budget should again be placed before the managers to

have their valuable feedback so that necessary modification can be made if

required.

The major limitations of the traditional budgeting are as follows:

i) It does not accurately represent the organizational goals as it involves huge

manipulations done by the managers in the projections made by them.

ii) It demands huge analysis of past year’s figure to justify the projections to be

made for the future years.

The concept of the traditional budget can be well understood with the help of

the following example:

Classification Last Fiscal

Year

Current

Budget

Next Fiscal

Year

Personnel Services

1110 Salaries $737,223 $802,975 $945,140

1120 Wages 0 0 0

1130 Overtime Payments $36,861 $40,150 $47,260

Subtotal: Personnel Services $774,084 $843,125 $992,400

Contractual Services

1210 General Repairs $398 $440 $505

1220 Utility Services $996 $1,100 $1,265

1230 Motor Vehicle Repairs $2,520 $2,750 $3,165

1240 Travel $1,000 $1,100 $1,210

1250 Professional Services $4,408 $6,600 $7,920

1260 Communications $795 $880 $1,010

1270 Printing 1,000 $1,100 $1,210

7 | P a g e

to be kept in mind:

i) Management should take an input from the managers during the early stages

of the development of the budget in order to ensure its smooth implementation

(Sirois, et al., 2018).

ii) Management should also make some sorts of comparison with their peer

organizations to justify the targets to be set through their budget.

iii) Post finalization of the budget should again be placed before the managers to

have their valuable feedback so that necessary modification can be made if

required.

The major limitations of the traditional budgeting are as follows:

i) It does not accurately represent the organizational goals as it involves huge

manipulations done by the managers in the projections made by them.

ii) It demands huge analysis of past year’s figure to justify the projections to be

made for the future years.

The concept of the traditional budget can be well understood with the help of

the following example:

Classification Last Fiscal

Year

Current

Budget

Next Fiscal

Year

Personnel Services

1110 Salaries $737,223 $802,975 $945,140

1120 Wages 0 0 0

1130 Overtime Payments $36,861 $40,150 $47,260

Subtotal: Personnel Services $774,084 $843,125 $992,400

Contractual Services

1210 General Repairs $398 $440 $505

1220 Utility Services $996 $1,100 $1,265

1230 Motor Vehicle Repairs $2,520 $2,750 $3,165

1240 Travel $1,000 $1,100 $1,210

1250 Professional Services $4,408 $6,600 $7,920

1260 Communications $795 $880 $1,010

1270 Printing 1,000 $1,100 $1,210

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

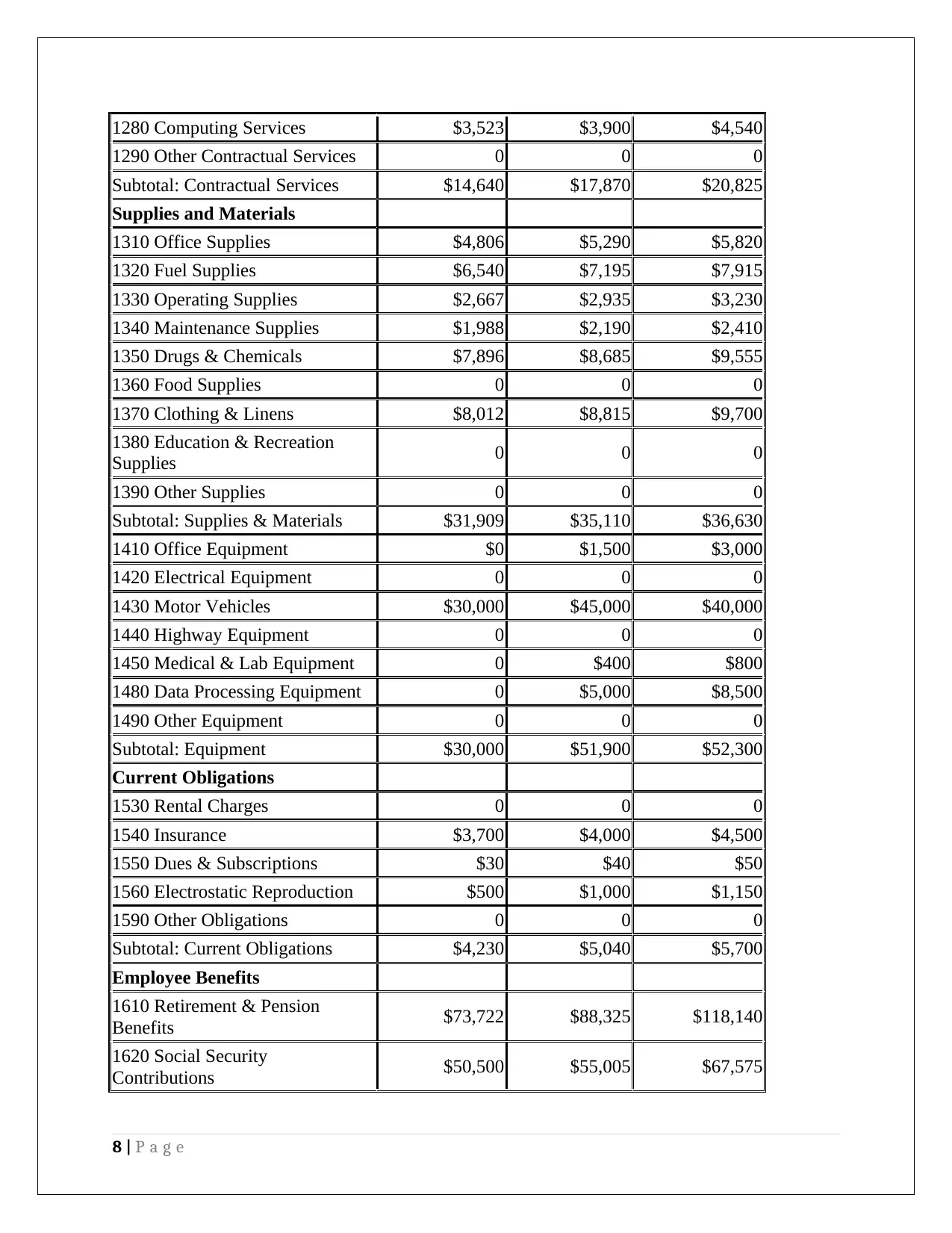

1280 Computing Services $3,523 $3,900 $4,540

1290 Other Contractual Services 0 0 0

Subtotal: Contractual Services $14,640 $17,870 $20,825

Supplies and Materials

1310 Office Supplies $4,806 $5,290 $5,820

1320 Fuel Supplies $6,540 $7,195 $7,915

1330 Operating Supplies $2,667 $2,935 $3,230

1340 Maintenance Supplies $1,988 $2,190 $2,410

1350 Drugs & Chemicals $7,896 $8,685 $9,555

1360 Food Supplies 0 0 0

1370 Clothing & Linens $8,012 $8,815 $9,700

1380 Education & Recreation

Supplies 0 0 0

1390 Other Supplies 0 0 0

Subtotal: Supplies & Materials $31,909 $35,110 $36,630

1410 Office Equipment $0 $1,500 $3,000

1420 Electrical Equipment 0 0 0

1430 Motor Vehicles $30,000 $45,000 $40,000

1440 Highway Equipment 0 0 0

1450 Medical & Lab Equipment 0 $400 $800

1480 Data Processing Equipment 0 $5,000 $8,500

1490 Other Equipment 0 0 0

Subtotal: Equipment $30,000 $51,900 $52,300

Current Obligations

1530 Rental Charges 0 0 0

1540 Insurance $3,700 $4,000 $4,500

1550 Dues & Subscriptions $30 $40 $50

1560 Electrostatic Reproduction $500 $1,000 $1,150

1590 Other Obligations 0 0 0

Subtotal: Current Obligations $4,230 $5,040 $5,700

Employee Benefits

1610 Retirement & Pension

Benefits $73,722 $88,325 $118,140

1620 Social Security

Contributions $50,500 $55,005 $67,575

8 | P a g e

1290 Other Contractual Services 0 0 0

Subtotal: Contractual Services $14,640 $17,870 $20,825

Supplies and Materials

1310 Office Supplies $4,806 $5,290 $5,820

1320 Fuel Supplies $6,540 $7,195 $7,915

1330 Operating Supplies $2,667 $2,935 $3,230

1340 Maintenance Supplies $1,988 $2,190 $2,410

1350 Drugs & Chemicals $7,896 $8,685 $9,555

1360 Food Supplies 0 0 0

1370 Clothing & Linens $8,012 $8,815 $9,700

1380 Education & Recreation

Supplies 0 0 0

1390 Other Supplies 0 0 0

Subtotal: Supplies & Materials $31,909 $35,110 $36,630

1410 Office Equipment $0 $1,500 $3,000

1420 Electrical Equipment 0 0 0

1430 Motor Vehicles $30,000 $45,000 $40,000

1440 Highway Equipment 0 0 0

1450 Medical & Lab Equipment 0 $400 $800

1480 Data Processing Equipment 0 $5,000 $8,500

1490 Other Equipment 0 0 0

Subtotal: Equipment $30,000 $51,900 $52,300

Current Obligations

1530 Rental Charges 0 0 0

1540 Insurance $3,700 $4,000 $4,500

1550 Dues & Subscriptions $30 $40 $50

1560 Electrostatic Reproduction $500 $1,000 $1,150

1590 Other Obligations 0 0 0

Subtotal: Current Obligations $4,230 $5,040 $5,700

Employee Benefits

1610 Retirement & Pension

Benefits $73,722 $88,325 $118,140

1620 Social Security

Contributions $50,500 $55,005 $67,575

8 | P a g e

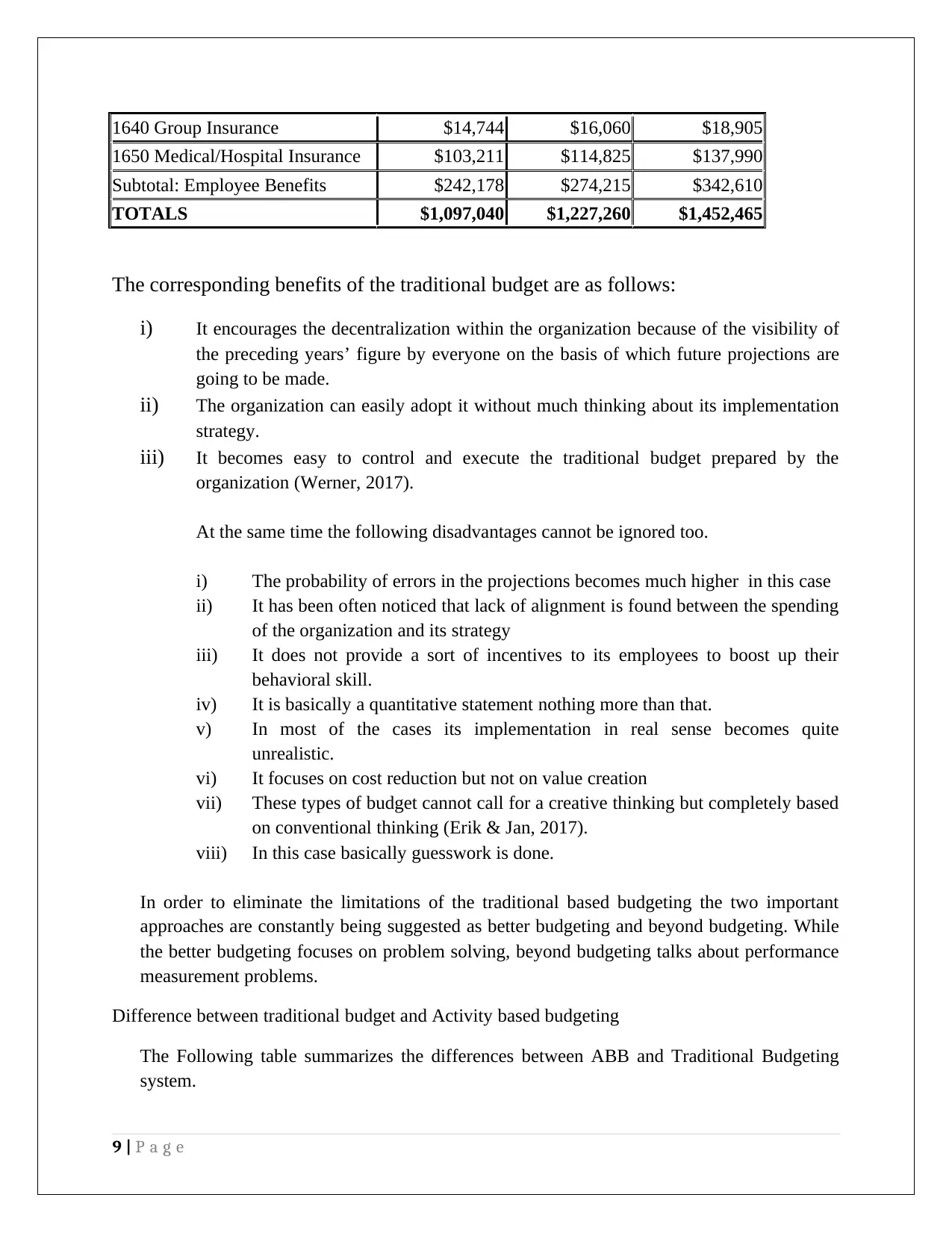

1640 Group Insurance $14,744 $16,060 $18,905

1650 Medical/Hospital Insurance $103,211 $114,825 $137,990

Subtotal: Employee Benefits $242,178 $274,215 $342,610

TOTALS $1,097,040 $1,227,260 $1,452,465

The corresponding benefits of the traditional budget are as follows:

i) It encourages the decentralization within the organization because of the visibility of

the preceding years’ figure by everyone on the basis of which future projections are

going to be made.

ii) The organization can easily adopt it without much thinking about its implementation

strategy.

iii) It becomes easy to control and execute the traditional budget prepared by the

organization (Werner, 2017).

At the same time the following disadvantages cannot be ignored too.

i) The probability of errors in the projections becomes much higher in this case

ii) It has been often noticed that lack of alignment is found between the spending

of the organization and its strategy

iii) It does not provide a sort of incentives to its employees to boost up their

behavioral skill.

iv) It is basically a quantitative statement nothing more than that.

v) In most of the cases its implementation in real sense becomes quite

unrealistic.

vi) It focuses on cost reduction but not on value creation

vii) These types of budget cannot call for a creative thinking but completely based

on conventional thinking (Erik & Jan, 2017).

viii) In this case basically guesswork is done.

In order to eliminate the limitations of the traditional based budgeting the two important

approaches are constantly being suggested as better budgeting and beyond budgeting. While

the better budgeting focuses on problem solving, beyond budgeting talks about performance

measurement problems.

Difference between traditional budget and Activity based budgeting

The Following table summarizes the differences between ABB and Traditional Budgeting

system.

9 | P a g e

1650 Medical/Hospital Insurance $103,211 $114,825 $137,990

Subtotal: Employee Benefits $242,178 $274,215 $342,610

TOTALS $1,097,040 $1,227,260 $1,452,465

The corresponding benefits of the traditional budget are as follows:

i) It encourages the decentralization within the organization because of the visibility of

the preceding years’ figure by everyone on the basis of which future projections are

going to be made.

ii) The organization can easily adopt it without much thinking about its implementation

strategy.

iii) It becomes easy to control and execute the traditional budget prepared by the

organization (Werner, 2017).

At the same time the following disadvantages cannot be ignored too.

i) The probability of errors in the projections becomes much higher in this case

ii) It has been often noticed that lack of alignment is found between the spending

of the organization and its strategy

iii) It does not provide a sort of incentives to its employees to boost up their

behavioral skill.

iv) It is basically a quantitative statement nothing more than that.

v) In most of the cases its implementation in real sense becomes quite

unrealistic.

vi) It focuses on cost reduction but not on value creation

vii) These types of budget cannot call for a creative thinking but completely based

on conventional thinking (Erik & Jan, 2017).

viii) In this case basically guesswork is done.

In order to eliminate the limitations of the traditional based budgeting the two important

approaches are constantly being suggested as better budgeting and beyond budgeting. While

the better budgeting focuses on problem solving, beyond budgeting talks about performance

measurement problems.

Difference between traditional budget and Activity based budgeting

The Following table summarizes the differences between ABB and Traditional Budgeting

system.

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

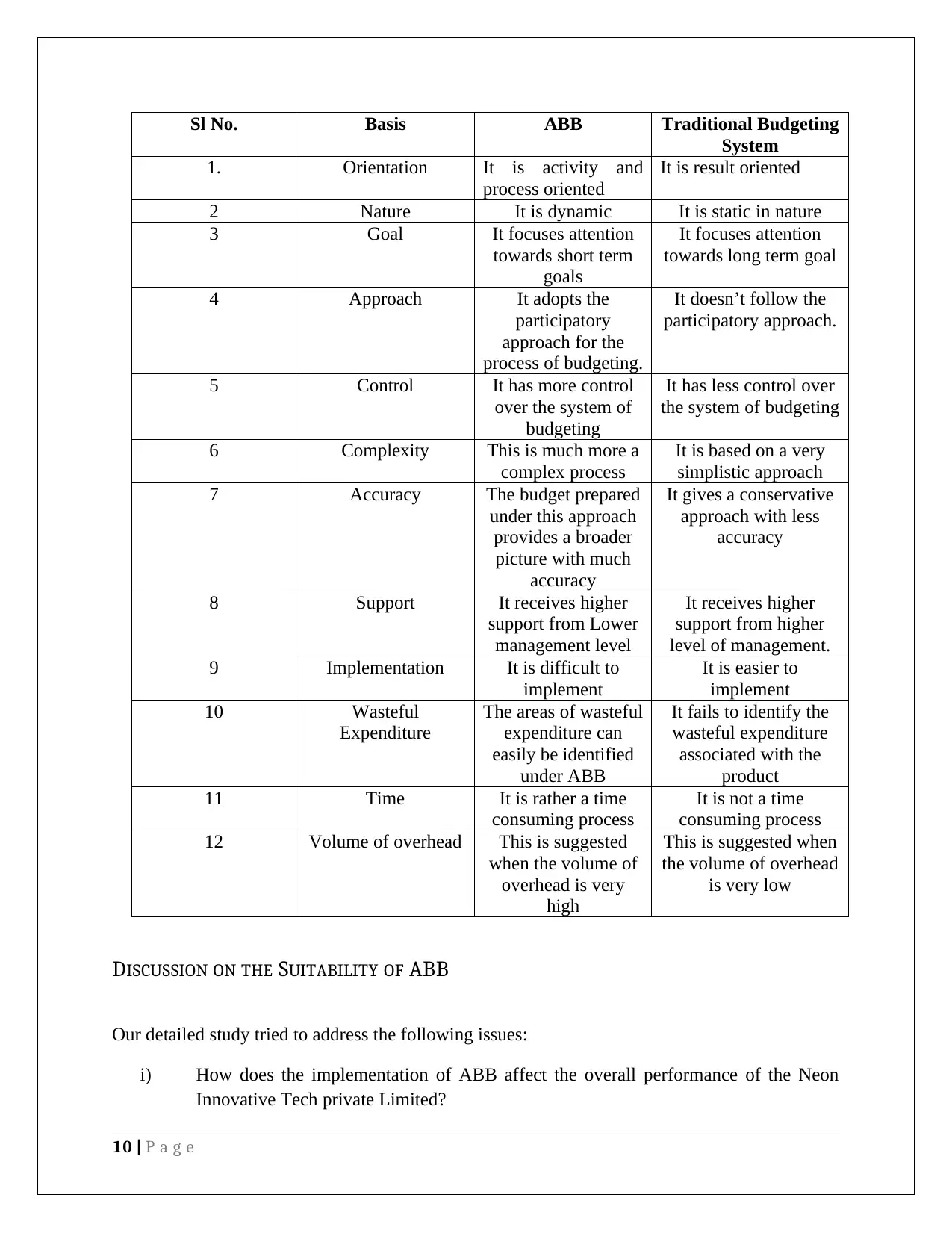

Sl No. Basis ABB Traditional Budgeting

System

1. Orientation It is activity and

process oriented

It is result oriented

2 Nature It is dynamic It is static in nature

3 Goal It focuses attention

towards short term

goals

It focuses attention

towards long term goal

4 Approach It adopts the

participatory

approach for the

process of budgeting.

It doesn’t follow the

participatory approach.

5 Control It has more control

over the system of

budgeting

It has less control over

the system of budgeting

6 Complexity This is much more a

complex process

It is based on a very

simplistic approach

7 Accuracy The budget prepared

under this approach

provides a broader

picture with much

accuracy

It gives a conservative

approach with less

accuracy

8 Support It receives higher

support from Lower

management level

It receives higher

support from higher

level of management.

9 Implementation It is difficult to

implement

It is easier to

implement

10 Wasteful

Expenditure

The areas of wasteful

expenditure can

easily be identified

under ABB

It fails to identify the

wasteful expenditure

associated with the

product

11 Time It is rather a time

consuming process

It is not a time

consuming process

12 Volume of overhead This is suggested

when the volume of

overhead is very

high

This is suggested when

the volume of overhead

is very low

DISCUSSION ON THE SUITABILITY OF ABB

Our detailed study tried to address the following issues:

i) How does the implementation of ABB affect the overall performance of the Neon

Innovative Tech private Limited?

10 | P a g e

System

1. Orientation It is activity and

process oriented

It is result oriented

2 Nature It is dynamic It is static in nature

3 Goal It focuses attention

towards short term

goals

It focuses attention

towards long term goal

4 Approach It adopts the

participatory

approach for the

process of budgeting.

It doesn’t follow the

participatory approach.

5 Control It has more control

over the system of

budgeting

It has less control over

the system of budgeting

6 Complexity This is much more a

complex process

It is based on a very

simplistic approach

7 Accuracy The budget prepared

under this approach

provides a broader

picture with much

accuracy

It gives a conservative

approach with less

accuracy

8 Support It receives higher

support from Lower

management level

It receives higher

support from higher

level of management.

9 Implementation It is difficult to

implement

It is easier to

implement

10 Wasteful

Expenditure

The areas of wasteful

expenditure can

easily be identified

under ABB

It fails to identify the

wasteful expenditure

associated with the

product

11 Time It is rather a time

consuming process

It is not a time

consuming process

12 Volume of overhead This is suggested

when the volume of

overhead is very

high

This is suggested when

the volume of overhead

is very low

DISCUSSION ON THE SUITABILITY OF ABB

Our detailed study tried to address the following issues:

i) How does the implementation of ABB affect the overall performance of the Neon

Innovative Tech private Limited?

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ii) Whether improvement in the allocation of institutional resources can be achieved

through the correct estimation of costs associated with the company?

iii) What is the procedure to be applied for the effective implementation of ABB in case

of our client company?

iv) Whether in case of our client company as the sufficient information about its costs

were not collected due to which it failed to make appropriate decision in appropriate

cases?

v) Does the company have sufficient time and resources available to implement the

system of ABB?

vi) Whether the organization has the sufficient resources to meet the cost requirement for

the implementation of the ABB?

As it is clear that our Client, being an IT company for whom ascertainment of the accurate

figures for the costs associated with its services are difficult to figure as the services provided are

mostly intangible ones, that is the first step towards implementation of the Activity based

budgeting (Delone & Mclean, 2004).

In our case the major challenges faced by us during conducting the detailed survey on the

feasibility of implementing the Activity based budgeting for Neon Innovative Tech private

limited was because of the frequent technological changes in the IT environment of the Company

the collection of the relevant information became a limitation for us. Still based on our study we

can recommend the following for the evaluation of the suitability for the implementation of the

ABB within the Company.

1. In order to ensure the ABB in the current scenario, the support and acceptance of the

senior management is demanded first along with the creation of awareness amongst the

employee about its impact on overall organizational goals. For which a detailed

discussion on this issue is being suggested as employees of the Neon Innovative Tech

private limited have been found not adequately equipped with the implementation of the

ABB (Das, 2017).

2. ABB can be of great help to our company while conducting a comparative analysis of the

various IT services provided by it through which the return on investment from its

various projects can be more accurately calculated.

3. As the company has incurred huge expenditure in terms of salary and remuneration to its

workforce because of which it failed to make required investments in other relevant area

like network connectivity, software and hardware, hence ABB can assist it to achieve this

objective.

4. In case of our company, the determination of the correct size of the cost driver has found

to be highly time consuming, hence it seems that its implementation can take long period

(Grenier, 2017).

11 | P a g e

through the correct estimation of costs associated with the company?

iii) What is the procedure to be applied for the effective implementation of ABB in case

of our client company?

iv) Whether in case of our client company as the sufficient information about its costs

were not collected due to which it failed to make appropriate decision in appropriate

cases?

v) Does the company have sufficient time and resources available to implement the

system of ABB?

vi) Whether the organization has the sufficient resources to meet the cost requirement for

the implementation of the ABB?

As it is clear that our Client, being an IT company for whom ascertainment of the accurate

figures for the costs associated with its services are difficult to figure as the services provided are

mostly intangible ones, that is the first step towards implementation of the Activity based

budgeting (Delone & Mclean, 2004).

In our case the major challenges faced by us during conducting the detailed survey on the

feasibility of implementing the Activity based budgeting for Neon Innovative Tech private

limited was because of the frequent technological changes in the IT environment of the Company

the collection of the relevant information became a limitation for us. Still based on our study we

can recommend the following for the evaluation of the suitability for the implementation of the

ABB within the Company.

1. In order to ensure the ABB in the current scenario, the support and acceptance of the

senior management is demanded first along with the creation of awareness amongst the

employee about its impact on overall organizational goals. For which a detailed

discussion on this issue is being suggested as employees of the Neon Innovative Tech

private limited have been found not adequately equipped with the implementation of the

ABB (Das, 2017).

2. ABB can be of great help to our company while conducting a comparative analysis of the

various IT services provided by it through which the return on investment from its

various projects can be more accurately calculated.

3. As the company has incurred huge expenditure in terms of salary and remuneration to its

workforce because of which it failed to make required investments in other relevant area

like network connectivity, software and hardware, hence ABB can assist it to achieve this

objective.

4. In case of our company, the determination of the correct size of the cost driver has found

to be highly time consuming, hence it seems that its implementation can take long period

(Grenier, 2017).

11 | P a g e

5. We have conducted an interview of around 51% of the employees at different level

associated with the company out of which 61% employees have expressed that senior

management’s approach towards implementation of ABB is democratic in nature,

whereas rest of the 39% termed it as autocratic in nature.

CONCLUSION

Based on the overall analysis of the current IT environment of the Neon Innovative Tech Private

Limited, it is being suggested to implement the ABB system in order to capitalize its tentative

benefits associated with the IT Company. It is a new cost technique which will help the company

in the long run in minimizing the overall costs and increasing the efficiency. Furthermore, since

the company being discussed here is a big company by volume, so Activity Based Budgeting

would fit into the schemes as the cost benefit analysis is in favor of the organization.

REFERENCES

Arnott, D., Lizama, F. & Song, Y., 2017. Patterns of business intelligence systems use in

organizations. Decision Support Systems, Volume 97, pp. 58-68.

12 | P a g e

associated with the company out of which 61% employees have expressed that senior

management’s approach towards implementation of ABB is democratic in nature,

whereas rest of the 39% termed it as autocratic in nature.

CONCLUSION

Based on the overall analysis of the current IT environment of the Neon Innovative Tech Private

Limited, it is being suggested to implement the ABB system in order to capitalize its tentative

benefits associated with the IT Company. It is a new cost technique which will help the company

in the long run in minimizing the overall costs and increasing the efficiency. Furthermore, since

the company being discussed here is a big company by volume, so Activity Based Budgeting

would fit into the schemes as the cost benefit analysis is in favor of the organization.

REFERENCES

Arnott, D., Lizama, F. & Song, Y., 2017. Patterns of business intelligence systems use in

organizations. Decision Support Systems, Volume 97, pp. 58-68.

12 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.