Nestle Australia: Budgetary Slack and Decision Making Report

VerifiedAdded on 2020/03/28

|10

|2365

|117

Report

AI Summary

This report examines budgetary slack, its definition, and its consequences for Nestle Australia's operations. It explores the ethical implications of branch managers' behavior, particularly concerning bonus programs and how they can encourage budget slack. The report analyzes the decision to manufacture versus buy, specifically for Water World Ltd, providing a cost analysis of both options and recommending the most cost-effective choice. The analysis includes detailed tables comparing manufacturing and buying costs, considering factors such as supervisor salaries, direct wages, material costs, and transport costs. The report concludes with recommendations for Water World Ltd and discusses additional factors that should be considered when making the decision to manufacture or buy, such as in-house expertise and long-term supplier relationships.

Running head: ASSESSMENT 3 - GROUP REPORT 1

Assessment 3 - Group Report

Author’s Name

Institution’s Name

Date

Assessment 3 - Group Report

Author’s Name

Institution’s Name

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ASSESSMENT 3 - GROUP REPORT 2

Task 1

Although the notion of the budgetary slack has been discussed all the way since 1953,

the issues are stick of greater importance today. According to Douglas (2002), there are still

some unresolved issues about budgetary slack one of which include consequences of

budgetary slack on organization’s operations and performance. Previous researches has

identified some negative and positive consequences of budgetary slack including motivating

employees; hence, improving organization’s performance. The conflicting issues on direction

of the consequences contribute to the unresolved issues (Van der Stede, 2000). With these

considerations, this report aims to present description of budgetary slack, its consequences on

Nestle Australia performance, ethics of the branch managers’ behaviour in relation to Nestle

Australia case study as well as how bonus programs could encourage budget slack and how

to resolve such issues.

Meaning of Budgetary Slack

This is usually the cautious move of under-estimating budgeted proceeds or over-

estimating budgeted costs. Basically, budgetary slack is the allowance for additional

investments and expenses for future cash flow of an organization. It is an intentional act of

underestimating revenue as well as productive capacities or overestimating of resources and

costs needed in completing a budgeted task (Fisher, Maines, Peffer & Sprinkle 2002).

Further, budgetary slack is the allowance for additional expense that an organization is going

to incur in future. For instance, if the manager believes cost of the raw materials would be

$10,000 but provide budgetary projection of around $15,000, the manager has $5,000 as

budgetary slack. In essence, it is the practice where enough amount of the intentional

allowance is introduced in a budget for miscellaneous expenses an organization is going to

sustain. This permits management of any organization much better chance of generating their

numbers which is specifically significant for them in case the performance appraisal as well

Task 1

Although the notion of the budgetary slack has been discussed all the way since 1953,

the issues are stick of greater importance today. According to Douglas (2002), there are still

some unresolved issues about budgetary slack one of which include consequences of

budgetary slack on organization’s operations and performance. Previous researches has

identified some negative and positive consequences of budgetary slack including motivating

employees; hence, improving organization’s performance. The conflicting issues on direction

of the consequences contribute to the unresolved issues (Van der Stede, 2000). With these

considerations, this report aims to present description of budgetary slack, its consequences on

Nestle Australia performance, ethics of the branch managers’ behaviour in relation to Nestle

Australia case study as well as how bonus programs could encourage budget slack and how

to resolve such issues.

Meaning of Budgetary Slack

This is usually the cautious move of under-estimating budgeted proceeds or over-

estimating budgeted costs. Basically, budgetary slack is the allowance for additional

investments and expenses for future cash flow of an organization. It is an intentional act of

underestimating revenue as well as productive capacities or overestimating of resources and

costs needed in completing a budgeted task (Fisher, Maines, Peffer & Sprinkle 2002).

Further, budgetary slack is the allowance for additional expense that an organization is going

to incur in future. For instance, if the manager believes cost of the raw materials would be

$10,000 but provide budgetary projection of around $15,000, the manager has $5,000 as

budgetary slack. In essence, it is the practice where enough amount of the intentional

allowance is introduced in a budget for miscellaneous expenses an organization is going to

sustain. This permits management of any organization much better chance of generating their

numbers which is specifically significant for them in case the performance appraisal as well

ASSESSMENT 3 - GROUP REPORT 3

as bonuses are tied up to accomplishment of the budgeted numbers. In addition, budgetary

slack might also take place whenever there is some considerable uncertainty on outcomes to

be anticipated in future (Mohamad Adnan & Sulaiman, 2007). Therefore, managers of

different organizations usually tend to be a bit conservative when producing budgets under

these conditions. This is mostly common in producing budget for the whole new production,

where past records of the probable outcomes that could be relied on are absent.

It is most common whenever an organization utilizes participating budgeting as this

budgeting comprises of participation of wide range of employees that provides a chance for

more people to introduce the budgetary slack in the budget. In essence, budgetary slack is

linked with dysfunctional behaviours; accomplishment of the budget target without more

effort, ineffective resource allocation, unreliable information as well as unethical behaviour

(Maiga & Jacobs, 2008). Practically, budgetary slack could be introduced in account of an

organization in either when revenues or incomes of the company are underestimated. This

would understate profit of an organization and the firm would show negative financial status.

Secondly, it could also be introduced when expenses are overstated. This would result in

decreased profits. Since budgetary slack involuntarily understates profit of an organization no

matter which technique is taken, the management of an organization is not involved in the

decisions. With the carelessness and negligence of the management, budgetary slack could be

approved but the board might not be involved in these activities. to be more specific,

budgetary slack is the practice of artificially adjusting the budget in order to make the

manager look better.

Consequences of the Budgetary Slack for Nestle Australia Operations

In this case, budgetary slack is more likely to affect operations of Nestle Australia

negatively. For instance, it might interfere with its corporate performance, since employees of

this company only have incentive to meet their budgetary objectives, which is relatively low.

as bonuses are tied up to accomplishment of the budgeted numbers. In addition, budgetary

slack might also take place whenever there is some considerable uncertainty on outcomes to

be anticipated in future (Mohamad Adnan & Sulaiman, 2007). Therefore, managers of

different organizations usually tend to be a bit conservative when producing budgets under

these conditions. This is mostly common in producing budget for the whole new production,

where past records of the probable outcomes that could be relied on are absent.

It is most common whenever an organization utilizes participating budgeting as this

budgeting comprises of participation of wide range of employees that provides a chance for

more people to introduce the budgetary slack in the budget. In essence, budgetary slack is

linked with dysfunctional behaviours; accomplishment of the budget target without more

effort, ineffective resource allocation, unreliable information as well as unethical behaviour

(Maiga & Jacobs, 2008). Practically, budgetary slack could be introduced in account of an

organization in either when revenues or incomes of the company are underestimated. This

would understate profit of an organization and the firm would show negative financial status.

Secondly, it could also be introduced when expenses are overstated. This would result in

decreased profits. Since budgetary slack involuntarily understates profit of an organization no

matter which technique is taken, the management of an organization is not involved in the

decisions. With the carelessness and negligence of the management, budgetary slack could be

approved but the board might not be involved in these activities. to be more specific,

budgetary slack is the practice of artificially adjusting the budget in order to make the

manager look better.

Consequences of the Budgetary Slack for Nestle Australia Operations

In this case, budgetary slack is more likely to affect operations of Nestle Australia

negatively. For instance, it might interfere with its corporate performance, since employees of

this company only have incentive to meet their budgetary objectives, which is relatively low.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ASSESSMENT 3 - GROUP REPORT 4

In addition, budgetary slack might also result in a decrease in performance of Nestle

Australia in comparison to its more aggressive competitor who makes use of the stretch

goals. Therefore, budgetary slack is more likely to have some long-term negative effect on

competitive position and profitability of Nestle Australia. Further, budget slack could also

undermine usefulness and credibility of Nestle Australia budget as the planning and control

technique. Therefore, when Nestle Australia budget includes a slack, the total amount in its

budget could no longer reveal truthful view of its forthcoming operations. This is based on

the notion that budget slack undermines usefulness and credibility of an organization’s

budget as the control and planning tool (Lau & Eggleton, 2004). In addition, budgetary slack

could increase inefficiencies in Nestle Australia resource allocation and could also affect

operating performance of this company.

Despite of these negative consequences, budgetary slack is also believed to lead to

positive impact on Nestle Australia. It is used in motivating personnel, enabling the work to

accomplish objective of management and managing budget risks. Further, budgetary slack

could also encourage creativity and innovation of personnel, resolve conflicts and absorb

stress amongst employees. This indicates that budgetary slack increases performance of

different personnel in Nestle Australia and its operations. In essence, budgetary slack

encourages employees’ creativity and innovation, resolved conflicting objectives and

absorbed tension; hence, it could lead to accomplishment of Nestle Australia objectives.

Ethics of the branch managers’ behaviour

Some of the ethics of the branch manager’s behaviour is the act of changing original

budget and setting budget lower and therefore getting rewarded.

How Bonus Program Could Encourage Budgetary Slack

Organization’s bonus system at times encourages budgetary slack. This is mainly due

to the fact that the bonus programs are determined by number of products produced or

In addition, budgetary slack might also result in a decrease in performance of Nestle

Australia in comparison to its more aggressive competitor who makes use of the stretch

goals. Therefore, budgetary slack is more likely to have some long-term negative effect on

competitive position and profitability of Nestle Australia. Further, budget slack could also

undermine usefulness and credibility of Nestle Australia budget as the planning and control

technique. Therefore, when Nestle Australia budget includes a slack, the total amount in its

budget could no longer reveal truthful view of its forthcoming operations. This is based on

the notion that budget slack undermines usefulness and credibility of an organization’s

budget as the control and planning tool (Lau & Eggleton, 2004). In addition, budgetary slack

could increase inefficiencies in Nestle Australia resource allocation and could also affect

operating performance of this company.

Despite of these negative consequences, budgetary slack is also believed to lead to

positive impact on Nestle Australia. It is used in motivating personnel, enabling the work to

accomplish objective of management and managing budget risks. Further, budgetary slack

could also encourage creativity and innovation of personnel, resolve conflicts and absorb

stress amongst employees. This indicates that budgetary slack increases performance of

different personnel in Nestle Australia and its operations. In essence, budgetary slack

encourages employees’ creativity and innovation, resolved conflicting objectives and

absorbed tension; hence, it could lead to accomplishment of Nestle Australia objectives.

Ethics of the branch managers’ behaviour

Some of the ethics of the branch manager’s behaviour is the act of changing original

budget and setting budget lower and therefore getting rewarded.

How Bonus Program Could Encourage Budgetary Slack

Organization’s bonus system at times encourages budgetary slack. This is mainly due

to the fact that the bonus programs are determined by number of products produced or

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ASSESSMENT 3 - GROUP REPORT 5

services offered over budgeted numbers and there is some incentive for managers for

understating their projection of the level of their production (Etemadi & Sirghani, 2016).

Description of improved production or performance manager’s behaviour indicates the

evidence of understatement. Thus, a percentage increase over the organization’s current

production would imply that additional production in future. The projection would make it

likely that actual number of the new products produced would exceed budgeted number.

To overcome such issues in future, the management of Nestle Australia should give

incentives to its key executives to achieve the budgetary projections as well as be able to give

accurate projections. The manager can also overcome the issue of budgetary slack by evading

overreliance on budgets as negative, evaluative tools. Further, to overcome such issues, the

management needs to come up with a common bonus programs that requires managements to

submit the budget for thorough assessment before passing them on. In addition, the

organization could consider some alternative measures in balancing the dysfunctional that is

encouraged by its current bonus program. This could include rewarding bonus for any

increase in operations or production. Perhaps they should pay bonuses for every one per cent

increase in target. Bonuses should also be based on performance targets; hence, encouraging

managers to maintain their client satisfaction and reduce in client complaints.

Further, to avoid such circumstances, the management should target to unattainable

levels; hence, demotivating revenue force. Here, the management would be commanding

targets on sales personnel while motivation is stirred by setting up the targets that would be

inclined by relevant sales representative (Van der Stede, 2000). This would make the sales

personnel work hard to achieve higher results instead of setting achievable outcomes. This

would tend to reduce issues of budgetary slack emerging from introduction of bonuses.

Task 2

services offered over budgeted numbers and there is some incentive for managers for

understating their projection of the level of their production (Etemadi & Sirghani, 2016).

Description of improved production or performance manager’s behaviour indicates the

evidence of understatement. Thus, a percentage increase over the organization’s current

production would imply that additional production in future. The projection would make it

likely that actual number of the new products produced would exceed budgeted number.

To overcome such issues in future, the management of Nestle Australia should give

incentives to its key executives to achieve the budgetary projections as well as be able to give

accurate projections. The manager can also overcome the issue of budgetary slack by evading

overreliance on budgets as negative, evaluative tools. Further, to overcome such issues, the

management needs to come up with a common bonus programs that requires managements to

submit the budget for thorough assessment before passing them on. In addition, the

organization could consider some alternative measures in balancing the dysfunctional that is

encouraged by its current bonus program. This could include rewarding bonus for any

increase in operations or production. Perhaps they should pay bonuses for every one per cent

increase in target. Bonuses should also be based on performance targets; hence, encouraging

managers to maintain their client satisfaction and reduce in client complaints.

Further, to avoid such circumstances, the management should target to unattainable

levels; hence, demotivating revenue force. Here, the management would be commanding

targets on sales personnel while motivation is stirred by setting up the targets that would be

inclined by relevant sales representative (Van der Stede, 2000). This would make the sales

personnel work hard to achieve higher results instead of setting achievable outcomes. This

would tend to reduce issues of budgetary slack emerging from introduction of bonuses.

Task 2

ASSESSMENT 3 - GROUP REPORT 6

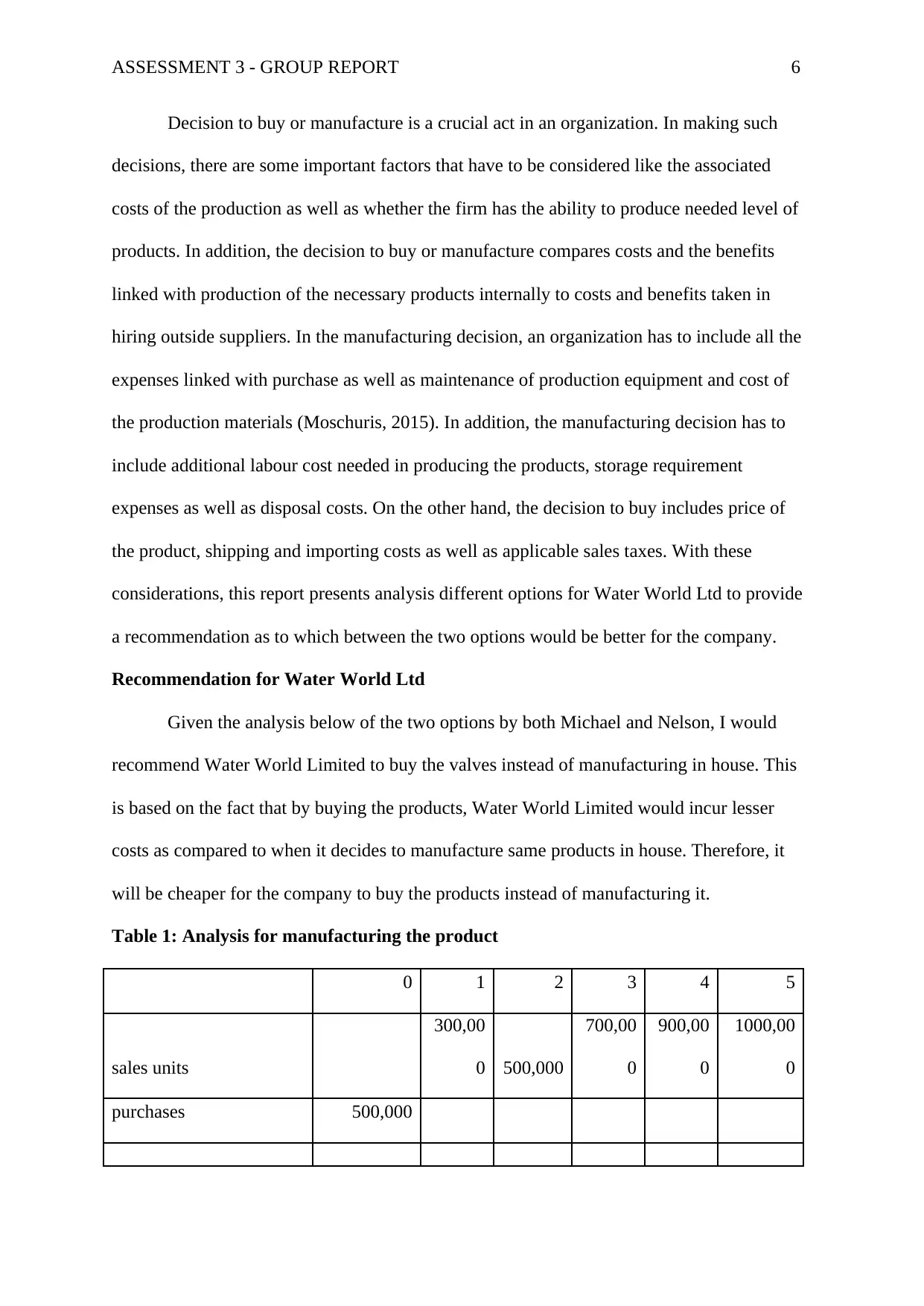

Decision to buy or manufacture is a crucial act in an organization. In making such

decisions, there are some important factors that have to be considered like the associated

costs of the production as well as whether the firm has the ability to produce needed level of

products. In addition, the decision to buy or manufacture compares costs and the benefits

linked with production of the necessary products internally to costs and benefits taken in

hiring outside suppliers. In the manufacturing decision, an organization has to include all the

expenses linked with purchase as well as maintenance of production equipment and cost of

the production materials (Moschuris, 2015). In addition, the manufacturing decision has to

include additional labour cost needed in producing the products, storage requirement

expenses as well as disposal costs. On the other hand, the decision to buy includes price of

the product, shipping and importing costs as well as applicable sales taxes. With these

considerations, this report presents analysis different options for Water World Ltd to provide

a recommendation as to which between the two options would be better for the company.

Recommendation for Water World Ltd

Given the analysis below of the two options by both Michael and Nelson, I would

recommend Water World Limited to buy the valves instead of manufacturing in house. This

is based on the fact that by buying the products, Water World Limited would incur lesser

costs as compared to when it decides to manufacture same products in house. Therefore, it

will be cheaper for the company to buy the products instead of manufacturing it.

Table 1: Analysis for manufacturing the product

0 1 2 3 4 5

sales units

300,00

0 500,000

700,00

0

900,00

0

1000,00

0

purchases 500,000

Decision to buy or manufacture is a crucial act in an organization. In making such

decisions, there are some important factors that have to be considered like the associated

costs of the production as well as whether the firm has the ability to produce needed level of

products. In addition, the decision to buy or manufacture compares costs and the benefits

linked with production of the necessary products internally to costs and benefits taken in

hiring outside suppliers. In the manufacturing decision, an organization has to include all the

expenses linked with purchase as well as maintenance of production equipment and cost of

the production materials (Moschuris, 2015). In addition, the manufacturing decision has to

include additional labour cost needed in producing the products, storage requirement

expenses as well as disposal costs. On the other hand, the decision to buy includes price of

the product, shipping and importing costs as well as applicable sales taxes. With these

considerations, this report presents analysis different options for Water World Ltd to provide

a recommendation as to which between the two options would be better for the company.

Recommendation for Water World Ltd

Given the analysis below of the two options by both Michael and Nelson, I would

recommend Water World Limited to buy the valves instead of manufacturing in house. This

is based on the fact that by buying the products, Water World Limited would incur lesser

costs as compared to when it decides to manufacture same products in house. Therefore, it

will be cheaper for the company to buy the products instead of manufacturing it.

Table 1: Analysis for manufacturing the product

0 1 2 3 4 5

sales units

300,00

0 500,000

700,00

0

900,00

0

1000,00

0

purchases 500,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ASSESSMENT 3 - GROUP REPORT 7

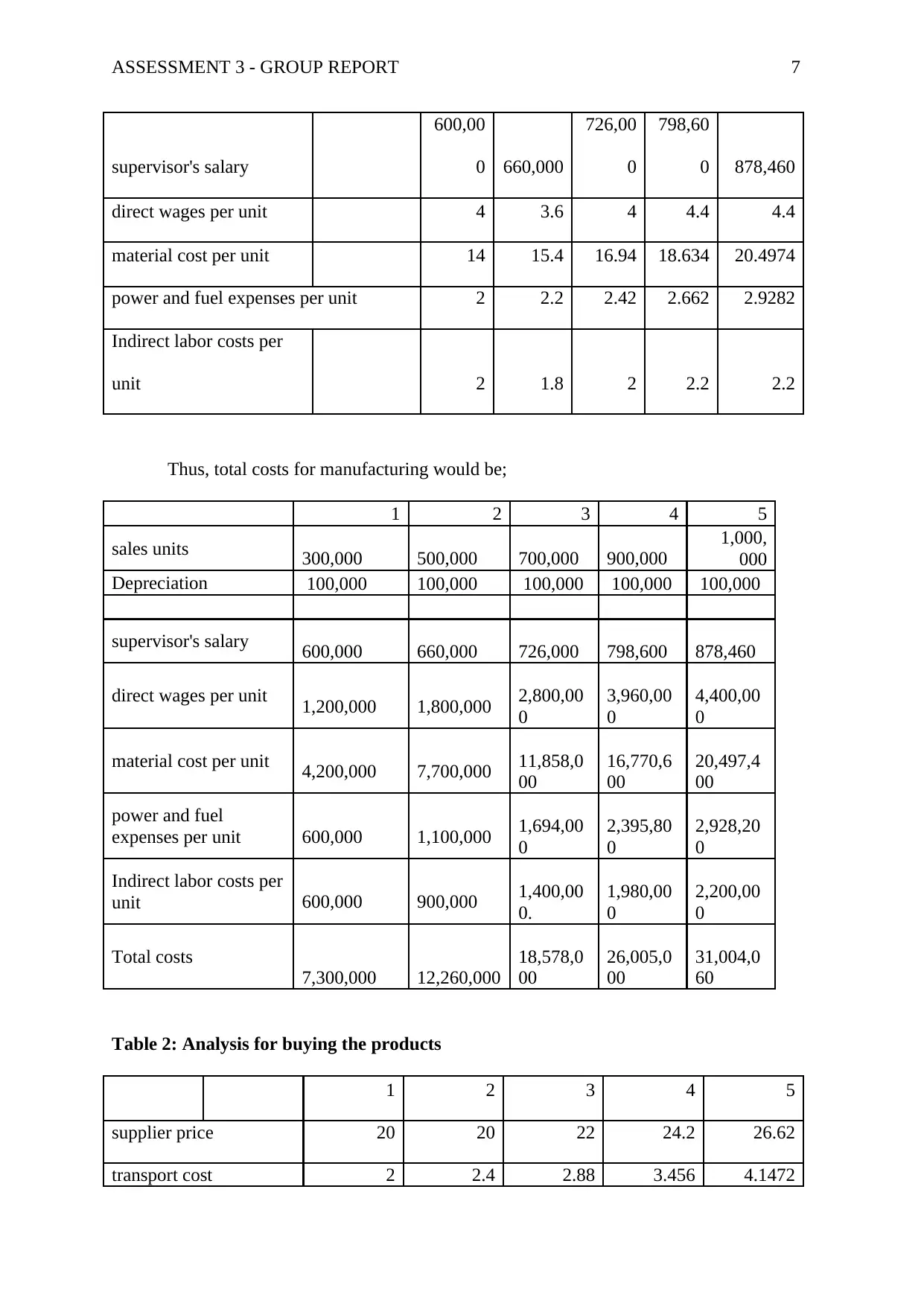

supervisor's salary

600,00

0 660,000

726,00

0

798,60

0 878,460

direct wages per unit 4 3.6 4 4.4 4.4

material cost per unit 14 15.4 16.94 18.634 20.4974

power and fuel expenses per unit 2 2.2 2.42 2.662 2.9282

Indirect labor costs per

unit 2 1.8 2 2.2 2.2

Thus, total costs for manufacturing would be;

1 2 3 4 5

sales units 300,000 500,000 700,000 900,000

1,000,

000

Depreciation 100,000 100,000 100,000 100,000 100,000

supervisor's salary 600,000 660,000 726,000 798,600 878,460

direct wages per unit 1,200,000 1,800,000 2,800,00

0

3,960,00

0

4,400,00

0

material cost per unit 4,200,000 7,700,000 11,858,0

00

16,770,6

00

20,497,4

00

power and fuel

expenses per unit 600,000 1,100,000 1,694,00

0

2,395,80

0

2,928,20

0

Indirect labor costs per

unit 600,000 900,000 1,400,00

0.

1,980,00

0

2,200,00

0

Total costs

7,300,000 12,260,000

18,578,0

00

26,005,0

00

31,004,0

60

Table 2: Analysis for buying the products

1 2 3 4 5

supplier price 20 20 22 24.2 26.62

transport cost 2 2.4 2.88 3.456 4.1472

supervisor's salary

600,00

0 660,000

726,00

0

798,60

0 878,460

direct wages per unit 4 3.6 4 4.4 4.4

material cost per unit 14 15.4 16.94 18.634 20.4974

power and fuel expenses per unit 2 2.2 2.42 2.662 2.9282

Indirect labor costs per

unit 2 1.8 2 2.2 2.2

Thus, total costs for manufacturing would be;

1 2 3 4 5

sales units 300,000 500,000 700,000 900,000

1,000,

000

Depreciation 100,000 100,000 100,000 100,000 100,000

supervisor's salary 600,000 660,000 726,000 798,600 878,460

direct wages per unit 1,200,000 1,800,000 2,800,00

0

3,960,00

0

4,400,00

0

material cost per unit 4,200,000 7,700,000 11,858,0

00

16,770,6

00

20,497,4

00

power and fuel

expenses per unit 600,000 1,100,000 1,694,00

0

2,395,80

0

2,928,20

0

Indirect labor costs per

unit 600,000 900,000 1,400,00

0.

1,980,00

0

2,200,00

0

Total costs

7,300,000 12,260,000

18,578,0

00

26,005,0

00

31,004,0

60

Table 2: Analysis for buying the products

1 2 3 4 5

supplier price 20 20 22 24.2 26.62

transport cost 2 2.4 2.88 3.456 4.1472

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ASSESSMENT 3 - GROUP REPORT 8

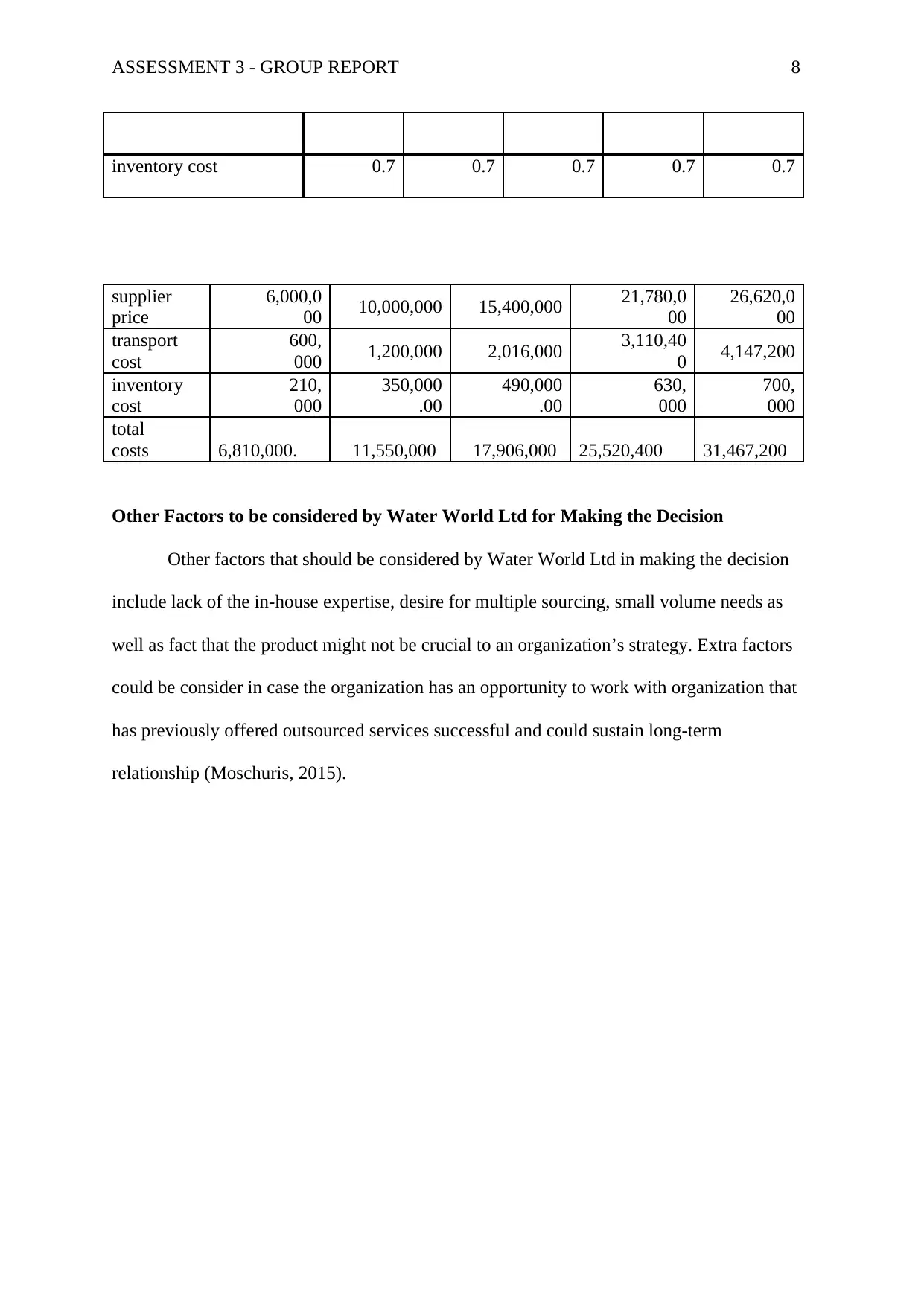

inventory cost 0.7 0.7 0.7 0.7 0.7

supplier

price

6,000,0

00 10,000,000 15,400,000 21,780,0

00

26,620,0

00

transport

cost

600,

000 1,200,000 2,016,000 3,110,40

0 4,147,200

inventory

cost

210,

000

350,000

.00

490,000

.00

630,

000

700,

000

total

costs 6,810,000. 11,550,000 17,906,000 25,520,400 31,467,200

Other Factors to be considered by Water World Ltd for Making the Decision

Other factors that should be considered by Water World Ltd in making the decision

include lack of the in-house expertise, desire for multiple sourcing, small volume needs as

well as fact that the product might not be crucial to an organization’s strategy. Extra factors

could be consider in case the organization has an opportunity to work with organization that

has previously offered outsourced services successful and could sustain long-term

relationship (Moschuris, 2015).

inventory cost 0.7 0.7 0.7 0.7 0.7

supplier

price

6,000,0

00 10,000,000 15,400,000 21,780,0

00

26,620,0

00

transport

cost

600,

000 1,200,000 2,016,000 3,110,40

0 4,147,200

inventory

cost

210,

000

350,000

.00

490,000

.00

630,

000

700,

000

total

costs 6,810,000. 11,550,000 17,906,000 25,520,400 31,467,200

Other Factors to be considered by Water World Ltd for Making the Decision

Other factors that should be considered by Water World Ltd in making the decision

include lack of the in-house expertise, desire for multiple sourcing, small volume needs as

well as fact that the product might not be crucial to an organization’s strategy. Extra factors

could be consider in case the organization has an opportunity to work with organization that

has previously offered outsourced services successful and could sustain long-term

relationship (Moschuris, 2015).

ASSESSMENT 3 - GROUP REPORT 9

References

Douglas, E.S. (2002).The effects of reputation and ethics on budgetary slack. Journal of

Management Accounting Research 14: 153.

Etemadi, H., & Sirghani, S. (2016). The effect of the budget slack creation and budget

internal control by managers on maximization of utility function in budgetary

participation. International Journal of Finance & Managerial Accounting, 1(2), 37-

49.

Fisher, J. G., Maines, L. A., Peffer, S.A., & Sprinkle G. B. (2002).Using budgets for

performance evaluation: Effects of resource allocation and horizontal information

asymmetry on budget proposals, budget slack, and performace. The Accounting

Review 77 (4): 847-865.

Frezatti, F., Beck, F., & da Silva, J. O. (2013). Percepções sobre a criação de reservas

orçamentárias em processo orçamentário participativo. Revista de Educação e

Pesquisa em Contabilidade (REPeC), 7(4).

Lau, C. M. & Eggleton, R.C. (2004).Cultural Differences in managers’ propens ity to create

slack. Advances in International Accounting 17: 137-174.

Maiga, A. S. & Jacobs, F. A. (2008). Moderating Effect of Manager’s Ethical Judgment on

the relationship between budget participation and budget slack. Advances in

Accounting, 23, 113–145.

Mohamad Adnan, S. & Sulaiman, M. (2007). Organizational, cultural and religious factors of

budgetary slack creation: Empirical evidence from Malaysia, International Review of

Business Research Papers, 3(3),17-34.

Moschuris, S. J. (2015). Decision-making criteria in tactical make-or-buy issues: an empirical

analysis. EuroMed Journal of Business, 10(1), 2-20.

References

Douglas, E.S. (2002).The effects of reputation and ethics on budgetary slack. Journal of

Management Accounting Research 14: 153.

Etemadi, H., & Sirghani, S. (2016). The effect of the budget slack creation and budget

internal control by managers on maximization of utility function in budgetary

participation. International Journal of Finance & Managerial Accounting, 1(2), 37-

49.

Fisher, J. G., Maines, L. A., Peffer, S.A., & Sprinkle G. B. (2002).Using budgets for

performance evaluation: Effects of resource allocation and horizontal information

asymmetry on budget proposals, budget slack, and performace. The Accounting

Review 77 (4): 847-865.

Frezatti, F., Beck, F., & da Silva, J. O. (2013). Percepções sobre a criação de reservas

orçamentárias em processo orçamentário participativo. Revista de Educação e

Pesquisa em Contabilidade (REPeC), 7(4).

Lau, C. M. & Eggleton, R.C. (2004).Cultural Differences in managers’ propens ity to create

slack. Advances in International Accounting 17: 137-174.

Maiga, A. S. & Jacobs, F. A. (2008). Moderating Effect of Manager’s Ethical Judgment on

the relationship between budget participation and budget slack. Advances in

Accounting, 23, 113–145.

Mohamad Adnan, S. & Sulaiman, M. (2007). Organizational, cultural and religious factors of

budgetary slack creation: Empirical evidence from Malaysia, International Review of

Business Research Papers, 3(3),17-34.

Moschuris, S. J. (2015). Decision-making criteria in tactical make-or-buy issues: an empirical

analysis. EuroMed Journal of Business, 10(1), 2-20.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ASSESSMENT 3 - GROUP REPORT 10

Van der Stede, W. A. (2000). The relationship between two consequences of budgetary

controls: budgetary slack creation and managerial short-term orientation. Accounting,

Organizations and Society, 25(6), 609-622.

Van der Stede, W. A. (2000). The relationship between two consequences of budgetary

controls: budgetary slack creation and managerial short-term orientation. Accounting,

Organizations and Society, 25(6), 609-622.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.