Analyzing Balanced Scorecard Implementation at Nestle Company

VerifiedAdded on 2021/05/31

|17

|4160

|41

Report

AI Summary

This report provides a comprehensive analysis of the Balanced Scorecard system and its application within Nestle Company. It begins with an executive summary and introduction, followed by an overview of Nestle, highlighting its position as a leading global food and beverage company. The core of the report focuses on the Balanced Scorecard, detailing its four perspectives (financial, customer, internal business processes, and learning and growth), its features, and its implementation within Nestle. The report also contrasts the Balanced Scorecard with traditional performance measurement systems, emphasizing the limitations of solely financial metrics. Furthermore, it assesses the suitability of the Balanced Scorecard for Nestle, covering operational activities, performance analysis, and strategic objective clarification. The conclusion summarizes the key findings, emphasizing the benefits of the Balanced Scorecard for comprehensive performance management within Nestle.

Management Accounting

Nestle

Nestle

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 1

Executive Summary

The aim of this report is to understand the concept of Balanced Scorecard and its adoption in

Nestle Company. It will also highlight how Balanced Scorecard is suitable for the company.

Along with this, a discussion will be done on how balanced scorecard is different from

traditional performance measurement system.

Executive Summary

The aim of this report is to understand the concept of Balanced Scorecard and its adoption in

Nestle Company. It will also highlight how Balanced Scorecard is suitable for the company.

Along with this, a discussion will be done on how balanced scorecard is different from

traditional performance measurement system.

MANAGEMENT ACCOUNTING 2

Table of Contents

Executive Summary...................................................................................................................1

Introduction................................................................................................................................3

Overview of Nestle................................................................................................................3

Balanced Scorecard................................................................................................................5

The Four perspectives of balanced scorecard....................................................................5

Features of Balanced Scorecard.........................................................................................6

Balanced Scorecard for Nestle Company..........................................................................8

Ways by which Balanced Scorecard is different from Traditional Performance

Measurement System.............................................................................................................8

Suitability of Balanced Scorecard for Nestle.......................................................................11

Covers Operational Activities..........................................................................................11

Allows Performance Analysis..........................................................................................12

Refine Measures and Metrics...........................................................................................12

Communicates Vision and Mission.................................................................................12

Clarifies Strategic Objectives...........................................................................................12

Conclusion................................................................................................................................13

References................................................................................................................................14

Table of Contents

Executive Summary...................................................................................................................1

Introduction................................................................................................................................3

Overview of Nestle................................................................................................................3

Balanced Scorecard................................................................................................................5

The Four perspectives of balanced scorecard....................................................................5

Features of Balanced Scorecard.........................................................................................6

Balanced Scorecard for Nestle Company..........................................................................8

Ways by which Balanced Scorecard is different from Traditional Performance

Measurement System.............................................................................................................8

Suitability of Balanced Scorecard for Nestle.......................................................................11

Covers Operational Activities..........................................................................................11

Allows Performance Analysis..........................................................................................12

Refine Measures and Metrics...........................................................................................12

Communicates Vision and Mission.................................................................................12

Clarifies Strategic Objectives...........................................................................................12

Conclusion................................................................................................................................13

References................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING 3

Introduction

A system of performance measurement helps in making and handling key performance

indicators which should be at the priority of the company's management. It has to excite the

most suitable behaviour (David and Joseph, 2014). Fruitful performance measures cover a

logically balanced set of measures of the organization which offers an impartial procedure

performance assessment that results in the 3 Rs of the business that is everyone one performs

right things, by doing it right at right time. Performance metrics which are also the part of

performance measurement system of organization can also result in unwelcome behaviors if

performed in separation from the total needs of the enterprise (Smarter Solution, 2018). This

report is being prepared in order to understand the performance measurement systems and

their operations that support business organizations to resolve identified issues. The system

which will be discussed in this report is Balanced Scorecard system and its implementation in

the Nestle Company to analyze whether it is suitable for the company or not. An overview of

the Nestle Company will also be provided to know more about the company. Further, a

discussion will be done to know the difference between traditional performance measurement

system and balanced scorecard system.

Overview of Nestle

Nestle is a Swizz drink and food company with headquarter in Vevey, Vaud, Switzerland. It

is the world’s biggest company of food, in terms of revenue, since 2014. In the Fortune

Global 500 list of biggest public company Nestle was ranked on No. 64 in 2017 and in 2016

it was ranked at 33 positions. The product range of the company comprised of medical food,

coffee and tea, snacks, bottles water, baby food, ice-cream, dairy products, pet foods,

confectionery, breakfast cereals, and frozen food. Around 29 brands of Nestle has yearly

sales of US$ 1.1 billion, comprising Kit Kat, Nesquik, Maggi, Nespresso, Vittel, Smarties,

Introduction

A system of performance measurement helps in making and handling key performance

indicators which should be at the priority of the company's management. It has to excite the

most suitable behaviour (David and Joseph, 2014). Fruitful performance measures cover a

logically balanced set of measures of the organization which offers an impartial procedure

performance assessment that results in the 3 Rs of the business that is everyone one performs

right things, by doing it right at right time. Performance metrics which are also the part of

performance measurement system of organization can also result in unwelcome behaviors if

performed in separation from the total needs of the enterprise (Smarter Solution, 2018). This

report is being prepared in order to understand the performance measurement systems and

their operations that support business organizations to resolve identified issues. The system

which will be discussed in this report is Balanced Scorecard system and its implementation in

the Nestle Company to analyze whether it is suitable for the company or not. An overview of

the Nestle Company will also be provided to know more about the company. Further, a

discussion will be done to know the difference between traditional performance measurement

system and balanced scorecard system.

Overview of Nestle

Nestle is a Swizz drink and food company with headquarter in Vevey, Vaud, Switzerland. It

is the world’s biggest company of food, in terms of revenue, since 2014. In the Fortune

Global 500 list of biggest public company Nestle was ranked on No. 64 in 2017 and in 2016

it was ranked at 33 positions. The product range of the company comprised of medical food,

coffee and tea, snacks, bottles water, baby food, ice-cream, dairy products, pet foods,

confectionery, breakfast cereals, and frozen food. Around 29 brands of Nestle has yearly

sales of US$ 1.1 billion, comprising Kit Kat, Nesquik, Maggi, Nespresso, Vittel, Smarties,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 4

Nescafe, and Stouffer’s. Nestle operates in 194 countries by owning 447 factories and hires

around 339,000 people. Nestle is one of the key L’Oreal’s shareholders, which is the world’s

major cosmetics company.

Nestle company was established in 1905, through the merger of the Milk Company i.e.

Anglo-Swiss, which was established by the brothers Charles page and George in 1866. The

company developed majorly in the time duration of First World War and followed the Second

World War, increasing its products beyond its initial condensed milk and baby formula

products. Nestle has been involved in various corporate acquisitions, comprising Findus in

1963, Rowntree Mackintosh in 1988, Gerber in 2007, Crosse & Blackwell in 1950, and

Libby's in 1971. The company is called as largest company of food and beverages. They have

around 2000 brands from global icons to domestic favorites. Singapore was unbiased in the

war and developed progressively isolated in Europe. Due to distribution issues in Asia and

Europe, Nestle started factories in emerging countries in Latin America. Production of the

products increased intensely after America arrived in the war and Nescafe turn out to be the

key beverage for the soldiers of America in Asia and Europe. From 1938 to 1945, the overall

sales of the company increased by $125 million (Nestle, 2018).

In 2002, there were two main acquirements in North America, the ice cream business of U.S

was sold by merging into Dreyer's. In August, acquisition of USD 2.6 bn was announced of

Chef America, Inc.

The purpose of the company is to improve the life quality and adding something to the

healthier future. They want to help people in living and providing healthier and better world.

They desire to influence people to live life healthier (Nestle, 2018). Nestle Company is listed

on the SIX Swiss Exchange and is a component of the Swiss Market Index. Along with this,

on Euronest it has a secondary listing.

Nescafe, and Stouffer’s. Nestle operates in 194 countries by owning 447 factories and hires

around 339,000 people. Nestle is one of the key L’Oreal’s shareholders, which is the world’s

major cosmetics company.

Nestle company was established in 1905, through the merger of the Milk Company i.e.

Anglo-Swiss, which was established by the brothers Charles page and George in 1866. The

company developed majorly in the time duration of First World War and followed the Second

World War, increasing its products beyond its initial condensed milk and baby formula

products. Nestle has been involved in various corporate acquisitions, comprising Findus in

1963, Rowntree Mackintosh in 1988, Gerber in 2007, Crosse & Blackwell in 1950, and

Libby's in 1971. The company is called as largest company of food and beverages. They have

around 2000 brands from global icons to domestic favorites. Singapore was unbiased in the

war and developed progressively isolated in Europe. Due to distribution issues in Asia and

Europe, Nestle started factories in emerging countries in Latin America. Production of the

products increased intensely after America arrived in the war and Nescafe turn out to be the

key beverage for the soldiers of America in Asia and Europe. From 1938 to 1945, the overall

sales of the company increased by $125 million (Nestle, 2018).

In 2002, there were two main acquirements in North America, the ice cream business of U.S

was sold by merging into Dreyer's. In August, acquisition of USD 2.6 bn was announced of

Chef America, Inc.

The purpose of the company is to improve the life quality and adding something to the

healthier future. They want to help people in living and providing healthier and better world.

They desire to influence people to live life healthier (Nestle, 2018). Nestle Company is listed

on the SIX Swiss Exchange and is a component of the Swiss Market Index. Along with this,

on Euronest it has a secondary listing.

MANAGEMENT ACCOUNTING 5

Balanced Scorecard

A management system which is focused towards translating the strategic goals of a company

into a fixed performance objective that are evaluated, controlled, and changed if required to

confirm that the strategic goals of the company are met is known as Balanced Scorecard

(Zizlavsky, 2014). A main evidence of the balanced scorecard system is that the companies of

financial accounting metrics usually track to observe their strategic objectives are inadequate

to maintain companies on track or right direction. Financial outcomes spread light on what

has occurred in the past, and where the business should move towards. The system of the

balanced scorecard is focused towards offering a more inclusive vision to the executives by

completing financial evaluations with extra metrics that device performance in regions like

product innovation and customer satisfaction (Rouse, 2018).

The balanced scorecard framework was established in 1992 in the paper printed in the

Harvard Business review by David P. Norton, and Robert S. Kaplan, who are broadly

accredited with having established the system of the balanced scorecard (Malgwi and Dahiru,

2014).

The Four perspectives of balanced scorecard

The financial analysis comprised of measures like sales growth, return on investment, and

operating income.

Customer analysis consider retention and satisfaction of the customers (Yilmaz, 2013)

The internal analysis concentrates on how the processes of business are associated with the

strategic goals.

Learning and growth analysis measures the satisfaction of employee and retention along

with information system performance (Clark, 2017).

Balanced Scorecard

A management system which is focused towards translating the strategic goals of a company

into a fixed performance objective that are evaluated, controlled, and changed if required to

confirm that the strategic goals of the company are met is known as Balanced Scorecard

(Zizlavsky, 2014). A main evidence of the balanced scorecard system is that the companies of

financial accounting metrics usually track to observe their strategic objectives are inadequate

to maintain companies on track or right direction. Financial outcomes spread light on what

has occurred in the past, and where the business should move towards. The system of the

balanced scorecard is focused towards offering a more inclusive vision to the executives by

completing financial evaluations with extra metrics that device performance in regions like

product innovation and customer satisfaction (Rouse, 2018).

The balanced scorecard framework was established in 1992 in the paper printed in the

Harvard Business review by David P. Norton, and Robert S. Kaplan, who are broadly

accredited with having established the system of the balanced scorecard (Malgwi and Dahiru,

2014).

The Four perspectives of balanced scorecard

The financial analysis comprised of measures like sales growth, return on investment, and

operating income.

Customer analysis consider retention and satisfaction of the customers (Yilmaz, 2013)

The internal analysis concentrates on how the processes of business are associated with the

strategic goals.

Learning and growth analysis measures the satisfaction of employee and retention along

with information system performance (Clark, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING 6

Norton and Kaplan stated two major advantages of the balanced scorecard approach. First,

the scorecard collects all the dissimilar elements of the competitive agenda of the company in

a sole report. Second, by taking all the essential operative metrics, executives are obligatory

to look at whether one development has been attained at the expense of another (Balanced

Scorecard Institute, 2017).

The balanced scorecard approach is utilized to strengthen organization's good behavior by

dividing four separate parts that should be analyzed. These four areas are also known as legs

of balanced scorecard approach which are discussed above i.e. business processes, finance,

learning and growth, and customers. The balanced scorecard is utilized by a company to

attain purposes, capacities, wits, and objectives that can be resulted from the four major

functions of the company (Simister, 2011). Companies can simply recognize factors that are

hampering the performance of the company and frame the strategic changes or variations

traced by future scorecards. With the help of balanced scorecard approach, the company has

been looked as a whole when watching the objectives of the company. A company can make

use of balanced scorecard approach in order to execute strategy mapping to look at the added

value of the company. It can also be used to create strategy objectives and strategic initiatives

(Charter Management Institute, 2018).

Features of Balanced Scorecard

A good balanced scorecard performs as a tool for communication that simply defines

that target of the company and strategic objectives to every employee. With the

support of this, each employee recognizes their responsibilities in the organization.

Additionally, this balanced scorecard must have a managing light for every member

of management when they get trapped in an inexperienced condition or when the

objective becomes indistinct (Pietrzak and Paliszkiewicz, 2015).

Norton and Kaplan stated two major advantages of the balanced scorecard approach. First,

the scorecard collects all the dissimilar elements of the competitive agenda of the company in

a sole report. Second, by taking all the essential operative metrics, executives are obligatory

to look at whether one development has been attained at the expense of another (Balanced

Scorecard Institute, 2017).

The balanced scorecard approach is utilized to strengthen organization's good behavior by

dividing four separate parts that should be analyzed. These four areas are also known as legs

of balanced scorecard approach which are discussed above i.e. business processes, finance,

learning and growth, and customers. The balanced scorecard is utilized by a company to

attain purposes, capacities, wits, and objectives that can be resulted from the four major

functions of the company (Simister, 2011). Companies can simply recognize factors that are

hampering the performance of the company and frame the strategic changes or variations

traced by future scorecards. With the help of balanced scorecard approach, the company has

been looked as a whole when watching the objectives of the company. A company can make

use of balanced scorecard approach in order to execute strategy mapping to look at the added

value of the company. It can also be used to create strategy objectives and strategic initiatives

(Charter Management Institute, 2018).

Features of Balanced Scorecard

A good balanced scorecard performs as a tool for communication that simply defines

that target of the company and strategic objectives to every employee. With the

support of this, each employee recognizes their responsibilities in the organization.

Additionally, this balanced scorecard must have a managing light for every member

of management when they get trapped in an inexperienced condition or when the

objective becomes indistinct (Pietrzak and Paliszkiewicz, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 7

An effectively balanced scorecard is very flexible. It does not frame inflexible

boundaries nearby the strategic objectives. In its place, it permits the management of

the company to do the essential changes every time the necessity gets up (Servizio,

2014).

A good balanced scorecard determines the cause and effect relationship of numerous

purposes to its employees and stakeholders. The explanation of the objective of the

company and its target must be simply explained as to decrease the probabilities of

any future clashes.

An effectively balanced scorecard must be capable enough to talk about the harm due

to short-term decisions on the potential development of the business. As sometimes

the conditions arise that few executives are incapable to have the foresight and they

end up spending or investing in the short-run plans. However, a good balanced

scorecard provides them a simple and clear view of cause and effect relationship that

support them in knowing the consequences of their actions.

The finest part of a good balanced scorecard is that it does not maintain the

executives' regularly involves in different measures. In fact, executive can involve

other essential functions such as coordinating employees, staffing, planning, and

checking risk factors.

The balanced scorecard reduces the number of measures utilized by recognizing only

the essential ones. Evading a propagation of measures emphases the attention of the

management on the key aspects of the implementation strategy.

The companies that are majorly concerned about the profit, the balanced scorecard

approach provides a strong influence on the financial measures and objectives. Every

so often executives provides too much significance to the quality, satisfaction of the

customer, innovation yet they might not create tangible benefits. An effectively

An effectively balanced scorecard is very flexible. It does not frame inflexible

boundaries nearby the strategic objectives. In its place, it permits the management of

the company to do the essential changes every time the necessity gets up (Servizio,

2014).

A good balanced scorecard determines the cause and effect relationship of numerous

purposes to its employees and stakeholders. The explanation of the objective of the

company and its target must be simply explained as to decrease the probabilities of

any future clashes.

An effectively balanced scorecard must be capable enough to talk about the harm due

to short-term decisions on the potential development of the business. As sometimes

the conditions arise that few executives are incapable to have the foresight and they

end up spending or investing in the short-run plans. However, a good balanced

scorecard provides them a simple and clear view of cause and effect relationship that

support them in knowing the consequences of their actions.

The finest part of a good balanced scorecard is that it does not maintain the

executives' regularly involves in different measures. In fact, executive can involve

other essential functions such as coordinating employees, staffing, planning, and

checking risk factors.

The balanced scorecard reduces the number of measures utilized by recognizing only

the essential ones. Evading a propagation of measures emphases the attention of the

management on the key aspects of the implementation strategy.

The companies that are majorly concerned about the profit, the balanced scorecard

approach provides a strong influence on the financial measures and objectives. Every

so often executives provides too much significance to the quality, satisfaction of the

customer, innovation yet they might not create tangible benefits. An effectively

MANAGEMENT ACCOUNTING 8

balanced scorecard observes non-financial measures as a major portion of the

programme or strategy to attain and enhance future financial performance. When non-

financial and financial measures of performance are correctly related in the balanced

scorecards, several non-financial measures assist as foremost pointers of upcoming

financial performance (Agarwal, 2018).

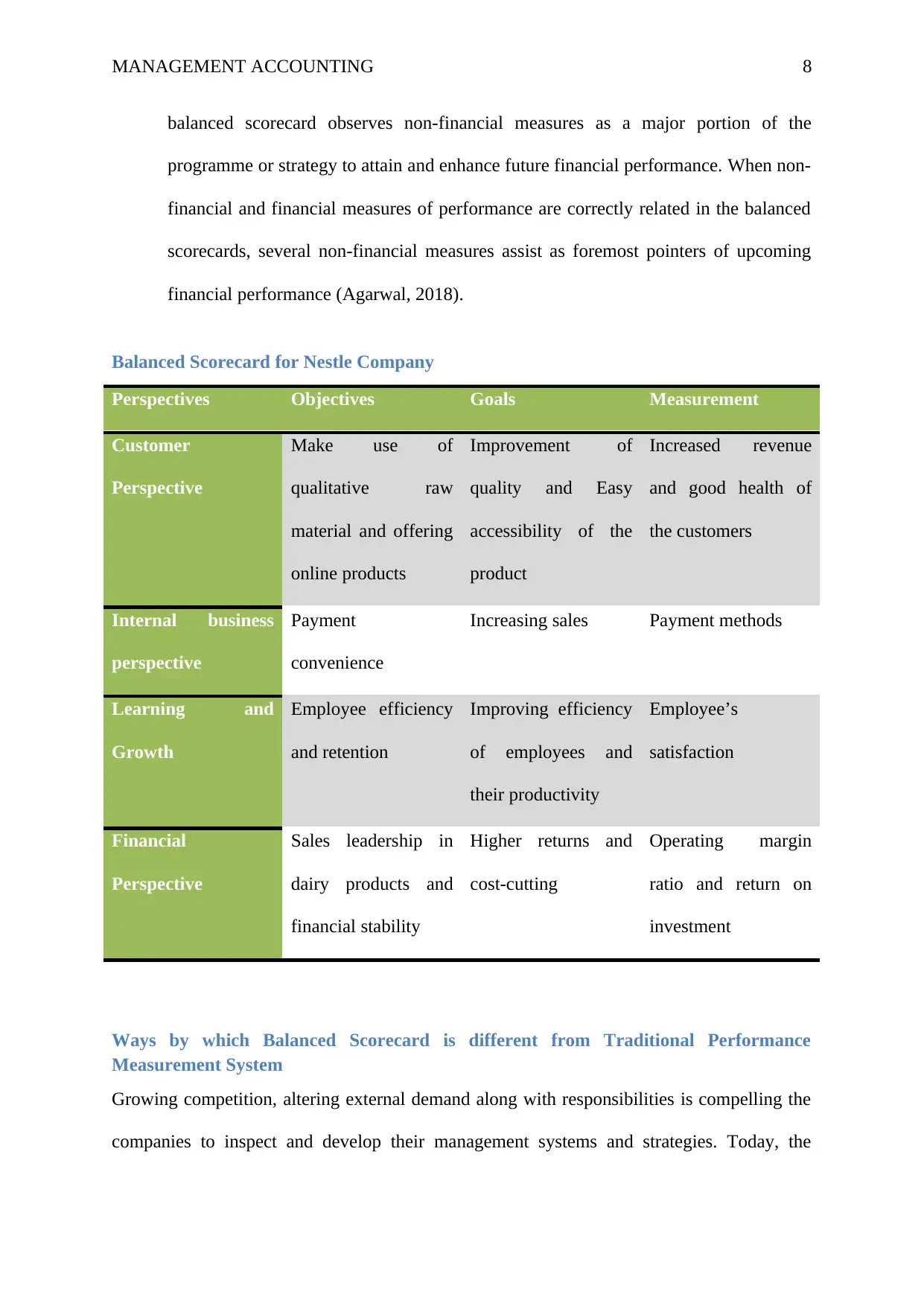

Balanced Scorecard for Nestle Company

Perspectives Objectives Goals Measurement

Customer

Perspective

Make use of

qualitative raw

material and offering

online products

Improvement of

quality and Easy

accessibility of the

product

Increased revenue

and good health of

the customers

Internal business

perspective

Payment

convenience

Increasing sales Payment methods

Learning and

Growth

Employee efficiency

and retention

Improving efficiency

of employees and

their productivity

Employee’s

satisfaction

Financial

Perspective

Sales leadership in

dairy products and

financial stability

Higher returns and

cost-cutting

Operating margin

ratio and return on

investment

Ways by which Balanced Scorecard is different from Traditional Performance

Measurement System

Growing competition, altering external demand along with responsibilities is compelling the

companies to inspect and develop their management systems and strategies. Today, the

balanced scorecard observes non-financial measures as a major portion of the

programme or strategy to attain and enhance future financial performance. When non-

financial and financial measures of performance are correctly related in the balanced

scorecards, several non-financial measures assist as foremost pointers of upcoming

financial performance (Agarwal, 2018).

Balanced Scorecard for Nestle Company

Perspectives Objectives Goals Measurement

Customer

Perspective

Make use of

qualitative raw

material and offering

online products

Improvement of

quality and Easy

accessibility of the

product

Increased revenue

and good health of

the customers

Internal business

perspective

Payment

convenience

Increasing sales Payment methods

Learning and

Growth

Employee efficiency

and retention

Improving efficiency

of employees and

their productivity

Employee’s

satisfaction

Financial

Perspective

Sales leadership in

dairy products and

financial stability

Higher returns and

cost-cutting

Operating margin

ratio and return on

investment

Ways by which Balanced Scorecard is different from Traditional Performance

Measurement System

Growing competition, altering external demand along with responsibilities is compelling the

companies to inspect and develop their management systems and strategies. Today, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING 9

environment in which businesses are being operated is very dynamic and achievement is

dependent on meeting the altering needs of every stakeholder, a company cannot create a

self-centered system of performance measurement. Organizations make use of traditional

performance measurement system which does not provide an overall evaluation. Therefore,

diverse systems performance measurement i.e. balanced scorecard was developed to overawe

the faults of the traditional systems of performance measurement (Striteska and Spickova,

2012).

The system of traditional performance measurement concentrate only on the financial

measures. The reports of the 1980s reflect that the holistic financial data is not sufficient to

gratify the Performance Measurement in the fresh economy due to the augmented

organization's complexities and the marketplaces in which businesses compete. Because the

financial statements and reports are less revealing of shareholder’s value. As reflected by

Cumby and Conrod (2001), justifiable shareholder value is instead determined by the factors

which are non-financial, like the satisfaction of employee, innovations of the organization,

the loyalty of the customer, and internal processes. According to the standard, only 10-15%

of the market value is covered by traditional accounting measures (Striteska and Spickova,

2012). Therefore, today it can be seen that there is increasing influence on the non-financial

measures that are forward-looking.

The balanced scorecard is one of the forward-looking performance measurement systems

which are different from traditional measurement system because it not only considers the

financial measures but also non-financial measures. It is a tool used to explain, execute and

handling strategy at every level in the company. The Balanced Scorecard system guides the

company in creating a better and improved performance measurement system than one

exclusively reliant on financial measures such as Traditional performance measurement.

environment in which businesses are being operated is very dynamic and achievement is

dependent on meeting the altering needs of every stakeholder, a company cannot create a

self-centered system of performance measurement. Organizations make use of traditional

performance measurement system which does not provide an overall evaluation. Therefore,

diverse systems performance measurement i.e. balanced scorecard was developed to overawe

the faults of the traditional systems of performance measurement (Striteska and Spickova,

2012).

The system of traditional performance measurement concentrate only on the financial

measures. The reports of the 1980s reflect that the holistic financial data is not sufficient to

gratify the Performance Measurement in the fresh economy due to the augmented

organization's complexities and the marketplaces in which businesses compete. Because the

financial statements and reports are less revealing of shareholder’s value. As reflected by

Cumby and Conrod (2001), justifiable shareholder value is instead determined by the factors

which are non-financial, like the satisfaction of employee, innovations of the organization,

the loyalty of the customer, and internal processes. According to the standard, only 10-15%

of the market value is covered by traditional accounting measures (Striteska and Spickova,

2012). Therefore, today it can be seen that there is increasing influence on the non-financial

measures that are forward-looking.

The balanced scorecard is one of the forward-looking performance measurement systems

which are different from traditional measurement system because it not only considers the

financial measures but also non-financial measures. It is a tool used to explain, execute and

handling strategy at every level in the company. The Balanced Scorecard system guides the

company in creating a better and improved performance measurement system than one

exclusively reliant on financial measures such as Traditional performance measurement.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 10

Additionally, balanced scorecard meets the organization's fundamental functions: the system

of strategic management, communication tool, and measurement system

In traditional performance measurement systems, the financial measures are also called as lag

indicators, as they only show the historical data and signify historical performance. However,

the metrics of quantitative performance can manage and enhance the internal performance of

the company and can result in wrong decision making in the future (Pourmoradi and Niknafs,

2016). Therefore, today only depending on the single measure i.e. financial measure is

unsuitable because this measure does not consider or evaluate intangible assets, does not

evaluate the problem of competitive rivalry (Suvarna, 2012). On the other side, the essential

aspect of the balanced scorecard is the expansion and execution of the organization’s vision

and the plan into a set target and comprehensible set of non-financial and financial indicators

of performance. The overview of balanced scorecard reflects that the aims, the pointers, and

the planned actions are allocated to a real point of view (Schmeisser and Clausen, 2011).

Traditional performance measures are not related to the strategy of the organization. The

strategy is linked to the long-term organizational objectives, the possibilities of the activities

of the organization, the matching, and assignment of the activities of the organization to its

resource competencies and needs of the business, and thought of the stakeholder’s

expectations and value of the organization (Agarwal, 2018). Traditional performance

measurement system concentrates on the short-run financial performance, causing in detach

between the short-term actions and long-term strategies of the organization. Organizations

should evaluate performance in the method that not just imitate past constructive

performance. Nowadays, the business environment is considered by the strong competitive

challenge and as an outcome businesses need to become adaptive and flexible in order to

attain a competitive advantage.

Additionally, balanced scorecard meets the organization's fundamental functions: the system

of strategic management, communication tool, and measurement system

In traditional performance measurement systems, the financial measures are also called as lag

indicators, as they only show the historical data and signify historical performance. However,

the metrics of quantitative performance can manage and enhance the internal performance of

the company and can result in wrong decision making in the future (Pourmoradi and Niknafs,

2016). Therefore, today only depending on the single measure i.e. financial measure is

unsuitable because this measure does not consider or evaluate intangible assets, does not

evaluate the problem of competitive rivalry (Suvarna, 2012). On the other side, the essential

aspect of the balanced scorecard is the expansion and execution of the organization’s vision

and the plan into a set target and comprehensible set of non-financial and financial indicators

of performance. The overview of balanced scorecard reflects that the aims, the pointers, and

the planned actions are allocated to a real point of view (Schmeisser and Clausen, 2011).

Traditional performance measures are not related to the strategy of the organization. The

strategy is linked to the long-term organizational objectives, the possibilities of the activities

of the organization, the matching, and assignment of the activities of the organization to its

resource competencies and needs of the business, and thought of the stakeholder’s

expectations and value of the organization (Agarwal, 2018). Traditional performance

measurement system concentrates on the short-run financial performance, causing in detach

between the short-term actions and long-term strategies of the organization. Organizations

should evaluate performance in the method that not just imitate past constructive

performance. Nowadays, the business environment is considered by the strong competitive

challenge and as an outcome businesses need to become adaptive and flexible in order to

attain a competitive advantage.

MANAGEMENT ACCOUNTING 11

On the other hand, the balanced scorecard is majorly focused towards the strategy of the

organization and how much they have been achieved. The normal balanced scorecard

observes the organization from the four perspectives or legs i.e. customer, business processes,

financial and learning and growth; all the perspectives should be balanced (Pramudita, 2016).

The balance refers to the equability among the long-term and short-term goals, required

outputs and inputs, external and internal performance factors, and non-financial and financial

indicators. The selection of these four perspectives has not been done randomly, it provides a

clear sight of interconnection between the success of the organization and performance

drivers. Therefore, they make a flexible system in the established strategy.

Therefore, in the end it can be said that the major difference between traditional performance

measurement system and balanced scorecard approach is that the traditional performance

measurement system is not effective in today's business environment because it only

considered one perspective i.e. financial and on the other side balance scorecard consider

both financial and non-financial measures which are very important for successful survival in

the market.

Suitability of Balanced Scorecard for Nestle

Balanced Scorecard can be established by Nestle Company in its business operations in order

to align all the activities. This system of performance management will add value to the non-

financial measures of Nestle to traditional financial metrics and will make the company the

market leader. If the company follows balanced scorecard approach then it will support in

tracking the non-financial measures such as relationship evaluation between employees,

customers, suppliers and company, and the ability of the company to handle a sustainable

business (Giannopoulos and Holt, 2013). Elements that state the suitability of balanced

scorecard in Nestle is:

On the other hand, the balanced scorecard is majorly focused towards the strategy of the

organization and how much they have been achieved. The normal balanced scorecard

observes the organization from the four perspectives or legs i.e. customer, business processes,

financial and learning and growth; all the perspectives should be balanced (Pramudita, 2016).

The balance refers to the equability among the long-term and short-term goals, required

outputs and inputs, external and internal performance factors, and non-financial and financial

indicators. The selection of these four perspectives has not been done randomly, it provides a

clear sight of interconnection between the success of the organization and performance

drivers. Therefore, they make a flexible system in the established strategy.

Therefore, in the end it can be said that the major difference between traditional performance

measurement system and balanced scorecard approach is that the traditional performance

measurement system is not effective in today's business environment because it only

considered one perspective i.e. financial and on the other side balance scorecard consider

both financial and non-financial measures which are very important for successful survival in

the market.

Suitability of Balanced Scorecard for Nestle

Balanced Scorecard can be established by Nestle Company in its business operations in order

to align all the activities. This system of performance management will add value to the non-

financial measures of Nestle to traditional financial metrics and will make the company the

market leader. If the company follows balanced scorecard approach then it will support in

tracking the non-financial measures such as relationship evaluation between employees,

customers, suppliers and company, and the ability of the company to handle a sustainable

business (Giannopoulos and Holt, 2013). Elements that state the suitability of balanced

scorecard in Nestle is:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.