Taxation of Trust Income and Beneficiaries: Finance Assignment

VerifiedAdded on 2023/06/03

|5

|594

|101

Homework Assignment

AI Summary

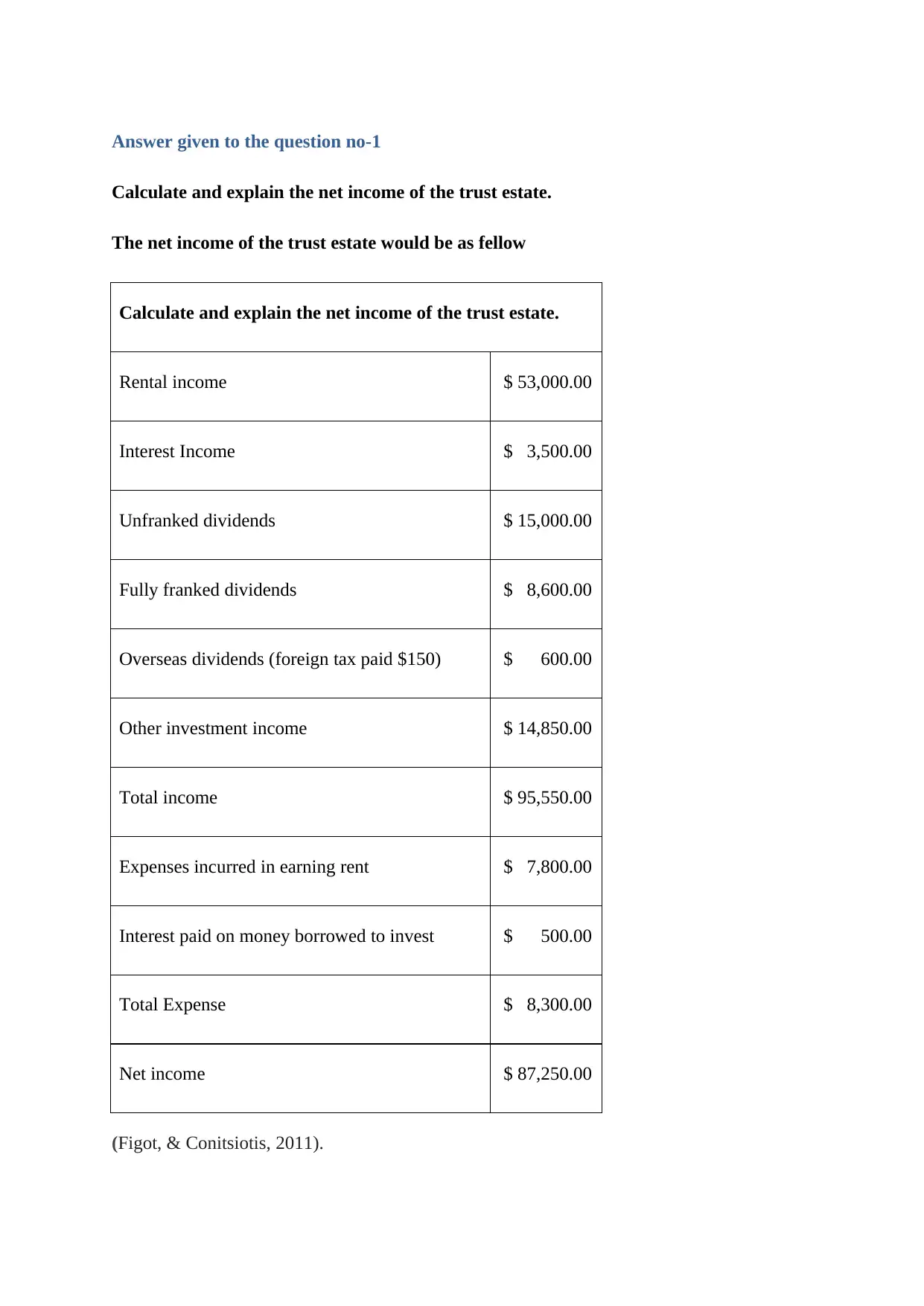

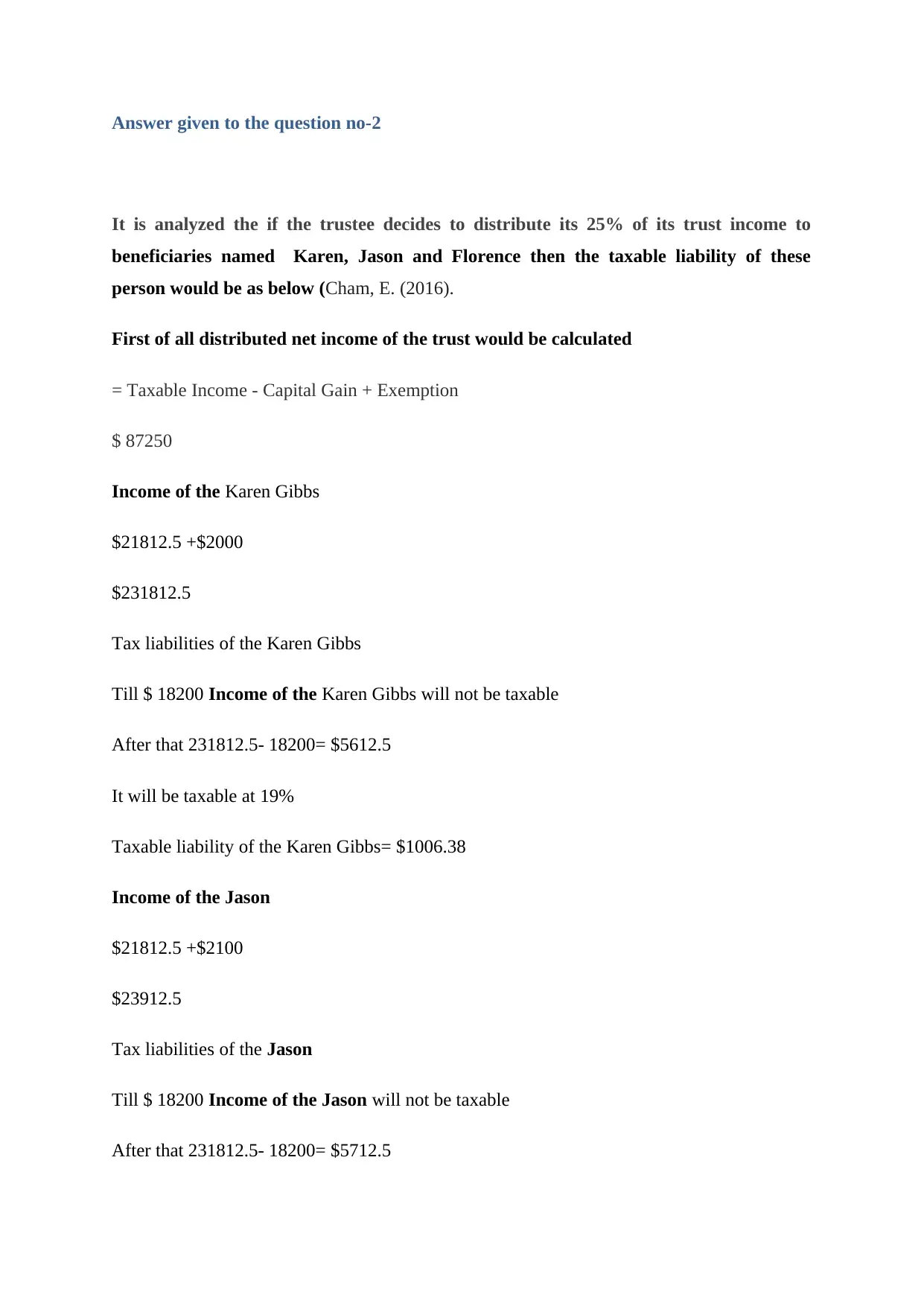

This assignment solution addresses the calculation of net income for a discretionary trust estate and the subsequent tax liabilities for its beneficiaries. The solution begins by calculating the trust's total income, including rental income, interest, dividends, and other investment income, and then subtracts the expenses incurred to arrive at the net income. The solution then analyzes the tax implications for beneficiaries Karen, Jason, and Florence, considering their individual income and the distribution of 25% of the trust income to each. The solution calculates each beneficiary's taxable income and tax liability. Finally, the solution touches upon tax-free income and the handling of international tax implications, such as the case of a beneficiary living in Tokyo. The assignment references relevant taxation literature.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.