Analysis of NEUROPOWER and IQFORCE Projects: Financial Report

VerifiedAdded on 2022/08/27

|10

|1731

|21

Report

AI Summary

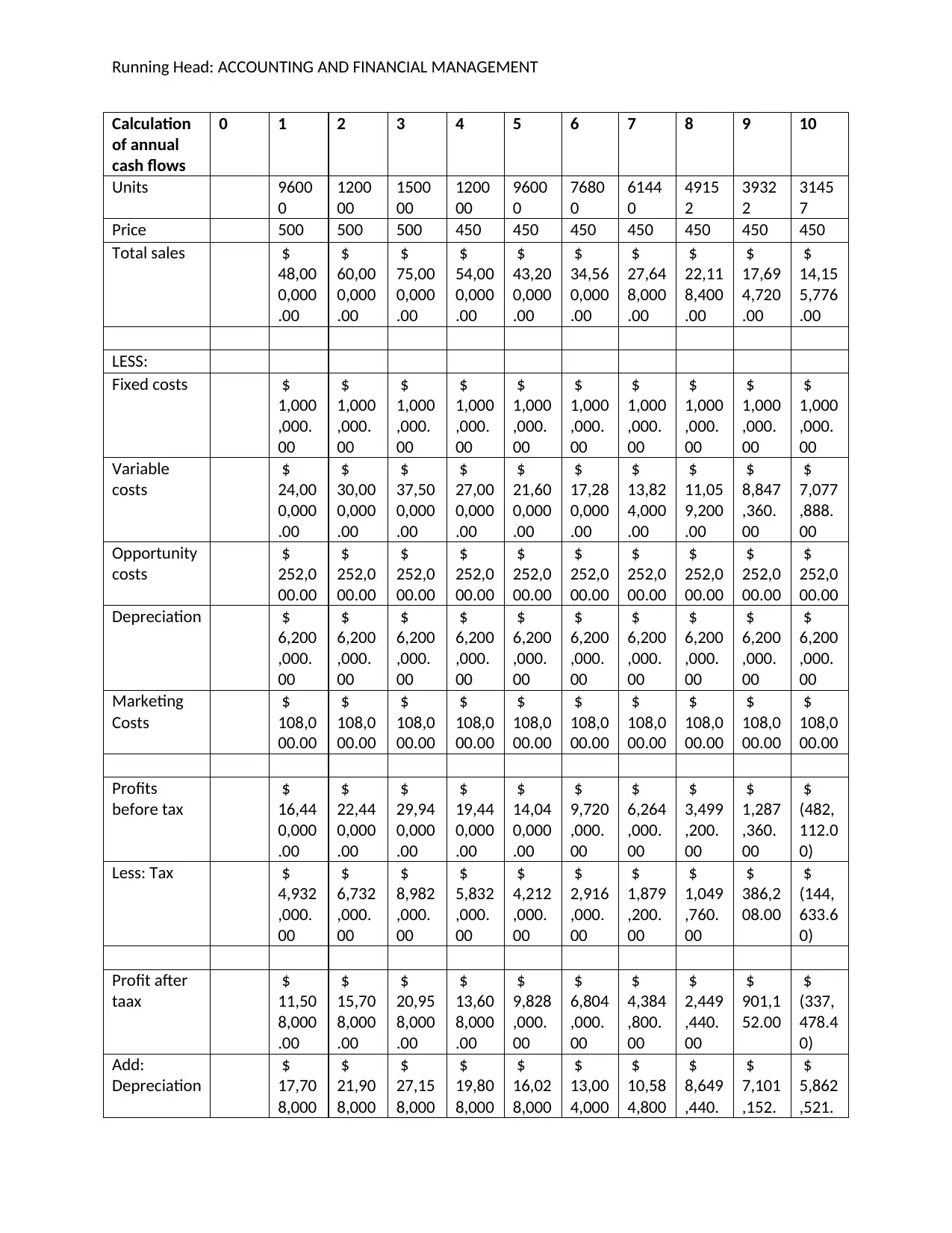

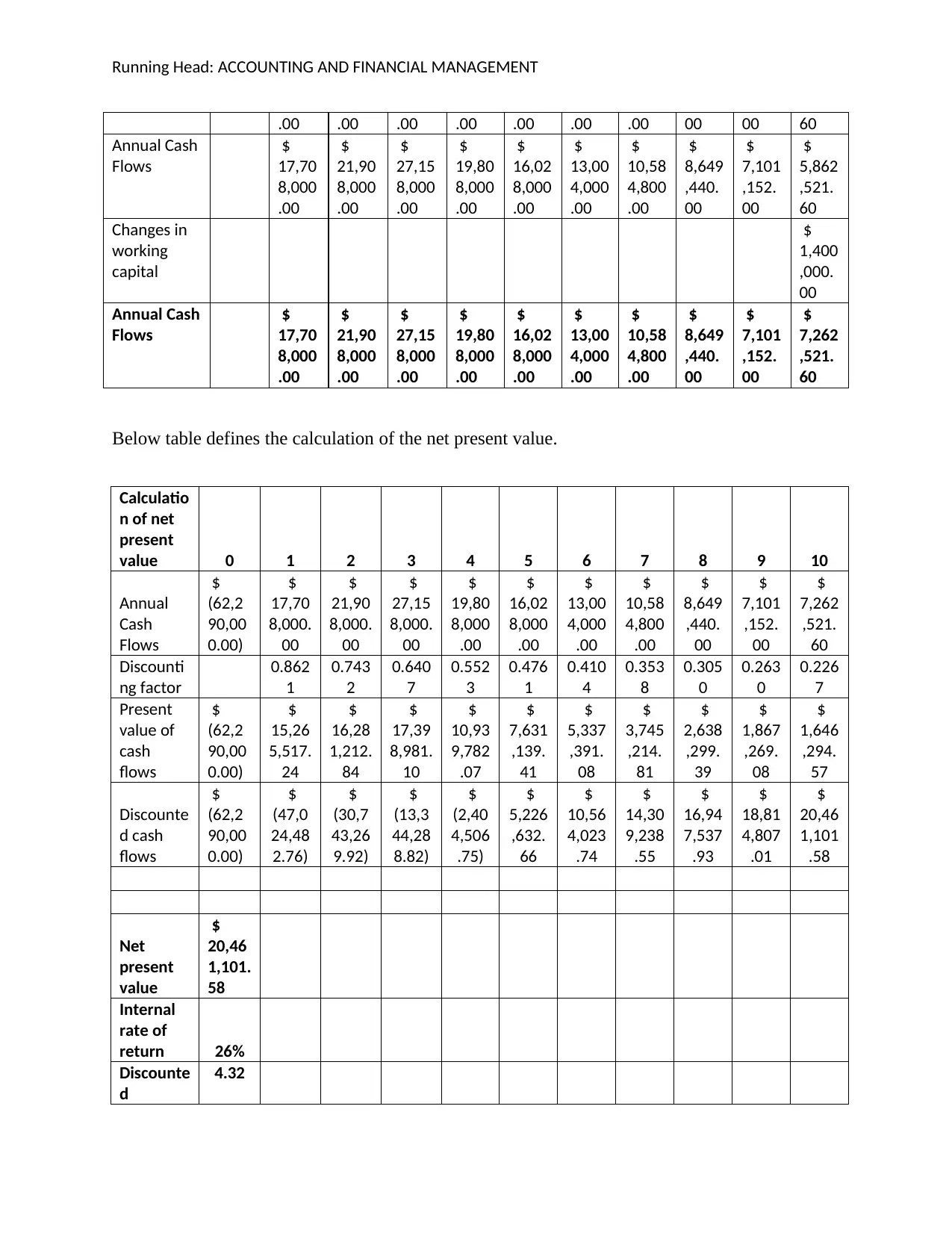

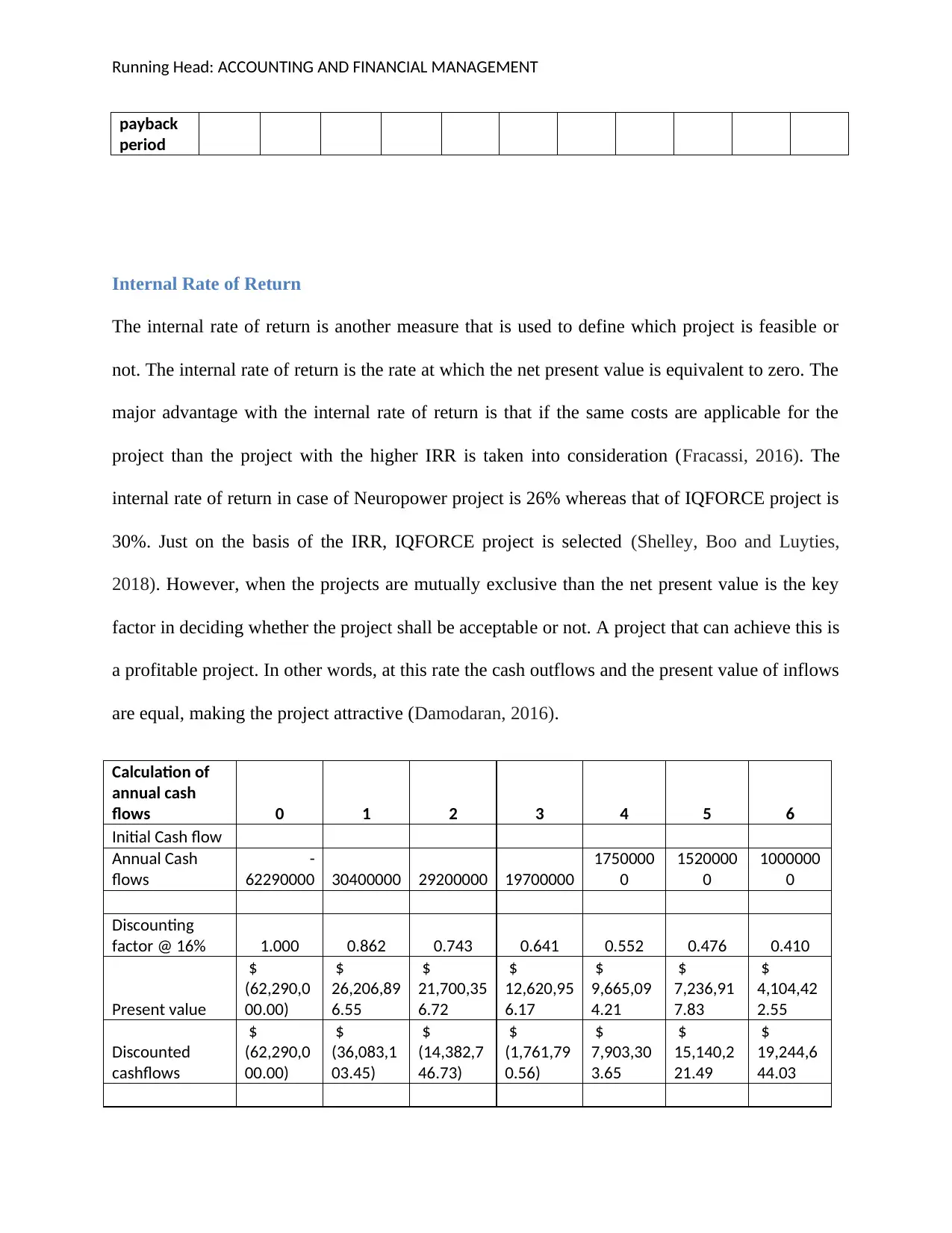

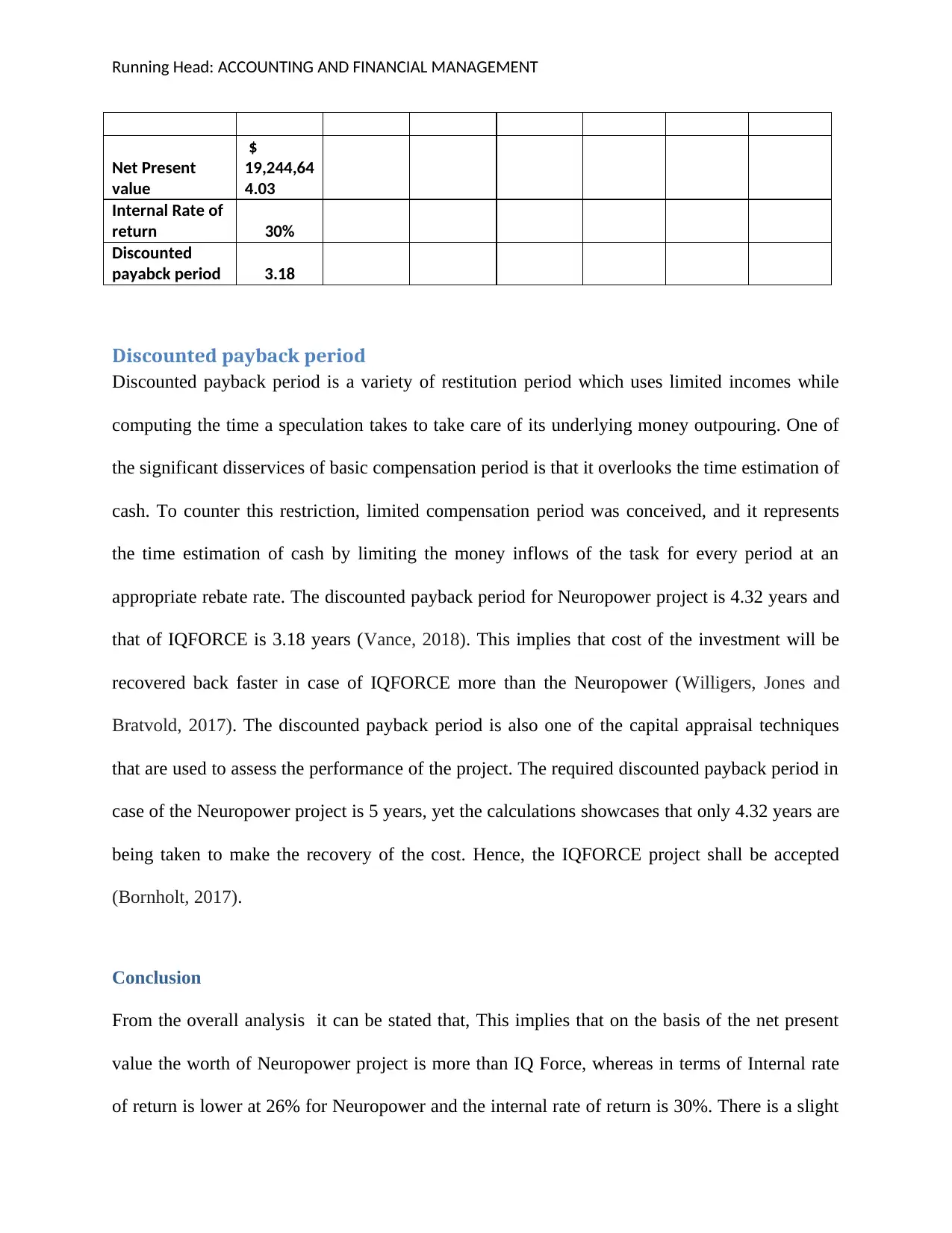

This report undertakes a detailed financial analysis of two projects, NEUROPOWER and IQFORCE, using capital budgeting techniques. The analysis focuses on Net Present Value (NPV), Internal Rate of Return (IRR), and discounted payback period to determine project viability. The report calculates annual cash flows, considering factors such as sales, fixed and variable costs, depreciation, and taxes. The NPV calculations show that NEUROPOWER has a higher value than IQFORCE. The IRR for NEUROPOWER is 26%, while IQFORCE has an IRR of 30%. The discounted payback period is 4.32 years for NEUROPOWER and 3.18 years for IQFORCE. Based on the analysis, the report recommends the IQFORCE project due to its higher IRR and faster payback period, despite NEUROPOWER's higher NPV.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.