Financial Statement & Ratio Analysis: New Century Resources

VerifiedAdded on 2023/06/11

|14

|2412

|345

Report

AI Summary

This report provides a financial analysis of New Century Resources Limited, an Australian base metal developing company, using ratio analysis based on their annual reports for 2016 and 2017. The analysis covers liquidity, solvency, and profitability, utilizing ratios such as the current ratio, debt-to-equity ratio, return on owner's equity, net profit margin, and expense ratio. The findings suggest that New Century Resources Limited faces significant financial challenges, including poor liquidity, high debt, and negative profitability, leading to the conclusion that the company's financial performance is unsustainable and unattractive to potential investors. Recommendations are made to improve liquidity by increasing current assets, reducing the debt-to-equity ratio through equity financing, and focusing on profitable operations to enhance shareholder returns. Desklib offers a variety of study tools and resources for students.

Running Head: Financial Statement Analysis

Ratio Analysis

Ratio Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Financial Statement Analysis 1

Running Head: Financial Statement Analysis 2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: Financial Statement Analysis 3

Introduction:

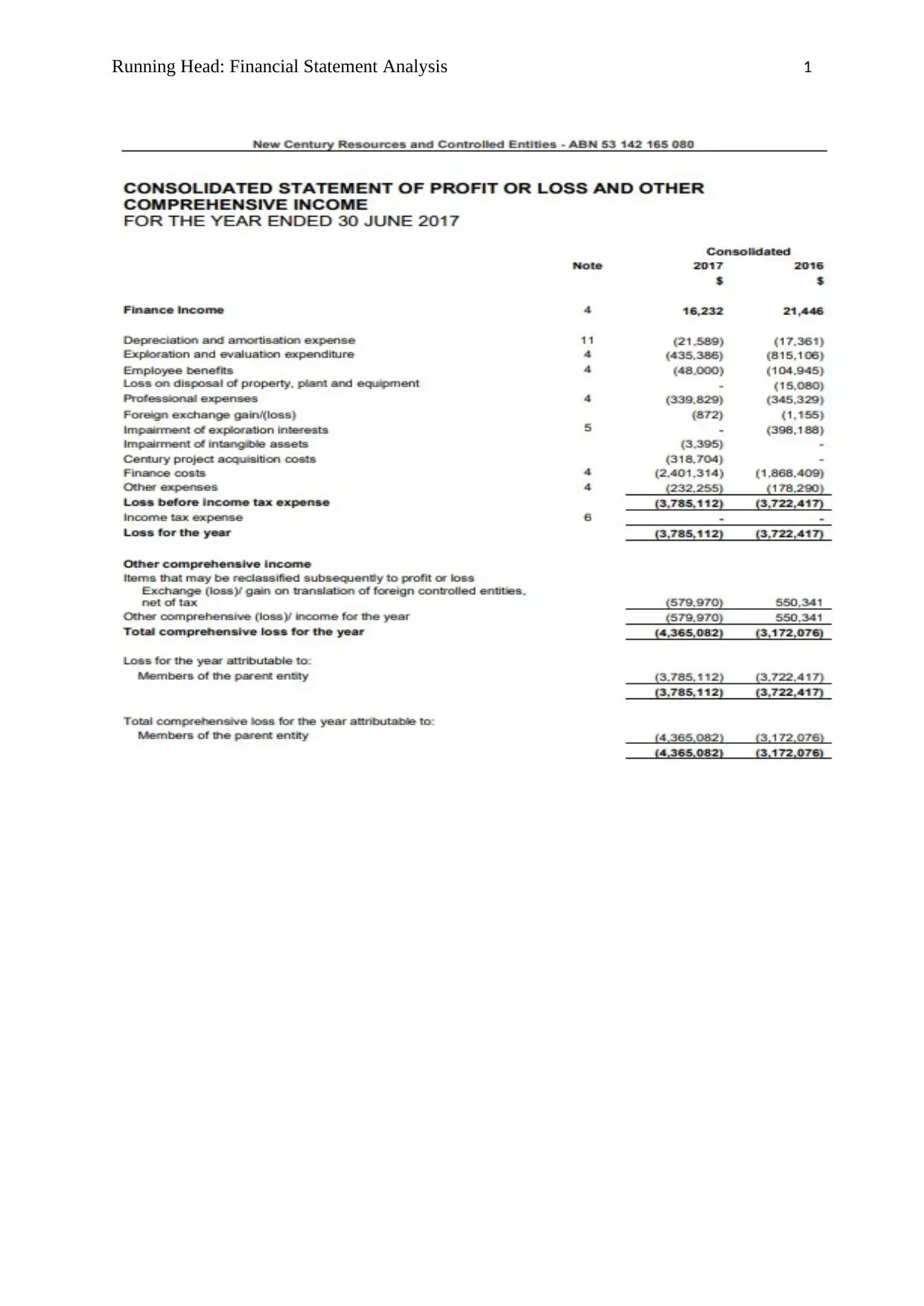

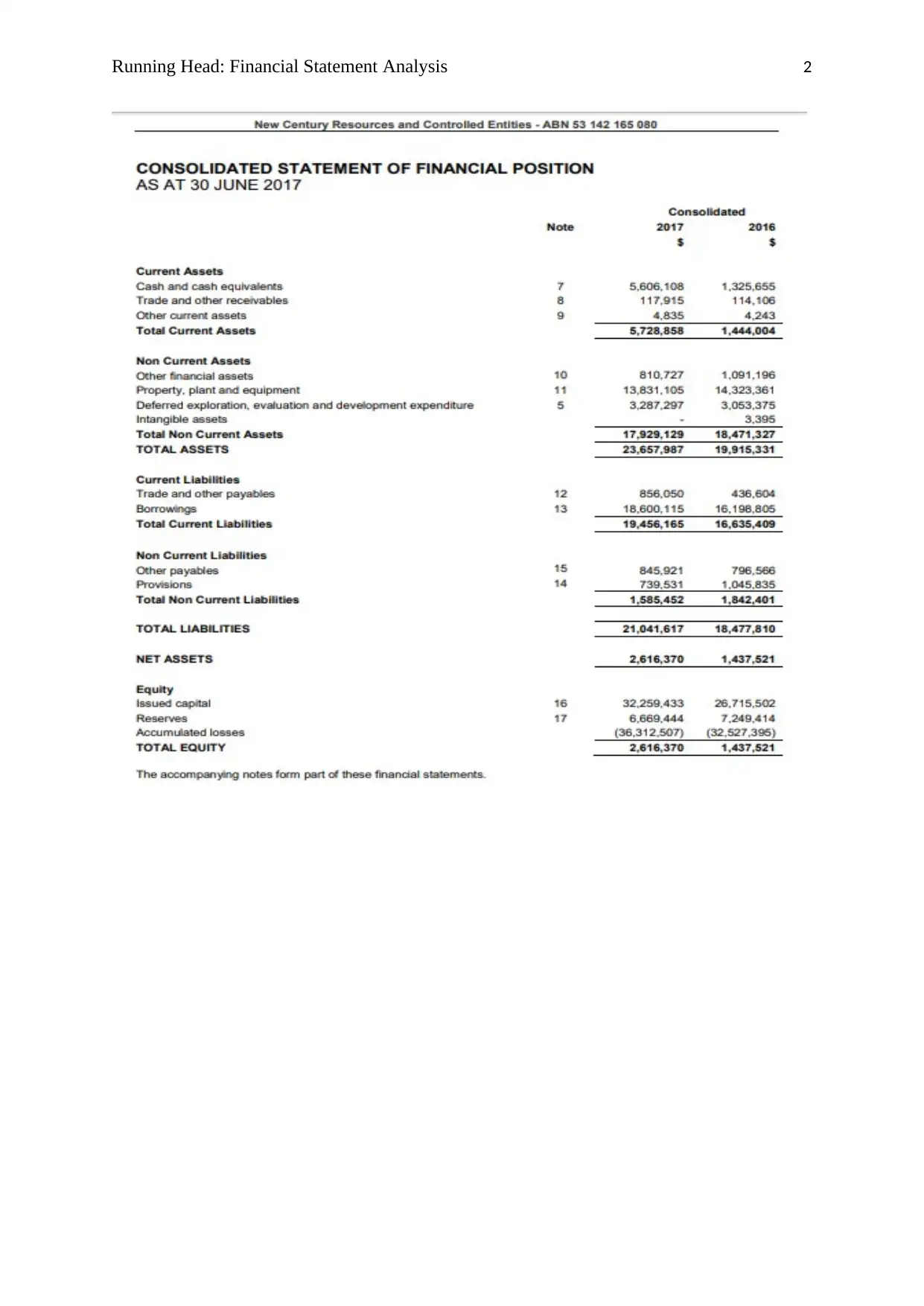

New century resources limited is an Australian company that was incorporated in year 2010.

The head office of the company is based in Perth. The company operates its business in

Australia as well as the United States as a based metal developing company. It was formerly

recognised with the name of Attila Resources Limited and since July 2017 it has changed its

name as New Century Resources Limited. The main operation of the company is the

exploration of zinc, lead, coking coal deposits and silver. NCZ Ltd. is holding 70% of the

stake in Century Zinc Mine, which is located in Queensland (Australia). Also, it holds 70%

interest in Kodiak Coking Coal Project, which has its head office in Cahaba Basin, Alabama. The

financial performance of the company since its incorporation is not well and therefore it is

operating with losses. This has been observed through the applying the concept ratio analysis

under financial management.

In this report, financial performance of the company is analysed using one of the most

important tool of financial management i.e. Ratio Analysis1. As a part of ratio analysis five

ratios have been determined using the financials of the company and on the basis of results of

those ratios, its financial performance has been evaluated. There are various aspects of the

company’s overall financial performance, such as its liquidity position, profitability state,

solvency position and the efficiency and effectiveness of various activities (inventory

management, payables and receivables management etc.2The data for the financial results

have been extracted from the annual report of the company for the year ending June 2017. To

critically analyse the company’s financial position a comparative study of the financials of

last two years i.e. 2017 and 2016 has been made in this report.

1 I.M. Pandey, Financial Management (India: Vikas Publishing House, 2015), 921

2 C, A., Lee, J, C. Lee, Cheng, F., and Lee. Financial Analysis, Planning & Forecasting: Theory and Application.

(Singapore: World Scientific, 2009), 1101.

Introduction:

New century resources limited is an Australian company that was incorporated in year 2010.

The head office of the company is based in Perth. The company operates its business in

Australia as well as the United States as a based metal developing company. It was formerly

recognised with the name of Attila Resources Limited and since July 2017 it has changed its

name as New Century Resources Limited. The main operation of the company is the

exploration of zinc, lead, coking coal deposits and silver. NCZ Ltd. is holding 70% of the

stake in Century Zinc Mine, which is located in Queensland (Australia). Also, it holds 70%

interest in Kodiak Coking Coal Project, which has its head office in Cahaba Basin, Alabama. The

financial performance of the company since its incorporation is not well and therefore it is

operating with losses. This has been observed through the applying the concept ratio analysis

under financial management.

In this report, financial performance of the company is analysed using one of the most

important tool of financial management i.e. Ratio Analysis1. As a part of ratio analysis five

ratios have been determined using the financials of the company and on the basis of results of

those ratios, its financial performance has been evaluated. There are various aspects of the

company’s overall financial performance, such as its liquidity position, profitability state,

solvency position and the efficiency and effectiveness of various activities (inventory

management, payables and receivables management etc.2The data for the financial results

have been extracted from the annual report of the company for the year ending June 2017. To

critically analyse the company’s financial position a comparative study of the financials of

last two years i.e. 2017 and 2016 has been made in this report.

1 I.M. Pandey, Financial Management (India: Vikas Publishing House, 2015), 921

2 C, A., Lee, J, C. Lee, Cheng, F., and Lee. Financial Analysis, Planning & Forecasting: Theory and Application.

(Singapore: World Scientific, 2009), 1101.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Financial Statement Analysis 4

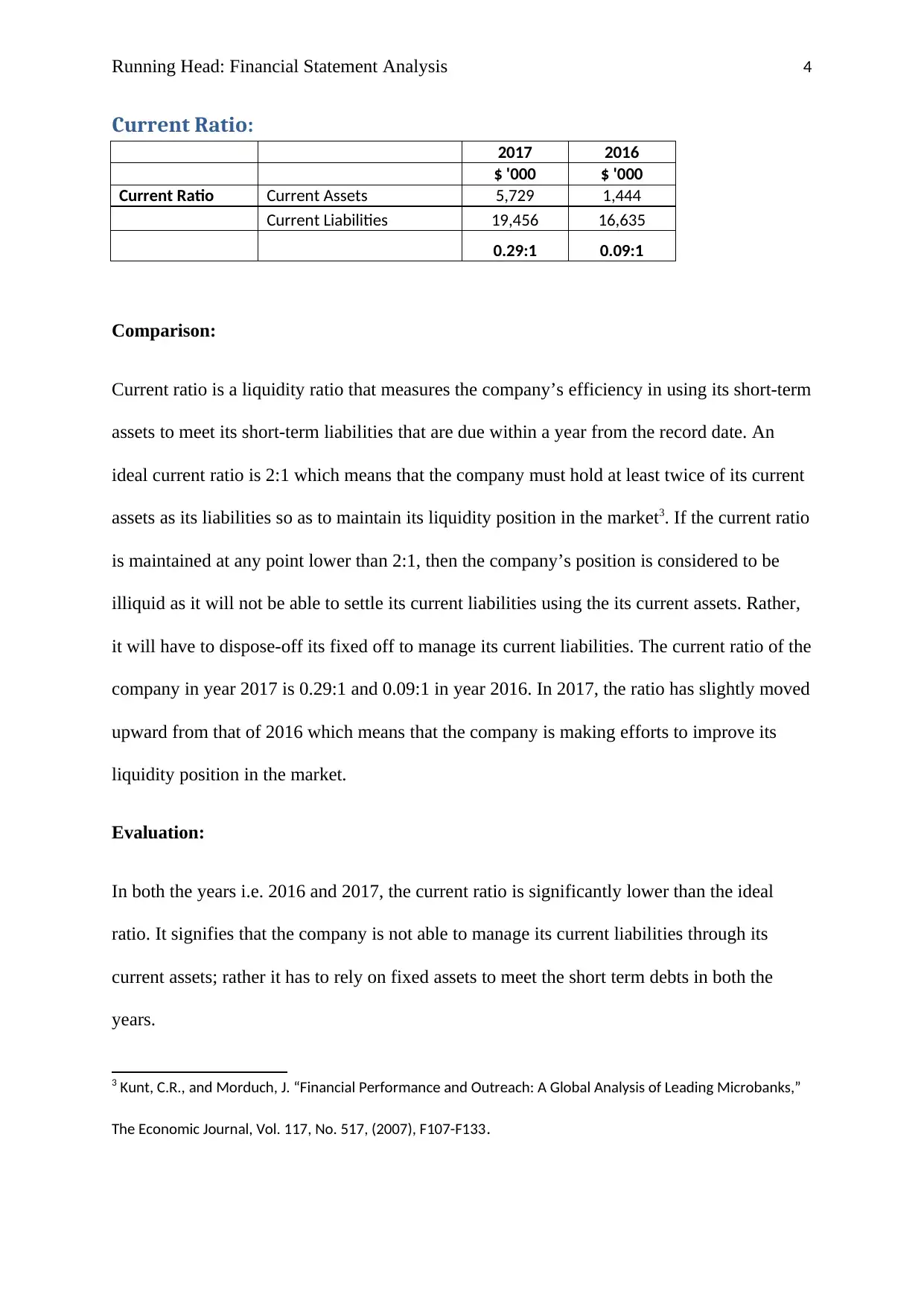

Current Ratio:

2017 2016

$ '000 $ '000

Current Ratio Current Assets 5,729 1,444

Current Liabilities 19,456 16,635

0.29:1 0.09:1

Comparison:

Current ratio is a liquidity ratio that measures the company’s efficiency in using its short-term

assets to meet its short-term liabilities that are due within a year from the record date. An

ideal current ratio is 2:1 which means that the company must hold at least twice of its current

assets as its liabilities so as to maintain its liquidity position in the market3. If the current ratio

is maintained at any point lower than 2:1, then the company’s position is considered to be

illiquid as it will not be able to settle its current liabilities using the its current assets. Rather,

it will have to dispose-off its fixed off to manage its current liabilities. The current ratio of the

company in year 2017 is 0.29:1 and 0.09:1 in year 2016. In 2017, the ratio has slightly moved

upward from that of 2016 which means that the company is making efforts to improve its

liquidity position in the market.

Evaluation:

In both the years i.e. 2016 and 2017, the current ratio is significantly lower than the ideal

ratio. It signifies that the company is not able to manage its current liabilities through its

current assets; rather it has to rely on fixed assets to meet the short term debts in both the

years.

3 Kunt, C.R., and Morduch, J. “Financial Performance and Outreach: A Global Analysis of Leading Microbanks,”

The Economic Journal, Vol. 117, No. 517, (2007), F107-F133.

Current Ratio:

2017 2016

$ '000 $ '000

Current Ratio Current Assets 5,729 1,444

Current Liabilities 19,456 16,635

0.29:1 0.09:1

Comparison:

Current ratio is a liquidity ratio that measures the company’s efficiency in using its short-term

assets to meet its short-term liabilities that are due within a year from the record date. An

ideal current ratio is 2:1 which means that the company must hold at least twice of its current

assets as its liabilities so as to maintain its liquidity position in the market3. If the current ratio

is maintained at any point lower than 2:1, then the company’s position is considered to be

illiquid as it will not be able to settle its current liabilities using the its current assets. Rather,

it will have to dispose-off its fixed off to manage its current liabilities. The current ratio of the

company in year 2017 is 0.29:1 and 0.09:1 in year 2016. In 2017, the ratio has slightly moved

upward from that of 2016 which means that the company is making efforts to improve its

liquidity position in the market.

Evaluation:

In both the years i.e. 2016 and 2017, the current ratio is significantly lower than the ideal

ratio. It signifies that the company is not able to manage its current liabilities through its

current assets; rather it has to rely on fixed assets to meet the short term debts in both the

years.

3 Kunt, C.R., and Morduch, J. “Financial Performance and Outreach: A Global Analysis of Leading Microbanks,”

The Economic Journal, Vol. 117, No. 517, (2007), F107-F133.

Running Head: Financial Statement Analysis 5

Recommendation:

To improve the liquidity position, the company must invest more in current assets to as to

square-off its liabilities that are due within one year from the date of transaction. It must al-

least hold doubles of its current assets in relation to current liabilities so that it does not have

to dispose-off its fixed assets for the purpose of current liabilities settlement4.

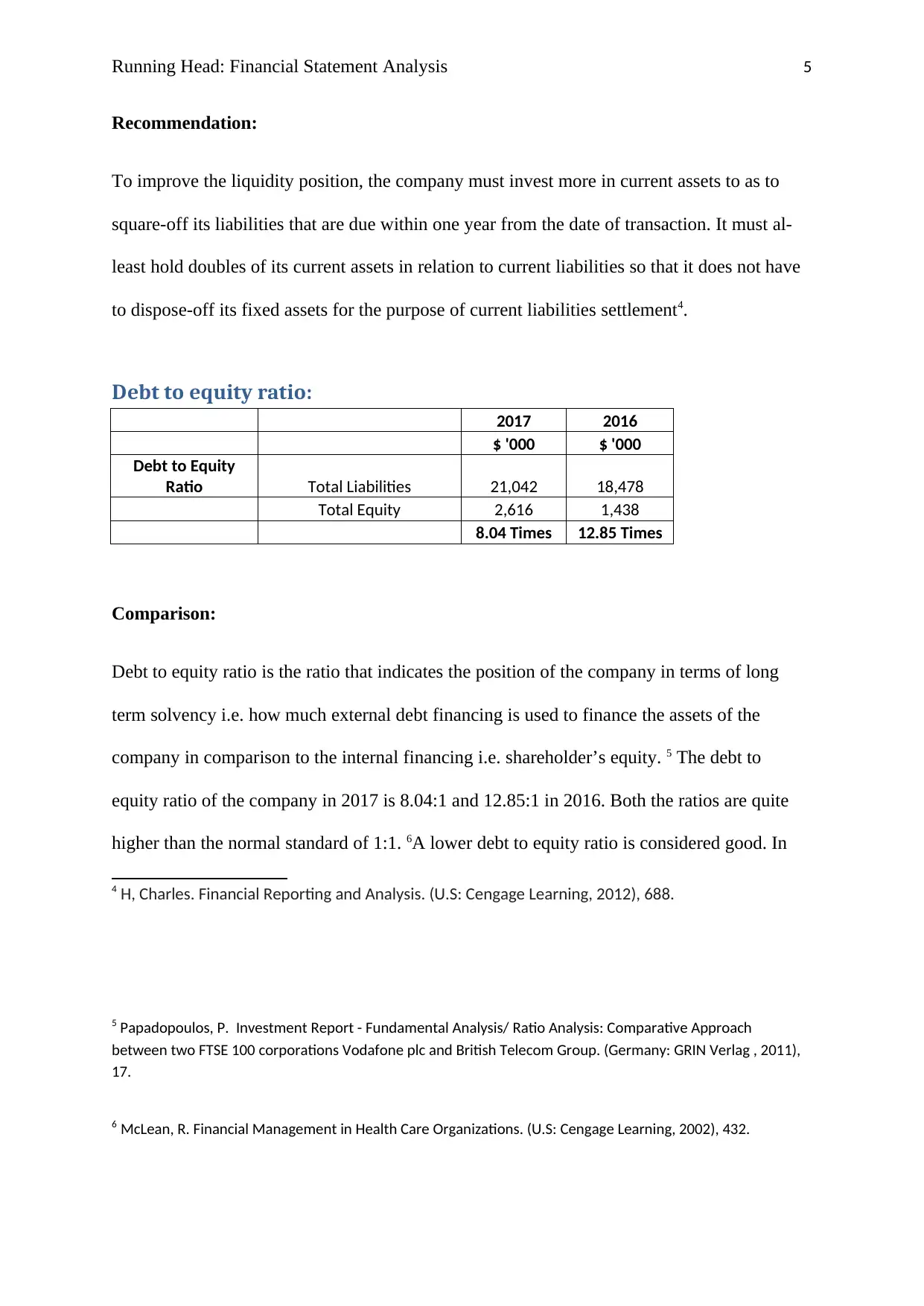

Debt to equity ratio:

2017 2016

$ '000 $ '000

Debt to Equity

Ratio Total Liabilities 21,042 18,478

Total Equity 2,616 1,438

8.04 Times 12.85 Times

Comparison:

Debt to equity ratio is the ratio that indicates the position of the company in terms of long

term solvency i.e. how much external debt financing is used to finance the assets of the

company in comparison to the internal financing i.e. shareholder’s equity. 5 The debt to

equity ratio of the company in 2017 is 8.04:1 and 12.85:1 in 2016. Both the ratios are quite

higher than the normal standard of 1:1. 6A lower debt to equity ratio is considered good. In

4 H, Charles. Financial Reporting and Analysis. (U.S: Cengage Learning, 2012), 688.

5 Papadopoulos, P. Investment Report - Fundamental Analysis/ Ratio Analysis: Comparative Approach

between two FTSE 100 corporations Vodafone plc and British Telecom Group. (Germany: GRIN Verlag , 2011),

17.

6 McLean, R. Financial Management in Health Care Organizations. (U.S: Cengage Learning, 2002), 432.

Recommendation:

To improve the liquidity position, the company must invest more in current assets to as to

square-off its liabilities that are due within one year from the date of transaction. It must al-

least hold doubles of its current assets in relation to current liabilities so that it does not have

to dispose-off its fixed assets for the purpose of current liabilities settlement4.

Debt to equity ratio:

2017 2016

$ '000 $ '000

Debt to Equity

Ratio Total Liabilities 21,042 18,478

Total Equity 2,616 1,438

8.04 Times 12.85 Times

Comparison:

Debt to equity ratio is the ratio that indicates the position of the company in terms of long

term solvency i.e. how much external debt financing is used to finance the assets of the

company in comparison to the internal financing i.e. shareholder’s equity. 5 The debt to

equity ratio of the company in 2017 is 8.04:1 and 12.85:1 in 2016. Both the ratios are quite

higher than the normal standard of 1:1. 6A lower debt to equity ratio is considered good. In

4 H, Charles. Financial Reporting and Analysis. (U.S: Cengage Learning, 2012), 688.

5 Papadopoulos, P. Investment Report - Fundamental Analysis/ Ratio Analysis: Comparative Approach

between two FTSE 100 corporations Vodafone plc and British Telecom Group. (Germany: GRIN Verlag , 2011),

17.

6 McLean, R. Financial Management in Health Care Organizations. (U.S: Cengage Learning, 2002), 432.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: Financial Statement Analysis 6

2017, the ratio has declined in comparison to year 2016 therefore, the solvency position of

company can be said to be improved in year 2017 in comparison to 2016.

Evaluation:

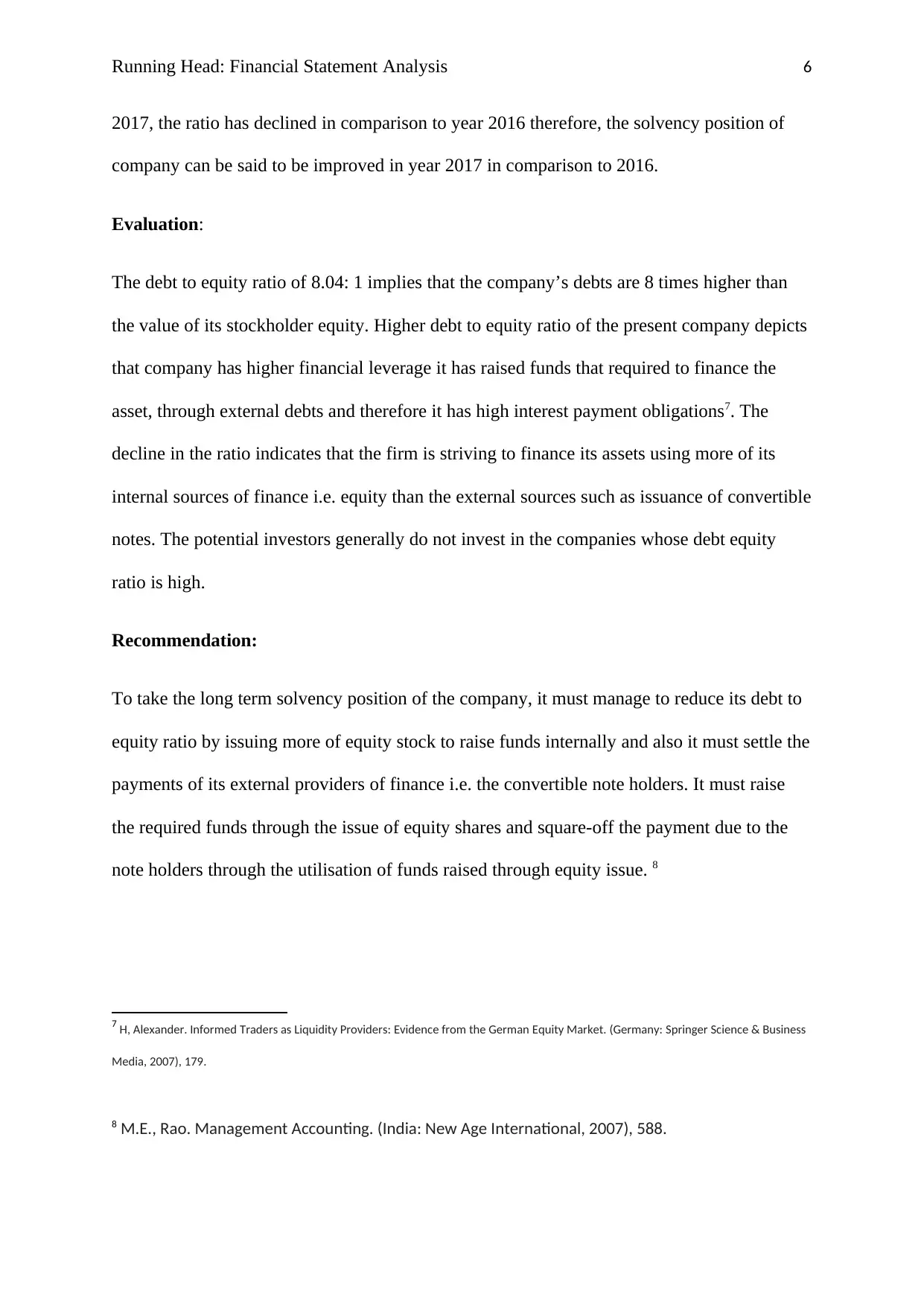

The debt to equity ratio of 8.04: 1 implies that the company’s debts are 8 times higher than

the value of its stockholder equity. Higher debt to equity ratio of the present company depicts

that company has higher financial leverage it has raised funds that required to finance the

asset, through external debts and therefore it has high interest payment obligations7. The

decline in the ratio indicates that the firm is striving to finance its assets using more of its

internal sources of finance i.e. equity than the external sources such as issuance of convertible

notes. The potential investors generally do not invest in the companies whose debt equity

ratio is high.

Recommendation:

To take the long term solvency position of the company, it must manage to reduce its debt to

equity ratio by issuing more of equity stock to raise funds internally and also it must settle the

payments of its external providers of finance i.e. the convertible note holders. It must raise

the required funds through the issue of equity shares and square-off the payment due to the

note holders through the utilisation of funds raised through equity issue. 8

7 H, Alexander. Informed Traders as Liquidity Providers: Evidence from the German Equity Market. (Germany: Springer Science & Business

Media, 2007), 179.

8 M.E., Rao. Management Accounting. (India: New Age International, 2007), 588.

2017, the ratio has declined in comparison to year 2016 therefore, the solvency position of

company can be said to be improved in year 2017 in comparison to 2016.

Evaluation:

The debt to equity ratio of 8.04: 1 implies that the company’s debts are 8 times higher than

the value of its stockholder equity. Higher debt to equity ratio of the present company depicts

that company has higher financial leverage it has raised funds that required to finance the

asset, through external debts and therefore it has high interest payment obligations7. The

decline in the ratio indicates that the firm is striving to finance its assets using more of its

internal sources of finance i.e. equity than the external sources such as issuance of convertible

notes. The potential investors generally do not invest in the companies whose debt equity

ratio is high.

Recommendation:

To take the long term solvency position of the company, it must manage to reduce its debt to

equity ratio by issuing more of equity stock to raise funds internally and also it must settle the

payments of its external providers of finance i.e. the convertible note holders. It must raise

the required funds through the issue of equity shares and square-off the payment due to the

note holders through the utilisation of funds raised through equity issue. 8

7 H, Alexander. Informed Traders as Liquidity Providers: Evidence from the German Equity Market. (Germany: Springer Science & Business

Media, 2007), 179.

8 M.E., Rao. Management Accounting. (India: New Age International, 2007), 588.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Financial Statement Analysis 7

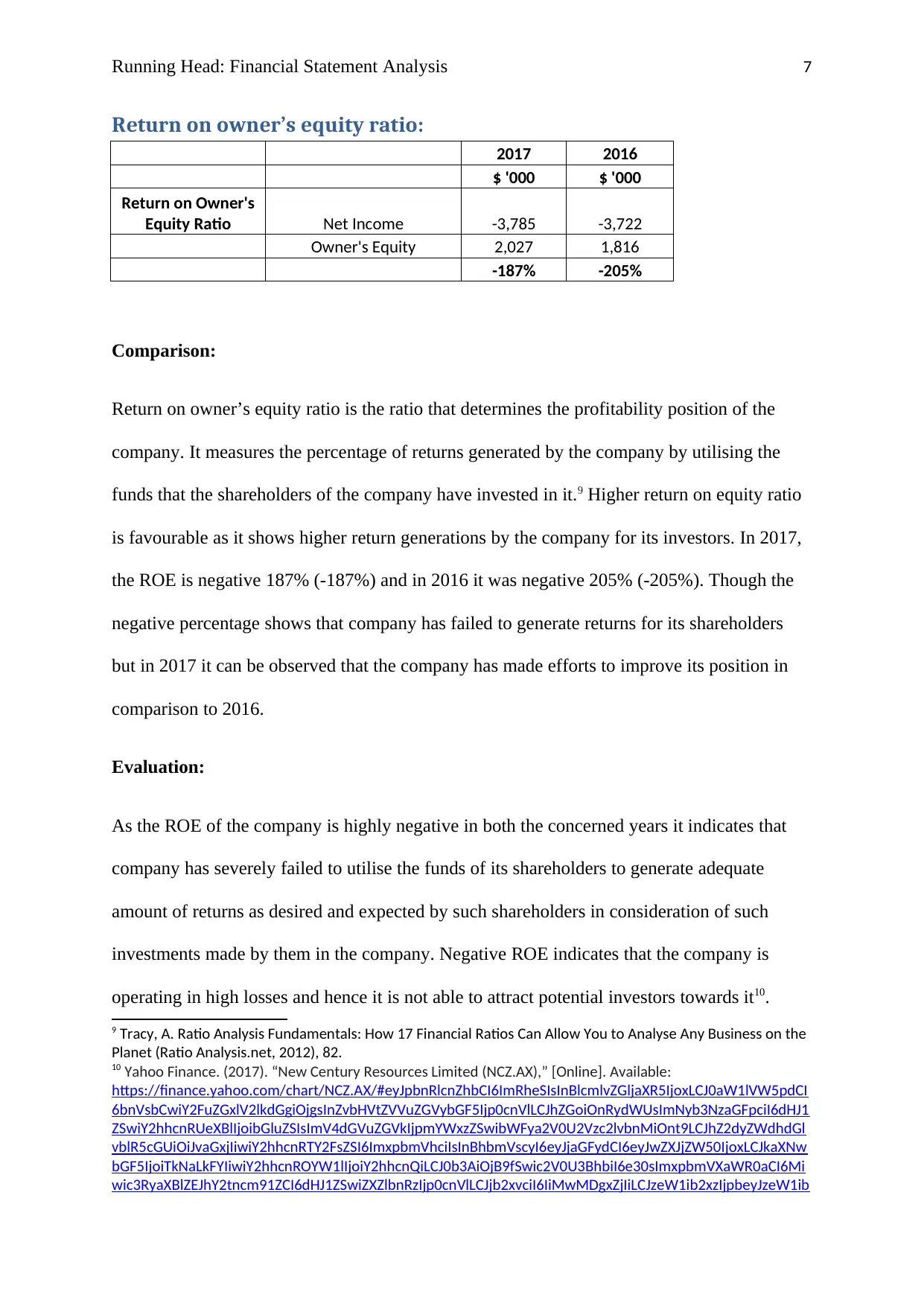

Return on owner’s equity ratio:

2017 2016

$ '000 $ '000

Return on Owner's

Equity Ratio Net Income -3,785 -3,722

Owner's Equity 2,027 1,816

-187% -205%

Comparison:

Return on owner’s equity ratio is the ratio that determines the profitability position of the

company. It measures the percentage of returns generated by the company by utilising the

funds that the shareholders of the company have invested in it.9 Higher return on equity ratio

is favourable as it shows higher return generations by the company for its investors. In 2017,

the ROE is negative 187% (-187%) and in 2016 it was negative 205% (-205%). Though the

negative percentage shows that company has failed to generate returns for its shareholders

but in 2017 it can be observed that the company has made efforts to improve its position in

comparison to 2016.

Evaluation:

As the ROE of the company is highly negative in both the concerned years it indicates that

company has severely failed to utilise the funds of its shareholders to generate adequate

amount of returns as desired and expected by such shareholders in consideration of such

investments made by them in the company. Negative ROE indicates that the company is

operating in high losses and hence it is not able to attract potential investors towards it10.

9 Tracy, A. Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the

Planet (Ratio Analysis.net, 2012), 82.

10 Yahoo Finance. (2017). “New Century Resources Limited (NCZ.AX),” [Online]. Available:

https://finance.yahoo.com/chart/NCZ.AX/#eyJpbnRlcnZhbCI6ImRheSIsInBlcmlvZGljaXR5IjoxLCJ0aW1lVW5pdCI

6bnVsbCwiY2FuZGxlV2lkdGgiOjgsInZvbHVtZVVuZGVybGF5Ijp0cnVlLCJhZGoiOnRydWUsImNyb3NzaGFpciI6dHJ1

ZSwiY2hhcnRUeXBlIjoibGluZSIsImV4dGVuZGVkIjpmYWxzZSwibWFya2V0U2Vzc2lvbnMiOnt9LCJhZ2dyZWdhdGl

vblR5cGUiOiJvaGxjIiwiY2hhcnRTY2FsZSI6ImxpbmVhciIsInBhbmVscyI6eyJjaGFydCI6eyJwZXJjZW50IjoxLCJkaXNw

bGF5IjoiTkNaLkFYIiwiY2hhcnROYW1lIjoiY2hhcnQiLCJ0b3AiOjB9fSwic2V0U3BhbiI6e30sImxpbmVXaWR0aCI6Mi

wic3RyaXBlZEJhY2tncm91ZCI6dHJ1ZSwiZXZlbnRzIjp0cnVlLCJjb2xvciI6IiMwMDgxZjIiLCJzeW1ib2xzIjpbeyJzeW1ib

Return on owner’s equity ratio:

2017 2016

$ '000 $ '000

Return on Owner's

Equity Ratio Net Income -3,785 -3,722

Owner's Equity 2,027 1,816

-187% -205%

Comparison:

Return on owner’s equity ratio is the ratio that determines the profitability position of the

company. It measures the percentage of returns generated by the company by utilising the

funds that the shareholders of the company have invested in it.9 Higher return on equity ratio

is favourable as it shows higher return generations by the company for its investors. In 2017,

the ROE is negative 187% (-187%) and in 2016 it was negative 205% (-205%). Though the

negative percentage shows that company has failed to generate returns for its shareholders

but in 2017 it can be observed that the company has made efforts to improve its position in

comparison to 2016.

Evaluation:

As the ROE of the company is highly negative in both the concerned years it indicates that

company has severely failed to utilise the funds of its shareholders to generate adequate

amount of returns as desired and expected by such shareholders in consideration of such

investments made by them in the company. Negative ROE indicates that the company is

operating in high losses and hence it is not able to attract potential investors towards it10.

9 Tracy, A. Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the

Planet (Ratio Analysis.net, 2012), 82.

10 Yahoo Finance. (2017). “New Century Resources Limited (NCZ.AX),” [Online]. Available:

https://finance.yahoo.com/chart/NCZ.AX/#eyJpbnRlcnZhbCI6ImRheSIsInBlcmlvZGljaXR5IjoxLCJ0aW1lVW5pdCI

6bnVsbCwiY2FuZGxlV2lkdGgiOjgsInZvbHVtZVVuZGVybGF5Ijp0cnVlLCJhZGoiOnRydWUsImNyb3NzaGFpciI6dHJ1

ZSwiY2hhcnRUeXBlIjoibGluZSIsImV4dGVuZGVkIjpmYWxzZSwibWFya2V0U2Vzc2lvbnMiOnt9LCJhZ2dyZWdhdGl

vblR5cGUiOiJvaGxjIiwiY2hhcnRTY2FsZSI6ImxpbmVhciIsInBhbmVscyI6eyJjaGFydCI6eyJwZXJjZW50IjoxLCJkaXNw

bGF5IjoiTkNaLkFYIiwiY2hhcnROYW1lIjoiY2hhcnQiLCJ0b3AiOjB9fSwic2V0U3BhbiI6e30sImxpbmVXaWR0aCI6Mi

wic3RyaXBlZEJhY2tncm91ZCI6dHJ1ZSwiZXZlbnRzIjp0cnVlLCJjb2xvciI6IiMwMDgxZjIiLCJzeW1ib2xzIjpbeyJzeW1ib

Running Head: Financial Statement Analysis 8

Recommendation:

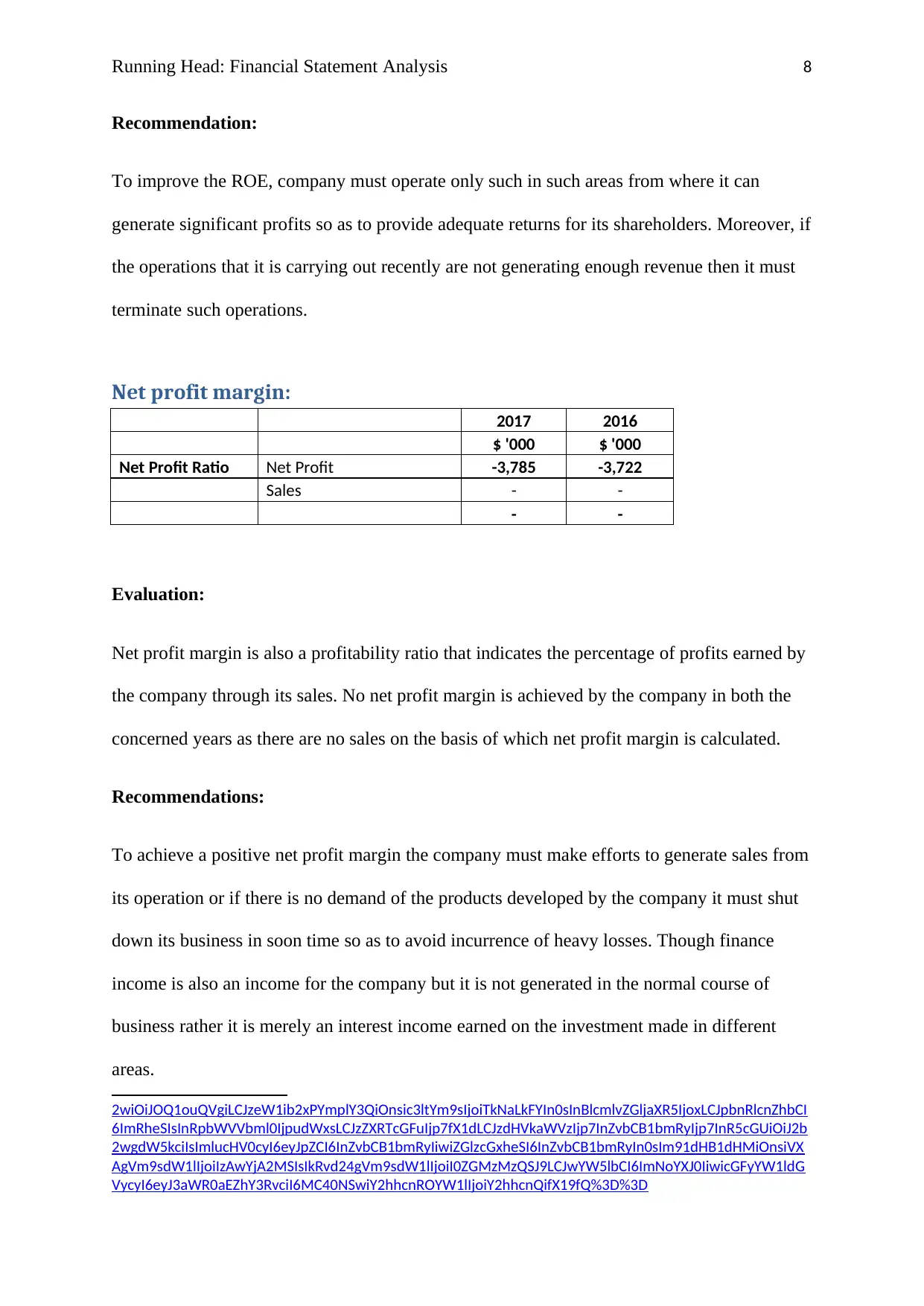

To improve the ROE, company must operate only such in such areas from where it can

generate significant profits so as to provide adequate returns for its shareholders. Moreover, if

the operations that it is carrying out recently are not generating enough revenue then it must

terminate such operations.

Net profit margin:

2017 2016

$ '000 $ '000

Net Profit Ratio Net Profit -3,785 -3,722

Sales - -

- -

Evaluation:

Net profit margin is also a profitability ratio that indicates the percentage of profits earned by

the company through its sales. No net profit margin is achieved by the company in both the

concerned years as there are no sales on the basis of which net profit margin is calculated.

Recommendations:

To achieve a positive net profit margin the company must make efforts to generate sales from

its operation or if there is no demand of the products developed by the company it must shut

down its business in soon time so as to avoid incurrence of heavy losses. Though finance

income is also an income for the company but it is not generated in the normal course of

business rather it is merely an interest income earned on the investment made in different

areas.

2wiOiJOQ1ouQVgiLCJzeW1ib2xPYmplY3QiOnsic3ltYm9sIjoiTkNaLkFYIn0sInBlcmlvZGljaXR5IjoxLCJpbnRlcnZhbCI

6ImRheSIsInRpbWVVbml0IjpudWxsLCJzZXRTcGFuIjp7fX1dLCJzdHVkaWVzIjp7InZvbCB1bmRyIjp7InR5cGUiOiJ2b

2wgdW5kciIsImlucHV0cyI6eyJpZCI6InZvbCB1bmRyIiwiZGlzcGxheSI6InZvbCB1bmRyIn0sIm91dHB1dHMiOnsiVX

AgVm9sdW1lIjoiIzAwYjA2MSIsIkRvd24gVm9sdW1lIjoiI0ZGMzMzQSJ9LCJwYW5lbCI6ImNoYXJ0IiwicGFyYW1ldG

VycyI6eyJ3aWR0aEZhY3RvciI6MC40NSwiY2hhcnROYW1lIjoiY2hhcnQifX19fQ%3D%3D

Recommendation:

To improve the ROE, company must operate only such in such areas from where it can

generate significant profits so as to provide adequate returns for its shareholders. Moreover, if

the operations that it is carrying out recently are not generating enough revenue then it must

terminate such operations.

Net profit margin:

2017 2016

$ '000 $ '000

Net Profit Ratio Net Profit -3,785 -3,722

Sales - -

- -

Evaluation:

Net profit margin is also a profitability ratio that indicates the percentage of profits earned by

the company through its sales. No net profit margin is achieved by the company in both the

concerned years as there are no sales on the basis of which net profit margin is calculated.

Recommendations:

To achieve a positive net profit margin the company must make efforts to generate sales from

its operation or if there is no demand of the products developed by the company it must shut

down its business in soon time so as to avoid incurrence of heavy losses. Though finance

income is also an income for the company but it is not generated in the normal course of

business rather it is merely an interest income earned on the investment made in different

areas.

2wiOiJOQ1ouQVgiLCJzeW1ib2xPYmplY3QiOnsic3ltYm9sIjoiTkNaLkFYIn0sInBlcmlvZGljaXR5IjoxLCJpbnRlcnZhbCI

6ImRheSIsInRpbWVVbml0IjpudWxsLCJzZXRTcGFuIjp7fX1dLCJzdHVkaWVzIjp7InZvbCB1bmRyIjp7InR5cGUiOiJ2b

2wgdW5kciIsImlucHV0cyI6eyJpZCI6InZvbCB1bmRyIiwiZGlzcGxheSI6InZvbCB1bmRyIn0sIm91dHB1dHMiOnsiVX

AgVm9sdW1lIjoiIzAwYjA2MSIsIkRvd24gVm9sdW1lIjoiI0ZGMzMzQSJ9LCJwYW5lbCI6ImNoYXJ0IiwicGFyYW1ldG

VycyI6eyJ3aWR0aEZhY3RvciI6MC40NSwiY2hhcnROYW1lIjoiY2hhcnQifX19fQ%3D%3D

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: Financial Statement Analysis 9

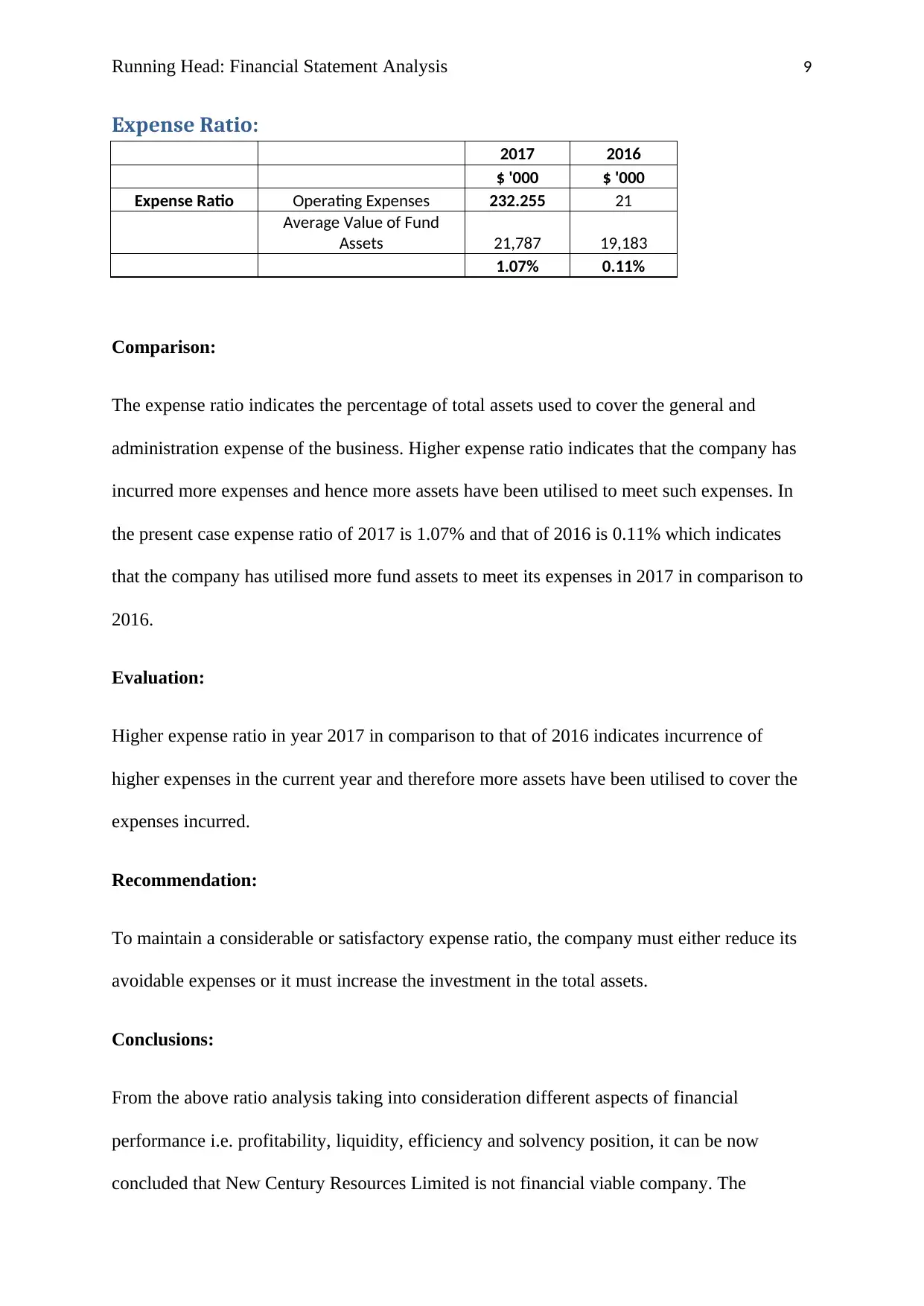

Expense Ratio:

2017 2016

$ '000 $ '000

Expense Ratio Operating Expenses 232.255 21

Average Value of Fund

Assets 21,787 19,183

1.07% 0.11%

Comparison:

The expense ratio indicates the percentage of total assets used to cover the general and

administration expense of the business. Higher expense ratio indicates that the company has

incurred more expenses and hence more assets have been utilised to meet such expenses. In

the present case expense ratio of 2017 is 1.07% and that of 2016 is 0.11% which indicates

that the company has utilised more fund assets to meet its expenses in 2017 in comparison to

2016.

Evaluation:

Higher expense ratio in year 2017 in comparison to that of 2016 indicates incurrence of

higher expenses in the current year and therefore more assets have been utilised to cover the

expenses incurred.

Recommendation:

To maintain a considerable or satisfactory expense ratio, the company must either reduce its

avoidable expenses or it must increase the investment in the total assets.

Conclusions:

From the above ratio analysis taking into consideration different aspects of financial

performance i.e. profitability, liquidity, efficiency and solvency position, it can be now

concluded that New Century Resources Limited is not financial viable company. The

Expense Ratio:

2017 2016

$ '000 $ '000

Expense Ratio Operating Expenses 232.255 21

Average Value of Fund

Assets 21,787 19,183

1.07% 0.11%

Comparison:

The expense ratio indicates the percentage of total assets used to cover the general and

administration expense of the business. Higher expense ratio indicates that the company has

incurred more expenses and hence more assets have been utilised to meet such expenses. In

the present case expense ratio of 2017 is 1.07% and that of 2016 is 0.11% which indicates

that the company has utilised more fund assets to meet its expenses in 2017 in comparison to

2016.

Evaluation:

Higher expense ratio in year 2017 in comparison to that of 2016 indicates incurrence of

higher expenses in the current year and therefore more assets have been utilised to cover the

expenses incurred.

Recommendation:

To maintain a considerable or satisfactory expense ratio, the company must either reduce its

avoidable expenses or it must increase the investment in the total assets.

Conclusions:

From the above ratio analysis taking into consideration different aspects of financial

performance i.e. profitability, liquidity, efficiency and solvency position, it can be now

concluded that New Century Resources Limited is not financial viable company. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Financial Statement Analysis 10

financial performance of the company is not sustainable and hence it is not capable of

attracting the potential investors towards it. The ratio analysis has clearly proved that the

company is not holding a profitable and liquidity position in the market.

financial performance of the company is not sustainable and hence it is not capable of

attracting the potential investors towards it. The ratio analysis has clearly proved that the

company is not holding a profitable and liquidity position in the market.

Running Head: Financial Statement Analysis 11

Bibliography:

Pandey, I.M. Financial Management. India: Vikas Publishing House, 2015.

Cull, R. K., and Morduch, J. “Financial Performance and Outreach: A Global Analysis of

Leading Microbanks”. The Economic Journal, Vol. 117, No. 517, F107-F133.

Axel, T. Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse

Any Business on the Planet. Ratio Analysis.net, 2012.

Panagiotis, P. Investment Report - Fundamental Analysis/ Ratio Analysis: Comparative

Approach between two FTSE 100 corporations Vodafone plc and British Telecom Group.

Germany: GRIN Verlag , 2011.

Alice, C., Lee, J, C. Lee, Cheng, F., and Lee. Financial Analysis, Planning & Forecasting:

Theory and Application. Singapore: World Scientific, 2009.

Robert, M. Financial Management in Health Care Organizations. U.S: Cengage Learning,

2002.

Alexandra, H. Informed Traders as Liquidity Providers: Evidence from the German Equity

Market. Germany: Springer Science & Business Media, 2007.

Yahoo Finance. (2017). “New Century Resources Limited (NCZ.AX),” [Online].

https://finance.yahoo.com/chart/NCZ.AX/#eyJpbnRlcnZhbCI6ImRheSIsInBlcmlvZGljaXR5I

joxLCJ0aW1lVW5pdCI6bnVsbCwiY2FuZGxlV2lkdGgiOjgsInZvbHVtZVVuZGVybGF5Ijp

0cnVlLCJhZGoiOnRydWUsImNyb3NzaGFpciI6dHJ1ZSwiY2hhcnRUeXBlIjoibGluZSIsIm

V4dGVuZGVkIjpmYWxzZSwibWFya2V0U2Vzc2lvbnMiOnt9LCJhZ2dyZWdhdGlvblR5c

GUiOiJvaGxjIiwiY2hhcnRTY2FsZSI6ImxpbmVhciIsInBhbmVscyI6eyJjaGFydCI6eyJwZXJ

jZW50IjoxLCJkaXNwbGF5IjoiTkNaLkFYIiwiY2hhcnROYW1lIjoiY2hhcnQiLCJ0b3AiOjB

Bibliography:

Pandey, I.M. Financial Management. India: Vikas Publishing House, 2015.

Cull, R. K., and Morduch, J. “Financial Performance and Outreach: A Global Analysis of

Leading Microbanks”. The Economic Journal, Vol. 117, No. 517, F107-F133.

Axel, T. Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse

Any Business on the Planet. Ratio Analysis.net, 2012.

Panagiotis, P. Investment Report - Fundamental Analysis/ Ratio Analysis: Comparative

Approach between two FTSE 100 corporations Vodafone plc and British Telecom Group.

Germany: GRIN Verlag , 2011.

Alice, C., Lee, J, C. Lee, Cheng, F., and Lee. Financial Analysis, Planning & Forecasting:

Theory and Application. Singapore: World Scientific, 2009.

Robert, M. Financial Management in Health Care Organizations. U.S: Cengage Learning,

2002.

Alexandra, H. Informed Traders as Liquidity Providers: Evidence from the German Equity

Market. Germany: Springer Science & Business Media, 2007.

Yahoo Finance. (2017). “New Century Resources Limited (NCZ.AX),” [Online].

https://finance.yahoo.com/chart/NCZ.AX/#eyJpbnRlcnZhbCI6ImRheSIsInBlcmlvZGljaXR5I

joxLCJ0aW1lVW5pdCI6bnVsbCwiY2FuZGxlV2lkdGgiOjgsInZvbHVtZVVuZGVybGF5Ijp

0cnVlLCJhZGoiOnRydWUsImNyb3NzaGFpciI6dHJ1ZSwiY2hhcnRUeXBlIjoibGluZSIsIm

V4dGVuZGVkIjpmYWxzZSwibWFya2V0U2Vzc2lvbnMiOnt9LCJhZ2dyZWdhdGlvblR5c

GUiOiJvaGxjIiwiY2hhcnRTY2FsZSI6ImxpbmVhciIsInBhbmVscyI6eyJjaGFydCI6eyJwZXJ

jZW50IjoxLCJkaXNwbGF5IjoiTkNaLkFYIiwiY2hhcnROYW1lIjoiY2hhcnQiLCJ0b3AiOjB

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.