Financial and Operational Analysis Report: New Life Brewery Expansion

VerifiedAdded on 2020/07/22

|21

|6204

|50

Report

AI Summary

This report provides a comprehensive analysis of New Life Brewery's operations and finances, examining the operational and regulatory factors the board must consider, particularly within the UK's beer industry. It details legal requirements, quality standards, record-keeping, transportation rules, and import regulations. The report also includes an overview of market conditions and trends, including the growth of the UK wine and beer markets, and suggests strategies for market development. Furthermore, it evaluates financing alternatives for the brewery's expansion plans, which include equity capital, loans, and venture funding. The financial analysis includes the costs associated with extending the brewery and purchasing new equipment. The report also challenges the proposed financial plan and performs calculations like break-even and contribution analysis to assess the project's viability, ultimately offering conclusions and recommendations based on the overall findings.

MANAGING FINANCE AND OPERATIONS

1 | P a g e

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

(a)Operational and Regulatory factors to be considered by board..............................................1

(b)Financing Alternatives for New Life Brewery.......................................................................4

©Critical evaluation of financial worth.......................................................................................6

Challenging the proposed plan:...................................................................................................4

(d)Conclusion and recommendation................................................................................................5

Conclusion...................................................................................................................................5

Recommendations........................................................................................................................6

REFERENCES................................................................................................................................7

2 | P a g e

INTRODUCTION...........................................................................................................................1

(a)Operational and Regulatory factors to be considered by board..............................................1

(b)Financing Alternatives for New Life Brewery.......................................................................4

©Critical evaluation of financial worth.......................................................................................6

Challenging the proposed plan:...................................................................................................4

(d)Conclusion and recommendation................................................................................................5

Conclusion...................................................................................................................................5

Recommendations........................................................................................................................6

REFERENCES................................................................................................................................7

2 | P a g e

INTRODUCTION

New life brewery is operating in beverage business. Becerage industry is growing at rapid

rate and due to this reason, number of firms in mentioned domain are also elevating consistently.

In the current report In this report, in context of firm’s operational and regulatory factors need to

be considered are described. Finance is the one of the important domain where firms needs to

focus heavily in order to improve their performance. Varied aspects of finance are discussed in

detail. Calculation related to project evaluation methods are applied on data and interpretation is

made. Viability of the project is measured because of with the help of calculated figures. Figures

that are taken into account in order to perform calculations are also challenged in order to make

project more viable. In the current research study, varied other calculations are also performed

like break-even analysis and contribution analysis. Apart from this, operational and regulatory

factors in respect to beer business are also discussed briefly. At end of the report on basis of

overall workings, conclusion is formed derived.

(a)Operational and regulatory factors to be considered by board

Legal part

There are number of operational and regulatory factors that need to be considered by

Board as per law of UK. This is because there are strict rules and regulations and firms are

required to follow them in order to do business in a lawful manner. In case managers fail to

comply with these rules, strict action can be taken against them. Thus, it is very important for the

firms to follow all rules and regulations tightly. In past couple of years, those firms that are in

beer business tried to improve their corporate governance system so that it can be ensured that all

rules are followed strictly in the organisation (Beer trade regulations, 2012).

It is observed that in UK, courts take strict decisions actions against firms who are

involved in unethical practices. Thus, it becomes very important for the companies to develop

separate team within their premise who will look after all legal matters and ensure that all rules

are abided by, for performing business operations. It can be observed that there are varied quality

standards for beer that must be followed by managers. Some of these quality standards are

explained below.

Minimum and maximum intensity of alcohol.

Level of acidity in beer.

1 | P a g e

New life brewery is operating in beverage business. Becerage industry is growing at rapid

rate and due to this reason, number of firms in mentioned domain are also elevating consistently.

In the current report In this report, in context of firm’s operational and regulatory factors need to

be considered are described. Finance is the one of the important domain where firms needs to

focus heavily in order to improve their performance. Varied aspects of finance are discussed in

detail. Calculation related to project evaluation methods are applied on data and interpretation is

made. Viability of the project is measured because of with the help of calculated figures. Figures

that are taken into account in order to perform calculations are also challenged in order to make

project more viable. In the current research study, varied other calculations are also performed

like break-even analysis and contribution analysis. Apart from this, operational and regulatory

factors in respect to beer business are also discussed briefly. At end of the report on basis of

overall workings, conclusion is formed derived.

(a)Operational and regulatory factors to be considered by board

Legal part

There are number of operational and regulatory factors that need to be considered by

Board as per law of UK. This is because there are strict rules and regulations and firms are

required to follow them in order to do business in a lawful manner. In case managers fail to

comply with these rules, strict action can be taken against them. Thus, it is very important for the

firms to follow all rules and regulations tightly. In past couple of years, those firms that are in

beer business tried to improve their corporate governance system so that it can be ensured that all

rules are followed strictly in the organisation (Beer trade regulations, 2012).

It is observed that in UK, courts take strict decisions actions against firms who are

involved in unethical practices. Thus, it becomes very important for the companies to develop

separate team within their premise who will look after all legal matters and ensure that all rules

are abided by, for performing business operations. It can be observed that there are varied quality

standards for beer that must be followed by managers. Some of these quality standards are

explained below.

Minimum and maximum intensity of alcohol.

Level of acidity in beer.

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Additives that are added in beer.

Sugar quantity in beer that is packed in bottle.

Concentration of additives on fragmentation.

Concentration of sulphur dioxide.

Copper presence in beer.

Beer blends.

Rules for labeling of beer bottles: These are some of the important parameters that are

taken into account for different categories and subcategories of beer. As per rules, testing

of beer is done in UK, by-UK Vineyards Association (UVKA). Apart from this, there are

labeling rules and regulations in respect to beer. It can be observed that labeling rules

apply to all beer-based products that are marketed in EU. In respect to specific situation,

if there is no rule then food regulations are applied on them. For all firms that are

operating their businesses in UK it is mandatory foe them to furnish information about

different categories and sub categories of beer (Galbreath, 2011). In case not all relevant

information is available, on packaged bottle then in that case warnings are given to the

firms and penalty is also charged on firm.

Rules for keeping record of transactions: Record keeping is another factor that need to

be considered by Board. As per rules, it is mandatory for the firms to keep record of

accomplishment of all transactions and movement in their goods and services. Means that

beermaker have liability, in which it is responsible to give notification to local beer

standard branch inspector ,48 hours before production (Beer duty, 2009). In this regard,

on basis of analysis it can be said that firm is required to fill a form, WSB10 notification

for enrichment. Business firm needs to keep record of accomplishment of enrichment

process of day-to-day operations. For example, it is mandatory for the firms to keep

record of ransactionsof movement of graphs like from vineyard to berry.

Rules for transportation of products: Commercial Accompanying Documents (CAD) are

required by the firms to give information to relevant authority about logistics related

operations. This document is needed to be filled by the firm when grapes are transported

more than 25 miles (Hanf, Belaya and Schweickert, 2012). CAD form also need to be

filled by those who are growing grapes, which will be sold to beer companies. Each year

before harvest relevant entity needs to submit document to relevant authority. This thing

2 | P a g e

Sugar quantity in beer that is packed in bottle.

Concentration of additives on fragmentation.

Concentration of sulphur dioxide.

Copper presence in beer.

Beer blends.

Rules for labeling of beer bottles: These are some of the important parameters that are

taken into account for different categories and subcategories of beer. As per rules, testing

of beer is done in UK, by-UK Vineyards Association (UVKA). Apart from this, there are

labeling rules and regulations in respect to beer. It can be observed that labeling rules

apply to all beer-based products that are marketed in EU. In respect to specific situation,

if there is no rule then food regulations are applied on them. For all firms that are

operating their businesses in UK it is mandatory foe them to furnish information about

different categories and sub categories of beer (Galbreath, 2011). In case not all relevant

information is available, on packaged bottle then in that case warnings are given to the

firms and penalty is also charged on firm.

Rules for keeping record of transactions: Record keeping is another factor that need to

be considered by Board. As per rules, it is mandatory for the firms to keep record of

accomplishment of all transactions and movement in their goods and services. Means that

beermaker have liability, in which it is responsible to give notification to local beer

standard branch inspector ,48 hours before production (Beer duty, 2009). In this regard,

on basis of analysis it can be said that firm is required to fill a form, WSB10 notification

for enrichment. Business firm needs to keep record of accomplishment of enrichment

process of day-to-day operations. For example, it is mandatory for the firms to keep

record of ransactionsof movement of graphs like from vineyard to berry.

Rules for transportation of products: Commercial Accompanying Documents (CAD) are

required by the firms to give information to relevant authority about logistics related

operations. This document is needed to be filled by the firm when grapes are transported

more than 25 miles (Hanf, Belaya and Schweickert, 2012). CAD form also need to be

filled by those who are growing grapes, which will be sold to beer companies. Each year

before harvest relevant entity needs to submit document to relevant authority. This thing

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

helps beer board to check berry record. On analysis, it can be said that in case it is

identified that beer making firms failed to submit relevant documents then in that case

strict action can be taken against them. For this the regulatory authority on the business

firm charges strict penalty. 24 hours before operation it is necessary to complete

procedures related to enrichment, de-acidification, sweetening, blending and packaging

as well as sparkling beer.

Rules for in depth recording of product related information: It is also mandatory for

beer making companies to record nature and quantity of products that they are producing

like cane, beet sugar and calcium bicarbonate. Managers need to forward information

about quantity of goods that they produced for different beer to relevant

authority(Mitchell, Charters and Albrecht, 2012). Managers require giving details of

supplier and date on which raw material was received from them. In case of bottling of

beer legally firm need to maintain record under which it need to reveal date of packaging,

number of packaging in single day and size of bottle. Electronic record of these facts

need to be kept in the firm. As per rules, Beer standard branch inspector must approve

computer.

Rules for import of beer products: Apart from this, in case of transport of beer also there

is strict need to follow rules very tightly. UK firms that import beer from other nations

needs to ensure that all documents are scrutinized and all rules are followed in conform to

EU rules. Several forms need to be received from exporting company like A VI 1 is the

document that is issued in third party country under which beer imported in to European

community is fully described in detail (Beer duty, 2009). In case consignment is splitting

to different locations in UK then in that case it is mandatory to receive VI 2 forms. It is

very hard task for the managers to keep in mind every rule and there are chances of

failure to comply with these rules. Government must try to simplify these rules so that

with limited procedures all rules can be followed.

Therefore, these are varied operational and legal rules and regulations that beer making

firms or those companies that are selling beer needs to follow in their business. It can be said that

slight failure in following rules and regulations may prove costly to the firm. In case of failure to

follow rules and regulations firm image may tarnished among customers. Thus, it is very

important for Board members to focus on all relevant factors. In this regard they can do lot of

3 | P a g e

identified that beer making firms failed to submit relevant documents then in that case

strict action can be taken against them. For this the regulatory authority on the business

firm charges strict penalty. 24 hours before operation it is necessary to complete

procedures related to enrichment, de-acidification, sweetening, blending and packaging

as well as sparkling beer.

Rules for in depth recording of product related information: It is also mandatory for

beer making companies to record nature and quantity of products that they are producing

like cane, beet sugar and calcium bicarbonate. Managers need to forward information

about quantity of goods that they produced for different beer to relevant

authority(Mitchell, Charters and Albrecht, 2012). Managers require giving details of

supplier and date on which raw material was received from them. In case of bottling of

beer legally firm need to maintain record under which it need to reveal date of packaging,

number of packaging in single day and size of bottle. Electronic record of these facts

need to be kept in the firm. As per rules, Beer standard branch inspector must approve

computer.

Rules for import of beer products: Apart from this, in case of transport of beer also there

is strict need to follow rules very tightly. UK firms that import beer from other nations

needs to ensure that all documents are scrutinized and all rules are followed in conform to

EU rules. Several forms need to be received from exporting company like A VI 1 is the

document that is issued in third party country under which beer imported in to European

community is fully described in detail (Beer duty, 2009). In case consignment is splitting

to different locations in UK then in that case it is mandatory to receive VI 2 forms. It is

very hard task for the managers to keep in mind every rule and there are chances of

failure to comply with these rules. Government must try to simplify these rules so that

with limited procedures all rules can be followed.

Therefore, these are varied operational and legal rules and regulations that beer making

firms or those companies that are selling beer needs to follow in their business. It can be said that

slight failure in following rules and regulations may prove costly to the firm. In case of failure to

follow rules and regulations firm image may tarnished among customers. Thus, it is very

important for Board members to focus on all relevant factors. In this regard they can do lot of

3 | P a g e

things such as they can form a team of 5 to 6 members who will look after entire process and

will ensure that each and every paper work is completed on time.

Market information and development

Figure 1Trends in market

4 | P a g e

will ensure that each and every paper work is completed on time.

Market information and development

Figure 1Trends in market

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

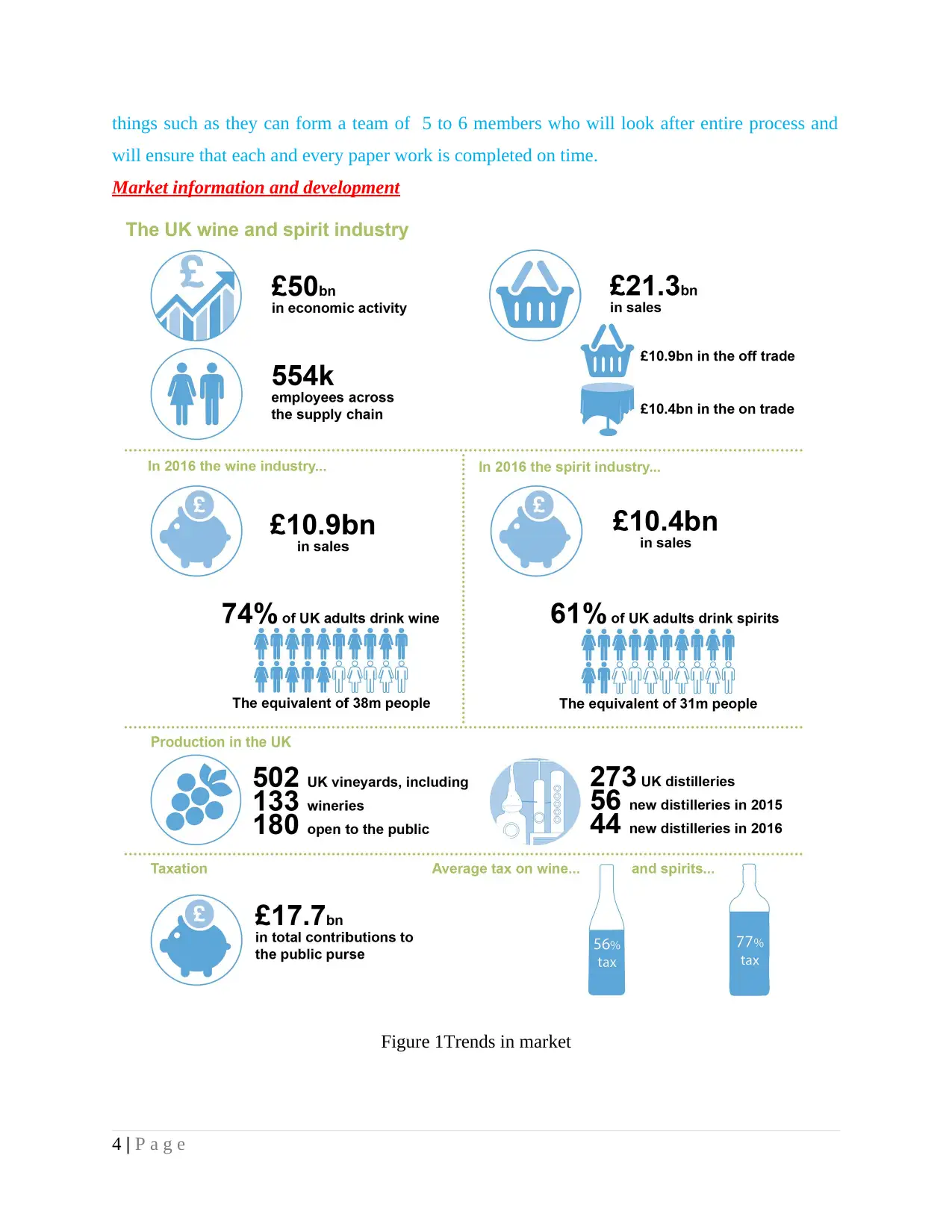

Above Figure is reflecting that 74% of UK adults drink wine. There are 502 vineyards in

the UK followed by 133 wineries. There are 273 distillers in UK, out of all distilleries 56 new

distilleries were opened in 2015. However, this number slightly declined to 44 in 2016. UK wine

industry have economic activity of 50 billion and it employe about 554000 employees in entire

supply chain. This reflects that there is huge size of UK wine industry. Market conditions for the

firm products improved in past years (Number of UK breweries rises as craft beer shows no

signs of going flat, 2012). Facts revealed that gin sales increased by 16% and sale of bear also

increased almost by same percentage on yearly basis. Extent to which market can be estimated

from the fact that in FY 2010 there were 116 distillers in the UK market which increased to 100

in just two years. This reflects that there is huge growth potential in the market and firm must

invest more to capitalize opportunity. In order to develop market, company can follow franchise

model and under this, it can establish contact with owners of medium sized retail shops and can

motivate them to take franchisee of the firm’s product. This will make brand name popular

among the firm and product sales will increase at rapid rate.

Logistic model of supply chain

As part of this supply chain model for distribution of goods in each state of UK, there

will be three hubs or warehouses. One of them will be located in central area of state and

remaining two will be located at the opposite border of state. According to demand and supply in

short duration, distillers gin can be distributed to any location according to orders received. In

this way transportation cost can also be controlled.

(b)Financing alternatives for New Life Brewery

The New Life Brewery Co. is looking to expand its product line in the near future. This

report is to identify the need for finance and defining alternatives to finance needs of the

expansion plan. The plan for launching the product specifies a need of:

Cost of extending the brewery for allowance of distillation process £5.0 million

Cost of purchase of new equipment for production £2.0 million

£7.0 million

The plan also specifies that in order to expand the brewery market, distilling gins, vodka

and cognac should be stored all in used beer casks to infuse the flavours of the New life brewery

beer. In this production of new products the staff cost per bottle is thought to be £3.00. And after

5 | P a g e

the UK followed by 133 wineries. There are 273 distillers in UK, out of all distilleries 56 new

distilleries were opened in 2015. However, this number slightly declined to 44 in 2016. UK wine

industry have economic activity of 50 billion and it employe about 554000 employees in entire

supply chain. This reflects that there is huge size of UK wine industry. Market conditions for the

firm products improved in past years (Number of UK breweries rises as craft beer shows no

signs of going flat, 2012). Facts revealed that gin sales increased by 16% and sale of bear also

increased almost by same percentage on yearly basis. Extent to which market can be estimated

from the fact that in FY 2010 there were 116 distillers in the UK market which increased to 100

in just two years. This reflects that there is huge growth potential in the market and firm must

invest more to capitalize opportunity. In order to develop market, company can follow franchise

model and under this, it can establish contact with owners of medium sized retail shops and can

motivate them to take franchisee of the firm’s product. This will make brand name popular

among the firm and product sales will increase at rapid rate.

Logistic model of supply chain

As part of this supply chain model for distribution of goods in each state of UK, there

will be three hubs or warehouses. One of them will be located in central area of state and

remaining two will be located at the opposite border of state. According to demand and supply in

short duration, distillers gin can be distributed to any location according to orders received. In

this way transportation cost can also be controlled.

(b)Financing alternatives for New Life Brewery

The New Life Brewery Co. is looking to expand its product line in the near future. This

report is to identify the need for finance and defining alternatives to finance needs of the

expansion plan. The plan for launching the product specifies a need of:

Cost of extending the brewery for allowance of distillation process £5.0 million

Cost of purchase of new equipment for production £2.0 million

£7.0 million

The plan also specifies that in order to expand the brewery market, distilling gins, vodka

and cognac should be stored all in used beer casks to infuse the flavours of the New life brewery

beer. In this production of new products the staff cost per bottle is thought to be £3.00. And after

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

listening to the plan the directors of the company pointed out that cost of ingredients £1.00 per

bottle was not omitted. If the company starts the production it needs long-term finance of at least

£7.00 million to develop the production capacity, and short-term finance as well to run the day to

day operations for the new production.

Long term financing alternatives: The long-term financing requirement can be fulfilled

by the following tools or alternatives for the amount needed for the installation of new product

line.

1. Equity capital: The New life brewery can satisfy its long-term financing

requirements by the issue of equity shares. The issue of equity of shares will

require a change in the memorandum of association as the authorised capital have

already been issued (Kalamova, Kaminker. and Johnstone, 2011). With an

addition to the equity share holding the financing needs can be achieved. Main

advantage of equity is that huge amount of funds can be raised from the market.

Major disadvantage is that increased shareholding lead to decline in decision-

making power of owners of the firm. Thus, firm must cautiously select mentioned

alternative.

2. Loan: Applying for a long-term credit facility in the financing institution for

fulfilling the financial needs of the company. The company can ask for a loan to

the bank on security of its total assets. Firm cannot make use of this alternative

because it has already taken sufficient amount of debt from the market.

3. Venture funding: Company can do arrange funds by taking from any interested

investor. Investors invest in new potential ventures of by the company. These

investors take a stake in the venture for the investment made (Corsatea, Giaccaria

and Arántegui, 2014). There are some advantages and disadvantages of the

venture funding. Main advantage of mentioned source of finance is that during

different stages of project, required amount can be obtained from the venture

capital firm easily. Thus, sufficient amount of fund is available through mentioned

source of finance. Main demerit is that cost of venture capital finance is so high

and nearby to 50% shareholding is given to VC firm. Thus, firm have to bear

burden of heavy cost of finance and control of real owners on the firm is reduced.

However, the situation where firm stands venture capital is the only source of

6 | P a g e

bottle was not omitted. If the company starts the production it needs long-term finance of at least

£7.00 million to develop the production capacity, and short-term finance as well to run the day to

day operations for the new production.

Long term financing alternatives: The long-term financing requirement can be fulfilled

by the following tools or alternatives for the amount needed for the installation of new product

line.

1. Equity capital: The New life brewery can satisfy its long-term financing

requirements by the issue of equity shares. The issue of equity of shares will

require a change in the memorandum of association as the authorised capital have

already been issued (Kalamova, Kaminker. and Johnstone, 2011). With an

addition to the equity share holding the financing needs can be achieved. Main

advantage of equity is that huge amount of funds can be raised from the market.

Major disadvantage is that increased shareholding lead to decline in decision-

making power of owners of the firm. Thus, firm must cautiously select mentioned

alternative.

2. Loan: Applying for a long-term credit facility in the financing institution for

fulfilling the financial needs of the company. The company can ask for a loan to

the bank on security of its total assets. Firm cannot make use of this alternative

because it has already taken sufficient amount of debt from the market.

3. Venture funding: Company can do arrange funds by taking from any interested

investor. Investors invest in new potential ventures of by the company. These

investors take a stake in the venture for the investment made (Corsatea, Giaccaria

and Arántegui, 2014). There are some advantages and disadvantages of the

venture funding. Main advantage of mentioned source of finance is that during

different stages of project, required amount can be obtained from the venture

capital firm easily. Thus, sufficient amount of fund is available through mentioned

source of finance. Main demerit is that cost of venture capital finance is so high

and nearby to 50% shareholding is given to VC firm. Thus, firm have to bear

burden of heavy cost of finance and control of real owners on the firm is reduced.

However, the situation where firm stands venture capital is the only source of

6 | P a g e

finance on which firm can focus to meet its needs.

4. Cloud funding: It is another alternative that is available to the firm and under this

through internet firm can raise 7 million amounts from different individuals. Main

advantage of cloud funding is that it is very easy approach through which in small

proportion large amount of fund can be raised from the market. Main limitation is

that it is not necessary that firm will successfully raise entire required amount

through this source of finance. Thus, any company cannot solely depend on cloud

funding to meet its needs.

Suggested source of finance

Venture capital as a source of finance is suggested to the firm because it has already taken

heavy loan from the market. There is probability that firm if intend to raise fund through equity

offer, which might remain unsubscribed. Thus, fund will be raised from venture capital so that

sufficient amount of fund may be available on time at different stages of project.

The company can also fund the project with the combination of the above financing

alternative. A good combination will require a part of equity and credit potential.

Short term financing alternatives: Short-term working capital needs or requirement of

finance to run the day to day errands:

1. Short-term loans: The Company can apply for short-term working capital loans

from commercial banks to run the day-to-day activities of the production in

application of a new plan of product line expansion. It is mandatory for the

managers to ensure that they will be able to pay short-term loan on time

(Caglayan and Demir, 2014). Default in repayment can tarnish firm image among

customers.

2. Loan from friends: Firm can take loan from business friends to meet its short-

term financial needs. This source must be kept as alternative option in case bank

deny from giving short-term loan to firm.

©Critical evaluation of financial worth

As we go through the New Life Brewery's statement. The 6 years of sales statement is

given in which up to 3 years the organization sales 100000 commodity at wholesale rate of 8 per

bottle. After 3 years until 6th year there is increment in the sales of the products which is 25000

per year at the same wholesale rate. Increase in sales is helpful for raising revenue, staff

7 | P a g e

4. Cloud funding: It is another alternative that is available to the firm and under this

through internet firm can raise 7 million amounts from different individuals. Main

advantage of cloud funding is that it is very easy approach through which in small

proportion large amount of fund can be raised from the market. Main limitation is

that it is not necessary that firm will successfully raise entire required amount

through this source of finance. Thus, any company cannot solely depend on cloud

funding to meet its needs.

Suggested source of finance

Venture capital as a source of finance is suggested to the firm because it has already taken

heavy loan from the market. There is probability that firm if intend to raise fund through equity

offer, which might remain unsubscribed. Thus, fund will be raised from venture capital so that

sufficient amount of fund may be available on time at different stages of project.

The company can also fund the project with the combination of the above financing

alternative. A good combination will require a part of equity and credit potential.

Short term financing alternatives: Short-term working capital needs or requirement of

finance to run the day to day errands:

1. Short-term loans: The Company can apply for short-term working capital loans

from commercial banks to run the day-to-day activities of the production in

application of a new plan of product line expansion. It is mandatory for the

managers to ensure that they will be able to pay short-term loan on time

(Caglayan and Demir, 2014). Default in repayment can tarnish firm image among

customers.

2. Loan from friends: Firm can take loan from business friends to meet its short-

term financial needs. This source must be kept as alternative option in case bank

deny from giving short-term loan to firm.

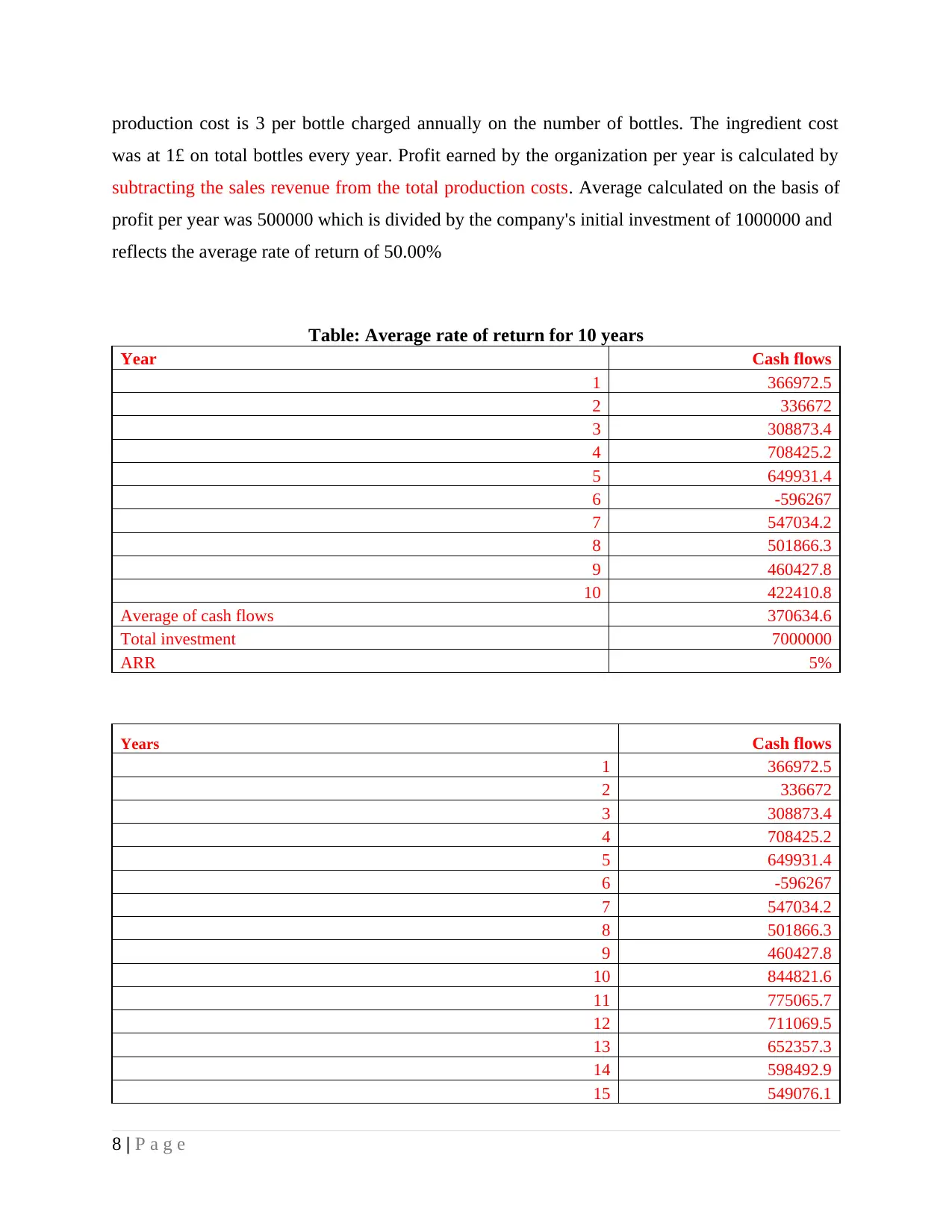

©Critical evaluation of financial worth

As we go through the New Life Brewery's statement. The 6 years of sales statement is

given in which up to 3 years the organization sales 100000 commodity at wholesale rate of 8 per

bottle. After 3 years until 6th year there is increment in the sales of the products which is 25000

per year at the same wholesale rate. Increase in sales is helpful for raising revenue, staff

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

production cost is 3 per bottle charged annually on the number of bottles. The ingredient cost

was at 1£ on total bottles every year. Profit earned by the organization per year is calculated by

subtracting the sales revenue from the total production costs. Average calculated on the basis of

profit per year was 500000 which is divided by the company's initial investment of 1000000 and

reflects the average rate of return of 50.00%

Table: Average rate of return for 10 years

Year Cash flows

1 366972.5

2 336672

3 308873.4

4 708425.2

5 649931.4

6 -596267

7 547034.2

8 501866.3

9 460427.8

10 422410.8

Average of cash flows 370634.6

Total investment 7000000

ARR 5%

Years Cash flows

1 366972.5

2 336672

3 308873.4

4 708425.2

5 649931.4

6 -596267

7 547034.2

8 501866.3

9 460427.8

10 844821.6

11 775065.7

12 711069.5

13 652357.3

14 598492.9

15 549076.1

8 | P a g e

was at 1£ on total bottles every year. Profit earned by the organization per year is calculated by

subtracting the sales revenue from the total production costs. Average calculated on the basis of

profit per year was 500000 which is divided by the company's initial investment of 1000000 and

reflects the average rate of return of 50.00%

Table: Average rate of return for 10 years

Year Cash flows

1 366972.5

2 336672

3 308873.4

4 708425.2

5 649931.4

6 -596267

7 547034.2

8 501866.3

9 460427.8

10 422410.8

Average of cash flows 370634.6

Total investment 7000000

ARR 5%

Years Cash flows

1 366972.5

2 336672

3 308873.4

4 708425.2

5 649931.4

6 -596267

7 547034.2

8 501866.3

9 460427.8

10 844821.6

11 775065.7

12 711069.5

13 652357.3

14 598492.9

15 549076.1

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

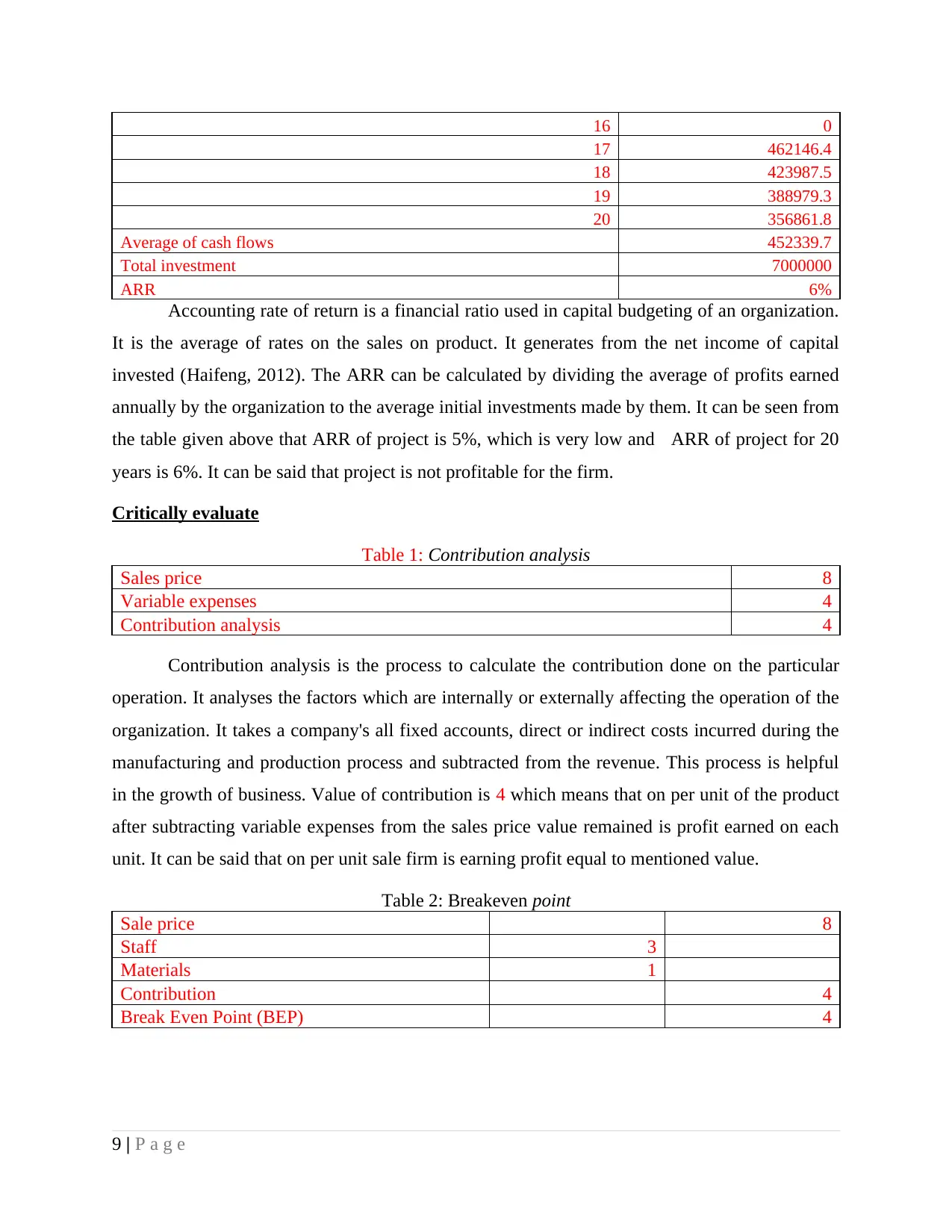

16 0

17 462146.4

18 423987.5

19 388979.3

20 356861.8

Average of cash flows 452339.7

Total investment 7000000

ARR 6%

Accounting rate of return is a financial ratio used in capital budgeting of an organization.

It is the average of rates on the sales on product. It generates from the net income of capital

invested (Haifeng, 2012). The ARR can be calculated by dividing the average of profits earned

annually by the organization to the average initial investments made by them. It can be seen from

the table given above that ARR of project is 5%, which is very low and ARR of project for 20

years is 6%. It can be said that project is not profitable for the firm.

Critically evaluate

Table 1: Contribution analysis

Sales price 8

Variable expenses 4

Contribution analysis 4

Contribution analysis is the process to calculate the contribution done on the particular

operation. It analyses the factors which are internally or externally affecting the operation of the

organization. It takes a company's all fixed accounts, direct or indirect costs incurred during the

manufacturing and production process and subtracted from the revenue. This process is helpful

in the growth of business. Value of contribution is 4 which means that on per unit of the product

after subtracting variable expenses from the sales price value remained is profit earned on each

unit. It can be said that on per unit sale firm is earning profit equal to mentioned value.

Table 2: Breakeven point

Sale price 8

Staff 3

Materials 1

Contribution 4

Break Even Point (BEP) 4

9 | P a g e

17 462146.4

18 423987.5

19 388979.3

20 356861.8

Average of cash flows 452339.7

Total investment 7000000

ARR 6%

Accounting rate of return is a financial ratio used in capital budgeting of an organization.

It is the average of rates on the sales on product. It generates from the net income of capital

invested (Haifeng, 2012). The ARR can be calculated by dividing the average of profits earned

annually by the organization to the average initial investments made by them. It can be seen from

the table given above that ARR of project is 5%, which is very low and ARR of project for 20

years is 6%. It can be said that project is not profitable for the firm.

Critically evaluate

Table 1: Contribution analysis

Sales price 8

Variable expenses 4

Contribution analysis 4

Contribution analysis is the process to calculate the contribution done on the particular

operation. It analyses the factors which are internally or externally affecting the operation of the

organization. It takes a company's all fixed accounts, direct or indirect costs incurred during the

manufacturing and production process and subtracted from the revenue. This process is helpful

in the growth of business. Value of contribution is 4 which means that on per unit of the product

after subtracting variable expenses from the sales price value remained is profit earned on each

unit. It can be said that on per unit sale firm is earning profit equal to mentioned value.

Table 2: Breakeven point

Sale price 8

Staff 3

Materials 1

Contribution 4

Break Even Point (BEP) 4

9 | P a g e

Breakeven point is the point at which the organization is balanced at no profit or no loss. The

organization has earned the equal amount as it has spent over the manufacturing process. The

production cost is same as revenue occurred. It can be seen from the table given above that

breakeven point value is 4 which reflect that firm needs to sale very less quantity of goods in the

market in order to cover fixed cost of business.

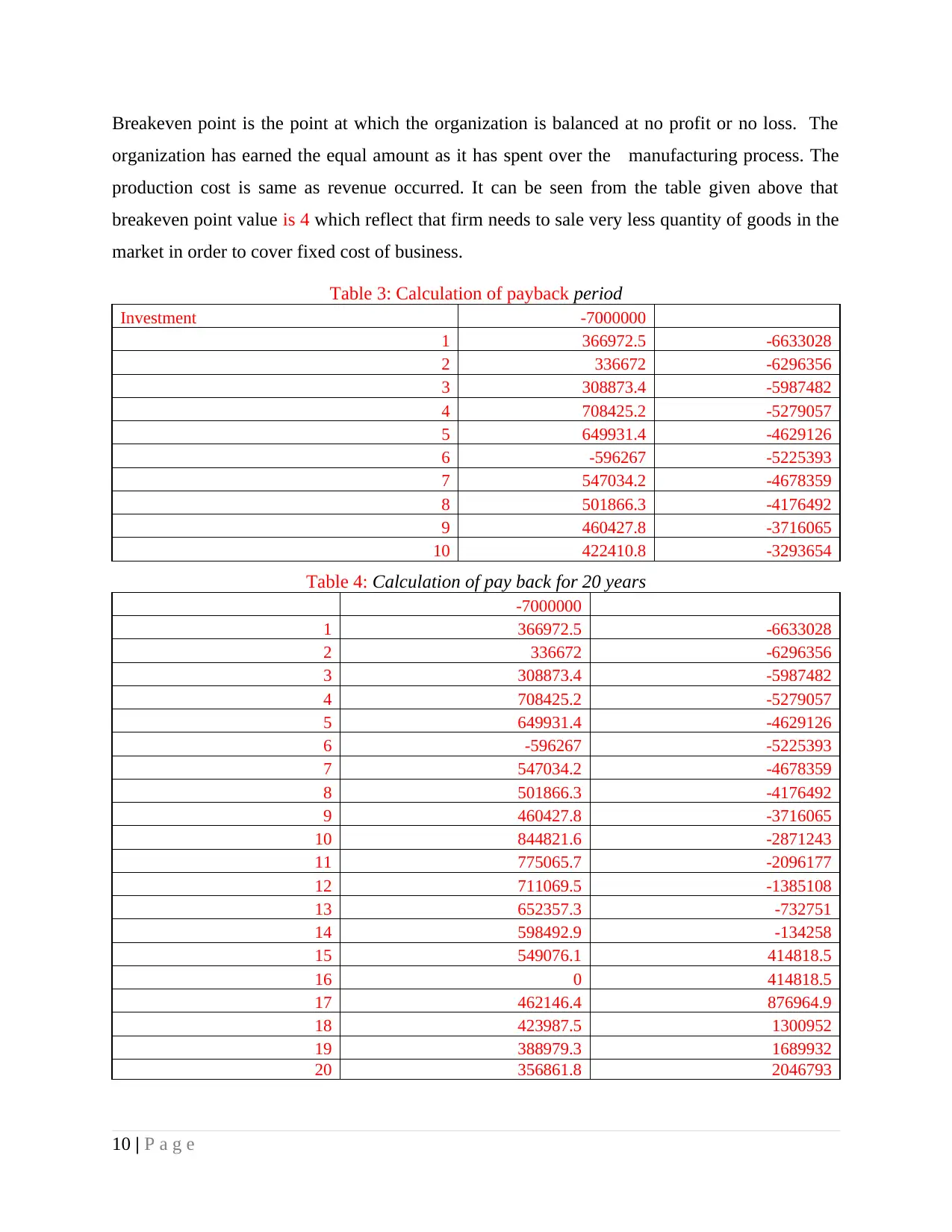

Table 3: Calculation of payback period

Investment -7000000

1 366972.5 -6633028

2 336672 -6296356

3 308873.4 -5987482

4 708425.2 -5279057

5 649931.4 -4629126

6 -596267 -5225393

7 547034.2 -4678359

8 501866.3 -4176492

9 460427.8 -3716065

10 422410.8 -3293654

Table 4: Calculation of pay back for 20 years

-7000000

1 366972.5 -6633028

2 336672 -6296356

3 308873.4 -5987482

4 708425.2 -5279057

5 649931.4 -4629126

6 -596267 -5225393

7 547034.2 -4678359

8 501866.3 -4176492

9 460427.8 -3716065

10 844821.6 -2871243

11 775065.7 -2096177

12 711069.5 -1385108

13 652357.3 -732751

14 598492.9 -134258

15 549076.1 414818.5

16 0 414818.5

17 462146.4 876964.9

18 423987.5 1300952

19 388979.3 1689932

20 356861.8 2046793

10 | P a g e

organization has earned the equal amount as it has spent over the manufacturing process. The

production cost is same as revenue occurred. It can be seen from the table given above that

breakeven point value is 4 which reflect that firm needs to sale very less quantity of goods in the

market in order to cover fixed cost of business.

Table 3: Calculation of payback period

Investment -7000000

1 366972.5 -6633028

2 336672 -6296356

3 308873.4 -5987482

4 708425.2 -5279057

5 649931.4 -4629126

6 -596267 -5225393

7 547034.2 -4678359

8 501866.3 -4176492

9 460427.8 -3716065

10 422410.8 -3293654

Table 4: Calculation of pay back for 20 years

-7000000

1 366972.5 -6633028

2 336672 -6296356

3 308873.4 -5987482

4 708425.2 -5279057

5 649931.4 -4629126

6 -596267 -5225393

7 547034.2 -4678359

8 501866.3 -4176492

9 460427.8 -3716065

10 844821.6 -2871243

11 775065.7 -2096177

12 711069.5 -1385108

13 652357.3 -732751

14 598492.9 -134258

15 549076.1 414818.5

16 0 414818.5

17 462146.4 876964.9

18 423987.5 1300952

19 388979.3 1689932

20 356861.8 2046793

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.