Corporate Finance Report: Newham Plc Funding and Expenditure

VerifiedAdded on 2020/06/05

|13

|4273

|33

Report

AI Summary

This report delves into the realm of corporate finance, specifically examining the case of Newham Plc and its funding strategies. It begins with an introduction to corporate finance, emphasizing the importance of maximizing shareholder value. The report then explores the Modigliani and Miller (MM) approach, discussing how a company's overall cost of capital can be reduced. It provides an analysis of the company's capital structure, including ordinary shares, preference shares, and debentures, and calculates the gearing ratio. The report further investigates the factors influencing the choice between preference shares and debentures as funding sources, including risk, return, and payment conditions. Additionally, it addresses factors impacting the amount of debentures a company might issue, such as trading on equity, expected cash flows, and market conditions. Finally, the report touches upon the evaluation, monitoring, and control of capital expenditure and concludes with the evaluation of investment appraisal methods.

CORPORATE FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

1A Explain Modigliani and Miler approach and its arguments that how company's overall cost

can be reduced.............................................................................................................................1

1B Factors need to be considered for preference shares ............................................................3

1C Factors influencing the additional debenture amount...........................................................4

2A Evaluate, monitor and control the capital expenditure.........................................................5

2B Explain mentioned Investment Appraisal Method ...............................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

1A Explain Modigliani and Miler approach and its arguments that how company's overall cost

can be reduced.............................................................................................................................1

1B Factors need to be considered for preference shares ............................................................3

1C Factors influencing the additional debenture amount...........................................................4

2A Evaluate, monitor and control the capital expenditure.........................................................5

2B Explain mentioned Investment Appraisal Method ...............................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

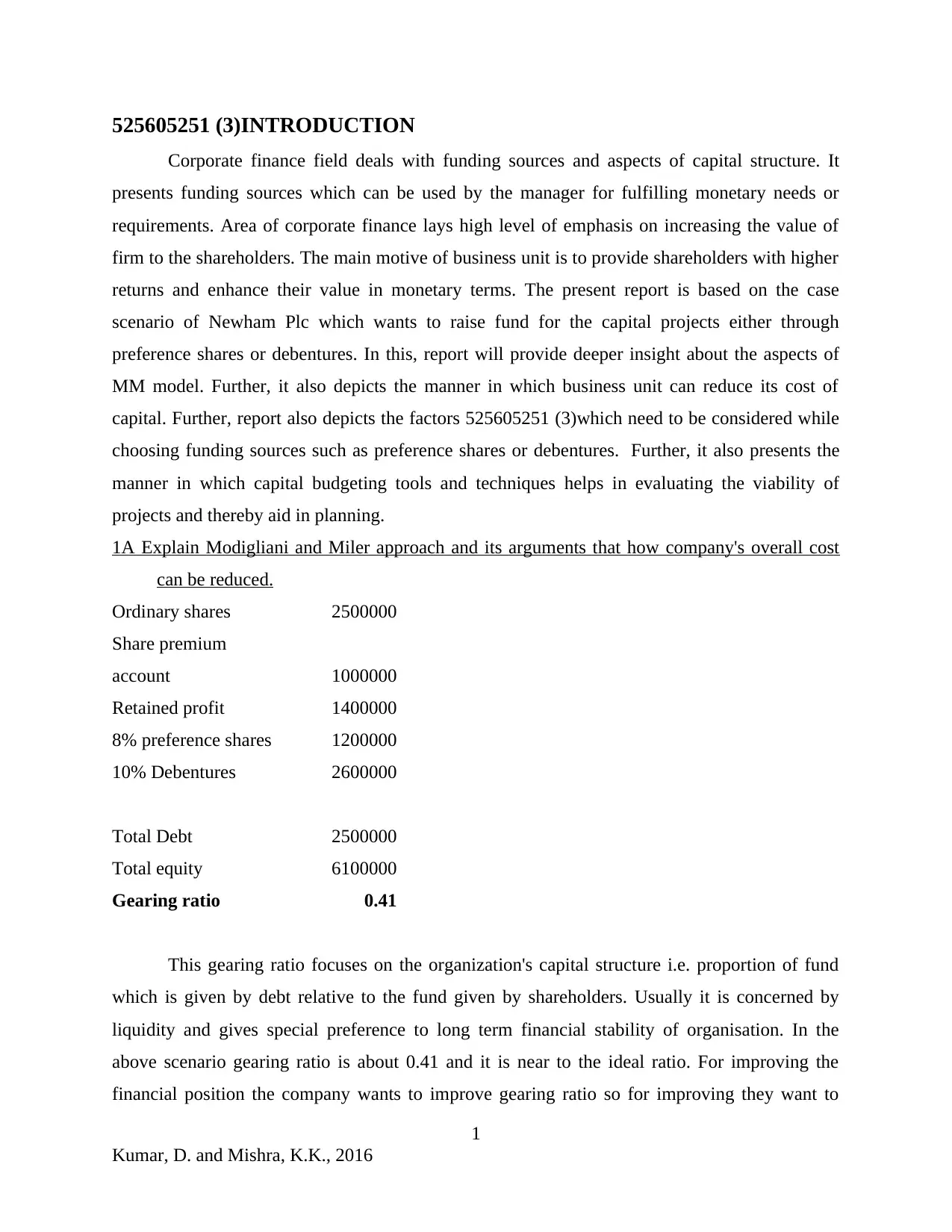

525605251 (3)INTRODUCTION

Corporate finance field deals with funding sources and aspects of capital structure. It

presents funding sources which can be used by the manager for fulfilling monetary needs or

requirements. Area of corporate finance lays high level of emphasis on increasing the value of

firm to the shareholders. The main motive of business unit is to provide shareholders with higher

returns and enhance their value in monetary terms. The present report is based on the case

scenario of Newham Plc which wants to raise fund for the capital projects either through

preference shares or debentures. In this, report will provide deeper insight about the aspects of

MM model. Further, it also depicts the manner in which business unit can reduce its cost of

capital. Further, report also depicts the factors 525605251 (3)which need to be considered while

choosing funding sources such as preference shares or debentures. Further, it also presents the

manner in which capital budgeting tools and techniques helps in evaluating the viability of

projects and thereby aid in planning.

1A Explain Modigliani and Miler approach and its arguments that how company's overall cost

can be reduced.

Ordinary shares 2500000

Share premium

account 1000000

Retained profit 1400000

8% preference shares 1200000

10% Debentures 2600000

Total Debt 2500000

Total equity 6100000

Gearing ratio 0.41

This gearing ratio focuses on the organization's capital structure i.e. proportion of fund

which is given by debt relative to the fund given by shareholders. Usually it is concerned by

liquidity and gives special preference to long term financial stability of organisation. In the

above scenario gearing ratio is about 0.41 and it is near to the ideal ratio. For improving the

financial position the company wants to improve gearing ratio so for improving they want to

1

Kumar, D. and Mishra, K.K., 2016

Corporate finance field deals with funding sources and aspects of capital structure. It

presents funding sources which can be used by the manager for fulfilling monetary needs or

requirements. Area of corporate finance lays high level of emphasis on increasing the value of

firm to the shareholders. The main motive of business unit is to provide shareholders with higher

returns and enhance their value in monetary terms. The present report is based on the case

scenario of Newham Plc which wants to raise fund for the capital projects either through

preference shares or debentures. In this, report will provide deeper insight about the aspects of

MM model. Further, it also depicts the manner in which business unit can reduce its cost of

capital. Further, report also depicts the factors 525605251 (3)which need to be considered while

choosing funding sources such as preference shares or debentures. Further, it also presents the

manner in which capital budgeting tools and techniques helps in evaluating the viability of

projects and thereby aid in planning.

1A Explain Modigliani and Miler approach and its arguments that how company's overall cost

can be reduced.

Ordinary shares 2500000

Share premium

account 1000000

Retained profit 1400000

8% preference shares 1200000

10% Debentures 2600000

Total Debt 2500000

Total equity 6100000

Gearing ratio 0.41

This gearing ratio focuses on the organization's capital structure i.e. proportion of fund

which is given by debt relative to the fund given by shareholders. Usually it is concerned by

liquidity and gives special preference to long term financial stability of organisation. In the

above scenario gearing ratio is about 0.41 and it is near to the ideal ratio. For improving the

financial position the company wants to improve gearing ratio so for improving they want to

1

Kumar, D. and Mishra, K.K., 2016

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

issue more debentures or to increase the WACC but along with this it will give impact to the

company's cost of capital. Companies always tries to reduce cost of capital. Usually debt is less

cheap than equity because all the creditors are paid before shareholders. If company wants to

issue preference shares but this is major component of overall cost of capital. The coupon rate on

the debenture is the basis for calculation of cost of debenture. The cost of debt capital increases,

the net proceeds from issue of debts decreases because investors

Ordinary shares 2500000

Share premium

account 1000000

Retained profit 1400000

8% preference shares 1200000

10% Debentures 2600000

Total Debt 2500000

Total equity 6100000

Gearing ratio 0.41

This gearing ratio focuses on the organization's capital structure i.e. proportion of fund

which is given by debt relative to the fund given by shareholders. Usually it is concerned by

liquidity and gives special preference to long term financial stability of organisation. In the

above scenario gearing ratio is about 0.41 and it is near to the ideal ratio. For improving the

financial position the company wants to improve gearing ratio so for improving they want to

issue more debentures or to increase the WACC but along with this it will give impact to the

company's cost of capital. Companies always tries to reduce cost of capital (Bennouna and et.al.,

2010). Usually debt is less cheap than equity because all the creditors are paid before

shareholders. If company wants to issue preference shares but this is major component of overall

cost of capital. The coupon rate on the debenture is the basis for calculation of cost of debenture.

The cost of debt capital increases, the net proceeds from issue of debts decreases because

investors have paid small amount and they will get the fixed interest payment. So this will

directly impact the cost of capital. Have paid small amount and they will get the fixed interest

payment. So this will directly impact the cost of capital.

2

Kumar, D. and Mishra, K.K., 2016

company's cost of capital. Companies always tries to reduce cost of capital. Usually debt is less

cheap than equity because all the creditors are paid before shareholders. If company wants to

issue preference shares but this is major component of overall cost of capital. The coupon rate on

the debenture is the basis for calculation of cost of debenture. The cost of debt capital increases,

the net proceeds from issue of debts decreases because investors

Ordinary shares 2500000

Share premium

account 1000000

Retained profit 1400000

8% preference shares 1200000

10% Debentures 2600000

Total Debt 2500000

Total equity 6100000

Gearing ratio 0.41

This gearing ratio focuses on the organization's capital structure i.e. proportion of fund

which is given by debt relative to the fund given by shareholders. Usually it is concerned by

liquidity and gives special preference to long term financial stability of organisation. In the

above scenario gearing ratio is about 0.41 and it is near to the ideal ratio. For improving the

financial position the company wants to improve gearing ratio so for improving they want to

issue more debentures or to increase the WACC but along with this it will give impact to the

company's cost of capital. Companies always tries to reduce cost of capital (Bennouna and et.al.,

2010). Usually debt is less cheap than equity because all the creditors are paid before

shareholders. If company wants to issue preference shares but this is major component of overall

cost of capital. The coupon rate on the debenture is the basis for calculation of cost of debenture.

The cost of debt capital increases, the net proceeds from issue of debts decreases because

investors have paid small amount and they will get the fixed interest payment. So this will

directly impact the cost of capital. Have paid small amount and they will get the fixed interest

payment. So this will directly impact the cost of capital.

2

Kumar, D. and Mishra, K.K., 2016

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Modigliani and Miler approach gives the suggestion that valuation of firm has no relevant

relationship to the capital structure of company. This approach is similar to Net operating income

approach. It gives behavioural justification and operational justification for constant cost of

capital. But net operating income approach does gives operational justification for independence.

Rather, a firm has low debt component or it is leveraged highly. This approach gives the

resemblance of Net operating income. Future growth affects the market value apart from risk

which is involved in investment. In this theory, Capital structure or finance decision of firm does

not link the valuation of the organization. If the prospect of the company has high growth, then

market value will be higher and it tends to high stock price (Chen and et.al., 2012). If attractive

growth has not been justified in a firm then market value would not be good of that same firm.

The Modigliani and Miler approach arguments about the company's overall cost of capital can be

reduced has been justified with these propositions: The total market value of firm and cost of

capital of firm are independent of its structure of capital. The capitalisation rate of equity stream

and cost of capital are equal to each other and market has been determined by capitalizing its

return which is expected at a proper rate of discount.

The expected yield on share and capitalisation rate for pure equity stream are usually

equal with the premium of financial risk which gives difference between Kd and K, in this Kd

refers to yield on debt and K is capitalisation rate. The point at which investor decide for

investing is always capitalisation rate which is purely not dependent and even unaffected by

securities which are invested. Preference shares are those shares which are owned by people who

have first right to receive the company's profit (Cheng and et.al., 2011). A share refers to a part

of capital which is issued by a company. Preference shareholder are the effectively owners.

Preference shareholders received profit in the form of dividends. Preference shares holders not

carry any voting power. In preference share there is fixed amount of dividend is given to the

shareholder.

1B Factors need to be considered for preference shares

Debenture is a long-term fund which is collected from public. In addition, it is a debt

instruments that shows a loan to the company. Debenture is important source of a finance which

is to raising the funds available to the company. In this, the company gives an interest at a

specified rate.

There are some factors which are considered to select between preference share and debenture:

3

Kumar, D. and Mishra, K.K., 2016

relationship to the capital structure of company. This approach is similar to Net operating income

approach. It gives behavioural justification and operational justification for constant cost of

capital. But net operating income approach does gives operational justification for independence.

Rather, a firm has low debt component or it is leveraged highly. This approach gives the

resemblance of Net operating income. Future growth affects the market value apart from risk

which is involved in investment. In this theory, Capital structure or finance decision of firm does

not link the valuation of the organization. If the prospect of the company has high growth, then

market value will be higher and it tends to high stock price (Chen and et.al., 2012). If attractive

growth has not been justified in a firm then market value would not be good of that same firm.

The Modigliani and Miler approach arguments about the company's overall cost of capital can be

reduced has been justified with these propositions: The total market value of firm and cost of

capital of firm are independent of its structure of capital. The capitalisation rate of equity stream

and cost of capital are equal to each other and market has been determined by capitalizing its

return which is expected at a proper rate of discount.

The expected yield on share and capitalisation rate for pure equity stream are usually

equal with the premium of financial risk which gives difference between Kd and K, in this Kd

refers to yield on debt and K is capitalisation rate. The point at which investor decide for

investing is always capitalisation rate which is purely not dependent and even unaffected by

securities which are invested. Preference shares are those shares which are owned by people who

have first right to receive the company's profit (Cheng and et.al., 2011). A share refers to a part

of capital which is issued by a company. Preference shareholder are the effectively owners.

Preference shareholders received profit in the form of dividends. Preference shares holders not

carry any voting power. In preference share there is fixed amount of dividend is given to the

shareholder.

1B Factors need to be considered for preference shares

Debenture is a long-term fund which is collected from public. In addition, it is a debt

instruments that shows a loan to the company. Debenture is important source of a finance which

is to raising the funds available to the company. In this, the company gives an interest at a

specified rate.

There are some factors which are considered to select between preference share and debenture:

3

Kumar, D. and Mishra, K.K., 2016

Debentures are a debt of a company and the debenture holders are creditor of the

company. Whereas preference share is the part of the company capital and their holders

are owner of the company.

Rate of return are fixed in debenture at the beginning of issuing the debentures. And in

preference share dividend rate on shares are fully depends on how much profit obtained

by the company (Kumar, D. and Mishra, K.K., 2016). Another factor is payment

condition. Shareholders are paid after the debenture holders paid interest.

If a company does not earn profit so the shareholders don't get dividend. Moreover, the

debenture holders get interest compulsorily if the company makes profit or not.

If any company wind up the preference shareholders lose a part or full of their capital.

And debenture holders get all their investment. Shareholders have right to attend

meetings and vote at meetings but debenture holders do not have any right to vote in the

meetings (Dhesi and Ausloos, 2016).

The main factor is risk. If any person invested in preference share it is considered risky.

And in debentures considered as a good investment because in these holders has right to

get investment back.

Debentures are very secured investment because holders have a charge on assets of the

company. And the share holders have no security for investment. For long – term finance

director should consider debenture because its secured, rate of return is fixed and if the

company winding up their business so the holder get back their investment. However, the

only drawback is that debenture holder having no voting rights in any company meetings.

1C Factors influencing the additional debenture amount

The capital structure has been influenced by many factors which are as follows:

Trading on Equity – the ownership of the company can be denoted by the word equity.

If trading on equity has been practised then it means gaining advantage of equity share capital to

the borrowed funds but it is on reasonable basis(Kumar, D. and Mishra, K.K., 2016). It replicated

the additional margin that is earned from equity share because of amount which is raised by

issuing securities such as debenture or preference shares. If the borrowed capital's interest rate

and dividend on preference capital both are lower than equity shareholders will gain advantage in

form of some additional margin or profit. By combining long-term loans or debentures and

preference shares and there return can be maximized (Shen, Firth and Poon, 2016). The

4

Kumar, D. and Mishra, K.K., 2016

company. Whereas preference share is the part of the company capital and their holders

are owner of the company.

Rate of return are fixed in debenture at the beginning of issuing the debentures. And in

preference share dividend rate on shares are fully depends on how much profit obtained

by the company (Kumar, D. and Mishra, K.K., 2016). Another factor is payment

condition. Shareholders are paid after the debenture holders paid interest.

If a company does not earn profit so the shareholders don't get dividend. Moreover, the

debenture holders get interest compulsorily if the company makes profit or not.

If any company wind up the preference shareholders lose a part or full of their capital.

And debenture holders get all their investment. Shareholders have right to attend

meetings and vote at meetings but debenture holders do not have any right to vote in the

meetings (Dhesi and Ausloos, 2016).

The main factor is risk. If any person invested in preference share it is considered risky.

And in debentures considered as a good investment because in these holders has right to

get investment back.

Debentures are very secured investment because holders have a charge on assets of the

company. And the share holders have no security for investment. For long – term finance

director should consider debenture because its secured, rate of return is fixed and if the

company winding up their business so the holder get back their investment. However, the

only drawback is that debenture holder having no voting rights in any company meetings.

1C Factors influencing the additional debenture amount

The capital structure has been influenced by many factors which are as follows:

Trading on Equity – the ownership of the company can be denoted by the word equity.

If trading on equity has been practised then it means gaining advantage of equity share capital to

the borrowed funds but it is on reasonable basis(Kumar, D. and Mishra, K.K., 2016). It replicated

the additional margin that is earned from equity share because of amount which is raised by

issuing securities such as debenture or preference shares. If the borrowed capital's interest rate

and dividend on preference capital both are lower than equity shareholders will gain advantage in

form of some additional margin or profit. By combining long-term loans or debentures and

preference shares and there return can be maximized (Shen, Firth and Poon, 2016). The

4

Kumar, D. and Mishra, K.K., 2016

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

possibilities of trading of equity are: Earnings of the company are stable, payment of interest on

debentures should be regularly paid, and earning rate of company should be higher than the

interest rate on debentures and preference shares. The last possibility can be that company’s

assets should be sufficient which can be used for raising borrowed fund's security. The capital

structure has been influenced by many factors which are as follows:

Expected cash flows – Debentures and preference shares both are to be refunded after

their maturity. The cash flows which are expected over the years should be able to meet interest

liability every year which is on debentures and maturity amount is also returned in the end in the

context of debentures. Companies which are going to have irregular cash flow in future then

debentures are not suitable for them.

Sales turnover – The ability of company to pay interest on debentures is being enhanced

by sales turnover stability. The company can use debt capital more but the condition is if sales is

rising then it will gain the position of paying interest but in vice versa condition it is not

suggested to company for employing additional capital.

Company's authority – It has been given to the Board of Directors which is selected by

equity shareholders (Kumar and Mishra, 2016). If Board of Directors and shareholders want to

retain the authority and control of the company then they should stop issuing equity shares to the

public so in this situation they can raise fund by issuing preference shares and debentures.

Duration of Financing – If the investment company which is permanent and has the

requirement of funds then the preference is given to equity shares but funds are required for

expanding organization and there are possibilities for redeemable of funds in the lifetime of

organization then preference shares and debentures are issued.

Floating capital – Usually the expense for issuing debentures and preference share of

well-known organization is low. Floatation cost should be considered while issuing shares and

debentures, advertisement etc.

Market Conditions – Debentures and preference shares always gives the fixed return

whatever be marketed during issuance during low market conditions or high market conditions.

Investors Types – Equity shares are always issued to the people who can afford risk for

investment in the organization and preference shares and debentures are issued in vice versa

situation.

5

Kumar, D. and Mishra, K.K., 2016

debentures should be regularly paid, and earning rate of company should be higher than the

interest rate on debentures and preference shares. The last possibility can be that company’s

assets should be sufficient which can be used for raising borrowed fund's security. The capital

structure has been influenced by many factors which are as follows:

Expected cash flows – Debentures and preference shares both are to be refunded after

their maturity. The cash flows which are expected over the years should be able to meet interest

liability every year which is on debentures and maturity amount is also returned in the end in the

context of debentures. Companies which are going to have irregular cash flow in future then

debentures are not suitable for them.

Sales turnover – The ability of company to pay interest on debentures is being enhanced

by sales turnover stability. The company can use debt capital more but the condition is if sales is

rising then it will gain the position of paying interest but in vice versa condition it is not

suggested to company for employing additional capital.

Company's authority – It has been given to the Board of Directors which is selected by

equity shareholders (Kumar and Mishra, 2016). If Board of Directors and shareholders want to

retain the authority and control of the company then they should stop issuing equity shares to the

public so in this situation they can raise fund by issuing preference shares and debentures.

Duration of Financing – If the investment company which is permanent and has the

requirement of funds then the preference is given to equity shares but funds are required for

expanding organization and there are possibilities for redeemable of funds in the lifetime of

organization then preference shares and debentures are issued.

Floating capital – Usually the expense for issuing debentures and preference share of

well-known organization is low. Floatation cost should be considered while issuing shares and

debentures, advertisement etc.

Market Conditions – Debentures and preference shares always gives the fixed return

whatever be marketed during issuance during low market conditions or high market conditions.

Investors Types – Equity shares are always issued to the people who can afford risk for

investment in the organization and preference shares and debentures are issued in vice versa

situation.

5

Kumar, D. and Mishra, K.K., 2016

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Legal Requirement – Statutory requirements gives high influence to the structure capital

of organization.

2A Evaluate, monitor and control the capital expenditure

Various methods for evaluating monitor and control the capital expenditure decisions are-

Discounted payback period: This method has come up for developing the disadvantages

of non-discounted payback period. In this, normal cash flows are replaced by discounted cash

flows for calculating payback period. In this scenario, it is the perfect time for recovering the

cost which was invested in the initial phase of project via discounted inflows. This developed

method also has disadvantage but on the other side advantages. In the series of advantages, it is

easy to calculate and even to understand. It also considers time value of money. This method also

helps in comparison of projects and in selecting profitable project among them and can give

negative effect (Dellavigna and Pollet, 2013). On the other hand its disadvantages are, it does not

consider the cash which is coming in the business after payback period and appropriate rate for

discounting is the biggest problem of payback period.

Net present Value: This If the Net present value is giving positive outcome then it is

accepted but if it is negative then it is rejected and while comparing two projects, one who is

giving highest NPV is given the highest preference (Luu, Pham and Pham, 2016). There are also

pros and cons of Net Present Value method. In the pros side, time value of money is considered

and entire series of cash flows is being analysed. Under NPV, comparison is more preferable and

easy (Mbabazize and Daniel, 2014). On the cons side, as compared to traditional method it is

difficult to calculate and to interpret. Discount rate selection is a problem of NPV.

Internal Rate of Return – This method also considers time value of money but in

Internal rate of Return method stipulated rate of interest is ignored. Yield on investment is

another name of IRR. Internal rate of return is the discounting rate which equates present value

of cash outflow and inflow of the project. Net present value becomes zero under Internal rate of

return. The certain rules for accepting and rejecting are as follows: If IRR is more than cost of

capital then it is accepted but when cost of capital is more than IRR then the project is rejected

(Kumar and Mishra, 2016). Its disadvantages are, it has lengthy and difficult equations, multiple

IRR creates confusion and sometimes projects which are giving highest IRR are not always

profitable in all scenarios.

6

Kumar, D. and Mishra, K.K., 2016

of organization.

2A Evaluate, monitor and control the capital expenditure

Various methods for evaluating monitor and control the capital expenditure decisions are-

Discounted payback period: This method has come up for developing the disadvantages

of non-discounted payback period. In this, normal cash flows are replaced by discounted cash

flows for calculating payback period. In this scenario, it is the perfect time for recovering the

cost which was invested in the initial phase of project via discounted inflows. This developed

method also has disadvantage but on the other side advantages. In the series of advantages, it is

easy to calculate and even to understand. It also considers time value of money. This method also

helps in comparison of projects and in selecting profitable project among them and can give

negative effect (Dellavigna and Pollet, 2013). On the other hand its disadvantages are, it does not

consider the cash which is coming in the business after payback period and appropriate rate for

discounting is the biggest problem of payback period.

Net present Value: This If the Net present value is giving positive outcome then it is

accepted but if it is negative then it is rejected and while comparing two projects, one who is

giving highest NPV is given the highest preference (Luu, Pham and Pham, 2016). There are also

pros and cons of Net Present Value method. In the pros side, time value of money is considered

and entire series of cash flows is being analysed. Under NPV, comparison is more preferable and

easy (Mbabazize and Daniel, 2014). On the cons side, as compared to traditional method it is

difficult to calculate and to interpret. Discount rate selection is a problem of NPV.

Internal Rate of Return – This method also considers time value of money but in

Internal rate of Return method stipulated rate of interest is ignored. Yield on investment is

another name of IRR. Internal rate of return is the discounting rate which equates present value

of cash outflow and inflow of the project. Net present value becomes zero under Internal rate of

return. The certain rules for accepting and rejecting are as follows: If IRR is more than cost of

capital then it is accepted but when cost of capital is more than IRR then the project is rejected

(Kumar and Mishra, 2016). Its disadvantages are, it has lengthy and difficult equations, multiple

IRR creates confusion and sometimes projects which are giving highest IRR are not always

profitable in all scenarios.

6

Kumar, D. and Mishra, K.K., 2016

Modified Internal Rate of Return – This method has been created for overcoming with

the limitations of internal rate of return. The assumption of IRR says that cash flows which are

positive of any project are reinvested but this is not realistic assumption because if it will be

reinvested at rate which is closer to cost of capital. If there is more than one IRR, or it has

alternative negative and positive cash flow which will replicate confusion. Under modified

internal rate of return all cDhesi, G. and Ausloos, M., 2016ash flows are brought to the specific

discount rate, usually the cost of capital (Pozzi and et.al., 2015). It equates compounded value of

cash outflows to the terminalDhesi, G. and Ausloos, M., 2016 value of cash inflows. It offers

advantages and disadvantages both like in advantage it considers time value of money and cash

flows over entire life of any of the project. It gives single rate and helps in solving the confusion

and disadvantages are same to the Internal rate of Return method.

Profitability Index : Profitability Index is also considered as Benefit Cost ratio. It is the

ratio of future inflow's present value and outflows of a project. In investment decision it indicates

as relative measure. The rules for monitoring that project is accepted or rejected for profitability

index is, when Profitability Index is more than 1, than it is accepted but when 1 is more than

profitability Index ratio than it is rejected. In advantages, it also considers Time value of money

and easy to calculate as compared to IRR and MIRR. It is also better for selecting the project in

comparison as compared to NPV. It also has some minor disadvantages such as complexity in

calculations and discounting rate selection is a major problem method is the most used and

common method for calculation of the capital expenditure and takes decision using cash flow

which is discounted.

In this, rate of interest and cost of capital are used for discounting the cash flow. The

difference between sum of present value of cash flow and initial investment gives Net present

value. If the Net present value is giving positive outcome then it is accepted but if it is negative

then it is rejected and while comparing two pDhesi, G. and Ausloos, M., 2016rojects, one who is

giving highest NPV is given the highest preference. There are also pros and cons of Net Present

Value method. In the pros side, time value of money is considered and entire series of cash flows

is being analysed. Under NPV, comparison is more preferable and easy. On the cons side, as

compared to traditional method it is difficult to calculate and to interpret. Discount rate selection

is a problem of NPV.

7

Kumar, D. and Mishra, K.K., 2016

the limitations of internal rate of return. The assumption of IRR says that cash flows which are

positive of any project are reinvested but this is not realistic assumption because if it will be

reinvested at rate which is closer to cost of capital. If there is more than one IRR, or it has

alternative negative and positive cash flow which will replicate confusion. Under modified

internal rate of return all cDhesi, G. and Ausloos, M., 2016ash flows are brought to the specific

discount rate, usually the cost of capital (Pozzi and et.al., 2015). It equates compounded value of

cash outflows to the terminalDhesi, G. and Ausloos, M., 2016 value of cash inflows. It offers

advantages and disadvantages both like in advantage it considers time value of money and cash

flows over entire life of any of the project. It gives single rate and helps in solving the confusion

and disadvantages are same to the Internal rate of Return method.

Profitability Index : Profitability Index is also considered as Benefit Cost ratio. It is the

ratio of future inflow's present value and outflows of a project. In investment decision it indicates

as relative measure. The rules for monitoring that project is accepted or rejected for profitability

index is, when Profitability Index is more than 1, than it is accepted but when 1 is more than

profitability Index ratio than it is rejected. In advantages, it also considers Time value of money

and easy to calculate as compared to IRR and MIRR. It is also better for selecting the project in

comparison as compared to NPV. It also has some minor disadvantages such as complexity in

calculations and discounting rate selection is a major problem method is the most used and

common method for calculation of the capital expenditure and takes decision using cash flow

which is discounted.

In this, rate of interest and cost of capital are used for discounting the cash flow. The

difference between sum of present value of cash flow and initial investment gives Net present

value. If the Net present value is giving positive outcome then it is accepted but if it is negative

then it is rejected and while comparing two pDhesi, G. and Ausloos, M., 2016rojects, one who is

giving highest NPV is given the highest preference. There are also pros and cons of Net Present

Value method. In the pros side, time value of money is considered and entire series of cash flows

is being analysed. Under NPV, comparison is more preferable and easy. On the cons side, as

compared to traditional method it is difficult to calculate and to interpret. Discount rate selection

is a problem of NPV.

7

Kumar, D. and Mishra, K.K., 2016

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

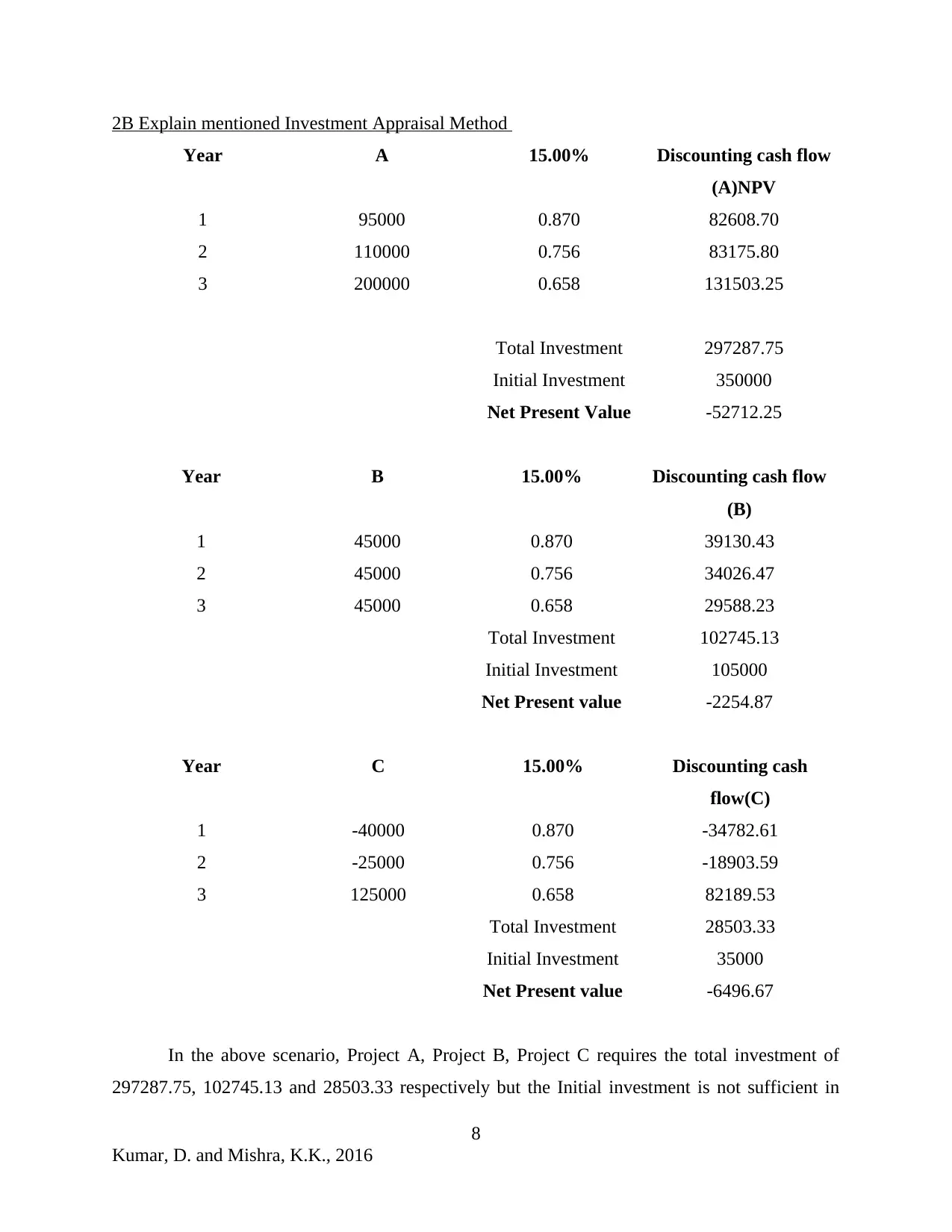

2B Explain mentioned Investment Appraisal Method

Year A 15.00% Discounting cash flow

(A)NPV

1 95000 0.870 82608.70

2 110000 0.756 83175.80

3 200000 0.658 131503.25

Total Investment 297287.75

Initial Investment 350000

Net Present Value -52712.25

Year B 15.00% Discounting cash flow

(B)

1 45000 0.870 39130.43

2 45000 0.756 34026.47

3 45000 0.658 29588.23

Total Investment 102745.13

Initial Investment 105000

Net Present value -2254.87

Year C 15.00% Discounting cash

flow(C)

1 -40000 0.870 -34782.61

2 -25000 0.756 -18903.59

3 125000 0.658 82189.53

Total Investment 28503.33

Initial Investment 35000

Net Present value -6496.67

In the above scenario, Project A, Project B, Project C requires the total investment of

297287.75, 102745.13 and 28503.33 respectively but the Initial investment is not sufficient in

8

Kumar, D. and Mishra, K.K., 2016

Year A 15.00% Discounting cash flow

(A)NPV

1 95000 0.870 82608.70

2 110000 0.756 83175.80

3 200000 0.658 131503.25

Total Investment 297287.75

Initial Investment 350000

Net Present Value -52712.25

Year B 15.00% Discounting cash flow

(B)

1 45000 0.870 39130.43

2 45000 0.756 34026.47

3 45000 0.658 29588.23

Total Investment 102745.13

Initial Investment 105000

Net Present value -2254.87

Year C 15.00% Discounting cash

flow(C)

1 -40000 0.870 -34782.61

2 -25000 0.756 -18903.59

3 125000 0.658 82189.53

Total Investment 28503.33

Initial Investment 35000

Net Present value -6496.67

In the above scenario, Project A, Project B, Project C requires the total investment of

297287.75, 102745.13 and 28503.33 respectively but the Initial investment is not sufficient in

8

Kumar, D. and Mishra, K.K., 2016

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

any of the project. Hence, the NPV of Project A, Project B and Project C is -52712.25, -2254.87

and -6496.67 and all are facing negative situation. All the projects are rejected on basis of Net

present value. The company should execute strategic investments and must be able to find better

projects for the company.

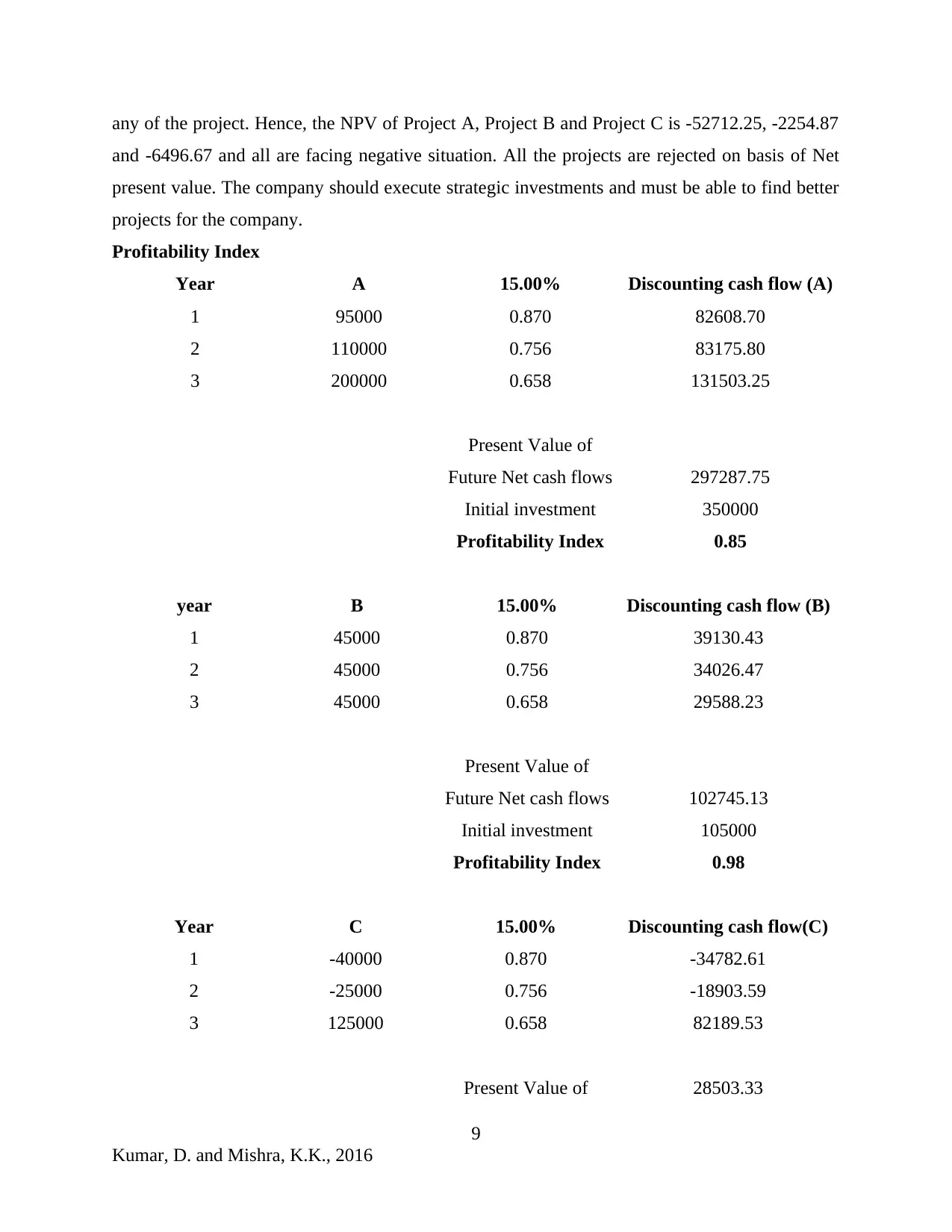

Profitability Index

Year A 15.00% Discounting cash flow (A)

1 95000 0.870 82608.70

2 110000 0.756 83175.80

3 200000 0.658 131503.25

Present Value of

Future Net cash flows 297287.75

Initial investment 350000

Profitability Index 0.85

year B 15.00% Discounting cash flow (B)

1 45000 0.870 39130.43

2 45000 0.756 34026.47

3 45000 0.658 29588.23

Present Value of

Future Net cash flows 102745.13

Initial investment 105000

Profitability Index 0.98

Year C 15.00% Discounting cash flow(C)

1 -40000 0.870 -34782.61

2 -25000 0.756 -18903.59

3 125000 0.658 82189.53

Present Value of 28503.33

9

Kumar, D. and Mishra, K.K., 2016

and -6496.67 and all are facing negative situation. All the projects are rejected on basis of Net

present value. The company should execute strategic investments and must be able to find better

projects for the company.

Profitability Index

Year A 15.00% Discounting cash flow (A)

1 95000 0.870 82608.70

2 110000 0.756 83175.80

3 200000 0.658 131503.25

Present Value of

Future Net cash flows 297287.75

Initial investment 350000

Profitability Index 0.85

year B 15.00% Discounting cash flow (B)

1 45000 0.870 39130.43

2 45000 0.756 34026.47

3 45000 0.658 29588.23

Present Value of

Future Net cash flows 102745.13

Initial investment 105000

Profitability Index 0.98

Year C 15.00% Discounting cash flow(C)

1 -40000 0.870 -34782.61

2 -25000 0.756 -18903.59

3 125000 0.658 82189.53

Present Value of 28503.33

9

Kumar, D. and Mishra, K.K., 2016

Future Net cash flows

Initial investment 35000

Profitability Index 0.81

In the above scenario, Project A, Project B, Project C requires the total investment of

297287.75, 102745.13 and 28503.33 respectively but the Initial investment is not sufficient in

any of the project. Hence, the Profitability Index of Project A, Project B and Project C is 0.85,

0.98 and 0.81 and all are facing negative situation. A ratio of 1 is the lowest acceptable measure

and below 1 are rejected. So in this scenario, all the projects are rejected on basis of Profitability

Index. The company should execute strategic investments and must be able to find better projects

for the company.

CONCLUSION

From the above report, it can be concluded that firm’s cost of equity increases along with

its debt-equity ratio. It can be seen in the report that gearing ratio increases when firm takes

resort of debentures for meeting financial needs. Along with this, it has been articulated that

while choosing debt source Newham plc should keep in mind coupon rate etc. On the other side,

in the case of preference shares dividend rate needs be considered. Along with this, it has been

articulated that investment appraisal techniques are highly significant which in turn helps in

evaluating the viability of projects. It can be summarized from the report that Newham plc

should make focus on finding profitable opportunities which in turn aid in company’s growth

and profit margin. Currently all the concerned three proposals are offering negative returns.

Thus, company should evaluate and undertake proposal or projects which offer positive results.

10

Kumar, D. and Mishra, K.K., 2016

Initial investment 35000

Profitability Index 0.81

In the above scenario, Project A, Project B, Project C requires the total investment of

297287.75, 102745.13 and 28503.33 respectively but the Initial investment is not sufficient in

any of the project. Hence, the Profitability Index of Project A, Project B and Project C is 0.85,

0.98 and 0.81 and all are facing negative situation. A ratio of 1 is the lowest acceptable measure

and below 1 are rejected. So in this scenario, all the projects are rejected on basis of Profitability

Index. The company should execute strategic investments and must be able to find better projects

for the company.

CONCLUSION

From the above report, it can be concluded that firm’s cost of equity increases along with

its debt-equity ratio. It can be seen in the report that gearing ratio increases when firm takes

resort of debentures for meeting financial needs. Along with this, it has been articulated that

while choosing debt source Newham plc should keep in mind coupon rate etc. On the other side,

in the case of preference shares dividend rate needs be considered. Along with this, it has been

articulated that investment appraisal techniques are highly significant which in turn helps in

evaluating the viability of projects. It can be summarized from the report that Newham plc

should make focus on finding profitable opportunities which in turn aid in company’s growth

and profit margin. Currently all the concerned three proposals are offering negative returns.

Thus, company should evaluate and undertake proposal or projects which offer positive results.

10

Kumar, D. and Mishra, K.K., 2016

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.