Financial Performance Analysis: Next plc and H&M Comparison Report

VerifiedAdded on 2020/01/21

|15

|3527

|134

Report

AI Summary

This report provides a detailed financial analysis of Next plc and Hennes & Mauritz (H&M), comparing their financial performance using various financial and non-financial ratios over a five-year period. The analysis includes profitability, liquidity, and efficiency ratios, presented graphically for easy comparison. The report also evaluates the companies' performance using non-financial metrics like EBITDA/employee and revenue/employee. Based on the analysis, the report recommends strategies for H&M to improve its financial position and suggests an investment decision for a CFO. Furthermore, it assesses the viability of two capital investment projects using investment appraisal techniques, including Net Cash Flow and depreciation calculations, and discusses the limitations of these techniques. Finally, the report provides a comprehensive overview of financial accounting and its role in understanding a business's position.

ACCOUNTING AND FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

ACCOUNTING AND FINANCE..................................................................................................1

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

1) Justification of the financial position and performance of the both the companies by using

various financial and non financial ratios...................................................................................1

2) Graphical presentation of ratios in the form of charts...........................................................3

3) Recommendation to H&M to improve financial performance and position..........................7

4) Limitation and drawbacks of using ratio analysis..................................................................8

TASK 2 Capital Investment Appraisal ...........................................................................................8

1) Analysing the viability of the project by using investment appraisal techniques...................8

Accounting rate of return (ARR)..............................................................................................11

2) Limitation of investment appraisals techniques...................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

ACCOUNTING AND FINANCE..................................................................................................1

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

1) Justification of the financial position and performance of the both the companies by using

various financial and non financial ratios...................................................................................1

2) Graphical presentation of ratios in the form of charts...........................................................3

3) Recommendation to H&M to improve financial performance and position..........................7

4) Limitation and drawbacks of using ratio analysis..................................................................8

TASK 2 Capital Investment Appraisal ...........................................................................................8

1) Analysing the viability of the project by using investment appraisal techniques...................8

Accounting rate of return (ARR)..............................................................................................11

2) Limitation of investment appraisals techniques...................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

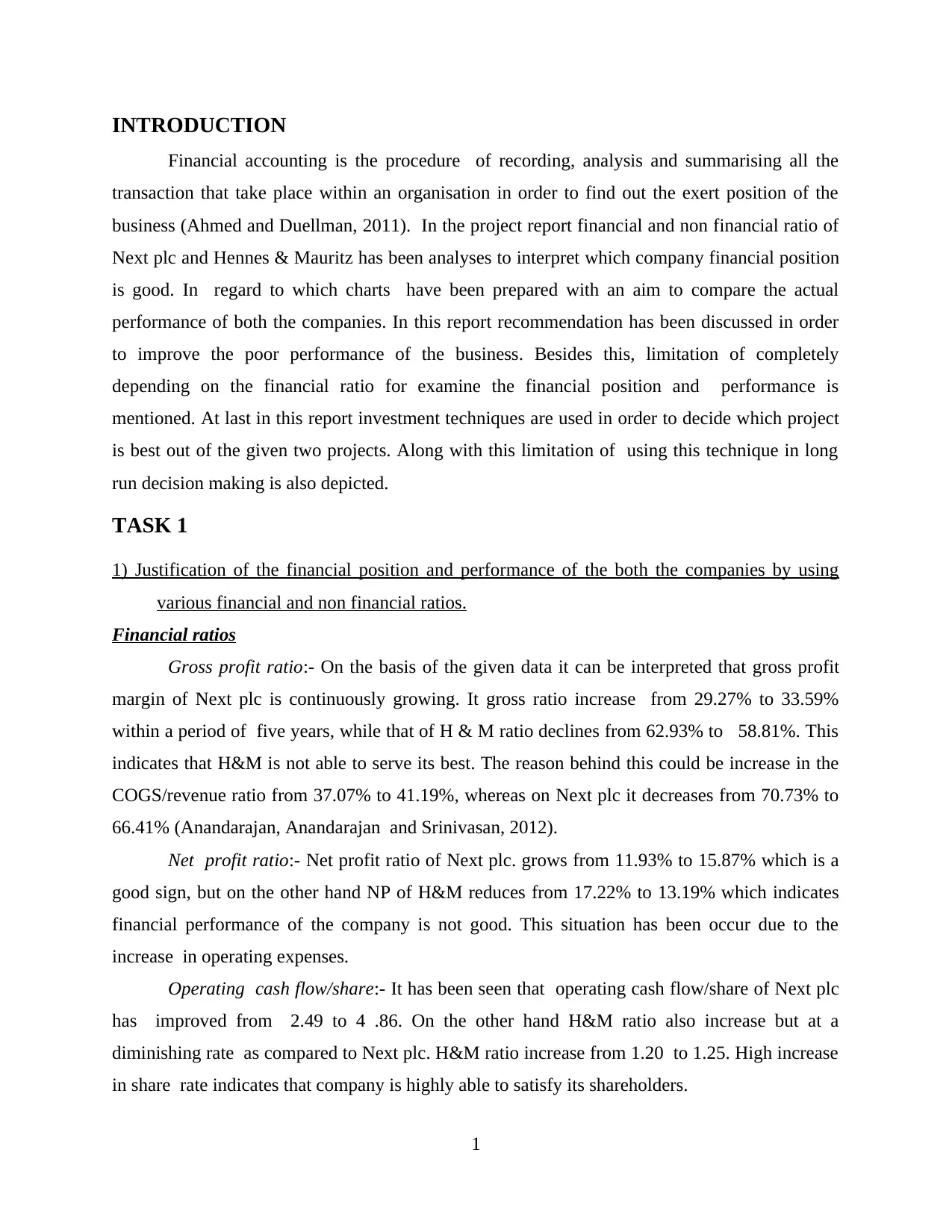

INTRODUCTION

Financial accounting is the procedure of recording, analysis and summarising all the

transaction that take place within an organisation in order to find out the exert position of the

business (Ahmed and Duellman, 2011). In the project report financial and non financial ratio of

Next plc and Hennes & Mauritz has been analyses to interpret which company financial position

is good. In regard to which charts have been prepared with an aim to compare the actual

performance of both the companies. In this report recommendation has been discussed in order

to improve the poor performance of the business. Besides this, limitation of completely

depending on the financial ratio for examine the financial position and performance is

mentioned. At last in this report investment techniques are used in order to decide which project

is best out of the given two projects. Along with this limitation of using this technique in long

run decision making is also depicted.

TASK 1

1) Justification of the financial position and performance of the both the companies by using

various financial and non financial ratios.

Financial ratios

Gross profit ratio:- On the basis of the given data it can be interpreted that gross profit

margin of Next plc is continuously growing. It gross ratio increase from 29.27% to 33.59%

within a period of five years, while that of H & M ratio declines from 62.93% to 58.81%. This

indicates that H&M is not able to serve its best. The reason behind this could be increase in the

COGS/revenue ratio from 37.07% to 41.19%, whereas on Next plc it decreases from 70.73% to

66.41% (Anandarajan, Anandarajan and Srinivasan, 2012).

Net profit ratio:- Net profit ratio of Next plc. grows from 11.93% to 15.87% which is a

good sign, but on the other hand NP of H&M reduces from 17.22% to 13.19% which indicates

financial performance of the company is not good. This situation has been occur due to the

increase in operating expenses.

Operating cash flow/share:- It has been seen that operating cash flow/share of Next plc

has improved from 2.49 to 4 .86. On the other hand H&M ratio also increase but at a

diminishing rate as compared to Next plc. H&M ratio increase from 1.20 to 1.25. High increase

in share rate indicates that company is highly able to satisfy its shareholders.

1

Financial accounting is the procedure of recording, analysis and summarising all the

transaction that take place within an organisation in order to find out the exert position of the

business (Ahmed and Duellman, 2011). In the project report financial and non financial ratio of

Next plc and Hennes & Mauritz has been analyses to interpret which company financial position

is good. In regard to which charts have been prepared with an aim to compare the actual

performance of both the companies. In this report recommendation has been discussed in order

to improve the poor performance of the business. Besides this, limitation of completely

depending on the financial ratio for examine the financial position and performance is

mentioned. At last in this report investment techniques are used in order to decide which project

is best out of the given two projects. Along with this limitation of using this technique in long

run decision making is also depicted.

TASK 1

1) Justification of the financial position and performance of the both the companies by using

various financial and non financial ratios.

Financial ratios

Gross profit ratio:- On the basis of the given data it can be interpreted that gross profit

margin of Next plc is continuously growing. It gross ratio increase from 29.27% to 33.59%

within a period of five years, while that of H & M ratio declines from 62.93% to 58.81%. This

indicates that H&M is not able to serve its best. The reason behind this could be increase in the

COGS/revenue ratio from 37.07% to 41.19%, whereas on Next plc it decreases from 70.73% to

66.41% (Anandarajan, Anandarajan and Srinivasan, 2012).

Net profit ratio:- Net profit ratio of Next plc. grows from 11.93% to 15.87% which is a

good sign, but on the other hand NP of H&M reduces from 17.22% to 13.19% which indicates

financial performance of the company is not good. This situation has been occur due to the

increase in operating expenses.

Operating cash flow/share:- It has been seen that operating cash flow/share of Next plc

has improved from 2.49 to 4 .86. On the other hand H&M ratio also increase but at a

diminishing rate as compared to Next plc. H&M ratio increase from 1.20 to 1.25. High increase

in share rate indicates that company is highly able to satisfy its shareholders.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

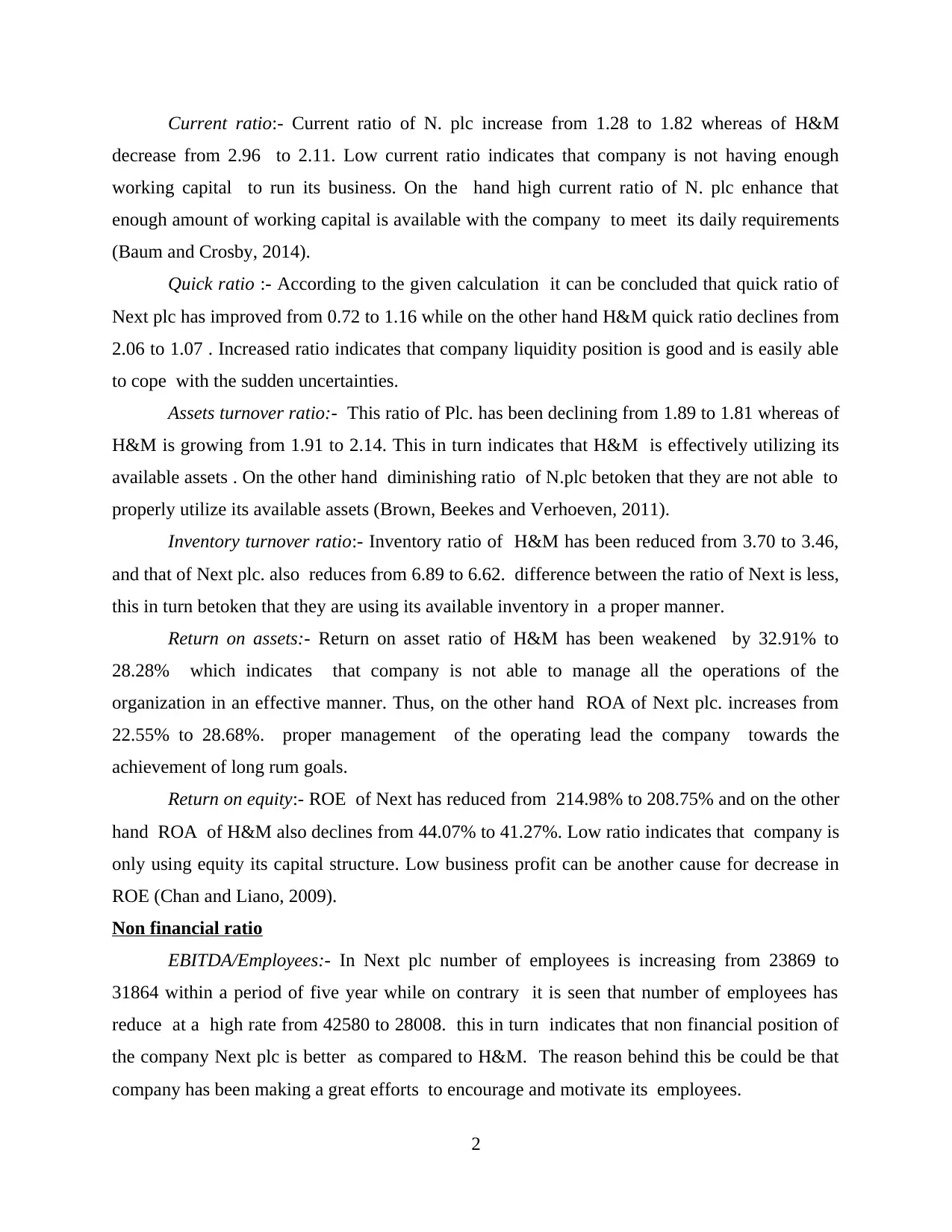

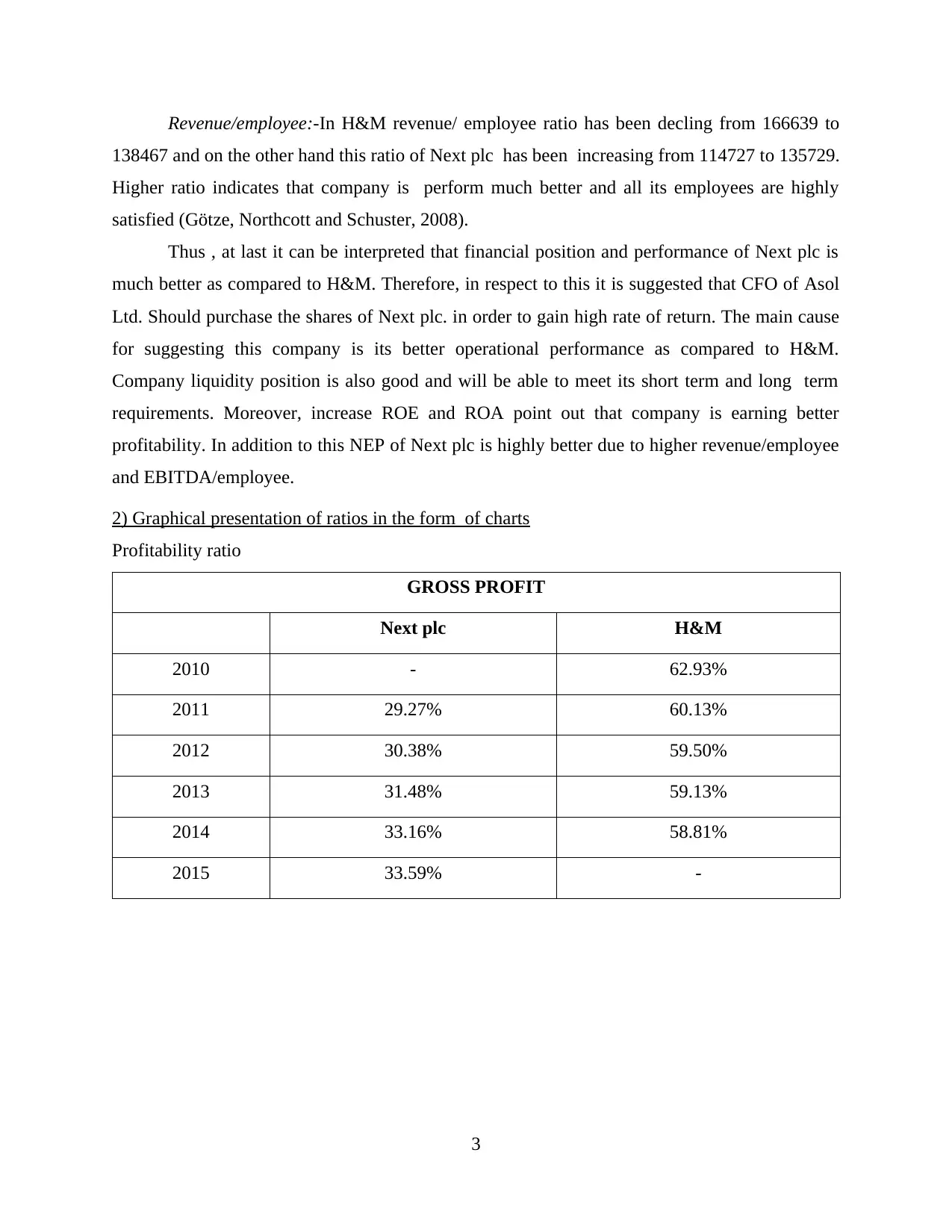

Current ratio:- Current ratio of N. plc increase from 1.28 to 1.82 whereas of H&M

decrease from 2.96 to 2.11. Low current ratio indicates that company is not having enough

working capital to run its business. On the hand high current ratio of N. plc enhance that

enough amount of working capital is available with the company to meet its daily requirements

(Baum and Crosby, 2014).

Quick ratio :- According to the given calculation it can be concluded that quick ratio of

Next plc has improved from 0.72 to 1.16 while on the other hand H&M quick ratio declines from

2.06 to 1.07 . Increased ratio indicates that company liquidity position is good and is easily able

to cope with the sudden uncertainties.

Assets turnover ratio:- This ratio of Plc. has been declining from 1.89 to 1.81 whereas of

H&M is growing from 1.91 to 2.14. This in turn indicates that H&M is effectively utilizing its

available assets . On the other hand diminishing ratio of N.plc betoken that they are not able to

properly utilize its available assets (Brown, Beekes and Verhoeven, 2011).

Inventory turnover ratio:- Inventory ratio of H&M has been reduced from 3.70 to 3.46,

and that of Next plc. also reduces from 6.89 to 6.62. difference between the ratio of Next is less,

this in turn betoken that they are using its available inventory in a proper manner.

Return on assets:- Return on asset ratio of H&M has been weakened by 32.91% to

28.28% which indicates that company is not able to manage all the operations of the

organization in an effective manner. Thus, on the other hand ROA of Next plc. increases from

22.55% to 28.68%. proper management of the operating lead the company towards the

achievement of long rum goals.

Return on equity:- ROE of Next has reduced from 214.98% to 208.75% and on the other

hand ROA of H&M also declines from 44.07% to 41.27%. Low ratio indicates that company is

only using equity its capital structure. Low business profit can be another cause for decrease in

ROE (Chan and Liano, 2009).

Non financial ratio

EBITDA/Employees:- In Next plc number of employees is increasing from 23869 to

31864 within a period of five year while on contrary it is seen that number of employees has

reduce at a high rate from 42580 to 28008. this in turn indicates that non financial position of

the company Next plc is better as compared to H&M. The reason behind this be could be that

company has been making a great efforts to encourage and motivate its employees.

2

decrease from 2.96 to 2.11. Low current ratio indicates that company is not having enough

working capital to run its business. On the hand high current ratio of N. plc enhance that

enough amount of working capital is available with the company to meet its daily requirements

(Baum and Crosby, 2014).

Quick ratio :- According to the given calculation it can be concluded that quick ratio of

Next plc has improved from 0.72 to 1.16 while on the other hand H&M quick ratio declines from

2.06 to 1.07 . Increased ratio indicates that company liquidity position is good and is easily able

to cope with the sudden uncertainties.

Assets turnover ratio:- This ratio of Plc. has been declining from 1.89 to 1.81 whereas of

H&M is growing from 1.91 to 2.14. This in turn indicates that H&M is effectively utilizing its

available assets . On the other hand diminishing ratio of N.plc betoken that they are not able to

properly utilize its available assets (Brown, Beekes and Verhoeven, 2011).

Inventory turnover ratio:- Inventory ratio of H&M has been reduced from 3.70 to 3.46,

and that of Next plc. also reduces from 6.89 to 6.62. difference between the ratio of Next is less,

this in turn betoken that they are using its available inventory in a proper manner.

Return on assets:- Return on asset ratio of H&M has been weakened by 32.91% to

28.28% which indicates that company is not able to manage all the operations of the

organization in an effective manner. Thus, on the other hand ROA of Next plc. increases from

22.55% to 28.68%. proper management of the operating lead the company towards the

achievement of long rum goals.

Return on equity:- ROE of Next has reduced from 214.98% to 208.75% and on the other

hand ROA of H&M also declines from 44.07% to 41.27%. Low ratio indicates that company is

only using equity its capital structure. Low business profit can be another cause for decrease in

ROE (Chan and Liano, 2009).

Non financial ratio

EBITDA/Employees:- In Next plc number of employees is increasing from 23869 to

31864 within a period of five year while on contrary it is seen that number of employees has

reduce at a high rate from 42580 to 28008. this in turn indicates that non financial position of

the company Next plc is better as compared to H&M. The reason behind this be could be that

company has been making a great efforts to encourage and motivate its employees.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Revenue/employee:-In H&M revenue/ employee ratio has been decling from 166639 to

138467 and on the other hand this ratio of Next plc has been increasing from 114727 to 135729.

Higher ratio indicates that company is perform much better and all its employees are highly

satisfied (Götze, Northcott and Schuster, 2008).

Thus , at last it can be interpreted that financial position and performance of Next plc is

much better as compared to H&M. Therefore, in respect to this it is suggested that CFO of Asol

Ltd. Should purchase the shares of Next plc. in order to gain high rate of return. The main cause

for suggesting this company is its better operational performance as compared to H&M.

Company liquidity position is also good and will be able to meet its short term and long term

requirements. Moreover, increase ROE and ROA point out that company is earning better

profitability. In addition to this NEP of Next plc is highly better due to higher revenue/employee

and EBITDA/employee.

2) Graphical presentation of ratios in the form of charts

Profitability ratio

GROSS PROFIT

Next plc H&M

2010 - 62.93%

2011 29.27% 60.13%

2012 30.38% 59.50%

2013 31.48% 59.13%

2014 33.16% 58.81%

2015 33.59% -

3

138467 and on the other hand this ratio of Next plc has been increasing from 114727 to 135729.

Higher ratio indicates that company is perform much better and all its employees are highly

satisfied (Götze, Northcott and Schuster, 2008).

Thus , at last it can be interpreted that financial position and performance of Next plc is

much better as compared to H&M. Therefore, in respect to this it is suggested that CFO of Asol

Ltd. Should purchase the shares of Next plc. in order to gain high rate of return. The main cause

for suggesting this company is its better operational performance as compared to H&M.

Company liquidity position is also good and will be able to meet its short term and long term

requirements. Moreover, increase ROE and ROA point out that company is earning better

profitability. In addition to this NEP of Next plc is highly better due to higher revenue/employee

and EBITDA/employee.

2) Graphical presentation of ratios in the form of charts

Profitability ratio

GROSS PROFIT

Next plc H&M

2010 - 62.93%

2011 29.27% 60.13%

2012 30.38% 59.50%

2013 31.48% 59.13%

2014 33.16% 58.81%

2015 33.59% -

3

NET PROFIT

Next plc H&M

2010 - 17.22%

2011 11.93% 14.38%

2012 12.62% 13.96%

2013 14.34% 13.30%

2014 14.79% 13.19%

2015 15.87% -

4

1 2 3 4 5 6

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0

0.29 0.3 0.31 0.33 0.34

62.93% 60.13% 59.50% 59.13% 58.81%

Next plc

H&M

Illustration 1: GROSS PROFIT

Next plc H&M

2010 - 17.22%

2011 11.93% 14.38%

2012 12.62% 13.96%

2013 14.34% 13.30%

2014 14.79% 13.19%

2015 15.87% -

4

1 2 3 4 5 6

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0

0.29 0.3 0.31 0.33 0.34

62.93% 60.13% 59.50% 59.13% 58.81%

Next plc

H&M

Illustration 1: GROSS PROFIT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CURRENT RATIO

Next plc H&M

2010 - 2.96

2011 1.28 2.71

2012 1.54 2.66

2013 1.48 2.25

2014 1.76 2.11

2015 1.82 -

5

1 2 3 4 5 6

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

0

0.12 0.13

0.14 0.15

0.16

17.22%

14.38% 13.96% 13.30% 13.19%

Next plc

H&M

Illustration 2: NET PROFIT

Next plc H&M

2010 - 2.96

2011 1.28 2.71

2012 1.54 2.66

2013 1.48 2.25

2014 1.76 2.11

2015 1.82 -

5

1 2 3 4 5 6

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

0

0.12 0.13

0.14 0.15

0.16

17.22%

14.38% 13.96% 13.30% 13.19%

Next plc

H&M

Illustration 2: NET PROFIT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

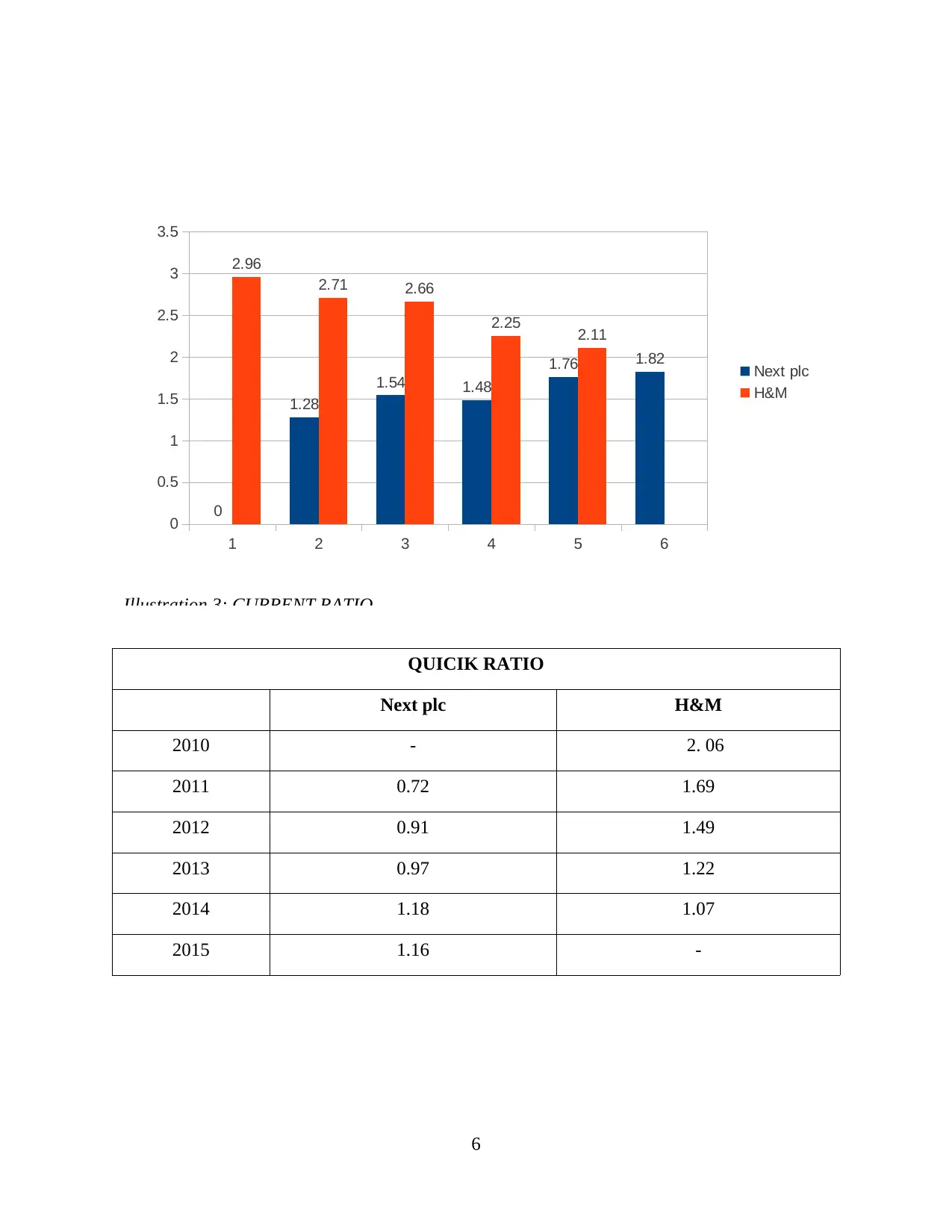

QUICIK RATIO

Next plc H&M

2010 - 2. 06

2011 0.72 1.69

2012 0.91 1.49

2013 0.97 1.22

2014 1.18 1.07

2015 1.16 -

6

1 2 3 4 5 6

0

0.5

1

1.5

2

2.5

3

3.5

0

1.28

1.54 1.48

1.76 1.82

2.96

2.71 2.66

2.25 2.11

Next plc

H&M

Illustration 3: CURRENT RATIO

Next plc H&M

2010 - 2. 06

2011 0.72 1.69

2012 0.91 1.49

2013 0.97 1.22

2014 1.18 1.07

2015 1.16 -

6

1 2 3 4 5 6

0

0.5

1

1.5

2

2.5

3

3.5

0

1.28

1.54 1.48

1.76 1.82

2.96

2.71 2.66

2.25 2.11

Next plc

H&M

Illustration 3: CURRENT RATIO

3) Recommendation to H&M to improve financial performance and position

On the basis of the above calculation it can be interpreted that financial position of H&M

is declining. Therefore, it respect to which it is suggested that company should develop various

strategies in order to improve its sales revenue. They should also try to fulfil the demand of the

customers by providing better quality products at low and affordable price. This in turn will

increase the sales of the company. Furthermore, manager should start keeping a constant look on

the operations of the organization with an aim to reduce the expenses of the company (Haka,

2006). In lieu of which company will be able to increase its profitability.

High operating expenses of the company will result in the reducing the operational

performance of the company. In addition to this H&M should make an efforts to control its

overheads which in turn will increase the net margin of the company. If profit of the company

will increase than ROA and ROE will also increase. This in turn will improve the operational

performance of the company.

Current and Quick ratio of the company indicates that they are financial sound in order

to meet up its short term requirement or any sudden uncertainties. Thus, in order to overcome

7

1 2 3 4 5 6

0

0.5

1

1.5

2

2.5

0

0.72

0.91 0.97

1.18 1.16

2.06

1.69

1.49

1.22

1.07 Next plc

H&M

Illustration 4: QUICK RATIO

On the basis of the above calculation it can be interpreted that financial position of H&M

is declining. Therefore, it respect to which it is suggested that company should develop various

strategies in order to improve its sales revenue. They should also try to fulfil the demand of the

customers by providing better quality products at low and affordable price. This in turn will

increase the sales of the company. Furthermore, manager should start keeping a constant look on

the operations of the organization with an aim to reduce the expenses of the company (Haka,

2006). In lieu of which company will be able to increase its profitability.

High operating expenses of the company will result in the reducing the operational

performance of the company. In addition to this H&M should make an efforts to control its

overheads which in turn will increase the net margin of the company. If profit of the company

will increase than ROA and ROE will also increase. This in turn will improve the operational

performance of the company.

Current and Quick ratio of the company indicates that they are financial sound in order

to meet up its short term requirement or any sudden uncertainties. Thus, in order to overcome

7

1 2 3 4 5 6

0

0.5

1

1.5

2

2.5

0

0.72

0.91 0.97

1.18 1.16

2.06

1.69

1.49

1.22

1.07 Next plc

H&M

Illustration 4: QUICK RATIO

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

this problem company should start collecting earlier payment from its receivables and should

start negotiating the payment of the creditors. This in turn will improve the liquid assets of the

company. Furthermore, speedy movement of inventory will improve the liquid assets of the

company. This in turn will help the company will further start its operating functions in a speedy

manner without facing any difficulties (Atrill and McLaney, 2006)..

Besides this, it is also recommend that should consider both debt and equity in order to

fulfil its capital requirement. This in turn will help the company to avail benefits on equity and

will increase the shareholders return. And will maintain the financial risk of the company at a

minimum level.

4) Limitation and drawbacks of using ratio analysis

There are certain types of drawbacks in making comparative logical thinking through

ratio analysis. Ratio analysis is done on the historical data basis but the investors prefer to

analysis the performance of the company by predicting future data. By using the concept of ratio

analysis investors are not able to determine the future performance of the company. Furthermore

, performance of the company cannot be compared properly because different companies use

different accounting standards, policies and methods to record its day to day transaction

(Karande and Chakraborty, 2012). In addition to this market condition highly affects the

performance of the business and this concept is not used at the time of doing ratio analysis.

Thus, comparison with different companies on the basis of ratio may prove to be hazardous for

the company. Besides this interpretation on the basis of ratio is very difficulty. Along with all

this different accounting principles and standards used for recording the day to day activities can

lead to inefficient an incorrect decisions. Thus completely rely on ratio analysis for comparing

and calculating the financial position of the company is not correct.

TASK 2 Capital Investment Appraisal

1) Analysing the viability of the project by using investment appraisal techniques

Investment appraisal techniques will assist the Hilltop to analyse the viability of the

company (Kavanagh and Drennan, 2008). By using this company will be able to analyse whether

they incur profit and will suffer the loss if they move on with a particular project. Thus, in regard

to this viability of both the given project for Hilltop is examined by using investment appraisal

techniques.

8

start negotiating the payment of the creditors. This in turn will improve the liquid assets of the

company. Furthermore, speedy movement of inventory will improve the liquid assets of the

company. This in turn will help the company will further start its operating functions in a speedy

manner without facing any difficulties (Atrill and McLaney, 2006)..

Besides this, it is also recommend that should consider both debt and equity in order to

fulfil its capital requirement. This in turn will help the company to avail benefits on equity and

will increase the shareholders return. And will maintain the financial risk of the company at a

minimum level.

4) Limitation and drawbacks of using ratio analysis

There are certain types of drawbacks in making comparative logical thinking through

ratio analysis. Ratio analysis is done on the historical data basis but the investors prefer to

analysis the performance of the company by predicting future data. By using the concept of ratio

analysis investors are not able to determine the future performance of the company. Furthermore

, performance of the company cannot be compared properly because different companies use

different accounting standards, policies and methods to record its day to day transaction

(Karande and Chakraborty, 2012). In addition to this market condition highly affects the

performance of the business and this concept is not used at the time of doing ratio analysis.

Thus, comparison with different companies on the basis of ratio may prove to be hazardous for

the company. Besides this interpretation on the basis of ratio is very difficulty. Along with all

this different accounting principles and standards used for recording the day to day activities can

lead to inefficient an incorrect decisions. Thus completely rely on ratio analysis for comparing

and calculating the financial position of the company is not correct.

TASK 2 Capital Investment Appraisal

1) Analysing the viability of the project by using investment appraisal techniques

Investment appraisal techniques will assist the Hilltop to analyse the viability of the

company (Kavanagh and Drennan, 2008). By using this company will be able to analyse whether

they incur profit and will suffer the loss if they move on with a particular project. Thus, in regard

to this viability of both the given project for Hilltop is examined by using investment appraisal

techniques.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

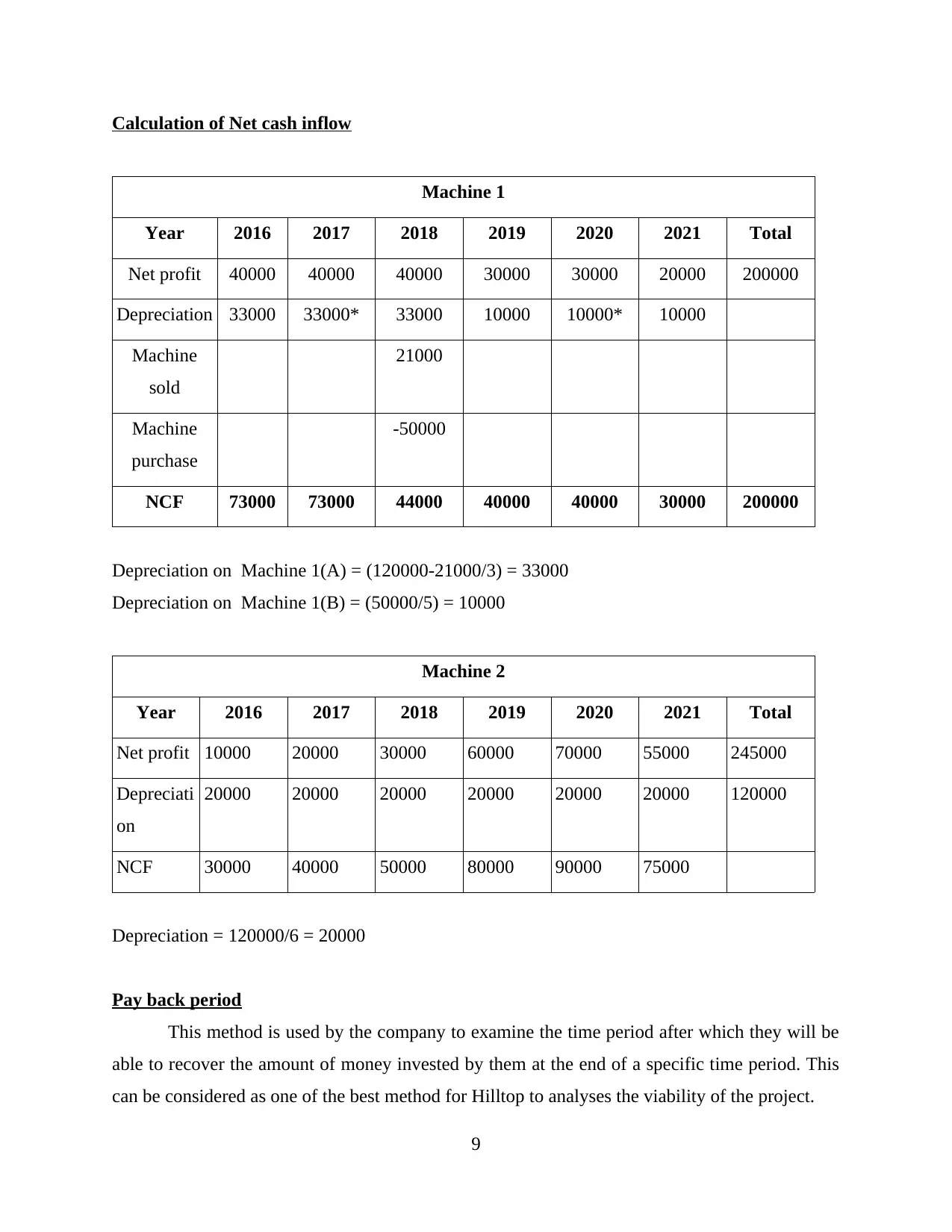

Calculation of Net cash inflow

Machine 1

Year 2016 2017 2018 2019 2020 2021 Total

Net profit 40000 40000 40000 30000 30000 20000 200000

Depreciation 33000 33000* 33000 10000 10000* 10000

Machine

sold

21000

Machine

purchase

-50000

NCF 73000 73000 44000 40000 40000 30000 200000

Depreciation on Machine 1(A) = (120000-21000/3) = 33000

Depreciation on Machine 1(B) = (50000/5) = 10000

Machine 2

Year 2016 2017 2018 2019 2020 2021 Total

Net profit 10000 20000 30000 60000 70000 55000 245000

Depreciati

on

20000 20000 20000 20000 20000 20000 120000

NCF 30000 40000 50000 80000 90000 75000

Depreciation = 120000/6 = 20000

Pay back period

This method is used by the company to examine the time period after which they will be

able to recover the amount of money invested by them at the end of a specific time period. This

can be considered as one of the best method for Hilltop to analyses the viability of the project.

9

Machine 1

Year 2016 2017 2018 2019 2020 2021 Total

Net profit 40000 40000 40000 30000 30000 20000 200000

Depreciation 33000 33000* 33000 10000 10000* 10000

Machine

sold

21000

Machine

purchase

-50000

NCF 73000 73000 44000 40000 40000 30000 200000

Depreciation on Machine 1(A) = (120000-21000/3) = 33000

Depreciation on Machine 1(B) = (50000/5) = 10000

Machine 2

Year 2016 2017 2018 2019 2020 2021 Total

Net profit 10000 20000 30000 60000 70000 55000 245000

Depreciati

on

20000 20000 20000 20000 20000 20000 120000

NCF 30000 40000 50000 80000 90000 75000

Depreciation = 120000/6 = 20000

Pay back period

This method is used by the company to examine the time period after which they will be

able to recover the amount of money invested by them at the end of a specific time period. This

can be considered as one of the best method for Hilltop to analyses the viability of the project.

9

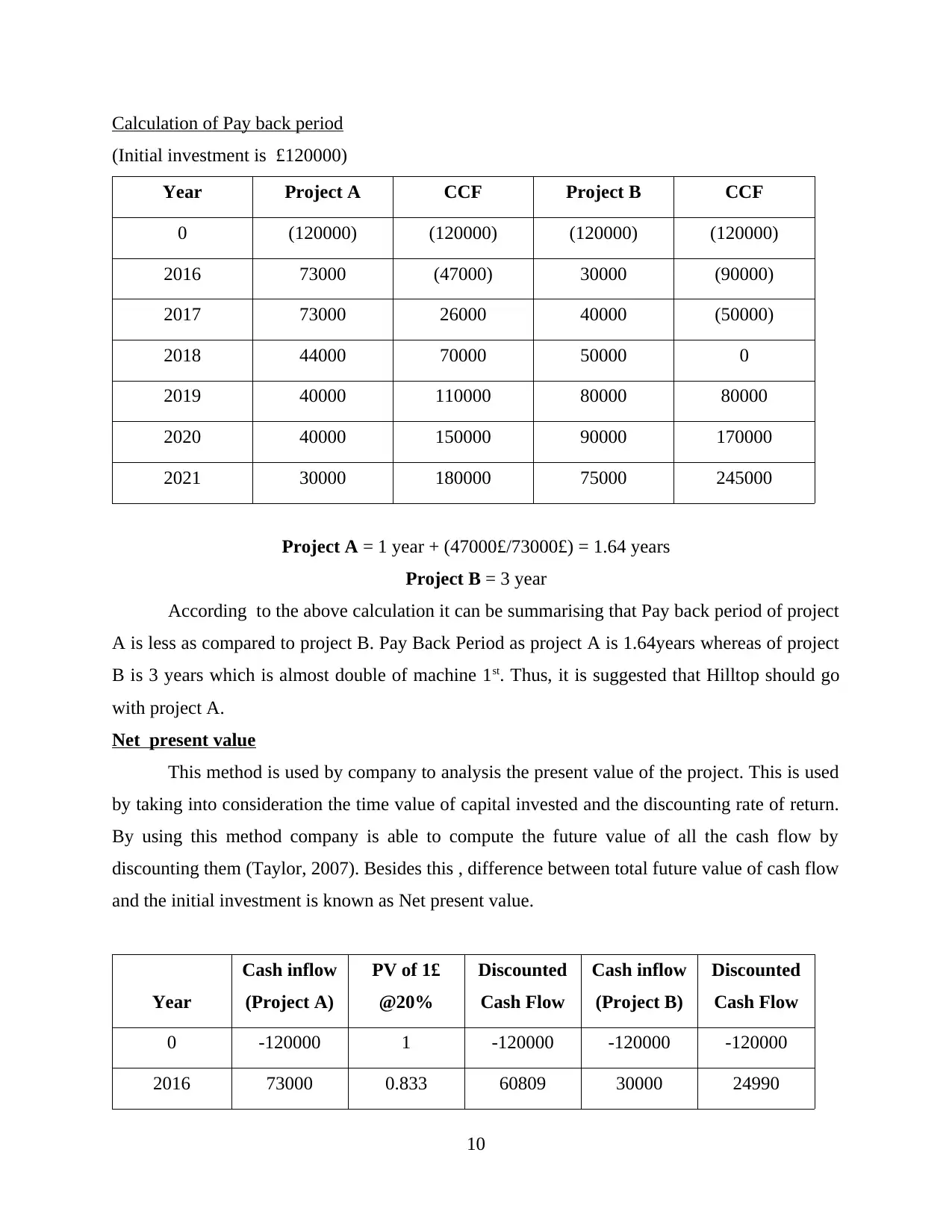

Calculation of Pay back period

(Initial investment is £120000)

Year Project A CCF Project B CCF

0 (120000) (120000) (120000) (120000)

2016 73000 (47000) 30000 (90000)

2017 73000 26000 40000 (50000)

2018 44000 70000 50000 0

2019 40000 110000 80000 80000

2020 40000 150000 90000 170000

2021 30000 180000 75000 245000

Project A = 1 year + (47000£/73000£) = 1.64 years

Project B = 3 year

According to the above calculation it can be summarising that Pay back period of project

A is less as compared to project B. Pay Back Period as project A is 1.64years whereas of project

B is 3 years which is almost double of machine 1st. Thus, it is suggested that Hilltop should go

with project A.

Net present value

This method is used by company to analysis the present value of the project. This is used

by taking into consideration the time value of capital invested and the discounting rate of return.

By using this method company is able to compute the future value of all the cash flow by

discounting them (Taylor, 2007). Besides this , difference between total future value of cash flow

and the initial investment is known as Net present value.

Year

Cash inflow

(Project A)

PV of 1£

@20%

Discounted

Cash Flow

Cash inflow

(Project B)

Discounted

Cash Flow

0 -120000 1 -120000 -120000 -120000

2016 73000 0.833 60809 30000 24990

10

(Initial investment is £120000)

Year Project A CCF Project B CCF

0 (120000) (120000) (120000) (120000)

2016 73000 (47000) 30000 (90000)

2017 73000 26000 40000 (50000)

2018 44000 70000 50000 0

2019 40000 110000 80000 80000

2020 40000 150000 90000 170000

2021 30000 180000 75000 245000

Project A = 1 year + (47000£/73000£) = 1.64 years

Project B = 3 year

According to the above calculation it can be summarising that Pay back period of project

A is less as compared to project B. Pay Back Period as project A is 1.64years whereas of project

B is 3 years which is almost double of machine 1st. Thus, it is suggested that Hilltop should go

with project A.

Net present value

This method is used by company to analysis the present value of the project. This is used

by taking into consideration the time value of capital invested and the discounting rate of return.

By using this method company is able to compute the future value of all the cash flow by

discounting them (Taylor, 2007). Besides this , difference between total future value of cash flow

and the initial investment is known as Net present value.

Year

Cash inflow

(Project A)

PV of 1£

@20%

Discounted

Cash Flow

Cash inflow

(Project B)

Discounted

Cash Flow

0 -120000 1 -120000 -120000 -120000

2016 73000 0.833 60809 30000 24990

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.