Financial Accounting Report on Next Plc: Ratio Analysis and ESG

VerifiedAdded on 2023/06/16

|12

|2822

|137

Report

AI Summary

This report provides a financial analysis of Next Plc, a UK-based apparel and home products company, using ratio analysis and an examination of ESG (Environmental, Social, and Governance) factors. The analysis includes profitability ratios (gross profit ratio, operating profit margin), liquidity ratios (current ratio, quick ratio), efficiency ratios (debtor turnover ratio, asset turnover ratio), and long-term financial stability ratios (debt to equity ratio, interest coverage ratio) calculated from the company's financial statements over the past five years. The report interprets these ratios to assess Next Plc's financial health, operational efficiency, and ability to manage debt. Furthermore, it discusses the impact of economic, social, and governmental ESG factors on the company's performance, including considerations of unemployment rates, exchange rates, demographic shifts, and regulatory compliance. The report concludes with recommendations for Next Plc to leverage economic trends, navigate political hindrances, capitalize on market trends, and maintain financial stability to enhance its brand image and market growth. The conclusion emphasizes the crucial role of financial accounting and ratio analysis in determining an organization's financial position.

Financial Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

Description and Purpose of ratios....................................................................................................3

ESG factors of Next Plc...................................................................................................................4

Recommendations............................................................................................................................6

Conclusion.......................................................................................................................................6

References........................................................................................................................................7

Appendix..........................................................................................................................................8

2

Introduction......................................................................................................................................3

Description and Purpose of ratios....................................................................................................3

ESG factors of Next Plc...................................................................................................................4

Recommendations............................................................................................................................6

Conclusion.......................................................................................................................................6

References........................................................................................................................................7

Appendix..........................................................................................................................................8

2

Introduction

Financial Accounting is referred as a branch of accounting that comprises of a process of

recording, analysing and summarising the reports. These transactions are a result of the business

operations that take place over a period of time (Lee, 2020).

Next plc is a UK based organisation that deals in apparels, footwear and home products.

The headquarters of Next Plc is situated at Enderby, England. The brand has nearly 700 stores

across the globe. The report revolves around the financial accounting of Next plc. The given

report will explore financial analysis of the given company through preparation of various

financial aspects of the company. Further, in the said report document several understandings are

being made in respect to analysing of each ration with ESG factors.

Description and Purpose of ratios

Ratio analysis is basically a comparison between the several line item data from the

organisation that is derived from the financial statements of the organisation. The ratio tends to

reveal the insight in context of profitability, liquidity, operational efficiency and solvency. The

concept revolves around the quantitative interpretation of the financial performance of the

organisation. The profitability and liquidity ratios have been calculated based upon the last five

years' financial statements.

Profitability ratio

The profitability ratios are the classification on the basis of the financial metrics that are helpful

in assessing the ability of the business in order to generate earnings of the organisation in context

to revenue, operating costs, balance sheets etc. The several profitability ratios have been

discussed below.

Gross Profit ratio- The gross profit ratio tends to measure the profitability of the

organisation while accounting for cost of goods sold (Porter, 2019).

Gross Profit ratio = Gross profit/ Sales * 100

Interpretation- The gross profit ratio has been witnessed at a higher pace in 202 as the

cost of goods had fallen in comparison to the 2021. The cost of goods sold have also reduced

which has shown an increase in the gross profit of the organisation for the year of 2021. The

ratio has been increasing at a positive rate which further fell in the year 2021.

3

Financial Accounting is referred as a branch of accounting that comprises of a process of

recording, analysing and summarising the reports. These transactions are a result of the business

operations that take place over a period of time (Lee, 2020).

Next plc is a UK based organisation that deals in apparels, footwear and home products.

The headquarters of Next Plc is situated at Enderby, England. The brand has nearly 700 stores

across the globe. The report revolves around the financial accounting of Next plc. The given

report will explore financial analysis of the given company through preparation of various

financial aspects of the company. Further, in the said report document several understandings are

being made in respect to analysing of each ration with ESG factors.

Description and Purpose of ratios

Ratio analysis is basically a comparison between the several line item data from the

organisation that is derived from the financial statements of the organisation. The ratio tends to

reveal the insight in context of profitability, liquidity, operational efficiency and solvency. The

concept revolves around the quantitative interpretation of the financial performance of the

organisation. The profitability and liquidity ratios have been calculated based upon the last five

years' financial statements.

Profitability ratio

The profitability ratios are the classification on the basis of the financial metrics that are helpful

in assessing the ability of the business in order to generate earnings of the organisation in context

to revenue, operating costs, balance sheets etc. The several profitability ratios have been

discussed below.

Gross Profit ratio- The gross profit ratio tends to measure the profitability of the

organisation while accounting for cost of goods sold (Porter, 2019).

Gross Profit ratio = Gross profit/ Sales * 100

Interpretation- The gross profit ratio has been witnessed at a higher pace in 202 as the

cost of goods had fallen in comparison to the 2021. The cost of goods sold have also reduced

which has shown an increase in the gross profit of the organisation for the year of 2021. The

ratio has been increasing at a positive rate which further fell in the year 2021.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

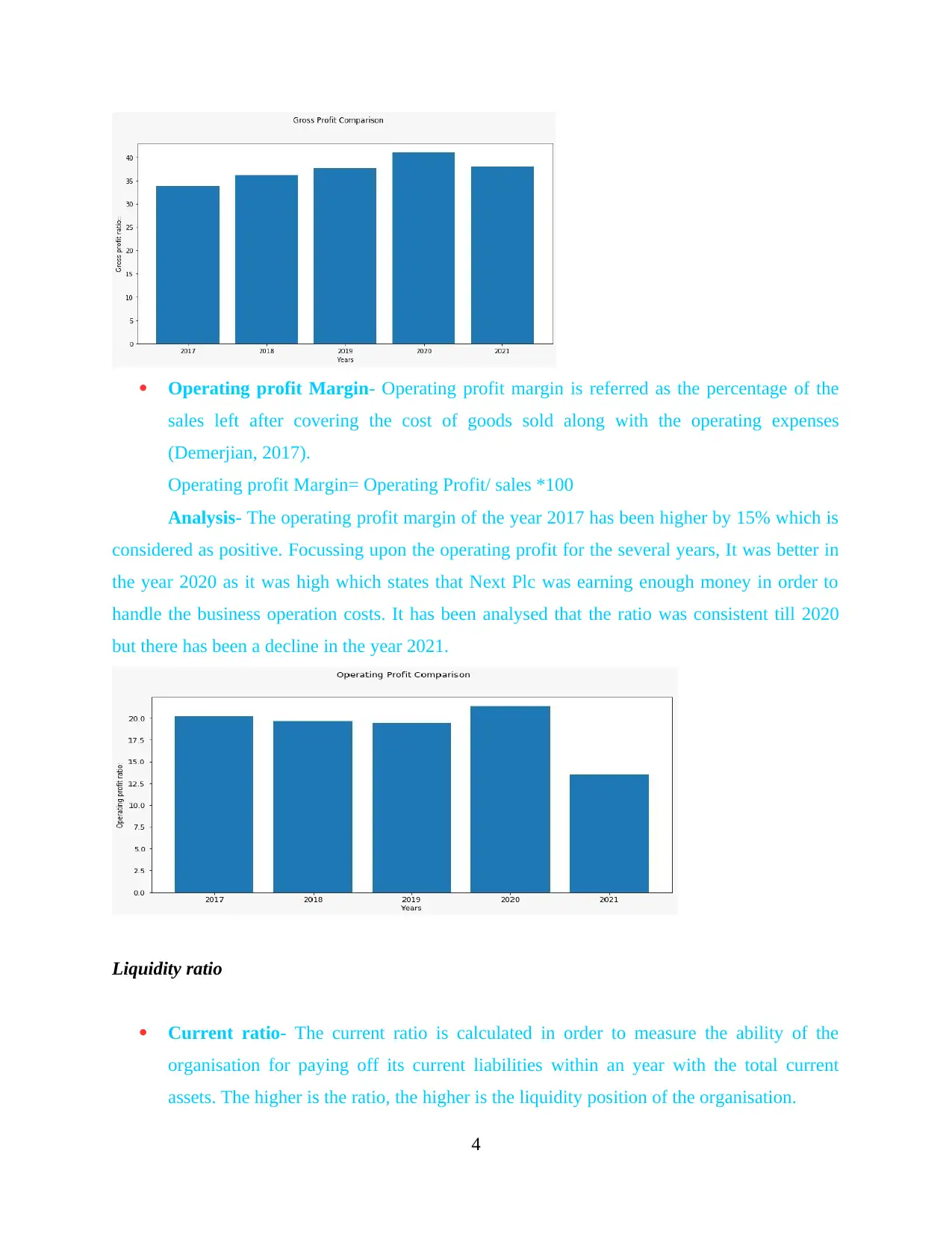

Operating profit Margin- Operating profit margin is referred as the percentage of the

sales left after covering the cost of goods sold along with the operating expenses

(Demerjian, 2017).

Operating profit Margin= Operating Profit/ sales *100

Analysis- The operating profit margin of the year 2017 has been higher by 15% which is

considered as positive. Focussing upon the operating profit for the several years, It was better in

the year 2020 as it was high which states that Next Plc was earning enough money in order to

handle the business operation costs. It has been analysed that the ratio was consistent till 2020

but there has been a decline in the year 2021.

Liquidity ratio

Current ratio- The current ratio is calculated in order to measure the ability of the

organisation for paying off its current liabilities within an year with the total current

assets. The higher is the ratio, the higher is the liquidity position of the organisation.

4

sales left after covering the cost of goods sold along with the operating expenses

(Demerjian, 2017).

Operating profit Margin= Operating Profit/ sales *100

Analysis- The operating profit margin of the year 2017 has been higher by 15% which is

considered as positive. Focussing upon the operating profit for the several years, It was better in

the year 2020 as it was high which states that Next Plc was earning enough money in order to

handle the business operation costs. It has been analysed that the ratio was consistent till 2020

but there has been a decline in the year 2021.

Liquidity ratio

Current ratio- The current ratio is calculated in order to measure the ability of the

organisation for paying off its current liabilities within an year with the total current

assets. The higher is the ratio, the higher is the liquidity position of the organisation.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

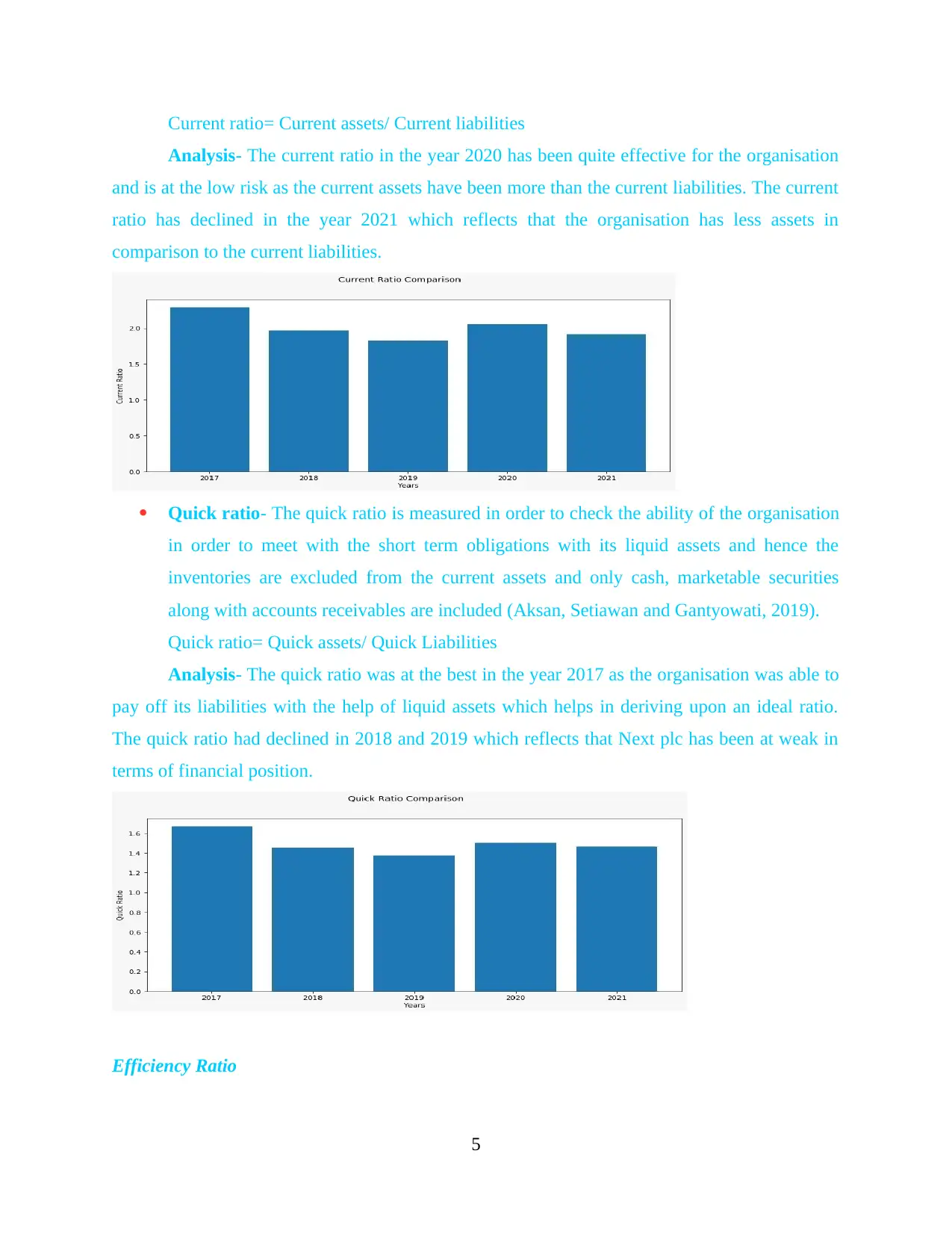

Current ratio= Current assets/ Current liabilities

Analysis- The current ratio in the year 2020 has been quite effective for the organisation

and is at the low risk as the current assets have been more than the current liabilities. The current

ratio has declined in the year 2021 which reflects that the organisation has less assets in

comparison to the current liabilities.

Quick ratio- The quick ratio is measured in order to check the ability of the organisation

in order to meet with the short term obligations with its liquid assets and hence the

inventories are excluded from the current assets and only cash, marketable securities

along with accounts receivables are included (Aksan, Setiawan and Gantyowati, 2019).

Quick ratio= Quick assets/ Quick Liabilities

Analysis- The quick ratio was at the best in the year 2017 as the organisation was able to

pay off its liabilities with the help of liquid assets which helps in deriving upon an ideal ratio.

The quick ratio had declined in 2018 and 2019 which reflects that Next plc has been at weak in

terms of financial position.

Efficiency Ratio

5

Analysis- The current ratio in the year 2020 has been quite effective for the organisation

and is at the low risk as the current assets have been more than the current liabilities. The current

ratio has declined in the year 2021 which reflects that the organisation has less assets in

comparison to the current liabilities.

Quick ratio- The quick ratio is measured in order to check the ability of the organisation

in order to meet with the short term obligations with its liquid assets and hence the

inventories are excluded from the current assets and only cash, marketable securities

along with accounts receivables are included (Aksan, Setiawan and Gantyowati, 2019).

Quick ratio= Quick assets/ Quick Liabilities

Analysis- The quick ratio was at the best in the year 2017 as the organisation was able to

pay off its liabilities with the help of liquid assets which helps in deriving upon an ideal ratio.

The quick ratio had declined in 2018 and 2019 which reflects that Next plc has been at weak in

terms of financial position.

Efficiency Ratio

5

Debtor turnover ratio- Debtor turnover ratio helps in measuring the capacity of Next

plc to extend the credit along with the collection of the debts. This has helped the

organisation understand the capability of the organisation to use its assets.

Analysis- The debtor turnover ratio states that the organisation will require 63 days in order to

pay off its debt in order to get back to solvency. Further it can be analysed that Next plc has been

performing at a better pace in the year 2020. It has helped the organisation to increase its level of

productivity as well as the efficiency in the business operations.

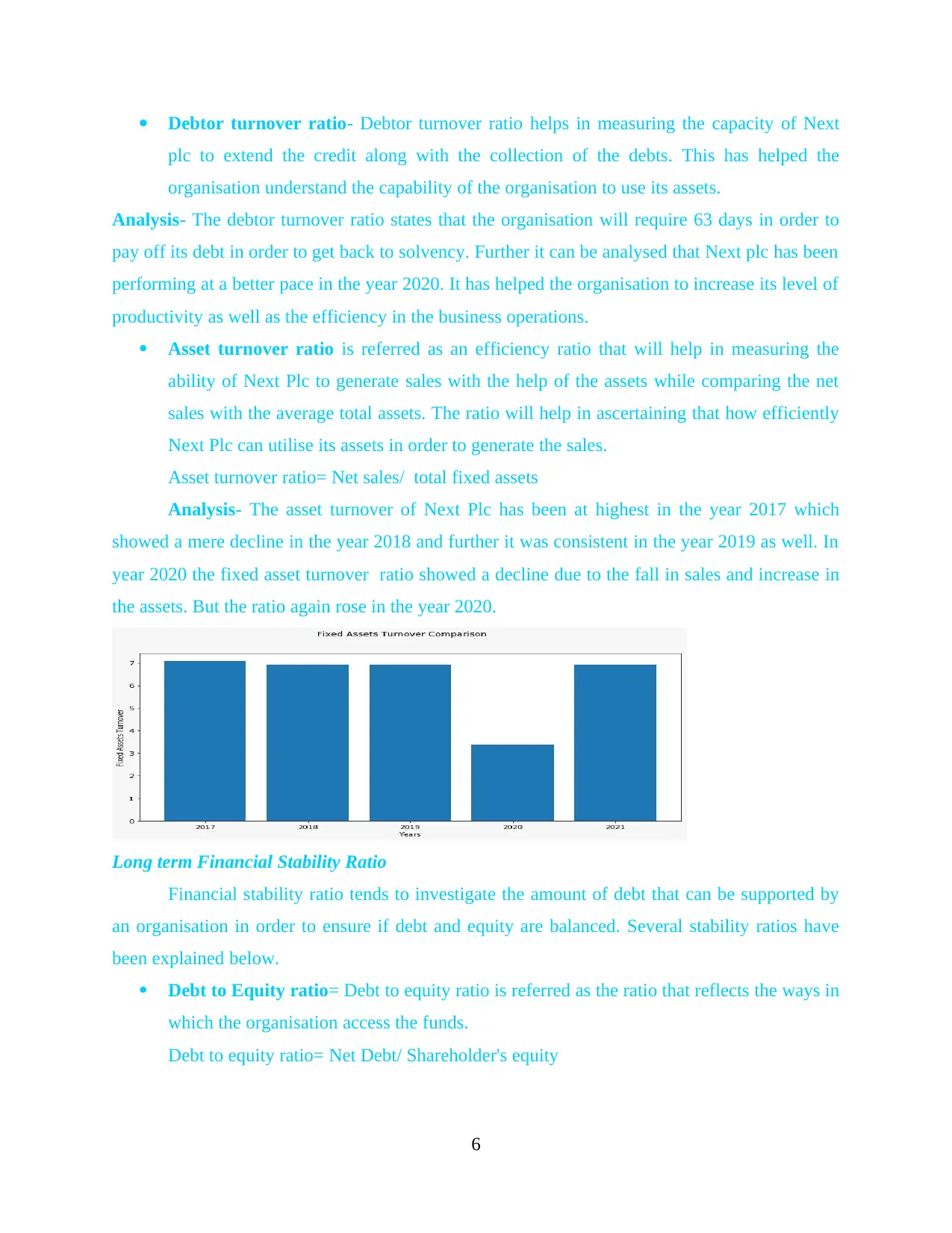

Asset turnover ratio is referred as an efficiency ratio that will help in measuring the

ability of Next Plc to generate sales with the help of the assets while comparing the net

sales with the average total assets. The ratio will help in ascertaining that how efficiently

Next Plc can utilise its assets in order to generate the sales.

Asset turnover ratio= Net sales/ total fixed assets

Analysis- The asset turnover of Next Plc has been at highest in the year 2017 which

showed a mere decline in the year 2018 and further it was consistent in the year 2019 as well. In

year 2020 the fixed asset turnover ratio showed a decline due to the fall in sales and increase in

the assets. But the ratio again rose in the year 2020.

Long term Financial Stability Ratio

Financial stability ratio tends to investigate the amount of debt that can be supported by

an organisation in order to ensure if debt and equity are balanced. Several stability ratios have

been explained below.

Debt to Equity ratio= Debt to equity ratio is referred as the ratio that reflects the ways in

which the organisation access the funds.

Debt to equity ratio= Net Debt/ Shareholder's equity

6

plc to extend the credit along with the collection of the debts. This has helped the

organisation understand the capability of the organisation to use its assets.

Analysis- The debtor turnover ratio states that the organisation will require 63 days in order to

pay off its debt in order to get back to solvency. Further it can be analysed that Next plc has been

performing at a better pace in the year 2020. It has helped the organisation to increase its level of

productivity as well as the efficiency in the business operations.

Asset turnover ratio is referred as an efficiency ratio that will help in measuring the

ability of Next Plc to generate sales with the help of the assets while comparing the net

sales with the average total assets. The ratio will help in ascertaining that how efficiently

Next Plc can utilise its assets in order to generate the sales.

Asset turnover ratio= Net sales/ total fixed assets

Analysis- The asset turnover of Next Plc has been at highest in the year 2017 which

showed a mere decline in the year 2018 and further it was consistent in the year 2019 as well. In

year 2020 the fixed asset turnover ratio showed a decline due to the fall in sales and increase in

the assets. But the ratio again rose in the year 2020.

Long term Financial Stability Ratio

Financial stability ratio tends to investigate the amount of debt that can be supported by

an organisation in order to ensure if debt and equity are balanced. Several stability ratios have

been explained below.

Debt to Equity ratio= Debt to equity ratio is referred as the ratio that reflects the ways in

which the organisation access the funds.

Debt to equity ratio= Net Debt/ Shareholder's equity

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

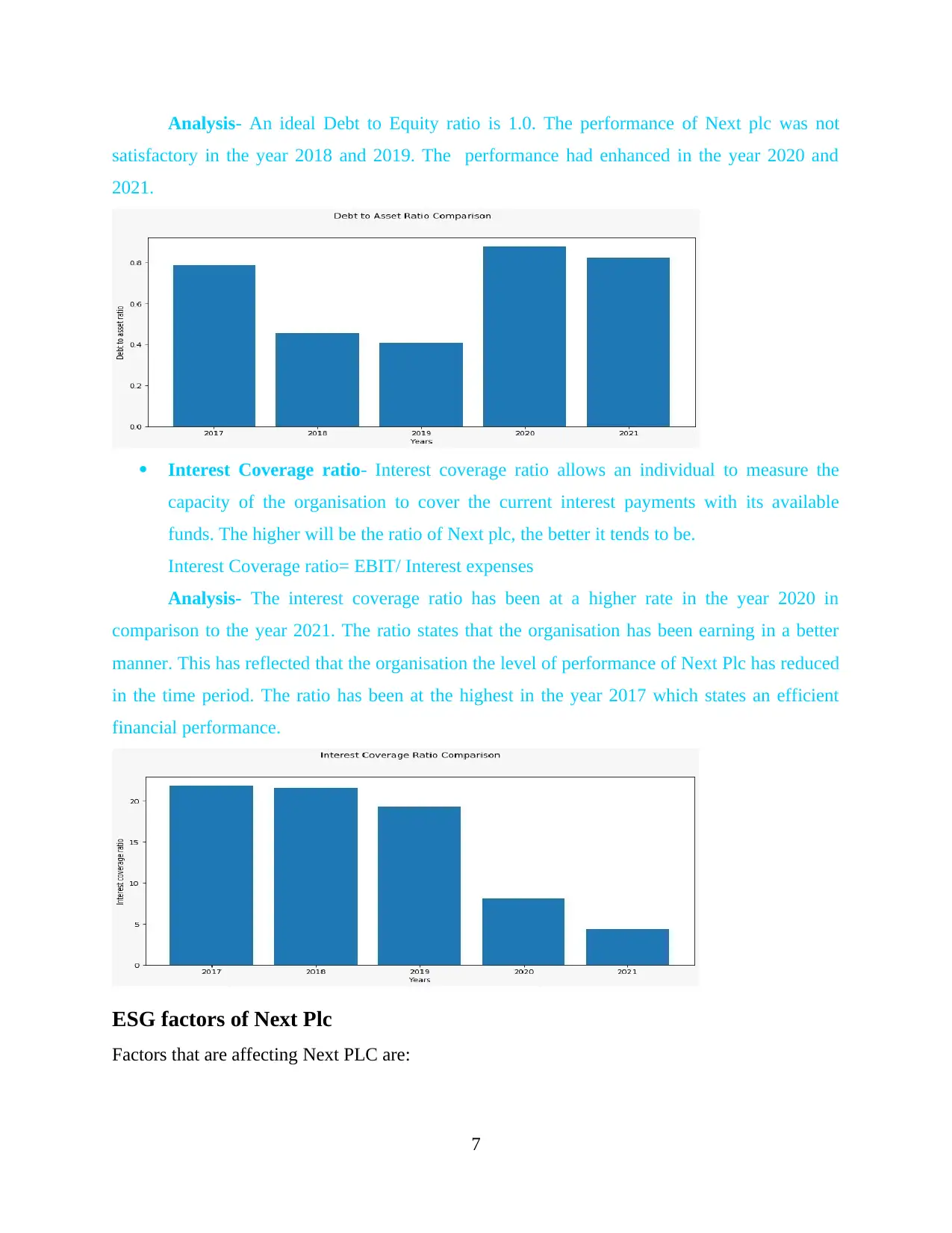

Analysis- An ideal Debt to Equity ratio is 1.0. The performance of Next plc was not

satisfactory in the year 2018 and 2019. The performance had enhanced in the year 2020 and

2021.

Interest Coverage ratio- Interest coverage ratio allows an individual to measure the

capacity of the organisation to cover the current interest payments with its available

funds. The higher will be the ratio of Next plc, the better it tends to be.

Interest Coverage ratio= EBIT/ Interest expenses

Analysis- The interest coverage ratio has been at a higher rate in the year 2020 in

comparison to the year 2021. The ratio states that the organisation has been earning in a better

manner. This has reflected that the organisation the level of performance of Next Plc has reduced

in the time period. The ratio has been at the highest in the year 2017 which states an efficient

financial performance.

ESG factors of Next Plc

Factors that are affecting Next PLC are:

7

satisfactory in the year 2018 and 2019. The performance had enhanced in the year 2020 and

2021.

Interest Coverage ratio- Interest coverage ratio allows an individual to measure the

capacity of the organisation to cover the current interest payments with its available

funds. The higher will be the ratio of Next plc, the better it tends to be.

Interest Coverage ratio= EBIT/ Interest expenses

Analysis- The interest coverage ratio has been at a higher rate in the year 2020 in

comparison to the year 2021. The ratio states that the organisation has been earning in a better

manner. This has reflected that the organisation the level of performance of Next Plc has reduced

in the time period. The ratio has been at the highest in the year 2017 which states an efficient

financial performance.

ESG factors of Next Plc

Factors that are affecting Next PLC are:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Economic factor: This factor refers to change in economy due to inflation, exchange

rate, unemployment and many other factors. In UK the unemployment rate is getting

reduce and it is good news for UK. But for big companies like Next Plc it is a challenge

as the demand for high wages as increased and it is getting difficult for them to recruit

them. Also, the exchange rate of UK with most of the countries is high which is making

difficult for them to export their goods in other countries. Inflation rate in UK is rising

again due to covid. So Next Plc need to look over at this factor also. As when inflation

rises, the prices goes up which affect the buying power of consumers (McCallig, Robb

and Rohde, 2019).

Social factors: This factor is also refer as demographic and cultural factors that affect

the environment on the basis of culture, buying pattern of consumers, ethnicity, religion

and many other factors. Next plc should focus upon ageing population of UK because

the needs and preferences of these people are different from younger population. Also,

the aged people will be more in number as compared to younger population. For them

they can use their online business model, where they can provide delivery of goods and

services at their doorstep. Also, younger population is more mobile when compared to

older population and they will use this online service which will be convenient for them.

Next plc need to focus upon ethnicity also, as there are different ethnic groups living

there. Different ethnic group have different taste and preferences and if they do not focus

on them, than they will not have competitive advantage. They also need to focus upon

other issues life lifestyle where they need to study the current consumption of the

consumers of UK.

Governmental factors: This factor refers to both political and legal factors that is

impacting the performance of the company in the market. For Next plc, they need to

look over the tax rate set up by the government as it keeps on changing every financial

year. Also, interest rate keeps on changing so they need to look over it as most of the

raw material comes from the Europe market. So if it increases it is good for them as they

will generate more profit and if it decreases it is not good for them as they need to pay

more which will result in less profit. They need to follow all the legal things set by

government which are environmental and health and safety of employees. They need to

protect their intellectual property rights because their designs will be copied which will

8

rate, unemployment and many other factors. In UK the unemployment rate is getting

reduce and it is good news for UK. But for big companies like Next Plc it is a challenge

as the demand for high wages as increased and it is getting difficult for them to recruit

them. Also, the exchange rate of UK with most of the countries is high which is making

difficult for them to export their goods in other countries. Inflation rate in UK is rising

again due to covid. So Next Plc need to look over at this factor also. As when inflation

rises, the prices goes up which affect the buying power of consumers (McCallig, Robb

and Rohde, 2019).

Social factors: This factor is also refer as demographic and cultural factors that affect

the environment on the basis of culture, buying pattern of consumers, ethnicity, religion

and many other factors. Next plc should focus upon ageing population of UK because

the needs and preferences of these people are different from younger population. Also,

the aged people will be more in number as compared to younger population. For them

they can use their online business model, where they can provide delivery of goods and

services at their doorstep. Also, younger population is more mobile when compared to

older population and they will use this online service which will be convenient for them.

Next plc need to focus upon ethnicity also, as there are different ethnic groups living

there. Different ethnic group have different taste and preferences and if they do not focus

on them, than they will not have competitive advantage. They also need to focus upon

other issues life lifestyle where they need to study the current consumption of the

consumers of UK.

Governmental factors: This factor refers to both political and legal factors that is

impacting the performance of the company in the market. For Next plc, they need to

look over the tax rate set up by the government as it keeps on changing every financial

year. Also, interest rate keeps on changing so they need to look over it as most of the

raw material comes from the Europe market. So if it increases it is good for them as they

will generate more profit and if it decreases it is not good for them as they need to pay

more which will result in less profit. They need to follow all the legal things set by

government which are environmental and health and safety of employees. They need to

protect their intellectual property rights because their designs will be copied which will

8

result in losing competitive advantage. They also need to protect rights of customer as

some customers have problem with the quality of the product so they need refund for it.

Also, while entering into new market they need to look up the legal environment of that

place as different countries have different laws (Pratt and Peters, 2017).

Recommendations

On the basis of the Ratio analysis and the ESG factors, several recommendations can be made.

The organisation, Next Plc can focus upon the trends in the economy in order to grab the

opportunities in order to enhance the market growth and capital of the organisation.

The organisation can keep a track of the recent political hindrances in the region that can

have an impact over the operational activities of the organisation. In order to keep a track

of the various political hindrances, the organisation and its management need to have

good awareness of the market.

Also, the organisation can look upon several legal formalities and obligations in order to

take benefits from the existing subsidiaries and tax concessions in the industry.

Next plc can focus upon the several trends in the market that are being favoured by the

customers in the market. This will help in attracting the customers towards the brand

outlets.

The organisation must focus upon its liquidity and profitability in order to develop and

sustain a positive brand image in the market. It can be done in consideration with the

assets and liabilities of the organisation (Yu, Lin and Tang, 2018).

Conclusion

It can be concluded from the report that Financial accounting plays a crucial role in the

organisation. Financial Accounting is referred as a branch of accounting that comprises of a

process of recording, analysing and summarising the reports. It can be concluded that ratio

analysis plays a crucial role in order to ascertain the financial position of the organisation. The

profitability and liquidity ratio have been calculated in the study along with the Economic, social

and governance factors that have an impact over the organisation. The report has recommended

few suggestions in order to improve the financial position of the organisation.

9

some customers have problem with the quality of the product so they need refund for it.

Also, while entering into new market they need to look up the legal environment of that

place as different countries have different laws (Pratt and Peters, 2017).

Recommendations

On the basis of the Ratio analysis and the ESG factors, several recommendations can be made.

The organisation, Next Plc can focus upon the trends in the economy in order to grab the

opportunities in order to enhance the market growth and capital of the organisation.

The organisation can keep a track of the recent political hindrances in the region that can

have an impact over the operational activities of the organisation. In order to keep a track

of the various political hindrances, the organisation and its management need to have

good awareness of the market.

Also, the organisation can look upon several legal formalities and obligations in order to

take benefits from the existing subsidiaries and tax concessions in the industry.

Next plc can focus upon the several trends in the market that are being favoured by the

customers in the market. This will help in attracting the customers towards the brand

outlets.

The organisation must focus upon its liquidity and profitability in order to develop and

sustain a positive brand image in the market. It can be done in consideration with the

assets and liabilities of the organisation (Yu, Lin and Tang, 2018).

Conclusion

It can be concluded from the report that Financial accounting plays a crucial role in the

organisation. Financial Accounting is referred as a branch of accounting that comprises of a

process of recording, analysing and summarising the reports. It can be concluded that ratio

analysis plays a crucial role in order to ascertain the financial position of the organisation. The

profitability and liquidity ratio have been calculated in the study along with the Economic, social

and governance factors that have an impact over the organisation. The report has recommended

few suggestions in order to improve the financial position of the organisation.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Books and Journals

Yu, T., Lin, Z. and Tang, Q., 2018. Blockchain: the introduction and its application in financial

accounting. Journal of Corporate Accounting & Finance, 29(4), pp.37-47.

Pratt, J. and Peters, M.F., 2017. Financial accounting in an economic context. John Wiley &

Sons.

McCallig, J., Robb, A. and Rohde, F., 2019. Establishing the representational faithfulness of

financial accounting information using multiparty security, network analysis and a

blockchain. International Journal of Accounting Information Systems, 33, pp.47-58.

Aksan, I., Setiawan, D. and Gantyowati, E., 2019. Research development related to

implementation of financial accounting standards in Indonesia. International Journal of

Economics, Business and Accounting Research (IJEBAR), 3(04).

Porter, J.C., 2019. Beyond debits and credits: Using integrated projects to improve students’

understanding of financial accounting. Journal of Accounting Education, 46, pp.53-71.

Lee, T.A., 2020. Financial accounting theory. In The Routledge companion to accounting

history (pp. 159-184). Routledge.

Demerjian, P.R., 2017. Calculating efficiency with financial accounting data: Data envelopment

analysis for accounting researchers. Available at SSRN 2993687.

10

Books and Journals

Yu, T., Lin, Z. and Tang, Q., 2018. Blockchain: the introduction and its application in financial

accounting. Journal of Corporate Accounting & Finance, 29(4), pp.37-47.

Pratt, J. and Peters, M.F., 2017. Financial accounting in an economic context. John Wiley &

Sons.

McCallig, J., Robb, A. and Rohde, F., 2019. Establishing the representational faithfulness of

financial accounting information using multiparty security, network analysis and a

blockchain. International Journal of Accounting Information Systems, 33, pp.47-58.

Aksan, I., Setiawan, D. and Gantyowati, E., 2019. Research development related to

implementation of financial accounting standards in Indonesia. International Journal of

Economics, Business and Accounting Research (IJEBAR), 3(04).

Porter, J.C., 2019. Beyond debits and credits: Using integrated projects to improve students’

understanding of financial accounting. Journal of Accounting Education, 46, pp.53-71.

Lee, T.A., 2020. Financial accounting theory. In The Routledge companion to accounting

history (pp. 159-184). Routledge.

Demerjian, P.R., 2017. Calculating efficiency with financial accounting data: Data envelopment

analysis for accounting researchers. Available at SSRN 2993687.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Appendix

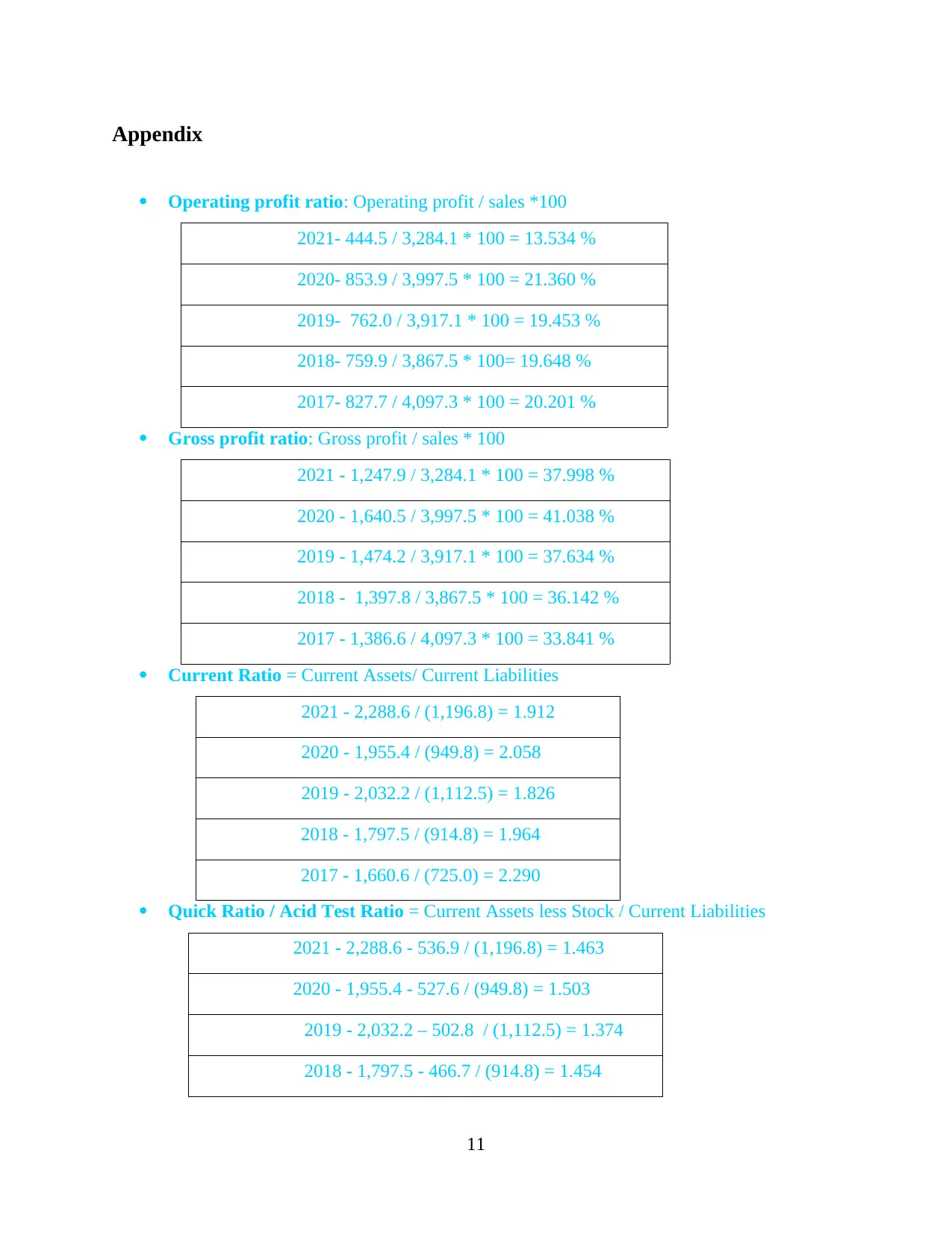

Operating profit ratio: Operating profit / sales *100

2021- 444.5 / 3,284.1 * 100 = 13.534 %

2020- 853.9 / 3,997.5 * 100 = 21.360 %

2019- 762.0 / 3,917.1 * 100 = 19.453 %

2018- 759.9 / 3,867.5 * 100= 19.648 %

2017- 827.7 / 4,097.3 * 100 = 20.201 %

Gross profit ratio: Gross profit / sales * 100

2021 - 1,247.9 / 3,284.1 * 100 = 37.998 %

2020 - 1,640.5 / 3,997.5 * 100 = 41.038 %

2019 - 1,474.2 / 3,917.1 * 100 = 37.634 %

2018 - 1,397.8 / 3,867.5 * 100 = 36.142 %

2017 - 1,386.6 / 4,097.3 * 100 = 33.841 %

Current Ratio = Current Assets/ Current Liabilities

2021 - 2,288.6 / (1,196.8) = 1.912

2020 - 1,955.4 / (949.8) = 2.058

2019 - 2,032.2 / (1,112.5) = 1.826

2018 - 1,797.5 / (914.8) = 1.964

2017 - 1,660.6 / (725.0) = 2.290

Quick Ratio / Acid Test Ratio = Current Assets less Stock / Current Liabilities

2021 - 2,288.6 - 536.9 / (1,196.8) = 1.463

2020 - 1,955.4 - 527.6 / (949.8) = 1.503

2019 - 2,032.2 – 502.8 / (1,112.5) = 1.374

2018 - 1,797.5 - 466.7 / (914.8) = 1.454

11

Operating profit ratio: Operating profit / sales *100

2021- 444.5 / 3,284.1 * 100 = 13.534 %

2020- 853.9 / 3,997.5 * 100 = 21.360 %

2019- 762.0 / 3,917.1 * 100 = 19.453 %

2018- 759.9 / 3,867.5 * 100= 19.648 %

2017- 827.7 / 4,097.3 * 100 = 20.201 %

Gross profit ratio: Gross profit / sales * 100

2021 - 1,247.9 / 3,284.1 * 100 = 37.998 %

2020 - 1,640.5 / 3,997.5 * 100 = 41.038 %

2019 - 1,474.2 / 3,917.1 * 100 = 37.634 %

2018 - 1,397.8 / 3,867.5 * 100 = 36.142 %

2017 - 1,386.6 / 4,097.3 * 100 = 33.841 %

Current Ratio = Current Assets/ Current Liabilities

2021 - 2,288.6 / (1,196.8) = 1.912

2020 - 1,955.4 / (949.8) = 2.058

2019 - 2,032.2 / (1,112.5) = 1.826

2018 - 1,797.5 / (914.8) = 1.964

2017 - 1,660.6 / (725.0) = 2.290

Quick Ratio / Acid Test Ratio = Current Assets less Stock / Current Liabilities

2021 - 2,288.6 - 536.9 / (1,196.8) = 1.463

2020 - 1,955.4 - 527.6 / (949.8) = 1.503

2019 - 2,032.2 – 502.8 / (1,112.5) = 1.374

2018 - 1,797.5 - 466.7 / (914.8) = 1.454

11

2017 - 1,660.6 – 451.1 / (725.0) = 1.668

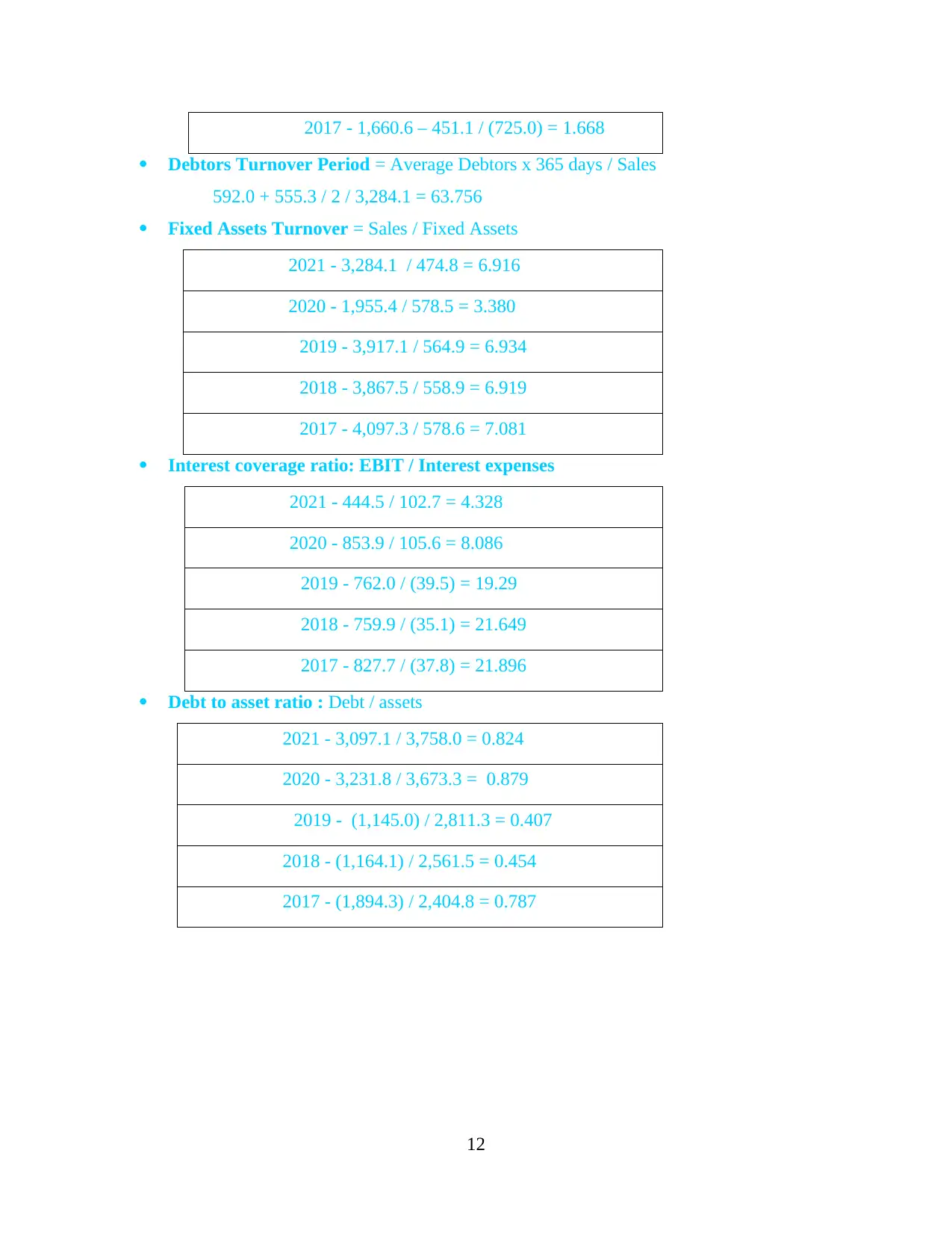

Debtors Turnover Period = Average Debtors x 365 days / Sales

592.0 + 555.3 / 2 / 3,284.1 = 63.756

Fixed Assets Turnover = Sales / Fixed Assets

2021 - 3,284.1 / 474.8 = 6.916

2020 - 1,955.4 / 578.5 = 3.380

2019 - 3,917.1 / 564.9 = 6.934

2018 - 3,867.5 / 558.9 = 6.919

2017 - 4,097.3 / 578.6 = 7.081

Interest coverage ratio: EBIT / Interest expenses

2021 - 444.5 / 102.7 = 4.328

2020 - 853.9 / 105.6 = 8.086

2019 - 762.0 / (39.5) = 19.29

2018 - 759.9 / (35.1) = 21.649

2017 - 827.7 / (37.8) = 21.896

Debt to asset ratio : Debt / assets

2021 - 3,097.1 / 3,758.0 = 0.824

2020 - 3,231.8 / 3,673.3 = 0.879

2019 - (1,145.0) / 2,811.3 = 0.407

2018 - (1,164.1) / 2,561.5 = 0.454

2017 - (1,894.3) / 2,404.8 = 0.787

12

Debtors Turnover Period = Average Debtors x 365 days / Sales

592.0 + 555.3 / 2 / 3,284.1 = 63.756

Fixed Assets Turnover = Sales / Fixed Assets

2021 - 3,284.1 / 474.8 = 6.916

2020 - 1,955.4 / 578.5 = 3.380

2019 - 3,917.1 / 564.9 = 6.934

2018 - 3,867.5 / 558.9 = 6.919

2017 - 4,097.3 / 578.6 = 7.081

Interest coverage ratio: EBIT / Interest expenses

2021 - 444.5 / 102.7 = 4.328

2020 - 853.9 / 105.6 = 8.086

2019 - 762.0 / (39.5) = 19.29

2018 - 759.9 / (35.1) = 21.649

2017 - 827.7 / (37.8) = 21.896

Debt to asset ratio : Debt / assets

2021 - 3,097.1 / 3,758.0 = 0.824

2020 - 3,231.8 / 3,673.3 = 0.879

2019 - (1,145.0) / 2,811.3 = 0.407

2018 - (1,164.1) / 2,561.5 = 0.454

2017 - (1,894.3) / 2,404.8 = 0.787

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.