Financial Accounting and Reporting: Ratio Analysis of Next PLC

VerifiedAdded on 2023/06/03

|15

|2578

|256

Report

AI Summary

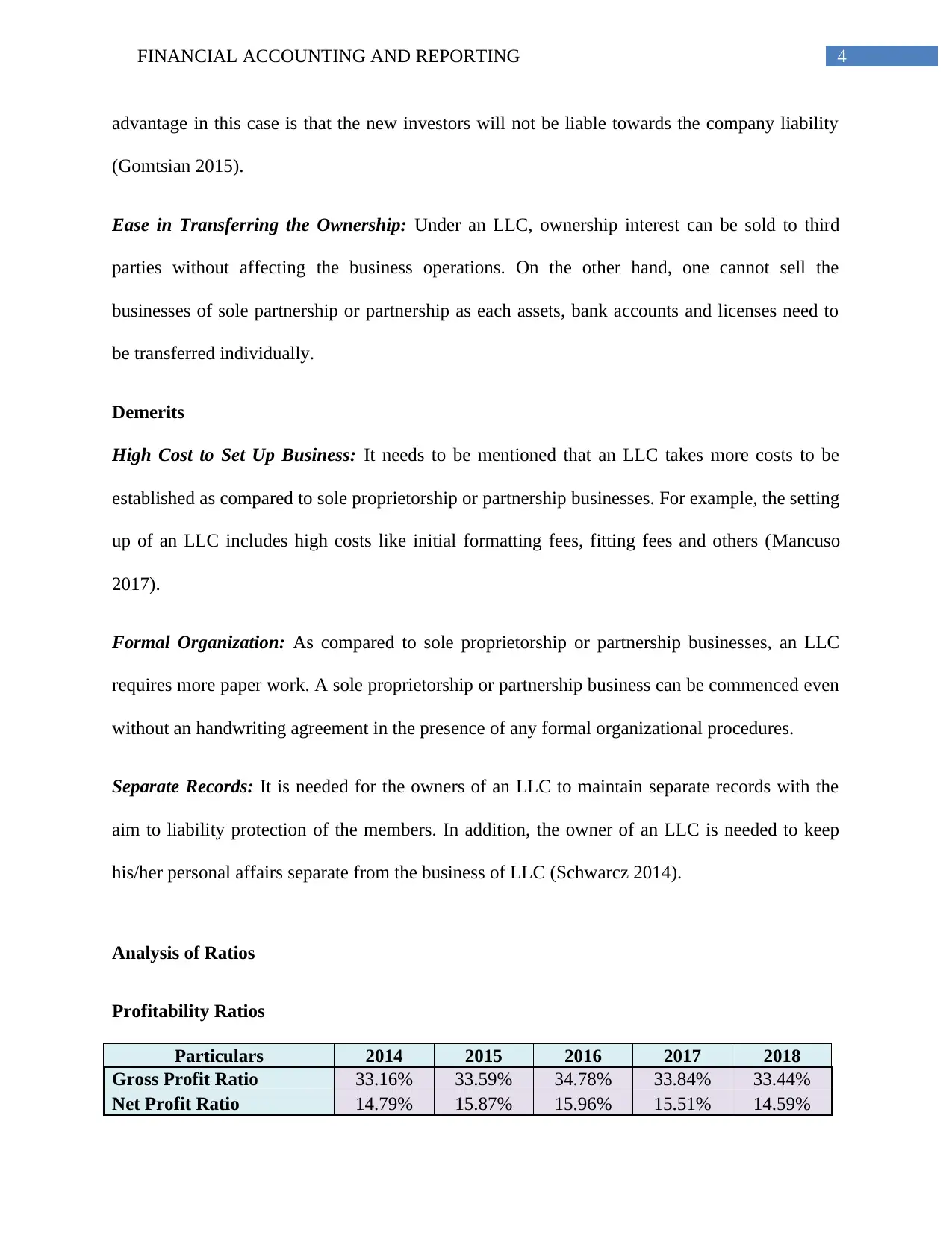

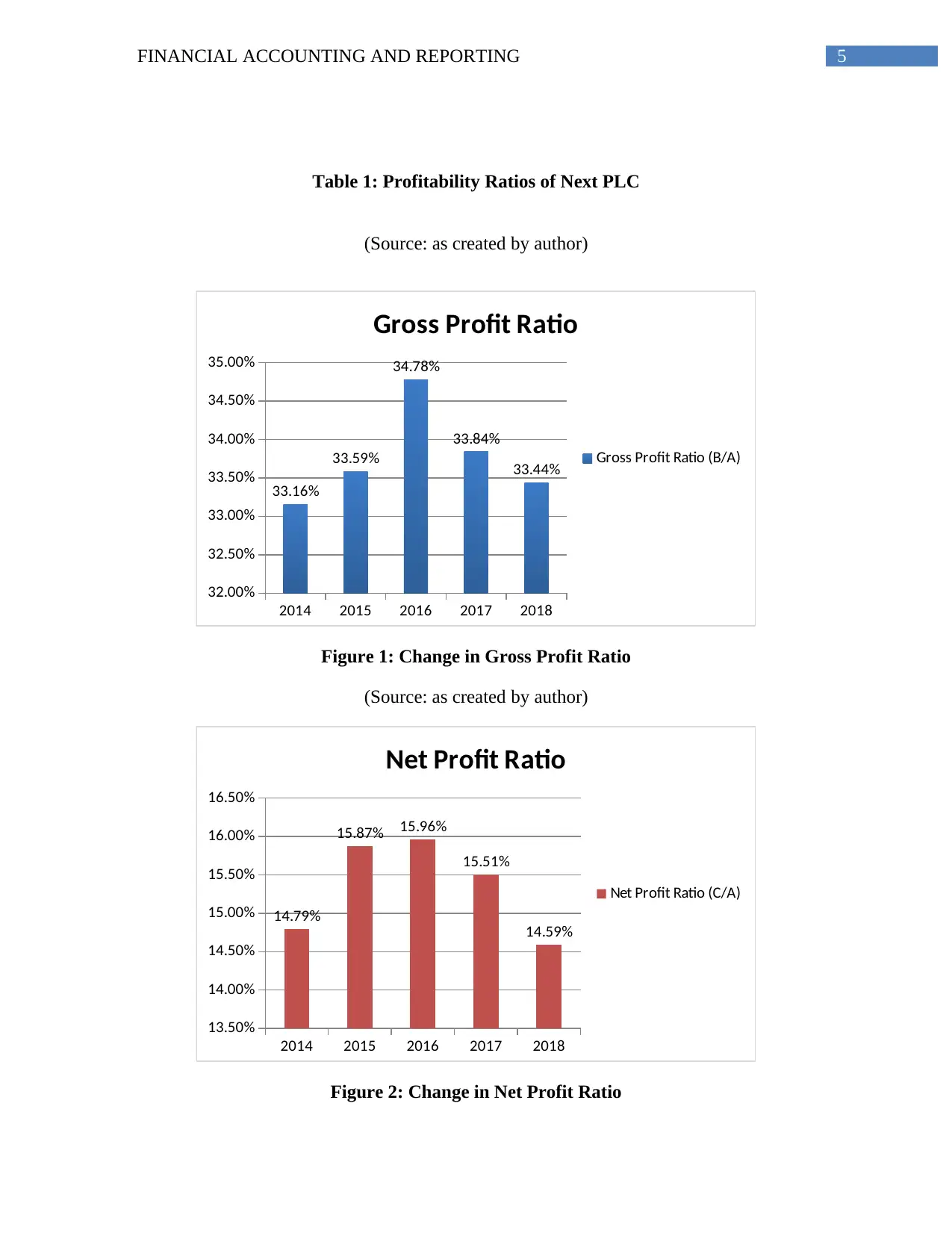

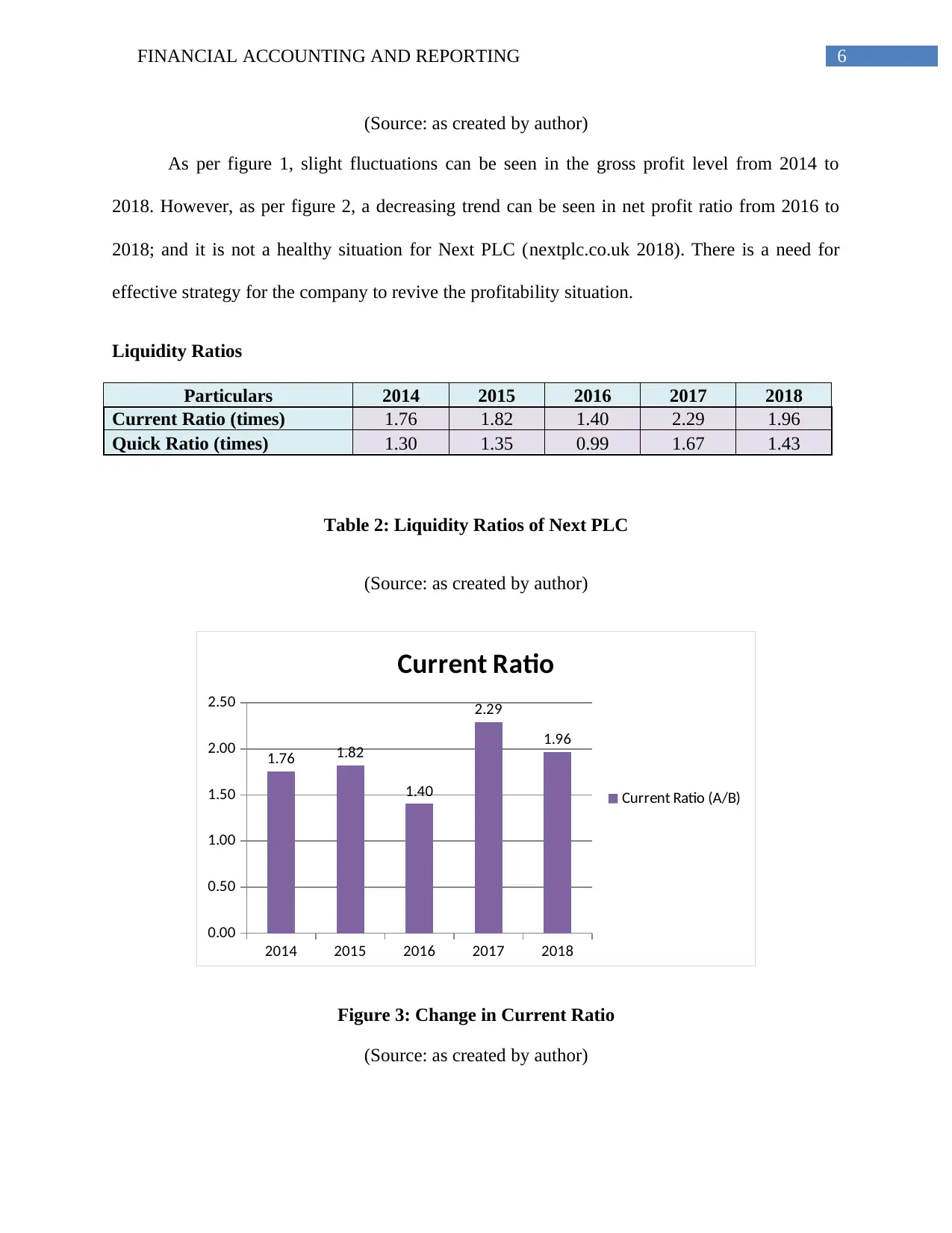

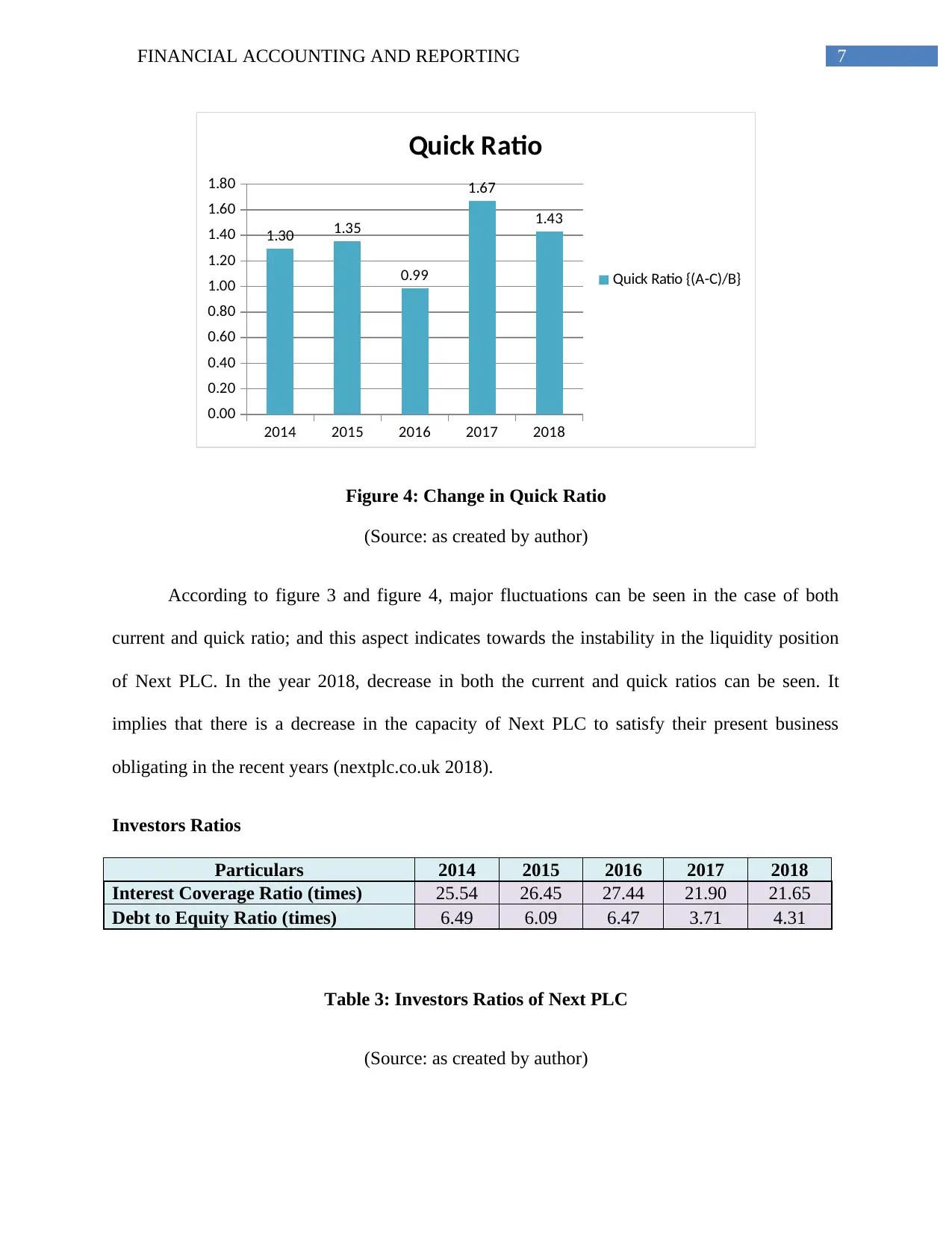

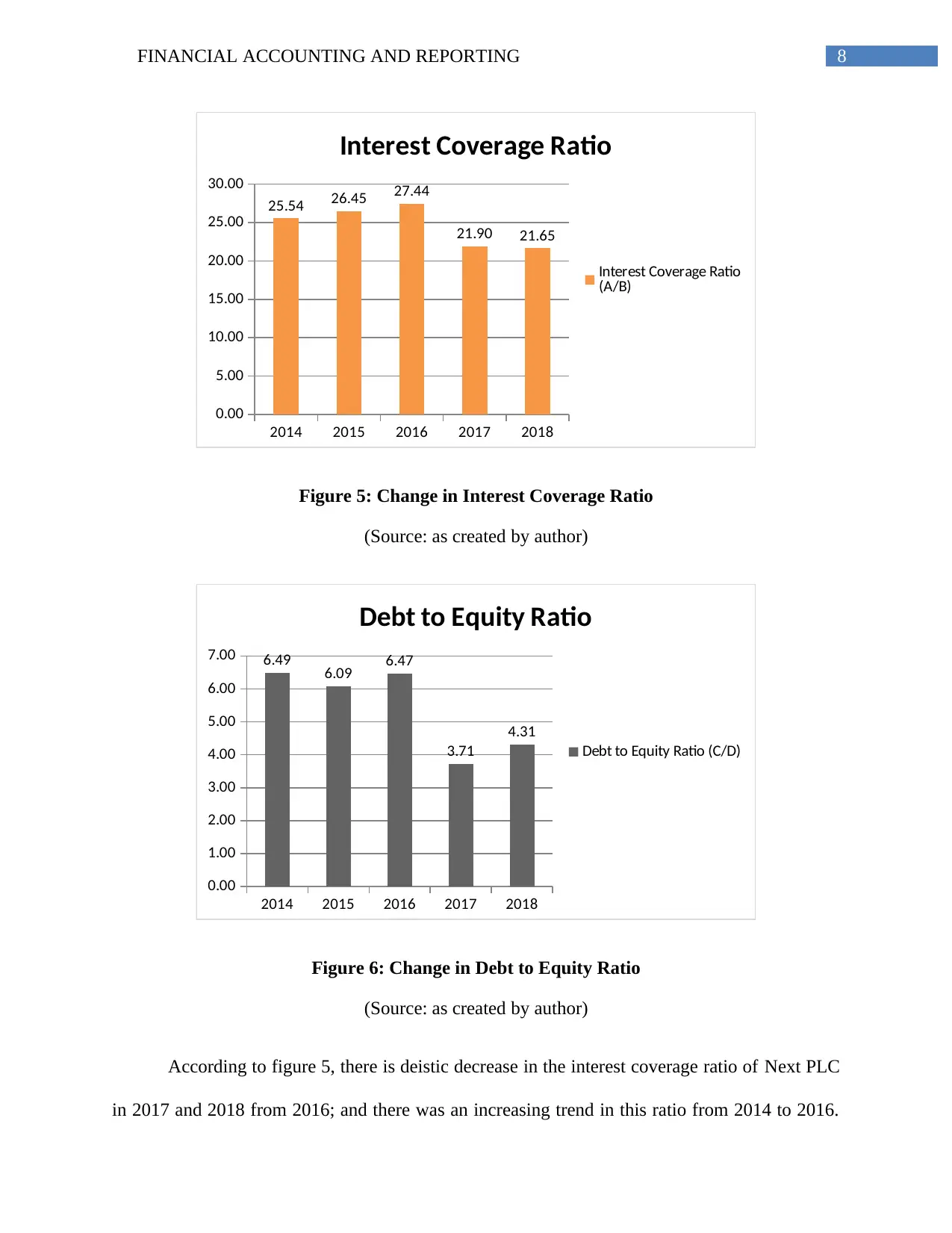

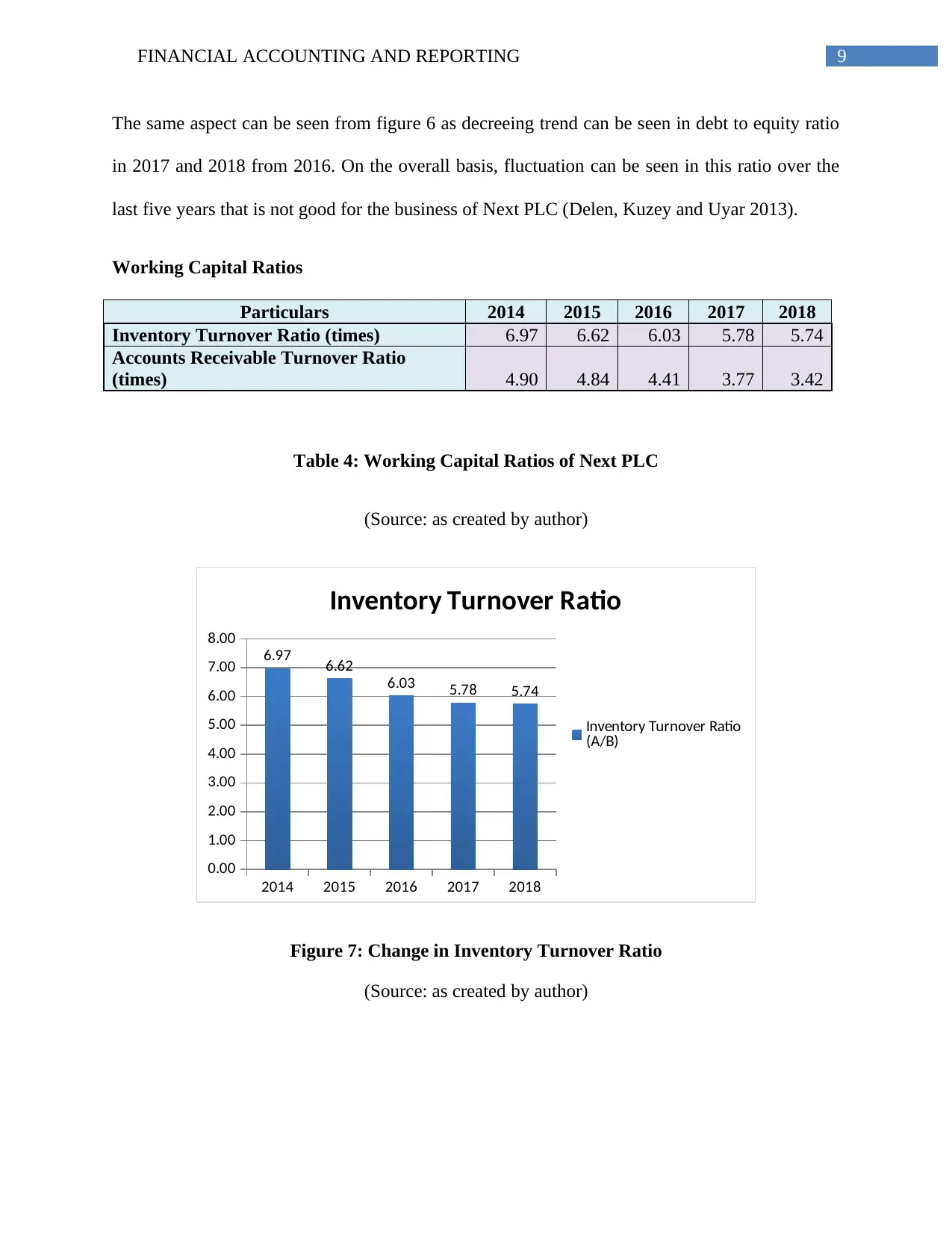

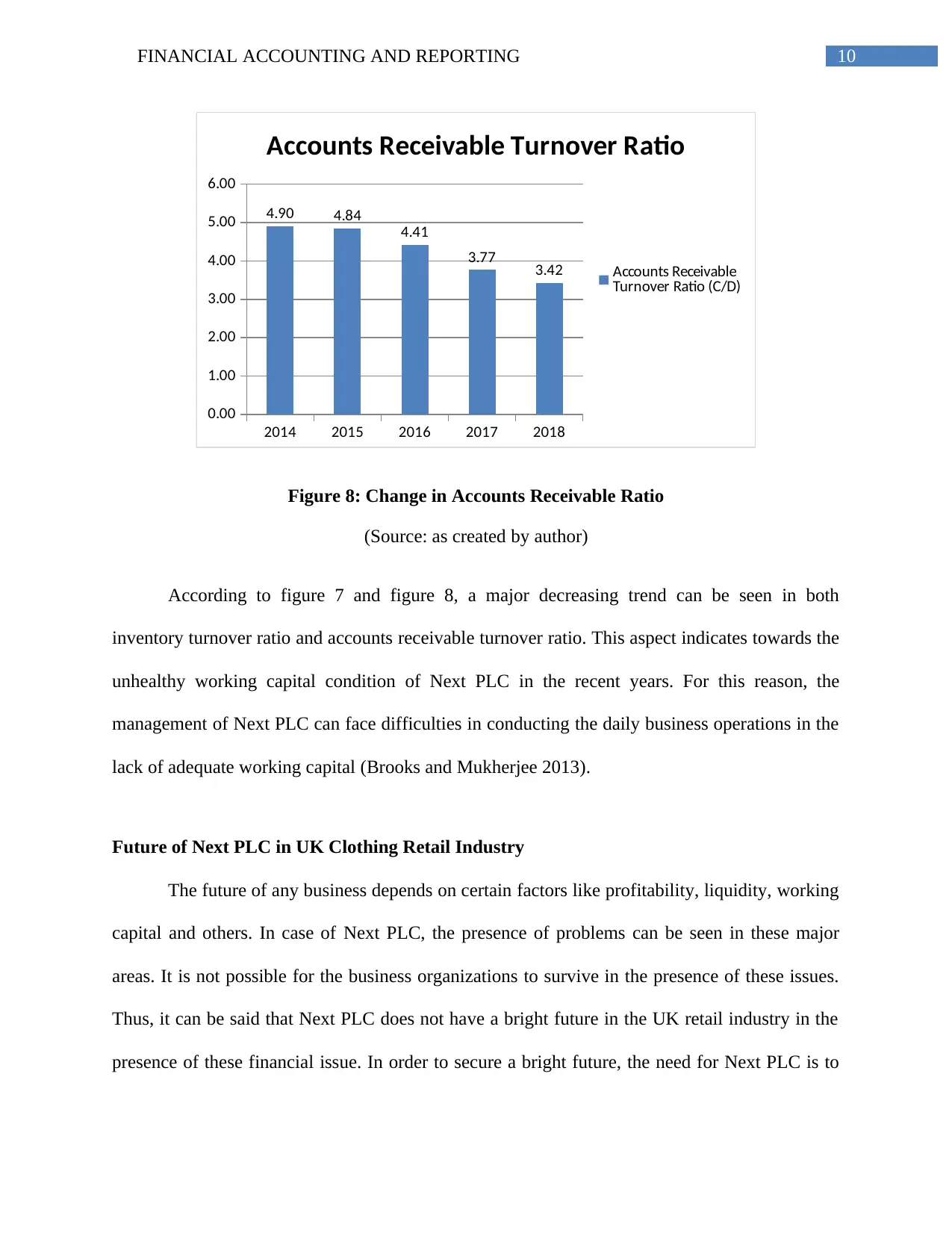

This report provides a financial analysis of Next PLC using various ratios, including profitability, liquidity, investor, and working capital ratios, derived from the company's financial statements. It also discusses the merits and demerits of Limited Liability Companies (LLC) compared to other business structures like sole proprietorships and partnerships, highlighting aspects such as liability, fundraising, and organizational structure. Based on the ratio analysis, the report offers specific recommendations to Next PLC's management to address financial issues, focusing on strategies to improve profitability, liquidity, and working capital management. The analysis suggests that Next PLC faces challenges in maintaining stable financial performance, impacting its future prospects in the UK clothing retail industry, and emphasizes the need for effective financial strategies to overcome these issues. Desklib provides access to this and other solved assignments to aid students in their studies.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.