Financial Analysis Report: Nextel Peru and Country Risk

VerifiedAdded on 2020/05/11

|9

|1546

|131

Report

AI Summary

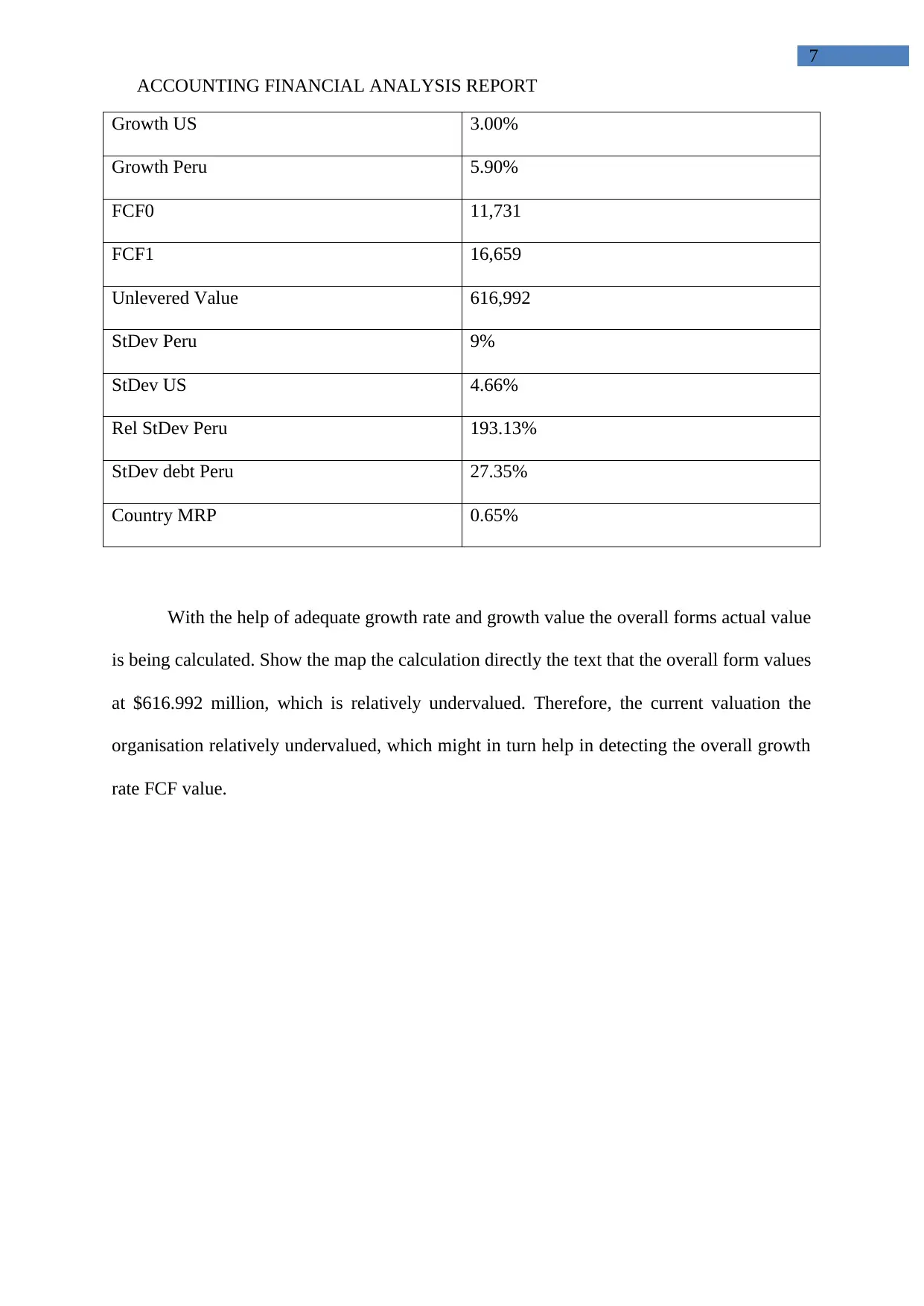

This financial analysis report delves into the valuation of Nextel Peru, examining its integration within global capital markets and the implications for country risk premiums. The report assesses the impact of Peru's operations in various countries on the organization's value, and analyzes the correlation between market factors and country risk premiums. It calculates Nextel Peru's asset beta, required return on assets, cost of capital, and long-range growth rate, using relevant financial data to determine the firm's value and whether it is undervalued or overvalued. The analysis incorporates key financial metrics like stock returns, bond yields, and growth rates to provide a comprehensive understanding of Nextel Peru's financial standing and market position. The report also references several academic sources to support its findings.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.