Report: Finance for Strategic Managers - NHS Financial Decision Making

VerifiedAdded on 2019/12/04

|15

|4784

|37

Report

AI Summary

This report provides a comprehensive analysis of finance for strategic managers, specifically within the context of the National Health Service (NHS). It begins by assessing the need for financial information in business operations, emphasizing its role in raising finance, supporting investment decisions, setting targets, managing risks, and satisfying stakeholder needs. The report then explores various business risks related to financial decisions, including market, operational, and compliance risks, and their potential impact on the NHS. It further outlines the financial information required for making strategic business decisions, such as income and expenditure, cash flow, and cash projections. The report also examines the purpose, structure, and content of published accounts, including formats like income statements and balance sheets, and how financial information can be interpreted using tools like ratio analysis. It discusses both long and short-term financial requirements, sources of finance, and cash flow management techniques. Additionally, the report covers business ownership structures, managerial roles in decision-making, and the evaluation of strategic capital or investment projects, including capital budgeting techniques. Overall, the report offers insights into how financial management supports strategic decision-making within the NHS.

Finance for Strategic

Managers

1

Managers

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction......................................................................................................................................3

Activity 1.........................................................................................................................................3

1. Assessment of why financial information is needed in business.............................................3

2. Business risks related to financial decisions............................................................................4

3. Summary of the financial information needed to make strategic business decisions..............5

ACTIVITY 2....................................................................................................................................5

1. Purpose, structure and content of published accounts.............................................................5

2. Interpretation of the financial information in these accounts..................................................7

3. Ratio Calculation.....................................................................................................................8

Activity 3.........................................................................................................................................9

1. Long and short-term financial requirements for businesses....................................................9

2. Sources of finance....................................................................................................................9

3. Cash flow management technique.........................................................................................10

ACTIVITY 4..................................................................................................................................10

1. Various business ownership structure, roles and accountability of owners and managers in

decision making.........................................................................................................................10

2. Evaluating methods for appraisal of strategic capital or investment projects.......................11

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................12

2

Introduction......................................................................................................................................3

Activity 1.........................................................................................................................................3

1. Assessment of why financial information is needed in business.............................................3

2. Business risks related to financial decisions............................................................................4

3. Summary of the financial information needed to make strategic business decisions..............5

ACTIVITY 2....................................................................................................................................5

1. Purpose, structure and content of published accounts.............................................................5

2. Interpretation of the financial information in these accounts..................................................7

3. Ratio Calculation.....................................................................................................................8

Activity 3.........................................................................................................................................9

1. Long and short-term financial requirements for businesses....................................................9

2. Sources of finance....................................................................................................................9

3. Cash flow management technique.........................................................................................10

ACTIVITY 4..................................................................................................................................10

1. Various business ownership structure, roles and accountability of owners and managers in

decision making.........................................................................................................................10

2. Evaluating methods for appraisal of strategic capital or investment projects.......................11

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................12

2

INTRODUCTION

Looking at the competitive environment of current corporate market managers have

various responsibility regarding carrying out the operations. In particular finance managers play

crucial role because he/she have authority and responsibility regarding managing the inflow and

outflow of funds within the company so that desired results and outcomes can be generated

(Duffy, 2000). Herein, researcher has undertaken the case of healthcare organisation which

requires proper management of money so that proper medical services can be given to the

patients. Therefore, investigator focuses on evaluating the need of financial information within

the NHS along with this, its financial position has been evaluated on the basis of ratio analysis.

Further, variance between short and long term economic requirement of business is illustrated

with the help of different cash flow management tools and their significances. Lastly, ownership

structure of structure and accountability of managerial level people in making decisions has been

understood and viability of project is computed through the capital budgeting techniques.

ACTIVITY 1

1. Assessment of why financial information is needed in business

To carry out the operations of business, varied information is required and especially

financial information so that managers can make smart and effective decisions. Following are the

financial information required by the managers of NHS: Raise finance: The main purpose of gathering information related to economic prospects

is to evaluate the need of funds or money within the NHS. Further, it assist in analyzing

the current position of NHS and if required managers can take potential measures

accordingly (Guzman, 2015). Furthermore, through the means of assessing the

information such as, firm's expenditures, revenues, operational performance, assets,

liabilities and owner's equity, finance manager of NHS can make smart decisions of the

raising the funds as well as the selecting the best suitable source. Supportive investment decisions: having adequate and proper financial information leads

to assist the managerial people to make smart and effective investment decisions.

However, it is because, for investing the fund managers should identify the position of

available funds which can be done only by assessing financial information. Herein, in-

3

Looking at the competitive environment of current corporate market managers have

various responsibility regarding carrying out the operations. In particular finance managers play

crucial role because he/she have authority and responsibility regarding managing the inflow and

outflow of funds within the company so that desired results and outcomes can be generated

(Duffy, 2000). Herein, researcher has undertaken the case of healthcare organisation which

requires proper management of money so that proper medical services can be given to the

patients. Therefore, investigator focuses on evaluating the need of financial information within

the NHS along with this, its financial position has been evaluated on the basis of ratio analysis.

Further, variance between short and long term economic requirement of business is illustrated

with the help of different cash flow management tools and their significances. Lastly, ownership

structure of structure and accountability of managerial level people in making decisions has been

understood and viability of project is computed through the capital budgeting techniques.

ACTIVITY 1

1. Assessment of why financial information is needed in business

To carry out the operations of business, varied information is required and especially

financial information so that managers can make smart and effective decisions. Following are the

financial information required by the managers of NHS: Raise finance: The main purpose of gathering information related to economic prospects

is to evaluate the need of funds or money within the NHS. Further, it assist in analyzing

the current position of NHS and if required managers can take potential measures

accordingly (Guzman, 2015). Furthermore, through the means of assessing the

information such as, firm's expenditures, revenues, operational performance, assets,

liabilities and owner's equity, finance manager of NHS can make smart decisions of the

raising the funds as well as the selecting the best suitable source. Supportive investment decisions: having adequate and proper financial information leads

to assist the managerial people to make smart and effective investment decisions.

However, it is because, for investing the fund managers should identify the position of

available funds which can be done only by assessing financial information. Herein, in-

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

depth analysis of profitability statement assist the managers in making smart decision

regarding use of reserves and surplus effectively. Setting and meeting targets: On the basis of current financial position, managers of NHS

set the future targets of business and accordingly employ the strategies to accomplish the

goals (Kaplan and Atkinson, 2015). Apart from monetary decision it is important for the

managers to organize meetings at regular intervals to assess the human resources needs

and wants which indeed are the integral part of NHS. Managing risks: NHS being of the biggest healthcare system in UK, needs to manage its

risks and uncertainties in every department. Thus, managers requires proper financial

information to manage all the risks associated with funding because without proper funds

NHS will be unable to provide superior quality of medical services to its patients. In

addition to it, to overcome technological failures and financial shortage as well as to meet

needs of changing environment, managers requires proper information (Ryan, 2009).

Furthermore, financial information assist managers in making use of available assists in

effective and efficient manner so that better revenue and profitability can be generated.

By the means of this risks associated with use of cash flows can be managed adequately

as well as future investment decisions can be taken appropriately.

Satisfying external and internal needs: In context to NHS, managers need such

information because it helps in satisfying internal and external need of business i.e.

employees, shareholders, suppliers, creditors, customers etc. Every stakeholder has its

own interest within the functioning of NHS, thus, providing them adequate and accurate

information will assist the course of stakeholders to make effective and smart decisions

regarding future contingency.

2. Business risks related to financial decisions

There are several risks and uncertainties associated with the NHS and it may directly

hamper the decisions related financial position. Thus, managerial level people require adequate

and accurate internal and external information to support their decisions so that hurdles and

hindrance can be avoided or mitigated. Market risk: In decision making process, market risk is considered as the most because

constantly changing environment of corporate world, companies facing various risks

4

regarding use of reserves and surplus effectively. Setting and meeting targets: On the basis of current financial position, managers of NHS

set the future targets of business and accordingly employ the strategies to accomplish the

goals (Kaplan and Atkinson, 2015). Apart from monetary decision it is important for the

managers to organize meetings at regular intervals to assess the human resources needs

and wants which indeed are the integral part of NHS. Managing risks: NHS being of the biggest healthcare system in UK, needs to manage its

risks and uncertainties in every department. Thus, managers requires proper financial

information to manage all the risks associated with funding because without proper funds

NHS will be unable to provide superior quality of medical services to its patients. In

addition to it, to overcome technological failures and financial shortage as well as to meet

needs of changing environment, managers requires proper information (Ryan, 2009).

Furthermore, financial information assist managers in making use of available assists in

effective and efficient manner so that better revenue and profitability can be generated.

By the means of this risks associated with use of cash flows can be managed adequately

as well as future investment decisions can be taken appropriately.

Satisfying external and internal needs: In context to NHS, managers need such

information because it helps in satisfying internal and external need of business i.e.

employees, shareholders, suppliers, creditors, customers etc. Every stakeholder has its

own interest within the functioning of NHS, thus, providing them adequate and accurate

information will assist the course of stakeholders to make effective and smart decisions

regarding future contingency.

2. Business risks related to financial decisions

There are several risks and uncertainties associated with the NHS and it may directly

hamper the decisions related financial position. Thus, managerial level people require adequate

and accurate internal and external information to support their decisions so that hurdles and

hindrance can be avoided or mitigated. Market risk: In decision making process, market risk is considered as the most because

constantly changing environment of corporate world, companies facing various risks

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

associated with it (Kevin and et. al, 2010). Further, NHS managers required to assess the

conditions of market appropriately so that they minimize the effect of risk on services and

operations. Herein, NHS management can take wrong decision regarding purchase of

new medical equipment. It is because if the machinery is unable to satisfy the needs and

wants of patients than it may possess high strategic risk for the NHS. Operational risk: It is considered as the most common risk in all because it is an

influencing risk that hampers the financial decisions of NHS managers. It is linked to the

internal process of the hospital functioning (Ryan, 2009). Present of such risk may affect

the course of services offered to the patients as well as create obstacle in growth and

development of certain departments of NHS. Herein, management of NHS invest in

building new CRM with the aim of maintaining long term relationship with patients. In

this case, if any breakdown occur in such software then it may leads to destroy all the

confidential information about patients as well as affect the band image of NHS.

Therefore, building and maintaining of CRM possess high monetary operational risk

upon the firm.

Compliance risk: There are various law and regulations that NHS has to comply in terms

of operating smoothly within the market. However, change in policies or regulations like

trade policies, health and safety regulations, taxation policy etc. may impact on the

financial decision of business (Schuster, 2007). In this regard, it is important for the

management of NHS to make sure that they are updated with compliance and legislation

so as to maintain the ethicality of business activities. By the means of this, senior

authority may reduce the risk of compliance associated with the activities of NHS.

3. Summary of the financial information needed to make strategic business decisions

Before making any strategic financial decisions it is important for the managerial level

people of NHS to gather appropriate information from the financial statements of the company

so that they can justify their decisions. Following are the wide range of information that is

required to make strategic business decisions: Income and expenditure: Being a non-profit organisation, NHS managers requires

adequate information regarding all the income generated and expenditure made during

the reporting period so that they can make strategic decisions such as raising funds,

5

conditions of market appropriately so that they minimize the effect of risk on services and

operations. Herein, NHS management can take wrong decision regarding purchase of

new medical equipment. It is because if the machinery is unable to satisfy the needs and

wants of patients than it may possess high strategic risk for the NHS. Operational risk: It is considered as the most common risk in all because it is an

influencing risk that hampers the financial decisions of NHS managers. It is linked to the

internal process of the hospital functioning (Ryan, 2009). Present of such risk may affect

the course of services offered to the patients as well as create obstacle in growth and

development of certain departments of NHS. Herein, management of NHS invest in

building new CRM with the aim of maintaining long term relationship with patients. In

this case, if any breakdown occur in such software then it may leads to destroy all the

confidential information about patients as well as affect the band image of NHS.

Therefore, building and maintaining of CRM possess high monetary operational risk

upon the firm.

Compliance risk: There are various law and regulations that NHS has to comply in terms

of operating smoothly within the market. However, change in policies or regulations like

trade policies, health and safety regulations, taxation policy etc. may impact on the

financial decision of business (Schuster, 2007). In this regard, it is important for the

management of NHS to make sure that they are updated with compliance and legislation

so as to maintain the ethicality of business activities. By the means of this, senior

authority may reduce the risk of compliance associated with the activities of NHS.

3. Summary of the financial information needed to make strategic business decisions

Before making any strategic financial decisions it is important for the managerial level

people of NHS to gather appropriate information from the financial statements of the company

so that they can justify their decisions. Following are the wide range of information that is

required to make strategic business decisions: Income and expenditure: Being a non-profit organisation, NHS managers requires

adequate information regarding all the income generated and expenditure made during

the reporting period so that they can make strategic decisions such as raising funds,

5

introducing of new medical equipment’s etc (Barrett, 2007). The income side of this

statement assist in illustrating the revenue generated by the NHS during the course of

accounting period. While on the other hand, the expenditure made by the NHS will be

stated in the expenditure side of the statement. The main purpose of this statement is to

cut down the unnecessary expenditure which may cause decrease of profit. Along with

this, managerial people of NHS can make out growth prospects through the means of

Income statement. Cash inflow and outflow: The main purpose behind evaluating inflow and outflow of

funds is that it helps in developing suitable base for investment related decisions.

However, as per the data on cash available, managers can easily make the future

investment decisions. Furthermore, cash flow statement clearly reflects the operating,

financing and investment activities of business separately. By the means of this,

managers of NHS can make reliable and suitable investment and financial decisions.

Cash projections: Forecasting of cash or cash equivalents is based on the budgeting or

other forecasting techniques. The main purpose of projecting cash is to evaluate the

reliable source of funding so that desired selection can be made that can fulfil the needs

and expectations. In order to review the financial position of different department

financial statements are assessed or reviewed (Sofat and Hiro, 2011). Furthermore,

Profitability position of business assist in encouraging mangers to make more investment

in near future so that they can take steps to enhance the business functioning and expand

the different portfolios of the business.

ACTIVITY 2

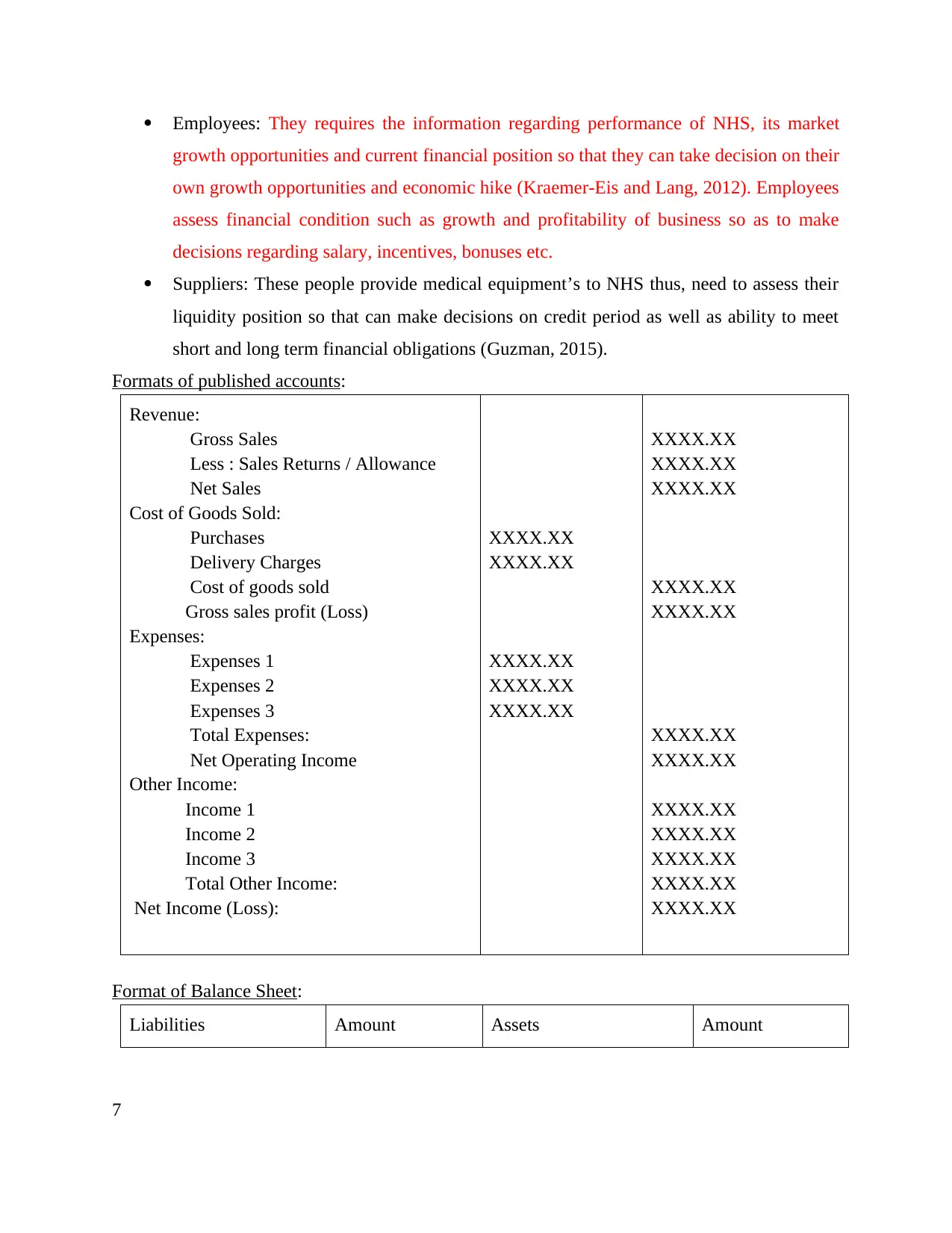

1. Purpose, structure and content of published accounts

Company publish its account to provide wide range of accurate and reliable information

to different stakeholders.

Investors: Investors of NHS requires the information relating to profitability position,

liquidity earnings of the company, solvency position and goodwill so that they can make

decisions regarding future investments. In this, investors assess the ability of firm on the

basis of return on equity and return on investment so that reliability of future investment

can be evaluated properly and accordingly smart decisions can be made.

6

statement assist in illustrating the revenue generated by the NHS during the course of

accounting period. While on the other hand, the expenditure made by the NHS will be

stated in the expenditure side of the statement. The main purpose of this statement is to

cut down the unnecessary expenditure which may cause decrease of profit. Along with

this, managerial people of NHS can make out growth prospects through the means of

Income statement. Cash inflow and outflow: The main purpose behind evaluating inflow and outflow of

funds is that it helps in developing suitable base for investment related decisions.

However, as per the data on cash available, managers can easily make the future

investment decisions. Furthermore, cash flow statement clearly reflects the operating,

financing and investment activities of business separately. By the means of this,

managers of NHS can make reliable and suitable investment and financial decisions.

Cash projections: Forecasting of cash or cash equivalents is based on the budgeting or

other forecasting techniques. The main purpose of projecting cash is to evaluate the

reliable source of funding so that desired selection can be made that can fulfil the needs

and expectations. In order to review the financial position of different department

financial statements are assessed or reviewed (Sofat and Hiro, 2011). Furthermore,

Profitability position of business assist in encouraging mangers to make more investment

in near future so that they can take steps to enhance the business functioning and expand

the different portfolios of the business.

ACTIVITY 2

1. Purpose, structure and content of published accounts

Company publish its account to provide wide range of accurate and reliable information

to different stakeholders.

Investors: Investors of NHS requires the information relating to profitability position,

liquidity earnings of the company, solvency position and goodwill so that they can make

decisions regarding future investments. In this, investors assess the ability of firm on the

basis of return on equity and return on investment so that reliability of future investment

can be evaluated properly and accordingly smart decisions can be made.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Employees: They requires the information regarding performance of NHS, its market

growth opportunities and current financial position so that they can take decision on their

own growth opportunities and economic hike (Kraemer-Eis and Lang, 2012). Employees

assess financial condition such as growth and profitability of business so as to make

decisions regarding salary, incentives, bonuses etc.

Suppliers: These people provide medical equipment’s to NHS thus, need to assess their

liquidity position so that can make decisions on credit period as well as ability to meet

short and long term financial obligations (Guzman, 2015).

Formats of published accounts:

Revenue:

Gross Sales

Less : Sales Returns / Allowance

Net Sales

Cost of Goods Sold:

Purchases

Delivery Charges

Cost of goods sold

Gross sales profit (Loss)

Expenses:

Expenses 1

Expenses 2

Expenses 3

Total Expenses:

Net Operating Income

Other Income:

Income 1

Income 2

Income 3

Total Other Income:

Net Income (Loss):

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

Format of Balance Sheet:

Liabilities Amount Assets Amount

7

growth opportunities and current financial position so that they can take decision on their

own growth opportunities and economic hike (Kraemer-Eis and Lang, 2012). Employees

assess financial condition such as growth and profitability of business so as to make

decisions regarding salary, incentives, bonuses etc.

Suppliers: These people provide medical equipment’s to NHS thus, need to assess their

liquidity position so that can make decisions on credit period as well as ability to meet

short and long term financial obligations (Guzman, 2015).

Formats of published accounts:

Revenue:

Gross Sales

Less : Sales Returns / Allowance

Net Sales

Cost of Goods Sold:

Purchases

Delivery Charges

Cost of goods sold

Gross sales profit (Loss)

Expenses:

Expenses 1

Expenses 2

Expenses 3

Total Expenses:

Net Operating Income

Other Income:

Income 1

Income 2

Income 3

Total Other Income:

Net Income (Loss):

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

Format of Balance Sheet:

Liabilities Amount Assets Amount

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

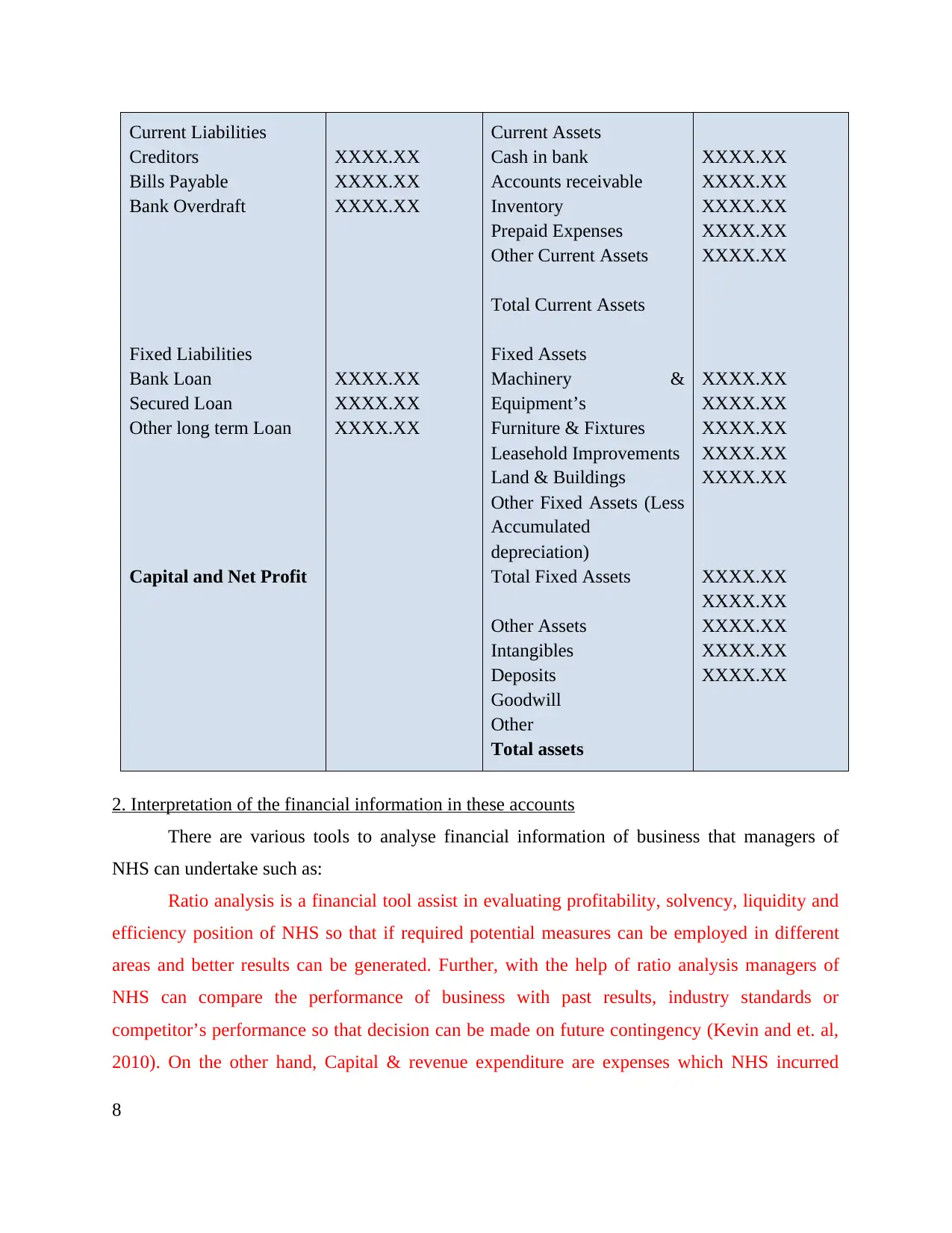

Current Liabilities

Creditors

Bills Payable

Bank Overdraft

Fixed Liabilities

Bank Loan

Secured Loan

Other long term Loan

Capital and Net Profit

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

Current Assets

Cash in bank

Accounts receivable

Inventory

Prepaid Expenses

Other Current Assets

Total Current Assets

Fixed Assets

Machinery &

Equipment’s

Furniture & Fixtures

Leasehold Improvements

Land & Buildings

Other Fixed Assets (Less

Accumulated

depreciation)

Total Fixed Assets

Other Assets

Intangibles

Deposits

Goodwill

Other

Total assets

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

2. Interpretation of the financial information in these accounts

There are various tools to analyse financial information of business that managers of

NHS can undertake such as:

Ratio analysis is a financial tool assist in evaluating profitability, solvency, liquidity and

efficiency position of NHS so that if required potential measures can be employed in different

areas and better results can be generated. Further, with the help of ratio analysis managers of

NHS can compare the performance of business with past results, industry standards or

competitor’s performance so that decision can be made on future contingency (Kevin and et. al,

2010). On the other hand, Capital & revenue expenditure are expenses which NHS incurred

8

Creditors

Bills Payable

Bank Overdraft

Fixed Liabilities

Bank Loan

Secured Loan

Other long term Loan

Capital and Net Profit

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

Current Assets

Cash in bank

Accounts receivable

Inventory

Prepaid Expenses

Other Current Assets

Total Current Assets

Fixed Assets

Machinery &

Equipment’s

Furniture & Fixtures

Leasehold Improvements

Land & Buildings

Other Fixed Assets (Less

Accumulated

depreciation)

Total Fixed Assets

Other Assets

Intangibles

Deposits

Goodwill

Other

Total assets

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

2. Interpretation of the financial information in these accounts

There are various tools to analyse financial information of business that managers of

NHS can undertake such as:

Ratio analysis is a financial tool assist in evaluating profitability, solvency, liquidity and

efficiency position of NHS so that if required potential measures can be employed in different

areas and better results can be generated. Further, with the help of ratio analysis managers of

NHS can compare the performance of business with past results, industry standards or

competitor’s performance so that decision can be made on future contingency (Kevin and et. al,

2010). On the other hand, Capital & revenue expenditure are expenses which NHS incurred

8

while acquiring fixed assets. In this, costs related to buying of machinery, legal and registration

charges, delivery charges etc. All these expenditures are recorded in balance sheet of NHS

(Srinivasan, 2012).

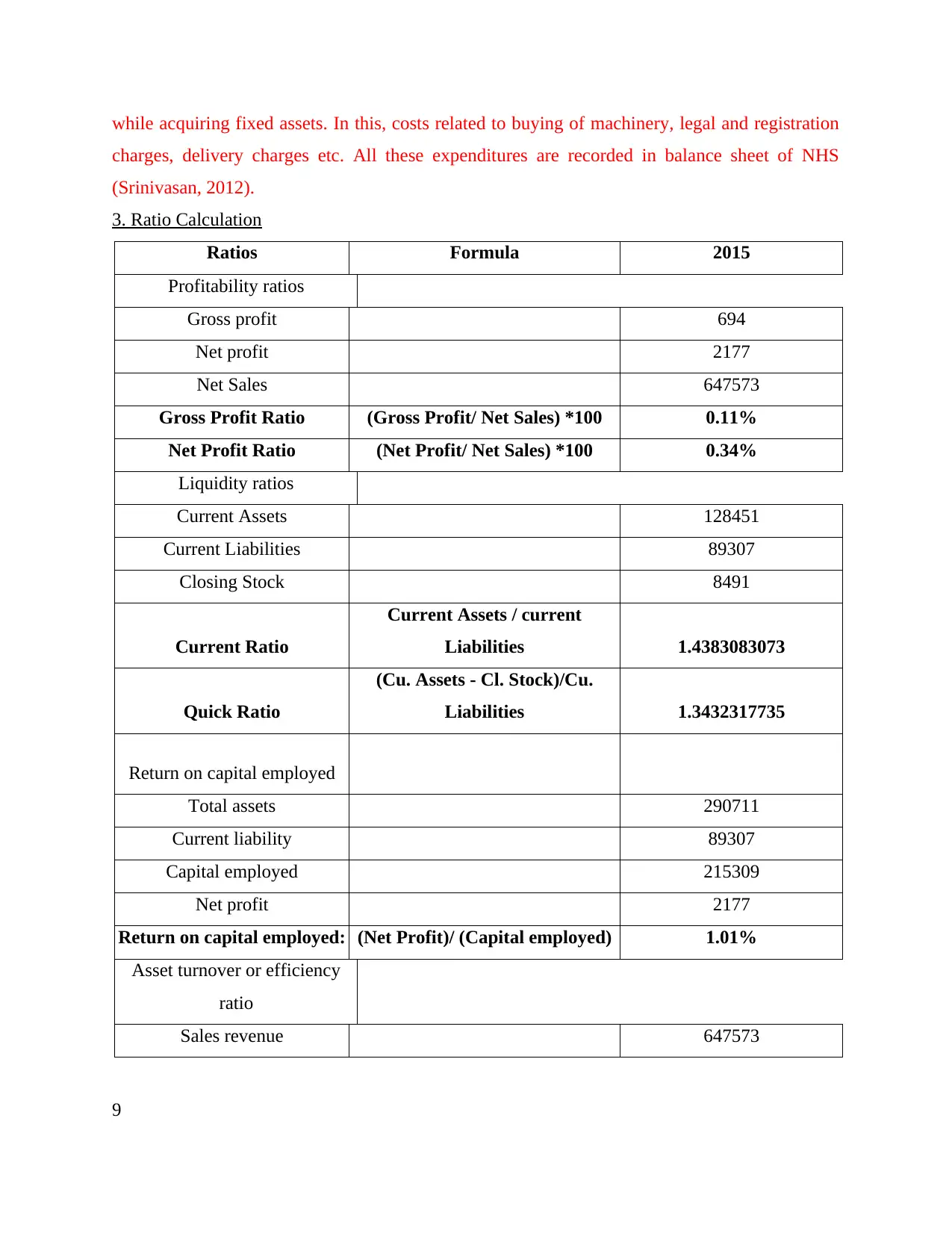

3. Ratio Calculation

Ratios Formula 2015

Profitability ratios

Gross profit 694

Net profit 2177

Net Sales 647573

Gross Profit Ratio (Gross Profit/ Net Sales) *100 0.11%

Net Profit Ratio (Net Profit/ Net Sales) *100 0.34%

Liquidity ratios

Current Assets 128451

Current Liabilities 89307

Closing Stock 8491

Current Ratio

Current Assets / current

Liabilities 1.4383083073

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities 1.3432317735

Return on capital employed

Total assets 290711

Current liability 89307

Capital employed 215309

Net profit 2177

Return on capital employed: (Net Profit)/ (Capital employed) 1.01%

Asset turnover or efficiency

ratio

Sales revenue 647573

9

charges, delivery charges etc. All these expenditures are recorded in balance sheet of NHS

(Srinivasan, 2012).

3. Ratio Calculation

Ratios Formula 2015

Profitability ratios

Gross profit 694

Net profit 2177

Net Sales 647573

Gross Profit Ratio (Gross Profit/ Net Sales) *100 0.11%

Net Profit Ratio (Net Profit/ Net Sales) *100 0.34%

Liquidity ratios

Current Assets 128451

Current Liabilities 89307

Closing Stock 8491

Current Ratio

Current Assets / current

Liabilities 1.4383083073

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities 1.3432317735

Return on capital employed

Total assets 290711

Current liability 89307

Capital employed 215309

Net profit 2177

Return on capital employed: (Net Profit)/ (Capital employed) 1.01%

Asset turnover or efficiency

ratio

Sales revenue 647573

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total asset 290711

Asset turnover ratio Sales revenue / Total assets 2.2275490092

Interpretation:

On the basis of above computation of ratio analysis it has been evaluated that,

profitability position of NHS is not good because it offers free of cost medical services to its

patients as well as it is a non-profit organisation. Further, GP of 0.11% and NP of 0.34% clearly

indicates that despite of being a NPO, management is able to cover all its expenses from its

operational performance. Further, liquidity position of NHS is showing better results which

indicates the capability of firm in meeting its short term financial obligations through its current

assets. However, current ratio and quick ratio of NHS is 1.43 and 1.34 respectively. In terms of

efficiency ratio illustrates that, managers of the NHS are making effective use of its assets in

terms of generating higher sales so that they can overcome short and long term assets.

ACTIVITY 3

1. Long and short-term financial requirements for businesses

Financial need takes place in every kind of organization. It is categorized into two that

includes short term and long term. Short term finance is essential so as to meet daily

requirements of the business and this is also useful for the purpose of managing business

liquidity. Every business has to incur several expenditure; therefore it is necessary to have proper

cash reserve ratio (Palepu and Healy, 2007). Hence, with the help of such sources, NHS will be

able to manage all the small scale operations and expenses in optimum manner. For instance

every firm needs to make purchase of material, pay wages, rent, and advertisement expense and

stationery charges. Therefore in order to meet such adequate amount of funds are needed by firm

which is referred to as short term financing.

In contrast to this, Long term financing methods can be used in the case if the business

entity desires to attain long term aims and objectives. As per the source, management can

generate financial assistance through emphasizing more on long terms projects (Hershey, Austin

and Gutierrez, 2015). Long term finance is essential for the purpose of purchasing land,

machinery and also in the areas where huge investment is required. Corporate bonds, equity

funding, loans, retained earnings and selling of fixed assets are some of the sources through

10

Asset turnover ratio Sales revenue / Total assets 2.2275490092

Interpretation:

On the basis of above computation of ratio analysis it has been evaluated that,

profitability position of NHS is not good because it offers free of cost medical services to its

patients as well as it is a non-profit organisation. Further, GP of 0.11% and NP of 0.34% clearly

indicates that despite of being a NPO, management is able to cover all its expenses from its

operational performance. Further, liquidity position of NHS is showing better results which

indicates the capability of firm in meeting its short term financial obligations through its current

assets. However, current ratio and quick ratio of NHS is 1.43 and 1.34 respectively. In terms of

efficiency ratio illustrates that, managers of the NHS are making effective use of its assets in

terms of generating higher sales so that they can overcome short and long term assets.

ACTIVITY 3

1. Long and short-term financial requirements for businesses

Financial need takes place in every kind of organization. It is categorized into two that

includes short term and long term. Short term finance is essential so as to meet daily

requirements of the business and this is also useful for the purpose of managing business

liquidity. Every business has to incur several expenditure; therefore it is necessary to have proper

cash reserve ratio (Palepu and Healy, 2007). Hence, with the help of such sources, NHS will be

able to manage all the small scale operations and expenses in optimum manner. For instance

every firm needs to make purchase of material, pay wages, rent, and advertisement expense and

stationery charges. Therefore in order to meet such adequate amount of funds are needed by firm

which is referred to as short term financing.

In contrast to this, Long term financing methods can be used in the case if the business

entity desires to attain long term aims and objectives. As per the source, management can

generate financial assistance through emphasizing more on long terms projects (Hershey, Austin

and Gutierrez, 2015). Long term finance is essential for the purpose of purchasing land,

machinery and also in the areas where huge investment is required. Corporate bonds, equity

funding, loans, retained earnings and selling of fixed assets are some of the sources through

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which financial arrangement can be made. The organization need to purchase the assets such as

property, plant and equipments. For this sake it requires long term finance. Hence, it can be said

that both the sources are essential for the business entity and through such sources, NHS will be

able to conduct all the practices in adequate manner.

2. Sources of finance

There are various sources of funds available with NHS such as internal, external and

other and from all such sources, NHS could manage all the necessary activities and operations.

Short term finance sources Long term finance sources

Short term finance sources are the one where

in NHS can raise money with the help of

personal capital and retained earnings. Short

term finance source should be utilized in

optimum manner so that investment capacity

of the entity can be generated. In order to

deliver quality services to the patients, it is

essential for NHS to have basic services and

such services can only be delivered if NHS has

the arrangement of short term modes of

financing (Nobes, 2014).

Retained earning: Under this NHS can make

use of funds that are available with it. Through

this it can meet it short term requirements for

funds in an effective manner.

Bank overdraft: It is regarded as the facility

wherein the firm can withdraw greater amount

in comparison with the balance that exists in

the account of an individual. It acts as an aid in

mitigating the emergency need for funds.

Long term finance sources are useful in the

case where in large amount of investment is

required for business processes. Bank loan,

borrowings and leasing can be taken in this

case. Moreover, NHS can also manage long

term projects through selling its assets and also

through acquiring assistance from investors

(Chand, 2015). This sources are useful for

NHS for retaining its position in health care

sector.

Bank loan: Loan for bank is offered for fix

duration of time and it is regarded as the most

suitable financial source that assist in meeting

the long term need for funds. Under this

organization is required to make payment of

interest on time.

Leasing: In this NHS can take assets for

certain duration of time for which is required

to make payment of rent. This is beneficial is

terms when the cost of assets is greater than

rental price.

11

property, plant and equipments. For this sake it requires long term finance. Hence, it can be said

that both the sources are essential for the business entity and through such sources, NHS will be

able to conduct all the practices in adequate manner.

2. Sources of finance

There are various sources of funds available with NHS such as internal, external and

other and from all such sources, NHS could manage all the necessary activities and operations.

Short term finance sources Long term finance sources

Short term finance sources are the one where

in NHS can raise money with the help of

personal capital and retained earnings. Short

term finance source should be utilized in

optimum manner so that investment capacity

of the entity can be generated. In order to

deliver quality services to the patients, it is

essential for NHS to have basic services and

such services can only be delivered if NHS has

the arrangement of short term modes of

financing (Nobes, 2014).

Retained earning: Under this NHS can make

use of funds that are available with it. Through

this it can meet it short term requirements for

funds in an effective manner.

Bank overdraft: It is regarded as the facility

wherein the firm can withdraw greater amount

in comparison with the balance that exists in

the account of an individual. It acts as an aid in

mitigating the emergency need for funds.

Long term finance sources are useful in the

case where in large amount of investment is

required for business processes. Bank loan,

borrowings and leasing can be taken in this

case. Moreover, NHS can also manage long

term projects through selling its assets and also

through acquiring assistance from investors

(Chand, 2015). This sources are useful for

NHS for retaining its position in health care

sector.

Bank loan: Loan for bank is offered for fix

duration of time and it is regarded as the most

suitable financial source that assist in meeting

the long term need for funds. Under this

organization is required to make payment of

interest on time.

Leasing: In this NHS can take assets for

certain duration of time for which is required

to make payment of rent. This is beneficial is

terms when the cost of assets is greater than

rental price.

11

3. Cash flow management technique

Cash flow statement is useful in managing all the organizational operations in effectual

manner and through this, expenditures can also be recorded in optimum manner. NHS can record

all the expenses and income with the help of cash flow management and this further investment

can also be made (Liao, 2013). Cash flow statement could assist NHS to identify the all those

functions through which stable income can be acquired for the business entity. NHS should have

to emphasize on increasing the ratio of working capital so that patients can be treated with

effective services with latest technology. Moreover, NHS can also focus on budgeting technique

in which every aspect of health care entity could be managed according to inflow and outflow of

funds. Firm cannot survive without availability of adequate amount of cash. It is important for

the manager to keep the cash flow management of organization's inflow and outflow. Further

they needs to ensure surplus cash available for the business activities. Project cash flow is

regarded as the tool that assists in administrating cash flow within the firm. In accordance with

the tool manager needs to make determination of the potential earning for future and make

efforts in order to attain this. They would make sure that actual expenses would not exceed the

set maximum limit by the means of controlling and monitoring. In addition to this improvement

in the receivable days as well as management of payables acts as an aid in enhancing the balance

of cash. It assist in efficient resource allocation in several operating activities. Along with this

they develop sales target and makes efforts in achieving them by the means of constructing

several policies. Therefore organization would be able to possess surplus net cash available and

carry out business activities in an effective manner.

ACTIVITY 4

1. Various business ownership structure, roles and accountability of owners and managers in

decision making Ownership structure: There is presence of three types of business structure that possess

their own requirement of financials as well as various responsibilities of demonstrating

financial information. The structure of the firm involves sole trader, limited company as

well as partnership. In case of sole trade single person owns and manages the firm. He

makes investment of his own funds for the purpose of generating income. On the other

hand partnership is regarded as the association among two or more individuals in which

12

Cash flow statement is useful in managing all the organizational operations in effectual

manner and through this, expenditures can also be recorded in optimum manner. NHS can record

all the expenses and income with the help of cash flow management and this further investment

can also be made (Liao, 2013). Cash flow statement could assist NHS to identify the all those

functions through which stable income can be acquired for the business entity. NHS should have

to emphasize on increasing the ratio of working capital so that patients can be treated with

effective services with latest technology. Moreover, NHS can also focus on budgeting technique

in which every aspect of health care entity could be managed according to inflow and outflow of

funds. Firm cannot survive without availability of adequate amount of cash. It is important for

the manager to keep the cash flow management of organization's inflow and outflow. Further

they needs to ensure surplus cash available for the business activities. Project cash flow is

regarded as the tool that assists in administrating cash flow within the firm. In accordance with

the tool manager needs to make determination of the potential earning for future and make

efforts in order to attain this. They would make sure that actual expenses would not exceed the

set maximum limit by the means of controlling and monitoring. In addition to this improvement

in the receivable days as well as management of payables acts as an aid in enhancing the balance

of cash. It assist in efficient resource allocation in several operating activities. Along with this

they develop sales target and makes efforts in achieving them by the means of constructing

several policies. Therefore organization would be able to possess surplus net cash available and

carry out business activities in an effective manner.

ACTIVITY 4

1. Various business ownership structure, roles and accountability of owners and managers in

decision making Ownership structure: There is presence of three types of business structure that possess

their own requirement of financials as well as various responsibilities of demonstrating

financial information. The structure of the firm involves sole trader, limited company as

well as partnership. In case of sole trade single person owns and manages the firm. He

makes investment of his own funds for the purpose of generating income. On the other

hand partnership is regarded as the association among two or more individuals in which

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.