Financial Analysis of Nice Cars: Liquidity, Leverage, and Share Price

VerifiedAdded on 2022/09/12

|14

|3027

|19

Report

AI Summary

This report provides a comprehensive financial analysis of Nice Cars, examining its performance from 2015 to 2017. The analysis includes a detailed evaluation of various financial ratios, such as liquidity ratios (current and quick ratios), leverage ratios (debt ratio and debt-to-equity ratio), operating leverage, and working capital ratio. The report assesses Nice Cars' ability to manage short-term obligations, its financing strategies, and the efficiency of its operations. Furthermore, the report compares Nice Cars' financial position with those of competitors, Alpine and Peugeot, highlighting their respective strengths and weaknesses. The analysis also delves into the company's cash flow from operations and share price valuation, determining whether the shares are undervalued or overvalued. The findings reveal insights into Nice Cars' financial health, providing a basis for strategic recommendations and decision-making.

Financial Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Analysis 1

Tasks

A. Financial Ratios

Financial Ratio is a relative magnitude of two selected numerical values taken from enterprises

financial position. Financial ratio contains the two numerical values that help to define the

financial situation of the firm. There are different kinds of financial ratios that determine the

financial performance of the company such as profitability, current, solvency, leverage, working

capital and the other ratios. The different financial ratio defines the different area and capabilities

of the firm to generate the profit and the others (Robinson, Henry, Pirie, and Broihahn, 2015). In

this task, the financial ratio has been used to examine the financial performance.

Financial Ratio

Analysis

Nice

cars

2015 2016 2017

Liquidity Ratio

Current Ratio Current assets 91847 102052 106735

Current liabilities 77081 84457 87105

1.19 1.21 1.23

Quick Ratio Quick assets 49875 56627 58821

Current liabilities 77081 84457 87105

0.65 0.67 0.68

Tasks

A. Financial Ratios

Financial Ratio is a relative magnitude of two selected numerical values taken from enterprises

financial position. Financial ratio contains the two numerical values that help to define the

financial situation of the firm. There are different kinds of financial ratios that determine the

financial performance of the company such as profitability, current, solvency, leverage, working

capital and the other ratios. The different financial ratio defines the different area and capabilities

of the firm to generate the profit and the others (Robinson, Henry, Pirie, and Broihahn, 2015). In

this task, the financial ratio has been used to examine the financial performance.

Financial Ratio

Analysis

Nice

cars

2015 2016 2017

Liquidity Ratio

Current Ratio Current assets 91847 102052 106735

Current liabilities 77081 84457 87105

1.19 1.21 1.23

Quick Ratio Quick assets 49875 56627 58821

Current liabilities 77081 84457 87105

0.65 0.67 0.68

Financial Analysis 2

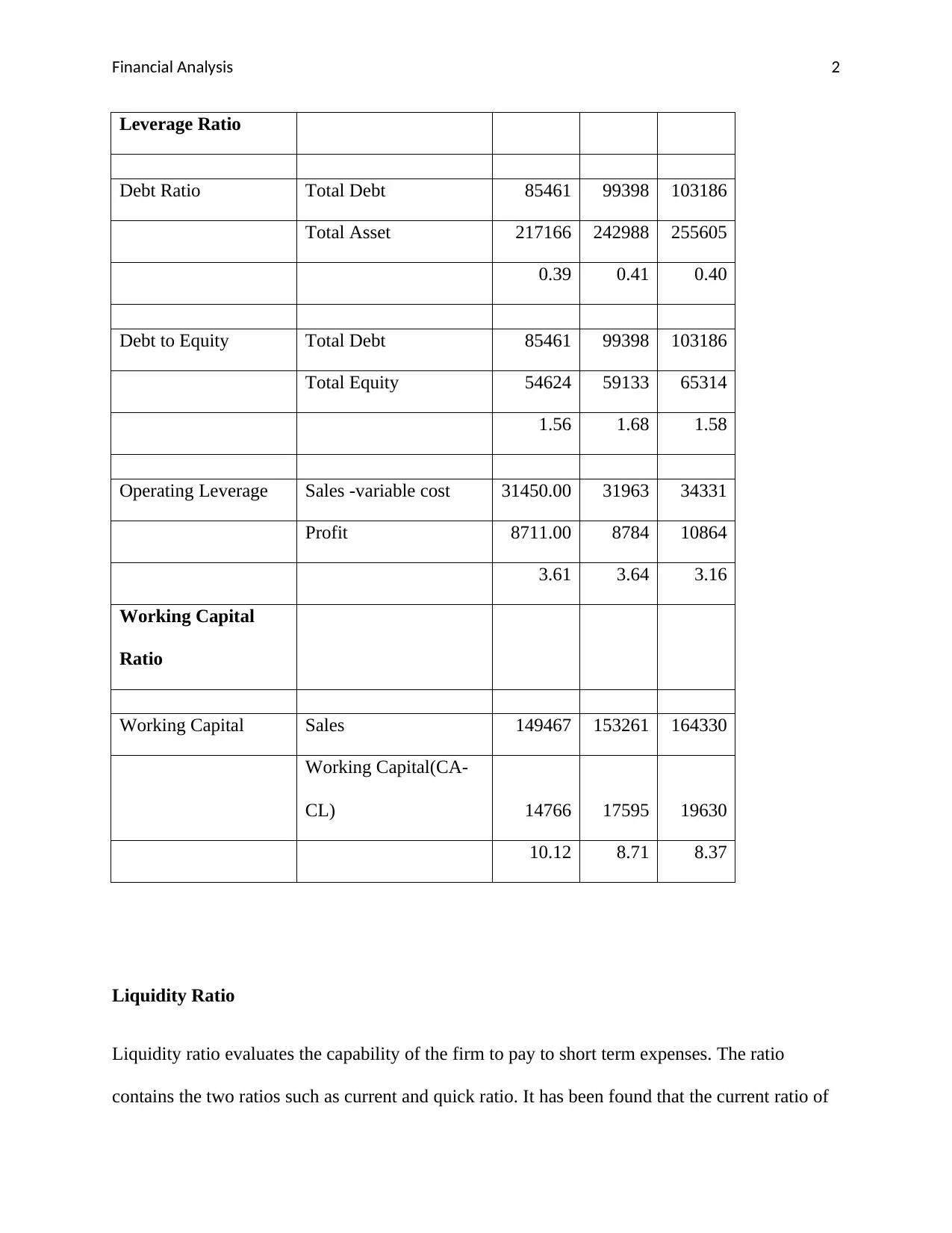

Leverage Ratio

Debt Ratio Total Debt 85461 99398 103186

Total Asset 217166 242988 255605

0.39 0.41 0.40

Debt to Equity Total Debt 85461 99398 103186

Total Equity 54624 59133 65314

1.56 1.68 1.58

Operating Leverage Sales -variable cost 31450.00 31963 34331

Profit 8711.00 8784 10864

3.61 3.64 3.16

Working Capital

Ratio

Working Capital Sales 149467 153261 164330

Working Capital(CA-

CL) 14766 17595 19630

10.12 8.71 8.37

Liquidity Ratio

Liquidity ratio evaluates the capability of the firm to pay to short term expenses. The ratio

contains the two ratios such as current and quick ratio. It has been found that the current ratio of

Leverage Ratio

Debt Ratio Total Debt 85461 99398 103186

Total Asset 217166 242988 255605

0.39 0.41 0.40

Debt to Equity Total Debt 85461 99398 103186

Total Equity 54624 59133 65314

1.56 1.68 1.58

Operating Leverage Sales -variable cost 31450.00 31963 34331

Profit 8711.00 8784 10864

3.61 3.64 3.16

Working Capital

Ratio

Working Capital Sales 149467 153261 164330

Working Capital(CA-

CL) 14766 17595 19630

10.12 8.71 8.37

Liquidity Ratio

Liquidity ratio evaluates the capability of the firm to pay to short term expenses. The ratio

contains the two ratios such as current and quick ratio. It has been found that the current ratio of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Analysis 3

the firm has been increasing from the three years such 2015-2017. From the last three years, it is

observed that the current ratio of the business is increasing such as 1.19, 1.21 and 1.23 in 2015,

2016 and 2017 respectively. The reason behind the increases of current ratio is increasing current

assets as compare to current liabilities. The increasing current assets depicts that the company

invest in current assets more instead of fixed assets. The increasing current assets as compare to

current liabilities depicts that the firm has the capabilities to pay its all short term obligations.

The evaluation of quick ratio also represents the increasing ratio as the amount of cash in hand

has been increases such as 0.65, 0.67 and 0.68 in 2015, 2016, and 2017 respectively. The

liquidity position of the organization becomes strong that helps to pay the short term

expenditures (Schroeder, Clark, and Cathey, 2019).

Financial Leverage Ratio

Financial leverage ratio evaluates the finance activities of the company. There are two ways in

which the company can finance its operation activities such as issuing equity shares and

borrowing money from other as debt. According to calculation of financial leverage ratio of the

firm, it has been analyzed that the company finance operating activities by borrowing the money

from the third parties. The company prefers to uses the debt as a financial source as compare to

equity. According to the evaluation of debt to equity ratio, it is observed that 1.56, 1.68 and 1.58

are the ratio in the three years such as 2015, 2016 and 2017 respectively. As per the financial

ratio result, it depicts that the company uses the debt as source to finance the operation activities.

It affects the financial position of the company in coming future as debt can increases the

chances of insolvency (Williams, and Dobelman, 2017).

Operation Leverage Ratio

the firm has been increasing from the three years such 2015-2017. From the last three years, it is

observed that the current ratio of the business is increasing such as 1.19, 1.21 and 1.23 in 2015,

2016 and 2017 respectively. The reason behind the increases of current ratio is increasing current

assets as compare to current liabilities. The increasing current assets depicts that the company

invest in current assets more instead of fixed assets. The increasing current assets as compare to

current liabilities depicts that the firm has the capabilities to pay its all short term obligations.

The evaluation of quick ratio also represents the increasing ratio as the amount of cash in hand

has been increases such as 0.65, 0.67 and 0.68 in 2015, 2016, and 2017 respectively. The

liquidity position of the organization becomes strong that helps to pay the short term

expenditures (Schroeder, Clark, and Cathey, 2019).

Financial Leverage Ratio

Financial leverage ratio evaluates the finance activities of the company. There are two ways in

which the company can finance its operation activities such as issuing equity shares and

borrowing money from other as debt. According to calculation of financial leverage ratio of the

firm, it has been analyzed that the company finance operating activities by borrowing the money

from the third parties. The company prefers to uses the debt as a financial source as compare to

equity. According to the evaluation of debt to equity ratio, it is observed that 1.56, 1.68 and 1.58

are the ratio in the three years such as 2015, 2016 and 2017 respectively. As per the financial

ratio result, it depicts that the company uses the debt as source to finance the operation activities.

It affects the financial position of the company in coming future as debt can increases the

chances of insolvency (Williams, and Dobelman, 2017).

Operation Leverage Ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Analysis 4

Operation leverage ratio is a financial efficiency ratio that has been measured percentage of

using the fixed cost in order to generate the profits. As per the calculation of operating leverage

ratio, the amount of leverage ratio is increasing from 3.61, 3.64 and 3.16 in the year 2015, 2016,

and 2017 respectively. The company has the capability to generate the revenue has been

increases.

Working Capital Ratio

Working capital ratio is also a part of liquidity as it helps to evaluate the liquidity of the firm to

pay the short term obligations. The ratio of working capital has been evaluated with the help of

current assets and current liabilities (Storey, Keasey, Watson, and Wynarczyk, 2016). According

to the evaluation of working capital ratio, it has been determined that the situation of capital

employed has been increases from the year 2015, 2016 and 2017 such as 14766, 17595 and

19630 respectively. Sales amount to the company has been increases from the three years but the

ratio of working capital has been decreases. The decreasing working capital ratio 10.12, 8.71 and

8.37 depicts the ability of the firm has been decreases to pay the all the obligations.

B. Financial Ratios of Competitors

In this task, financial position of the firm has been examined and compare with the other

companies in order to evaluate the financial performance of the firm in the market.

Financial

Ratio Analysis

Nice Alp Peu

Operation leverage ratio is a financial efficiency ratio that has been measured percentage of

using the fixed cost in order to generate the profits. As per the calculation of operating leverage

ratio, the amount of leverage ratio is increasing from 3.61, 3.64 and 3.16 in the year 2015, 2016,

and 2017 respectively. The company has the capability to generate the revenue has been

increases.

Working Capital Ratio

Working capital ratio is also a part of liquidity as it helps to evaluate the liquidity of the firm to

pay the short term obligations. The ratio of working capital has been evaluated with the help of

current assets and current liabilities (Storey, Keasey, Watson, and Wynarczyk, 2016). According

to the evaluation of working capital ratio, it has been determined that the situation of capital

employed has been increases from the year 2015, 2016 and 2017 such as 14766, 17595 and

19630 respectively. Sales amount to the company has been increases from the three years but the

ratio of working capital has been decreases. The decreasing working capital ratio 10.12, 8.71 and

8.37 depicts the ability of the firm has been decreases to pay the all the obligations.

B. Financial Ratios of Competitors

In this task, financial position of the firm has been examined and compare with the other

companies in order to evaluate the financial performance of the firm in the market.

Financial

Ratio Analysis

Nice Alp Peu

Financial Analysis 5

cars ine oget

2015 2016

201

7

201

5

201

6

201

7

201

5 2016

201

7

Liquidity

Ratio

Current Ratio Current assets

9184

7

1020

52

106

735

142

952

130

382

128

330

220

31

1942

4

264

99

Current

liabilities

7708

1

8445

7

871

05

577

84

509

61

467

05

309

03

2295

8

292

34

1.19 1.21 1.23 2.47 2.56 2.75

0.7

1 0.85

0.9

1

Quick Ratio Quick assets

4987

5

5662

7

588

21

983

88

860

24

927

38

150

01

1644

7

215

48

Current

liabilities

7708

1

8445

7

871

05

577

84

509

61

467

05

309

03

2295

8

292

34

0.65 0.67 0.68 1.70 1.69 1.99

0.4

9 0.72

0.7

4

Leverage

Ratio

Debt Ratio Total Debt

8546

1

9939

8

103

186

930

2

104

16

982

3

129

85

1000

1

115

51

Total Asset 2171 2429 255 211 205 201 597 4244 451

cars ine oget

2015 2016

201

7

201

5

201

6

201

7

201

5 2016

201

7

Liquidity

Ratio

Current Ratio Current assets

9184

7

1020

52

106

735

142

952

130

382

128

330

220

31

1942

4

264

99

Current

liabilities

7708

1

8445

7

871

05

577

84

509

61

467

05

309

03

2295

8

292

34

1.19 1.21 1.23 2.47 2.56 2.75

0.7

1 0.85

0.9

1

Quick Ratio Quick assets

4987

5

5662

7

588

21

983

88

860

24

927

38

150

01

1644

7

215

48

Current

liabilities

7708

1

8445

7

871

05

577

84

509

61

467

05

309

03

2295

8

292

34

0.65 0.67 0.68 1.70 1.69 1.99

0.4

9 0.72

0.7

4

Leverage

Ratio

Debt Ratio Total Debt

8546

1

9939

8

103

186

930

2

104

16

982

3

129

85

1000

1

115

51

Total Asset 2171 2429 255 211 205 201 597 4244 451

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Analysis 6

66 88 605 309 182 857 64 4 53

0.39 0.41 0.40 0.04 0.05 0.05

0.2

2 0.24

0.2

6

Debt to Equity Total Debt

8546

1

9939

8

103

186

930

2

104

16

982

3

129

85

1000

1

115

51

Total Equity

5462

4

5913

3

653

14

123

949

131

534

137

180

104

18

1221

9

146

18

1.56 1.68 1.58 0.08 0.08 0.07

1.2

5 0.82

0.7

9

Operating

Leverage

Sales -variable

cost

3145

0.00

3196

3

343

31

516

36

419

49

422

56

-

364 2733

323

5

Profit

8711.

00 8784

108

64

127

04

109

55

789

4

-

222

7 951

194

4

3.61 3.64 3.16 4.06 3.83 5.35

0.1

6 2.87

1.6

6

Working

Capital Ratio

Working

Capital Sales

1494

67

1532

61

164

330

294

560

273

056

247

751

530

79

5476

7

540

30

Working

Capital(CA-

1476

6

1759

5

196

30

851

68

794

21

816

25

-

887

-

3534

-

273

66 88 605 309 182 857 64 4 53

0.39 0.41 0.40 0.04 0.05 0.05

0.2

2 0.24

0.2

6

Debt to Equity Total Debt

8546

1

9939

8

103

186

930

2

104

16

982

3

129

85

1000

1

115

51

Total Equity

5462

4

5913

3

653

14

123

949

131

534

137

180

104

18

1221

9

146

18

1.56 1.68 1.58 0.08 0.08 0.07

1.2

5 0.82

0.7

9

Operating

Leverage

Sales -variable

cost

3145

0.00

3196

3

343

31

516

36

419

49

422

56

-

364 2733

323

5

Profit

8711.

00 8784

108

64

127

04

109

55

789

4

-

222

7 951

194

4

3.61 3.64 3.16 4.06 3.83 5.35

0.1

6 2.87

1.6

6

Working

Capital Ratio

Working

Capital Sales

1494

67

1532

61

164

330

294

560

273

056

247

751

530

79

5476

7

540

30

Working

Capital(CA-

1476

6

1759

5

196

30

851

68

794

21

816

25

-

887

-

3534

-

273

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Analysis 7

CL) 2 5

10.12 8.71 8.37 3.46 3.44 3.04

-

5.9

8

-

15.5

0

-

19.

76

By evaluating the financial ratio of two more automakers companies of French, it is observed

that the financial situation of Alpine is strong as compare to nicecars, and Peugeot. According to

the financial ratio, liquidity position of Alpine is strong as compare to nicecars, and Peugeot

(Alpine, 2016). After the liquidity position, Nicecars have a strong liquidity position in the

market. The amount of current assets is high due to which the capability of Alpine is high in

order to pay short term obligations. The debt to equity ratio of Nice cars is 1.56, 1.68 and 1.58,

Alpine is 0.08, 0.08 and 0.07, and Peugeot is 1.25, 0.82 and 0.79 (Peugeot, 2016). From the

above debt to equity ratio, it is observed that Alpine is the only company that finance the

operating activities by issuing the share instead of debt. But Nicecars is also the company that

finances the operating activities by borrowing the money on debt instead of issuing of equity

shares. Peugeot is also the company that more prefers the debt instead of equity due to which it

debt to equity ratio is less as compare to Nice cars and Alpine companies (Peugeot, 2017).

Increasing the debt of Nicecars increases the risk of insolvency in the coming future. Nicecars

has to issues the share as per the Alpine so that the financing activities will not affect the

financial performance of the organization. Peugeot also has to finance the operation activities by

issuing the shares so that the risk of insolvency has been reduces. At the end, it can be said that

Nicecars have less financial position as compare to Alpine (Alpine, 2017). The company faces

CL) 2 5

10.12 8.71 8.37 3.46 3.44 3.04

-

5.9

8

-

15.5

0

-

19.

76

By evaluating the financial ratio of two more automakers companies of French, it is observed

that the financial situation of Alpine is strong as compare to nicecars, and Peugeot. According to

the financial ratio, liquidity position of Alpine is strong as compare to nicecars, and Peugeot

(Alpine, 2016). After the liquidity position, Nicecars have a strong liquidity position in the

market. The amount of current assets is high due to which the capability of Alpine is high in

order to pay short term obligations. The debt to equity ratio of Nice cars is 1.56, 1.68 and 1.58,

Alpine is 0.08, 0.08 and 0.07, and Peugeot is 1.25, 0.82 and 0.79 (Peugeot, 2016). From the

above debt to equity ratio, it is observed that Alpine is the only company that finance the

operating activities by issuing the share instead of debt. But Nicecars is also the company that

finances the operating activities by borrowing the money on debt instead of issuing of equity

shares. Peugeot is also the company that more prefers the debt instead of equity due to which it

debt to equity ratio is less as compare to Nice cars and Alpine companies (Peugeot, 2017).

Increasing the debt of Nicecars increases the risk of insolvency in the coming future. Nicecars

has to issues the share as per the Alpine so that the financing activities will not affect the

financial performance of the organization. Peugeot also has to finance the operation activities by

issuing the shares so that the risk of insolvency has been reduces. At the end, it can be said that

Nicecars have less financial position as compare to Alpine (Alpine, 2017). The company faces

Financial Analysis 8

the financial crisis in coming future and Alpine is the best company in terms of financial

position.

C. Cash Flow From Operations

Cash flow from operations is the section of a firm's cash flow statement. The operating statement

depicts that the amount of cash that has been generated or used from carrying out its operating

activities in a specific period of time. The increasing amount of cash flow of operating activities

states that the company earns the high revenue by selling the goods and investing in further

activities. The increasing cash flow from of operating activities is beneficial for the company.

According to the financial situation of the firm, it has been found that the company operating

activities has been decreases and in the year 2017, the amount of operating activities reflects the

negative amount which is not beneficial for the organization. In the year 2015, 2016, and 2017,

the amount of cash flow from operating activities is 222, 3711, and -1652. In the year 2015, the

amount of operating is 222 which is increasing with the high gap in the year 2016 with the

amount of 3711 which is beneficial for the company. In the year 2017, the amount of operation

activities reflects the negative amount that is -1652. The amount of cash flow from operating

activities has been fluctuated year by year. At the initial year, it is observed that the amount

from operating activities has been increases but after that its getting negative that is not

beneficial for the company.

There are various reasons behind the increasing the amount of cash flow from operating

activities. The biggest reason in this case behind the increasing cash flow from operation

activities is to improve the efficiency in maintaining the current assets with the motive to pay the

current liabilities and the other short term expenses. It is necessary for the firm to maintain the

the financial crisis in coming future and Alpine is the best company in terms of financial

position.

C. Cash Flow From Operations

Cash flow from operations is the section of a firm's cash flow statement. The operating statement

depicts that the amount of cash that has been generated or used from carrying out its operating

activities in a specific period of time. The increasing amount of cash flow of operating activities

states that the company earns the high revenue by selling the goods and investing in further

activities. The increasing cash flow from of operating activities is beneficial for the company.

According to the financial situation of the firm, it has been found that the company operating

activities has been decreases and in the year 2017, the amount of operating activities reflects the

negative amount which is not beneficial for the organization. In the year 2015, 2016, and 2017,

the amount of cash flow from operating activities is 222, 3711, and -1652. In the year 2015, the

amount of operating is 222 which is increasing with the high gap in the year 2016 with the

amount of 3711 which is beneficial for the company. In the year 2017, the amount of operation

activities reflects the negative amount that is -1652. The amount of cash flow from operating

activities has been fluctuated year by year. At the initial year, it is observed that the amount

from operating activities has been increases but after that its getting negative that is not

beneficial for the company.

There are various reasons behind the increasing the amount of cash flow from operating

activities. The biggest reason in this case behind the increasing cash flow from operation

activities is to improve the efficiency in maintaining the current assets with the motive to pay the

current liabilities and the other short term expenses. It is necessary for the firm to maintain the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Analysis 9

current assets and current liabilities so that the capabilities to pay the short term obligations have

been increases. Increasing operating activities helps the company to operate effectively and

efficiency in the market. The other reason behind increasing the amount of cash flow from

operation is inventory, account receivable, and sales. The rising amount of these turnovers helps

the organization to operate effectively. It also reflects that the company operates the business for

long term. But decreasing the amount of cash flow from operating activities has also some

reasons which are required to improve by the company for increasing the operation activities.

There are also various reasons behind the decreasing of cash flow from operating activities and

these are declining net income, sales and change in working capital. In this case, the amount of

expenses has been increases in the last three years such as 18247, 19348, and 19432. The amount

of cost of goods sold has been increases due to which the net profit margin of the firm has been

decreasing. The decreasing ratio of net margin and increasing expenses affects the amount of

cash flow from operating activities. These are the reasons in the case of nice cars due to which

the amount of cash flow from operating has been decreases.

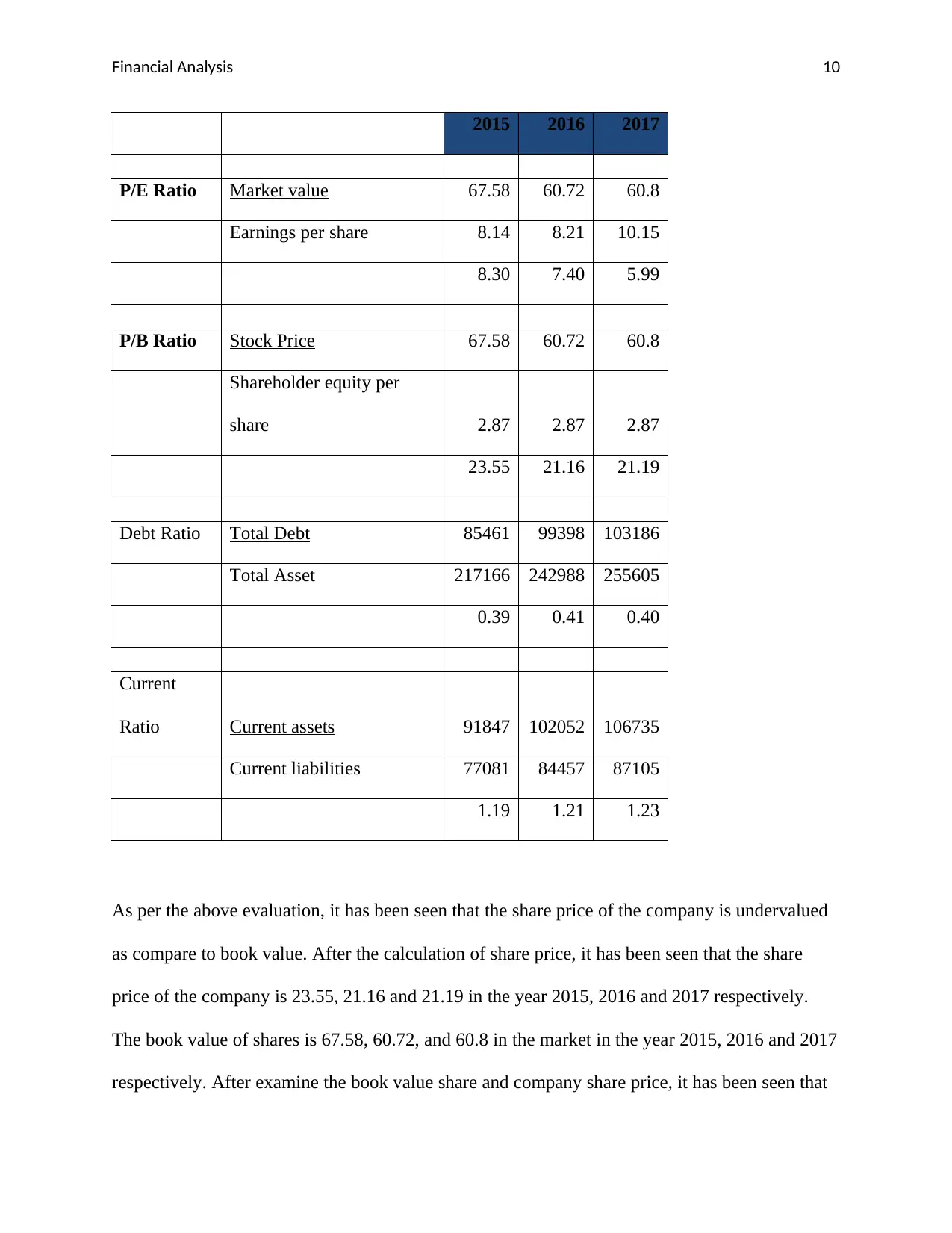

D. Share Price

There are two ways to measures the share prices of the company such as undervalued and

overvalued. The evaluation of share price has been done.

Nice

cars

current assets and current liabilities so that the capabilities to pay the short term obligations have

been increases. Increasing operating activities helps the company to operate effectively and

efficiency in the market. The other reason behind increasing the amount of cash flow from

operation is inventory, account receivable, and sales. The rising amount of these turnovers helps

the organization to operate effectively. It also reflects that the company operates the business for

long term. But decreasing the amount of cash flow from operating activities has also some

reasons which are required to improve by the company for increasing the operation activities.

There are also various reasons behind the decreasing of cash flow from operating activities and

these are declining net income, sales and change in working capital. In this case, the amount of

expenses has been increases in the last three years such as 18247, 19348, and 19432. The amount

of cost of goods sold has been increases due to which the net profit margin of the firm has been

decreasing. The decreasing ratio of net margin and increasing expenses affects the amount of

cash flow from operating activities. These are the reasons in the case of nice cars due to which

the amount of cash flow from operating has been decreases.

D. Share Price

There are two ways to measures the share prices of the company such as undervalued and

overvalued. The evaluation of share price has been done.

Nice

cars

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Analysis 10

2015 2016 2017

P/E Ratio Market value 67.58 60.72 60.8

Earnings per share 8.14 8.21 10.15

8.30 7.40 5.99

P/B Ratio Stock Price 67.58 60.72 60.8

Shareholder equity per

share 2.87 2.87 2.87

23.55 21.16 21.19

Debt Ratio Total Debt 85461 99398 103186

Total Asset 217166 242988 255605

0.39 0.41 0.40

Current

Ratio Current assets 91847 102052 106735

Current liabilities 77081 84457 87105

1.19 1.21 1.23

As per the above evaluation, it has been seen that the share price of the company is undervalued

as compare to book value. After the calculation of share price, it has been seen that the share

price of the company is 23.55, 21.16 and 21.19 in the year 2015, 2016 and 2017 respectively.

The book value of shares is 67.58, 60.72, and 60.8 in the market in the year 2015, 2016 and 2017

respectively. After examine the book value share and company share price, it has been seen that

2015 2016 2017

P/E Ratio Market value 67.58 60.72 60.8

Earnings per share 8.14 8.21 10.15

8.30 7.40 5.99

P/B Ratio Stock Price 67.58 60.72 60.8

Shareholder equity per

share 2.87 2.87 2.87

23.55 21.16 21.19

Debt Ratio Total Debt 85461 99398 103186

Total Asset 217166 242988 255605

0.39 0.41 0.40

Current

Ratio Current assets 91847 102052 106735

Current liabilities 77081 84457 87105

1.19 1.21 1.23

As per the above evaluation, it has been seen that the share price of the company is undervalued

as compare to book value. After the calculation of share price, it has been seen that the share

price of the company is 23.55, 21.16 and 21.19 in the year 2015, 2016 and 2017 respectively.

The book value of shares is 67.58, 60.72, and 60.8 in the market in the year 2015, 2016 and 2017

respectively. After examine the book value share and company share price, it has been seen that

Financial Analysis 11

share price of the firm is undervalued. The value of share of the organization is less as compare

to the market value. The share price of the firm has been decreases continuously year by year due

to which the investors think twice to invest in it (Chen, Ong, and Hsu, 2016).

A. Investors always invest in the company when the share price of the organization that has

been decreases. But in this case, the share price of the firm has been decreases year by

year due to which the chance of increasing the share price value is also less. Investors

have a risk to invest in it by purchasing the shares and also to retain the shares of the

company for long time (Di Tella, 2017). Retain the share of the company increase the

risk for investors because if in the coming future the amount of share has been reduce

then the investors faces the challenges and risk of facing the loss (DeFusco, et. al, 2015).

Being an investor, it is required to sale the shares in the market with the current share

price otherwise the prices of share has been decreases and the chances of facing the loss

is high. Facing the loss is the main reason of reducing the share price of the firm as

compare the share price of the market. The other reason of selling the share price is that

the amount of debt is also increasing due to which in the coming future the company face

the financial crisis. It is observed that the high debt increases the case of insolvency for

the company. As the chances of insolvency has been increases due to which the investors

has the risk of facing the loss instead of profit.

B. Yes, it is observed that the shares of the company are undervalued. By evaluating the

share price, it has been seen that the market price of shares is 67.58, 60.72, and 60.8 in

2015, 2016 and 2017 respectively. But the company share prices are 23.55, 21.16 and

21.19 in 2015, 2016 and 2017 respectively. By comparing the share price of company

share price of the firm is undervalued. The value of share of the organization is less as compare

to the market value. The share price of the firm has been decreases continuously year by year due

to which the investors think twice to invest in it (Chen, Ong, and Hsu, 2016).

A. Investors always invest in the company when the share price of the organization that has

been decreases. But in this case, the share price of the firm has been decreases year by

year due to which the chance of increasing the share price value is also less. Investors

have a risk to invest in it by purchasing the shares and also to retain the shares of the

company for long time (Di Tella, 2017). Retain the share of the company increase the

risk for investors because if in the coming future the amount of share has been reduce

then the investors faces the challenges and risk of facing the loss (DeFusco, et. al, 2015).

Being an investor, it is required to sale the shares in the market with the current share

price otherwise the prices of share has been decreases and the chances of facing the loss

is high. Facing the loss is the main reason of reducing the share price of the firm as

compare the share price of the market. The other reason of selling the share price is that

the amount of debt is also increasing due to which in the coming future the company face

the financial crisis. It is observed that the high debt increases the case of insolvency for

the company. As the chances of insolvency has been increases due to which the investors

has the risk of facing the loss instead of profit.

B. Yes, it is observed that the shares of the company are undervalued. By evaluating the

share price, it has been seen that the market price of shares is 67.58, 60.72, and 60.8 in

2015, 2016 and 2017 respectively. But the company share prices are 23.55, 21.16 and

21.19 in 2015, 2016 and 2017 respectively. By comparing the share price of company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.