Analysis of Nike's Financial Performance and Accounting Practices

VerifiedAdded on 2023/05/29

|11

|2283

|346

Report

AI Summary

This report provides a comprehensive analysis of Nike's financial performance and accounting practices, focusing on inventory management and long-term debt treatment. Part C analyzes Nike's accounting for inventories and bonds/long-term debt, comparing it with US GAAP and conceptual frameworks. It examines inventory measurement, disclosure, and compliance with standards, as well as long-term debt classification, recognition, and compliance. Part D critically evaluates Nike's financial performance based on the latest financial results, ratio analysis (liquidity, solvency, and profitability), share price movement, and relevant news flow, including its performance in the FIFA World Cup 2018 and its brand value. The report concludes with an investment recommendation based on the analysis of Nike's financial health and market position, suggesting that investment in the stock is a good idea.

RESEARCH PAPER

NIKE –PART C & PART D

STUDENT ID:

[Pick the date]

NIKE –PART C & PART D

STUDENT ID:

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART C

Introduction

The objective of this task is to analyse the accounting treatment provided by the company

(Nike) with regards to two critical items namely inventories and bond & long term debts.

This has been analysed with reference to the appropriate treatment that has been suggested as

part of conceptual framework along with the US GAAP.

Inventories: Measurement

Importance to Nike

The given topic has significant relevant to Nike considering that it needs to manage the

inventory in order to ensure that there is no shortage of supply. Lack of inventory can lead to

loss of sales. However, inventory needs to be managed in a manner whereby associated

storage and handling costs are minimised. Additionally, considering that the company keeps

on coming up with new models, hence obsolescence risk exists owing to which inventory

management is imperative.

Disclosure in financial statements

The closing inventory for the company as on May 31, 2018 is $ 5,261 million while the

opening inventory for the company as on May 31, 2017 is $ 5,055 million. The inventory

balance has been reported as part of the current assets of the company since these are

expected to be sold within one year period.

Recommended accounting treatment

Considering that inventory potentially brings in sales in the future, hence it would be

considered as asset in accordance with the asset definition highlighted in conceptual

framework. Additional aspect that is noteworthy that the inventory on books is expected to be

sold within one year, hence it is reported as current asset (MASB, 2018).

The inventory treatment under US GAAP is different from IFRS. As per US GAAP, there are

three acceptable costing methods i.e. FIFO, weighted average and LIFO (Last In First Out)

and the flexibility remains with the company to deploy suitable method. This is in sharp

contrast with IFRS which prohibits the use of LIFO. With regards to measurement of

inventory, the lower of the market value and the cost is taken into consideration. The market

Introduction

The objective of this task is to analyse the accounting treatment provided by the company

(Nike) with regards to two critical items namely inventories and bond & long term debts.

This has been analysed with reference to the appropriate treatment that has been suggested as

part of conceptual framework along with the US GAAP.

Inventories: Measurement

Importance to Nike

The given topic has significant relevant to Nike considering that it needs to manage the

inventory in order to ensure that there is no shortage of supply. Lack of inventory can lead to

loss of sales. However, inventory needs to be managed in a manner whereby associated

storage and handling costs are minimised. Additionally, considering that the company keeps

on coming up with new models, hence obsolescence risk exists owing to which inventory

management is imperative.

Disclosure in financial statements

The closing inventory for the company as on May 31, 2018 is $ 5,261 million while the

opening inventory for the company as on May 31, 2017 is $ 5,055 million. The inventory

balance has been reported as part of the current assets of the company since these are

expected to be sold within one year period.

Recommended accounting treatment

Considering that inventory potentially brings in sales in the future, hence it would be

considered as asset in accordance with the asset definition highlighted in conceptual

framework. Additional aspect that is noteworthy that the inventory on books is expected to be

sold within one year, hence it is reported as current asset (MASB, 2018).

The inventory treatment under US GAAP is different from IFRS. As per US GAAP, there are

three acceptable costing methods i.e. FIFO, weighted average and LIFO (Last In First Out)

and the flexibility remains with the company to deploy suitable method. This is in sharp

contrast with IFRS which prohibits the use of LIFO. With regards to measurement of

inventory, the lower of the market value and the cost is taken into consideration. The market

value is essentially the current replacement cost. With regards to inventory write down also

reversal is not permissible under US GAAP but it is permissible under IFRS (IASplus, n.d.).

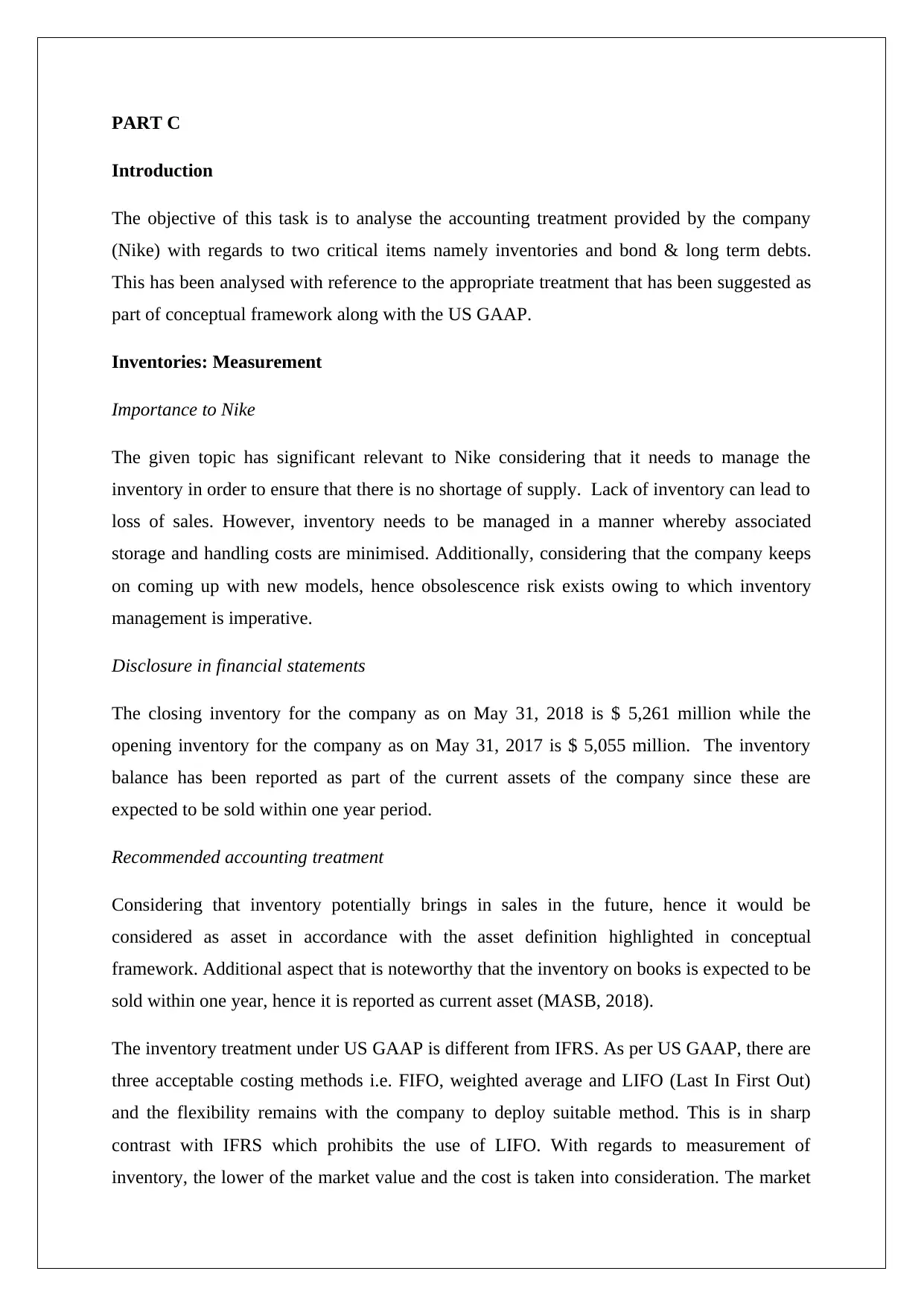

Inventory treatment by Nike

The recognition of the inventory is based on cost. The company has highlighted the inventory

reserves related policy in significant policies as indicated below.

Further, there is a note to inventory which only mentions that the reported inventories in the

financial statements essentially comprises of the finished goods inventory (Nike, 2018).

Compliance with Standards

The company’s inventory relating accounting treatment is broadly in line with that

highlighted by relevant US GAAP norms. The costing method of choice is average cost basis

and also inventory reserves are built by comparison of the cost to the net realisable value

which may not be the same as market value. Further, these reserves are periodically adjusted

against the cost of sales as indicated in US GAAP and also this would not be reversible.

Bonds & Long Term Debt

reversal is not permissible under US GAAP but it is permissible under IFRS (IASplus, n.d.).

Inventory treatment by Nike

The recognition of the inventory is based on cost. The company has highlighted the inventory

reserves related policy in significant policies as indicated below.

Further, there is a note to inventory which only mentions that the reported inventories in the

financial statements essentially comprises of the finished goods inventory (Nike, 2018).

Compliance with Standards

The company’s inventory relating accounting treatment is broadly in line with that

highlighted by relevant US GAAP norms. The costing method of choice is average cost basis

and also inventory reserves are built by comparison of the cost to the net realisable value

which may not be the same as market value. Further, these reserves are periodically adjusted

against the cost of sales as indicated in US GAAP and also this would not be reversible.

Bonds & Long Term Debt

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Importance to Nike

The above instruments tend to provide required capital for the company which is used for

expansion, branding along with product development. In the absence of long term financing

options, the company would have to rely on short term debt along with equity. This would be

an issue for the company considering that equity dilution is prudent to an extent only and

short term debt is not suitable for funding capital assets.

Disclosure in financial statements

The long term debt for the company as on May 31, 2018 is $ 3,468 million while the long

term debt for the company as on May 31, 2017 was $ 3,471 million. The long term debt has

been reported as part of the non-current liabilities of the company since these are expected to

be paid over long term (i.e. have maturity in excess of one year). It is imperative to note that

all of this long term debt is in the form of long term bonds (Nike, 2018).

Recommended accounting treatment

The long term debt (including bonds) should be treated as liability considering that in the

future there would be cash outflow associated for settling the same. Besides, the liability

arises on account of transactions taken in the past. Besides, considering that these liabilities

are expected to require cash outflow in the long term (i.e. more than one year), hence the

nature of liabilities would be non-current liabilities as per conceptual framework (MASB,

2018)

As per US GAAP, classification of debt liabilities takes place on the basis of repayment and

also if the debt is callable. Typically, callable obligations would be considered as current

despite the actual repayment being greater than one year. In accordance with US GAAP, any

issuance cost associated with long term bonds is capitalised at the time of bond issue and is

expensed during the maturity period of the bond (IASplus, 2018). The repayment of principal

refers to the repayment of borrowings and thus, suitable adjustment would be made in the

item. Further, the bonds are stated based on their adjusted cost considering the principal

repayments made and the market value is not reflected (Navigating Accouting, nd).

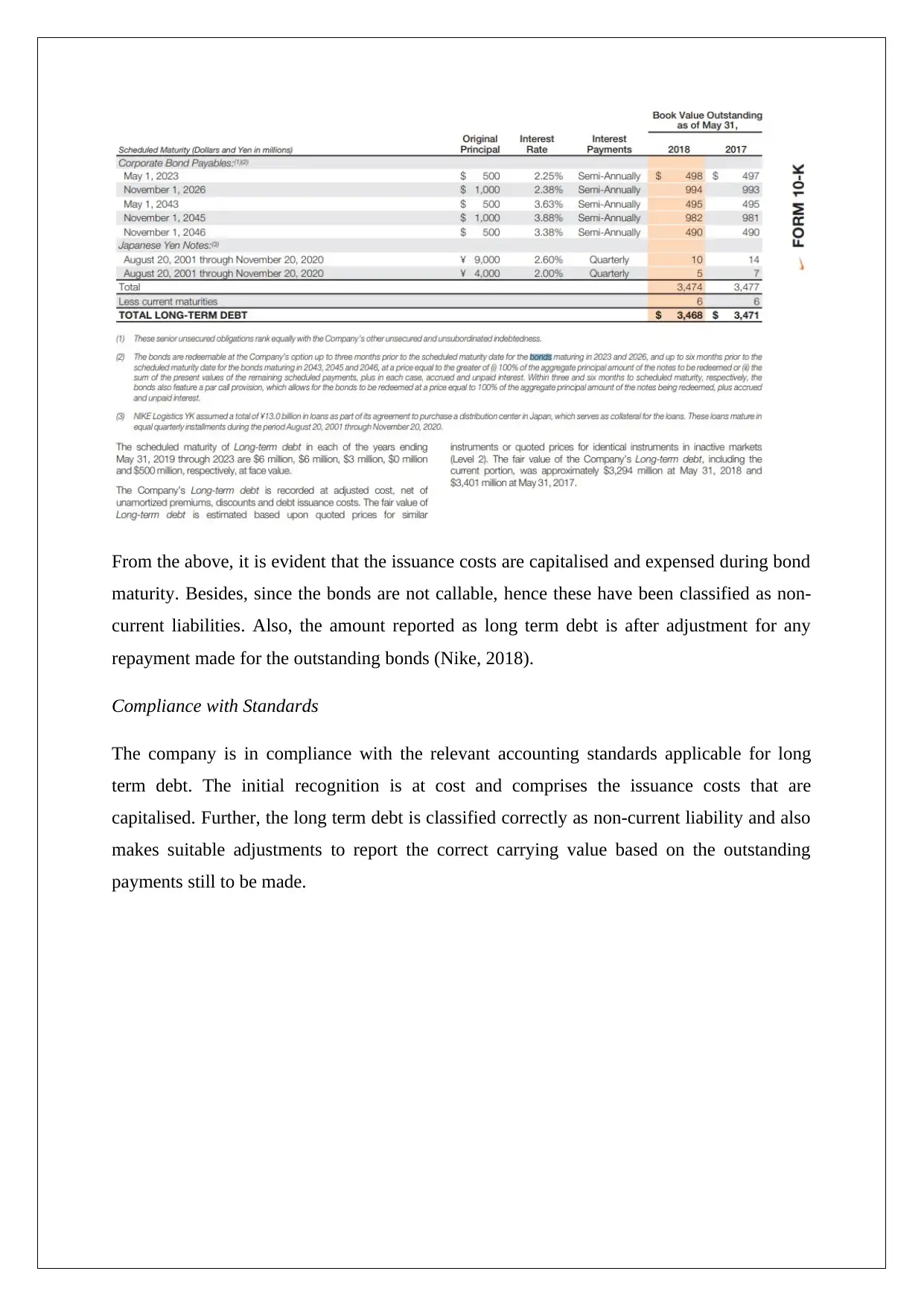

Long term debt treatment by Nike

A relevant disclosure regarding the composition of long term debt with regards to the

currency and other relevant details is indicated below.

The above instruments tend to provide required capital for the company which is used for

expansion, branding along with product development. In the absence of long term financing

options, the company would have to rely on short term debt along with equity. This would be

an issue for the company considering that equity dilution is prudent to an extent only and

short term debt is not suitable for funding capital assets.

Disclosure in financial statements

The long term debt for the company as on May 31, 2018 is $ 3,468 million while the long

term debt for the company as on May 31, 2017 was $ 3,471 million. The long term debt has

been reported as part of the non-current liabilities of the company since these are expected to

be paid over long term (i.e. have maturity in excess of one year). It is imperative to note that

all of this long term debt is in the form of long term bonds (Nike, 2018).

Recommended accounting treatment

The long term debt (including bonds) should be treated as liability considering that in the

future there would be cash outflow associated for settling the same. Besides, the liability

arises on account of transactions taken in the past. Besides, considering that these liabilities

are expected to require cash outflow in the long term (i.e. more than one year), hence the

nature of liabilities would be non-current liabilities as per conceptual framework (MASB,

2018)

As per US GAAP, classification of debt liabilities takes place on the basis of repayment and

also if the debt is callable. Typically, callable obligations would be considered as current

despite the actual repayment being greater than one year. In accordance with US GAAP, any

issuance cost associated with long term bonds is capitalised at the time of bond issue and is

expensed during the maturity period of the bond (IASplus, 2018). The repayment of principal

refers to the repayment of borrowings and thus, suitable adjustment would be made in the

item. Further, the bonds are stated based on their adjusted cost considering the principal

repayments made and the market value is not reflected (Navigating Accouting, nd).

Long term debt treatment by Nike

A relevant disclosure regarding the composition of long term debt with regards to the

currency and other relevant details is indicated below.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the above, it is evident that the issuance costs are capitalised and expensed during bond

maturity. Besides, since the bonds are not callable, hence these have been classified as non-

current liabilities. Also, the amount reported as long term debt is after adjustment for any

repayment made for the outstanding bonds (Nike, 2018).

Compliance with Standards

The company is in compliance with the relevant accounting standards applicable for long

term debt. The initial recognition is at cost and comprises the issuance costs that are

capitalised. Further, the long term debt is classified correctly as non-current liability and also

makes suitable adjustments to report the correct carrying value based on the outstanding

payments still to be made.

maturity. Besides, since the bonds are not callable, hence these have been classified as non-

current liabilities. Also, the amount reported as long term debt is after adjustment for any

repayment made for the outstanding bonds (Nike, 2018).

Compliance with Standards

The company is in compliance with the relevant accounting standards applicable for long

term debt. The initial recognition is at cost and comprises the issuance costs that are

capitalised. Further, the long term debt is classified correctly as non-current liability and also

makes suitable adjustments to report the correct carrying value based on the outstanding

payments still to be made.

PART D

Introduction

The objective of this report is to critically analyse the financial performance of Nike with

reference to the current news flow so as to highlight if it is suitable choice for investment or

not. In order to facilitate the same, a general overview of the latest financial results would be

presented so as to highlight how the company is performing. Additionally, ratio analysis

would be also performed besides analysing the share price movement in the recent past.

Finally, relevant news flow would also be considered so as to offer prudent investment

advice.

Financial Results Analysis

The latest financial statements available for the company correspond to year ending on May

31, 2018. It is apparent that for FY2018, the company has witnessed about 6% topline

growth. Driven by higher revenues, the gross profit of the company has also increased in

FY2018. However, the net income of the company in FY2018 has taken a serious plunge in

excess of 50% owing to reduced gross margins coupled with higher income tax expense.

However, the dividend declared for the ordinary shareholders by the company has seen an

increase in excess of 10%. A positive aspect of the company’s financial performance is that

the cash flows generated from operations has jumped by about 30% in FY2018 over FY2017.

Also, the company is aggressively repurchasing stock which augers well for the shareholders.

The quantum of this purchase was $ 4.25 billion in FY2018 and $ 3.22 billion in FY2017

(Nike, 2018).

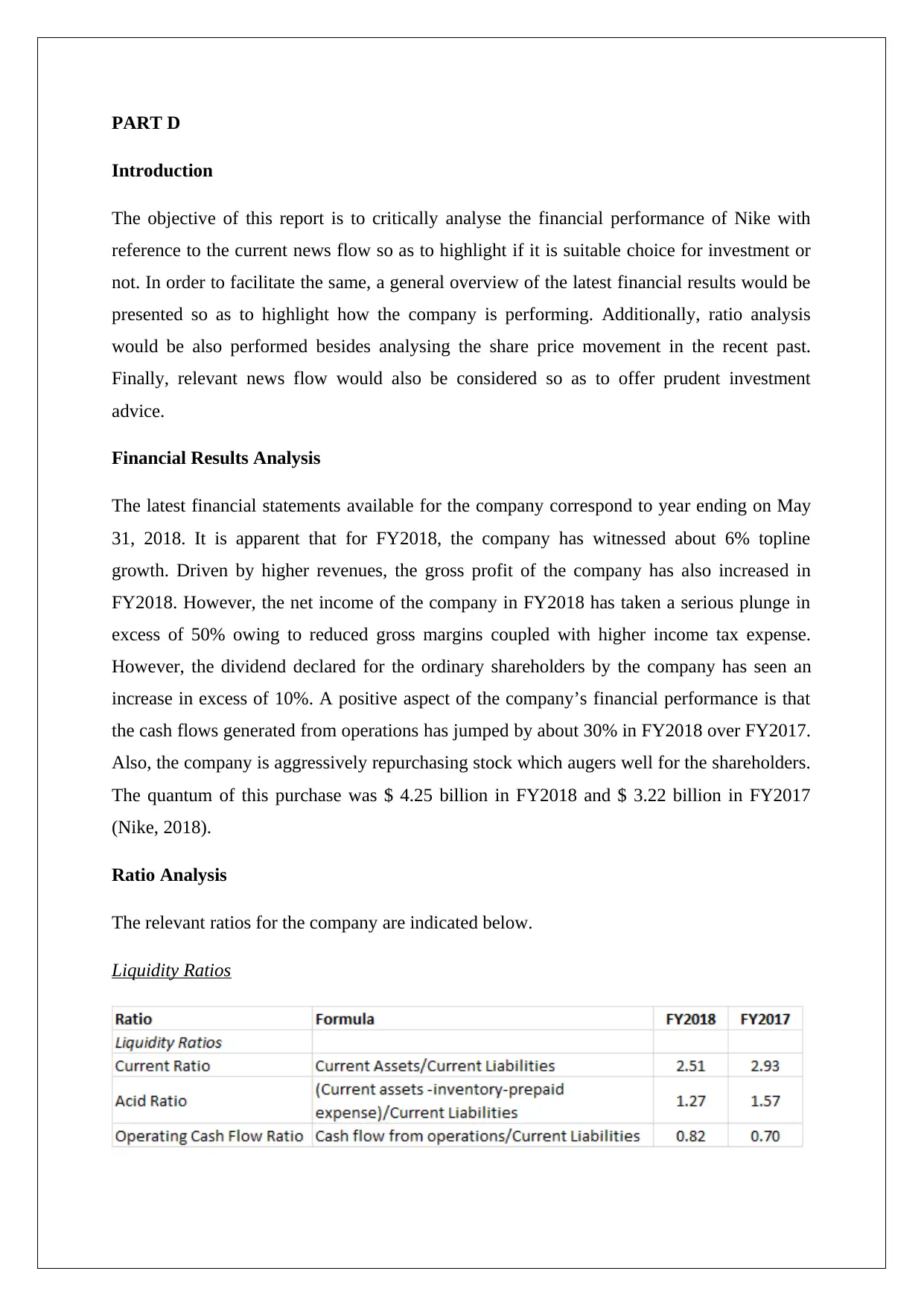

Ratio Analysis

The relevant ratios for the company are indicated below.

Liquidity Ratios

Introduction

The objective of this report is to critically analyse the financial performance of Nike with

reference to the current news flow so as to highlight if it is suitable choice for investment or

not. In order to facilitate the same, a general overview of the latest financial results would be

presented so as to highlight how the company is performing. Additionally, ratio analysis

would be also performed besides analysing the share price movement in the recent past.

Finally, relevant news flow would also be considered so as to offer prudent investment

advice.

Financial Results Analysis

The latest financial statements available for the company correspond to year ending on May

31, 2018. It is apparent that for FY2018, the company has witnessed about 6% topline

growth. Driven by higher revenues, the gross profit of the company has also increased in

FY2018. However, the net income of the company in FY2018 has taken a serious plunge in

excess of 50% owing to reduced gross margins coupled with higher income tax expense.

However, the dividend declared for the ordinary shareholders by the company has seen an

increase in excess of 10%. A positive aspect of the company’s financial performance is that

the cash flows generated from operations has jumped by about 30% in FY2018 over FY2017.

Also, the company is aggressively repurchasing stock which augers well for the shareholders.

The quantum of this purchase was $ 4.25 billion in FY2018 and $ 3.22 billion in FY2017

(Nike, 2018).

Ratio Analysis

The relevant ratios for the company are indicated below.

Liquidity Ratios

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is apparent from the above ratios analysis that liquidity ratios barring operating cash flow

ratio have witnessed a decline in FY2018 in comparison to FY2017. The operating cash flow

ratio has improved on account of robust increase in the cash flow generated from operations

in FY2018 in comparison to FY2017 (Nike, 2018). Even though, there is some decline in the

current ratios and acid ratios, but still the short term liquidity of the company remains quite

robust and no short term cash crunch seems imminent from the above analysis.

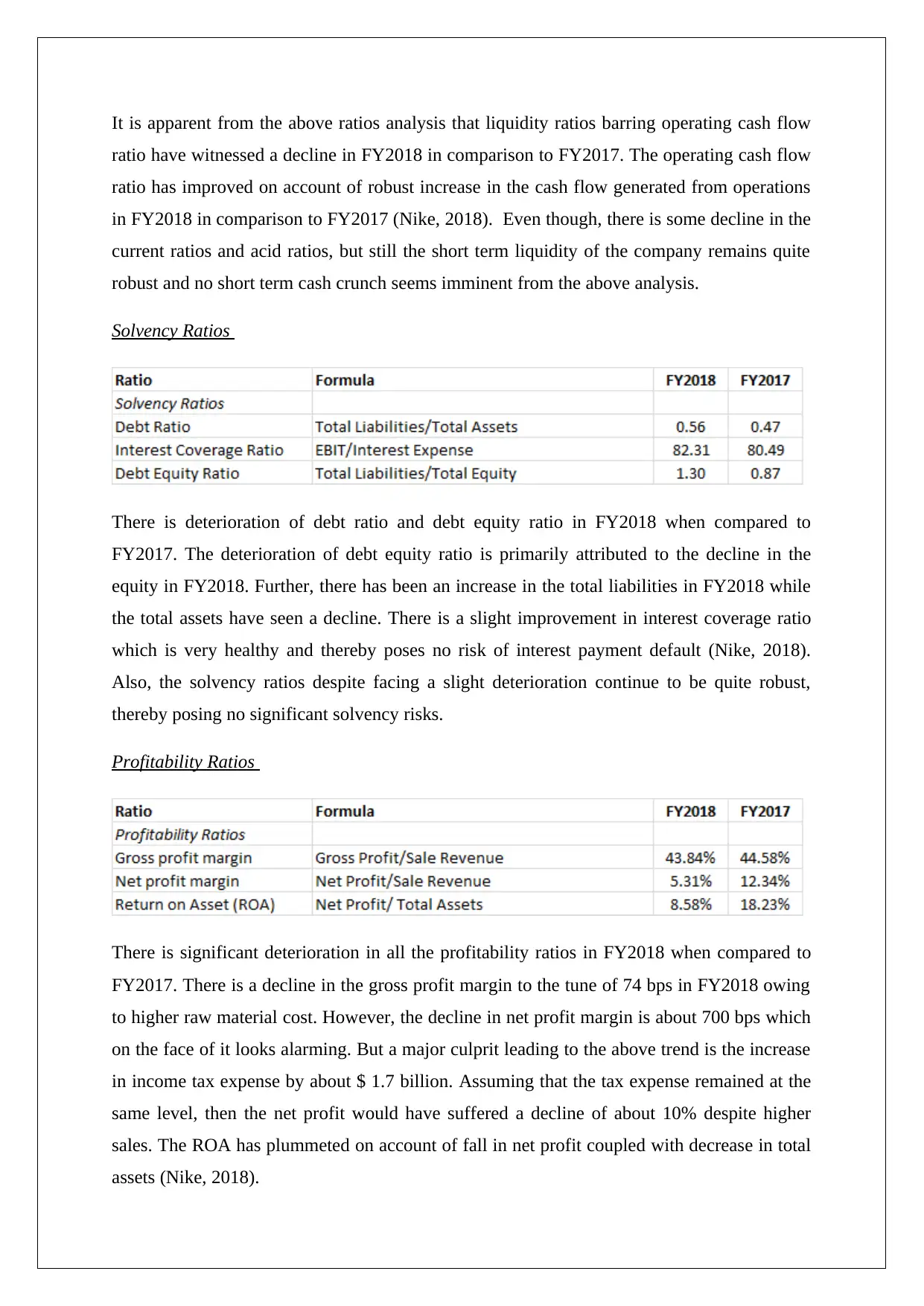

Solvency Ratios

There is deterioration of debt ratio and debt equity ratio in FY2018 when compared to

FY2017. The deterioration of debt equity ratio is primarily attributed to the decline in the

equity in FY2018. Further, there has been an increase in the total liabilities in FY2018 while

the total assets have seen a decline. There is a slight improvement in interest coverage ratio

which is very healthy and thereby poses no risk of interest payment default (Nike, 2018).

Also, the solvency ratios despite facing a slight deterioration continue to be quite robust,

thereby posing no significant solvency risks.

Profitability Ratios

There is significant deterioration in all the profitability ratios in FY2018 when compared to

FY2017. There is a decline in the gross profit margin to the tune of 74 bps in FY2018 owing

to higher raw material cost. However, the decline in net profit margin is about 700 bps which

on the face of it looks alarming. But a major culprit leading to the above trend is the increase

in income tax expense by about $ 1.7 billion. Assuming that the tax expense remained at the

same level, then the net profit would have suffered a decline of about 10% despite higher

sales. The ROA has plummeted on account of fall in net profit coupled with decrease in total

assets (Nike, 2018).

ratio have witnessed a decline in FY2018 in comparison to FY2017. The operating cash flow

ratio has improved on account of robust increase in the cash flow generated from operations

in FY2018 in comparison to FY2017 (Nike, 2018). Even though, there is some decline in the

current ratios and acid ratios, but still the short term liquidity of the company remains quite

robust and no short term cash crunch seems imminent from the above analysis.

Solvency Ratios

There is deterioration of debt ratio and debt equity ratio in FY2018 when compared to

FY2017. The deterioration of debt equity ratio is primarily attributed to the decline in the

equity in FY2018. Further, there has been an increase in the total liabilities in FY2018 while

the total assets have seen a decline. There is a slight improvement in interest coverage ratio

which is very healthy and thereby poses no risk of interest payment default (Nike, 2018).

Also, the solvency ratios despite facing a slight deterioration continue to be quite robust,

thereby posing no significant solvency risks.

Profitability Ratios

There is significant deterioration in all the profitability ratios in FY2018 when compared to

FY2017. There is a decline in the gross profit margin to the tune of 74 bps in FY2018 owing

to higher raw material cost. However, the decline in net profit margin is about 700 bps which

on the face of it looks alarming. But a major culprit leading to the above trend is the increase

in income tax expense by about $ 1.7 billion. Assuming that the tax expense remained at the

same level, then the net profit would have suffered a decline of about 10% despite higher

sales. The ROA has plummeted on account of fall in net profit coupled with decrease in total

assets (Nike, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

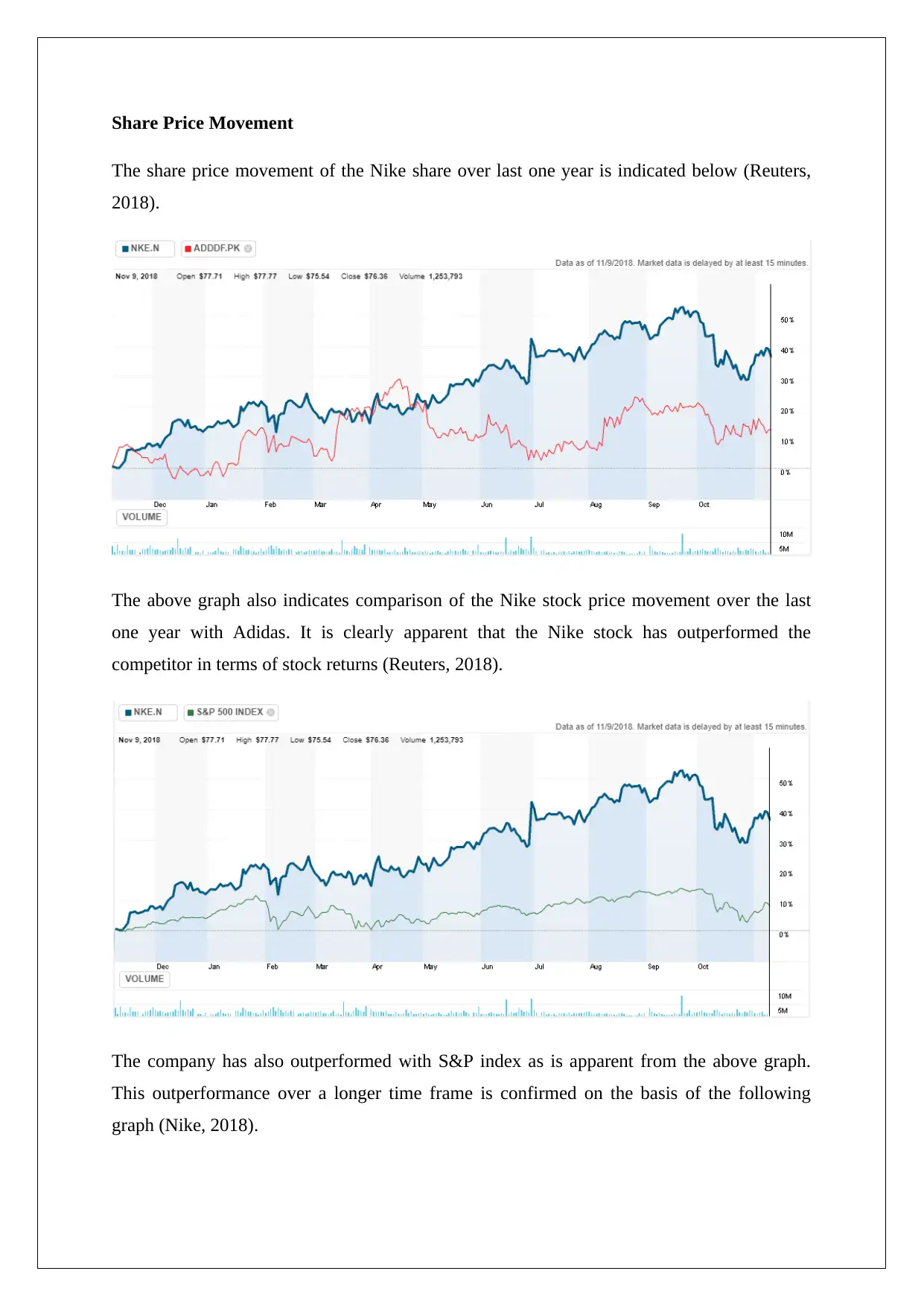

Share Price Movement

The share price movement of the Nike share over last one year is indicated below (Reuters,

2018).

The above graph also indicates comparison of the Nike stock price movement over the last

one year with Adidas. It is clearly apparent that the Nike stock has outperformed the

competitor in terms of stock returns (Reuters, 2018).

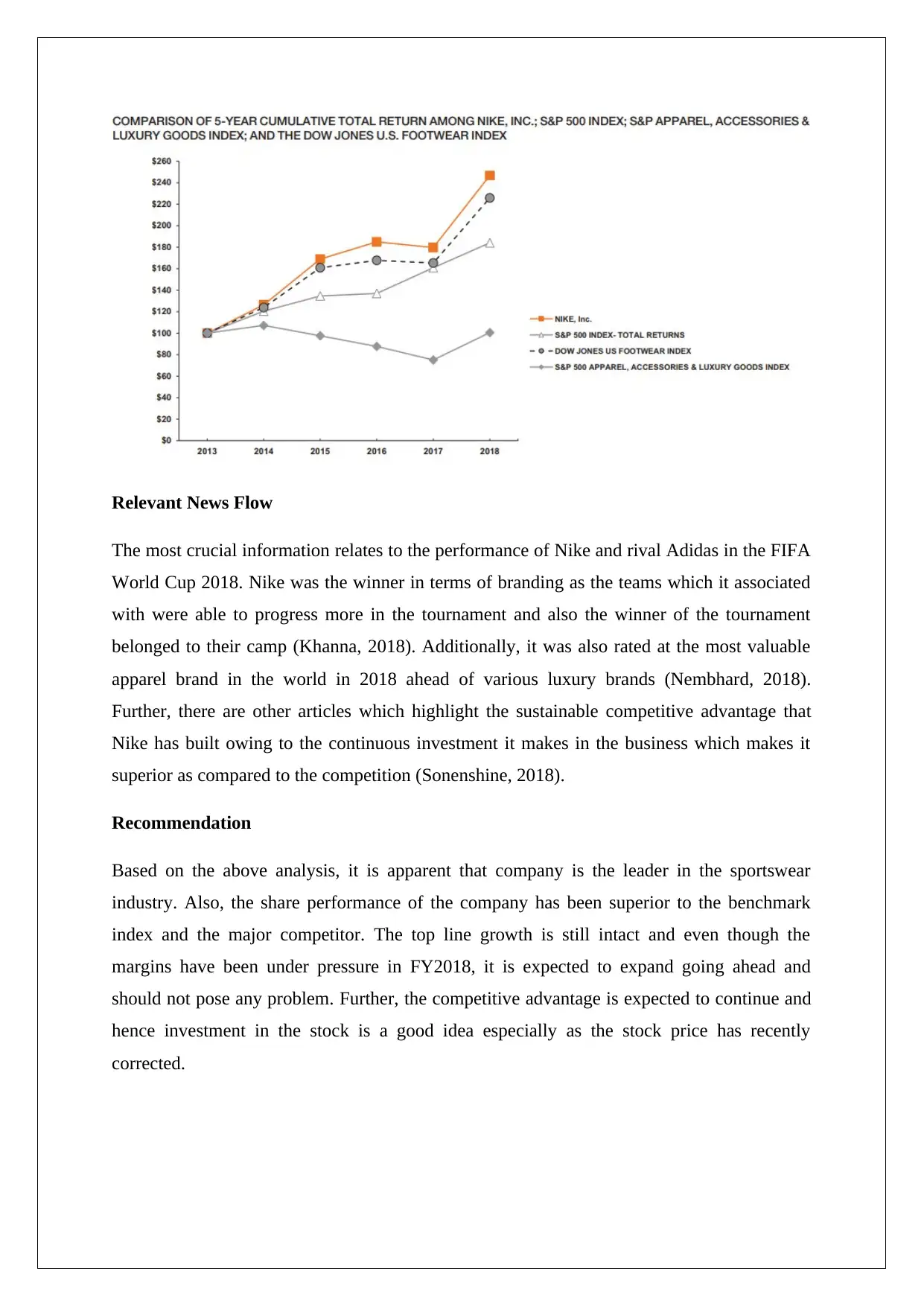

The company has also outperformed with S&P index as is apparent from the above graph.

This outperformance over a longer time frame is confirmed on the basis of the following

graph (Nike, 2018).

The share price movement of the Nike share over last one year is indicated below (Reuters,

2018).

The above graph also indicates comparison of the Nike stock price movement over the last

one year with Adidas. It is clearly apparent that the Nike stock has outperformed the

competitor in terms of stock returns (Reuters, 2018).

The company has also outperformed with S&P index as is apparent from the above graph.

This outperformance over a longer time frame is confirmed on the basis of the following

graph (Nike, 2018).

Relevant News Flow

The most crucial information relates to the performance of Nike and rival Adidas in the FIFA

World Cup 2018. Nike was the winner in terms of branding as the teams which it associated

with were able to progress more in the tournament and also the winner of the tournament

belonged to their camp (Khanna, 2018). Additionally, it was also rated at the most valuable

apparel brand in the world in 2018 ahead of various luxury brands (Nembhard, 2018).

Further, there are other articles which highlight the sustainable competitive advantage that

Nike has built owing to the continuous investment it makes in the business which makes it

superior as compared to the competition (Sonenshine, 2018).

Recommendation

Based on the above analysis, it is apparent that company is the leader in the sportswear

industry. Also, the share performance of the company has been superior to the benchmark

index and the major competitor. The top line growth is still intact and even though the

margins have been under pressure in FY2018, it is expected to expand going ahead and

should not pose any problem. Further, the competitive advantage is expected to continue and

hence investment in the stock is a good idea especially as the stock price has recently

corrected.

The most crucial information relates to the performance of Nike and rival Adidas in the FIFA

World Cup 2018. Nike was the winner in terms of branding as the teams which it associated

with were able to progress more in the tournament and also the winner of the tournament

belonged to their camp (Khanna, 2018). Additionally, it was also rated at the most valuable

apparel brand in the world in 2018 ahead of various luxury brands (Nembhard, 2018).

Further, there are other articles which highlight the sustainable competitive advantage that

Nike has built owing to the continuous investment it makes in the business which makes it

superior as compared to the competition (Sonenshine, 2018).

Recommendation

Based on the above analysis, it is apparent that company is the leader in the sportswear

industry. Also, the share performance of the company has been superior to the benchmark

index and the major competitor. The top line growth is still intact and even though the

margins have been under pressure in FY2018, it is expected to expand going ahead and

should not pose any problem. Further, the competitive advantage is expected to continue and

hence investment in the stock is a good idea especially as the stock price has recently

corrected.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

IASplus (2018) Conceptual Framework for Financial Reporting 2018, Retrieved from

https://www.iasplus.com/en/standards/other/framework

IASplus (n.d.) Inventories: Key differences between U.S. GAAP and IFRSs, Retrieved from

https://www.iasplus.com/en-us/standards/ifrs-usgaap/inventories

Khanna, A. (2018) Nike beats Adidas to win FIFA World Cup 2018, Retrieved from

https://www.insidesport.co/nike-beats-adidas-to-win-fifa-world-cup-2018/

MASB (2011) The Conceptual Framework for Financial Reporting, Retrieved from

http://www.masb.org.my/pdf.php?pdf=conceptual%20framework

%20042015t.pdf&file_path=pdf

Navigating accounting (nd) Accounting for Long-term Assets, Long-term Debt and Leases,

Retrieved from

http://www.navigatingaccounting.com/sites/default/files/Posted/Chapters/Ch_10_db/

3%20Wbn/6_txt/Documents/Acrobat/Long-term_assets_long-term_debt_leases.pdf

Nembhard, C. (2018) Nike remains the most valuable apparel brand in 2018, Retrieved from

https://www.highsnobiety.com/p/nike-most-valuable-apparel-brand-2018/

Nike (2018) 2018 Form 10-K, Retrieved from

https://s1.q4cdn.com/806093406/files/doc_financials/2018/ar/docs/nike-2018-form-

10K.pdf

Reuters (2018) Nike Inc (NKE.N), Retrieved from

https://www.reuters.com/finance/stocks/chart/NKE.N

Sonenshine, J. (2018) Nike's competitive advantage is a lot like Amazon's, Retrieved from

https://www.businessinsider.in/Nikes-competitive-advantage-is-a-lot-like-Amazons/

articleshow/64798603.cms

IASplus (2018) Conceptual Framework for Financial Reporting 2018, Retrieved from

https://www.iasplus.com/en/standards/other/framework

IASplus (n.d.) Inventories: Key differences between U.S. GAAP and IFRSs, Retrieved from

https://www.iasplus.com/en-us/standards/ifrs-usgaap/inventories

Khanna, A. (2018) Nike beats Adidas to win FIFA World Cup 2018, Retrieved from

https://www.insidesport.co/nike-beats-adidas-to-win-fifa-world-cup-2018/

MASB (2011) The Conceptual Framework for Financial Reporting, Retrieved from

http://www.masb.org.my/pdf.php?pdf=conceptual%20framework

%20042015t.pdf&file_path=pdf

Navigating accounting (nd) Accounting for Long-term Assets, Long-term Debt and Leases,

Retrieved from

http://www.navigatingaccounting.com/sites/default/files/Posted/Chapters/Ch_10_db/

3%20Wbn/6_txt/Documents/Acrobat/Long-term_assets_long-term_debt_leases.pdf

Nembhard, C. (2018) Nike remains the most valuable apparel brand in 2018, Retrieved from

https://www.highsnobiety.com/p/nike-most-valuable-apparel-brand-2018/

Nike (2018) 2018 Form 10-K, Retrieved from

https://s1.q4cdn.com/806093406/files/doc_financials/2018/ar/docs/nike-2018-form-

10K.pdf

Reuters (2018) Nike Inc (NKE.N), Retrieved from

https://www.reuters.com/finance/stocks/chart/NKE.N

Sonenshine, J. (2018) Nike's competitive advantage is a lot like Amazon's, Retrieved from

https://www.businessinsider.in/Nikes-competitive-advantage-is-a-lot-like-Amazons/

articleshow/64798603.cms

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.