ACC00724 Accounting for Managers: Financial Statement Ratio Analysis

VerifiedAdded on 2023/06/15

|10

|1773

|55

Homework Assignment

AI Summary

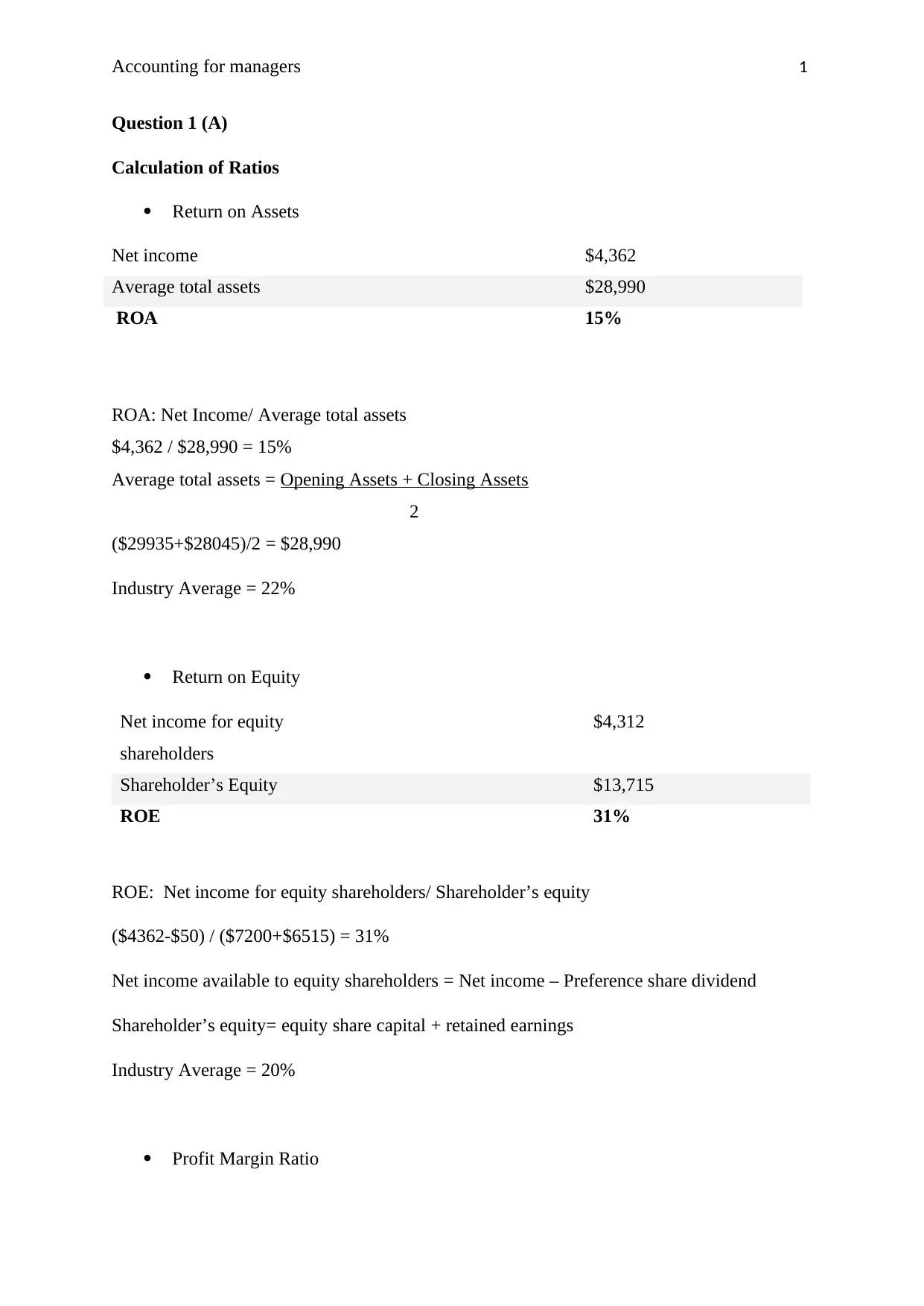

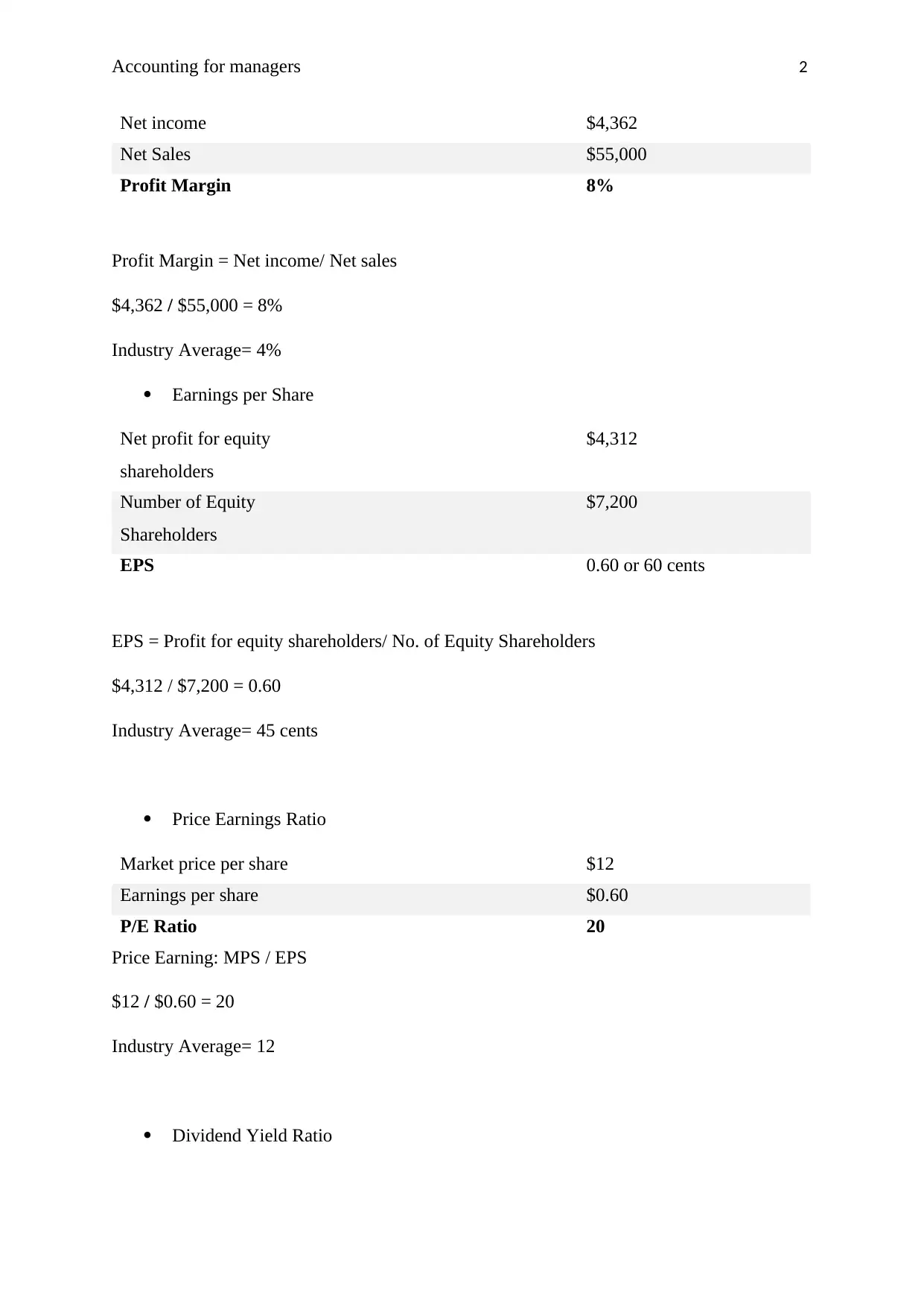

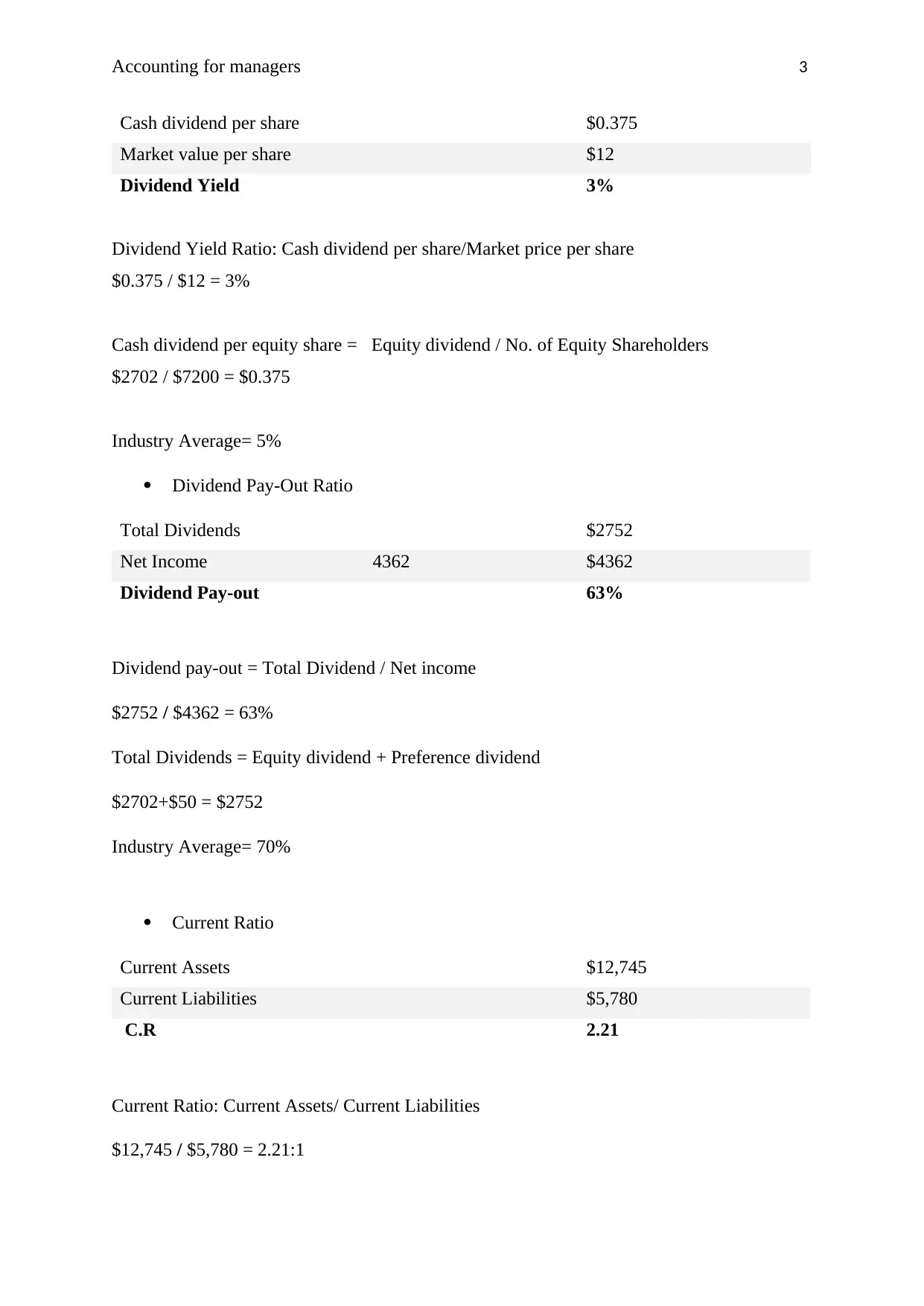

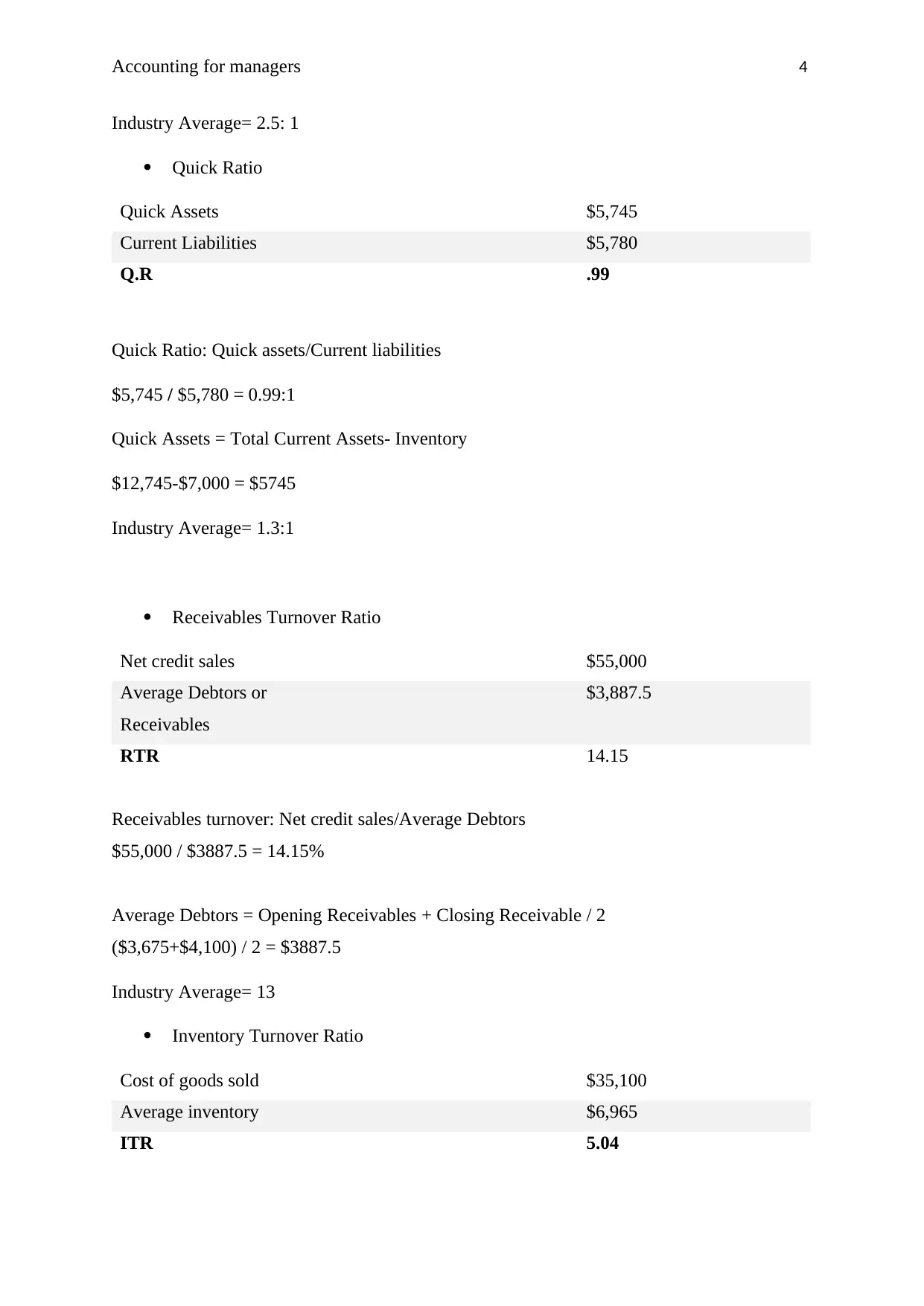

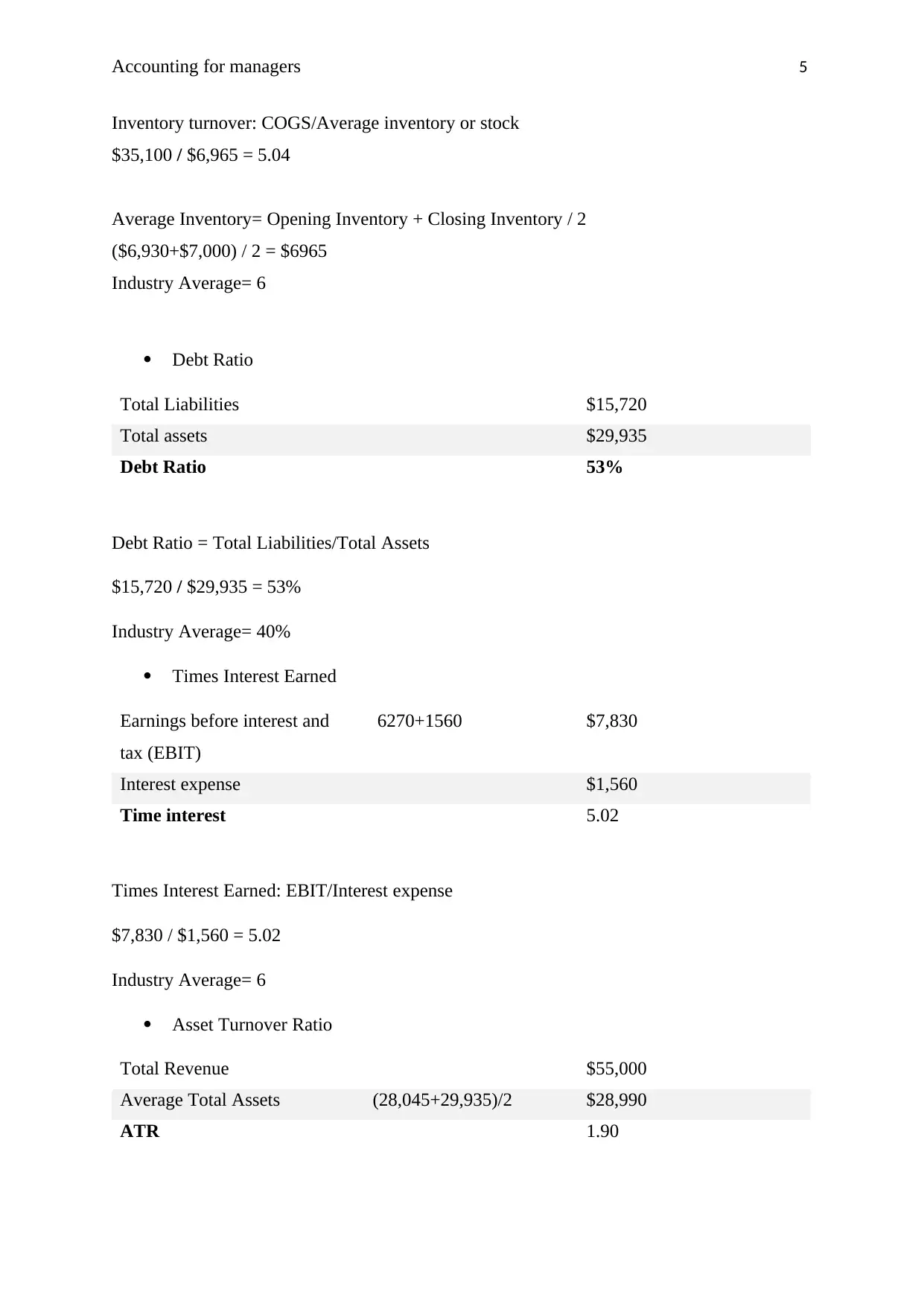

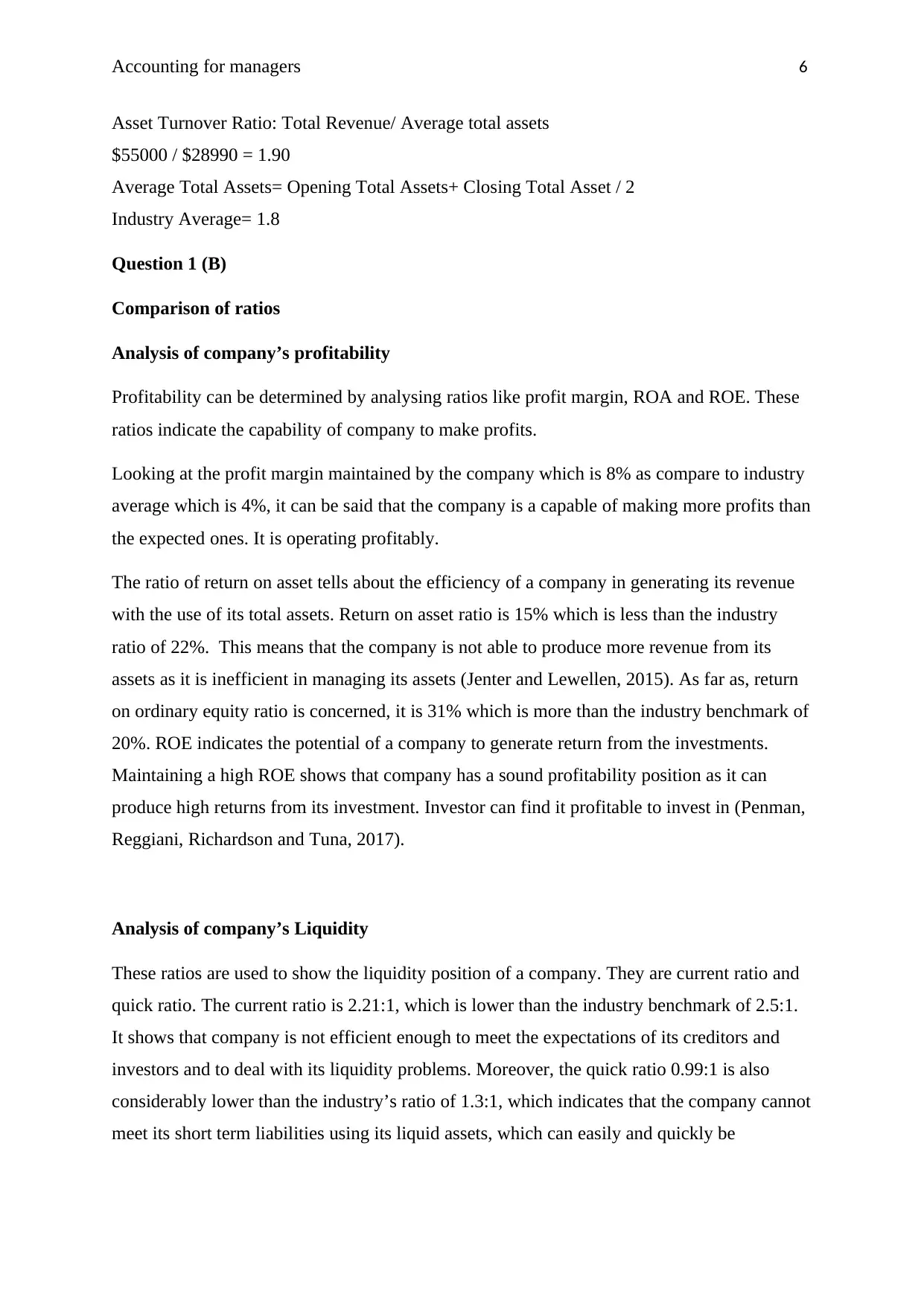

This assignment provides a comprehensive financial ratio analysis of Nimbin Pty Ltd, utilizing financial statements to calculate and interpret key metrics such as Return on Assets (ROA), Return on Equity (ROE), Profit Margin, Earnings per Share (EPS), and various liquidity and solvency ratios. The analysis compares these ratios against industry averages to assess the company's profitability, liquidity, and financial gearing. Additionally, the assignment addresses the accounting treatment of human resources and examines the impact of various transactions on the statement of financial position, statement of financial performance, and statement of cash flows. This document is available on Desklib, a platform offering a wide range of study tools and solved assignments for students.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.