Management Accounting Report: Financial Problem Solving for NISA

VerifiedAdded on 2023/01/13

|15

|3135

|64

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within an organizational context, specifically focusing on NISA, a retail business. It explores the importance of management accounting for decision-making, cost control, and profit maximization. The report details various management accounting techniques, including job costing, budget reports, inventory reports, and accounts receivable aging reports, and evaluates their benefits. It also covers the calculation of costs and preparation of profitability statements using both absorption and marginal costing methods. Furthermore, the report examines different planning tools for budgetary control, such as cash budgets, operating budgets, and investment appraisal tools, analyzing their advantages, disadvantages, and applications in forecasting and responding to financial problems. The analysis includes a comparison of how these tools can be utilized to address financial challenges and lead organizations towards sustainable success, concluding with a summary of the key findings and recommendations for NISA.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................4

TASK 1......................................................................................................................................4

Explaining the principles of management accounting and stating its importance pertaining

to integration within an organisation......................................................................................4

Explaining different techniques and methods used for management accounting reporting. .4

Evaluating the benefits of MA systems and their application within an organisational

context....................................................................................................................................5

TASK 2......................................................................................................................................8

Calculating cost and preparing profitability statements as per absorption & marginal

costing....................................................................................................................................8

TASK 3....................................................................................................................................10

Explaining the advantages and disadvantages of different types of planning tools used for

budgetary control.................................................................................................................10

Analyzing the use of different planning tools and their application for preparing and

forecasting budgets...............................................................................................................12

Comparing how varied MA tools can be used for responding financial problems..............13

Analyzing how management accounting can lead organizations to sustainable success.....14

CONCLUSION........................................................................................................................14

REFERENCES.........................................................................................................................15

INTRODUCTION......................................................................................................................4

TASK 1......................................................................................................................................4

Explaining the principles of management accounting and stating its importance pertaining

to integration within an organisation......................................................................................4

Explaining different techniques and methods used for management accounting reporting. .4

Evaluating the benefits of MA systems and their application within an organisational

context....................................................................................................................................5

TASK 2......................................................................................................................................8

Calculating cost and preparing profitability statements as per absorption & marginal

costing....................................................................................................................................8

TASK 3....................................................................................................................................10

Explaining the advantages and disadvantages of different types of planning tools used for

budgetary control.................................................................................................................10

Analyzing the use of different planning tools and their application for preparing and

forecasting budgets...............................................................................................................12

Comparing how varied MA tools can be used for responding financial problems..............13

Analyzing how management accounting can lead organizations to sustainable success.....14

CONCLUSION........................................................................................................................14

REFERENCES.........................................................................................................................15

INTRODUCTION

In the recent times, every business unit is placing emphasis on employing

management accounting (MA) system with the motive to make optimum utilization of

financial resources. Moreover, such system lay focus on cost control as well as profit

maximization and thereby contributes in organizational success. For this project, NISA has

been selected which offers retail products or services to the customers. In this, report will

shed light on different system that can be used by the firm for evaluation and reporting

purpose. Besides this, report will shed light on the tools that assists in planning as well as

solving monetary problems effectually.

TASK 1

Explaining the principles of management accounting and stating its importance pertaining to

integration within an organisation

Management accounting may be presented as a process of offering financial

information and resources to the managers for decision making aspects (Weetman, 2019).

Principles of management accounting

Cost reduction

Presents solution considering both controllable and non-controllable cost

Optimum utilization of resources

Importance of management accounting

Helps in setting budgets or financial plans for upcoming time period

Assists in setting prices for the products or services

Provides management team with timely information for planning & decision making

purpose (Otley, 2016).

Explaining different techniques and methods used for management accounting reporting

Manger of Nisa prepares managerial reports for providing the team of higher

management with suitable information about internal performance. This in turn helps in

several aspects regarding panning, decision making as well as measuring and evaluating

In the recent times, every business unit is placing emphasis on employing

management accounting (MA) system with the motive to make optimum utilization of

financial resources. Moreover, such system lay focus on cost control as well as profit

maximization and thereby contributes in organizational success. For this project, NISA has

been selected which offers retail products or services to the customers. In this, report will

shed light on different system that can be used by the firm for evaluation and reporting

purpose. Besides this, report will shed light on the tools that assists in planning as well as

solving monetary problems effectually.

TASK 1

Explaining the principles of management accounting and stating its importance pertaining to

integration within an organisation

Management accounting may be presented as a process of offering financial

information and resources to the managers for decision making aspects (Weetman, 2019).

Principles of management accounting

Cost reduction

Presents solution considering both controllable and non-controllable cost

Optimum utilization of resources

Importance of management accounting

Helps in setting budgets or financial plans for upcoming time period

Assists in setting prices for the products or services

Provides management team with timely information for planning & decision making

purpose (Otley, 2016).

Explaining different techniques and methods used for management accounting reporting

Manger of Nisa prepares managerial reports for providing the team of higher

management with suitable information about internal performance. This in turn helps in

several aspects regarding panning, decision making as well as measuring and evaluating

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

performance. Reports which can be prepared by Nisa for decision making purpose are

enumerated below:

Job cost report: This report furnishes information about expenditure incurred while

performing specific job. It helps in doing evaluation of existing performance over estimated

revenue and thereby highlights profitability related to each job. Through this, business unit

can make efforts on the profitable areas and thereby improves performance level.

Budget report: It assists manager in doing assessment of departmental performance

and controlling cost. Further, variances found in the actual performance also help in setting

budget for the near future (Types of managerial reports, 2020). In addition to this, owner of

Nisa can also use this report for offering incentives to the employees.

Inventory report: By preparing and using this report manager of Nisa can make

manufacturing process more efficient. It contains information about wastage, cost level and

overhead expenses in relation to inventory usage and management (Cooper, Ezzamel and Qu,

2017). Along with this, inventory report also helps in doing comparison of different assembly

lines and thereby helps in setting bonuses for the best performing areas.

Accounts receivable ageing report: By this, cash flow can be managed and monitored

by Nisa prominently. Moreover, it presents time period from which debtor’s payment is due.

Through this, manager can ascertain customers who are facing difficulty in paying their

balances. In this way, such report helps in assessing problems that take place in company’s

collection process. Referring all these aspects, firm can take decision pertaining to allowing

credit extension to the customers.

Evaluating the benefits of MA systems and their application within an organisational context

Applicability and benefits of varied MA tools in the context of Nisa is enumerated

below:

Job costing

According to this, cost of production is determined referring to the number of

completed jobs. By applying this, manager of Nisa can identify whether production cost

exceeds overheads and price of material. Thus, referring this, resources can be used in the

profitable areas for improving overall performance.

enumerated below:

Job cost report: This report furnishes information about expenditure incurred while

performing specific job. It helps in doing evaluation of existing performance over estimated

revenue and thereby highlights profitability related to each job. Through this, business unit

can make efforts on the profitable areas and thereby improves performance level.

Budget report: It assists manager in doing assessment of departmental performance

and controlling cost. Further, variances found in the actual performance also help in setting

budget for the near future (Types of managerial reports, 2020). In addition to this, owner of

Nisa can also use this report for offering incentives to the employees.

Inventory report: By preparing and using this report manager of Nisa can make

manufacturing process more efficient. It contains information about wastage, cost level and

overhead expenses in relation to inventory usage and management (Cooper, Ezzamel and Qu,

2017). Along with this, inventory report also helps in doing comparison of different assembly

lines and thereby helps in setting bonuses for the best performing areas.

Accounts receivable ageing report: By this, cash flow can be managed and monitored

by Nisa prominently. Moreover, it presents time period from which debtor’s payment is due.

Through this, manager can ascertain customers who are facing difficulty in paying their

balances. In this way, such report helps in assessing problems that take place in company’s

collection process. Referring all these aspects, firm can take decision pertaining to allowing

credit extension to the customers.

Evaluating the benefits of MA systems and their application within an organisational context

Applicability and benefits of varied MA tools in the context of Nisa is enumerated

below:

Job costing

According to this, cost of production is determined referring to the number of

completed jobs. By applying this, manager of Nisa can identify whether production cost

exceeds overheads and price of material. Thus, referring this, resources can be used in the

profitable areas for improving overall performance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages Disadvantages

Profitability can be determined

pertaining to each job.

Helps in doing estimation about cost

(Job costing advantages and

disadvantages, 2020)

Requires clerical work

Time consuming process

Cost accounting

Such system of management accounting assists in determining cost of production

(both fixed & variable). In other words, by accumulating both direct and indirect expenses

manager of Nisa can assess production cost. Further, by adding mark-up or desired profit

margin in the unit cost product’s price can be ascertained (Maas, Schaltegger and Crutzen,

2016). By using following formula manager of Nisa can set suitable price:

Price = unit cost + (cost * profit%)

Advantages Disadvantages

Facilitates elimination of wastage,

losses and inefficiencies from

operations.

Ensures cost reduction

Helps in identifying reasons behind

profit or loss (Advantages and

Disadvantages of Cost Accounting,

2020)

Assists in setting suitable prices of

product

Offers framework for decision

making by taking into account

previous figures, whereas

management is concerned about

future.

Leads problems of under and over

absorption

Inventory management system

Profitability can be determined

pertaining to each job.

Helps in doing estimation about cost

(Job costing advantages and

disadvantages, 2020)

Requires clerical work

Time consuming process

Cost accounting

Such system of management accounting assists in determining cost of production

(both fixed & variable). In other words, by accumulating both direct and indirect expenses

manager of Nisa can assess production cost. Further, by adding mark-up or desired profit

margin in the unit cost product’s price can be ascertained (Maas, Schaltegger and Crutzen,

2016). By using following formula manager of Nisa can set suitable price:

Price = unit cost + (cost * profit%)

Advantages Disadvantages

Facilitates elimination of wastage,

losses and inefficiencies from

operations.

Ensures cost reduction

Helps in identifying reasons behind

profit or loss (Advantages and

Disadvantages of Cost Accounting,

2020)

Assists in setting suitable prices of

product

Offers framework for decision

making by taking into account

previous figures, whereas

management is concerned about

future.

Leads problems of under and over

absorption

Inventory management system

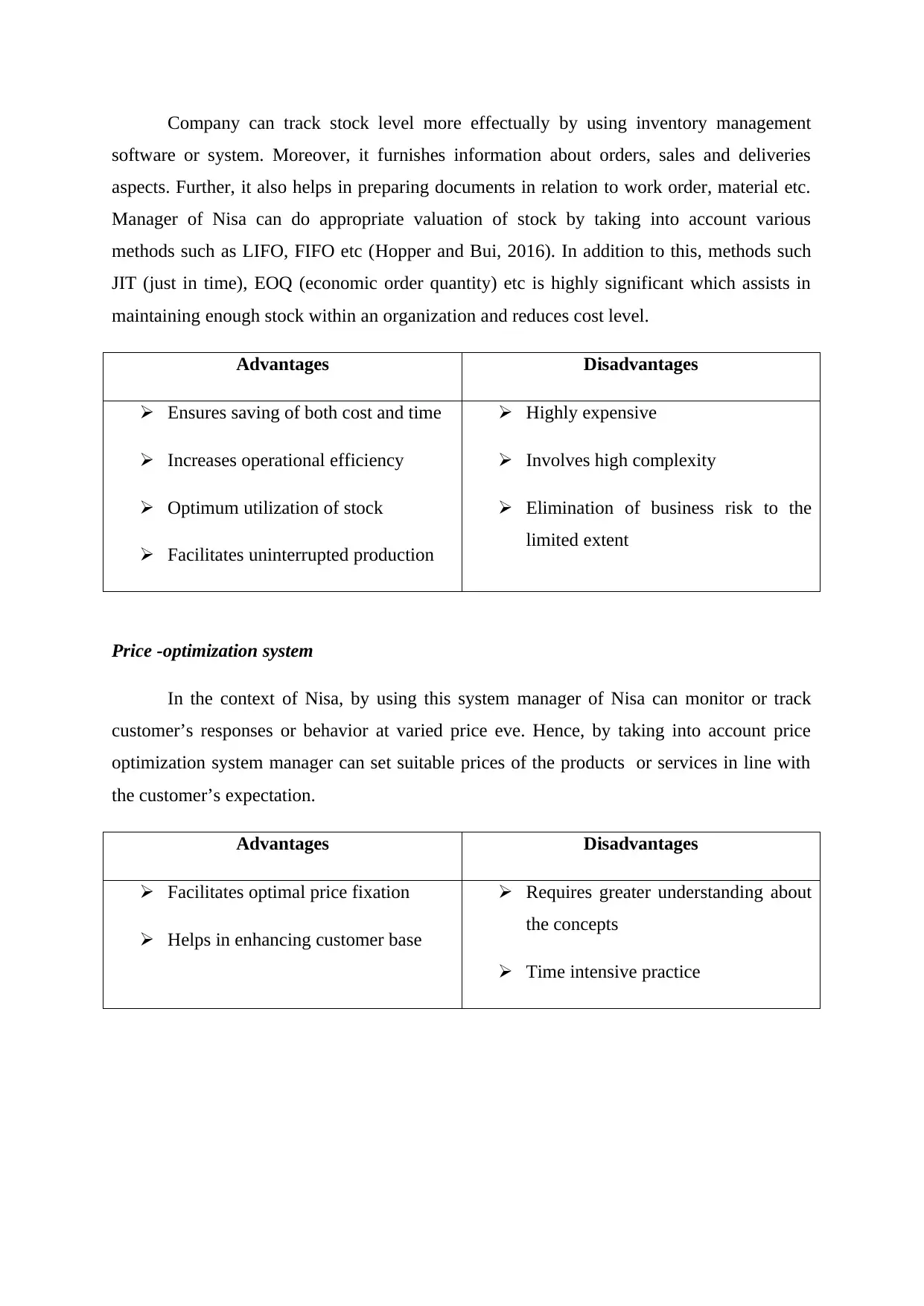

Company can track stock level more effectually by using inventory management

software or system. Moreover, it furnishes information about orders, sales and deliveries

aspects. Further, it also helps in preparing documents in relation to work order, material etc.

Manager of Nisa can do appropriate valuation of stock by taking into account various

methods such as LIFO, FIFO etc (Hopper and Bui, 2016). In addition to this, methods such

JIT (just in time), EOQ (economic order quantity) etc is highly significant which assists in

maintaining enough stock within an organization and reduces cost level.

Advantages Disadvantages

Ensures saving of both cost and time

Increases operational efficiency

Optimum utilization of stock

Facilitates uninterrupted production

Highly expensive

Involves high complexity

Elimination of business risk to the

limited extent

Price -optimization system

In the context of Nisa, by using this system manager of Nisa can monitor or track

customer’s responses or behavior at varied price eve. Hence, by taking into account price

optimization system manager can set suitable prices of the products or services in line with

the customer’s expectation.

Advantages Disadvantages

Facilitates optimal price fixation

Helps in enhancing customer base

Requires greater understanding about

the concepts

Time intensive practice

software or system. Moreover, it furnishes information about orders, sales and deliveries

aspects. Further, it also helps in preparing documents in relation to work order, material etc.

Manager of Nisa can do appropriate valuation of stock by taking into account various

methods such as LIFO, FIFO etc (Hopper and Bui, 2016). In addition to this, methods such

JIT (just in time), EOQ (economic order quantity) etc is highly significant which assists in

maintaining enough stock within an organization and reduces cost level.

Advantages Disadvantages

Ensures saving of both cost and time

Increases operational efficiency

Optimum utilization of stock

Facilitates uninterrupted production

Highly expensive

Involves high complexity

Elimination of business risk to the

limited extent

Price -optimization system

In the context of Nisa, by using this system manager of Nisa can monitor or track

customer’s responses or behavior at varied price eve. Hence, by taking into account price

optimization system manager can set suitable prices of the products or services in line with

the customer’s expectation.

Advantages Disadvantages

Facilitates optimal price fixation

Helps in enhancing customer base

Requires greater understanding about

the concepts

Time intensive practice

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

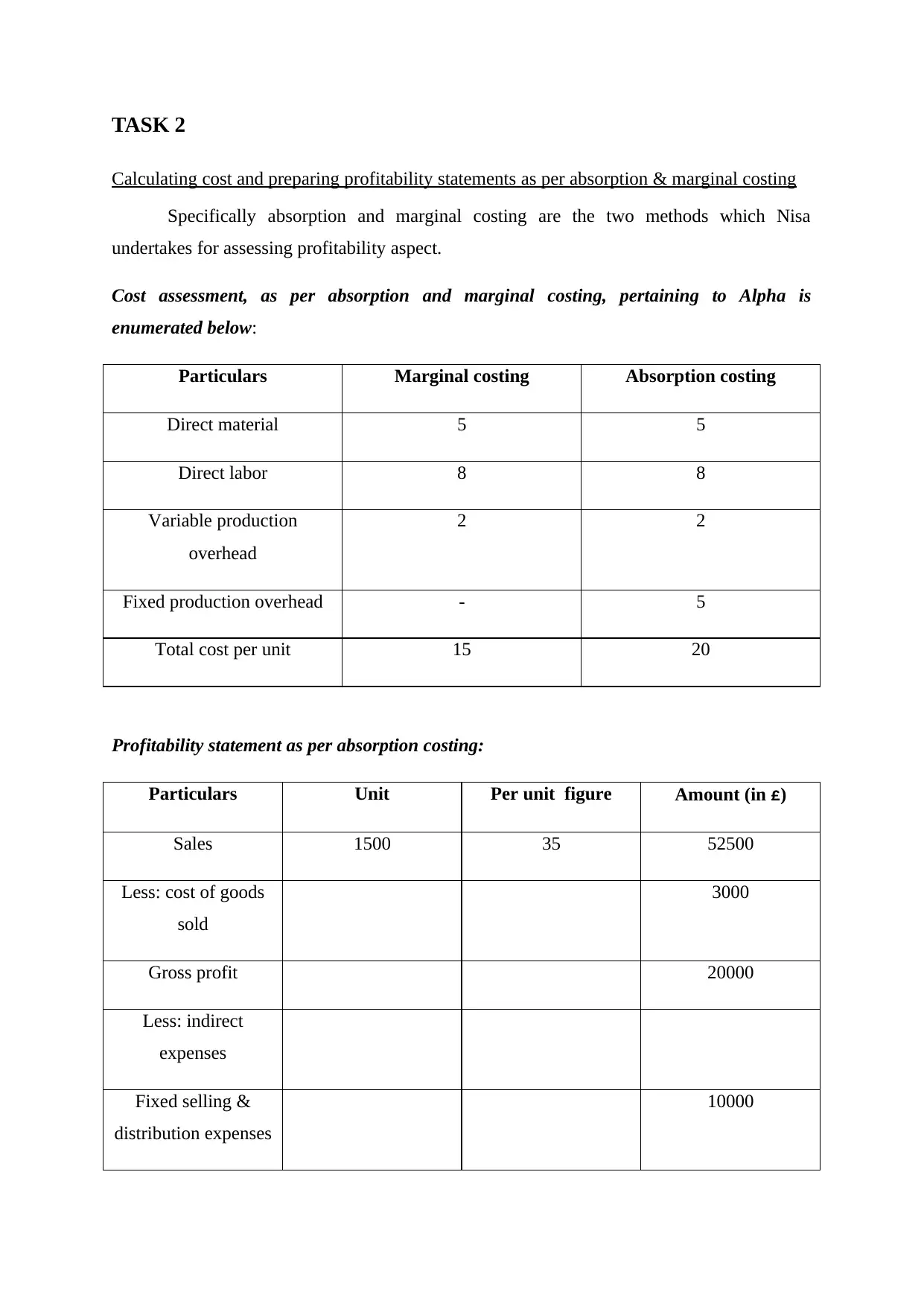

TASK 2

Calculating cost and preparing profitability statements as per absorption & marginal costing

Specifically absorption and marginal costing are the two methods which Nisa

undertakes for assessing profitability aspect.

Cost assessment, as per absorption and marginal costing, pertaining to Alpha is

enumerated below:

Particulars Marginal costing Absorption costing

Direct material 5 5

Direct labor 8 8

Variable production

overhead

2 2

Fixed production overhead - 5

Total cost per unit 15 20

Profitability statement as per absorption costing:

Particulars Unit Per unit figure Amount (in £)

Sales 1500 35 52500

Less: cost of goods

sold

3000

Gross profit 20000

Less: indirect

expenses

Fixed selling &

distribution expenses

10000

Calculating cost and preparing profitability statements as per absorption & marginal costing

Specifically absorption and marginal costing are the two methods which Nisa

undertakes for assessing profitability aspect.

Cost assessment, as per absorption and marginal costing, pertaining to Alpha is

enumerated below:

Particulars Marginal costing Absorption costing

Direct material 5 5

Direct labor 8 8

Variable production

overhead

2 2

Fixed production overhead - 5

Total cost per unit 15 20

Profitability statement as per absorption costing:

Particulars Unit Per unit figure Amount (in £)

Sales 1500 35 52500

Less: cost of goods

sold

3000

Gross profit 20000

Less: indirect

expenses

Fixed selling &

distribution expenses

10000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

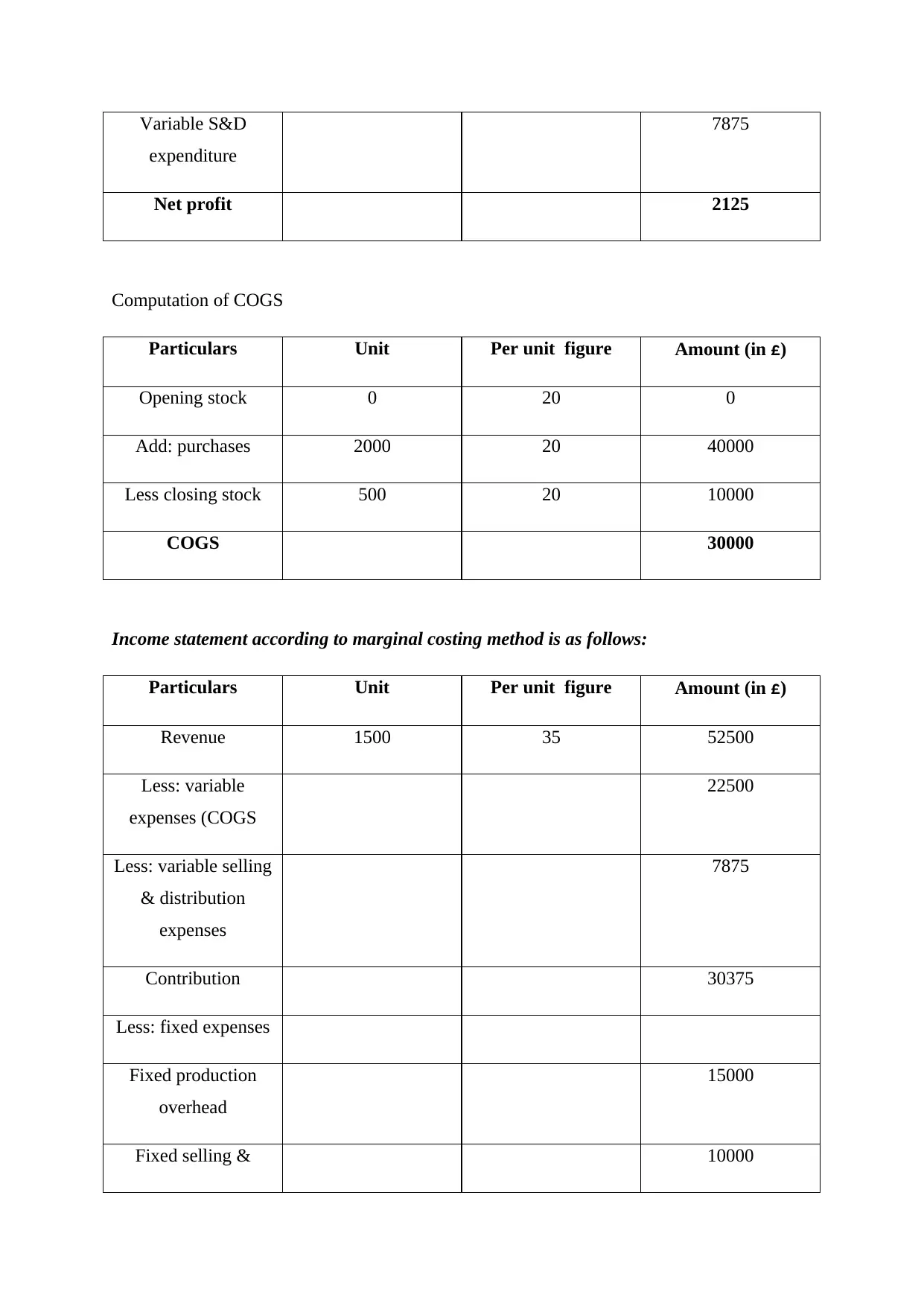

Variable S&D

expenditure

7875

Net profit 2125

Computation of COGS

Particulars Unit Per unit figure Amount (in £)

Opening stock 0 20 0

Add: purchases 2000 20 40000

Less closing stock 500 20 10000

COGS 30000

Income statement according to marginal costing method is as follows:

Particulars Unit Per unit figure Amount (in £)

Revenue 1500 35 52500

Less: variable

expenses (COGS

22500

Less: variable selling

& distribution

expenses

7875

Contribution 30375

Less: fixed expenses

Fixed production

overhead

15000

Fixed selling & 10000

expenditure

7875

Net profit 2125

Computation of COGS

Particulars Unit Per unit figure Amount (in £)

Opening stock 0 20 0

Add: purchases 2000 20 40000

Less closing stock 500 20 10000

COGS 30000

Income statement according to marginal costing method is as follows:

Particulars Unit Per unit figure Amount (in £)

Revenue 1500 35 52500

Less: variable

expenses (COGS

22500

Less: variable selling

& distribution

expenses

7875

Contribution 30375

Less: fixed expenses

Fixed production

overhead

15000

Fixed selling & 10000

distribution expenses

Profit 5375

Particulars Unit Per unit figure Amount (in £)

Opening stock 0 15 0

Add: purchases 2000 15 30000

Less closing stock 500 15 7500

COGS or total

variable cost

22500

By doing assessment, it has found that business unit should follow absorption costing

system for cost and profitability assessment. Moreover, absorption costing method presents

highly suitable view of production cost as it considers both fixed and variable expenses

(Geddes, 2020). This in turn gives clear indication about profitability aspect.

TASK 3

Explaining the advantages and disadvantages of different types of planning tools used for

budgetary control

There are several tools which Nisa can employ for the purpose of budgetary control

includes investment appraisal tools, cash and operating budget. By undertaking such

budgeting frameworks organization can monitor or compare expenses and thereby take

suitable measure for improvement (Ax and Greve, 2017).

Cash budget

It may be presented as financial framework which includes both estimated cash

inflows and outflows pertaining to the specific time frame (Weetman, 2019). By preparing

cash budget manager of Nisa would become able to know whether company has enough

funds for performing business activities or not.

Advantages Disadvantages

Profit 5375

Particulars Unit Per unit figure Amount (in £)

Opening stock 0 15 0

Add: purchases 2000 15 30000

Less closing stock 500 15 7500

COGS or total

variable cost

22500

By doing assessment, it has found that business unit should follow absorption costing

system for cost and profitability assessment. Moreover, absorption costing method presents

highly suitable view of production cost as it considers both fixed and variable expenses

(Geddes, 2020). This in turn gives clear indication about profitability aspect.

TASK 3

Explaining the advantages and disadvantages of different types of planning tools used for

budgetary control

There are several tools which Nisa can employ for the purpose of budgetary control

includes investment appraisal tools, cash and operating budget. By undertaking such

budgeting frameworks organization can monitor or compare expenses and thereby take

suitable measure for improvement (Ax and Greve, 2017).

Cash budget

It may be presented as financial framework which includes both estimated cash

inflows and outflows pertaining to the specific time frame (Weetman, 2019). By preparing

cash budget manager of Nisa would become able to know whether company has enough

funds for performing business activities or not.

Advantages Disadvantages

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

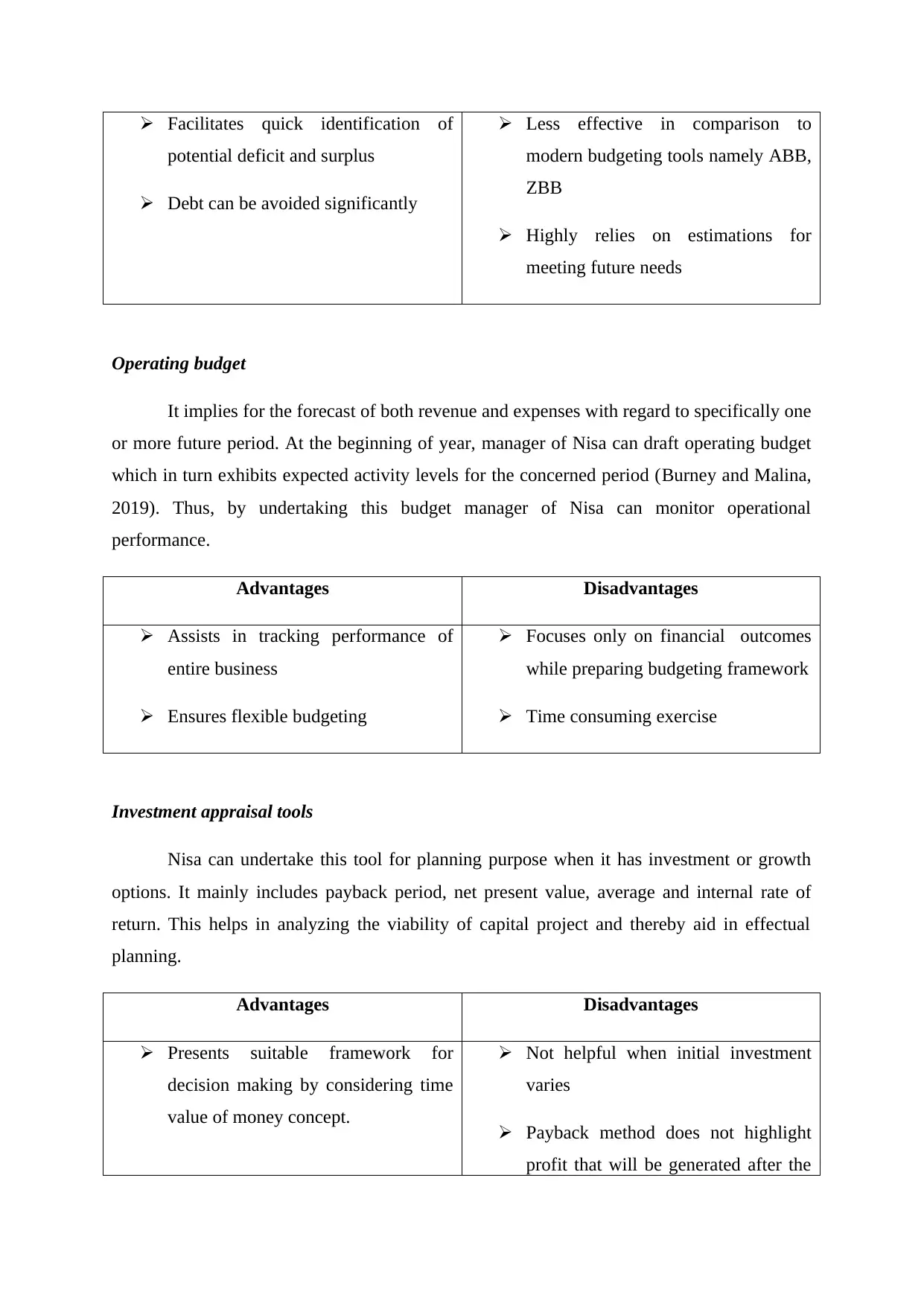

Facilitates quick identification of

potential deficit and surplus

Debt can be avoided significantly

Less effective in comparison to

modern budgeting tools namely ABB,

ZBB

Highly relies on estimations for

meeting future needs

Operating budget

It implies for the forecast of both revenue and expenses with regard to specifically one

or more future period. At the beginning of year, manager of Nisa can draft operating budget

which in turn exhibits expected activity levels for the concerned period (Burney and Malina,

2019). Thus, by undertaking this budget manager of Nisa can monitor operational

performance.

Advantages Disadvantages

Assists in tracking performance of

entire business

Ensures flexible budgeting

Focuses only on financial outcomes

while preparing budgeting framework

Time consuming exercise

Investment appraisal tools

Nisa can undertake this tool for planning purpose when it has investment or growth

options. It mainly includes payback period, net present value, average and internal rate of

return. This helps in analyzing the viability of capital project and thereby aid in effectual

planning.

Advantages Disadvantages

Presents suitable framework for

decision making by considering time

value of money concept.

Not helpful when initial investment

varies

Payback method does not highlight

profit that will be generated after the

potential deficit and surplus

Debt can be avoided significantly

Less effective in comparison to

modern budgeting tools namely ABB,

ZBB

Highly relies on estimations for

meeting future needs

Operating budget

It implies for the forecast of both revenue and expenses with regard to specifically one

or more future period. At the beginning of year, manager of Nisa can draft operating budget

which in turn exhibits expected activity levels for the concerned period (Burney and Malina,

2019). Thus, by undertaking this budget manager of Nisa can monitor operational

performance.

Advantages Disadvantages

Assists in tracking performance of

entire business

Ensures flexible budgeting

Focuses only on financial outcomes

while preparing budgeting framework

Time consuming exercise

Investment appraisal tools

Nisa can undertake this tool for planning purpose when it has investment or growth

options. It mainly includes payback period, net present value, average and internal rate of

return. This helps in analyzing the viability of capital project and thereby aid in effectual

planning.

Advantages Disadvantages

Presents suitable framework for

decision making by considering time

value of money concept.

Not helpful when initial investment

varies

Payback method does not highlight

profit that will be generated after the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Clearly indicates return associated

with project

recovery of initial investment.

Analyzing the use of different planning tools and their application for preparing and

forecasting budgets

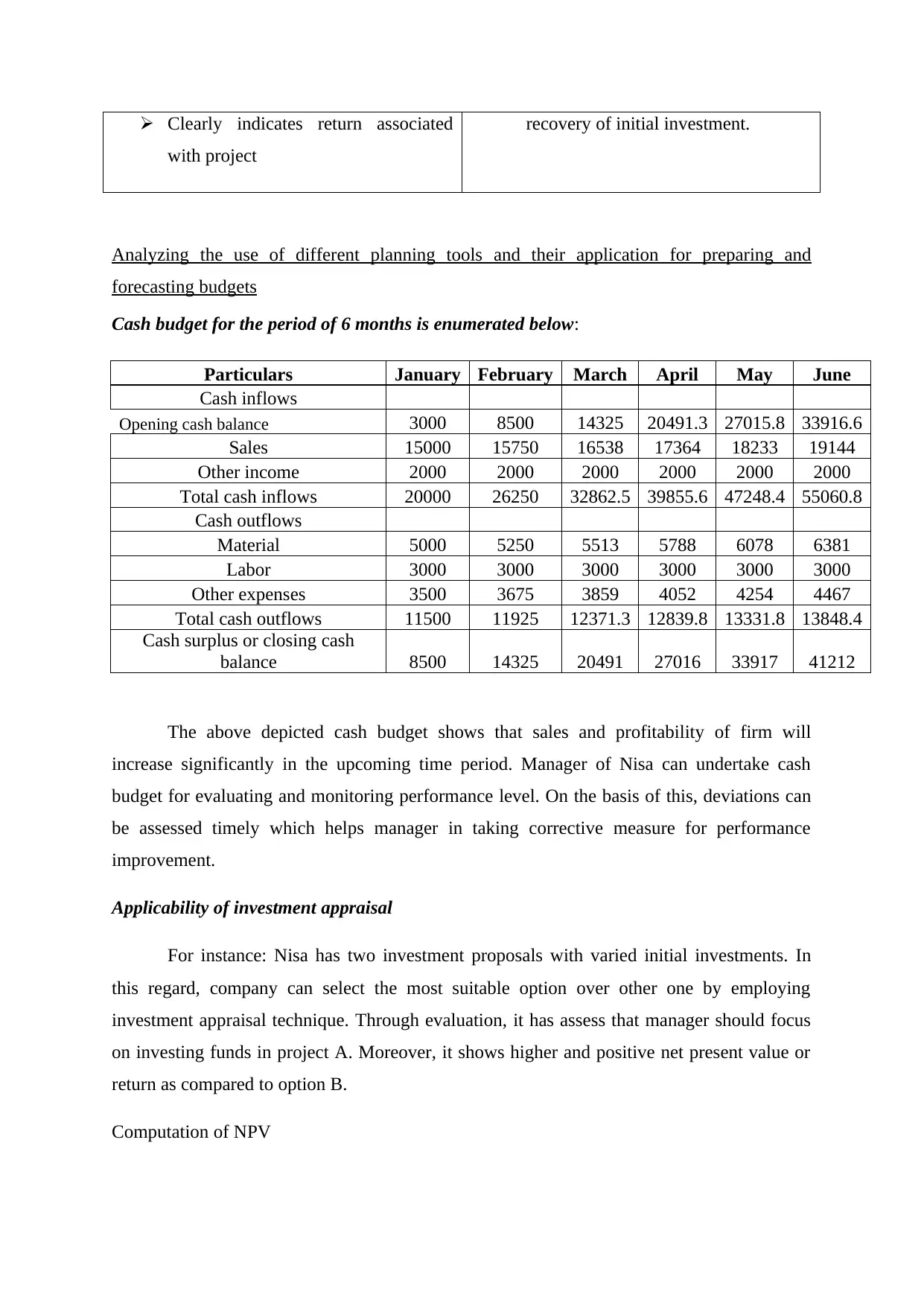

Cash budget for the period of 6 months is enumerated below:

Particulars January February March April May June

Cash inflows

Opening cash balance 3000 8500 14325 20491.3 27015.8 33916.6

Sales 15000 15750 16538 17364 18233 19144

Other income 2000 2000 2000 2000 2000 2000

Total cash inflows 20000 26250 32862.5 39855.6 47248.4 55060.8

Cash outflows

Material 5000 5250 5513 5788 6078 6381

Labor 3000 3000 3000 3000 3000 3000

Other expenses 3500 3675 3859 4052 4254 4467

Total cash outflows 11500 11925 12371.3 12839.8 13331.8 13848.4

Cash surplus or closing cash

balance 8500 14325 20491 27016 33917 41212

The above depicted cash budget shows that sales and profitability of firm will

increase significantly in the upcoming time period. Manager of Nisa can undertake cash

budget for evaluating and monitoring performance level. On the basis of this, deviations can

be assessed timely which helps manager in taking corrective measure for performance

improvement.

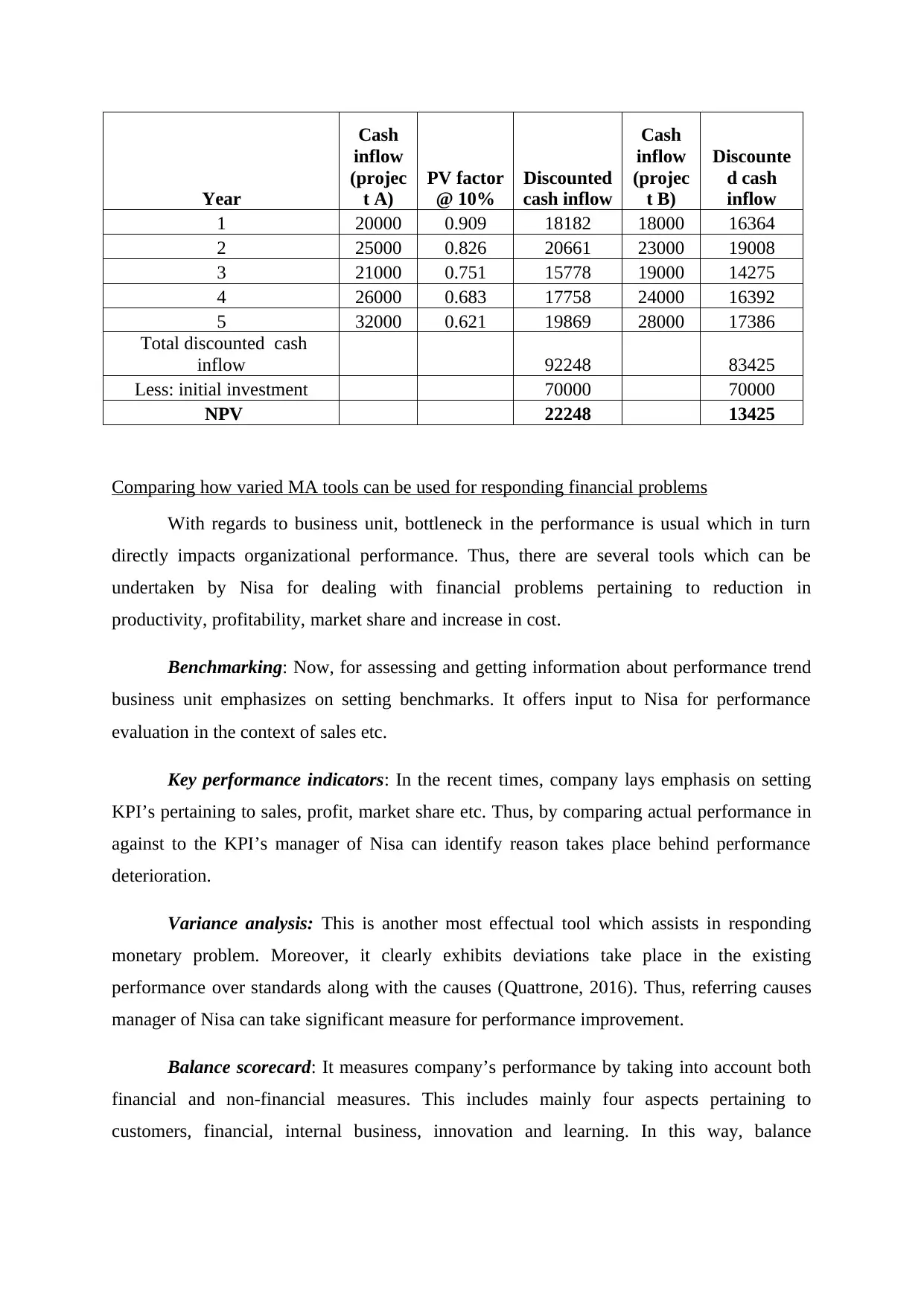

Applicability of investment appraisal

For instance: Nisa has two investment proposals with varied initial investments. In

this regard, company can select the most suitable option over other one by employing

investment appraisal technique. Through evaluation, it has assess that manager should focus

on investing funds in project A. Moreover, it shows higher and positive net present value or

return as compared to option B.

Computation of NPV

with project

recovery of initial investment.

Analyzing the use of different planning tools and their application for preparing and

forecasting budgets

Cash budget for the period of 6 months is enumerated below:

Particulars January February March April May June

Cash inflows

Opening cash balance 3000 8500 14325 20491.3 27015.8 33916.6

Sales 15000 15750 16538 17364 18233 19144

Other income 2000 2000 2000 2000 2000 2000

Total cash inflows 20000 26250 32862.5 39855.6 47248.4 55060.8

Cash outflows

Material 5000 5250 5513 5788 6078 6381

Labor 3000 3000 3000 3000 3000 3000

Other expenses 3500 3675 3859 4052 4254 4467

Total cash outflows 11500 11925 12371.3 12839.8 13331.8 13848.4

Cash surplus or closing cash

balance 8500 14325 20491 27016 33917 41212

The above depicted cash budget shows that sales and profitability of firm will

increase significantly in the upcoming time period. Manager of Nisa can undertake cash

budget for evaluating and monitoring performance level. On the basis of this, deviations can

be assessed timely which helps manager in taking corrective measure for performance

improvement.

Applicability of investment appraisal

For instance: Nisa has two investment proposals with varied initial investments. In

this regard, company can select the most suitable option over other one by employing

investment appraisal technique. Through evaluation, it has assess that manager should focus

on investing funds in project A. Moreover, it shows higher and positive net present value or

return as compared to option B.

Computation of NPV

Year

Cash

inflow

(projec

t A)

PV factor

@ 10%

Discounted

cash inflow

Cash

inflow

(projec

t B)

Discounte

d cash

inflow

1 20000 0.909 18182 18000 16364

2 25000 0.826 20661 23000 19008

3 21000 0.751 15778 19000 14275

4 26000 0.683 17758 24000 16392

5 32000 0.621 19869 28000 17386

Total discounted cash

inflow 92248 83425

Less: initial investment 70000 70000

NPV 22248 13425

Comparing how varied MA tools can be used for responding financial problems

With regards to business unit, bottleneck in the performance is usual which in turn

directly impacts organizational performance. Thus, there are several tools which can be

undertaken by Nisa for dealing with financial problems pertaining to reduction in

productivity, profitability, market share and increase in cost.

Benchmarking: Now, for assessing and getting information about performance trend

business unit emphasizes on setting benchmarks. It offers input to Nisa for performance

evaluation in the context of sales etc.

Key performance indicators: In the recent times, company lays emphasis on setting

KPI’s pertaining to sales, profit, market share etc. Thus, by comparing actual performance in

against to the KPI’s manager of Nisa can identify reason takes place behind performance

deterioration.

Variance analysis: This is another most effectual tool which assists in responding

monetary problem. Moreover, it clearly exhibits deviations take place in the existing

performance over standards along with the causes (Quattrone, 2016). Thus, referring causes

manager of Nisa can take significant measure for performance improvement.

Balance scorecard: It measures company’s performance by taking into account both

financial and non-financial measures. This includes mainly four aspects pertaining to

customers, financial, internal business, innovation and learning. In this way, balance

Cash

inflow

(projec

t A)

PV factor

@ 10%

Discounted

cash inflow

Cash

inflow

(projec

t B)

Discounte

d cash

inflow

1 20000 0.909 18182 18000 16364

2 25000 0.826 20661 23000 19008

3 21000 0.751 15778 19000 14275

4 26000 0.683 17758 24000 16392

5 32000 0.621 19869 28000 17386

Total discounted cash

inflow 92248 83425

Less: initial investment 70000 70000

NPV 22248 13425

Comparing how varied MA tools can be used for responding financial problems

With regards to business unit, bottleneck in the performance is usual which in turn

directly impacts organizational performance. Thus, there are several tools which can be

undertaken by Nisa for dealing with financial problems pertaining to reduction in

productivity, profitability, market share and increase in cost.

Benchmarking: Now, for assessing and getting information about performance trend

business unit emphasizes on setting benchmarks. It offers input to Nisa for performance

evaluation in the context of sales etc.

Key performance indicators: In the recent times, company lays emphasis on setting

KPI’s pertaining to sales, profit, market share etc. Thus, by comparing actual performance in

against to the KPI’s manager of Nisa can identify reason takes place behind performance

deterioration.

Variance analysis: This is another most effectual tool which assists in responding

monetary problem. Moreover, it clearly exhibits deviations take place in the existing

performance over standards along with the causes (Quattrone, 2016). Thus, referring causes

manager of Nisa can take significant measure for performance improvement.

Balance scorecard: It measures company’s performance by taking into account both

financial and non-financial measures. This includes mainly four aspects pertaining to

customers, financial, internal business, innovation and learning. In this way, balance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.