Management Accounting Report: Analysis of Nisa Retail Accounting

VerifiedAdded on 2020/01/28

|20

|5225

|114

Report

AI Summary

This report provides a comprehensive analysis of management accounting, using Nisa Retail as a case study. It begins with an introduction to management accounting, its functions, and various accounting systems like traditional, lean, throughput, and transfer accounting. The report delves into the uses of different accounting methods, including financial planning, cost accounting, and budgetary control. The benefits of management accounting, such as reduced expenses, improved cash flow, and enhanced decision-making, are also discussed. Furthermore, the report examines cost calculation methods, specifically marginal and absorption costing. It explores the advantages and disadvantages of different budgetary planning tools and evaluates management accounting techniques in responding to financial problems, with a focus on achieving success through effective financial management. The report includes calculations, evaluations, and recommendations for Nisa Retail's financial management practices.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction......................................................................................................................................3

Task 1 ..............................................................................................................................................3

P1 Explaining the management accounting along with the different kinds of management

accounting systems......................................................................................................................3

P2 Uses of different accounting methods in management accounting system reporting............5

M1 Benefits and uses of management accounting system...........................................................6

TASK 2 ...........................................................................................................................................7

P3 Calculation of cost using marginal and absorption costing....................................................7

D1 Critically evaluation of management accounting system....................................................11

M2 Range of management accounting techniques ...................................................................12

D2 Producing financial report that accurately apply and interpret data for a range of business

activities.....................................................................................................................................12

Task 3 ............................................................................................................................................13

P4 Advantages and disadvantages of different types of budgetary planning tools....................13

M3 Analyzing the different planning tools and applications for forecasting the budget...........13

D3 Evaluating the planning tools that helps in to solve financial problems..............................14

Task 4.............................................................................................................................................14

P5 Selecting the management accounting techniques towards responding the financial

problems.....................................................................................................................................14

M4 Management accounting responds to financial problems in order to achieve sucess ........15

Conclusion.....................................................................................................................................15

References......................................................................................................................................16

2

Introduction......................................................................................................................................3

Task 1 ..............................................................................................................................................3

P1 Explaining the management accounting along with the different kinds of management

accounting systems......................................................................................................................3

P2 Uses of different accounting methods in management accounting system reporting............5

M1 Benefits and uses of management accounting system...........................................................6

TASK 2 ...........................................................................................................................................7

P3 Calculation of cost using marginal and absorption costing....................................................7

D1 Critically evaluation of management accounting system....................................................11

M2 Range of management accounting techniques ...................................................................12

D2 Producing financial report that accurately apply and interpret data for a range of business

activities.....................................................................................................................................12

Task 3 ............................................................................................................................................13

P4 Advantages and disadvantages of different types of budgetary planning tools....................13

M3 Analyzing the different planning tools and applications for forecasting the budget...........13

D3 Evaluating the planning tools that helps in to solve financial problems..............................14

Task 4.............................................................................................................................................14

P5 Selecting the management accounting techniques towards responding the financial

problems.....................................................................................................................................14

M4 Management accounting responds to financial problems in order to achieve sucess ........15

Conclusion.....................................................................................................................................15

References......................................................................................................................................16

2

INTRODUCTION

Management accounting is the process of identifying, analyzing, recording and

presenting financial information that is used as internal information by management for

planning, decision making and control. It is also concerned with the providing helpful

information and reports to managers and entrepreneurs. It helps in planning of business

activities. Management accounting includes the integration of financial and non financial

statements that provide useful information to management that helps in to take effective decision

for the organization (Sullivan, 2017). The scope of management accounting is very wide it

contains all types of accounting information to particular organization.

The present report is based on management accounting and to understand this, Nisa case

study is taken in to consideration. It is one of the top leading retail chain in UK where it has been

offered wide range of product and services to customer at affordable prices. The choose firm

have 50 employees and an annual turnover is 500000 Euro. Various types of management

accounting techniques are to be used such as cost volume- profit analysis, marginal costing and

absorption accounting that helps in to evaluating the company financial condition. Nisa

accounting managers identifies and managing the accounting records for day to day activity

transactions. Management accounting officer are also responsible for preparing the budget and

controlling the expenses in order to manage high profitability of an organization. The main

objective of this report is to analyze existing cost accounting system and to develop product

costing on the basis of ABC.

TASK 1

P1 Explaining the management accounting along with the different kinds of management

accounting systems

Managerial accounting is the process of identifying, analyzing, recording and presenting

financial information that is used as internal information by management for planning, decision

making and controlling of business financial operations (Vitez, 2017). It is mainly concerned

with the providing helpful information and report to internal users such as managers and

entrepreneurs. Management accounting tools are may be different for different organization, it

basically depends on the size and policy of an organization. It increases the efficiency of an

3

Management accounting is the process of identifying, analyzing, recording and

presenting financial information that is used as internal information by management for

planning, decision making and control. It is also concerned with the providing helpful

information and reports to managers and entrepreneurs. It helps in planning of business

activities. Management accounting includes the integration of financial and non financial

statements that provide useful information to management that helps in to take effective decision

for the organization (Sullivan, 2017). The scope of management accounting is very wide it

contains all types of accounting information to particular organization.

The present report is based on management accounting and to understand this, Nisa case

study is taken in to consideration. It is one of the top leading retail chain in UK where it has been

offered wide range of product and services to customer at affordable prices. The choose firm

have 50 employees and an annual turnover is 500000 Euro. Various types of management

accounting techniques are to be used such as cost volume- profit analysis, marginal costing and

absorption accounting that helps in to evaluating the company financial condition. Nisa

accounting managers identifies and managing the accounting records for day to day activity

transactions. Management accounting officer are also responsible for preparing the budget and

controlling the expenses in order to manage high profitability of an organization. The main

objective of this report is to analyze existing cost accounting system and to develop product

costing on the basis of ABC.

TASK 1

P1 Explaining the management accounting along with the different kinds of management

accounting systems

Managerial accounting is the process of identifying, analyzing, recording and presenting

financial information that is used as internal information by management for planning, decision

making and controlling of business financial operations (Vitez, 2017). It is mainly concerned

with the providing helpful information and report to internal users such as managers and

entrepreneurs. Management accounting tools are may be different for different organization, it

basically depends on the size and policy of an organization. It increases the efficiency of an

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organization in financial term like financial position and company profitability through the

analyzing of inefficiency of accounting information. Management accounting provides fact and

information along with its interpretation that helps in to take decision by senior management

team, management accounting is a guide not a decision maker. Management accounting forecast

the relevant information of effective decision making through the analyzing of financial

statements, ratio analysis and fund flow analysis it provides approximate information towards

the forecasting of financial budget (Weygandt, Kimmel, and Kieso, 2015). Management

accounting helps management to record, planning and controlling the activities to decision

making processes. Accounting information are to be used within an organization and it focuses

on future accountability. Managerial accounting is not used for specific department of an

organization, it used for entire organization after the effective coordination of all departments. It

is a fundamental tool for making strategic planning. If an organization wants to develop new

product line and acquiring another business or expanding the existing business in to other

countries so that they uses number of tools for assisting decision making.

Functions of management accounting are:

Margin analysis- It determines the amount of profit that is generated from the specific

product, product line, customer, store etc. Cash flow statement also describes the amount of cash

at the beginning of a period and the amount of cash at the end of that period its difference shows

the profit and loss of the company. Profit is earned when the closing balance is higher than

opening balance.

Break even analysis- It is the position of no profit no loss of company. It determines the

price points for product and services (Fayol, 2016).

Constraint analysis- In constraint analysis element, factors or subsystem that work as a

bottleneck, It restricts an entity, project or system (such as manufacturing or decision making

process) from achieving its potential (higher level of output) with reference to its goal.

Target costing- It helps in assisting in the design of new product by accumulating the cost

of new designs, comparing them to target cost levels, and reporting this information to

management.

4

analyzing of inefficiency of accounting information. Management accounting provides fact and

information along with its interpretation that helps in to take decision by senior management

team, management accounting is a guide not a decision maker. Management accounting forecast

the relevant information of effective decision making through the analyzing of financial

statements, ratio analysis and fund flow analysis it provides approximate information towards

the forecasting of financial budget (Weygandt, Kimmel, and Kieso, 2015). Management

accounting helps management to record, planning and controlling the activities to decision

making processes. Accounting information are to be used within an organization and it focuses

on future accountability. Managerial accounting is not used for specific department of an

organization, it used for entire organization after the effective coordination of all departments. It

is a fundamental tool for making strategic planning. If an organization wants to develop new

product line and acquiring another business or expanding the existing business in to other

countries so that they uses number of tools for assisting decision making.

Functions of management accounting are:

Margin analysis- It determines the amount of profit that is generated from the specific

product, product line, customer, store etc. Cash flow statement also describes the amount of cash

at the beginning of a period and the amount of cash at the end of that period its difference shows

the profit and loss of the company. Profit is earned when the closing balance is higher than

opening balance.

Break even analysis- It is the position of no profit no loss of company. It determines the

price points for product and services (Fayol, 2016).

Constraint analysis- In constraint analysis element, factors or subsystem that work as a

bottleneck, It restricts an entity, project or system (such as manufacturing or decision making

process) from achieving its potential (higher level of output) with reference to its goal.

Target costing- It helps in assisting in the design of new product by accumulating the cost

of new designs, comparing them to target cost levels, and reporting this information to

management.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting system tracks the cost of production of goods and services in a

company. A few of the most common accounting systems includes traditional cost accounting,

lean accounting, throughput accounting and transfer pricing methods are to be used.

Traditional accounting- It includes the job offer and process costing methods. Each of

these methods determines the allocation of funds to direct material, direct cost and

manufacturing overhead. Job order costing method are used for a large size project where all the

costs are easily traceable, Process costing method allocates the costs to number to processes that

is used to produce homogeneous product.

Lean accounting- It is most economical used method where cost reducing technique are

to be used for eliminating the waste. Management accountant gives immediate financial

information for making decisions, assessing value stream and measuring profitability.

Through put accounting- Accountants mainly focuses on identifying the certain

constraints within the company's production system. It includes insufficient levels of materials,

labor, or production capacity so that this accounting method helps in reducing these constraints

in order to allow for more throughput's towards the increment in production volume, thereby

lowering the cost for each individual unit produced.

Transfer accounting- It is another most common method that are flexibly used in most of

the retail companies like Nisa, Company calculates the cost of product or services according to

the number of department through which good are passes during the manufacturing process.

For Nisa it is important to plan the costs and understand the behavior of people and the

cost that is incurred on various activities over the period. The cost that is incurred by Smart

Looks Ltd. for the certain period to make his operations work smoothly are:

Material- Material is important for the company to manufacture the clothes, because if

raw material is not provided to the factory workers how will they be able to produce the product

and start the process of manufacturing the the cost involved in raw material acquisition is very

large because it is the main element of the process of making the clothes.

Factory Rent: Another cost which is related to Smart Looks is the rent of the premises

where manufacturing process will goes on and this costs is a fixed cost for Smart Looks because

whether if operations are held or not rent will be paid to the landlord or factory owner in any of

the case.

5

company. A few of the most common accounting systems includes traditional cost accounting,

lean accounting, throughput accounting and transfer pricing methods are to be used.

Traditional accounting- It includes the job offer and process costing methods. Each of

these methods determines the allocation of funds to direct material, direct cost and

manufacturing overhead. Job order costing method are used for a large size project where all the

costs are easily traceable, Process costing method allocates the costs to number to processes that

is used to produce homogeneous product.

Lean accounting- It is most economical used method where cost reducing technique are

to be used for eliminating the waste. Management accountant gives immediate financial

information for making decisions, assessing value stream and measuring profitability.

Through put accounting- Accountants mainly focuses on identifying the certain

constraints within the company's production system. It includes insufficient levels of materials,

labor, or production capacity so that this accounting method helps in reducing these constraints

in order to allow for more throughput's towards the increment in production volume, thereby

lowering the cost for each individual unit produced.

Transfer accounting- It is another most common method that are flexibly used in most of

the retail companies like Nisa, Company calculates the cost of product or services according to

the number of department through which good are passes during the manufacturing process.

For Nisa it is important to plan the costs and understand the behavior of people and the

cost that is incurred on various activities over the period. The cost that is incurred by Smart

Looks Ltd. for the certain period to make his operations work smoothly are:

Material- Material is important for the company to manufacture the clothes, because if

raw material is not provided to the factory workers how will they be able to produce the product

and start the process of manufacturing the the cost involved in raw material acquisition is very

large because it is the main element of the process of making the clothes.

Factory Rent: Another cost which is related to Smart Looks is the rent of the premises

where manufacturing process will goes on and this costs is a fixed cost for Smart Looks because

whether if operations are held or not rent will be paid to the landlord or factory owner in any of

the case.

5

Sewing Machines in Factory- Well the sewing machines have also an important place in

garment industry. It is one of the main assets of the clothing industry. As the power of sewing

machines are based on the unit of electricity it is variable cost.

Factory Supervisors Wages- It is Semi-variable cost for the company because a fixed

amount and also a performance based bonus is a variable aspect of the cost so, it is a semi

variable cost. Supervisors are also an important element in the industry and needs to be attended

very well.

P2 Uses of different accounting methods in management accounting system reporting

Several methods are to be used in management accounting system, these are stated that in

a manner below:

Financial planning- The main objective of any business organization is profit

maximization. It can be achieved by making proper or sound financial planning. It is the most

appropriate tool for achieving the business objective.

Financial statement analysis- It includes profit and loss account, balance sheet and

financial statements. From these analysis management are effectively know about the growth

rate of business concern. It can be done through comparative financial statements, common size

statements and ratio analysis (McKinney, 2015).

Cost accounting- It represents the cost according to product, process, department and

branch wise. These cost are basically compared with predetermined one.

Fund flow analysis- It find outs the movement of fund from one period to another. This

analysis helps to know about the allocated fund is properly used or not in a year compare to

previous one.

Cash flow analysis- It describes the movement of cash from one period to another.

Behind this cash balance and changes between two periods are also find out. It also describes the

cash from operations and the movement in a particular period.

Standard costing- It is a predetermined cost. It provides bench mark for measuring the

actual performance. It can be used for finding out the deviation between the actual and standard

performance.

Marginal costing- This technique is used to fix selling price of goods, optimum

utilization of raw materials and resources, it helps in to take make or buy decision. Acceptance

6

garment industry. It is one of the main assets of the clothing industry. As the power of sewing

machines are based on the unit of electricity it is variable cost.

Factory Supervisors Wages- It is Semi-variable cost for the company because a fixed

amount and also a performance based bonus is a variable aspect of the cost so, it is a semi

variable cost. Supervisors are also an important element in the industry and needs to be attended

very well.

P2 Uses of different accounting methods in management accounting system reporting

Several methods are to be used in management accounting system, these are stated that in

a manner below:

Financial planning- The main objective of any business organization is profit

maximization. It can be achieved by making proper or sound financial planning. It is the most

appropriate tool for achieving the business objective.

Financial statement analysis- It includes profit and loss account, balance sheet and

financial statements. From these analysis management are effectively know about the growth

rate of business concern. It can be done through comparative financial statements, common size

statements and ratio analysis (McKinney, 2015).

Cost accounting- It represents the cost according to product, process, department and

branch wise. These cost are basically compared with predetermined one.

Fund flow analysis- It find outs the movement of fund from one period to another. This

analysis helps to know about the allocated fund is properly used or not in a year compare to

previous one.

Cash flow analysis- It describes the movement of cash from one period to another.

Behind this cash balance and changes between two periods are also find out. It also describes the

cash from operations and the movement in a particular period.

Standard costing- It is a predetermined cost. It provides bench mark for measuring the

actual performance. It can be used for finding out the deviation between the actual and standard

performance.

Marginal costing- This technique is used to fix selling price of goods, optimum

utilization of raw materials and resources, it helps in to take make or buy decision. Acceptance

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and rejection of bulk or foreign order and other profit oriented things are taken in to

consideration under this technique.

Budgetary control- It is used for the estimation of future financial needs according to

order. It is used to control the financial performance of a business concern. It directed the

business operation in a desired direction.

M1 Benefits and uses of management accounting system

The benefits associated with management accounting systems are enumerated in the

manner below:

Management accounting system has several advantages. These advantages are usually

coincide with the company ability towards the improvement in company operations and

profitability. It helps in to achieve competitive advantage by developing cost allocation process

in its management accounting functions (Golini, Kalchschmidt, and Landoni, 2015).

Reduces expenses- Management accounting helps in to reduce operational expenses. It

helps in to review the cost of economic resources and other operation costs. It also provides the

information about the amount of cost are incurred in smooth running of business operations. In

helps in to analyze the quality of economic resources used to produce goods and services.

Improvement in cash flow- Budget are the major tool in the management accounting.

Budget are the financial road map for future business expenditure. Larger business organization

creates a master budget for entire organization. But organizations uses uses several smaller

budgets for division or departments. The main objective of budget is to save money through

careful analysis of necessary and unnecessary cash expenditures.

Business decisions- Management accounting improves the decision making ability of

business owners. Management accounting information are taking as decision making tool. it

usually provides a quantitative analysis of various decision making opportunities.

Increment in financial returns- Business owners uses management accounting in order to

increase company financial return. Management accountants forecasting the financial budget

relating to consumer demand, potential sales or the effects of changes in consumer prices in

economic marketplace. Management accounting information gives ensurity about the production

of goods and services in order to effective meet of consumer demand at current prices.

7

consideration under this technique.

Budgetary control- It is used for the estimation of future financial needs according to

order. It is used to control the financial performance of a business concern. It directed the

business operation in a desired direction.

M1 Benefits and uses of management accounting system

The benefits associated with management accounting systems are enumerated in the

manner below:

Management accounting system has several advantages. These advantages are usually

coincide with the company ability towards the improvement in company operations and

profitability. It helps in to achieve competitive advantage by developing cost allocation process

in its management accounting functions (Golini, Kalchschmidt, and Landoni, 2015).

Reduces expenses- Management accounting helps in to reduce operational expenses. It

helps in to review the cost of economic resources and other operation costs. It also provides the

information about the amount of cost are incurred in smooth running of business operations. In

helps in to analyze the quality of economic resources used to produce goods and services.

Improvement in cash flow- Budget are the major tool in the management accounting.

Budget are the financial road map for future business expenditure. Larger business organization

creates a master budget for entire organization. But organizations uses uses several smaller

budgets for division or departments. The main objective of budget is to save money through

careful analysis of necessary and unnecessary cash expenditures.

Business decisions- Management accounting improves the decision making ability of

business owners. Management accounting information are taking as decision making tool. it

usually provides a quantitative analysis of various decision making opportunities.

Increment in financial returns- Business owners uses management accounting in order to

increase company financial return. Management accountants forecasting the financial budget

relating to consumer demand, potential sales or the effects of changes in consumer prices in

economic marketplace. Management accounting information gives ensurity about the production

of goods and services in order to effective meet of consumer demand at current prices.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Uses of management accounting is record keeping, planning and control or decision

making etc.

TASK 2

P3 Calculation of cost using marginal and absorption costing

Cost determination is the one of the important element of the management accounting

techniques, because inaccurate cost identification makes adverse impact on the Nisa pricing

decisions or vice versa. Accurate cost are identify by following techniques that helps to generate

higher profitability with minimization of wastage. There are following cost determination

techniques are to used such as marginal costing, absorption costing etc.

Marginal/ variable costing- It is ascertainment by differentiation of fixed costs and

variable cost. It is dependent on the volume of activity which are separated from the fixed cost.

Marginal cost are variable cost consisting labor and material cost plus an estimation portion of

fixed cost (Klychova, Fakhretdinova, Klychova, and Antonova, 2015). That kind of cost are

unchanged with a change in the volume of activity. Marginal costing helps in cost ascertainment,

cost control and decision for a particular time period. In addition to this it helps in profit

planning, pricing of production, make or buy decisions and product mix etc. It is used to know

about the impact of variable cost on the volume of production or output.

Advantages of marginal costing:

It is easy to operate and simple to understand.

It is useful in profit planning through break even and profit graph, it helps in to determine

profitability at different level of production and sale.

8

making etc.

TASK 2

P3 Calculation of cost using marginal and absorption costing

Cost determination is the one of the important element of the management accounting

techniques, because inaccurate cost identification makes adverse impact on the Nisa pricing

decisions or vice versa. Accurate cost are identify by following techniques that helps to generate

higher profitability with minimization of wastage. There are following cost determination

techniques are to used such as marginal costing, absorption costing etc.

Marginal/ variable costing- It is ascertainment by differentiation of fixed costs and

variable cost. It is dependent on the volume of activity which are separated from the fixed cost.

Marginal cost are variable cost consisting labor and material cost plus an estimation portion of

fixed cost (Klychova, Fakhretdinova, Klychova, and Antonova, 2015). That kind of cost are

unchanged with a change in the volume of activity. Marginal costing helps in cost ascertainment,

cost control and decision for a particular time period. In addition to this it helps in profit

planning, pricing of production, make or buy decisions and product mix etc. It is used to know

about the impact of variable cost on the volume of production or output.

Advantages of marginal costing:

It is easy to operate and simple to understand.

It is useful in profit planning through break even and profit graph, it helps in to determine

profitability at different level of production and sale.

8

It helps in to take decision of make or buy.

A clear cut division of costs in to fixed and variable cost that makes the budgetary control

flexible.

Evaluation of different department cost are easy through the use of this technique.

Under this technique fixed overhead recovery rate is easy.

Disadvantages of marginal costing:

Segregation of all costs in to fixed and variable is very difficult.

In marginal costing method greater importance are gives to sales function rather than to

production function (Busco, and Quattrone, 2015).

Elimination of fixed cost from the inventory valuation is illogical because costs are also

incurred at the time of manufacturing the goods.

The application of this technique is limited in case of industries because most of costs are

incurred during the manufacturing process.

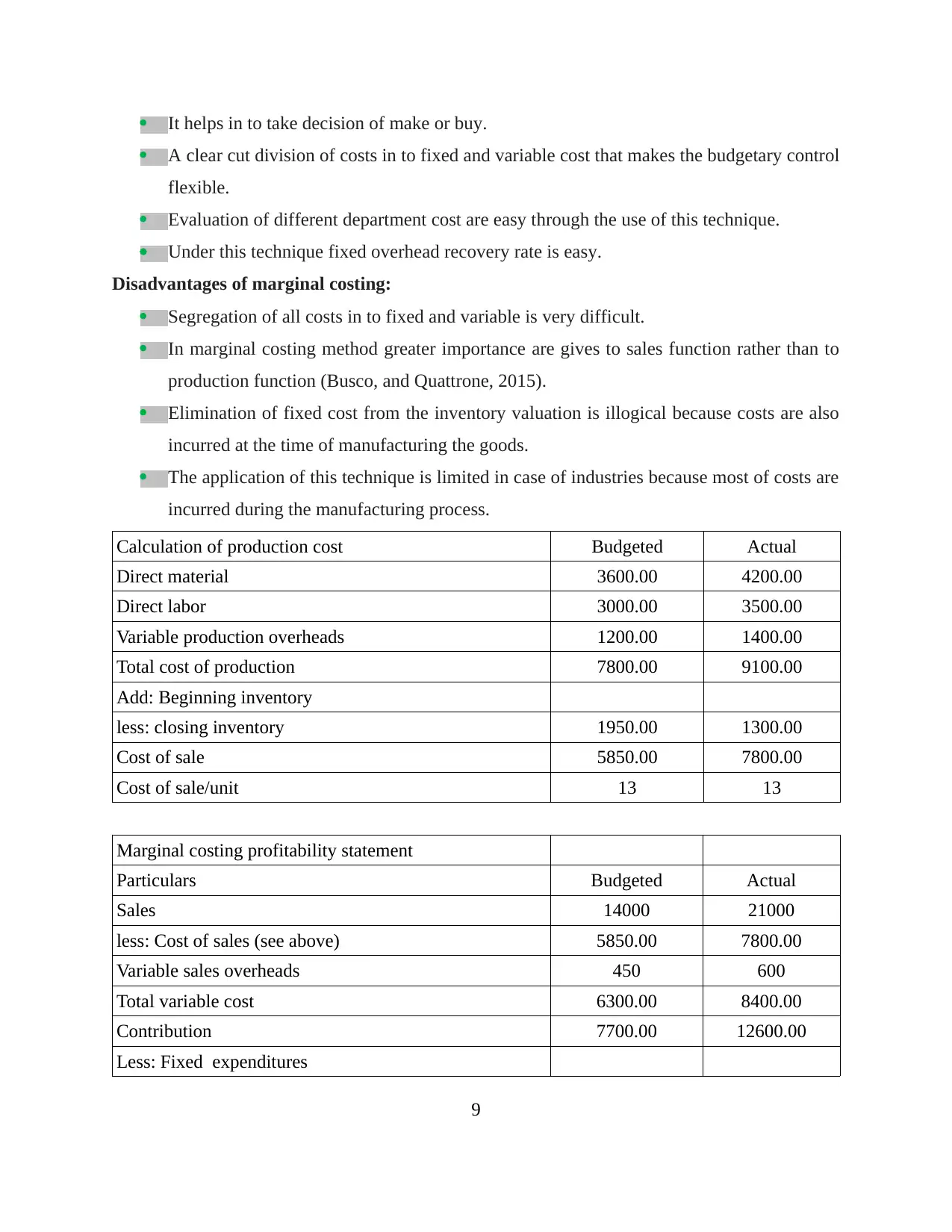

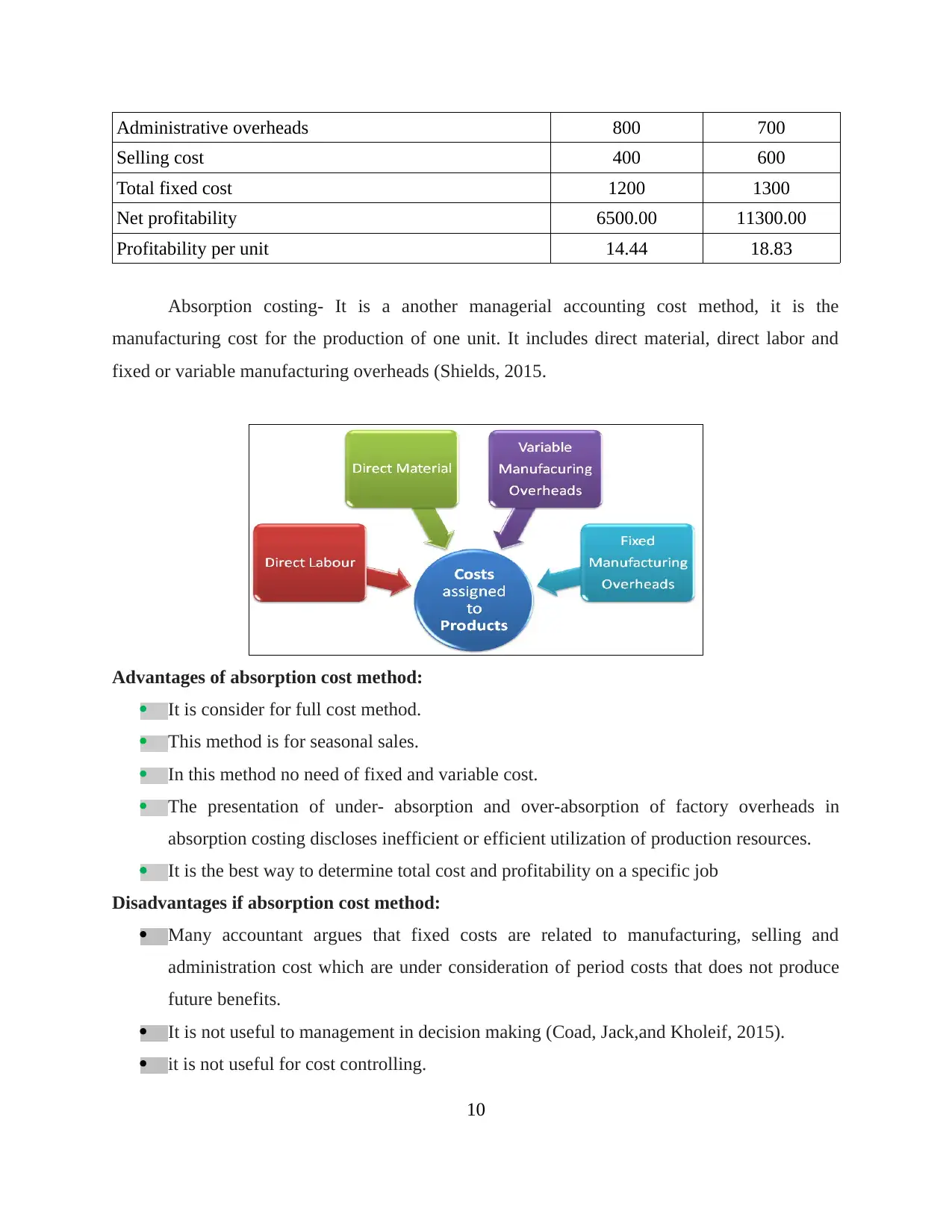

Calculation of production cost Budgeted Actual

Direct material 3600.00 4200.00

Direct labor 3000.00 3500.00

Variable production overheads 1200.00 1400.00

Total cost of production 7800.00 9100.00

Add: Beginning inventory

less: closing inventory 1950.00 1300.00

Cost of sale 5850.00 7800.00

Cost of sale/unit 13 13

Marginal costing profitability statement

Particulars Budgeted Actual

Sales 14000 21000

less: Cost of sales (see above) 5850.00 7800.00

Variable sales overheads 450 600

Total variable cost 6300.00 8400.00

Contribution 7700.00 12600.00

Less: Fixed expenditures

9

A clear cut division of costs in to fixed and variable cost that makes the budgetary control

flexible.

Evaluation of different department cost are easy through the use of this technique.

Under this technique fixed overhead recovery rate is easy.

Disadvantages of marginal costing:

Segregation of all costs in to fixed and variable is very difficult.

In marginal costing method greater importance are gives to sales function rather than to

production function (Busco, and Quattrone, 2015).

Elimination of fixed cost from the inventory valuation is illogical because costs are also

incurred at the time of manufacturing the goods.

The application of this technique is limited in case of industries because most of costs are

incurred during the manufacturing process.

Calculation of production cost Budgeted Actual

Direct material 3600.00 4200.00

Direct labor 3000.00 3500.00

Variable production overheads 1200.00 1400.00

Total cost of production 7800.00 9100.00

Add: Beginning inventory

less: closing inventory 1950.00 1300.00

Cost of sale 5850.00 7800.00

Cost of sale/unit 13 13

Marginal costing profitability statement

Particulars Budgeted Actual

Sales 14000 21000

less: Cost of sales (see above) 5850.00 7800.00

Variable sales overheads 450 600

Total variable cost 6300.00 8400.00

Contribution 7700.00 12600.00

Less: Fixed expenditures

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Administrative overheads 800 700

Selling cost 400 600

Total fixed cost 1200 1300

Net profitability 6500.00 11300.00

Profitability per unit 14.44 18.83

Absorption costing- It is a another managerial accounting cost method, it is the

manufacturing cost for the production of one unit. It includes direct material, direct labor and

fixed or variable manufacturing overheads (Shields, 2015.

Advantages of absorption cost method:

It is consider for full cost method.

This method is for seasonal sales.

In this method no need of fixed and variable cost.

The presentation of under- absorption and over-absorption of factory overheads in

absorption costing discloses inefficient or efficient utilization of production resources.

It is the best way to determine total cost and profitability on a specific job

Disadvantages if absorption cost method:

Many accountant argues that fixed costs are related to manufacturing, selling and

administration cost which are under consideration of period costs that does not produce

future benefits.

It is not useful to management in decision making (Coad, Jack,and Kholeif, 2015).

it is not useful for cost controlling.

10

Selling cost 400 600

Total fixed cost 1200 1300

Net profitability 6500.00 11300.00

Profitability per unit 14.44 18.83

Absorption costing- It is a another managerial accounting cost method, it is the

manufacturing cost for the production of one unit. It includes direct material, direct labor and

fixed or variable manufacturing overheads (Shields, 2015.

Advantages of absorption cost method:

It is consider for full cost method.

This method is for seasonal sales.

In this method no need of fixed and variable cost.

The presentation of under- absorption and over-absorption of factory overheads in

absorption costing discloses inefficient or efficient utilization of production resources.

It is the best way to determine total cost and profitability on a specific job

Disadvantages if absorption cost method:

Many accountant argues that fixed costs are related to manufacturing, selling and

administration cost which are under consideration of period costs that does not produce

future benefits.

It is not useful to management in decision making (Coad, Jack,and Kholeif, 2015).

it is not useful for cost controlling.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

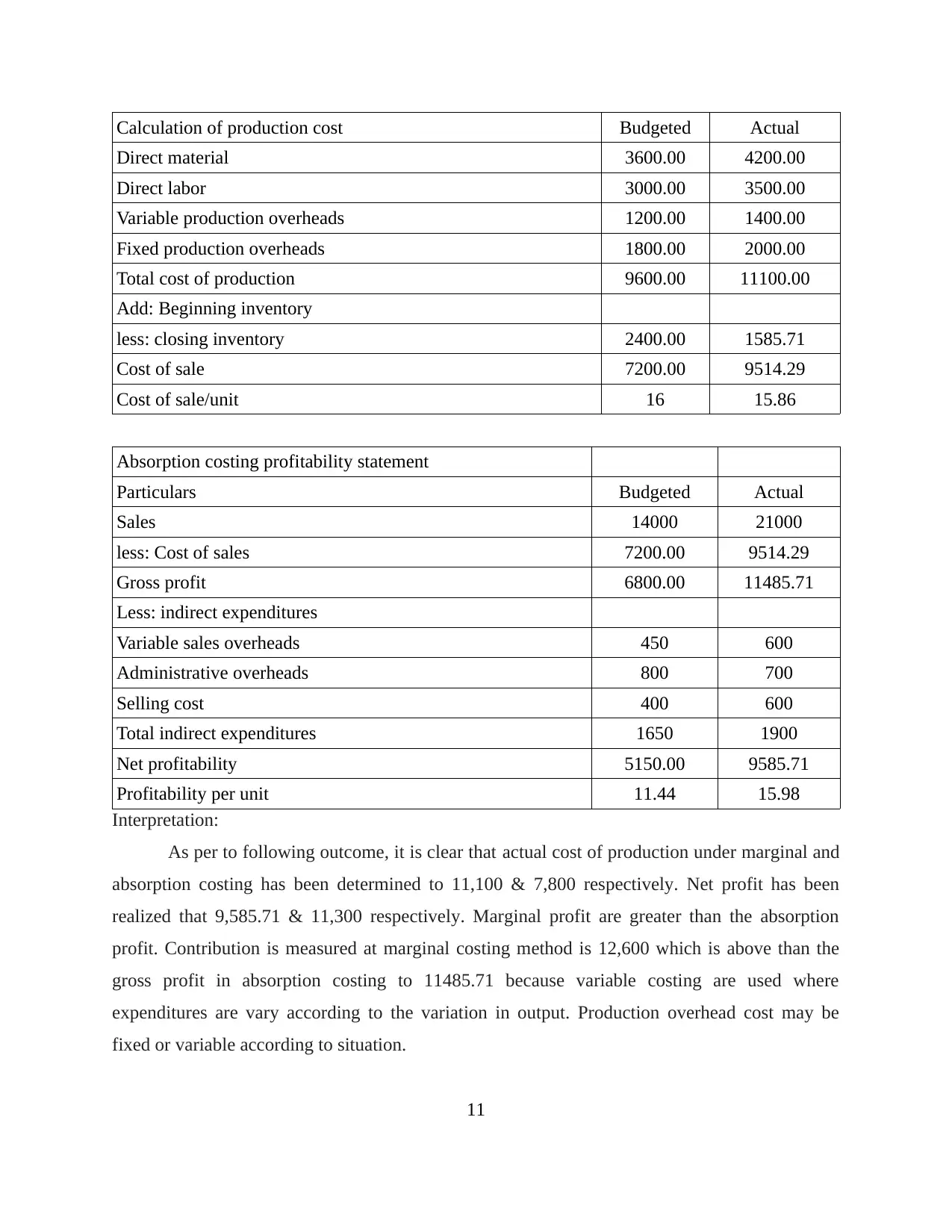

Calculation of production cost Budgeted Actual

Direct material 3600.00 4200.00

Direct labor 3000.00 3500.00

Variable production overheads 1200.00 1400.00

Fixed production overheads 1800.00 2000.00

Total cost of production 9600.00 11100.00

Add: Beginning inventory

less: closing inventory 2400.00 1585.71

Cost of sale 7200.00 9514.29

Cost of sale/unit 16 15.86

Absorption costing profitability statement

Particulars Budgeted Actual

Sales 14000 21000

less: Cost of sales 7200.00 9514.29

Gross profit 6800.00 11485.71

Less: indirect expenditures

Variable sales overheads 450 600

Administrative overheads 800 700

Selling cost 400 600

Total indirect expenditures 1650 1900

Net profitability 5150.00 9585.71

Profitability per unit 11.44 15.98

Interpretation:

As per to following outcome, it is clear that actual cost of production under marginal and

absorption costing has been determined to 11,100 & 7,800 respectively. Net profit has been

realized that 9,585.71 & 11,300 respectively. Marginal profit are greater than the absorption

profit. Contribution is measured at marginal costing method is 12,600 which is above than the

gross profit in absorption costing to 11485.71 because variable costing are used where

expenditures are vary according to the variation in output. Production overhead cost may be

fixed or variable according to situation.

11

Direct material 3600.00 4200.00

Direct labor 3000.00 3500.00

Variable production overheads 1200.00 1400.00

Fixed production overheads 1800.00 2000.00

Total cost of production 9600.00 11100.00

Add: Beginning inventory

less: closing inventory 2400.00 1585.71

Cost of sale 7200.00 9514.29

Cost of sale/unit 16 15.86

Absorption costing profitability statement

Particulars Budgeted Actual

Sales 14000 21000

less: Cost of sales 7200.00 9514.29

Gross profit 6800.00 11485.71

Less: indirect expenditures

Variable sales overheads 450 600

Administrative overheads 800 700

Selling cost 400 600

Total indirect expenditures 1650 1900

Net profitability 5150.00 9585.71

Profitability per unit 11.44 15.98

Interpretation:

As per to following outcome, it is clear that actual cost of production under marginal and

absorption costing has been determined to 11,100 & 7,800 respectively. Net profit has been

realized that 9,585.71 & 11,300 respectively. Marginal profit are greater than the absorption

profit. Contribution is measured at marginal costing method is 12,600 which is above than the

gross profit in absorption costing to 11485.71 because variable costing are used where

expenditures are vary according to the variation in output. Production overhead cost may be

fixed or variable according to situation.

11

Difference between marginal and absorption costing:

Marginal technique are at value inventory where variable production cost are to be used,

In absorption costing inventory are measures at full costing value.

In marginal costing less volume of closing inventory, it gives less return, while in

absorption costing large closing inventory gives larger return.

D1 Critically evaluation of management accounting system

Management accounting system is really helpful for Nisa retailer to integrate and

summarize the result of financial activities in a meaningful manner in order to make effective

decisions for the prospective growth of an organization. Its information helps in to detect the

areas where Nisa mangers must put focus towards the improvement in operational areas, which

in turn, results in declining operational cost at greater return (Christensen, Lee, Walker, and

Zeng, 2015). In contrast, management accounting system reporting such as job report, cost

report, budgeting etc. helps in to analyze the firm performance that helps in to create the best

planning for the betterment. Internal organization report of Nisa presents the result for a

specified time duration. Management accounting system presents the report for more than one

duration at a single time time of point that is useful for trend analysis as well as forecasting of

budget. This system is helpful to work on the lean management principle in order to minimize

wastage of resources and business success.

M2 Range of management accounting techniques

As per the report, Nisa has been used marginal and absorption costing technique.

Marginal costing ascertains the total cost of production as variable cost. In absorption costing

method recognize both the cost fixed and variable cost. Profitability are quantified by the profit

volume ratio it includes total fixed cost that directly affects the net profitability. Marginal costing

measures profit per unit of contribution, It is measures outcomes in terms of net profit per unit.

Out of both the techniques, marginal costing method is more appropriate and used by the most of

organizations because it measures contribution and overall net profit and helpful in short-term

managerial planning (Busco, and Quattrone, 2015). In this, break-even point analysis, cost-

volume-profit analysis and margin of safety that assist the Nisa to make excellent plan for

deriving success.

12

Marginal technique are at value inventory where variable production cost are to be used,

In absorption costing inventory are measures at full costing value.

In marginal costing less volume of closing inventory, it gives less return, while in

absorption costing large closing inventory gives larger return.

D1 Critically evaluation of management accounting system

Management accounting system is really helpful for Nisa retailer to integrate and

summarize the result of financial activities in a meaningful manner in order to make effective

decisions for the prospective growth of an organization. Its information helps in to detect the

areas where Nisa mangers must put focus towards the improvement in operational areas, which

in turn, results in declining operational cost at greater return (Christensen, Lee, Walker, and

Zeng, 2015). In contrast, management accounting system reporting such as job report, cost

report, budgeting etc. helps in to analyze the firm performance that helps in to create the best

planning for the betterment. Internal organization report of Nisa presents the result for a

specified time duration. Management accounting system presents the report for more than one

duration at a single time time of point that is useful for trend analysis as well as forecasting of

budget. This system is helpful to work on the lean management principle in order to minimize

wastage of resources and business success.

M2 Range of management accounting techniques

As per the report, Nisa has been used marginal and absorption costing technique.

Marginal costing ascertains the total cost of production as variable cost. In absorption costing

method recognize both the cost fixed and variable cost. Profitability are quantified by the profit

volume ratio it includes total fixed cost that directly affects the net profitability. Marginal costing

measures profit per unit of contribution, It is measures outcomes in terms of net profit per unit.

Out of both the techniques, marginal costing method is more appropriate and used by the most of

organizations because it measures contribution and overall net profit and helpful in short-term

managerial planning (Busco, and Quattrone, 2015). In this, break-even point analysis, cost-

volume-profit analysis and margin of safety that assist the Nisa to make excellent plan for

deriving success.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.