Noccio Chocolate Company: A Case Study in Production Optimization

VerifiedAdded on 2023/06/11

|19

|2586

|289

Case Study

AI Summary

This case study delves into the production analysis of Noccio Chocolate Company (NCC), founded by Jaan and Ting, focusing on optimizing their chocolate production and blending processes. The analysis covers the determination of total revenue, total costs, and the optimum product mix using linear programming to maximize profit. It addresses key questions posed by Ting, including the number of boxes produced for each product, the cost of wasted cocoa powder, and a comparison between fixed and variable volume agreements. The study also explores the impact of negotiating different pricing models and the potential benefits of acquiring additional Grade A cocoa powder. Sensitivity analysis is conducted to assess the stability of the preferred product mix, culminating in a decision table and recommendations for enhancing NCC's production efficiency and profitability. Desklib provides access to similar case studies and solved assignments for students.

Executive summary

The main founders of Noccio Chocolate Company (NCC) are Jaan and Ting who were former

students of the University of New South Wales (UNSW) student, with the key drive and mission

of blending Chocolate, moreover to mix and fill machine. At the present moment production

analysis done showed that more than 30, 000 kg of the products were produced yearly, the

achievement has resulted from production of quality product at a moderate price.

1

The main founders of Noccio Chocolate Company (NCC) are Jaan and Ting who were former

students of the University of New South Wales (UNSW) student, with the key drive and mission

of blending Chocolate, moreover to mix and fill machine. At the present moment production

analysis done showed that more than 30, 000 kg of the products were produced yearly, the

achievement has resulted from production of quality product at a moderate price.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Executive summary.....................................................................................................................................1

Introduction.................................................................................................................................................3

Determination of total revenue...................................................................................................................4

Determination of total cost.........................................................................................................................5

Optimum product mix.................................................................................................................................6

Determination of net profit based on product mix.....................................................................................7

Determination of the constraints................................................................................................................9

Solution to Ting`s questions......................................................................................................................10

Number of boxes produced for each product.........................................................................................10

Cost of wasted cocoa powder................................................................................................................11

Comparison between the current strategy of a fixed volume agreement and variable volume agreement.

...............................................................................................................................................................12

Decision on negotiating a different pricing model.................................................................................13

Decision on additional 800 kg of Grade A powder with similar cost as the initial................................14

Sensitivity of preferred product mix......................................................................................................15

Results.......................................................................................................................................................16

Decision Table:......................................................................................................................................16

Conclusion.................................................................................................................................................17

Recommendation......................................................................................................................................18

Reference...................................................................................................................................................19

2

Executive summary.....................................................................................................................................1

Introduction.................................................................................................................................................3

Determination of total revenue...................................................................................................................4

Determination of total cost.........................................................................................................................5

Optimum product mix.................................................................................................................................6

Determination of net profit based on product mix.....................................................................................7

Determination of the constraints................................................................................................................9

Solution to Ting`s questions......................................................................................................................10

Number of boxes produced for each product.........................................................................................10

Cost of wasted cocoa powder................................................................................................................11

Comparison between the current strategy of a fixed volume agreement and variable volume agreement.

...............................................................................................................................................................12

Decision on negotiating a different pricing model.................................................................................13

Decision on additional 800 kg of Grade A powder with similar cost as the initial................................14

Sensitivity of preferred product mix......................................................................................................15

Results.......................................................................................................................................................16

Decision Table:......................................................................................................................................16

Conclusion.................................................................................................................................................17

Recommendation......................................................................................................................................18

Reference...................................................................................................................................................19

2

Introduction

The company departments heads carried out analysis on their respective areas in order to come

out with proper and effective results of enhancing production in the company.

Firstly, Jaan a production manager conducted a random sampling as a part of the consignment

whose aims was to determine the quality of beans. The estimation was about 20% of the

consignment which was Grade “A” that is regarded as the best available, what remained was

Grade “B”. The agreed delivered price to the factory is $ 18,000 per tonne of powder. However,

the standard used by Jaan were personal hence it could have never been documented rating

system, moreover, there was on the relationship between Jaan’s rating and the agreed purchase

price per tonne.

Secondly, Ian the sale manager of Noccio determined all the premium bars that Noccio could

have managed to produce. This premium bar was manufactured from the finest powder and

ingredients, essentially, other two products had a limitation on markets..

Finally, Mal finance head prepared a pro-form statement about profit. Where calculation of profit

contribution of each product was done, on its analysis he noted that the chocolate sauce product

hard to make losses that year.

3

The company departments heads carried out analysis on their respective areas in order to come

out with proper and effective results of enhancing production in the company.

Firstly, Jaan a production manager conducted a random sampling as a part of the consignment

whose aims was to determine the quality of beans. The estimation was about 20% of the

consignment which was Grade “A” that is regarded as the best available, what remained was

Grade “B”. The agreed delivered price to the factory is $ 18,000 per tonne of powder. However,

the standard used by Jaan were personal hence it could have never been documented rating

system, moreover, there was on the relationship between Jaan’s rating and the agreed purchase

price per tonne.

Secondly, Ian the sale manager of Noccio determined all the premium bars that Noccio could

have managed to produce. This premium bar was manufactured from the finest powder and

ingredients, essentially, other two products had a limitation on markets..

Finally, Mal finance head prepared a pro-form statement about profit. Where calculation of profit

contribution of each product was done, on its analysis he noted that the chocolate sauce product

hard to make losses that year.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

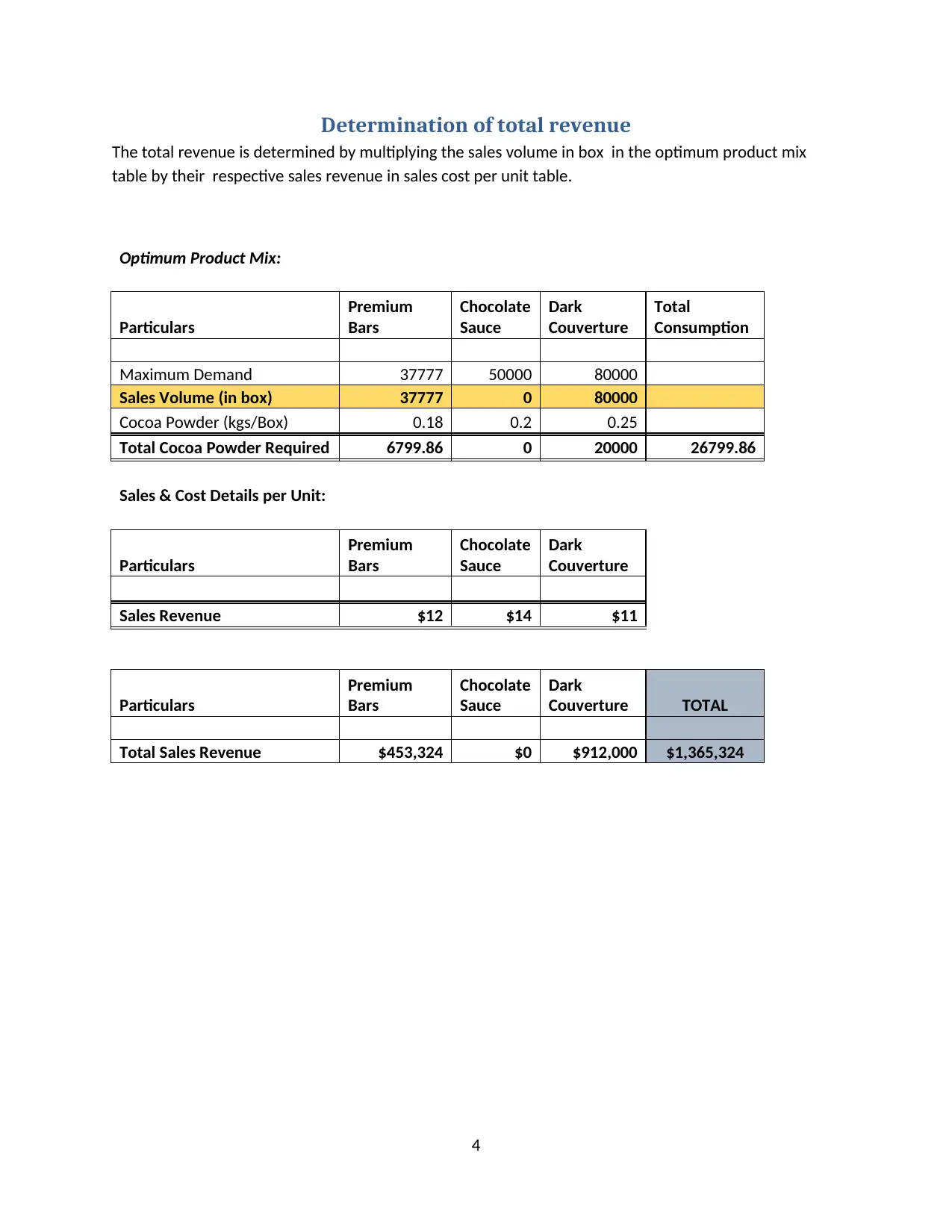

Determination of total revenue

The total revenue is determined by multiplying the sales volume in box in the optimum product mix

table by their respective sales revenue in sales cost per unit table.

Optimum Product Mix:

Particulars

Premium

Bars

Chocolate

Sauce

Dark

Couverture

Total

Consumption

Maximum Demand 37777 50000 80000

Sales Volume (in box) 37777 0 80000

Cocoa Powder (kgs/Box) 0.18 0.2 0.25

Total Cocoa Powder Required 6799.86 0 20000 26799.86

Sales & Cost Details per Unit:

Particulars

Premium

Bars

Chocolate

Sauce

Dark

Couverture

Sales Revenue $12 $14 $11

Particulars

Premium

Bars

Chocolate

Sauce

Dark

Couverture TOTAL

Total Sales Revenue $453,324 $0 $912,000 $1,365,324

4

The total revenue is determined by multiplying the sales volume in box in the optimum product mix

table by their respective sales revenue in sales cost per unit table.

Optimum Product Mix:

Particulars

Premium

Bars

Chocolate

Sauce

Dark

Couverture

Total

Consumption

Maximum Demand 37777 50000 80000

Sales Volume (in box) 37777 0 80000

Cocoa Powder (kgs/Box) 0.18 0.2 0.25

Total Cocoa Powder Required 6799.86 0 20000 26799.86

Sales & Cost Details per Unit:

Particulars

Premium

Bars

Chocolate

Sauce

Dark

Couverture

Sales Revenue $12 $14 $11

Particulars

Premium

Bars

Chocolate

Sauce

Dark

Couverture TOTAL

Total Sales Revenue $453,324 $0 $912,000 $1,365,324

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

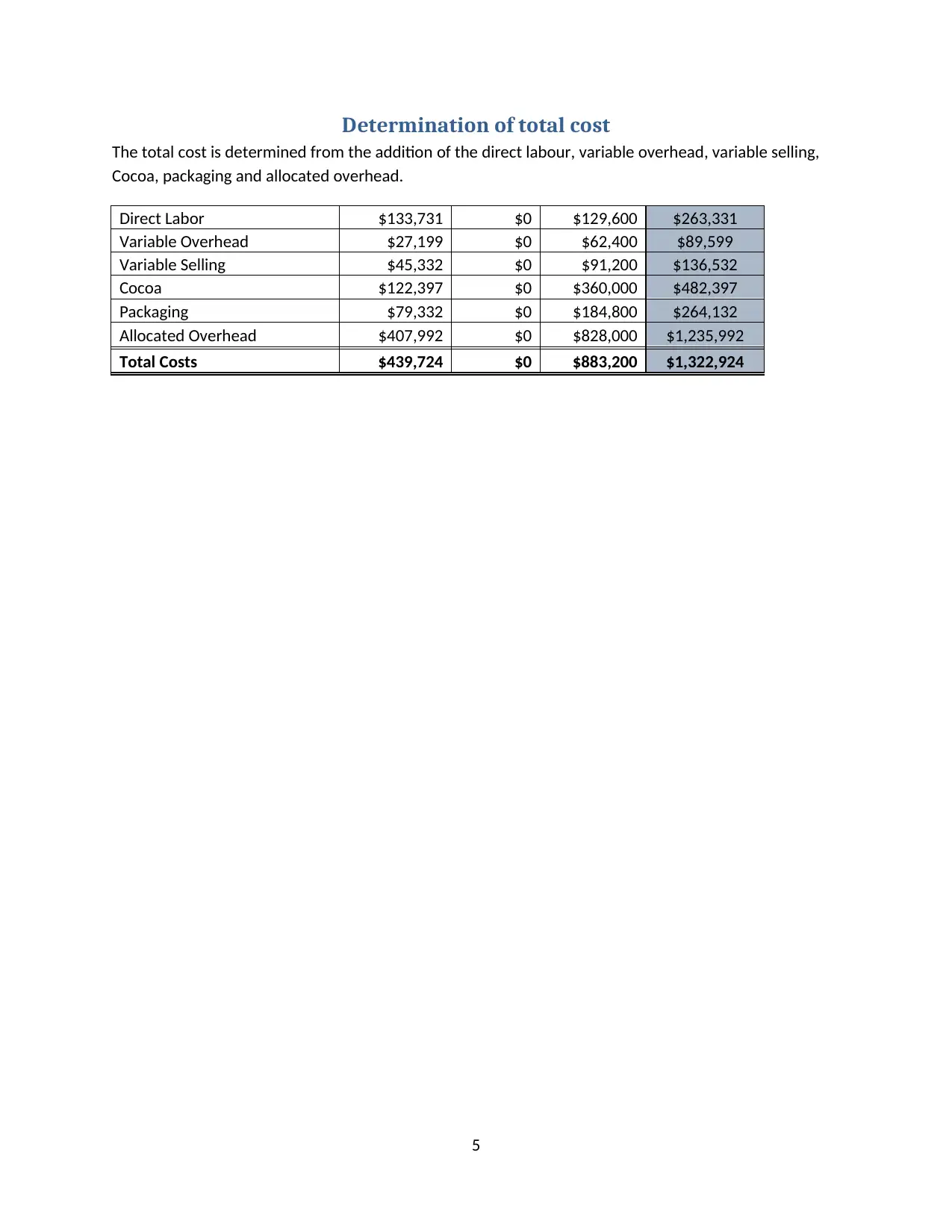

Determination of total cost

The total cost is determined from the addition of the direct labour, variable overhead, variable selling,

Cocoa, packaging and allocated overhead.

Direct Labor $133,731 $0 $129,600 $263,331

Variable Overhead $27,199 $0 $62,400 $89,599

Variable Selling $45,332 $0 $91,200 $136,532

Cocoa $122,397 $0 $360,000 $482,397

Packaging $79,332 $0 $184,800 $264,132

Allocated Overhead $407,992 $0 $828,000 $1,235,992

Total Costs $439,724 $0 $883,200 $1,322,924

5

The total cost is determined from the addition of the direct labour, variable overhead, variable selling,

Cocoa, packaging and allocated overhead.

Direct Labor $133,731 $0 $129,600 $263,331

Variable Overhead $27,199 $0 $62,400 $89,599

Variable Selling $45,332 $0 $91,200 $136,532

Cocoa $122,397 $0 $360,000 $482,397

Packaging $79,332 $0 $184,800 $264,132

Allocated Overhead $407,992 $0 $828,000 $1,235,992

Total Costs $439,724 $0 $883,200 $1,322,924

5

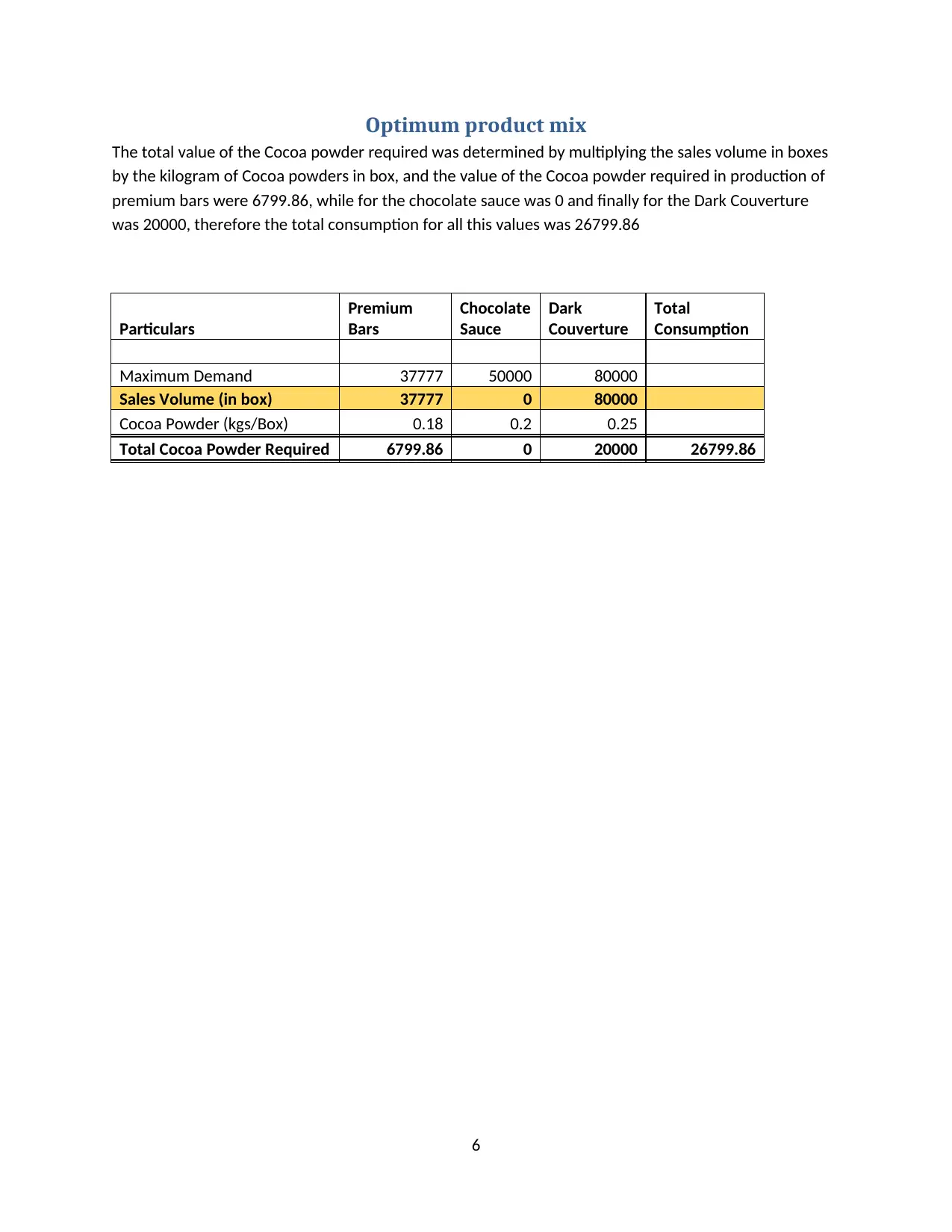

Optimum product mix

The total value of the Cocoa powder required was determined by multiplying the sales volume in boxes

by the kilogram of Cocoa powders in box, and the value of the Cocoa powder required in production of

premium bars were 6799.86, while for the chocolate sauce was 0 and finally for the Dark Couverture

was 20000, therefore the total consumption for all this values was 26799.86

Particulars

Premium

Bars

Chocolate

Sauce

Dark

Couverture

Total

Consumption

Maximum Demand 37777 50000 80000

Sales Volume (in box) 37777 0 80000

Cocoa Powder (kgs/Box) 0.18 0.2 0.25

Total Cocoa Powder Required 6799.86 0 20000 26799.86

6

The total value of the Cocoa powder required was determined by multiplying the sales volume in boxes

by the kilogram of Cocoa powders in box, and the value of the Cocoa powder required in production of

premium bars were 6799.86, while for the chocolate sauce was 0 and finally for the Dark Couverture

was 20000, therefore the total consumption for all this values was 26799.86

Particulars

Premium

Bars

Chocolate

Sauce

Dark

Couverture

Total

Consumption

Maximum Demand 37777 50000 80000

Sales Volume (in box) 37777 0 80000

Cocoa Powder (kgs/Box) 0.18 0.2 0.25

Total Cocoa Powder Required 6799.86 0 20000 26799.86

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

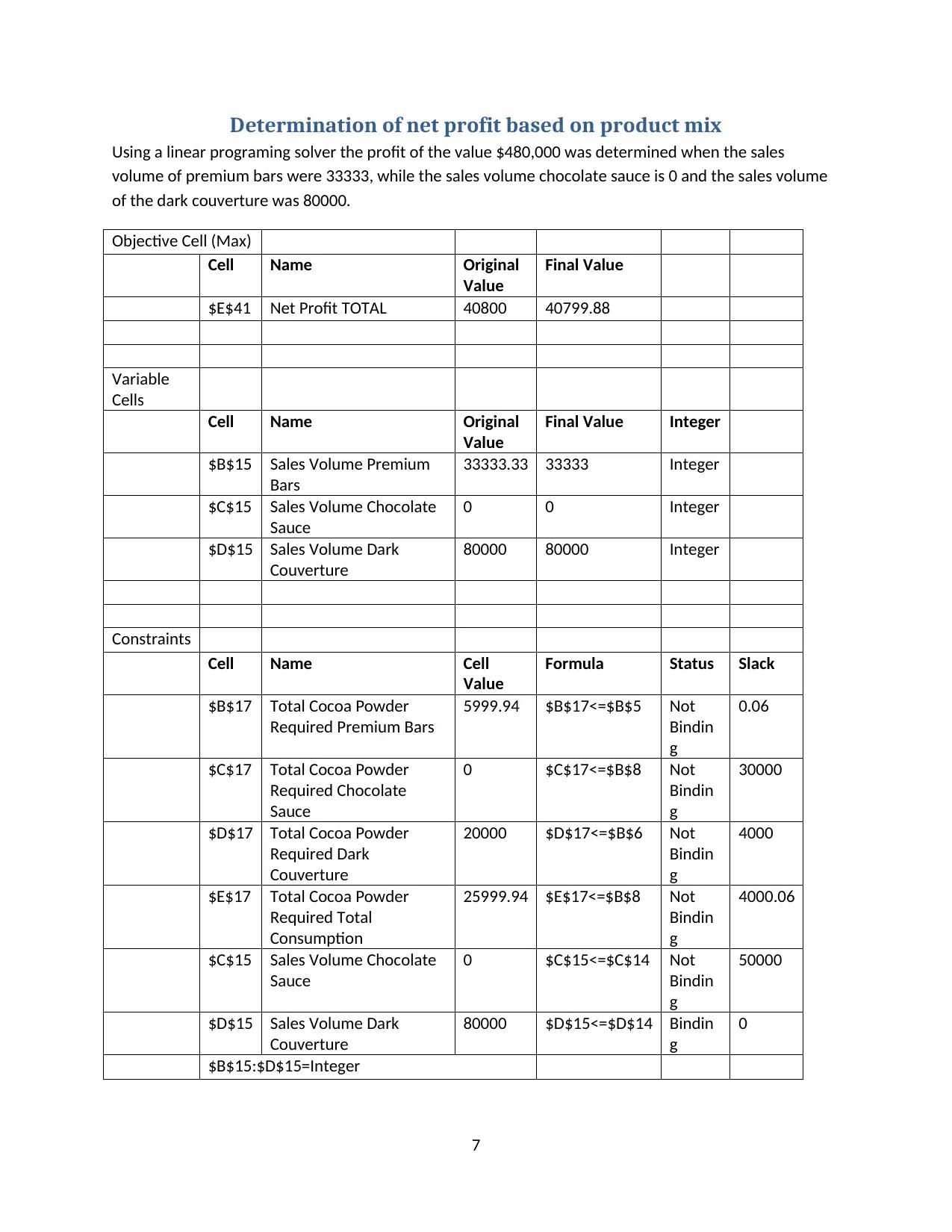

Determination of net profit based on product mix

Using a linear programing solver the profit of the value $480,000 was determined when the sales

volume of premium bars were 33333, while the sales volume chocolate sauce is 0 and the sales volume

of the dark couverture was 80000.

Objective Cell (Max)

Cell Name Original

Value

Final Value

$E$41 Net Profit TOTAL 40800 40799.88

Variable

Cells

Cell Name Original

Value

Final Value Integer

$B$15 Sales Volume Premium

Bars

33333.33 33333 Integer

$C$15 Sales Volume Chocolate

Sauce

0 0 Integer

$D$15 Sales Volume Dark

Couverture

80000 80000 Integer

Constraints

Cell Name Cell

Value

Formula Status Slack

$B$17 Total Cocoa Powder

Required Premium Bars

5999.94 $B$17<=$B$5 Not

Bindin

g

0.06

$C$17 Total Cocoa Powder

Required Chocolate

Sauce

0 $C$17<=$B$8 Not

Bindin

g

30000

$D$17 Total Cocoa Powder

Required Dark

Couverture

20000 $D$17<=$B$6 Not

Bindin

g

4000

$E$17 Total Cocoa Powder

Required Total

Consumption

25999.94 $E$17<=$B$8 Not

Bindin

g

4000.06

$C$15 Sales Volume Chocolate

Sauce

0 $C$15<=$C$14 Not

Bindin

g

50000

$D$15 Sales Volume Dark

Couverture

80000 $D$15<=$D$14 Bindin

g

0

$B$15:$D$15=Integer

7

Using a linear programing solver the profit of the value $480,000 was determined when the sales

volume of premium bars were 33333, while the sales volume chocolate sauce is 0 and the sales volume

of the dark couverture was 80000.

Objective Cell (Max)

Cell Name Original

Value

Final Value

$E$41 Net Profit TOTAL 40800 40799.88

Variable

Cells

Cell Name Original

Value

Final Value Integer

$B$15 Sales Volume Premium

Bars

33333.33 33333 Integer

$C$15 Sales Volume Chocolate

Sauce

0 0 Integer

$D$15 Sales Volume Dark

Couverture

80000 80000 Integer

Constraints

Cell Name Cell

Value

Formula Status Slack

$B$17 Total Cocoa Powder

Required Premium Bars

5999.94 $B$17<=$B$5 Not

Bindin

g

0.06

$C$17 Total Cocoa Powder

Required Chocolate

Sauce

0 $C$17<=$B$8 Not

Bindin

g

30000

$D$17 Total Cocoa Powder

Required Dark

Couverture

20000 $D$17<=$B$6 Not

Bindin

g

4000

$E$17 Total Cocoa Powder

Required Total

Consumption

25999.94 $E$17<=$B$8 Not

Bindin

g

4000.06

$C$15 Sales Volume Chocolate

Sauce

0 $C$15<=$C$14 Not

Bindin

g

50000

$D$15 Sales Volume Dark

Couverture

80000 $D$15<=$D$14 Bindin

g

0

$B$15:$D$15=Integer

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The net profit determined must be too be equivalent to getting the difference between the total

revenue and the total cost

Net profit = $1,311,996 - $1,271,196 = $40,800

8

revenue and the total cost

Net profit = $1,311,996 - $1,271,196 = $40,800

8

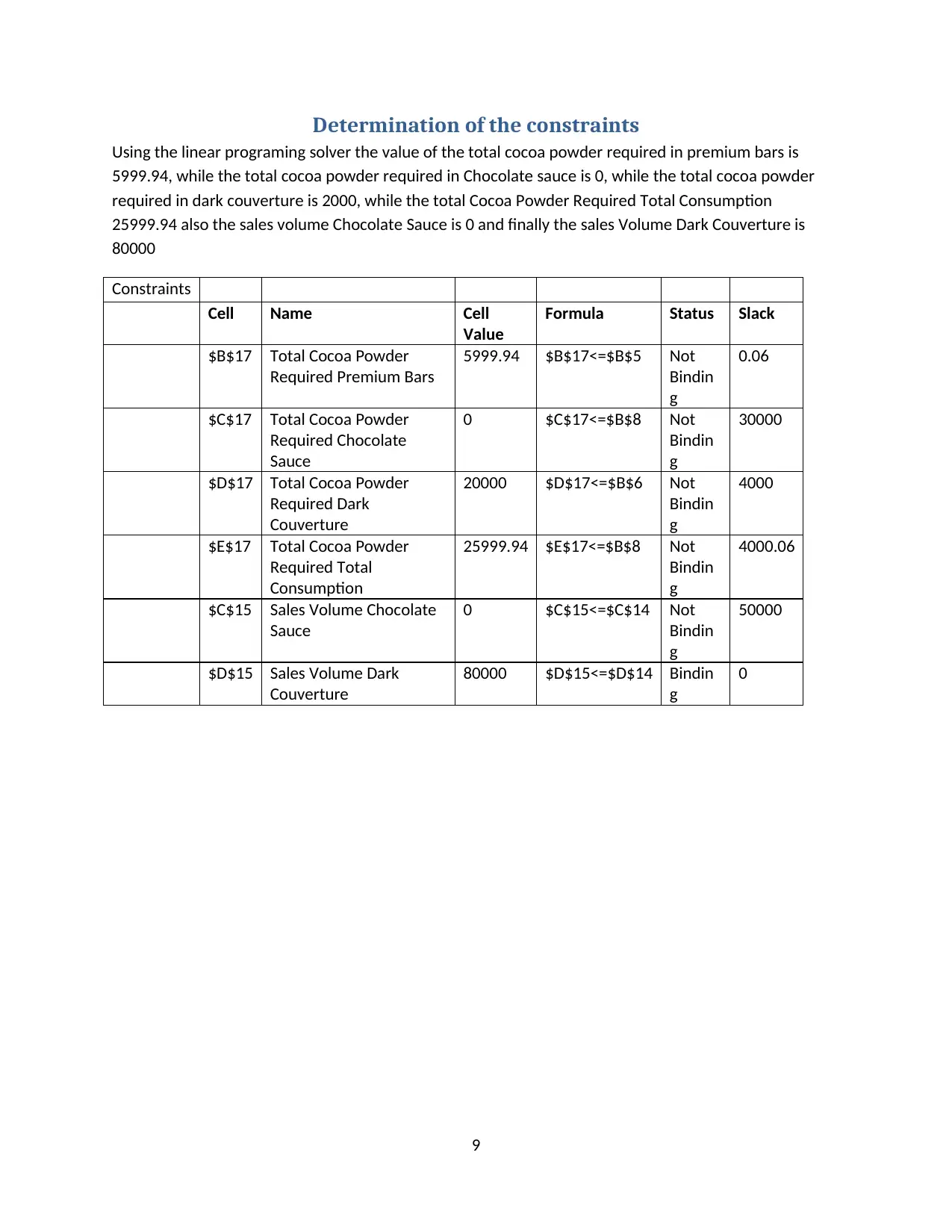

Determination of the constraints

Using the linear programing solver the value of the total cocoa powder required in premium bars is

5999.94, while the total cocoa powder required in Chocolate sauce is 0, while the total cocoa powder

required in dark couverture is 2000, while the total Cocoa Powder Required Total Consumption

25999.94 also the sales volume Chocolate Sauce is 0 and finally the sales Volume Dark Couverture is

80000

Constraints

Cell Name Cell

Value

Formula Status Slack

$B$17 Total Cocoa Powder

Required Premium Bars

5999.94 $B$17<=$B$5 Not

Bindin

g

0.06

$C$17 Total Cocoa Powder

Required Chocolate

Sauce

0 $C$17<=$B$8 Not

Bindin

g

30000

$D$17 Total Cocoa Powder

Required Dark

Couverture

20000 $D$17<=$B$6 Not

Bindin

g

4000

$E$17 Total Cocoa Powder

Required Total

Consumption

25999.94 $E$17<=$B$8 Not

Bindin

g

4000.06

$C$15 Sales Volume Chocolate

Sauce

0 $C$15<=$C$14 Not

Bindin

g

50000

$D$15 Sales Volume Dark

Couverture

80000 $D$15<=$D$14 Bindin

g

0

9

Using the linear programing solver the value of the total cocoa powder required in premium bars is

5999.94, while the total cocoa powder required in Chocolate sauce is 0, while the total cocoa powder

required in dark couverture is 2000, while the total Cocoa Powder Required Total Consumption

25999.94 also the sales volume Chocolate Sauce is 0 and finally the sales Volume Dark Couverture is

80000

Constraints

Cell Name Cell

Value

Formula Status Slack

$B$17 Total Cocoa Powder

Required Premium Bars

5999.94 $B$17<=$B$5 Not

Bindin

g

0.06

$C$17 Total Cocoa Powder

Required Chocolate

Sauce

0 $C$17<=$B$8 Not

Bindin

g

30000

$D$17 Total Cocoa Powder

Required Dark

Couverture

20000 $D$17<=$B$6 Not

Bindin

g

4000

$E$17 Total Cocoa Powder

Required Total

Consumption

25999.94 $E$17<=$B$8 Not

Bindin

g

4000.06

$C$15 Sales Volume Chocolate

Sauce

0 $C$15<=$C$14 Not

Bindin

g

50000

$D$15 Sales Volume Dark

Couverture

80000 $D$15<=$D$14 Bindin

g

0

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Solution to Ting`s questions

Number of boxes produced for each product

When determining the number of boxes that would be produced for each of the product, it was

found that 33333 boxes would be required in order to pack the premium chocolate bars and

80000 boxes would be required in order to pack the dark couverture. In case of packing the

chocolate sauce, there are no boxes required and therefore in an overall manner it is observed

that there is a requirement of 113333 boxes in order to pack all the chocolates and thereafter

offer for sales in the market. The linear program for the same is given below:

Max 12A + 14B + 11C

Where, 0.18A <= 6000 kgs.

0.2B <= 30000 kgs.

0.25C <= 24000 kgs.

0.18A + 0.2B + 0.25C <= 30000 kgs.

10

Number of boxes produced for each product

When determining the number of boxes that would be produced for each of the product, it was

found that 33333 boxes would be required in order to pack the premium chocolate bars and

80000 boxes would be required in order to pack the dark couverture. In case of packing the

chocolate sauce, there are no boxes required and therefore in an overall manner it is observed

that there is a requirement of 113333 boxes in order to pack all the chocolates and thereafter

offer for sales in the market. The linear program for the same is given below:

Max 12A + 14B + 11C

Where, 0.18A <= 6000 kgs.

0.2B <= 30000 kgs.

0.25C <= 24000 kgs.

0.18A + 0.2B + 0.25C <= 30000 kgs.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

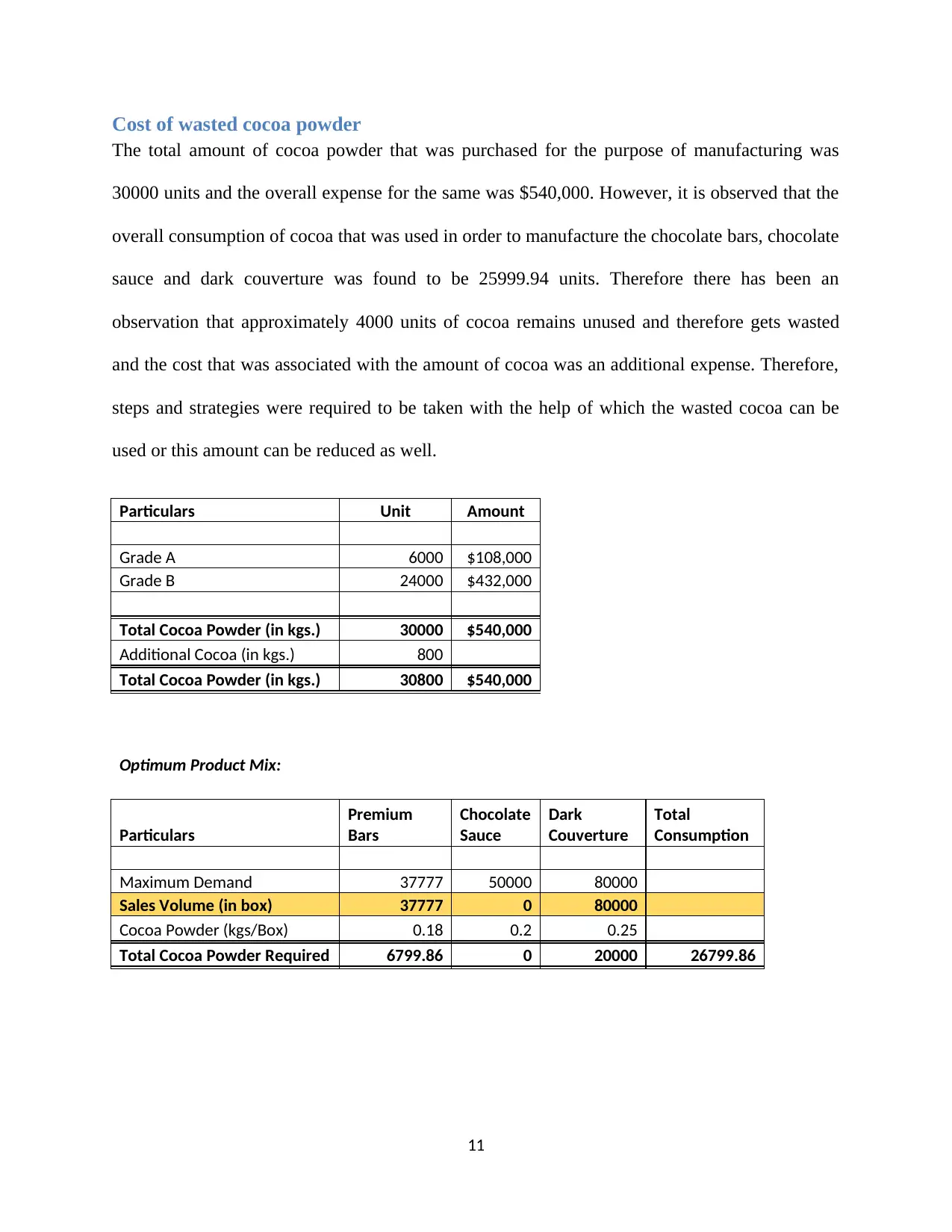

Cost of wasted cocoa powder

The total amount of cocoa powder that was purchased for the purpose of manufacturing was

30000 units and the overall expense for the same was $540,000. However, it is observed that the

overall consumption of cocoa that was used in order to manufacture the chocolate bars, chocolate

sauce and dark couverture was found to be 25999.94 units. Therefore there has been an

observation that approximately 4000 units of cocoa remains unused and therefore gets wasted

and the cost that was associated with the amount of cocoa was an additional expense. Therefore,

steps and strategies were required to be taken with the help of which the wasted cocoa can be

used or this amount can be reduced as well.

Particulars Unit Amount

Grade A 6000 $108,000

Grade B 24000 $432,000

Total Cocoa Powder (in kgs.) 30000 $540,000

Additional Cocoa (in kgs.) 800

Total Cocoa Powder (in kgs.) 30800 $540,000

Optimum Product Mix:

Particulars

Premium

Bars

Chocolate

Sauce

Dark

Couverture

Total

Consumption

Maximum Demand 37777 50000 80000

Sales Volume (in box) 37777 0 80000

Cocoa Powder (kgs/Box) 0.18 0.2 0.25

Total Cocoa Powder Required 6799.86 0 20000 26799.86

11

The total amount of cocoa powder that was purchased for the purpose of manufacturing was

30000 units and the overall expense for the same was $540,000. However, it is observed that the

overall consumption of cocoa that was used in order to manufacture the chocolate bars, chocolate

sauce and dark couverture was found to be 25999.94 units. Therefore there has been an

observation that approximately 4000 units of cocoa remains unused and therefore gets wasted

and the cost that was associated with the amount of cocoa was an additional expense. Therefore,

steps and strategies were required to be taken with the help of which the wasted cocoa can be

used or this amount can be reduced as well.

Particulars Unit Amount

Grade A 6000 $108,000

Grade B 24000 $432,000

Total Cocoa Powder (in kgs.) 30000 $540,000

Additional Cocoa (in kgs.) 800

Total Cocoa Powder (in kgs.) 30800 $540,000

Optimum Product Mix:

Particulars

Premium

Bars

Chocolate

Sauce

Dark

Couverture

Total

Consumption

Maximum Demand 37777 50000 80000

Sales Volume (in box) 37777 0 80000

Cocoa Powder (kgs/Box) 0.18 0.2 0.25

Total Cocoa Powder Required 6799.86 0 20000 26799.86

11

Comparison between the current strategy of a fixed volume agreement and variable

volume agreement.

Itn accordance to the current strategy which was a fixed volume agreement, there have been

wastage of approximately 4000 units of cocoa for which a certain amount of money was

invested. The maintenance of the fixed volume agreement refers to the fact that in each month

and year the company would be purchasing the same unit of cocoa irrespective of the fact that

whether they are able to optimally make use of the total amount of cocoa purchased. Hence, it is

agreeable that variable volume contract can be taken into consideration. Therefore, it would be

better for the company to shift their intention from the fixed volume agreement to the variable

volume of contract in which the company would be able to purchase the raw material based on

the demand in the market and the amount of production they would undertake. In this manner,

the unit of cocoa can vary according to the demand of the final product and thereby the amount

of wastage can be reduced and the additional cost that was added with the wasted material can be

mitigated. It is even seen that the company would be able to optimally make use of their

resources and in this manner would be able to enhance their operational activities and their

effectiveness in production.

12

volume agreement.

Itn accordance to the current strategy which was a fixed volume agreement, there have been

wastage of approximately 4000 units of cocoa for which a certain amount of money was

invested. The maintenance of the fixed volume agreement refers to the fact that in each month

and year the company would be purchasing the same unit of cocoa irrespective of the fact that

whether they are able to optimally make use of the total amount of cocoa purchased. Hence, it is

agreeable that variable volume contract can be taken into consideration. Therefore, it would be

better for the company to shift their intention from the fixed volume agreement to the variable

volume of contract in which the company would be able to purchase the raw material based on

the demand in the market and the amount of production they would undertake. In this manner,

the unit of cocoa can vary according to the demand of the final product and thereby the amount

of wastage can be reduced and the additional cost that was added with the wasted material can be

mitigated. It is even seen that the company would be able to optimally make use of their

resources and in this manner would be able to enhance their operational activities and their

effectiveness in production.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.