Foundations in Accounting: AGL Energy Non-Current Assets Report

VerifiedAdded on 2022/09/18

|12

|2451

|19

Report

AI Summary

This report examines the valuation of non-current assets, specifically focusing on AGL Energy Limited and its application of International Financial Reporting Standards (IFRS). The report begins with an overview of AGL Energy's operations within the Australian energy sector, highlighting key industry characteristics and strategic priorities. A literature review discusses the issues surrounding non-current asset valuation under IFRS, including the choice between cost and fair value models, depreciation methods, and impairment considerations for both Property, Plant, and Equipment (PPE) and intangible assets. The report then analyzes AGL Energy's practices, noting the use of the cost model for PPE, straight-line depreciation, and impairment reviews in accordance with AASB standards. It also examines the company's treatment of intangible assets, including software and licenses, and its approach to goodwill impairment. The analysis reveals AGL Energy's adherence to AASB standards and consistency in its valuation methods, providing insights into the company's financial reporting practices and the importance of accurate asset valuation for stakeholders. The report concludes by emphasizing the significance of proper non-current asset valuation for reflecting a company's true financial standing.

Running head: FOUNDATIONS IN ACCOUNTING

Foundations in Accounting

Name of the Student

Name of the University

Author’s Note

Foundations in Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FOUNDATIONS IN ACCOUNTING

Table of Contents

Introduction................................................................................................................................2

Description of the Company and Industry in which It Operates................................................2

Valuation of Non-Current Assets...............................................................................................3

Issues in Non-current assets Valuation under IFRS...............................................................3

Changes in PPE and Intangibles associated Valuation Depreciation and Impairment..........5

PPE.........................................................................................................................................5

Intangible Assets....................................................................................................................6

Conclusion..................................................................................................................................8

References................................................................................................................................10

Table of Contents

Introduction................................................................................................................................2

Description of the Company and Industry in which It Operates................................................2

Valuation of Non-Current Assets...............................................................................................3

Issues in Non-current assets Valuation under IFRS...............................................................3

Changes in PPE and Intangibles associated Valuation Depreciation and Impairment..........5

PPE.........................................................................................................................................5

Intangible Assets....................................................................................................................6

Conclusion..................................................................................................................................8

References................................................................................................................................10

2FOUNDATIONS IN ACCOUNTING

Introduction

Non-current assets form a major part of the total assets of a company and this has

major importance in the financial reporting. Two major parts of non-current assets are

Property, Plant and Equipment (PPE) and Intangible assets. It is the obligation on the

business organizations to comply with the appropriate principles and standards in order to

report and record the non-current assets in the financial statements. They are also required to

disclose the required additional information associated with non-current assets. The

Australian Accounting Standards Board (AASB) under the International Financial Reporting

Standards (IFRS)provides the Australian companies with the required standards for the

financial reporting of non-current assets. This report aims at discussing different aspects

associated with the PPE and intangible assets associated financial reporting of AGL Energy

Limited (AGL Energy).

Description of the Company and Industry in which It Operates

AGL Energy is an Australian Securities Exchange (ASX) listed company involved in

the operation to generate and retail electricity and gas for both the commercial and residential

use. It is regarded a leading energy company operating the largest private electricity

generation portfolio of Australia. AGL Energy caters to the need for electricity and gas of a

3.7 million customer base that includes residents, small and large businesses and wholesalers.

The business of AGL Energy is grounded on three strategic priorities; they are Growth,

Transformation and Social License. The ability of AGL Energy of undertaking major

investments in the capital projects and acquisitions has developed the ground for it to create

value for its shareholders. The key three focus areas of the next phase of growth investment

of AGL Energy include optimization of existing portfolio for performance and value,

Introduction

Non-current assets form a major part of the total assets of a company and this has

major importance in the financial reporting. Two major parts of non-current assets are

Property, Plant and Equipment (PPE) and Intangible assets. It is the obligation on the

business organizations to comply with the appropriate principles and standards in order to

report and record the non-current assets in the financial statements. They are also required to

disclose the required additional information associated with non-current assets. The

Australian Accounting Standards Board (AASB) under the International Financial Reporting

Standards (IFRS)provides the Australian companies with the required standards for the

financial reporting of non-current assets. This report aims at discussing different aspects

associated with the PPE and intangible assets associated financial reporting of AGL Energy

Limited (AGL Energy).

Description of the Company and Industry in which It Operates

AGL Energy is an Australian Securities Exchange (ASX) listed company involved in

the operation to generate and retail electricity and gas for both the commercial and residential

use. It is regarded a leading energy company operating the largest private electricity

generation portfolio of Australia. AGL Energy caters to the need for electricity and gas of a

3.7 million customer base that includes residents, small and large businesses and wholesalers.

The business of AGL Energy is grounded on three strategic priorities; they are Growth,

Transformation and Social License. The ability of AGL Energy of undertaking major

investments in the capital projects and acquisitions has developed the ground for it to create

value for its shareholders. The key three focus areas of the next phase of growth investment

of AGL Energy include optimization of existing portfolio for performance and value,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FOUNDATIONS IN ACCOUNTING

evolving and expanding the core energy market offerings and creation of new opportunities

with connected customers (agl.com.au, 2020).

AGL Energy operates in the Australian energy sector which can be considered as a

major sector contributing largely towards the economic development of the country. There

has been major changes in the Australian energy industry due to the shift in customer

expectations, new technologies adopting, greater intervention of the government and

regulators and investment environment full of uncertainties. These are the main

characteristics of this particular industry. At the same time, there has been major transitioning

taking place in the Australian energy sector from a system dependent ageing thermal

generation assets to an industry that is characterized by the aspects like renewable energy,

technologies with lower emissions, energy storage and firming technologies. As AGL Energy

is the largest generator of energy in the National Electricity Market, the company has a major

role to play in the development of the Australian energy sector(agl.com.au, 2020).

Valuation of Non-Current Assets

Issues in Non-current assets Valuation under IFRS

The involvement of the firms in valuing their non-current assets is considered as a

crucial aspect for the business organizations. This valuation process is subject to certain

issues under the IFRS that include both PPE and intangible assets. It involves both the

recognition and measurement of these assets in the most proper manner so that the correct

financial position of the companies reflect from them. The main issues faced by the IFRS

regarding the valuation of these assets include adoption of the correct recognition basis,

application of the relevant measurement base, depreciation method and impairment. The

companies are needed to adopt the appropriate method as per the standards of IFRS (Yao,

Percy & Hu, 2015).

evolving and expanding the core energy market offerings and creation of new opportunities

with connected customers (agl.com.au, 2020).

AGL Energy operates in the Australian energy sector which can be considered as a

major sector contributing largely towards the economic development of the country. There

has been major changes in the Australian energy industry due to the shift in customer

expectations, new technologies adopting, greater intervention of the government and

regulators and investment environment full of uncertainties. These are the main

characteristics of this particular industry. At the same time, there has been major transitioning

taking place in the Australian energy sector from a system dependent ageing thermal

generation assets to an industry that is characterized by the aspects like renewable energy,

technologies with lower emissions, energy storage and firming technologies. As AGL Energy

is the largest generator of energy in the National Electricity Market, the company has a major

role to play in the development of the Australian energy sector(agl.com.au, 2020).

Valuation of Non-Current Assets

Issues in Non-current assets Valuation under IFRS

The involvement of the firms in valuing their non-current assets is considered as a

crucial aspect for the business organizations. This valuation process is subject to certain

issues under the IFRS that include both PPE and intangible assets. It involves both the

recognition and measurement of these assets in the most proper manner so that the correct

financial position of the companies reflect from them. The main issues faced by the IFRS

regarding the valuation of these assets include adoption of the correct recognition basis,

application of the relevant measurement base, depreciation method and impairment. The

companies are needed to adopt the appropriate method as per the standards of IFRS (Yao,

Percy & Hu, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FOUNDATIONS IN ACCOUNTING

The most crucial issue in IFRS regarding the valuation of non-current asset is whether

to adopt fair value measurement base or historical cost measurement base after the

recognition of these assets. The presence of both cost model and revaluation model can be

seen for the valuation of the non-current assets. Under the cost model, the intangible assets,

specially the PPE, are valued at the cost of acquisition after the deduction of amortization,

depreciation and impairment losses. Therefore, impairment is a crucial aspect in the valuation

of the non-current assets under IFRS and obligation on the companies is to evaluate as well as

account for the impairment through considering appropriate accounting standard (Ball, Li

&Shivakumar, 2015).

Apart from the cost model, the presence of revaluation model can be seen in

measuring these assets assets where the companies are required to measure the non-current

assets at their fair values minis accumulated amortization and impairment losses. Even in this

case, the companies are required to consider the assessment of impairment of non-current

assets for recognizing any impairment losses. One crucial issue associated with this model is

the frequency in which the non-current assets are to be reviewed. IFRS has not explicitly

mentioned the frequency of revaluation of the non-current assets, but it has mentioned that

the frequency needs to be adequate so that there is not any material difference in the carrying

value from the fair value of the assets in the balance sheet (Nobes, 2015).

In the valuation of PPE under the non-current assets, selection of the appropriate

depreciation method can be considered as a major issue under IFRS. Selection and

application of the appropriate depreciation method helps in reflecting the correct value of the

non-current assets in the financial statements (Bryce, Ali & Mather, 2015). As mentioned by

the IFRS, the adopted depreciation method needs to reflect the design in which the future

economic benefits of the assets are expected to be consumed by the company. There are

different methods of depreciation that can be adopted by the company for depreciating the

The most crucial issue in IFRS regarding the valuation of non-current asset is whether

to adopt fair value measurement base or historical cost measurement base after the

recognition of these assets. The presence of both cost model and revaluation model can be

seen for the valuation of the non-current assets. Under the cost model, the intangible assets,

specially the PPE, are valued at the cost of acquisition after the deduction of amortization,

depreciation and impairment losses. Therefore, impairment is a crucial aspect in the valuation

of the non-current assets under IFRS and obligation on the companies is to evaluate as well as

account for the impairment through considering appropriate accounting standard (Ball, Li

&Shivakumar, 2015).

Apart from the cost model, the presence of revaluation model can be seen in

measuring these assets assets where the companies are required to measure the non-current

assets at their fair values minis accumulated amortization and impairment losses. Even in this

case, the companies are required to consider the assessment of impairment of non-current

assets for recognizing any impairment losses. One crucial issue associated with this model is

the frequency in which the non-current assets are to be reviewed. IFRS has not explicitly

mentioned the frequency of revaluation of the non-current assets, but it has mentioned that

the frequency needs to be adequate so that there is not any material difference in the carrying

value from the fair value of the assets in the balance sheet (Nobes, 2015).

In the valuation of PPE under the non-current assets, selection of the appropriate

depreciation method can be considered as a major issue under IFRS. Selection and

application of the appropriate depreciation method helps in reflecting the correct value of the

non-current assets in the financial statements (Bryce, Ali & Mather, 2015). As mentioned by

the IFRS, the adopted depreciation method needs to reflect the design in which the future

economic benefits of the assets are expected to be consumed by the company. There are

different methods of depreciation that can be adopted by the company for depreciating the

5FOUNDATIONS IN ACCOUNTING

PPE; such as straight-line method, diminishing balance method and the unit of production

method. The business organizations are required to take into consideration all these issues

and the solutions prescribed by the IFRS while firms involve in estimation PPE and

intangible assets (André, Dionysiou&Tsalavoutas, 2018).

Changes in PPE and Intangibles associated Valuation Depreciation and Impairment

PPE

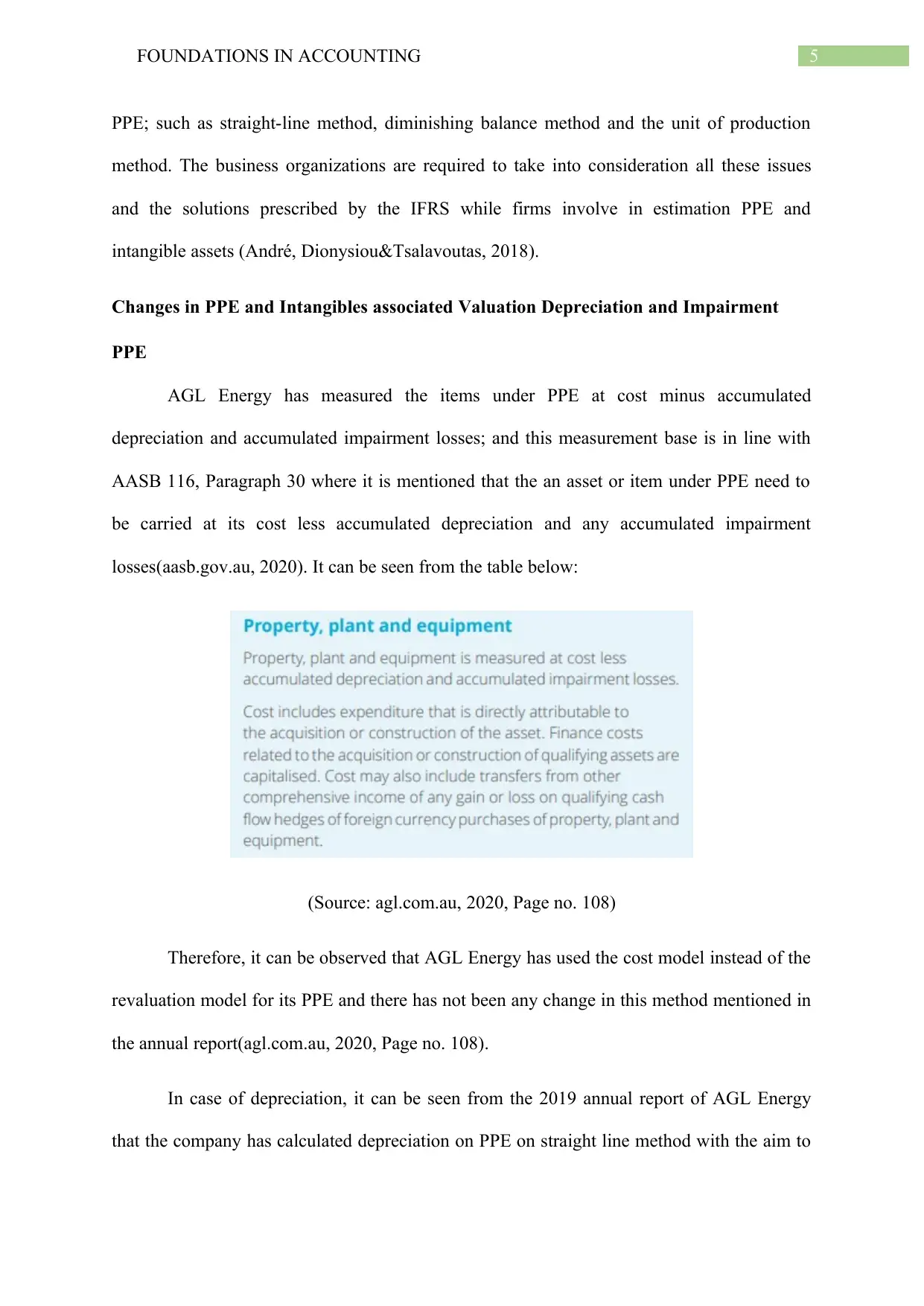

AGL Energy has measured the items under PPE at cost minus accumulated

depreciation and accumulated impairment losses; and this measurement base is in line with

AASB 116, Paragraph 30 where it is mentioned that the an asset or item under PPE need to

be carried at its cost less accumulated depreciation and any accumulated impairment

losses(aasb.gov.au, 2020). It can be seen from the table below:

(Source: agl.com.au, 2020, Page no. 108)

Therefore, it can be observed that AGL Energy has used the cost model instead of the

revaluation model for its PPE and there has not been any change in this method mentioned in

the annual report(agl.com.au, 2020, Page no. 108).

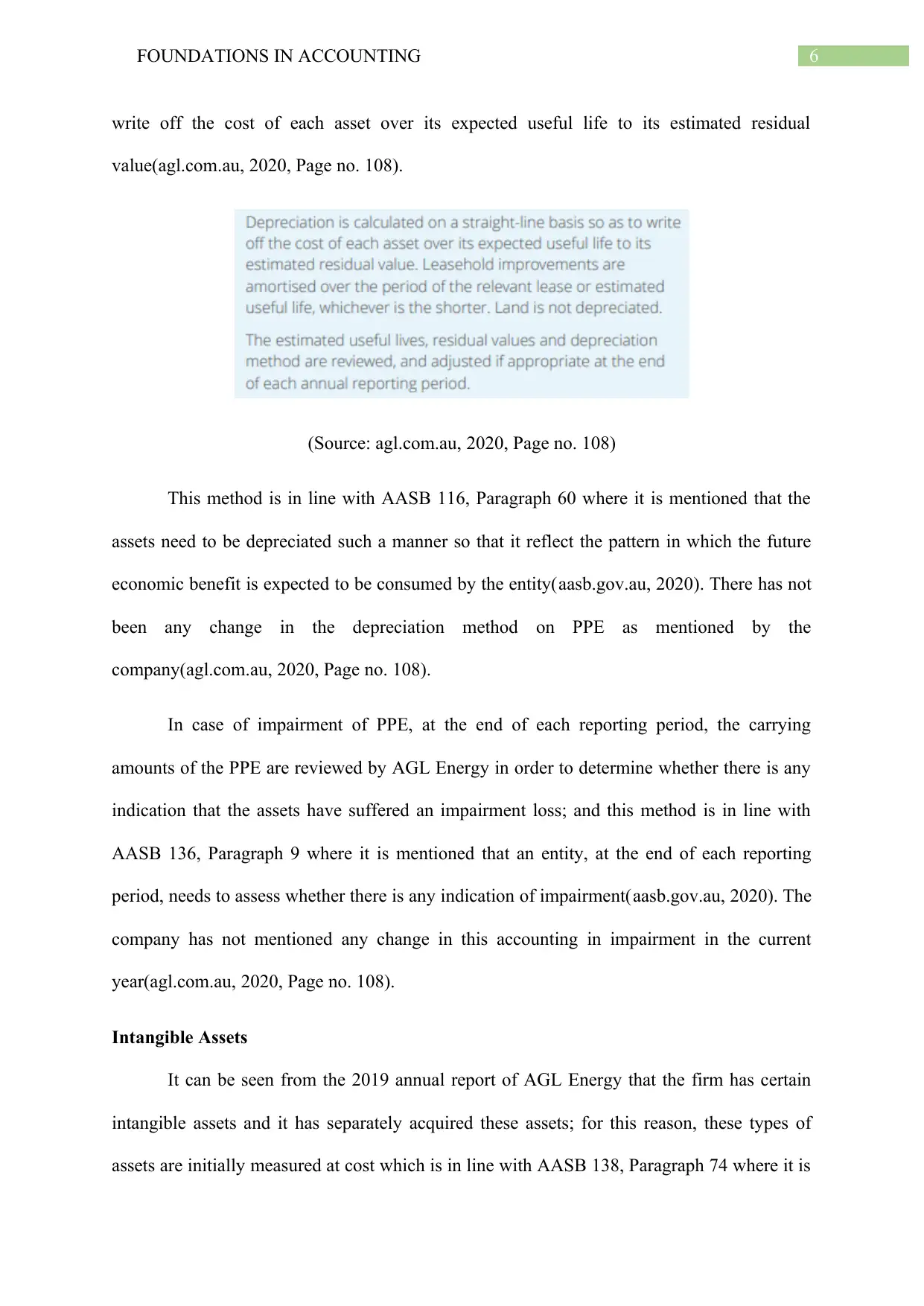

In case of depreciation, it can be seen from the 2019 annual report of AGL Energy

that the company has calculated depreciation on PPE on straight line method with the aim to

PPE; such as straight-line method, diminishing balance method and the unit of production

method. The business organizations are required to take into consideration all these issues

and the solutions prescribed by the IFRS while firms involve in estimation PPE and

intangible assets (André, Dionysiou&Tsalavoutas, 2018).

Changes in PPE and Intangibles associated Valuation Depreciation and Impairment

PPE

AGL Energy has measured the items under PPE at cost minus accumulated

depreciation and accumulated impairment losses; and this measurement base is in line with

AASB 116, Paragraph 30 where it is mentioned that the an asset or item under PPE need to

be carried at its cost less accumulated depreciation and any accumulated impairment

losses(aasb.gov.au, 2020). It can be seen from the table below:

(Source: agl.com.au, 2020, Page no. 108)

Therefore, it can be observed that AGL Energy has used the cost model instead of the

revaluation model for its PPE and there has not been any change in this method mentioned in

the annual report(agl.com.au, 2020, Page no. 108).

In case of depreciation, it can be seen from the 2019 annual report of AGL Energy

that the company has calculated depreciation on PPE on straight line method with the aim to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FOUNDATIONS IN ACCOUNTING

write off the cost of each asset over its expected useful life to its estimated residual

value(agl.com.au, 2020, Page no. 108).

(Source: agl.com.au, 2020, Page no. 108)

This method is in line with AASB 116, Paragraph 60 where it is mentioned that the

assets need to be depreciated such a manner so that it reflect the pattern in which the future

economic benefit is expected to be consumed by the entity(aasb.gov.au, 2020). There has not

been any change in the depreciation method on PPE as mentioned by the

company(agl.com.au, 2020, Page no. 108).

In case of impairment of PPE, at the end of each reporting period, the carrying

amounts of the PPE are reviewed by AGL Energy in order to determine whether there is any

indication that the assets have suffered an impairment loss; and this method is in line with

AASB 136, Paragraph 9 where it is mentioned that an entity, at the end of each reporting

period, needs to assess whether there is any indication of impairment(aasb.gov.au, 2020). The

company has not mentioned any change in this accounting in impairment in the current

year(agl.com.au, 2020, Page no. 108).

Intangible Assets

It can be seen from the 2019 annual report of AGL Energy that the firm has certain

intangible assets and it has separately acquired these assets; for this reason, these types of

assets are initially measured at cost which is in line with AASB 138, Paragraph 74 where it is

write off the cost of each asset over its expected useful life to its estimated residual

value(agl.com.au, 2020, Page no. 108).

(Source: agl.com.au, 2020, Page no. 108)

This method is in line with AASB 116, Paragraph 60 where it is mentioned that the

assets need to be depreciated such a manner so that it reflect the pattern in which the future

economic benefit is expected to be consumed by the entity(aasb.gov.au, 2020). There has not

been any change in the depreciation method on PPE as mentioned by the

company(agl.com.au, 2020, Page no. 108).

In case of impairment of PPE, at the end of each reporting period, the carrying

amounts of the PPE are reviewed by AGL Energy in order to determine whether there is any

indication that the assets have suffered an impairment loss; and this method is in line with

AASB 136, Paragraph 9 where it is mentioned that an entity, at the end of each reporting

period, needs to assess whether there is any indication of impairment(aasb.gov.au, 2020). The

company has not mentioned any change in this accounting in impairment in the current

year(agl.com.au, 2020, Page no. 108).

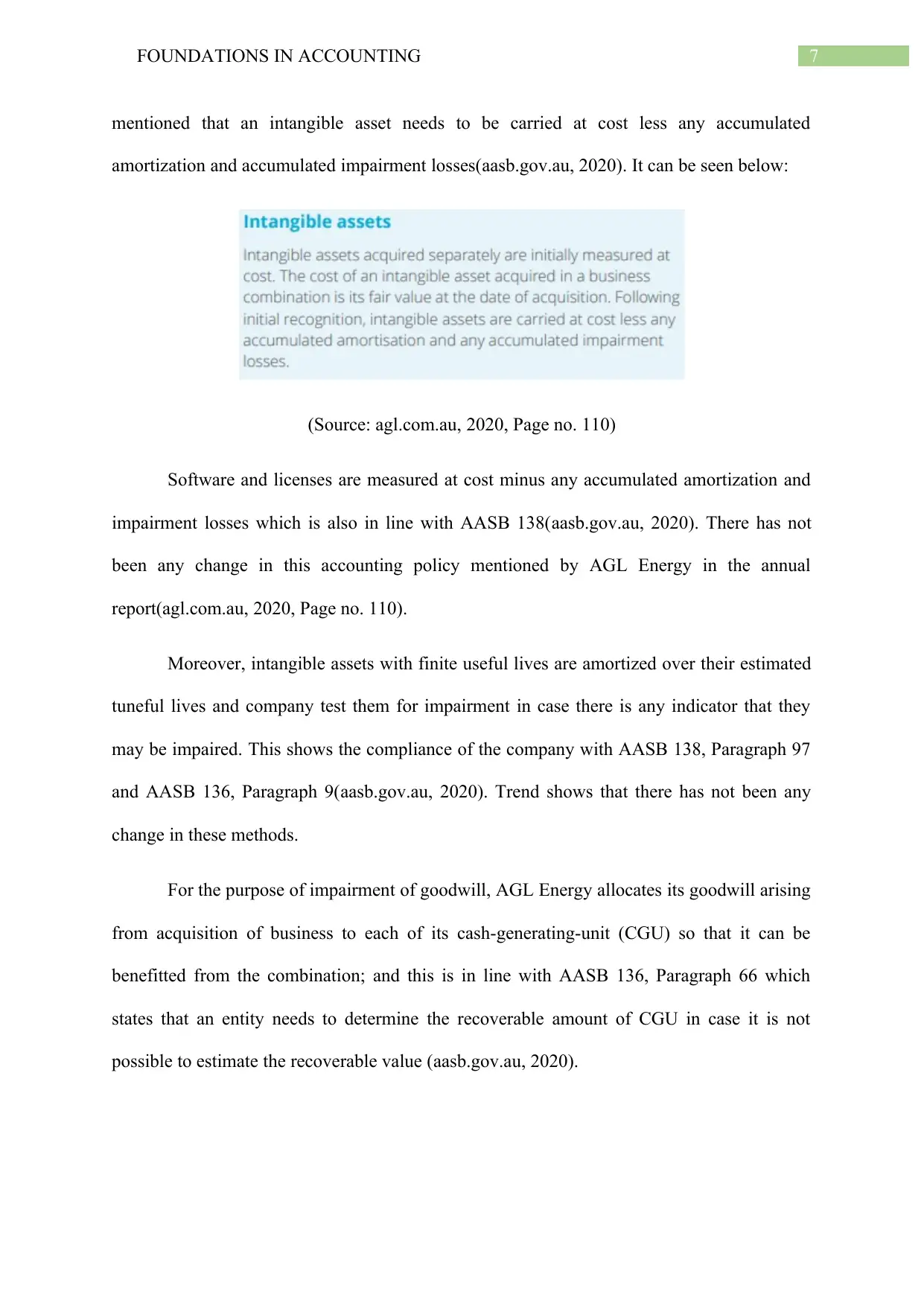

Intangible Assets

It can be seen from the 2019 annual report of AGL Energy that the firm has certain

intangible assets and it has separately acquired these assets; for this reason, these types of

assets are initially measured at cost which is in line with AASB 138, Paragraph 74 where it is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FOUNDATIONS IN ACCOUNTING

mentioned that an intangible asset needs to be carried at cost less any accumulated

amortization and accumulated impairment losses(aasb.gov.au, 2020). It can be seen below:

(Source: agl.com.au, 2020, Page no. 110)

Software and licenses are measured at cost minus any accumulated amortization and

impairment losses which is also in line with AASB 138(aasb.gov.au, 2020). There has not

been any change in this accounting policy mentioned by AGL Energy in the annual

report(agl.com.au, 2020, Page no. 110).

Moreover, intangible assets with finite useful lives are amortized over their estimated

tuneful lives and company test them for impairment in case there is any indicator that they

may be impaired. This shows the compliance of the company with AASB 138, Paragraph 97

and AASB 136, Paragraph 9(aasb.gov.au, 2020). Trend shows that there has not been any

change in these methods.

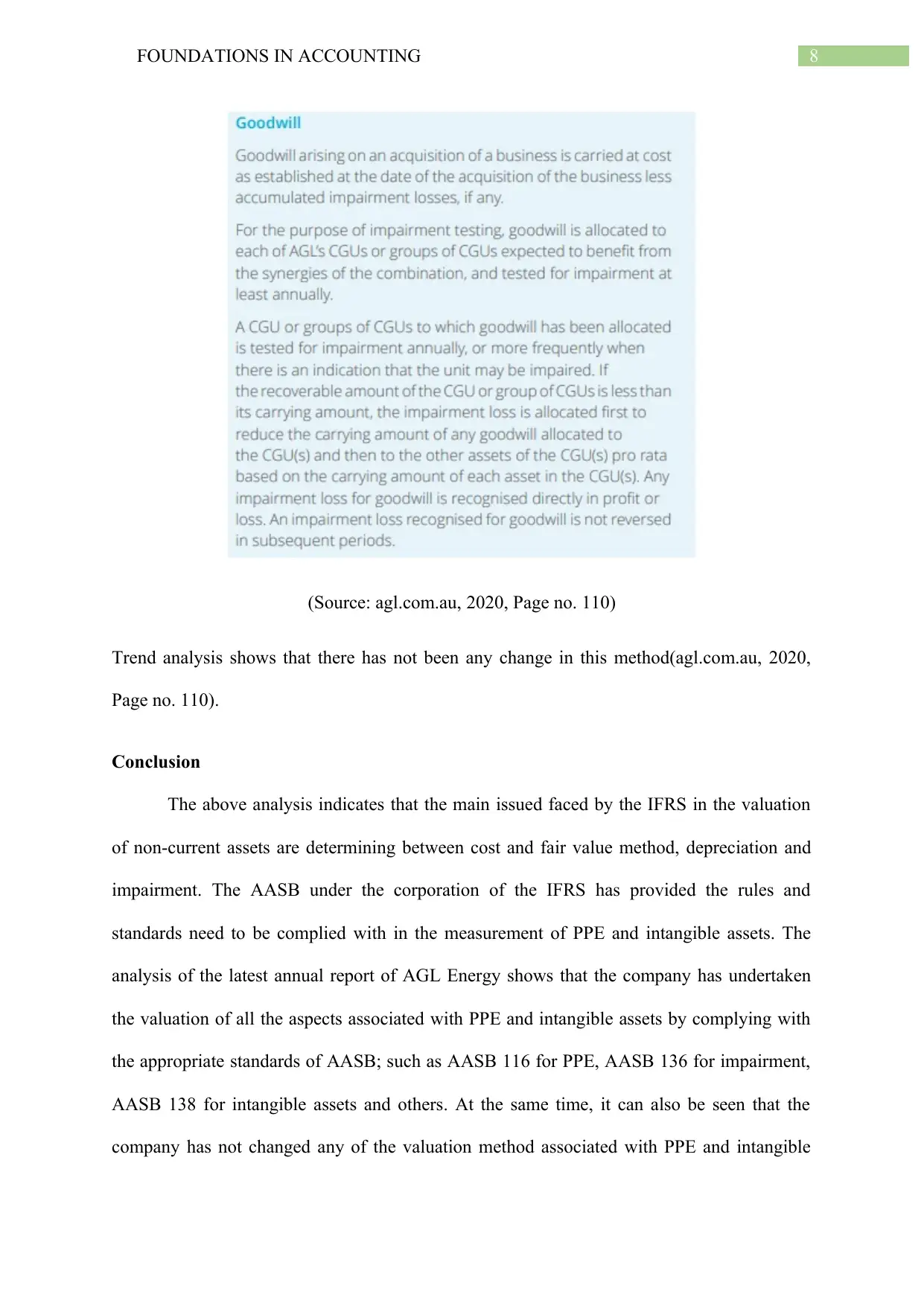

For the purpose of impairment of goodwill, AGL Energy allocates its goodwill arising

from acquisition of business to each of its cash-generating-unit (CGU) so that it can be

benefitted from the combination; and this is in line with AASB 136, Paragraph 66 which

states that an entity needs to determine the recoverable amount of CGU in case it is not

possible to estimate the recoverable value (aasb.gov.au, 2020).

mentioned that an intangible asset needs to be carried at cost less any accumulated

amortization and accumulated impairment losses(aasb.gov.au, 2020). It can be seen below:

(Source: agl.com.au, 2020, Page no. 110)

Software and licenses are measured at cost minus any accumulated amortization and

impairment losses which is also in line with AASB 138(aasb.gov.au, 2020). There has not

been any change in this accounting policy mentioned by AGL Energy in the annual

report(agl.com.au, 2020, Page no. 110).

Moreover, intangible assets with finite useful lives are amortized over their estimated

tuneful lives and company test them for impairment in case there is any indicator that they

may be impaired. This shows the compliance of the company with AASB 138, Paragraph 97

and AASB 136, Paragraph 9(aasb.gov.au, 2020). Trend shows that there has not been any

change in these methods.

For the purpose of impairment of goodwill, AGL Energy allocates its goodwill arising

from acquisition of business to each of its cash-generating-unit (CGU) so that it can be

benefitted from the combination; and this is in line with AASB 136, Paragraph 66 which

states that an entity needs to determine the recoverable amount of CGU in case it is not

possible to estimate the recoverable value (aasb.gov.au, 2020).

8FOUNDATIONS IN ACCOUNTING

(Source: agl.com.au, 2020, Page no. 110)

Trend analysis shows that there has not been any change in this method(agl.com.au, 2020,

Page no. 110).

Conclusion

The above analysis indicates that the main issued faced by the IFRS in the valuation

of non-current assets are determining between cost and fair value method, depreciation and

impairment. The AASB under the corporation of the IFRS has provided the rules and

standards need to be complied with in the measurement of PPE and intangible assets. The

analysis of the latest annual report of AGL Energy shows that the company has undertaken

the valuation of all the aspects associated with PPE and intangible assets by complying with

the appropriate standards of AASB; such as AASB 116 for PPE, AASB 136 for impairment,

AASB 138 for intangible assets and others. At the same time, it can also be seen that the

company has not changed any of the valuation method associated with PPE and intangible

(Source: agl.com.au, 2020, Page no. 110)

Trend analysis shows that there has not been any change in this method(agl.com.au, 2020,

Page no. 110).

Conclusion

The above analysis indicates that the main issued faced by the IFRS in the valuation

of non-current assets are determining between cost and fair value method, depreciation and

impairment. The AASB under the corporation of the IFRS has provided the rules and

standards need to be complied with in the measurement of PPE and intangible assets. The

analysis of the latest annual report of AGL Energy shows that the company has undertaken

the valuation of all the aspects associated with PPE and intangible assets by complying with

the appropriate standards of AASB; such as AASB 116 for PPE, AASB 136 for impairment,

AASB 138 for intangible assets and others. At the same time, it can also be seen that the

company has not changed any of the valuation method associated with PPE and intangible

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FOUNDATIONS IN ACCOUNTING

assets in 2019. Careful consideration of the issues associated with the measurement of the

assets like PPE and intangible assets assures that the firms report and record the correct

values of the same assets in the financial statements. This is crucial for the investors and

other users to assess the proper financial standings of the firms.

assets in 2019. Careful consideration of the issues associated with the measurement of the

assets like PPE and intangible assets assures that the firms report and record the correct

values of the same assets in the financial statements. This is crucial for the investors and

other users to assess the proper financial standings of the firms.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FOUNDATIONS IN ACCOUNTING

References

Aasb.gov.au. (2020). Property, Plant and Equipment. Retrieved 10 April 2020, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB116_08-

15_COMPdec16_01-19.pdf

Yao, D. F. T., Percy, M., & Hu, F. (2015). Fair value accounting for non-current assets and

audit fees: Evidence from Australian companies. Journal of Contemporary

Accounting & Economics, 11(1), 31-45.

Ball, R., Li, X., &Shivakumar, L. (2015). Contractibility and transparency of financial

statement information prepared under IFRS: Evidence from debt contracts around

IFRS adoption. Journal of Accounting Research, 53(5), 915-963.

Nobes, C. (2015). IFRS ten years on: has the IASB imposed extensive use of fair value? Has

the EU learnt to love IFRS? And does the use of fair value make IFRS illegal in the

EU?. Accounting in Europe, 12(2), 153-170.

Bryce, M., Ali, M. J., & Mather, P. R. (2015). Accounting quality in the pre-/post-IFRS

adoption periods and the impact on audit committee effectiveness—Evidence from

Australia. Pacific-Basin Finance Journal, 35, 163-181.

André, P., Dionysiou, D., &Tsalavoutas, I. (2018). Mandated disclosures under IAS 36

Impairment of Assets and IAS 38 Intangible Assets: value relevance and impact on

analysts’ forecasts. Applied Economics, 50(7), 707-725.

Barker, R., & Teixeira, A. (2018). Gaps in the IFRS conceptual framework. Accounting in

Europe, 15(2), 153-166.

References

Aasb.gov.au. (2020). Property, Plant and Equipment. Retrieved 10 April 2020, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB116_08-

15_COMPdec16_01-19.pdf

Yao, D. F. T., Percy, M., & Hu, F. (2015). Fair value accounting for non-current assets and

audit fees: Evidence from Australian companies. Journal of Contemporary

Accounting & Economics, 11(1), 31-45.

Ball, R., Li, X., &Shivakumar, L. (2015). Contractibility and transparency of financial

statement information prepared under IFRS: Evidence from debt contracts around

IFRS adoption. Journal of Accounting Research, 53(5), 915-963.

Nobes, C. (2015). IFRS ten years on: has the IASB imposed extensive use of fair value? Has

the EU learnt to love IFRS? And does the use of fair value make IFRS illegal in the

EU?. Accounting in Europe, 12(2), 153-170.

Bryce, M., Ali, M. J., & Mather, P. R. (2015). Accounting quality in the pre-/post-IFRS

adoption periods and the impact on audit committee effectiveness—Evidence from

Australia. Pacific-Basin Finance Journal, 35, 163-181.

André, P., Dionysiou, D., &Tsalavoutas, I. (2018). Mandated disclosures under IAS 36

Impairment of Assets and IAS 38 Intangible Assets: value relevance and impact on

analysts’ forecasts. Applied Economics, 50(7), 707-725.

Barker, R., & Teixeira, A. (2018). Gaps in the IFRS conceptual framework. Accounting in

Europe, 15(2), 153-166.

11FOUNDATIONS IN ACCOUNTING

Aasb.gov.au. (2020). Impairment of Assets. Retrieved 10 April 2020, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB136_08-

15_COMPdec16_01-19.pdf

Agl.com.au. (2020). 2019 Annual Report. Retrieved 10 April 2020, from

https://www.agl.com.au/-/media/aglmedia/documents/about-agl/investors/annual-

reports/agl_annual_report_090819.pdf?

la=en&hash=2890C67A39531E9197467BBC1F87B463

Who we are. (2020). Retrieved 10 April 2020, from https://www.agl.com.au/about-agl/who-

we-are

Aasb.gov.au. (2020). Intangible Assets. Retrieved 10 April 2020, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-

15_COMPjul17_01-20.pdf

Aasb.gov.au. (2020). Impairment of Assets. Retrieved 10 April 2020, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB136_08-

15_COMPdec16_01-19.pdf

Agl.com.au. (2020). 2019 Annual Report. Retrieved 10 April 2020, from

https://www.agl.com.au/-/media/aglmedia/documents/about-agl/investors/annual-

reports/agl_annual_report_090819.pdf?

la=en&hash=2890C67A39531E9197467BBC1F87B463

Who we are. (2020). Retrieved 10 April 2020, from https://www.agl.com.au/about-agl/who-

we-are

Aasb.gov.au. (2020). Intangible Assets. Retrieved 10 April 2020, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-

15_COMPjul17_01-20.pdf

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.