Non-Performing Loans and Profitability of Agrani Bank Limited

VerifiedAdded on 2020/10/27

|43

|8453

|598

Report

AI Summary

This report, prepared for the Department of Banking and Insurance at the University of Dhaka, investigates the issue of non-performing loans (NPLs) and their impact on the profitability of Agrani Bank Limited in Bangladesh. The study begins with an introduction to the problem, highlighting the adverse effects of NPLs on the banking sector and the broader economy. It outlines the objectives, methodology, and data collection methods used in the research, including both quantitative and qualitative approaches. The report then delves into a literature review, discussing the causes and consequences of NPLs, as well as existing research on the topic. The study also includes an overview of Agrani Bank Limited and an analysis of its financial performance. The report aims to identify the factors contributing to NPLs, assess their impact on the bank's profitability, and provide recommendations to mitigate the burden of NPLs. The research incorporates time-series data and secondary sources to analyze the trends and effects of NPLs. It also explores the role of government policies, such as interest rate policies, in influencing loan defaults. The findings of this report are crucial for policymakers and stakeholders in the banking sector seeking to improve the financial health of Agrani Bank and the overall economy.

A Report on

Non-Performing Loan and Its Impacts on Profitability

of Agrani Bank Limited

Submitted To,

Abu Taleb

Professor

Department of Banking and Insurance

Faculty of Business Studies

University of Dhaka

Submitted By,

Gazi Rahat

ID: 22-124

Department of Banking and Insurance

Faculty of Business Studies

University of Dhaka

Non-Performing Loan and Its Impacts on Profitability

of Agrani Bank Limited

Submitted To,

Abu Taleb

Professor

Department of Banking and Insurance

Faculty of Business Studies

University of Dhaka

Submitted By,

Gazi Rahat

ID: 22-124

Department of Banking and Insurance

Faculty of Business Studies

University of Dhaka

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Chapter-One: Introduction

1. 00 Introduction

For economic development, a country needs balanced and feasible flow of saving investment

process. Bangladesh now is in developing phase because of rapid growth in RMG sector but this

growth is also hampered by the underdeveloped capital market, raise of Non-performing loans

both on private commercial and state owned commercial banks. The intermediary activity of a

bank is providing loans to the potential investors by checking their credit worthiness.

It is known that profitability of a bank is reduces by the NPL , because banks cannot generate the

appropriate interest income from the classified loans. When a bank has high number of loan

defaults than the bank has to set aside a portion of income as a loss reserve.

At present, the Agrani Bank limited having unfavorable position of NPLs compare to other

private commercial banks in Bangladesh. “Bad Loan” management is the most unsatisfactory

performance in the bank, which consistently accounts for more that 80% of total NPLs. This

scenario is clearly saying that the inefficiency of the credit management to tackle the “flow

problem of bad loans”. Therefore, the first challenge facing Agrani Bank Limited is how to

address the flow problem of bad loans.

In Bangladesh there are nine state run banks and there are accounted for 51.27% of total NPL of

TK.1,16288.31 crore in banking sector. According to the ministry of finance Agrani bank has the

percentage of NPL in first quarter of 2019 is 16.67% and in second quarter it went down to

14.5%.

1.01 Background

Non-performing loans (NPL) or classified loans have a demolishing impact not only on overall

banking sector in Bangladesh but also on the whole economy of the country. Reasons behind the

classified loans are willful defaulters who are unwilling to repay the loans and next reason is

loans go to down grade because of poor business performance due to changes in the political

economy and environmental changes. For this NPL, provisions should be set aside on classified

For economic development, a country needs balanced and feasible flow of saving investment

process. Bangladesh now is in developing phase because of rapid growth in RMG sector but this

growth is also hampered by the underdeveloped capital market, raise of Non-performing loans

both on private commercial and state owned commercial banks. The intermediary activity of a

bank is providing loans to the potential investors by checking their credit worthiness.

It is known that profitability of a bank is reduces by the NPL , because banks cannot generate the

appropriate interest income from the classified loans. When a bank has high number of loan

defaults than the bank has to set aside a portion of income as a loss reserve.

At present, the Agrani Bank limited having unfavorable position of NPLs compare to other

private commercial banks in Bangladesh. “Bad Loan” management is the most unsatisfactory

performance in the bank, which consistently accounts for more that 80% of total NPLs. This

scenario is clearly saying that the inefficiency of the credit management to tackle the “flow

problem of bad loans”. Therefore, the first challenge facing Agrani Bank Limited is how to

address the flow problem of bad loans.

In Bangladesh there are nine state run banks and there are accounted for 51.27% of total NPL of

TK.1,16288.31 crore in banking sector. According to the ministry of finance Agrani bank has the

percentage of NPL in first quarter of 2019 is 16.67% and in second quarter it went down to

14.5%.

1.01 Background

Non-performing loans (NPL) or classified loans have a demolishing impact not only on overall

banking sector in Bangladesh but also on the whole economy of the country. Reasons behind the

classified loans are willful defaulters who are unwilling to repay the loans and next reason is

loans go to down grade because of poor business performance due to changes in the political

economy and environmental changes. For this NPL, provisions should be set aside on classified

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

loans. This report has carry the actual reasons of NPL and the impacts of NPL on the

profitability, deposits and in banking operation. Bank’s NPL rose by 20.23 percent or tk. 15,037

crores in the space of just six months to june 2019, that is higher than cost or expenses for

development budget of last fiscal year. Increasing trend of NPL has the significant effects

because of bad loans on the profitability, total deposits and also on operation of the banking

system. Internationally tolerable level for NPLS is 2%-3% of total loans where in Bangladesh,

NPLs is 20.23 of total loans according to Bangladesh Bank. In the meantime, state-owned banks

are incurring NPLs in the highest rate than the others like PCBs, FCBs, DFIs or Specialized

Banks in Bangladesh.

This study will identify the actual picture of non-performing loans (NPLs) of banking sector in

Bangladesh. This report will also state the reasons and facts of non-performing loans (NPLs).

This study will figure out the way to rescue our banking sector from this bad practice through

proper analysis and documentation. For conducting this research collection of secondary data

relating to financial position and policies from Agrani Bank Limited.

1.02 Objectives of the study

To know the current scenario of non- performing loan of Agrani bank of Bangladesh.

To familiar with loan granting supervision and monitoring process of Agrani bank of

Bangladesh.

To identify the ever increasing trend of non-performing loan of the bank.

To examine the impacts of non-performing loan of the bank.

To put forward some suggestion and recommendation to lessen the non-performing loan

burden of the bank.

1.03 Methodology

In this research the used methods are quantitative and qualitative. Here I will try to Measure the

condition of NPL and how the profitability is affected by the defaulter especially on Agrani Bank

Bangladesh Ltd. In this research time series data of Agrani bank limited will be used to show the

NPL condition of the bank. It is a research on trend analysis on the degree and direction of the

NPLs and its profitability.

profitability, deposits and in banking operation. Bank’s NPL rose by 20.23 percent or tk. 15,037

crores in the space of just six months to june 2019, that is higher than cost or expenses for

development budget of last fiscal year. Increasing trend of NPL has the significant effects

because of bad loans on the profitability, total deposits and also on operation of the banking

system. Internationally tolerable level for NPLS is 2%-3% of total loans where in Bangladesh,

NPLs is 20.23 of total loans according to Bangladesh Bank. In the meantime, state-owned banks

are incurring NPLs in the highest rate than the others like PCBs, FCBs, DFIs or Specialized

Banks in Bangladesh.

This study will identify the actual picture of non-performing loans (NPLs) of banking sector in

Bangladesh. This report will also state the reasons and facts of non-performing loans (NPLs).

This study will figure out the way to rescue our banking sector from this bad practice through

proper analysis and documentation. For conducting this research collection of secondary data

relating to financial position and policies from Agrani Bank Limited.

1.02 Objectives of the study

To know the current scenario of non- performing loan of Agrani bank of Bangladesh.

To familiar with loan granting supervision and monitoring process of Agrani bank of

Bangladesh.

To identify the ever increasing trend of non-performing loan of the bank.

To examine the impacts of non-performing loan of the bank.

To put forward some suggestion and recommendation to lessen the non-performing loan

burden of the bank.

1.03 Methodology

In this research the used methods are quantitative and qualitative. Here I will try to Measure the

condition of NPL and how the profitability is affected by the defaulter especially on Agrani Bank

Bangladesh Ltd. In this research time series data of Agrani bank limited will be used to show the

NPL condition of the bank. It is a research on trend analysis on the degree and direction of the

NPLs and its profitability.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.3.01 Research design

A research design is considered as the framework or plan for a study that guides as well as helps

the data collection and analysis of data. The research design may be exploratory descriptive and

experimental for the present study. The descriptive and experimental research design is adopted

for this project. For this study purpose, I have conducted the time series data of Agrani Bank

Bangladesh Ltd. to evaluate the impact of non-performing loans on profitability of the bank.

1.3.02 Data Collection

The data collection has been done from different journals and other reliable secondary sources to

find out the effect of NPLs on profitability and data from Agrani Bank Ltd.

1.3.03 Data Analysis

The data is collected from different authentic sources and analyzed to get the hints and facts

about the presumption that is whether there has impact of non-performing loan on profitability.

There has been taken Secondary data to analyzed the regression and correlation among the

dependent and independent variables. Dependent and independent variables have been taken to

assess the association among them.

1.04 Problem Statement

The mandatory aim of commercial bank is to generate profit by collecting the deposits from the

customers of surplus units of money and lend loans to the people of deficit units of the financial

sectors of a country. The purpose of our Banking sector is also the same. Non-performing loans

are hampering the regular business activities of state owned commercial banks. Our state owned

commercial banks follows rules and regulations from the Bank Company Act 1991 and time-to-

time guidelines of Bangladesh bank. The most dangerous thing for our banking industry is the

NPLs and it is increasing. The Bangladesh Bank is on the way to solve this problem. They are

increasing the provisions for classified loans to reduce aggressive lending. However, the amount

of NPLs is not controlled by the commercial banks. My research proposal is to identify the

causes of non-performing loans, its actual amount, and find out the ways to get round the NPLs.

A research design is considered as the framework or plan for a study that guides as well as helps

the data collection and analysis of data. The research design may be exploratory descriptive and

experimental for the present study. The descriptive and experimental research design is adopted

for this project. For this study purpose, I have conducted the time series data of Agrani Bank

Bangladesh Ltd. to evaluate the impact of non-performing loans on profitability of the bank.

1.3.02 Data Collection

The data collection has been done from different journals and other reliable secondary sources to

find out the effect of NPLs on profitability and data from Agrani Bank Ltd.

1.3.03 Data Analysis

The data is collected from different authentic sources and analyzed to get the hints and facts

about the presumption that is whether there has impact of non-performing loan on profitability.

There has been taken Secondary data to analyzed the regression and correlation among the

dependent and independent variables. Dependent and independent variables have been taken to

assess the association among them.

1.04 Problem Statement

The mandatory aim of commercial bank is to generate profit by collecting the deposits from the

customers of surplus units of money and lend loans to the people of deficit units of the financial

sectors of a country. The purpose of our Banking sector is also the same. Non-performing loans

are hampering the regular business activities of state owned commercial banks. Our state owned

commercial banks follows rules and regulations from the Bank Company Act 1991 and time-to-

time guidelines of Bangladesh bank. The most dangerous thing for our banking industry is the

NPLs and it is increasing. The Bangladesh Bank is on the way to solve this problem. They are

increasing the provisions for classified loans to reduce aggressive lending. However, the amount

of NPLs is not controlled by the commercial banks. My research proposal is to identify the

causes of non-performing loans, its actual amount, and find out the ways to get round the NPLs.

Chapter-Two: Literature Review

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.00 Literature Review

Nonperforming loans (“NPLs”) means when banks financial asset no longer receive the

installment payment and or interest as scheduled. It known as non-performing because it reduce

loan performance or bank income generate from its loan products. Choudhury and Adhikary

(2002) stated that NPL is a “multiclass” concept but rather not a “uniclass”, which means that

NPLs can be classified into different varieties usually based on the “length of overdue” of the

said loans. In the eve of financial crisis NPLs are worked as a typical byproduct. It is an

occasional accident of the lending process not a basic product of the lending function, one that

has enormous potential to deepen the severity and duration of financial crisis and to complicate

macroeconomic management (Podderand Al Mamun, 2004).

That is because it (NPLs) bring down depositors confidence in the banking sectors, piling up

unproductive economic resources and impeding the resource allocation process. On the other

hand, Lack of diverted uses of funds, proper customer verification, real estate business slow

pace, political instability, weak supervision power of central bank etc. are the root causes of NPL

in Bangladesh. Sustainable banking activities are given priority by the authors which means

future resources will not be compromised to augment the today’soutputs.

The argument is that if NPL remains in the growing trend by taking the path of aggressive banki

ng like buying bad loans, giving the loans to traditional defaulters, massive influence of the inter

nal customers of banks and board of directors in sanctioning poor loans to political people, sustai

nability will be compromised Repetitive restructuring of loans is appeared as good loans in the

financial statement of banks which are actually not good loans.

Such types of activities help to demonstrate superior performance in bank operations, resulting in

increased bank profitability, which encourages investors to have a good relationship with banks a

nd customers, particularly depositors, face problems with withdrawing their deposited fundsbank

s should therefore take appropriate measures to create transparency in the sanctioning of credit, a

nd bangladesh bank should take some steps to ensure that commercial banks and nationalize ban

ks are subject to serious inspection of every loan application before penalizing loans to potential

customers. (alam, shafiqul, mahbubul haq, md., & kader, abul, 2015,

Nonperforming loans (“NPLs”) means when banks financial asset no longer receive the

installment payment and or interest as scheduled. It known as non-performing because it reduce

loan performance or bank income generate from its loan products. Choudhury and Adhikary

(2002) stated that NPL is a “multiclass” concept but rather not a “uniclass”, which means that

NPLs can be classified into different varieties usually based on the “length of overdue” of the

said loans. In the eve of financial crisis NPLs are worked as a typical byproduct. It is an

occasional accident of the lending process not a basic product of the lending function, one that

has enormous potential to deepen the severity and duration of financial crisis and to complicate

macroeconomic management (Podderand Al Mamun, 2004).

That is because it (NPLs) bring down depositors confidence in the banking sectors, piling up

unproductive economic resources and impeding the resource allocation process. On the other

hand, Lack of diverted uses of funds, proper customer verification, real estate business slow

pace, political instability, weak supervision power of central bank etc. are the root causes of NPL

in Bangladesh. Sustainable banking activities are given priority by the authors which means

future resources will not be compromised to augment the today’soutputs.

The argument is that if NPL remains in the growing trend by taking the path of aggressive banki

ng like buying bad loans, giving the loans to traditional defaulters, massive influence of the inter

nal customers of banks and board of directors in sanctioning poor loans to political people, sustai

nability will be compromised Repetitive restructuring of loans is appeared as good loans in the

financial statement of banks which are actually not good loans.

Such types of activities help to demonstrate superior performance in bank operations, resulting in

increased bank profitability, which encourages investors to have a good relationship with banks a

nd customers, particularly depositors, face problems with withdrawing their deposited fundsbank

s should therefore take appropriate measures to create transparency in the sanctioning of credit, a

nd bangladesh bank should take some steps to ensure that commercial banks and nationalize ban

ks are subject to serious inspection of every loan application before penalizing loans to potential

customers. (alam, shafiqul, mahbubul haq, md., & kader, abul, 2015,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Mohanty (2006)states that financial risk increases in the banking sectors that causes the liquidity

crisis if the risk is not quickly eliminated. These crises not only lower the living of standard but

also can erase much of the successes of economic reform overnight.

Desai and Farmer (2001)argued that the expansion of credit policy during the early liberation

period, aimed at comparatively easier lending, merely increased credit nominally within the econ

omy. Neverthelessit also created a large number of willing history defaulters who subsequently u

ndermined banks ' financial health through the "sick industry syndrome."Nevertheless, in the 199

0s a broadbased financial initiativewas implemented in the name of FSRP, enlisting World Bank

support to restore the country's financial discipline. The banking industry has since implemented

"prudential rules" for the classification and provisioning of loans (Bangladesh Bank, 2014).

Certain rules, legislation, and instruments such as loan ledger book, loan risk analysis manual, pe

rformance planning program, interest rate reform, and the 1990 Money Loan Court Act were also

enacted to encourage safe, efficient and stable banking procedure. Surprisingly, Bangladesh's ba

nking system has yet to free itself from the grip of the NPL fiasco, even after so many steps. The

question thus arises, what are the reasons behind such a large proportion of nonperforming loans

in the economy of Bangladesh?

Is it because of the banks ' ' flexibility in identifying NPLs ' or lack of successful ' recovery strate

gies? Alt-ernatively, is this due to weak legal status of non-performing loans legislation? He

present study focused primarily on the above issue with a view to assisting policymakers in

formulating concrete steps concerning sound management of NPLs in Bangladesh. (Boi.gov.bd,

2015)

Government interest rate policy leads significantly to ineffective loans in a paper published by

Hossian and Hoque. They also reported that loans default in emerging and developed economies

is growing despite the banking remedial steps. Remedial practices for securing repayment of

installments or complete loans given to major corporations or industrial sectors are facing

problems with their loan recovery. Measures to recover loans from customers are like offering

fresh loans to help customers struggle to reinvigorate their company to run profitability,

rescheduling loans, legal proceeding, interest rate as a penalty etc. are failing back to recover

default loan from customers.

crisis if the risk is not quickly eliminated. These crises not only lower the living of standard but

also can erase much of the successes of economic reform overnight.

Desai and Farmer (2001)argued that the expansion of credit policy during the early liberation

period, aimed at comparatively easier lending, merely increased credit nominally within the econ

omy. Neverthelessit also created a large number of willing history defaulters who subsequently u

ndermined banks ' financial health through the "sick industry syndrome."Nevertheless, in the 199

0s a broadbased financial initiativewas implemented in the name of FSRP, enlisting World Bank

support to restore the country's financial discipline. The banking industry has since implemented

"prudential rules" for the classification and provisioning of loans (Bangladesh Bank, 2014).

Certain rules, legislation, and instruments such as loan ledger book, loan risk analysis manual, pe

rformance planning program, interest rate reform, and the 1990 Money Loan Court Act were also

enacted to encourage safe, efficient and stable banking procedure. Surprisingly, Bangladesh's ba

nking system has yet to free itself from the grip of the NPL fiasco, even after so many steps. The

question thus arises, what are the reasons behind such a large proportion of nonperforming loans

in the economy of Bangladesh?

Is it because of the banks ' ' flexibility in identifying NPLs ' or lack of successful ' recovery strate

gies? Alt-ernatively, is this due to weak legal status of non-performing loans legislation? He

present study focused primarily on the above issue with a view to assisting policymakers in

formulating concrete steps concerning sound management of NPLs in Bangladesh. (Boi.gov.bd,

2015)

Government interest rate policy leads significantly to ineffective loans in a paper published by

Hossian and Hoque. They also reported that loans default in emerging and developed economies

is growing despite the banking remedial steps. Remedial practices for securing repayment of

installments or complete loans given to major corporations or industrial sectors are facing

problems with their loan recovery. Measures to recover loans from customers are like offering

fresh loans to help customers struggle to reinvigorate their company to run profitability,

rescheduling loans, legal proceeding, interest rate as a penalty etc. are failing back to recover

default loan from customers.

Authors also distinguished between the defaulters that are regular defaulters, and those who are n

ot. Typically default happens when lenders are prepared to repay their loans but are unable to. Ha

bitual defaults occur when lenders can repay but don't want to repay their loans. They decided to

view us that interest rate policy has a major effect on the borrowers ' default loan rate. Not only i

s the reluctance of lenders not a prime component of defaults but even the policy of government i

nterest rates will lead to the non-repayment of payments.

That means high interest rates lead to high default rates for the borrowers. From 1995 to 2008, th

e interest rate for industrial loans has nearly doubled (10 to 17 per cent). Since the companies bea

r high interest rates on industrial loans, they often are incapable of repaying their borrowed mone

y when the role of industry in the economy is not good or safe. From the hypothesis testing, auth

ors found that a strong negative association exists between loan default and high market interest r

ate introduced by Bangladesh government. (Ziaul Hoque, Mohammad, Zakir Hossain,

Mohammad, 2008,

ot. Typically default happens when lenders are prepared to repay their loans but are unable to. Ha

bitual defaults occur when lenders can repay but don't want to repay their loans. They decided to

view us that interest rate policy has a major effect on the borrowers ' default loan rate. Not only i

s the reluctance of lenders not a prime component of defaults but even the policy of government i

nterest rates will lead to the non-repayment of payments.

That means high interest rates lead to high default rates for the borrowers. From 1995 to 2008, th

e interest rate for industrial loans has nearly doubled (10 to 17 per cent). Since the companies bea

r high interest rates on industrial loans, they often are incapable of repaying their borrowed mone

y when the role of industry in the economy is not good or safe. From the hypothesis testing, auth

ors found that a strong negative association exists between loan default and high market interest r

ate introduced by Bangladesh government. (Ziaul Hoque, Mohammad, Zakir Hossain,

Mohammad, 2008,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Chapter-Three: Overview of Agrani Bank

Limited & Conceptual Framework of NPL

Limited & Conceptual Framework of NPL

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

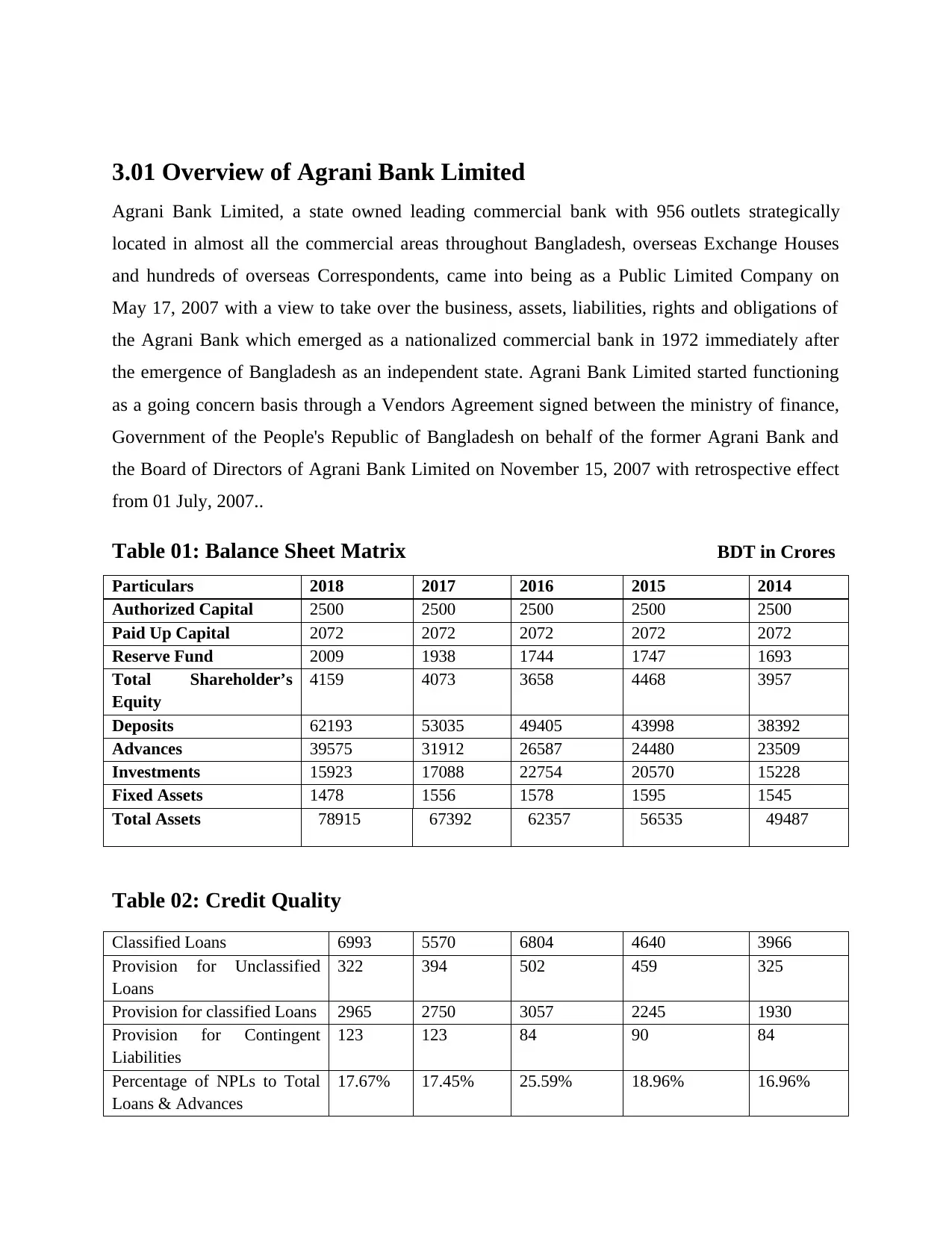

3.01 Overview of Agrani Bank Limited

Agrani Bank Limited, a state owned leading commercial bank with 956 outlets strategically

located in almost all the commercial areas throughout Bangladesh, overseas Exchange Houses

and hundreds of overseas Correspondents, came into being as a Public Limited Company on

May 17, 2007 with a view to take over the business, assets, liabilities, rights and obligations of

the Agrani Bank which emerged as a nationalized commercial bank in 1972 immediately after

the emergence of Bangladesh as an independent state. Agrani Bank Limited started functioning

as a going concern basis through a Vendors Agreement signed between the ministry of finance,

Government of the People's Republic of Bangladesh on behalf of the former Agrani Bank and

the Board of Directors of Agrani Bank Limited on November 15, 2007 with retrospective effect

from 01 July, 2007..

Table 01: Balance Sheet Matrix BDT in Crores

Particulars 2018 2017 2016 2015 2014

Authorized Capital 2500 2500 2500 2500 2500

Paid Up Capital 2072 2072 2072 2072 2072

Reserve Fund 2009 1938 1744 1747 1693

Total Shareholder’s

Equity

4159 4073 3658 4468 3957

Deposits 62193 53035 49405 43998 38392

Advances 39575 31912 26587 24480 23509

Investments 15923 17088 22754 20570 15228

Fixed Assets 1478 1556 1578 1595 1545

Total Assets 78915 67392 62357 56535 49487

Table 02: Credit Quality

Classified Loans 6993 5570 6804 4640 3966

Provision for Unclassified

Loans

322 394 502 459 325

Provision for classified Loans 2965 2750 3057 2245 1930

Provision for Contingent

Liabilities

123 123 84 90 84

Percentage of NPLs to Total

Loans & Advances

17.67% 17.45% 25.59% 18.96% 16.96%

Agrani Bank Limited, a state owned leading commercial bank with 956 outlets strategically

located in almost all the commercial areas throughout Bangladesh, overseas Exchange Houses

and hundreds of overseas Correspondents, came into being as a Public Limited Company on

May 17, 2007 with a view to take over the business, assets, liabilities, rights and obligations of

the Agrani Bank which emerged as a nationalized commercial bank in 1972 immediately after

the emergence of Bangladesh as an independent state. Agrani Bank Limited started functioning

as a going concern basis through a Vendors Agreement signed between the ministry of finance,

Government of the People's Republic of Bangladesh on behalf of the former Agrani Bank and

the Board of Directors of Agrani Bank Limited on November 15, 2007 with retrospective effect

from 01 July, 2007..

Table 01: Balance Sheet Matrix BDT in Crores

Particulars 2018 2017 2016 2015 2014

Authorized Capital 2500 2500 2500 2500 2500

Paid Up Capital 2072 2072 2072 2072 2072

Reserve Fund 2009 1938 1744 1747 1693

Total Shareholder’s

Equity

4159 4073 3658 4468 3957

Deposits 62193 53035 49405 43998 38392

Advances 39575 31912 26587 24480 23509

Investments 15923 17088 22754 20570 15228

Fixed Assets 1478 1556 1578 1595 1545

Total Assets 78915 67392 62357 56535 49487

Table 02: Credit Quality

Classified Loans 6993 5570 6804 4640 3966

Provision for Unclassified

Loans

322 394 502 459 325

Provision for classified Loans 2965 2750 3057 2245 1930

Provision for Contingent

Liabilities

123 123 84 90 84

Percentage of NPLs to Total

Loans & Advances

17.67% 17.45% 25.59% 18.96% 16.96%

3.02 Conceptual Framework

3.2.01 Non-Performing Loans (NPLs)

Nonperforming loans (NPLs) were widely used by lending institutions as a measure of asset

quality,and are frequently associated with both developed and developing world failures and

financial crises.Banks need a ranking and classification system for loans to facilitate credit

monitoring and control in theirlending portfolios.The loan portfolio of a bank can be divided

into five major groups, namely, in order to pass, special note, substandard, doubtful and loss.

Macroeconomic and structural factors influence NPLs which are demonstrated by empirical

studies. One of the common macro-economic factors are GDP growth, inflation and interest

rates, while size and lending policy are known as micro-economic variables (Greenidge and

Grosvenor, 2010).

“Nonperforming loans (“NPLs”) refer to those financial assets from which banks

no longer receive interest and/or installment payments as scheduled. They are

known as non-performing because the loan ceases to “perform” or generate

income for the bank

--David Woo

3.2.02 Categories of Loans and Advances

According to the master Circular: Loan classification and provisioning (BRPD Circular No. 14)

loans and advances of commercial banks in Bangladesh are grouped into four (4) categories for

the purpose of classification these are (Bangladesh Bank, 2012), -

a) Continuous Loan: A continuous or revolving loan is a loan, where you can withdraw the loan

amount or agreed amount in one go, or in parts. Examples are- Cash Credit, Overdraft, etc.

b) Demand Loan: The loans when the lender demands the money, the borrower must pay. Such

as: Forced LIM, PAD, etc.

3.2.01 Non-Performing Loans (NPLs)

Nonperforming loans (NPLs) were widely used by lending institutions as a measure of asset

quality,and are frequently associated with both developed and developing world failures and

financial crises.Banks need a ranking and classification system for loans to facilitate credit

monitoring and control in theirlending portfolios.The loan portfolio of a bank can be divided

into five major groups, namely, in order to pass, special note, substandard, doubtful and loss.

Macroeconomic and structural factors influence NPLs which are demonstrated by empirical

studies. One of the common macro-economic factors are GDP growth, inflation and interest

rates, while size and lending policy are known as micro-economic variables (Greenidge and

Grosvenor, 2010).

“Nonperforming loans (“NPLs”) refer to those financial assets from which banks

no longer receive interest and/or installment payments as scheduled. They are

known as non-performing because the loan ceases to “perform” or generate

income for the bank

--David Woo

3.2.02 Categories of Loans and Advances

According to the master Circular: Loan classification and provisioning (BRPD Circular No. 14)

loans and advances of commercial banks in Bangladesh are grouped into four (4) categories for

the purpose of classification these are (Bangladesh Bank, 2012), -

a) Continuous Loan: A continuous or revolving loan is a loan, where you can withdraw the loan

amount or agreed amount in one go, or in parts. Examples are- Cash Credit, Overdraft, etc.

b) Demand Loan: The loans when the lender demands the money, the borrower must pay. Such

as: Forced LIM, PAD, etc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 43

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.