Financial Analysis Report: Investment Appraisal using NPV and IRR

VerifiedAdded on 2023/06/18

|11

|2457

|140

Report

AI Summary

This report provides a financial analysis focused on investment appraisal techniques, specifically the Net Present Value (NPV) and Internal Rate of Return (IRR) methods. It begins by calculating the net present value of a company, detailing cash inflow calculations for the years 2021-2025, considering variable and fixed costs, tax implications, and discounted rates to determine the present value of cash inflow and the overall net present value. The report emphasizes the significance of NPV in evaluating investment projects and incorporating the time value of money. Furthermore, it estimates the Internal Rate of Return, highlighting its role in identifying beneficial projects, while also cautioning about potential complexities and the importance of accurate initial investment data. The analysis contrasts NPV and IRR, suggesting NPV as a simpler and more direct technique for investment decision-making. The report concludes that investment decision-making is crucial for business operations, with NPV and IRR being primary techniques to aid in this process, while reiterating the importance of considering all factors before making a final decision. Desklib provides various study tools and solved assignments for students.

FINANCIAL ANALYSIS

(REPORT)

(REPORT)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Estimate net present value of company.......................................................................................3

(b) Estimated Internal Rate of Return.........................................................................................5

(C) Interpretation of result..........................................................................................................7

Comparison between the net present value and internal rate if retrh technqiue.........................8

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Estimate net present value of company.......................................................................................3

(b) Estimated Internal Rate of Return.........................................................................................5

(C) Interpretation of result..........................................................................................................7

Comparison between the net present value and internal rate if retrh technqiue.........................8

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION

Investment appraisal is a defined as a technique that involve analysing the various

investment options that empower the company to address the investment in the best way possible

(Dhavale and Sarkis, 2018). This is a practice that is about to evaluate and interpret the particular

investment choice of the business entity. This is all about analysing the investment of the

business entity so that most appropriate investment decision company can take that can also

support the capital maximisation policy of the business entity. This project would discuss the

different investment appraisal techniques that can support the business venture for taking the

most suitable investment decision-making. Henceforth, report will emphasis over the net present

value technique of investment decision-making. Furthermore, project would emphasis over the

internal rate of return technique of investment appraisal practice. IN this project both the

techniques will be discussed and evaluation would be done in regard to the most suitable

technique available for investment appraisal practice.

MAIN BODY

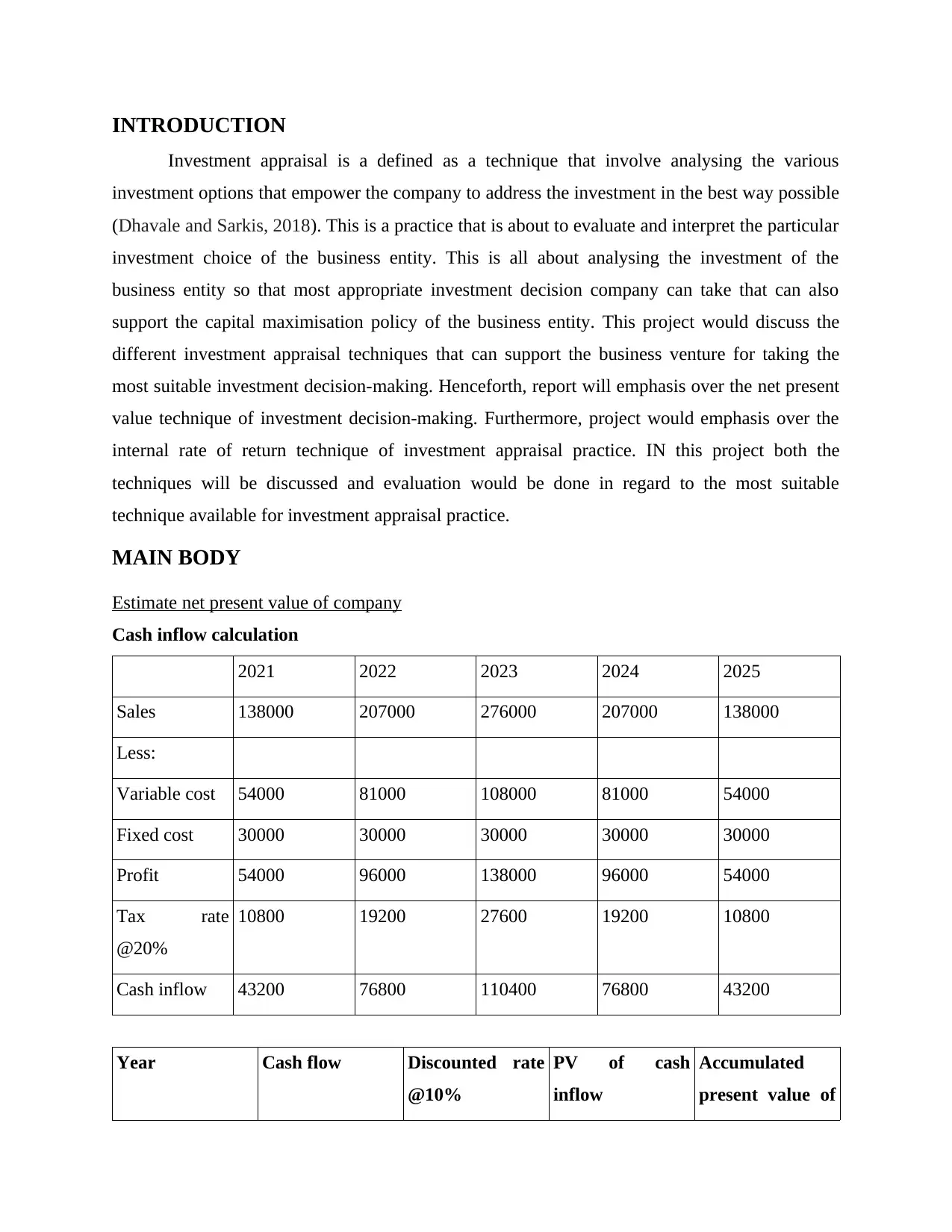

Estimate net present value of company

Cash inflow calculation

2021 2022 2023 2024 2025

Sales 138000 207000 276000 207000 138000

Less:

Variable cost 54000 81000 108000 81000 54000

Fixed cost 30000 30000 30000 30000 30000

Profit 54000 96000 138000 96000 54000

Tax rate

@20%

10800 19200 27600 19200 10800

Cash inflow 43200 76800 110400 76800 43200

Year Cash flow Discounted rate

@10%

PV of cash

inflow

Accumulated

present value of

Investment appraisal is a defined as a technique that involve analysing the various

investment options that empower the company to address the investment in the best way possible

(Dhavale and Sarkis, 2018). This is a practice that is about to evaluate and interpret the particular

investment choice of the business entity. This is all about analysing the investment of the

business entity so that most appropriate investment decision company can take that can also

support the capital maximisation policy of the business entity. This project would discuss the

different investment appraisal techniques that can support the business venture for taking the

most suitable investment decision-making. Henceforth, report will emphasis over the net present

value technique of investment decision-making. Furthermore, project would emphasis over the

internal rate of return technique of investment appraisal practice. IN this project both the

techniques will be discussed and evaluation would be done in regard to the most suitable

technique available for investment appraisal practice.

MAIN BODY

Estimate net present value of company

Cash inflow calculation

2021 2022 2023 2024 2025

Sales 138000 207000 276000 207000 138000

Less:

Variable cost 54000 81000 108000 81000 54000

Fixed cost 30000 30000 30000 30000 30000

Profit 54000 96000 138000 96000 54000

Tax rate

@20%

10800 19200 27600 19200 10800

Cash inflow 43200 76800 110400 76800 43200

Year Cash flow Discounted rate

@10%

PV of cash

inflow

Accumulated

present value of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

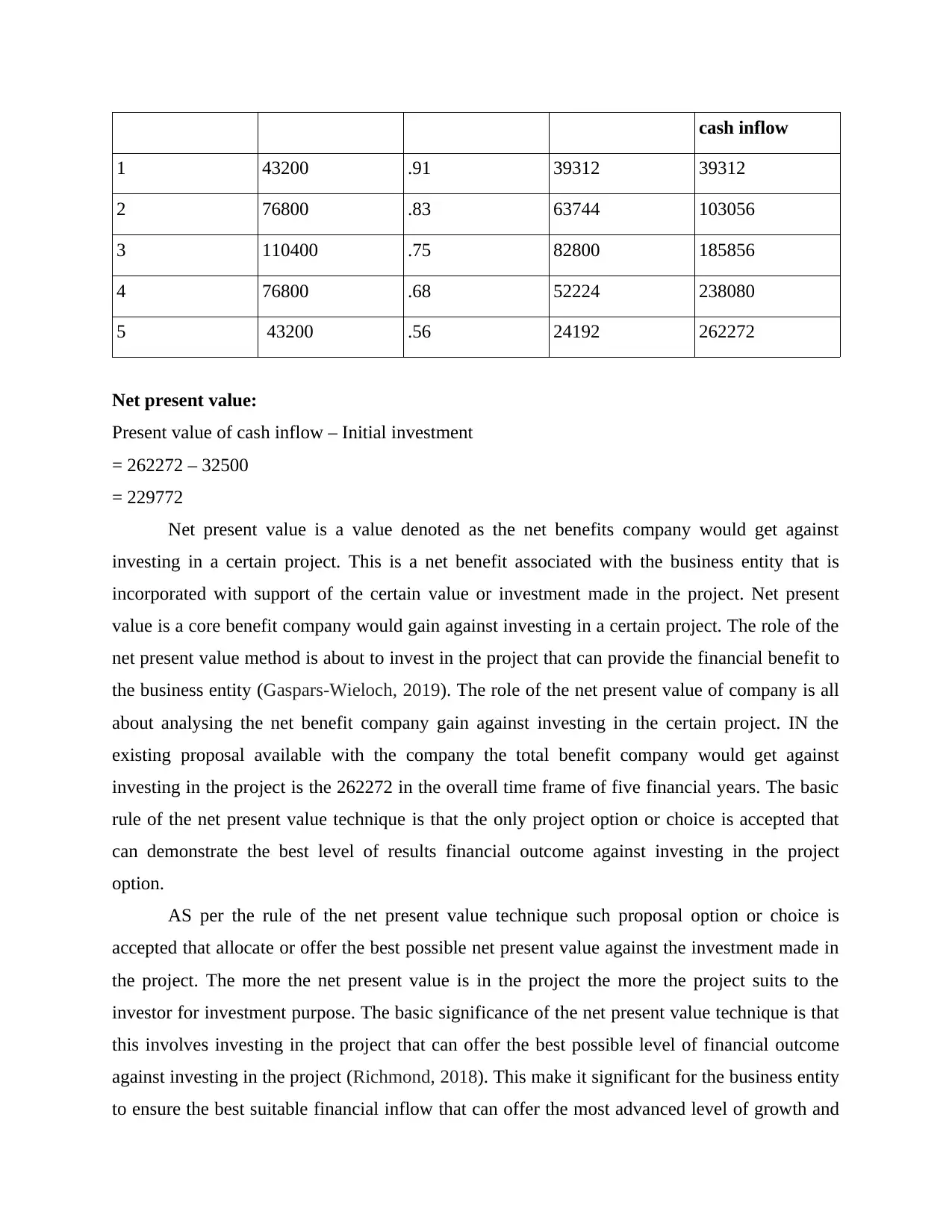

cash inflow

1 43200 .91 39312 39312

2 76800 .83 63744 103056

3 110400 .75 82800 185856

4 76800 .68 52224 238080

5 43200 .56 24192 262272

Net present value:

Present value of cash inflow – Initial investment

= 262272 – 32500

= 229772

Net present value is a value denoted as the net benefits company would get against

investing in a certain project. This is a net benefit associated with the business entity that is

incorporated with support of the certain value or investment made in the project. Net present

value is a core benefit company would gain against investing in a certain project. The role of the

net present value method is about to invest in the project that can provide the financial benefit to

the business entity (Gaspars-Wieloch, 2019). The role of the net present value of company is all

about analysing the net benefit company gain against investing in the certain project. IN the

existing proposal available with the company the total benefit company would get against

investing in the project is the 262272 in the overall time frame of five financial years. The basic

rule of the net present value technique is that the only project option or choice is accepted that

can demonstrate the best level of results financial outcome against investing in the project

option.

AS per the rule of the net present value technique such proposal option or choice is

accepted that allocate or offer the best possible net present value against the investment made in

the project. The more the net present value is in the project the more the project suits to the

investor for investment purpose. The basic significance of the net present value technique is that

this involves investing in the project that can offer the best possible level of financial outcome

against investing in the project (Richmond, 2018). This make it significant for the business entity

to ensure the best suitable financial inflow that can offer the most advanced level of growth and

1 43200 .91 39312 39312

2 76800 .83 63744 103056

3 110400 .75 82800 185856

4 76800 .68 52224 238080

5 43200 .56 24192 262272

Net present value:

Present value of cash inflow – Initial investment

= 262272 – 32500

= 229772

Net present value is a value denoted as the net benefits company would get against

investing in a certain project. This is a net benefit associated with the business entity that is

incorporated with support of the certain value or investment made in the project. Net present

value is a core benefit company would gain against investing in a certain project. The role of the

net present value method is about to invest in the project that can provide the financial benefit to

the business entity (Gaspars-Wieloch, 2019). The role of the net present value of company is all

about analysing the net benefit company gain against investing in the certain project. IN the

existing proposal available with the company the total benefit company would get against

investing in the project is the 262272 in the overall time frame of five financial years. The basic

rule of the net present value technique is that the only project option or choice is accepted that

can demonstrate the best level of results financial outcome against investing in the project

option.

AS per the rule of the net present value technique such proposal option or choice is

accepted that allocate or offer the best possible net present value against the investment made in

the project. The more the net present value is in the project the more the project suits to the

investor for investment purpose. The basic significance of the net present value technique is that

this involves investing in the project that can offer the best possible level of financial outcome

against investing in the project (Richmond, 2018). This make it significant for the business entity

to ensure the best suitable financial inflow that can offer the most advanced level of growth and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

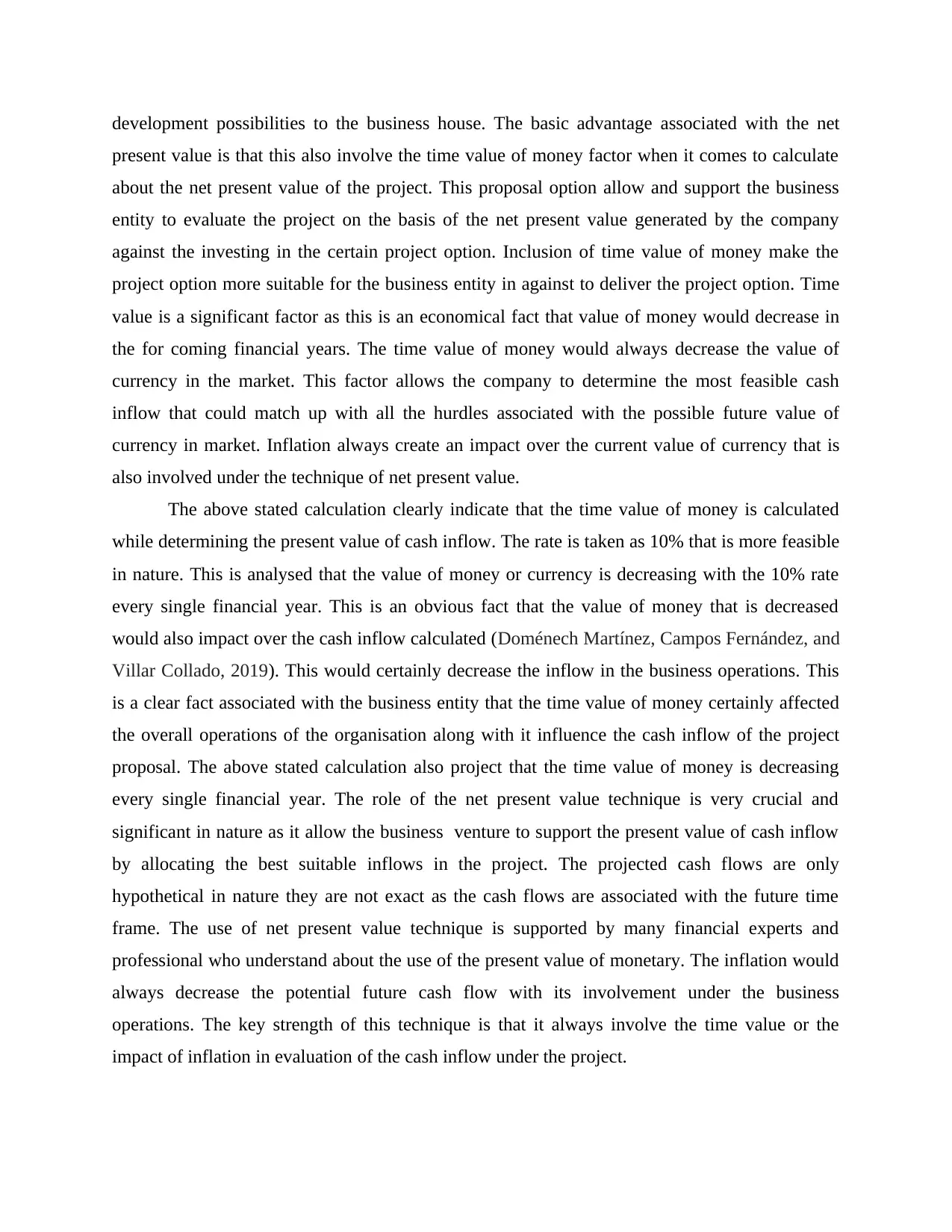

development possibilities to the business house. The basic advantage associated with the net

present value is that this also involve the time value of money factor when it comes to calculate

about the net present value of the project. This proposal option allow and support the business

entity to evaluate the project on the basis of the net present value generated by the company

against the investing in the certain project option. Inclusion of time value of money make the

project option more suitable for the business entity in against to deliver the project option. Time

value is a significant factor as this is an economical fact that value of money would decrease in

the for coming financial years. The time value of money would always decrease the value of

currency in the market. This factor allows the company to determine the most feasible cash

inflow that could match up with all the hurdles associated with the possible future value of

currency in market. Inflation always create an impact over the current value of currency that is

also involved under the technique of net present value.

The above stated calculation clearly indicate that the time value of money is calculated

while determining the present value of cash inflow. The rate is taken as 10% that is more feasible

in nature. This is analysed that the value of money or currency is decreasing with the 10% rate

every single financial year. This is an obvious fact that the value of money that is decreased

would also impact over the cash inflow calculated (Doménech Martínez, Campos Fernández, and

Villar Collado, 2019). This would certainly decrease the inflow in the business operations. This

is a clear fact associated with the business entity that the time value of money certainly affected

the overall operations of the organisation along with it influence the cash inflow of the project

proposal. The above stated calculation also project that the time value of money is decreasing

every single financial year. The role of the net present value technique is very crucial and

significant in nature as it allow the business venture to support the present value of cash inflow

by allocating the best suitable inflows in the project. The projected cash flows are only

hypothetical in nature they are not exact as the cash flows are associated with the future time

frame. The use of net present value technique is supported by many financial experts and

professional who understand about the use of the present value of monetary. The inflation would

always decrease the potential future cash flow with its involvement under the business

operations. The key strength of this technique is that it always involve the time value or the

impact of inflation in evaluation of the cash inflow under the project.

present value is that this also involve the time value of money factor when it comes to calculate

about the net present value of the project. This proposal option allow and support the business

entity to evaluate the project on the basis of the net present value generated by the company

against the investing in the certain project option. Inclusion of time value of money make the

project option more suitable for the business entity in against to deliver the project option. Time

value is a significant factor as this is an economical fact that value of money would decrease in

the for coming financial years. The time value of money would always decrease the value of

currency in the market. This factor allows the company to determine the most feasible cash

inflow that could match up with all the hurdles associated with the possible future value of

currency in market. Inflation always create an impact over the current value of currency that is

also involved under the technique of net present value.

The above stated calculation clearly indicate that the time value of money is calculated

while determining the present value of cash inflow. The rate is taken as 10% that is more feasible

in nature. This is analysed that the value of money or currency is decreasing with the 10% rate

every single financial year. This is an obvious fact that the value of money that is decreased

would also impact over the cash inflow calculated (Doménech Martínez, Campos Fernández, and

Villar Collado, 2019). This would certainly decrease the inflow in the business operations. This

is a clear fact associated with the business entity that the time value of money certainly affected

the overall operations of the organisation along with it influence the cash inflow of the project

proposal. The above stated calculation also project that the time value of money is decreasing

every single financial year. The role of the net present value technique is very crucial and

significant in nature as it allow the business venture to support the present value of cash inflow

by allocating the best suitable inflows in the project. The projected cash flows are only

hypothetical in nature they are not exact as the cash flows are associated with the future time

frame. The use of net present value technique is supported by many financial experts and

professional who understand about the use of the present value of monetary. The inflation would

always decrease the potential future cash flow with its involvement under the business

operations. The key strength of this technique is that it always involve the time value or the

impact of inflation in evaluation of the cash inflow under the project.

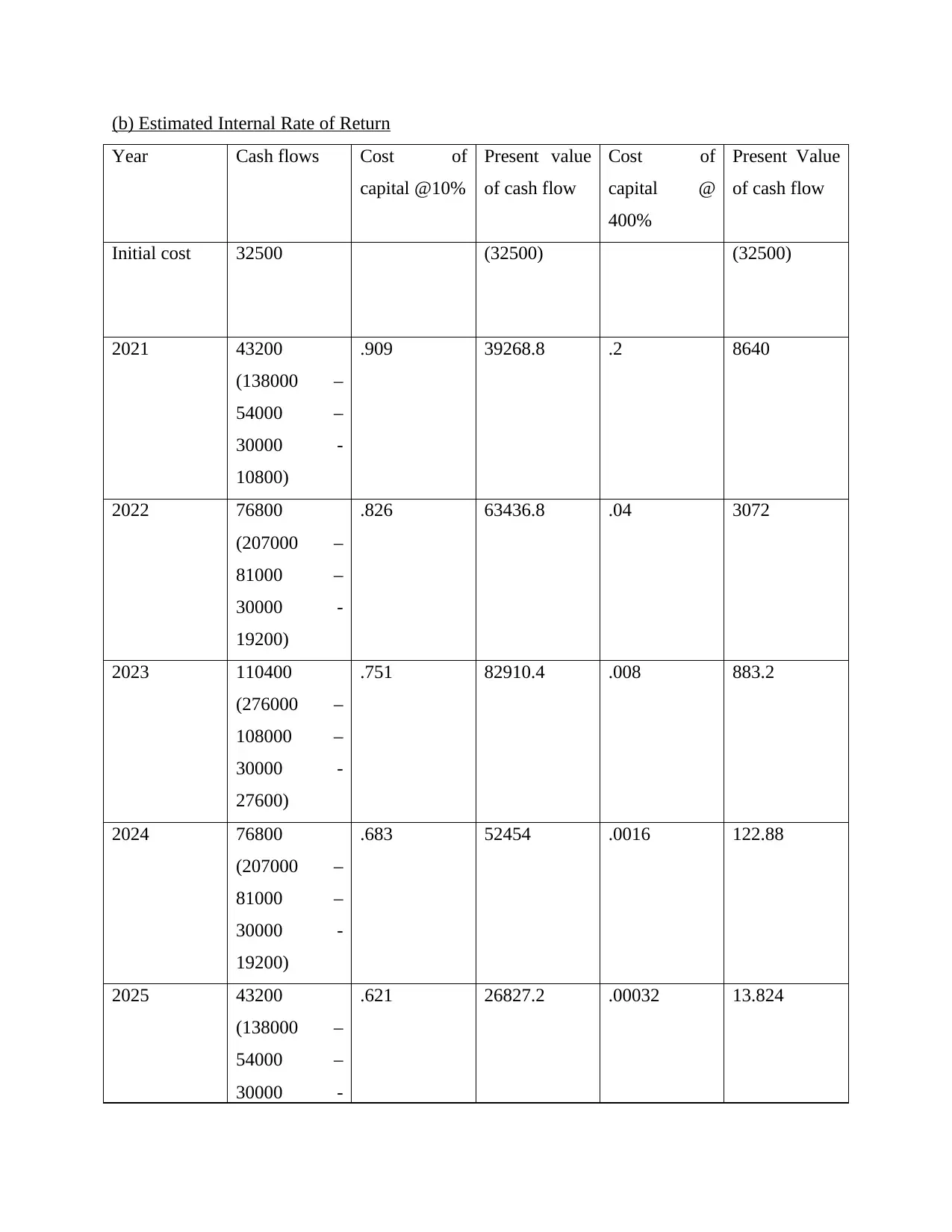

(b) Estimated Internal Rate of Return

Year Cash flows Cost of

capital @10%

Present value

of cash flow

Cost of

capital @

400%

Present Value

of cash flow

Initial cost 32500 (32500) (32500)

2021 43200

(138000 –

54000 –

30000 -

10800)

.909 39268.8 .2 8640

2022 76800

(207000 –

81000 –

30000 -

19200)

.826 63436.8 .04 3072

2023 110400

(276000 –

108000 –

30000 -

27600)

.751 82910.4 .008 883.2

2024 76800

(207000 –

81000 –

30000 -

19200)

.683 52454 .0016 122.88

2025 43200

(138000 –

54000 –

30000 -

.621 26827.2 .00032 13.824

Year Cash flows Cost of

capital @10%

Present value

of cash flow

Cost of

capital @

400%

Present Value

of cash flow

Initial cost 32500 (32500) (32500)

2021 43200

(138000 –

54000 –

30000 -

10800)

.909 39268.8 .2 8640

2022 76800

(207000 –

81000 –

30000 -

19200)

.826 63436.8 .04 3072

2023 110400

(276000 –

108000 –

30000 -

27600)

.751 82910.4 .008 883.2

2024 76800

(207000 –

81000 –

30000 -

19200)

.683 52454 .0016 122.88

2025 43200

(138000 –

54000 –

30000 -

.621 26827.2 .00032 13.824

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10800)

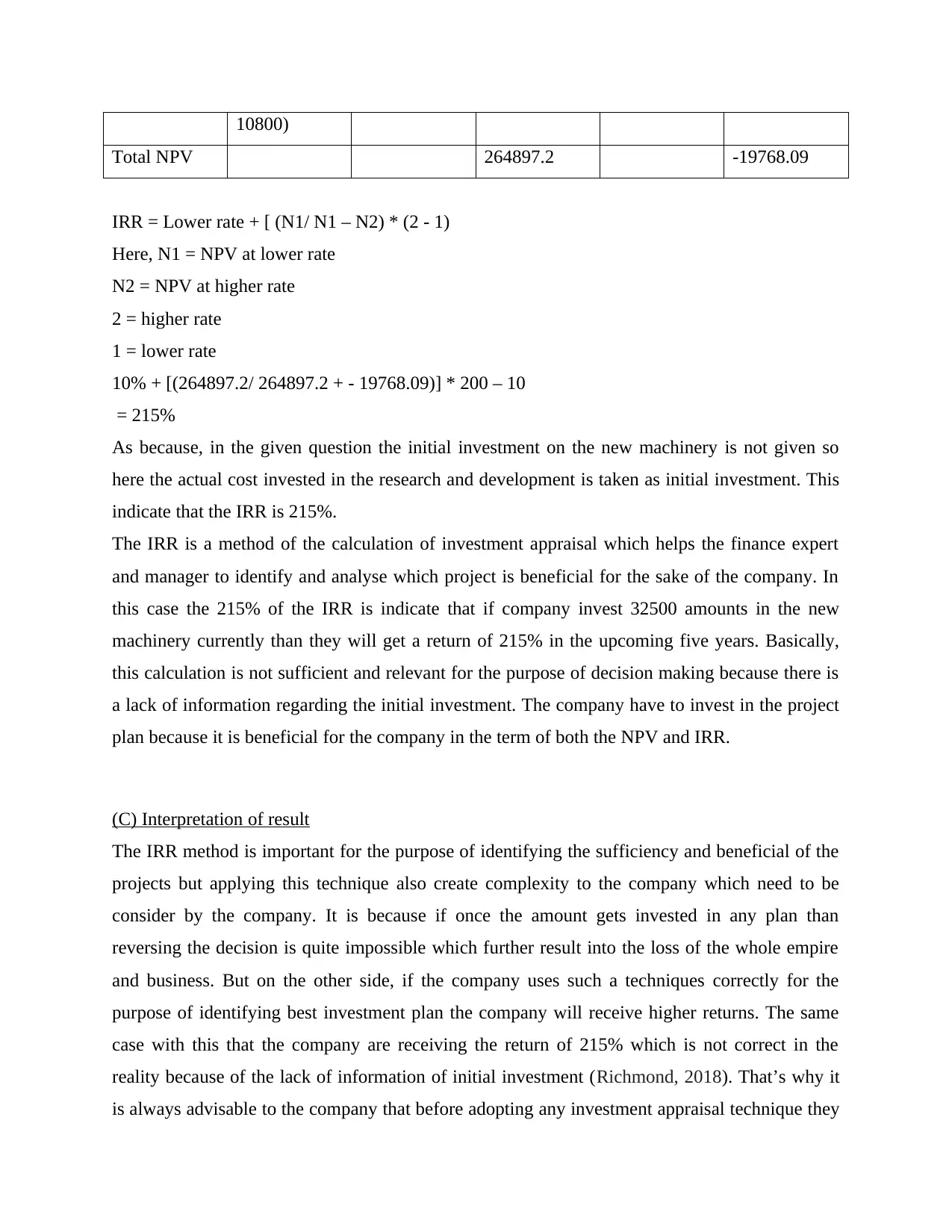

Total NPV 264897.2 -19768.09

IRR = Lower rate + [ (N1/ N1 – N2) * (2 - 1)

Here, N1 = NPV at lower rate

N2 = NPV at higher rate

2 = higher rate

1 = lower rate

10% + [(264897.2/ 264897.2 + - 19768.09)] * 200 – 10

= 215%

As because, in the given question the initial investment on the new machinery is not given so

here the actual cost invested in the research and development is taken as initial investment. This

indicate that the IRR is 215%.

The IRR is a method of the calculation of investment appraisal which helps the finance expert

and manager to identify and analyse which project is beneficial for the sake of the company. In

this case the 215% of the IRR is indicate that if company invest 32500 amounts in the new

machinery currently than they will get a return of 215% in the upcoming five years. Basically,

this calculation is not sufficient and relevant for the purpose of decision making because there is

a lack of information regarding the initial investment. The company have to invest in the project

plan because it is beneficial for the company in the term of both the NPV and IRR.

(C) Interpretation of result

The IRR method is important for the purpose of identifying the sufficiency and beneficial of the

projects but applying this technique also create complexity to the company which need to be

consider by the company. It is because if once the amount gets invested in any plan than

reversing the decision is quite impossible which further result into the loss of the whole empire

and business. But on the other side, if the company uses such a techniques correctly for the

purpose of identifying best investment plan the company will receive higher returns. The same

case with this that the company are receiving the return of 215% which is not correct in the

reality because of the lack of information of initial investment (Richmond, 2018). That’s why it

is always advisable to the company that before adopting any investment appraisal technique they

Total NPV 264897.2 -19768.09

IRR = Lower rate + [ (N1/ N1 – N2) * (2 - 1)

Here, N1 = NPV at lower rate

N2 = NPV at higher rate

2 = higher rate

1 = lower rate

10% + [(264897.2/ 264897.2 + - 19768.09)] * 200 – 10

= 215%

As because, in the given question the initial investment on the new machinery is not given so

here the actual cost invested in the research and development is taken as initial investment. This

indicate that the IRR is 215%.

The IRR is a method of the calculation of investment appraisal which helps the finance expert

and manager to identify and analyse which project is beneficial for the sake of the company. In

this case the 215% of the IRR is indicate that if company invest 32500 amounts in the new

machinery currently than they will get a return of 215% in the upcoming five years. Basically,

this calculation is not sufficient and relevant for the purpose of decision making because there is

a lack of information regarding the initial investment. The company have to invest in the project

plan because it is beneficial for the company in the term of both the NPV and IRR.

(C) Interpretation of result

The IRR method is important for the purpose of identifying the sufficiency and beneficial of the

projects but applying this technique also create complexity to the company which need to be

consider by the company. It is because if once the amount gets invested in any plan than

reversing the decision is quite impossible which further result into the loss of the whole empire

and business. But on the other side, if the company uses such a techniques correctly for the

purpose of identifying best investment plan the company will receive higher returns. The same

case with this that the company are receiving the return of 215% which is not correct in the

reality because of the lack of information of initial investment (Richmond, 2018). That’s why it

is always advisable to the company that before adopting any investment appraisal technique they

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

must know about the initial cost of the project because without such information analysing the

correct result is not possible. The positive NPV of the project also indicate that the company

must invest in this project but that result is depending upon the R&D cost of machinery rather

than initial investment information.

Comparison between the net present value and internal rate if retrh technqiue

The investment appraisal techniques are immensely segregated into different types. The

net present value technique is all about analysing the actual value in amount company would

entertain against the investment made in a certain project. This is considered as the net financial

benefit company would gain against the investment entertained by the project. This technique

look more professional and feasible in nature when it comes to analysing the investment in the

project. On the other hand the internal rate of return is a technique that is about to analysis the

expected rate of return company would gain against investing in the project. This is a rate of

return against the investment in the project (Peymankar and Ranjbar, 2019). The basic different

between the internal rate of return technique and the net present value method is that in one

method the benefit is denoted in overall value and in one technique the rate is identified that can

denote the total benefit company could gain against the investment made in the project.

The critical assessment of both the techniques denote that the net present value method is

more simple technique in nature when it comes to analysis of the investment decision making of

the project. The role of the net present value method is to state the investor about the actual

outcome and benefit to the investor against making the investment decision making. This is

about to state the best possible level of outflow company would entertain against making the

investment decision-making (Mellichamp, 2017). ON the other hand internal rate of return

technique state only about the percentage of outcome company would gain against the

investment made in the project. Both the technique has its own significance but this is obvious

that many times internal rate of return technique mislead to the decision-making process of the

investor as it denote the rate. Whereas, the net present value method indicate about the total

expected outcome against the investment made in the project. Both the technique has a different

projection but net present value is more feasible in nature as compare to the internal rate of reyrb

technique when it comes to making the investment decision making.

correct result is not possible. The positive NPV of the project also indicate that the company

must invest in this project but that result is depending upon the R&D cost of machinery rather

than initial investment information.

Comparison between the net present value and internal rate if retrh technqiue

The investment appraisal techniques are immensely segregated into different types. The

net present value technique is all about analysing the actual value in amount company would

entertain against the investment made in a certain project. This is considered as the net financial

benefit company would gain against the investment entertained by the project. This technique

look more professional and feasible in nature when it comes to analysing the investment in the

project. On the other hand the internal rate of return is a technique that is about to analysis the

expected rate of return company would gain against investing in the project. This is a rate of

return against the investment in the project (Peymankar and Ranjbar, 2019). The basic different

between the internal rate of return technique and the net present value method is that in one

method the benefit is denoted in overall value and in one technique the rate is identified that can

denote the total benefit company could gain against the investment made in the project.

The critical assessment of both the techniques denote that the net present value method is

more simple technique in nature when it comes to analysis of the investment decision making of

the project. The role of the net present value method is to state the investor about the actual

outcome and benefit to the investor against making the investment decision making. This is

about to state the best possible level of outflow company would entertain against making the

investment decision-making (Mellichamp, 2017). ON the other hand internal rate of return

technique state only about the percentage of outcome company would gain against the

investment made in the project. Both the technique has its own significance but this is obvious

that many times internal rate of return technique mislead to the decision-making process of the

investor as it denote the rate. Whereas, the net present value method indicate about the total

expected outcome against the investment made in the project. Both the technique has a different

projection but net present value is more feasible in nature as compare to the internal rate of reyrb

technique when it comes to making the investment decision making.

CONCLUSION

The investment decision making is about the process that involve making the best level of

investment decision-making for the business operation. The technique that allow the company to

take the investment decision-making involve internal rate of return technique and the net present

value technique on a priority basis. ON the basis of the comparative assessment between both the

technique it is determined that the net present value method is more feasible in nature to take the

investment decision whereas the internal rate of return technique is not like that much effective.

The investment decision making is about the process that involve making the best level of

investment decision-making for the business operation. The technique that allow the company to

take the investment decision-making involve internal rate of return technique and the net present

value technique on a priority basis. ON the basis of the comparative assessment between both the

technique it is determined that the net present value method is more feasible in nature to take the

investment decision whereas the internal rate of return technique is not like that much effective.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journal

Dhavale, D. G. and Sarkis, J., 2018. Stochastic internal rate of return on investments in

sustainable assets generating carbon credits. Computers & Operations Research, 89.

pp.324-336.

Doménech Martínez, S., Campos Fernández, F. A. and Villar Collado, J., 2019. Generation

expansion planning based on positive net present value.

Gaspars-Wieloch, H., 2019. Project net present value estimation under uncertainty. Central

European Journal of Operations Research, 27(1). pp.179-197.

Kulakov, N. and Blaset, A., 2020. Rehabilitation of the Internal Rate of Return. Available at

SSRN 3593173.

Mellichamp, D .A., 2017. Internal rate of return: Good and bad features, and a new way of

interpreting the historic measure. Computers & Chemical Engineering, 106. pp.396-

406.

Negrete, G .L., 2020. A review of:“THE MODIFIED INTERNAL RATE OF RETURN AND

INVESTMENT CRITERION”, A REPLY.

Peymankar, M. and Ranjbar, M., 2019, June. Net present value maximization in project

scheduling with an external resource. In Workshop on Models and Algorithms for

Planning and Scheduling Problems, MAPSP 2019.

Richmond, A., 2018. Direct net present value open pit optimisation with probabilistic models.

In Advances in applied strategic mine planning (pp. 217-228). Springer, Cham.

Books and Journal

Dhavale, D. G. and Sarkis, J., 2018. Stochastic internal rate of return on investments in

sustainable assets generating carbon credits. Computers & Operations Research, 89.

pp.324-336.

Doménech Martínez, S., Campos Fernández, F. A. and Villar Collado, J., 2019. Generation

expansion planning based on positive net present value.

Gaspars-Wieloch, H., 2019. Project net present value estimation under uncertainty. Central

European Journal of Operations Research, 27(1). pp.179-197.

Kulakov, N. and Blaset, A., 2020. Rehabilitation of the Internal Rate of Return. Available at

SSRN 3593173.

Mellichamp, D .A., 2017. Internal rate of return: Good and bad features, and a new way of

interpreting the historic measure. Computers & Chemical Engineering, 106. pp.396-

406.

Negrete, G .L., 2020. A review of:“THE MODIFIED INTERNAL RATE OF RETURN AND

INVESTMENT CRITERION”, A REPLY.

Peymankar, M. and Ranjbar, M., 2019, June. Net present value maximization in project

scheduling with an external resource. In Workshop on Models and Algorithms for

Planning and Scheduling Problems, MAPSP 2019.

Richmond, A., 2018. Direct net present value open pit optimisation with probabilistic models.

In Advances in applied strategic mine planning (pp. 217-228). Springer, Cham.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.