Financial Management Report: Case Analysis of Nursing Service Plan

VerifiedAdded on 2022/09/29

|17

|4370

|16

Report

AI Summary

This report presents a financial management plan for a nursing service, addressing key areas such as business plan development, potential steps for service improvement, required documents, and service demand analysis. It delves into workload methodology, staff requirements, skill-mix considerations, and the benefits of cost center budgeting. The report explores various budgeting methods, including zero-based budgeting, and provides a sample salaries and wages budget. The introduction outlines the importance of a well-structured business plan in the context of a hospital's general surgical ward. The report also emphasizes assessment, diagnosis, outcome, planning, implementation, and evaluation processes. Furthermore, it discusses the crucial role of documents like healthcare proxy, living will, and HIPAA forms in service delivery. The discussion on staff requirements covers acuity-quality methodology, skill-mix, and the legal framework governing healthcare practices. The conclusion summarizes the importance of financial planning and efficient resource allocation in healthcare management.

Running head: FINANCIAL MANAGEMENT

Financial Management

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL MANAGEMENT

Table of Contents

Introduction......................................................................................................................................2

Potential Steps to Develop Nursing Service....................................................................................2

Documents Required to Measure Service Profile............................................................................3

The demand for the New Service Profile........................................................................................4

Determination of Workload Methodology & Staff Requirement....................................................5

Skill-Mix or Staff Education...........................................................................................................5

Benefits of Cost Center Budget.......................................................................................................6

Budgeting Methods..........................................................................................................................7

Cost Center Expenditure Budget.....................................................................................................8

Sample Salaries and Wages Budget................................................................................................9

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Bibliography..................................................................................................................................15

Page 1

Table of Contents

Introduction......................................................................................................................................2

Potential Steps to Develop Nursing Service....................................................................................2

Documents Required to Measure Service Profile............................................................................3

The demand for the New Service Profile........................................................................................4

Determination of Workload Methodology & Staff Requirement....................................................5

Skill-Mix or Staff Education...........................................................................................................5

Benefits of Cost Center Budget.......................................................................................................6

Budgeting Methods..........................................................................................................................7

Cost Center Expenditure Budget.....................................................................................................8

Sample Salaries and Wages Budget................................................................................................9

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Bibliography..................................................................................................................................15

Page 1

FINANCIAL MANAGEMENT

Introduction

A proper business plan is aimed to be developed in this study as a nurse manager. The business

aims to develop the existing service by following the main business principles such as the patient

need, staff required and the organizational capability. This business plan will help to develop

general surgical ward of the hospital in order to render quality based services to the patients.

Most importantly, a proper budget has been developed through the study so that cost-related

decisions for new services in general surgical ward could be undertaken effectively. Through this

business plan, required steps associated with the nursing service have been elaborated in details.

Thereafter, a short discussion of salaries and wages while formulating a budget is also provided

in order to understand the feasibility of the plan.

Potential Steps to Develop Nursing Service

A nurse manager must formulate some important steps to reform the hospital network as well as

improve the healthcare services. The hospital needs to reform the management team so that the

needs and the requirements of the patients can be met easily. The following steps can help to

develop the business plan in an efficient way. The hospital must focus on the major nursing

processes in order to augment the quality of the healthcare services i.e. assessment, outcome,

diagnosis, implementation, planning, and evaluation (American Nurses Association, 2019).

Step 1: Assessment

The assessment process needs to use adequate machinery and latest technologies in order to find

out the healthcare problems of the patients easily. It helps to provide required help to the patients

who are in utmost need.

Page 2

Introduction

A proper business plan is aimed to be developed in this study as a nurse manager. The business

aims to develop the existing service by following the main business principles such as the patient

need, staff required and the organizational capability. This business plan will help to develop

general surgical ward of the hospital in order to render quality based services to the patients.

Most importantly, a proper budget has been developed through the study so that cost-related

decisions for new services in general surgical ward could be undertaken effectively. Through this

business plan, required steps associated with the nursing service have been elaborated in details.

Thereafter, a short discussion of salaries and wages while formulating a budget is also provided

in order to understand the feasibility of the plan.

Potential Steps to Develop Nursing Service

A nurse manager must formulate some important steps to reform the hospital network as well as

improve the healthcare services. The hospital needs to reform the management team so that the

needs and the requirements of the patients can be met easily. The following steps can help to

develop the business plan in an efficient way. The hospital must focus on the major nursing

processes in order to augment the quality of the healthcare services i.e. assessment, outcome,

diagnosis, implementation, planning, and evaluation (American Nurses Association, 2019).

Step 1: Assessment

The assessment process needs to use adequate machinery and latest technologies in order to find

out the healthcare problems of the patients easily. It helps to provide required help to the patients

who are in utmost need.

Page 2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL MANAGEMENT

Step 2: Diagnosis

Through the diagnosis process, the healthcare team must conduct the required medical tests and

create a proper plan to cure the diseases. The main reason of this step is to find out adequate

diseases and suitable interventions to cope with the same.

Step 3: Outcome

Based on the identified issues, proper diagnosis needs to be conducted so as to deliver services to

the patients and develop their wellbeing. Based on the outcomes, the doctors can improve the

medications of the respective patients.

Step 4: Planning

In the planning phase, each member in the hospital must work collaboratively with the highest

potential to maintain service quality. Furthermore, appropriate interventions can be implemented

if the team has proper knowledge and experience regarding the same. The hospital needs to find

out the ability of the healthcare workers so that their expertise can be properly utilized in the

organization to facilitate change (American Nurses Association, 2019).

Step 5: Implementation

In the implementation phase, a proper training and development process must also be facilitated

for enhancing the capabilities of the healthcare personnel. Besides, proper cost maintenance of

mentioned activities can lead the organization towards success (American Nurses Association,

2019).

Page 3

Step 2: Diagnosis

Through the diagnosis process, the healthcare team must conduct the required medical tests and

create a proper plan to cure the diseases. The main reason of this step is to find out adequate

diseases and suitable interventions to cope with the same.

Step 3: Outcome

Based on the identified issues, proper diagnosis needs to be conducted so as to deliver services to

the patients and develop their wellbeing. Based on the outcomes, the doctors can improve the

medications of the respective patients.

Step 4: Planning

In the planning phase, each member in the hospital must work collaboratively with the highest

potential to maintain service quality. Furthermore, appropriate interventions can be implemented

if the team has proper knowledge and experience regarding the same. The hospital needs to find

out the ability of the healthcare workers so that their expertise can be properly utilized in the

organization to facilitate change (American Nurses Association, 2019).

Step 5: Implementation

In the implementation phase, a proper training and development process must also be facilitated

for enhancing the capabilities of the healthcare personnel. Besides, proper cost maintenance of

mentioned activities can lead the organization towards success (American Nurses Association,

2019).

Page 3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL MANAGEMENT

Step 6: Evaluation

The nurse manager must find out the issues that are visible within the organization so that the

improvement process can be facilitated with the help of an efficient team. Based on the issues

identified and their adverse effects, specific aim and objectives must be developed that can help

the management team to recreate and implement efficient services (AHRQ, 2014).

Documents Required to Measure Service Profile

The hospital needs to consider certain documents during the facilitation of the plan. In the initial

stage, the management team must consider a healthcare proxy document to increase the

feasibility of the services to be provided to the patients (Mauterstock, 2019). Using this

document, the organization can easily understand the needs of the patient’s family. This can

further help the team to provide the required healthcare services according to the requirements of

the patient. Hence, maintenance of transparency can be easily considered through this document.

However, this document is generally applied when the patient is unable to choose the care

process. In the case of a conscious patient, the hospital can use The Living Will document in

order to facilitate the same work. Through this document, the patient can provide his or her

preferences while facilitating the treatment. Besides, The Health Insurance Portability and

Accountability (HIPAA) Form is another document, which restricts the hospital authority to

reveal any kind of information to the patients’ family in any condition. The form is generally

signed by both parties i.e. hospital staff and the patients’ family. It is mainly applicable when the

patient is in critical condition. Moreover, Do Not Resuscitate (DNR) Form is also necessary

when the patient does not like to be revived adequately (Mauterstock, 2019). However, in an

emergency scenario, this form may not be applicable to a certain extent. Furthermore, other

documents such as Documents of Hospital and Health Services, Documents Mix baseline and

Page 4

Step 6: Evaluation

The nurse manager must find out the issues that are visible within the organization so that the

improvement process can be facilitated with the help of an efficient team. Based on the issues

identified and their adverse effects, specific aim and objectives must be developed that can help

the management team to recreate and implement efficient services (AHRQ, 2014).

Documents Required to Measure Service Profile

The hospital needs to consider certain documents during the facilitation of the plan. In the initial

stage, the management team must consider a healthcare proxy document to increase the

feasibility of the services to be provided to the patients (Mauterstock, 2019). Using this

document, the organization can easily understand the needs of the patient’s family. This can

further help the team to provide the required healthcare services according to the requirements of

the patient. Hence, maintenance of transparency can be easily considered through this document.

However, this document is generally applied when the patient is unable to choose the care

process. In the case of a conscious patient, the hospital can use The Living Will document in

order to facilitate the same work. Through this document, the patient can provide his or her

preferences while facilitating the treatment. Besides, The Health Insurance Portability and

Accountability (HIPAA) Form is another document, which restricts the hospital authority to

reveal any kind of information to the patients’ family in any condition. The form is generally

signed by both parties i.e. hospital staff and the patients’ family. It is mainly applicable when the

patient is in critical condition. Moreover, Do Not Resuscitate (DNR) Form is also necessary

when the patient does not like to be revived adequately (Mauterstock, 2019). However, in an

emergency scenario, this form may not be applicable to a certain extent. Furthermore, other

documents such as Documents of Hospital and Health Services, Documents Mix baseline and

Page 4

FINANCIAL MANAGEMENT

patient care documents among others will also consider for this business enhancement in general

surgical ward of the hospital (Queensland, 2016).

The Demand for the New Service Profile

The service delivered by the hospital must comprise of the three main sections i.e., emergency

care for patients, surgical services and inpatient care. The whole hospital must also be divided

into different types of inpatient units in such a way that each section specializes in providing

specific care. They must also include intensive care unit (ICU) where the patients suffering from

serious health problems can be treated as fast as possible such as neurological or cardiac patients

monitored under highly expert team (University of Oxford, 2014). The service profile must also

include the emergency department as well as hospitalization. Furthermore, other services must be

considered by the management as required in general surgical ward. The staff must be able to

take proper care of the patients thereby efficiently coordinating with the other healthcare

professionals so that patients’ health problems can be cured (Gupta & Potthof, 2016). The

service must also be provided within low cost alongside considering a standard model of the care

plan. Besides, the satisfaction level of the patients must also be kept into high consideration so

that the potential of the services provided by the hospital can be highlighted. Additionally, the

services provided to the patients by the hospital must also include proper meals along with the

accommodation or rehabilitation facilities. The hospital could also include the facility of

providing detoxification services after the approval of the management and the family of the

patients (Government of Northwest Territories, n.d.)

Page 5

patient care documents among others will also consider for this business enhancement in general

surgical ward of the hospital (Queensland, 2016).

The Demand for the New Service Profile

The service delivered by the hospital must comprise of the three main sections i.e., emergency

care for patients, surgical services and inpatient care. The whole hospital must also be divided

into different types of inpatient units in such a way that each section specializes in providing

specific care. They must also include intensive care unit (ICU) where the patients suffering from

serious health problems can be treated as fast as possible such as neurological or cardiac patients

monitored under highly expert team (University of Oxford, 2014). The service profile must also

include the emergency department as well as hospitalization. Furthermore, other services must be

considered by the management as required in general surgical ward. The staff must be able to

take proper care of the patients thereby efficiently coordinating with the other healthcare

professionals so that patients’ health problems can be cured (Gupta & Potthof, 2016). The

service must also be provided within low cost alongside considering a standard model of the care

plan. Besides, the satisfaction level of the patients must also be kept into high consideration so

that the potential of the services provided by the hospital can be highlighted. Additionally, the

services provided to the patients by the hospital must also include proper meals along with the

accommodation or rehabilitation facilities. The hospital could also include the facility of

providing detoxification services after the approval of the management and the family of the

patients (Government of Northwest Territories, n.d.)

Page 5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL MANAGEMENT

Determination of Workload Methodology & Staff Requirement

Nurses provide the maximum amount of care for the patients in the hospital; therefore, they are

the vital asset of the healthcare organization. To provide appropriate nurse care, as well as the

services, to the patients, one must put additional efforts besides calculating the ratios. Nowadays,

it is the responsibility of the managers to ensure that the patients are provided with exact along

with reliable care, which is both safe and clinically prescribed (Brown, Donaldson, Bolton &

Aydin, 2010). The staffs hired for the service must ensure knowledgeable and safe practices

while the management focuses on the cost of recruitment. Thus, a strategic approach must be

applied for the allocation of the workload so that the efficiency of the human resources could be

enhanced. The hospital can follow certain approaches for the division of the staff required for the

new services. The process of staffing known as ‘Acuity-quality Method’ can also be taken into

account because it is one of the useful methods for the medical as well as surgical units.

Calculating the data, as per nursing care time, is necessary per day in the surgical ward to

generate positive healthcare outcomes of the patients (Kaur, Vati, & Chhabra, 2010). This

method ensures evidence-based methodology where the hospital can select the staff according to

the numbers of care providers needed along with the type of care that must be provided to every

patient. This method also provides staffing solution with the help of pre-clinical documents

recorded to classify the numbers of patients. Besides, it does not allow any kind of duplicity

especially in terms of data entry and further helps in reducing the complexity of the workload

(Harris Healthcare, 2019).

Skill-Mix or Staff Education

The term ‘skill-mix’ is defined as the mixture of various posts or occupations within an

organization. This includes the combination of various activities or proficiencies that must be

Page 6

Determination of Workload Methodology & Staff Requirement

Nurses provide the maximum amount of care for the patients in the hospital; therefore, they are

the vital asset of the healthcare organization. To provide appropriate nurse care, as well as the

services, to the patients, one must put additional efforts besides calculating the ratios. Nowadays,

it is the responsibility of the managers to ensure that the patients are provided with exact along

with reliable care, which is both safe and clinically prescribed (Brown, Donaldson, Bolton &

Aydin, 2010). The staffs hired for the service must ensure knowledgeable and safe practices

while the management focuses on the cost of recruitment. Thus, a strategic approach must be

applied for the allocation of the workload so that the efficiency of the human resources could be

enhanced. The hospital can follow certain approaches for the division of the staff required for the

new services. The process of staffing known as ‘Acuity-quality Method’ can also be taken into

account because it is one of the useful methods for the medical as well as surgical units.

Calculating the data, as per nursing care time, is necessary per day in the surgical ward to

generate positive healthcare outcomes of the patients (Kaur, Vati, & Chhabra, 2010). This

method ensures evidence-based methodology where the hospital can select the staff according to

the numbers of care providers needed along with the type of care that must be provided to every

patient. This method also provides staffing solution with the help of pre-clinical documents

recorded to classify the numbers of patients. Besides, it does not allow any kind of duplicity

especially in terms of data entry and further helps in reducing the complexity of the workload

(Harris Healthcare, 2019).

Skill-Mix or Staff Education

The term ‘skill-mix’ is defined as the mixture of various posts or occupations within an

organization. This includes the combination of various activities or proficiencies that must be

Page 6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL MANAGEMENT

involved in a particular job role. The organization must be able to optimize the efficiency of the

workforce. Without any defined objective, it is difficult to evaluate the performance of the nurses

(Duffield, Roche, & Merrick, 2006). To be specific, there are various attributes, which must be

focused by the healthcare professionals for availing proper healthcare services in the

organization. These include educational qualification, abilities of the nurses and their behavior

towards patients. All these skills can be considered as important for the healthcare staffs to

perform effectively in the organization. The overall management of the skills also helps the

management in availing flexible and cost-efficient human resources. However, the staff must be

also able to adapt to the proposed changes in all the circumstances. Every staff must put an equal

amount of effort to enhance clinical practices with the help of education and personal

development (Dubois, & Singh, 2009). All the employees must also work according to the legal

procedures provided by the legislation for better performance without any kind of discrimination

such as ‘Health Practitioner Regulation National Law Act 2009’ (The State of Queensland,

2019).

Benefits of Cost Center Budget

The cost center does not focus on the actual profit but does contribute to maintaining the overall

wellbeing of the healthcare organization. Hence, the manager must ensure to provide adequate

financial resources to meet the costs of every unit. Therefore, the focus of the manager lies on

providing the most suitable services along with additional goods to the patients for generating

revenue. Such budgets will be based on the operational objectives that can easily help the

management to estimate the cash received and expenses required for the proper functioning of

the organization. Hence, preparing the cost center budget is highly beneficial for the overall

management to provide a cash flow mechanism where the managers can compare the actual

Page 7

involved in a particular job role. The organization must be able to optimize the efficiency of the

workforce. Without any defined objective, it is difficult to evaluate the performance of the nurses

(Duffield, Roche, & Merrick, 2006). To be specific, there are various attributes, which must be

focused by the healthcare professionals for availing proper healthcare services in the

organization. These include educational qualification, abilities of the nurses and their behavior

towards patients. All these skills can be considered as important for the healthcare staffs to

perform effectively in the organization. The overall management of the skills also helps the

management in availing flexible and cost-efficient human resources. However, the staff must be

also able to adapt to the proposed changes in all the circumstances. Every staff must put an equal

amount of effort to enhance clinical practices with the help of education and personal

development (Dubois, & Singh, 2009). All the employees must also work according to the legal

procedures provided by the legislation for better performance without any kind of discrimination

such as ‘Health Practitioner Regulation National Law Act 2009’ (The State of Queensland,

2019).

Benefits of Cost Center Budget

The cost center does not focus on the actual profit but does contribute to maintaining the overall

wellbeing of the healthcare organization. Hence, the manager must ensure to provide adequate

financial resources to meet the costs of every unit. Therefore, the focus of the manager lies on

providing the most suitable services along with additional goods to the patients for generating

revenue. Such budgets will be based on the operational objectives that can easily help the

management to estimate the cash received and expenses required for the proper functioning of

the organization. Hence, preparing the cost center budget is highly beneficial for the overall

management to provide a cash flow mechanism where the managers can compare the actual

Page 7

FINANCIAL MANAGEMENT

figures with respect to the estimated value. This budget is always helpful in terms of estimating

the overall expense alongside evaluating the necessities for all the activities, which are related to

the cash receipts along with the disbursements. This also provides a standard for the overall

expenses of the organization that must be maintained in order to perform all the related activities

smoothly thereby focusing on all the employees working in the hospital (Nordmeyer, 2019).

Budgeting Methods

The budget of an organization provides a better understanding of the cash flow. There are three

ways of calculating budget, one of them is a flexible budget wherein the values are estimated

based on the current amount and can be adjusted. This method is used where the estimation of

sales is difficult. A zero-based budget is another method, which is based on the outcome

expected by the organization or estimation. This method is also useful for service-level

organizations (AccountingTools, 2019a). The third method is the output-based budget, also

known as outcome-based budgeting wherein the budget is estimated based on funding as well as

the expected results. It is generally used for government budgeting IES (National Center for

Education Statistics, 2004). Among all these methods, the zero-based method can be the most

appropriate one for estimating the budget of the health care services since it determines three

factors namely expenses, the revenue, as well as the profit generated. This will allow the

manager to estimate the budget plan from the zero levels. Each amount of expense is justified

before the calculation of the actual budget. Some of the advantages of using a zero-based budget

are that it helps in resource allocation and cost reduction thereby maintaining its accuracy. It is

also helpful in coordinating between various departments of an organization. This method has

also been beneficial in the elimination of unproductive activities. However, it is one of the

demerits is that it requires huge manpower, which might not be available in every organization.

Page 8

figures with respect to the estimated value. This budget is always helpful in terms of estimating

the overall expense alongside evaluating the necessities for all the activities, which are related to

the cash receipts along with the disbursements. This also provides a standard for the overall

expenses of the organization that must be maintained in order to perform all the related activities

smoothly thereby focusing on all the employees working in the hospital (Nordmeyer, 2019).

Budgeting Methods

The budget of an organization provides a better understanding of the cash flow. There are three

ways of calculating budget, one of them is a flexible budget wherein the values are estimated

based on the current amount and can be adjusted. This method is used where the estimation of

sales is difficult. A zero-based budget is another method, which is based on the outcome

expected by the organization or estimation. This method is also useful for service-level

organizations (AccountingTools, 2019a). The third method is the output-based budget, also

known as outcome-based budgeting wherein the budget is estimated based on funding as well as

the expected results. It is generally used for government budgeting IES (National Center for

Education Statistics, 2004). Among all these methods, the zero-based method can be the most

appropriate one for estimating the budget of the health care services since it determines three

factors namely expenses, the revenue, as well as the profit generated. This will allow the

manager to estimate the budget plan from the zero levels. Each amount of expense is justified

before the calculation of the actual budget. Some of the advantages of using a zero-based budget

are that it helps in resource allocation and cost reduction thereby maintaining its accuracy. It is

also helpful in coordinating between various departments of an organization. This method has

also been beneficial in the elimination of unproductive activities. However, it is one of the

demerits is that it requires huge manpower, which might not be available in every organization.

Page 8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL MANAGEMENT

This implies that the method is time-consuming as well as the mangers must be skilled for

preparing the budget (Cleartax, 2019).

In comparison with the zero-based budgeting, a flexible budget is difficult to calculate and can

be problematic while formulating. The formula related to the fixed cost and variable cost may

take more time. The manager may not be able to add the values before the overall financial

report is completed therefore it may delay the process. The values cannot be compared with the

actual revenues, as they are flexible and are adjusted to make the actual as well as the expected

values similar. Even for companies with less variable cost, the flexible budget will not be able to

show any variation. Flexible budgets are only useful for business purposes where there are more

variables, which can be segregated into fixed and variable costs. It is useful for evaluation

including the performance of an organization. Hence, this can be easy for keeping the budget

updated (AccountingTools, 2019b).

Even the output-based budget makes the process difficult in finding accurate data. The single

budget may be provided with multiple outcomes, which might become complicated in nature.

Even the process itself is very complex, which requires more investment for calculation. This

method is advantageous for identifying cost and highlights the section, which may require higher

investment (Grant Thornton, 2017).

Cost Center Expenditure Budget

The three key areas of expenditure which will be considered in the budget are the cost of

additional supplies, the cost of recruiting new nurse for more patients and salaries for the staffs

(Dredge, 2004). The additional supplies such as the cost of buying new beds will also lead to

buying of food and other medicals tools for a large number of patients. They may vary according

Page 9

This implies that the method is time-consuming as well as the mangers must be skilled for

preparing the budget (Cleartax, 2019).

In comparison with the zero-based budgeting, a flexible budget is difficult to calculate and can

be problematic while formulating. The formula related to the fixed cost and variable cost may

take more time. The manager may not be able to add the values before the overall financial

report is completed therefore it may delay the process. The values cannot be compared with the

actual revenues, as they are flexible and are adjusted to make the actual as well as the expected

values similar. Even for companies with less variable cost, the flexible budget will not be able to

show any variation. Flexible budgets are only useful for business purposes where there are more

variables, which can be segregated into fixed and variable costs. It is useful for evaluation

including the performance of an organization. Hence, this can be easy for keeping the budget

updated (AccountingTools, 2019b).

Even the output-based budget makes the process difficult in finding accurate data. The single

budget may be provided with multiple outcomes, which might become complicated in nature.

Even the process itself is very complex, which requires more investment for calculation. This

method is advantageous for identifying cost and highlights the section, which may require higher

investment (Grant Thornton, 2017).

Cost Center Expenditure Budget

The three key areas of expenditure which will be considered in the budget are the cost of

additional supplies, the cost of recruiting new nurse for more patients and salaries for the staffs

(Dredge, 2004). The additional supplies such as the cost of buying new beds will also lead to

buying of food and other medicals tools for a large number of patients. They may vary according

Page 9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL MANAGEMENT

to the demand that may be high or low as per the number of patients admitted in the hospital. The

recruitment of new nurses will also lead to a rise in expenditure. As the number of beds

increases, the requirement for more number of staff will also rise. The salaries of the staff will

also increase along with their numbers so that quality health care services can be availed.

However, the salary may also increase based on their performance and efficiency. In addition,

other expenses may be incurred during the facilitation of healthcare services.

The cost center budget will be based on the reconstruction of the medical health care system

where the addition of 12 new beds will be done. This addition will provide a change in the

existing budget, where the purchase of the new beds will be included. Staff will also be added,

hence, the salaries or the wages for the nurses as well as for other labors working in the

organization will also change accordingly. Nevertheless, the fixed cost of health care will remain

constant. The addition of the new section will also increase the variable goods required for the

treatment of the patients such as tools for treatment, food for the patients, and more number of

emergency wards for the patients. The cost center budget will also focus on the amount of cash

incurred due to the inflow of patients in the hospital. Such cost will be depending on the type of

treatment patients are receiving along with the inpatient or outpatient in the health centers. This

overall expenditure will act as a budget baseline to provide a comparable report for future

context. The baseline budget will be beneficial in evaluating the current spending so that the

future costs in terms of funding are controlled effectively (Abdo, Eick & Meyers, LLP, 2019).

Page

10

to the demand that may be high or low as per the number of patients admitted in the hospital. The

recruitment of new nurses will also lead to a rise in expenditure. As the number of beds

increases, the requirement for more number of staff will also rise. The salaries of the staff will

also increase along with their numbers so that quality health care services can be availed.

However, the salary may also increase based on their performance and efficiency. In addition,

other expenses may be incurred during the facilitation of healthcare services.

The cost center budget will be based on the reconstruction of the medical health care system

where the addition of 12 new beds will be done. This addition will provide a change in the

existing budget, where the purchase of the new beds will be included. Staff will also be added,

hence, the salaries or the wages for the nurses as well as for other labors working in the

organization will also change accordingly. Nevertheless, the fixed cost of health care will remain

constant. The addition of the new section will also increase the variable goods required for the

treatment of the patients such as tools for treatment, food for the patients, and more number of

emergency wards for the patients. The cost center budget will also focus on the amount of cash

incurred due to the inflow of patients in the hospital. Such cost will be depending on the type of

treatment patients are receiving along with the inpatient or outpatient in the health centers. This

overall expenditure will act as a budget baseline to provide a comparable report for future

context. The baseline budget will be beneficial in evaluating the current spending so that the

future costs in terms of funding are controlled effectively (Abdo, Eick & Meyers, LLP, 2019).

Page

10

FINANCIAL MANAGEMENT

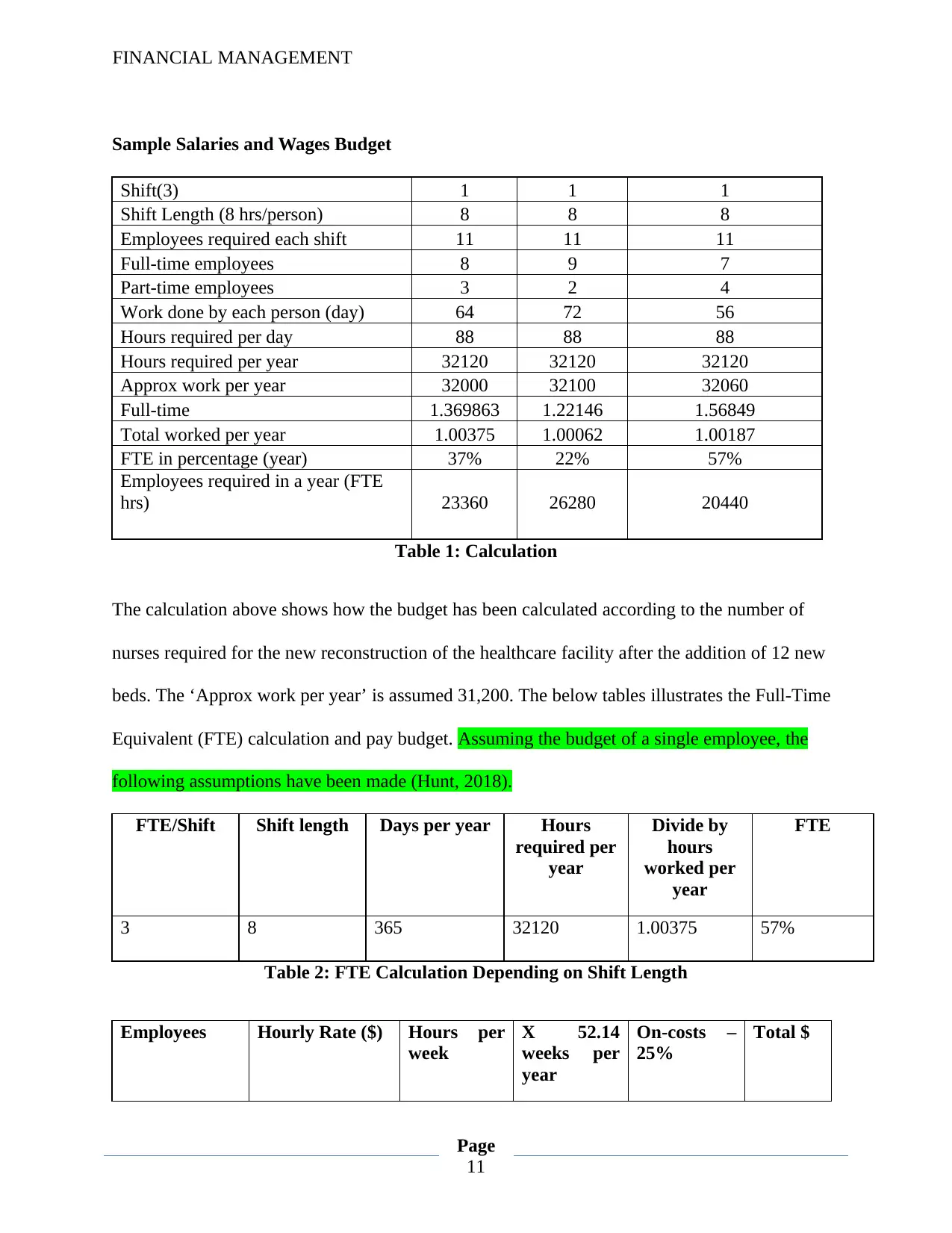

Sample Salaries and Wages Budget

Shift(3) 1 1 1

Shift Length (8 hrs/person) 8 8 8

Employees required each shift 11 11 11

Full-time employees 8 9 7

Part-time employees 3 2 4

Work done by each person (day) 64 72 56

Hours required per day 88 88 88

Hours required per year 32120 32120 32120

Approx work per year 32000 32100 32060

Full-time 1.369863 1.22146 1.56849

Total worked per year 1.00375 1.00062 1.00187

FTE in percentage (year) 37% 22% 57%

Employees required in a year (FTE

hrs) 23360 26280 20440

Table 1: Calculation

The calculation above shows how the budget has been calculated according to the number of

nurses required for the new reconstruction of the healthcare facility after the addition of 12 new

beds. The ‘Approx work per year’ is assumed 31,200. The below tables illustrates the Full-Time

Equivalent (FTE) calculation and pay budget. Assuming the budget of a single employee, the

following assumptions have been made (Hunt, 2018).

FTE/Shift Shift length Days per year Hours

required per

year

Divide by

hours

worked per

year

FTE

3 8 365 32120 1.00375 57%

Table 2: FTE Calculation Depending on Shift Length

Employees Hourly Rate ($) Hours per

week

X 52.14

weeks per

year

On-costs –

25%

Total $

Page

11

Sample Salaries and Wages Budget

Shift(3) 1 1 1

Shift Length (8 hrs/person) 8 8 8

Employees required each shift 11 11 11

Full-time employees 8 9 7

Part-time employees 3 2 4

Work done by each person (day) 64 72 56

Hours required per day 88 88 88

Hours required per year 32120 32120 32120

Approx work per year 32000 32100 32060

Full-time 1.369863 1.22146 1.56849

Total worked per year 1.00375 1.00062 1.00187

FTE in percentage (year) 37% 22% 57%

Employees required in a year (FTE

hrs) 23360 26280 20440

Table 1: Calculation

The calculation above shows how the budget has been calculated according to the number of

nurses required for the new reconstruction of the healthcare facility after the addition of 12 new

beds. The ‘Approx work per year’ is assumed 31,200. The below tables illustrates the Full-Time

Equivalent (FTE) calculation and pay budget. Assuming the budget of a single employee, the

following assumptions have been made (Hunt, 2018).

FTE/Shift Shift length Days per year Hours

required per

year

Divide by

hours

worked per

year

FTE

3 8 365 32120 1.00375 57%

Table 2: FTE Calculation Depending on Shift Length

Employees Hourly Rate ($) Hours per

week

X 52.14

weeks per

year

On-costs –

25%

Total $

Page

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.