Report: Budgeting, Variance, and Staffing in a Nursing Unit

VerifiedAdded on 2021/09/29

|11

|2028

|264

Report

AI Summary

This report provides a comprehensive analysis of budgeting for a nursing unit. It begins with an introduction to healthcare finance and the role of a nurse manager in financial management, including budgeting, variance analysis, and staffing. The report then delves into a detailed analysis of the personnel budget, calculating the total and percentage increase in the budget, and exploring options for managing budget constraints. A significant portion of the report focuses on variance analysis, including the calculation of actual variances (in both dollar and percentage terms), identification of negative variances, and their impact on the budget. The report also examines the principles of nurse staffing according to the ANA, and discusses the nurse manager's role in budgeting, variance, and staffing, including suggestions for improving performance. The report concludes with a discussion of staffing and productivity, the FTE calculation, and recommendations for improving the nursing unit's financial performance, including controlling costs and increasing patient volume.

Running head: REPORT ON BUDGETING FOR A NURSING UNIT

Report On Budgeting For a Nursing Unit

Name of the Student

Name of the University

Author Note

Report On Budgeting For a Nursing Unit

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1REPORT ON BUDGETING FOR A NURSING UNIT

Introduction

A healthcare unit is a place where everyone is treated. Although treating patients is

the primary job of a nursing unit but financial management is also very important aspect. The

finances are important for procuring medicines, paying doctor’s bills, pay wages to

employees and be ready for any emergency. This is to achieve the goal and keep the unit

smoothly running.

Role of Nurse Manager is to look after the working of the hospital, like managers do

in any organisation. The basic job of Nurse Manager is to do financial management,

evaluation and planning, budgeting for next year, working capital management, recruitment,

monitoring and financial risk management. To fulfil these needs they need to have good soft

and hard skill. (Cherry & Jacob, 2016). A nursing manager plays a very essential role in

managing the finances, projecting the cash expenditure and maintaining the day-to-day cash

inflow.

A budget is a tabulated data projected expenditure and income is prepared by

comparing the previous year data. A nursing unit budget preparation may include changes in

price of medicine supplies or new purchase of the equipment or hiring of extra work force.

The nurse managers also requires considering productivity measures and provision for new or

existing services cost. Below is the analysis of the nursing unit with the given data.

Introduction

A healthcare unit is a place where everyone is treated. Although treating patients is

the primary job of a nursing unit but financial management is also very important aspect. The

finances are important for procuring medicines, paying doctor’s bills, pay wages to

employees and be ready for any emergency. This is to achieve the goal and keep the unit

smoothly running.

Role of Nurse Manager is to look after the working of the hospital, like managers do

in any organisation. The basic job of Nurse Manager is to do financial management,

evaluation and planning, budgeting for next year, working capital management, recruitment,

monitoring and financial risk management. To fulfil these needs they need to have good soft

and hard skill. (Cherry & Jacob, 2016). A nursing manager plays a very essential role in

managing the finances, projecting the cash expenditure and maintaining the day-to-day cash

inflow.

A budget is a tabulated data projected expenditure and income is prepared by

comparing the previous year data. A nursing unit budget preparation may include changes in

price of medicine supplies or new purchase of the equipment or hiring of extra work force.

The nurse managers also requires considering productivity measures and provision for new or

existing services cost. Below is the analysis of the nursing unit with the given data.

2REPORT ON BUDGETING FOR A NURSING UNIT

PART A: Personnel Budget

1. To find out Total increase in the Budget.

Formula= Current year total budget-previous total year budget

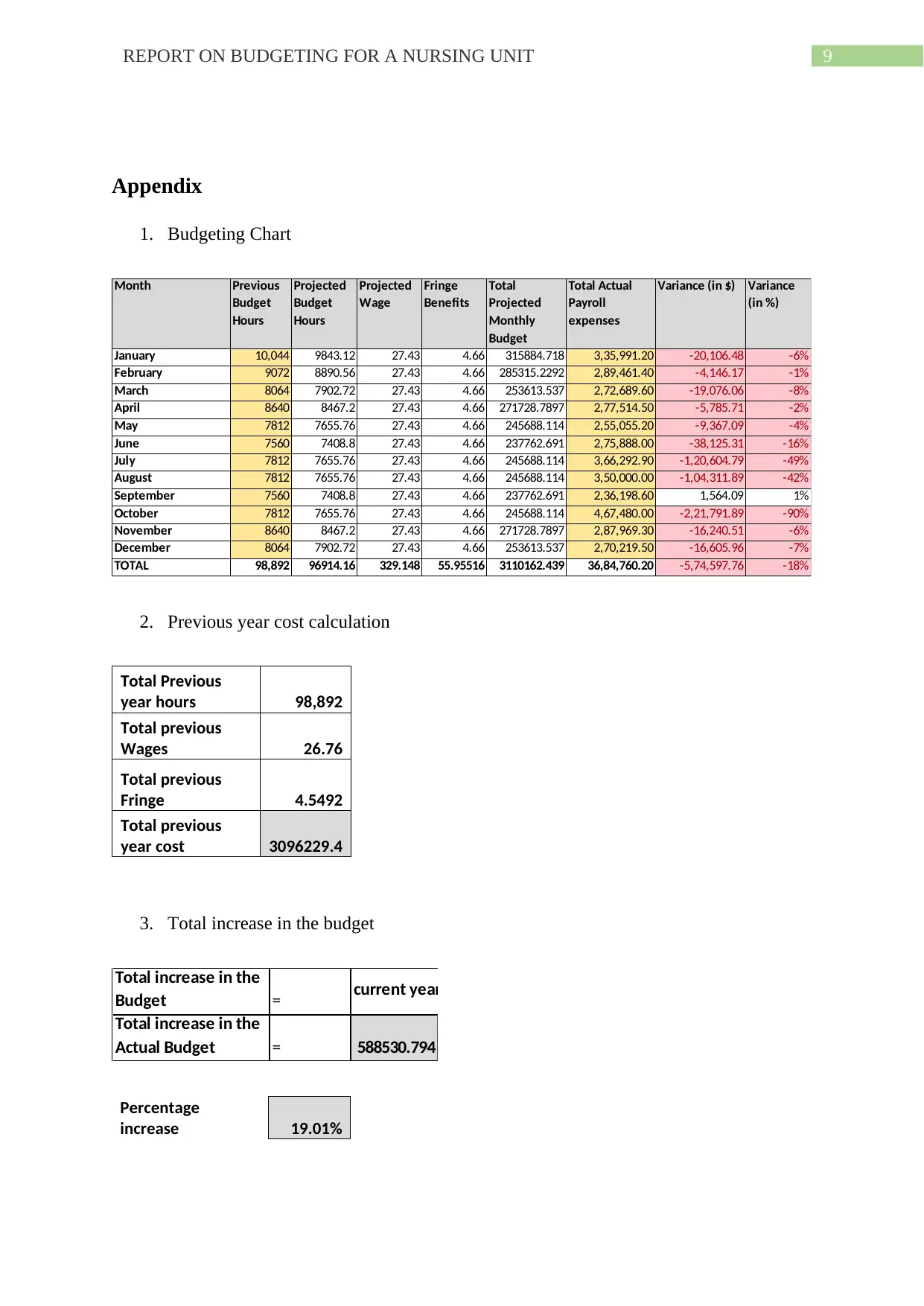

Calculation-3684760.2- 3096229.406= $588530.79.

Inference - The organisation needs to make payments for $588530.79 for this year

expenses, as this is the increased amount of expenditure.

2. What is the % increase of this requested budget amount?

Formula=(Current year total budget-previous total year budget)/previous year total

budget

Calculation - (3684760.2- 3096229.406)/ 3096229.406= 19.1%

Inference -The percentage increase as calculated is 19.1%.

3. If the hospital is unable to commit to this amount of increase, what are your options?

As a nurse manager?

The difference between the Actual and the budgeted amount is $588530.79. The may

management agrees to pay for the deficit which can be managed next year. However

sometimes management may deny the amount and ask the nurse manager to manage it with

whatever budgeted amount given. Here the nurse has to cut cost on variable items like cost on

medical supplies and working hours of the nurses appointed and the acuity time of the

patients. Keeping the salary and fringe not modifiable as assumed in this paper.

PART A: Personnel Budget

1. To find out Total increase in the Budget.

Formula= Current year total budget-previous total year budget

Calculation-3684760.2- 3096229.406= $588530.79.

Inference - The organisation needs to make payments for $588530.79 for this year

expenses, as this is the increased amount of expenditure.

2. What is the % increase of this requested budget amount?

Formula=(Current year total budget-previous total year budget)/previous year total

budget

Calculation - (3684760.2- 3096229.406)/ 3096229.406= 19.1%

Inference -The percentage increase as calculated is 19.1%.

3. If the hospital is unable to commit to this amount of increase, what are your options?

As a nurse manager?

The difference between the Actual and the budgeted amount is $588530.79. The may

management agrees to pay for the deficit which can be managed next year. However

sometimes management may deny the amount and ask the nurse manager to manage it with

whatever budgeted amount given. Here the nurse has to cut cost on variable items like cost on

medical supplies and working hours of the nurses appointed and the acuity time of the

patients. Keeping the salary and fringe not modifiable as assumed in this paper.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3REPORT ON BUDGETING FOR A NURSING UNIT

Part B:

Variance analysis is a tool to understand the potential business issues that could

impact sales or costs. Variance calculation justifies the resulting potential or actual effect on

the company's performance. Budget-to-actual variance is done to compare financial

performance. Actual cost is compared to the budgeted forecast. These forecast and variance

identification helps the management to identify upcoming problems so that the difference can

be eliminated on time. Comparing performance every month, quarterly or yearly can also

keep the organisation in safe working conditions rather than getting sudden jack in the work

(Ruland & Ravn, 2003)

Positive variance:

Positive variance is when actual sales revenue are higher than budgeted revenue, or

budgeted cost is higher than the actual expenses.

For example if the forecasted cost for a working unit is $10000 but the actual cost occurs is

$8000 then the difference shall be $2000 positive which indicates that the company has

managed to cut cost efficiently and expenses had decreased.

Incase of sales or revenue figure if the actual sales surpasses the budgeted then it’s

considered a positive indicator to the company.

Negative Variance:

Negative variances figure for cost or expenses is when actual exceed the budgeted

cost and whereas for sales and revenue when budgeted sales figure exceed the actual. These

figures can be the result of the companies missing targets.

Part B:

Variance analysis is a tool to understand the potential business issues that could

impact sales or costs. Variance calculation justifies the resulting potential or actual effect on

the company's performance. Budget-to-actual variance is done to compare financial

performance. Actual cost is compared to the budgeted forecast. These forecast and variance

identification helps the management to identify upcoming problems so that the difference can

be eliminated on time. Comparing performance every month, quarterly or yearly can also

keep the organisation in safe working conditions rather than getting sudden jack in the work

(Ruland & Ravn, 2003)

Positive variance:

Positive variance is when actual sales revenue are higher than budgeted revenue, or

budgeted cost is higher than the actual expenses.

For example if the forecasted cost for a working unit is $10000 but the actual cost occurs is

$8000 then the difference shall be $2000 positive which indicates that the company has

managed to cut cost efficiently and expenses had decreased.

Incase of sales or revenue figure if the actual sales surpasses the budgeted then it’s

considered a positive indicator to the company.

Negative Variance:

Negative variances figure for cost or expenses is when actual exceed the budgeted

cost and whereas for sales and revenue when budgeted sales figure exceed the actual. These

figures can be the result of the companies missing targets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4REPORT ON BUDGETING FOR A NURSING UNIT

An appropriate example for negative variance for Cost or expense is when budgeted

cost is $10000 and actual happens to be $12000. The $2000 considered a negative variance.

The cost increased was not projected or planned by the management.

A sales or revenue shall be vice versa. Budgeted sales was $10000 and actual is $

8000 than a miss of $2000 considered negative variance.

The method used for calculations are here:

Calculate the actual variance (in $): Total Projected Monthly- Total Actual Expenses

Calculation $315769.6-$3,35,991.20=$ -20,221.65 ( for one month)

Calculate the actual variance (in %): (Variance / total projected monthly)*100

Calculation ($-20,221.65/$315769.6)*100= 19.01% ( for one month)

We find that except in month of September ($1,477.41) all the variance is coming to

be negative in figures thus it can be concluded that the actual expense or actual nursing unit

cost has exceeded the budgeted. This is a negative variance and is not considered good. The

nursing unit should take measures to control the cost as it will affect the revenue for the year-

end. This shows that the management is not able to manage the cost effectively. The highest

variance in cost exceeding the projected is seen in month July, August and September to be -

1,20,694.36, -1,04,401.46 and -2,21,881.46 respectively.

The impact on the real budget:

Work harder to minimise the cost. The patient quantity needs to increase to maintain a

high revenue to run the unit. 30 patients for a day is not maintaining the required

revenue.

An appropriate example for negative variance for Cost or expense is when budgeted

cost is $10000 and actual happens to be $12000. The $2000 considered a negative variance.

The cost increased was not projected or planned by the management.

A sales or revenue shall be vice versa. Budgeted sales was $10000 and actual is $

8000 than a miss of $2000 considered negative variance.

The method used for calculations are here:

Calculate the actual variance (in $): Total Projected Monthly- Total Actual Expenses

Calculation $315769.6-$3,35,991.20=$ -20,221.65 ( for one month)

Calculate the actual variance (in %): (Variance / total projected monthly)*100

Calculation ($-20,221.65/$315769.6)*100= 19.01% ( for one month)

We find that except in month of September ($1,477.41) all the variance is coming to

be negative in figures thus it can be concluded that the actual expense or actual nursing unit

cost has exceeded the budgeted. This is a negative variance and is not considered good. The

nursing unit should take measures to control the cost as it will affect the revenue for the year-

end. This shows that the management is not able to manage the cost effectively. The highest

variance in cost exceeding the projected is seen in month July, August and September to be -

1,20,694.36, -1,04,401.46 and -2,21,881.46 respectively.

The impact on the real budget:

Work harder to minimise the cost. The patient quantity needs to increase to maintain a

high revenue to run the unit. 30 patients for a day is not maintaining the required

revenue.

5REPORT ON BUDGETING FOR A NURSING UNIT

A negative variance is always a serious issue for any organisation proper steps needs

to be taken to mitigate the consequences. Like modifying the working hours to

accommodate cost.

The salary cut on the staff or laying off some staffs shall be a remedy to increase the

production and manage the smooth running of the organisation.

Part C:

According to ANA Principles for Nurse Staff nurse, Second Edition Job of a nurse is

very essential. They have to deliver a safe and quality work. This will affect the patient

feedback and outcome. The expertise of a nurse is matched with profile needs of the nursing

unit (Weston et al., (2012).

Some Important points in accordance to staffing nurse according to ANA principles:

• Nursing staffing need a quality and cost effectiveness.

• A well-developed staffing guidelines to handle daily patients with least problems.

• All Registered nurses, must have an active role in staffing to make sure the necessary time

required to look after the patients.

• Cost effectiveness plays an important role for delivering a safe, quality care.

• Reimbursement structure has to be independent to staffing nurses.

Nurse Manager’s role in financing activity in relationship to Budgeting, variance

and staffing:

A nurse manager plays the most vital role in a nursing unit. They require multiple

skills to fulfil the job requirements successfully. They not only requires nursing skills but also

management skills for good communication and interpersonal skills.

A negative variance is always a serious issue for any organisation proper steps needs

to be taken to mitigate the consequences. Like modifying the working hours to

accommodate cost.

The salary cut on the staff or laying off some staffs shall be a remedy to increase the

production and manage the smooth running of the organisation.

Part C:

According to ANA Principles for Nurse Staff nurse, Second Edition Job of a nurse is

very essential. They have to deliver a safe and quality work. This will affect the patient

feedback and outcome. The expertise of a nurse is matched with profile needs of the nursing

unit (Weston et al., (2012).

Some Important points in accordance to staffing nurse according to ANA principles:

• Nursing staffing need a quality and cost effectiveness.

• A well-developed staffing guidelines to handle daily patients with least problems.

• All Registered nurses, must have an active role in staffing to make sure the necessary time

required to look after the patients.

• Cost effectiveness plays an important role for delivering a safe, quality care.

• Reimbursement structure has to be independent to staffing nurses.

Nurse Manager’s role in financing activity in relationship to Budgeting, variance

and staffing:

A nurse manager plays the most vital role in a nursing unit. They require multiple

skills to fulfil the job requirements successfully. They not only requires nursing skills but also

management skills for good communication and interpersonal skills.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6REPORT ON BUDGETING FOR A NURSING UNIT

Budgeting

Her role in respect to the budgeting is that a nurse manager needs to forecast the cost

for year ahead by preparing a fresh budgeting table by considering all major changes from the

previous year cost. The budgeting should be calculated on the projected cost and sales figure

as these are assumptions based on the previous year’s data. A nurse manager not only

understands it but also derive the future sales and cost.

The forecasted budget needs to be approved by the management. The need for an

extra cash or need for new equipment are to be explained to the management properly for the

budget to be approved which shall help the organisation to work smoothly. The manager

nurse’s duty is to explain the drawn budget with all clarifications required.

Variance

Many a times it happens that the budgeted forecast does not match with the actual

one. The nurse manager has to keep the records ready and calculate the variance to explain to

the management. It is the responsibility of the nurse manager to maintain the forecast and the

actual cost of revenue to be closely same. If there is any major difference than that has to be

immediately brought under the consideration to the management.

The difference of budgeted and actual cost is variance and the variance is an

important factor for the management to recognise as that it helps in making good decisions to

input any service or remove any unnecessary cost. This is the responsibility of the nurse

manager to calculate the variance also understand the reason for the same.

Staffing and productivity

A nurse manager are responsible for a safe, secure and quality care. The staffing in

relation to the calculations are good. It is concluded the unit is working well in compliance of

Budgeting

Her role in respect to the budgeting is that a nurse manager needs to forecast the cost

for year ahead by preparing a fresh budgeting table by considering all major changes from the

previous year cost. The budgeting should be calculated on the projected cost and sales figure

as these are assumptions based on the previous year’s data. A nurse manager not only

understands it but also derive the future sales and cost.

The forecasted budget needs to be approved by the management. The need for an

extra cash or need for new equipment are to be explained to the management properly for the

budget to be approved which shall help the organisation to work smoothly. The manager

nurse’s duty is to explain the drawn budget with all clarifications required.

Variance

Many a times it happens that the budgeted forecast does not match with the actual

one. The nurse manager has to keep the records ready and calculate the variance to explain to

the management. It is the responsibility of the nurse manager to maintain the forecast and the

actual cost of revenue to be closely same. If there is any major difference than that has to be

immediately brought under the consideration to the management.

The difference of budgeted and actual cost is variance and the variance is an

important factor for the management to recognise as that it helps in making good decisions to

input any service or remove any unnecessary cost. This is the responsibility of the nurse

manager to calculate the variance also understand the reason for the same.

Staffing and productivity

A nurse manager are responsible for a safe, secure and quality care. The staffing in

relation to the calculations are good. It is concluded the unit is working well in compliance of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7REPORT ON BUDGETING FOR A NURSING UNIT

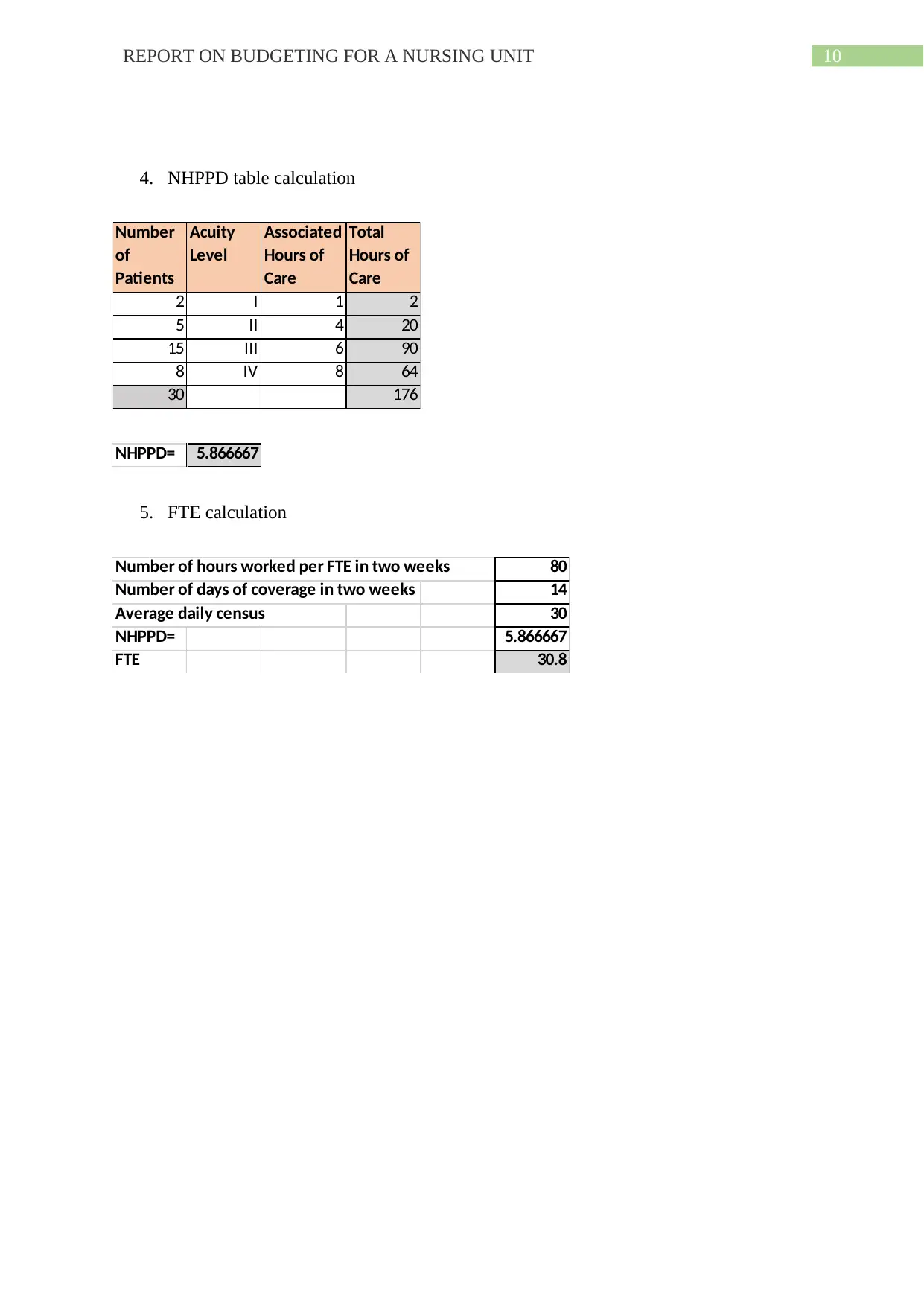

the requirement. If average number of daily patients is taken then it is a very good figure.

The number of hours required to do the work daily is 176 hrs with NHPPD to be 5.86.

FTE is for full-time equivalent it is the number of working hours for one full-time

employee completing during a fixed period. FTE helps manager to budget the cost of labour.

Here the calculated FTE 30.8 which is okay. The number of days worked in two week is 14

so there is no days off. The FTE 80 is also okay but can be altered by the nurse manager for

more efficiency.

Suggestions for improving performance:

The management is doing well but somehow the actual cost is surpassing the

budgeted cost. The amount exceeding is very high which requires to be controlled.

When the manager nurse has committed to keep the budget inline to project then

important things should be taken care.

The variance is all in negative, which is a sign that management is not adhering to the

important needs of the budgets. The actual is passing the projected and in continuous

3 months the budget is exceeding a huge amount. Strong actions should be taken to

bring it under control.

The variables that to be modified is working hours and acuity level. The costing

should be re-planned to match the productivity.

the requirement. If average number of daily patients is taken then it is a very good figure.

The number of hours required to do the work daily is 176 hrs with NHPPD to be 5.86.

FTE is for full-time equivalent it is the number of working hours for one full-time

employee completing during a fixed period. FTE helps manager to budget the cost of labour.

Here the calculated FTE 30.8 which is okay. The number of days worked in two week is 14

so there is no days off. The FTE 80 is also okay but can be altered by the nurse manager for

more efficiency.

Suggestions for improving performance:

The management is doing well but somehow the actual cost is surpassing the

budgeted cost. The amount exceeding is very high which requires to be controlled.

When the manager nurse has committed to keep the budget inline to project then

important things should be taken care.

The variance is all in negative, which is a sign that management is not adhering to the

important needs of the budgets. The actual is passing the projected and in continuous

3 months the budget is exceeding a huge amount. Strong actions should be taken to

bring it under control.

The variables that to be modified is working hours and acuity level. The costing

should be re-planned to match the productivity.

8REPORT ON BUDGETING FOR A NURSING UNIT

Referencing

Cherry, B., & Jacob, S. R. (2016). Contemporary nursing: Issues, trends, & management.

Elsevier Health Sciences.

Ruland, C. M., & Ravn, I. H. (2003). Usefulness and effects on costs and staff management

of a nursing resource management information system. Journal of nursing

management, 11(3), 208-215.

Weston, M. J., Brewer, K. C., & Peterson, C. A. (2012). ANA principles: The framework for

nurse staffing to positively impact outcomes. Nursing Economics, 30(5), 247.

Referencing

Cherry, B., & Jacob, S. R. (2016). Contemporary nursing: Issues, trends, & management.

Elsevier Health Sciences.

Ruland, C. M., & Ravn, I. H. (2003). Usefulness and effects on costs and staff management

of a nursing resource management information system. Journal of nursing

management, 11(3), 208-215.

Weston, M. J., Brewer, K. C., & Peterson, C. A. (2012). ANA principles: The framework for

nurse staffing to positively impact outcomes. Nursing Economics, 30(5), 247.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9REPORT ON BUDGETING FOR A NURSING UNIT

Appendix

1. Budgeting Chart

Month Previous

Budget

Hours

Projected

Budget

Hours

Projected

Wage

Fringe

Benefits

Total

Projected

Monthly

Budget

Total Actual

Payroll

expenses

Variance (in $) Variance

(in %)

January 10,044 9843.12 27.43 4.66 315884.718 3,35,991.20 -20,106.48 -6%

February 9072 8890.56 27.43 4.66 285315.2292 2,89,461.40 -4,146.17 -1%

March 8064 7902.72 27.43 4.66 253613.537 2,72,689.60 -19,076.06 -8%

April 8640 8467.2 27.43 4.66 271728.7897 2,77,514.50 -5,785.71 -2%

May 7812 7655.76 27.43 4.66 245688.114 2,55,055.20 -9,367.09 -4%

June 7560 7408.8 27.43 4.66 237762.691 2,75,888.00 -38,125.31 -16%

July 7812 7655.76 27.43 4.66 245688.114 3,66,292.90 -1,20,604.79 -49%

August 7812 7655.76 27.43 4.66 245688.114 3,50,000.00 -1,04,311.89 -42%

September 7560 7408.8 27.43 4.66 237762.691 2,36,198.60 1,564.09 1%

October 7812 7655.76 27.43 4.66 245688.114 4,67,480.00 -2,21,791.89 -90%

November 8640 8467.2 27.43 4.66 271728.7897 2,87,969.30 -16,240.51 -6%

December 8064 7902.72 27.43 4.66 253613.537 2,70,219.50 -16,605.96 -7%

TOTAL 98,892 96914.16 329.148 55.95516 3110162.439 36,84,760.20 -5,74,597.76 -18%

2. Previous year cost calculation

Total Previous

year hours 98,892

Total previous

Wages 26.76

Total previous

Fringe 4.5492

Total previous

year cost 3096229.4

3. Total increase in the budget

Total increase in the

Budget = current year total budget-previous total year budget

Total increase in the

Actual Budget = 588530.794

Percentage

increase 19.01%

Appendix

1. Budgeting Chart

Month Previous

Budget

Hours

Projected

Budget

Hours

Projected

Wage

Fringe

Benefits

Total

Projected

Monthly

Budget

Total Actual

Payroll

expenses

Variance (in $) Variance

(in %)

January 10,044 9843.12 27.43 4.66 315884.718 3,35,991.20 -20,106.48 -6%

February 9072 8890.56 27.43 4.66 285315.2292 2,89,461.40 -4,146.17 -1%

March 8064 7902.72 27.43 4.66 253613.537 2,72,689.60 -19,076.06 -8%

April 8640 8467.2 27.43 4.66 271728.7897 2,77,514.50 -5,785.71 -2%

May 7812 7655.76 27.43 4.66 245688.114 2,55,055.20 -9,367.09 -4%

June 7560 7408.8 27.43 4.66 237762.691 2,75,888.00 -38,125.31 -16%

July 7812 7655.76 27.43 4.66 245688.114 3,66,292.90 -1,20,604.79 -49%

August 7812 7655.76 27.43 4.66 245688.114 3,50,000.00 -1,04,311.89 -42%

September 7560 7408.8 27.43 4.66 237762.691 2,36,198.60 1,564.09 1%

October 7812 7655.76 27.43 4.66 245688.114 4,67,480.00 -2,21,791.89 -90%

November 8640 8467.2 27.43 4.66 271728.7897 2,87,969.30 -16,240.51 -6%

December 8064 7902.72 27.43 4.66 253613.537 2,70,219.50 -16,605.96 -7%

TOTAL 98,892 96914.16 329.148 55.95516 3110162.439 36,84,760.20 -5,74,597.76 -18%

2. Previous year cost calculation

Total Previous

year hours 98,892

Total previous

Wages 26.76

Total previous

Fringe 4.5492

Total previous

year cost 3096229.4

3. Total increase in the budget

Total increase in the

Budget = current year total budget-previous total year budget

Total increase in the

Actual Budget = 588530.794

Percentage

increase 19.01%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10REPORT ON BUDGETING FOR A NURSING UNIT

4. NHPPD table calculation

Number

of

Patients

Acuity

Level

Associated

Hours of

Care

Total

Hours of

Care

2 I 1 2

5 II 4 20

15 III 6 90

8 IV 8 64

30 176

NHPPD= 5.866667

5. FTE calculation

Number of hours worked per FTE in two weeks 80

Number of days of coverage in two weeks 14

Average daily census 30

NHPPD= 5.866667

FTE 30.8

4. NHPPD table calculation

Number

of

Patients

Acuity

Level

Associated

Hours of

Care

Total

Hours of

Care

2 I 1 2

5 II 4 20

15 III 6 90

8 IV 8 64

30 176

NHPPD= 5.866667

5. FTE calculation

Number of hours worked per FTE in two weeks 80

Number of days of coverage in two weeks 14

Average daily census 30

NHPPD= 5.866667

FTE 30.8

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.