Comprehensive Master Budget Analysis for Business Decision Making

VerifiedAdded on 2020/01/23

|13

|1872

|116

Report

AI Summary

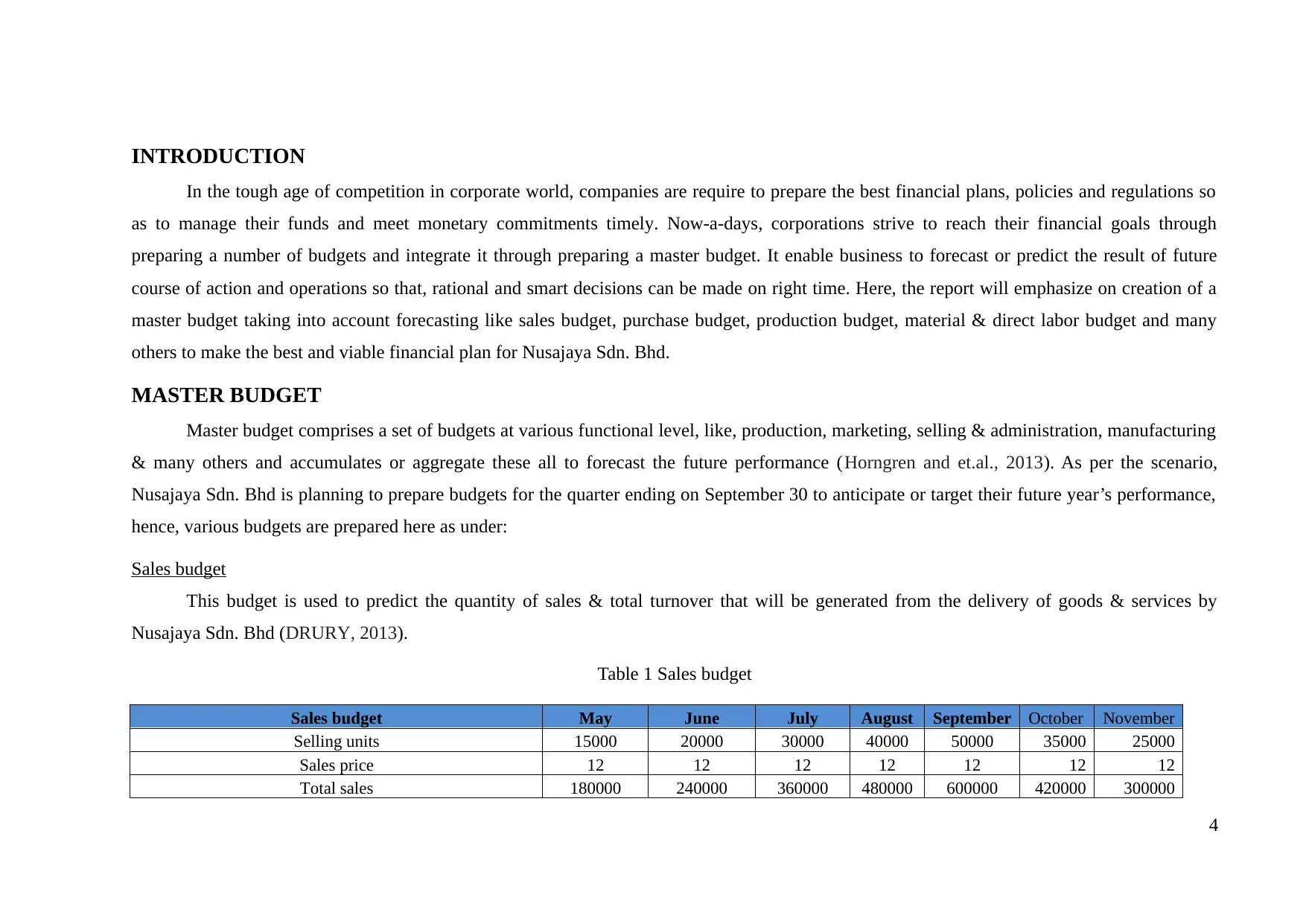

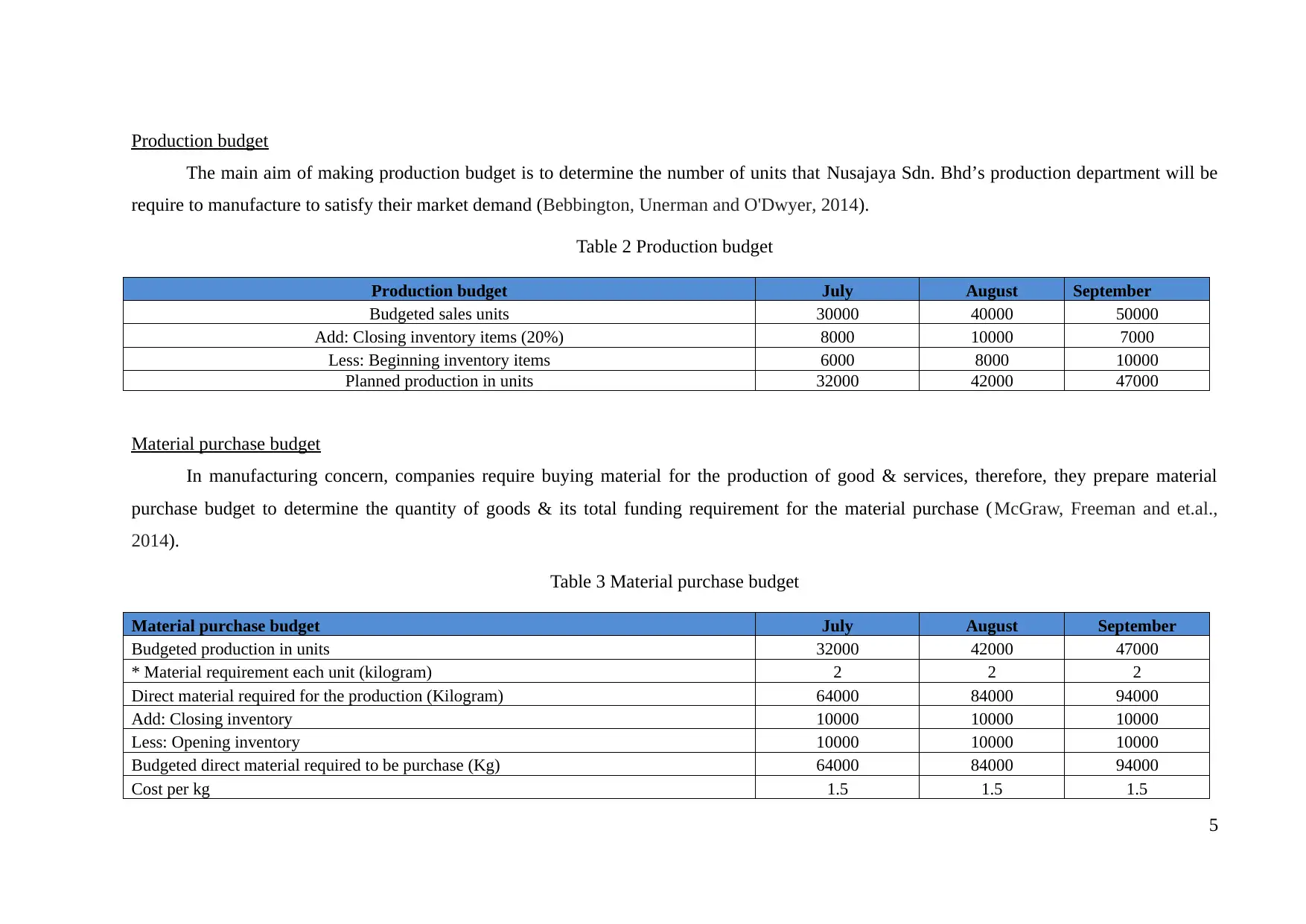

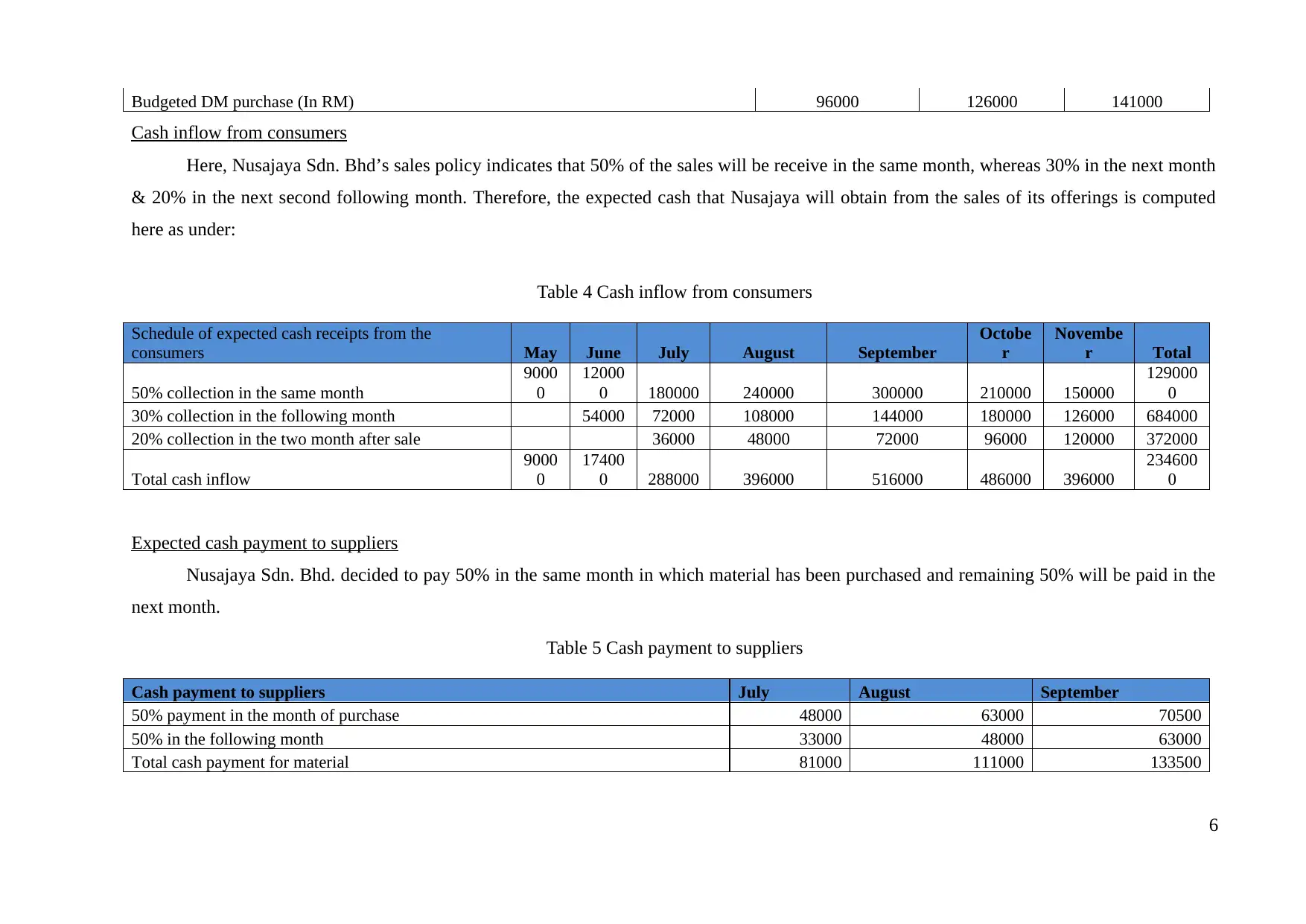

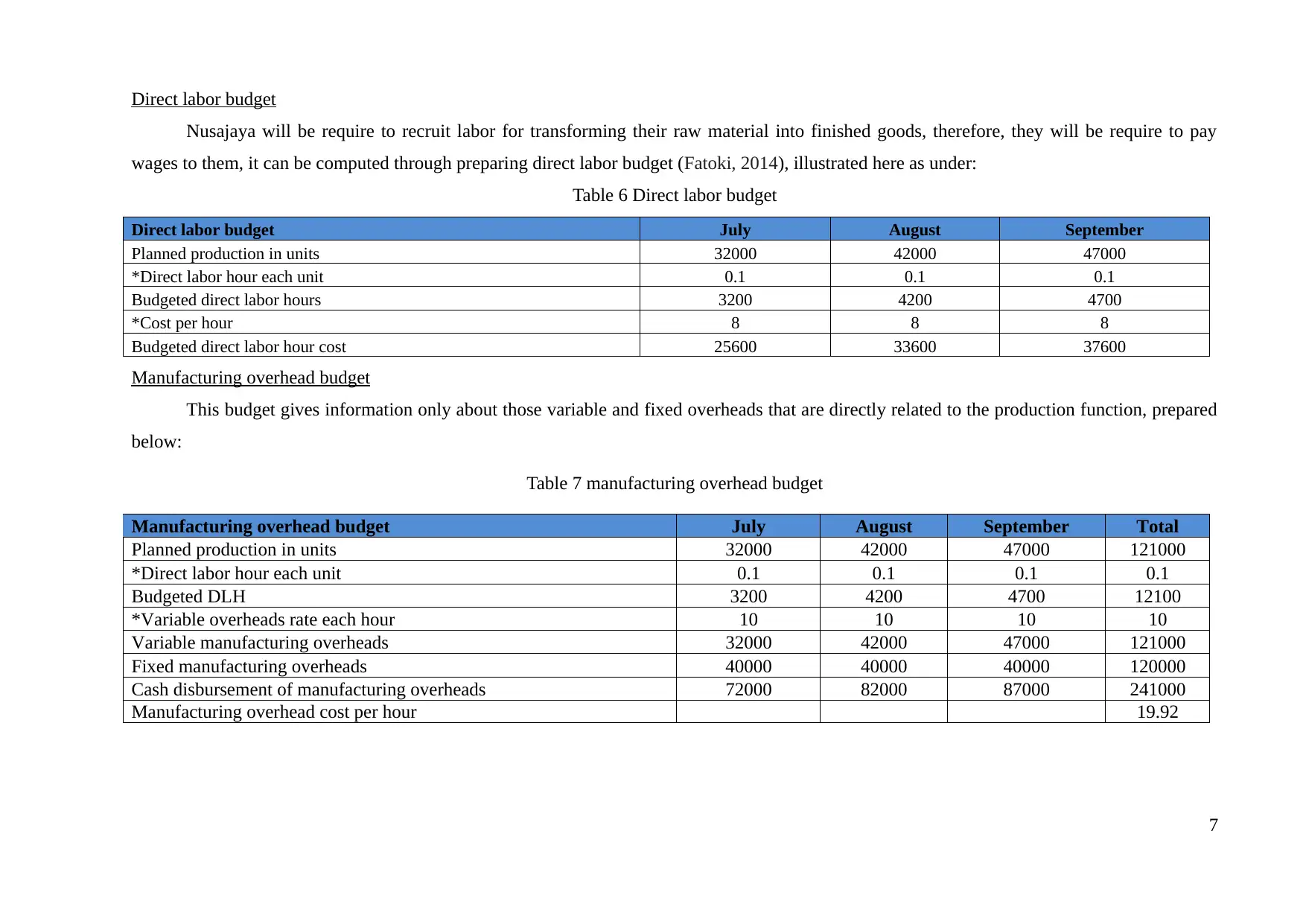

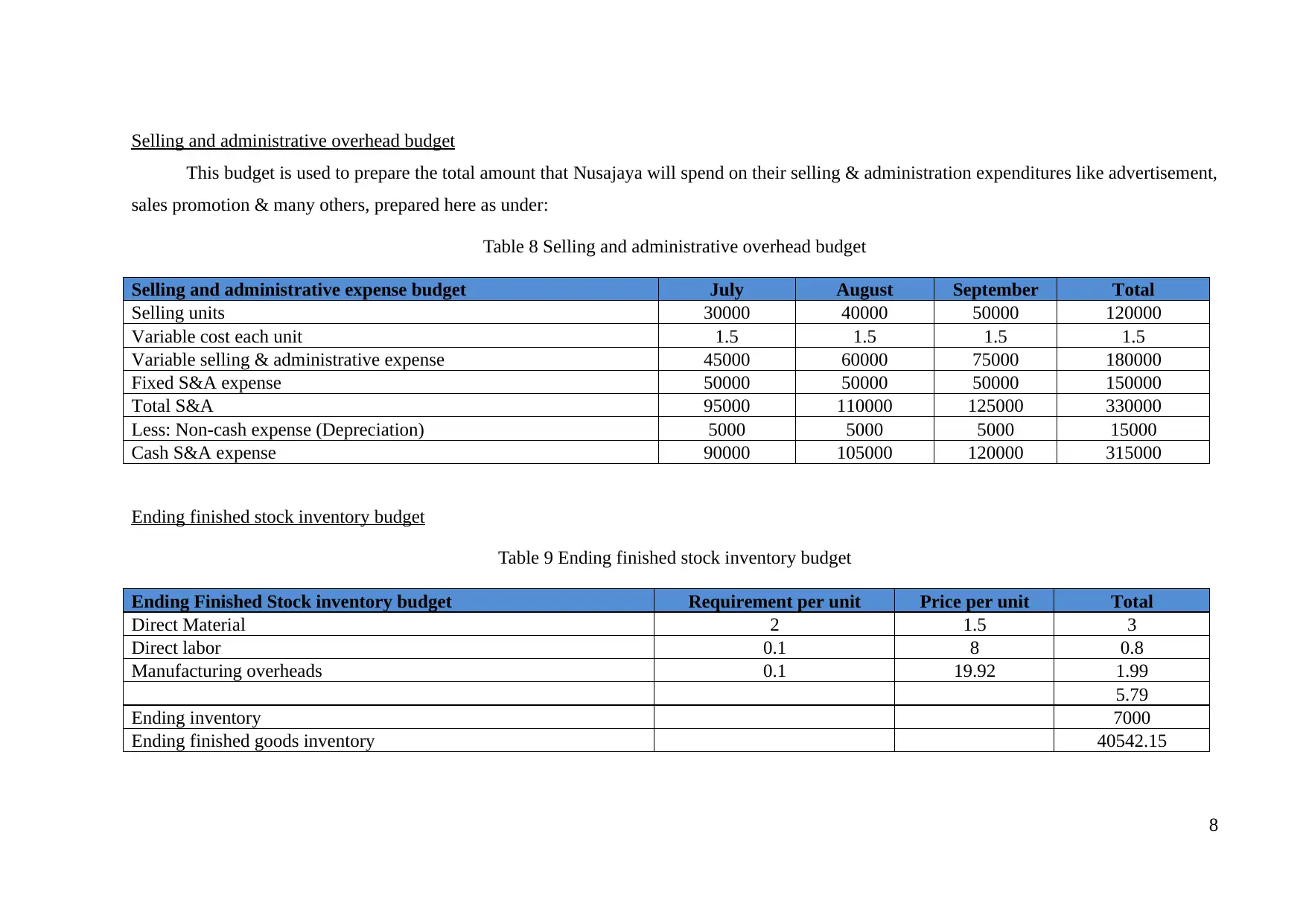

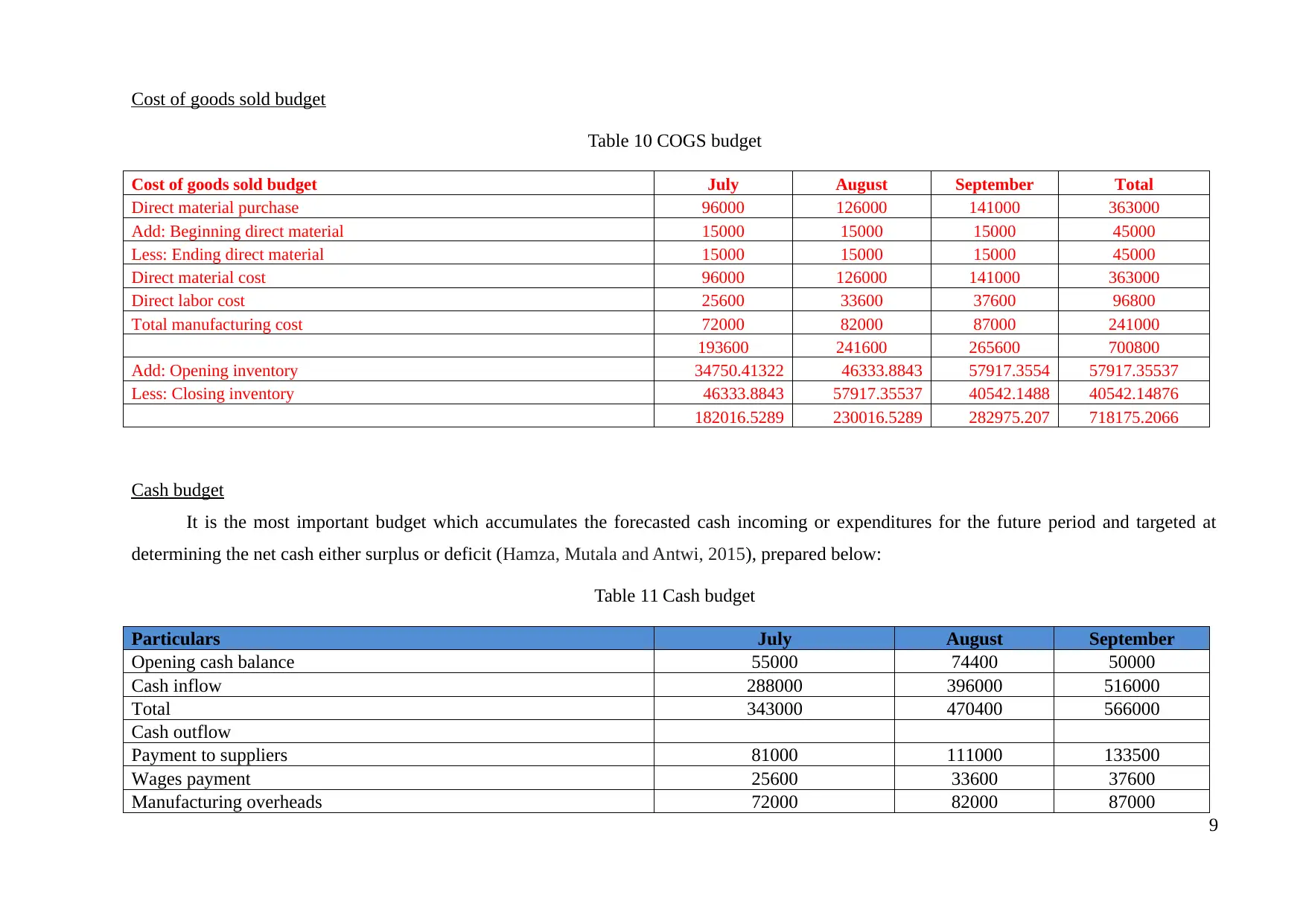

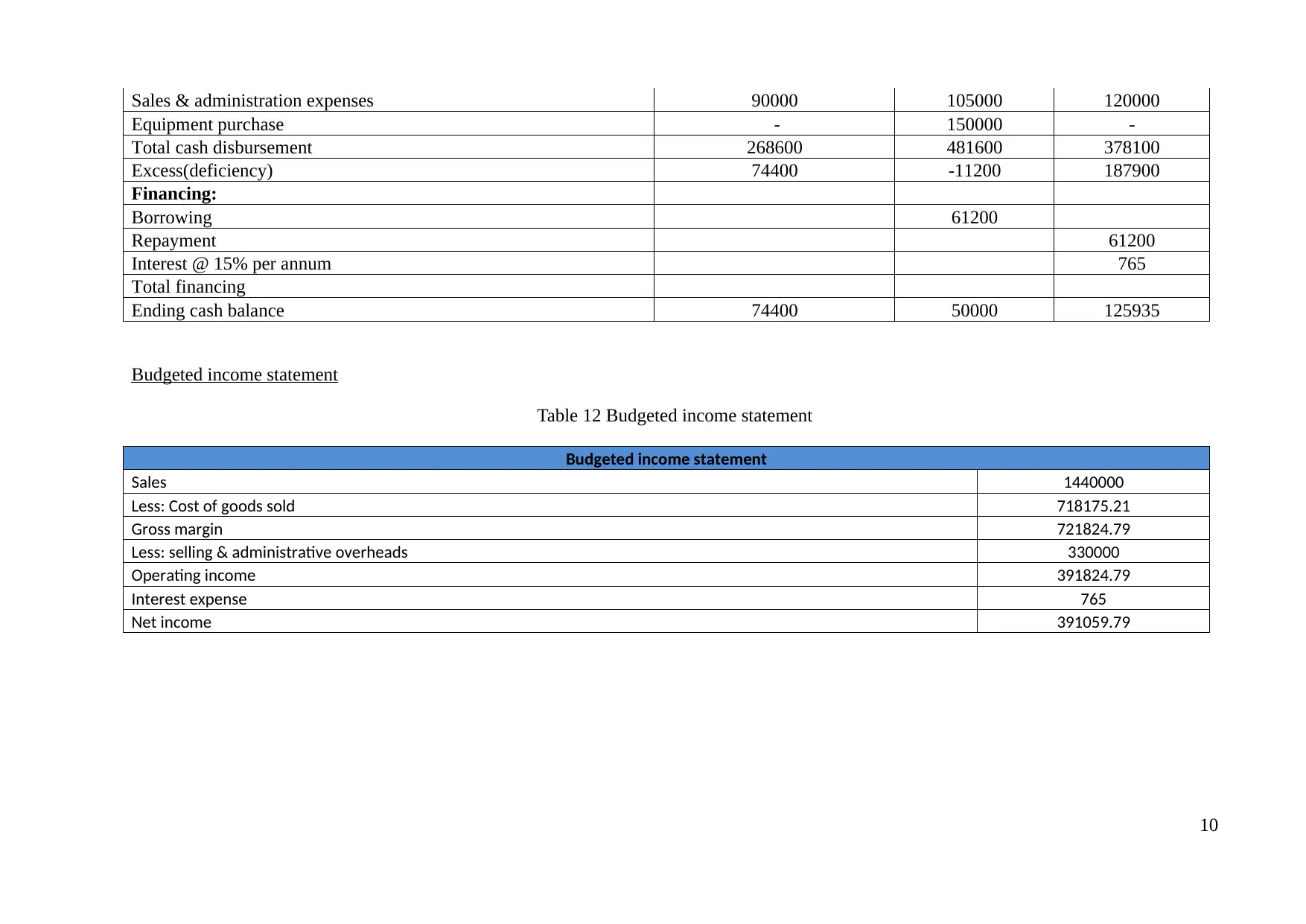

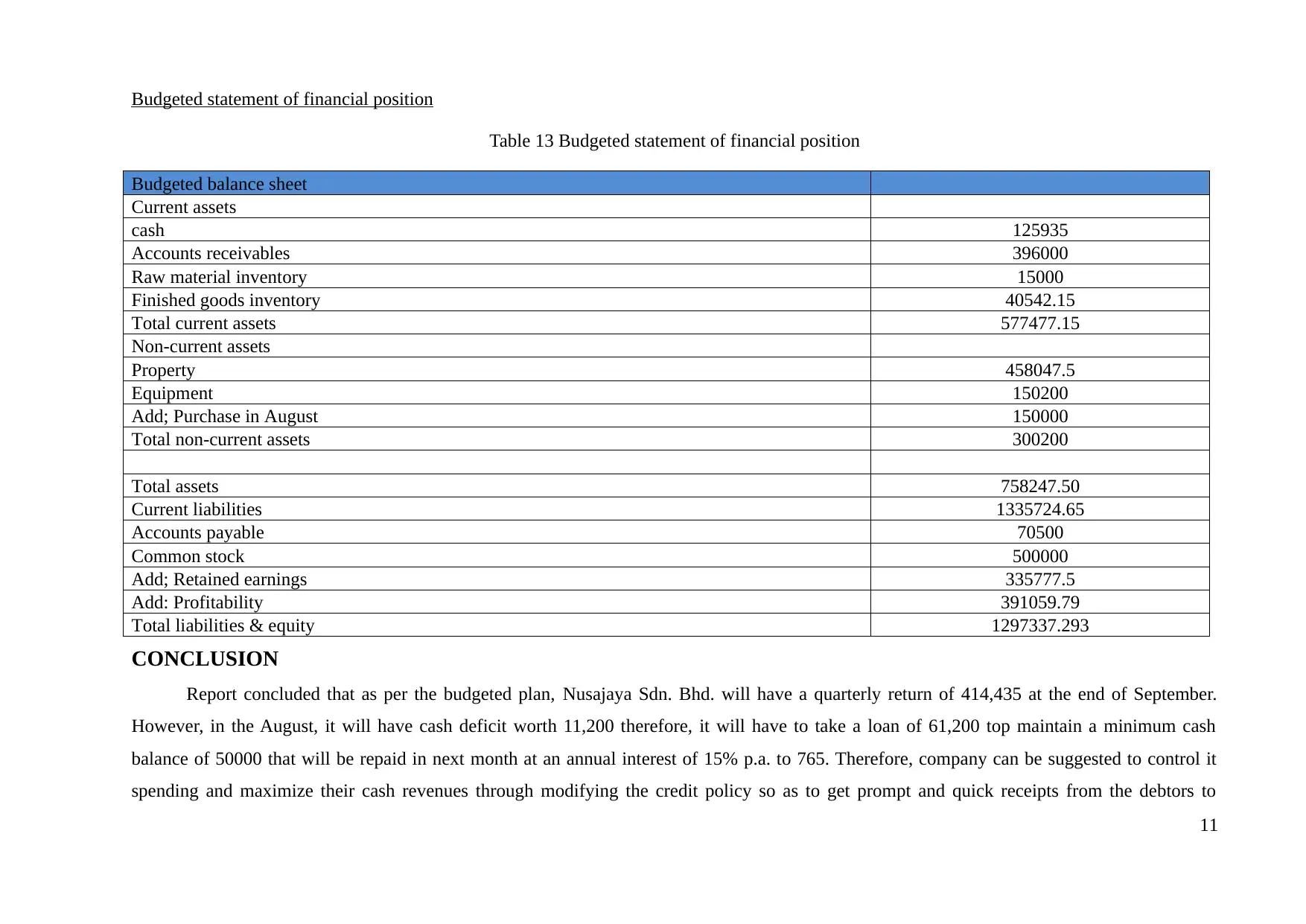

This report presents a comprehensive master budget for Nusajaya Sdn. Bhd., focusing on financial planning and decision-making. The report details the creation of various budgets, including sales, production, material purchase, cash inflow, direct labor, manufacturing overhead, and selling and administrative overhead budgets. It also includes an ending finished stock inventory budget, a cost of goods sold budget, a cash budget, a budgeted income statement, and a budgeted statement of financial position. The analysis provides a detailed financial forecast for the quarter ending September 30, highlighting key financial metrics, cash flow projections, and anticipated profitability. The report concludes with recommendations for financial management, emphasizing the importance of controlling spending and optimizing cash revenues through effective credit policies. The financial statements provide insights into the company's expected performance and financial position, aiding in strategic planning and resource allocation. The report also includes various tables that provide detailed data on the different components of the master budget.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.