Management Accounting Report: Oak Cash and Carry Business Analysis

VerifiedAdded on 2020/11/23

|17

|5444

|469

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on the financial practices of Oak Cash and Carry, a small wholesale firm. It begins by defining management accounting and exploring the requirements of different management accounting systems, including cost accounting, job costing, inventory management, and price optimization systems. The report then details various management accounting reporting methods such as budget reports, accounts receivable reports, inventory management reports, and performance reports. Furthermore, the report delves into cost analysis techniques used to prepare income statements using marginal and absorption costs. It also examines the advantages and disadvantages of planning tools for budgetary control and discusses how organizations should adapt management accounting systems to respond to financial problems. The report concludes by emphasizing the importance of management accounting for effective decision-making, planning, and control within a business context, providing valuable insights into the financial operations and strategic planning of the firm.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

P1 Management accounting and requirements of different types of management accounting

systems........................................................................................................................................1

P2 Explain different methods used for management accounting reporting................................3

TASK 2............................................................................................................................................6

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs. .........................................................................6

TASK 3............................................................................................................................................9

P4 Advantages and disadvantages of different types of planning tools for budgetary control..9

TASK 4..........................................................................................................................................11

P5 Compare how organisations should adapt management accounting systems to respond to

financial problems.....................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

P1 Management accounting and requirements of different types of management accounting

systems........................................................................................................................................1

P2 Explain different methods used for management accounting reporting................................3

TASK 2............................................................................................................................................6

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs. .........................................................................6

TASK 3............................................................................................................................................9

P4 Advantages and disadvantages of different types of planning tools for budgetary control..9

TASK 4..........................................................................................................................................11

P5 Compare how organisations should adapt management accounting systems to respond to

financial problems.....................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is a process to prepare reports and accounts to scale accurate

financial status of company. This is required to make day to day and short term decisions that are

beneficial to attain business goals. Every business has an objective and goal to gain profit against

investment. In beginning of a business firm's owner invest some amount that is known as capital.

There are various activities and operations that needs to be measured so that a final state of a

company can be analyzed in statistical form (Bodnar and Hopwood, 2012) . It is used to measure

the cost and operations of firm to prepare a internal management reports, records and accounts in

order to organization can analyze their actual status to achieve the goals. Oak Cash and Carry is

small firm which is working as a service provider in various fields such as tobacco, food,

beverages, cash & carry wholesale, grocery. The firm have between 20 to 49 employees at

present who are actively working for company. Hence, this report is consists of management

accounting and their importance along with their methods importance. It also covers cost

analysis techniques to prepare income statement, types of planning tools that are use for

budgetary control. Further it also comprises of financial problems with management accounting

system.

TASK 1

P1 Management accounting and requirements of different types of management accounting

systems.

Management accounting – It defines pattern to prepare and provide timely financial and

statistical information about business operations so managers can make daily accounts report that

helps them to achieve short term goal. As given in the scenario, it is a responsibility of

Management Accounting Officer that they notice every business activity which are conducting

within a business. For example, Oak cash and Carry is a wholesale company and in order to

run their business in an effective way they needs various sources like logistics services for

import and export (Macintosh and Quattrone, 2010) . Firm needs to spend money on carriage

inward and outward that needs to note in daily accounts books as an expense of organization.

Similarly, there are some various business operations that are counted as income of business like

purchased material such as machinery and other assets. These are recorded in accounts books

1

Management accounting is a process to prepare reports and accounts to scale accurate

financial status of company. This is required to make day to day and short term decisions that are

beneficial to attain business goals. Every business has an objective and goal to gain profit against

investment. In beginning of a business firm's owner invest some amount that is known as capital.

There are various activities and operations that needs to be measured so that a final state of a

company can be analyzed in statistical form (Bodnar and Hopwood, 2012) . It is used to measure

the cost and operations of firm to prepare a internal management reports, records and accounts in

order to organization can analyze their actual status to achieve the goals. Oak Cash and Carry is

small firm which is working as a service provider in various fields such as tobacco, food,

beverages, cash & carry wholesale, grocery. The firm have between 20 to 49 employees at

present who are actively working for company. Hence, this report is consists of management

accounting and their importance along with their methods importance. It also covers cost

analysis techniques to prepare income statement, types of planning tools that are use for

budgetary control. Further it also comprises of financial problems with management accounting

system.

TASK 1

P1 Management accounting and requirements of different types of management accounting

systems.

Management accounting – It defines pattern to prepare and provide timely financial and

statistical information about business operations so managers can make daily accounts report that

helps them to achieve short term goal. As given in the scenario, it is a responsibility of

Management Accounting Officer that they notice every business activity which are conducting

within a business. For example, Oak cash and Carry is a wholesale company and in order to

run their business in an effective way they needs various sources like logistics services for

import and export (Macintosh and Quattrone, 2010) . Firm needs to spend money on carriage

inward and outward that needs to note in daily accounts books as an expense of organization.

Similarly, there are some various business operations that are counted as income of business like

purchased material such as machinery and other assets. These are recorded in accounts books

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that supports to business activities to attain objectives and goals. Through these organization can

take short term decisions to attain the targets of the firm.

The core purpose of Management accounting system is to develops reports on the basis

of company's financial information so that managers can take decisions and also establish

effective planning to run a business smoothly. These reports are confidential because it contains

organization's internal information regarding entire income and expenses that needs to measure

required changes so that firm can be operated in an appropriate manner (Liandet. al., 2012) .

Types of management accounting system - There are different types of management

accounting systems which also has distinct use for Oak cash and Carry and these are

mentioned below -

Cost accounting system – It is a method which is used to analyse production cost through

assessing input costs of each stage. It includes cost of raw material, manufacturing,

testing, packaging etc. Cost accounting system is used to record individual cost of goods

and then it compares the results with output. For example, Oak Cash and Carry is

manufactures products then it will first measure production cost of products then it will

analyse actual result cost of goods.

Job costing system – It is used to monitor expenses on manufacturing of the products and

services. The managers keep track of expenses through dividing all expenses in overhead,

direct material, and direct labor. So that managers can estimate actual cost of product and

access value of raw materials, labor hours and equipment can be control in an effective

way. This is used to analyse the total cost of goods and then it can be control according

to the customers requirements (Sisaye and Birnberg, 2010) . For illustration, Oak cash

and Carry use it to monitor total cost of a product throughout manufacturing phase and it

can be reimburse according to customers needs. When customer needs goods at that time

only it can manufacture the product that needs some expenses such a they needs to pay

the labors, raw materials, packaging charges, etc. The overall cost can be control

thorough identifying the customer needs and requirements. If there is no requirement of

production then firm can keep its money safe for other operations.

Inventory management system – This is used to monitor available stocks within an

organization. Every department tracks their stored stuff whether they are company assets,

raw materials, supplies or finished goods. The core objective of inventory management

2

take short term decisions to attain the targets of the firm.

The core purpose of Management accounting system is to develops reports on the basis

of company's financial information so that managers can take decisions and also establish

effective planning to run a business smoothly. These reports are confidential because it contains

organization's internal information regarding entire income and expenses that needs to measure

required changes so that firm can be operated in an appropriate manner (Liandet. al., 2012) .

Types of management accounting system - There are different types of management

accounting systems which also has distinct use for Oak cash and Carry and these are

mentioned below -

Cost accounting system – It is a method which is used to analyse production cost through

assessing input costs of each stage. It includes cost of raw material, manufacturing,

testing, packaging etc. Cost accounting system is used to record individual cost of goods

and then it compares the results with output. For example, Oak Cash and Carry is

manufactures products then it will first measure production cost of products then it will

analyse actual result cost of goods.

Job costing system – It is used to monitor expenses on manufacturing of the products and

services. The managers keep track of expenses through dividing all expenses in overhead,

direct material, and direct labor. So that managers can estimate actual cost of product and

access value of raw materials, labor hours and equipment can be control in an effective

way. This is used to analyse the total cost of goods and then it can be control according

to the customers requirements (Sisaye and Birnberg, 2010) . For illustration, Oak cash

and Carry use it to monitor total cost of a product throughout manufacturing phase and it

can be reimburse according to customers needs. When customer needs goods at that time

only it can manufacture the product that needs some expenses such a they needs to pay

the labors, raw materials, packaging charges, etc. The overall cost can be control

thorough identifying the customer needs and requirements. If there is no requirement of

production then firm can keep its money safe for other operations.

Inventory management system – This is used to monitor available stocks within an

organization. Every department tracks their stored stuff whether they are company assets,

raw materials, supplies or finished goods. The core objective of inventory management

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

system is that manager watches every supply order that are ready to shift to the vendor.

As Oak cash and Carry is a small firm and that are used to manage ordering and sales

supply chain because it gives a clear statistics about availability of products.

Price optimization system – This is one of the crucial system for company because after

investing money on product. The firm needs to optimize price of finished goods that is

beneficial for firm and satisfactory for customers as well (Hoque, 2011) . For an example,

Oak cash and Carry is a wholesaler that provides finished goods to their clients and they

have spend money on production. These goods should have value for customer and in

order to provide products to customers they needs to measure total cost of product. So

that they can manage their investment and customer satisfaction level through identifying

their purchasing behavior and capacity. Thus, this price optimization system is used to

manage price according to customers and firm so that it can conduct business in an

appropriate manner.

All of these management accounting systems are required for different purpose such as

cost accounting is used to analyse actual cost of products. Job costing is require to monitor the

cost of goods that can be control according to the customer needs. It includes labor per hour cost,

equipment and machinery investment, etc. Inventory management system is used to watch stored

goods and products that are essential for Oak cash and Carry. Price optimization is used to

provide a price of a product that is profitable for firm and customer as well (Busco and Scapens,

2011) .

P2 Explain different methods used for management accounting reporting.

Management accounting reports are use for planning, regulating, decision making and

measuring performance. These reports are developing by various sections of an organization

throughout accounting and bookkeeping year. The major objective of developing these reports is

that crucial decisions depends on the accuracy and authenticity of these books. Manager

accounting officer of Oak cash and Carry analyses this information and then these reports are

use to gain valuable information.

Kinds of management accounting report - There are various management accounting

reports that are given below -

3

As Oak cash and Carry is a small firm and that are used to manage ordering and sales

supply chain because it gives a clear statistics about availability of products.

Price optimization system – This is one of the crucial system for company because after

investing money on product. The firm needs to optimize price of finished goods that is

beneficial for firm and satisfactory for customers as well (Hoque, 2011) . For an example,

Oak cash and Carry is a wholesaler that provides finished goods to their clients and they

have spend money on production. These goods should have value for customer and in

order to provide products to customers they needs to measure total cost of product. So

that they can manage their investment and customer satisfaction level through identifying

their purchasing behavior and capacity. Thus, this price optimization system is used to

manage price according to customers and firm so that it can conduct business in an

appropriate manner.

All of these management accounting systems are required for different purpose such as

cost accounting is used to analyse actual cost of products. Job costing is require to monitor the

cost of goods that can be control according to the customer needs. It includes labor per hour cost,

equipment and machinery investment, etc. Inventory management system is used to watch stored

goods and products that are essential for Oak cash and Carry. Price optimization is used to

provide a price of a product that is profitable for firm and customer as well (Busco and Scapens,

2011) .

P2 Explain different methods used for management accounting reporting.

Management accounting reports are use for planning, regulating, decision making and

measuring performance. These reports are developing by various sections of an organization

throughout accounting and bookkeeping year. The major objective of developing these reports is

that crucial decisions depends on the accuracy and authenticity of these books. Manager

accounting officer of Oak cash and Carry analyses this information and then these reports are

use to gain valuable information.

Kinds of management accounting report - There are various management accounting

reports that are given below -

3

Budget report – This is used to analyse the performance of business organization.

Budget report is managed by every company whether that is a small or a large

organization. In a small firm budget is prepared as a whole whereas large organizations

develops department wise budget. Oak cash and Carry is small firm that needs to prepare

a whole budget that covers the source of earnings and expenditure. Firm's budget is based

on previous year if there is some issues in past year then it needs to estimate accurate

budget that can give a better output for current year (Granlund, 2011) .

Accounts receivable reports – These reports are used to manage cash flow in a business.

For instance, if Oak cash and Carry sales their goods on credit to their customers. Then,

they manages a report to receive cash against the product but if credit limit exceeds for

30 days , 60 days and 90 day. Manager can find out problems in collection process that

needs improvement to run a business effectively. Accounts receivable reports plays a

crucial report to cater information about the customers dues that needs to be clear on

time. So that firm can conduct its business efficiently and in order to perform well the

business needs to change credit policies. The firm can also analyse these accounts

receivable reports periodically so that it can reduce credit issues that can impact on its

process if it monitored in the end of financial year (Faÿ, Introna and Puyou, 2010) .

Inventory management report – It is valuable for such firms which produces physical

products, it is valuable for especially those which have less manufacturing risk factors.

This is used to support centralize data on inventory costs, labor, and other overheads that

includes production process, raw material to optimize machining. As Oak cash and Carry

is small business that maintains physical inventory to supply products in market then it is

beneficial and efficient for it. It consists of inventory waste, hourly labor cost and per

unit overhead costs. Management accounts officer can compare this with with other

assembly line of the organization so that they can identify areas of improvement.

Performance report – These reports are created to scale performance of company and

employees as well. In the year ending, organizations prepares departmental performance

reports so that owners can analyse performance of each section with respect to company.

These reports will assists in to develop strategic decision that can aid to support for the

future growth. Oak cash and Carry can measure their performance in order to identify

company performance and it can also awards their employees for their working process.

4

Budget report is managed by every company whether that is a small or a large

organization. In a small firm budget is prepared as a whole whereas large organizations

develops department wise budget. Oak cash and Carry is small firm that needs to prepare

a whole budget that covers the source of earnings and expenditure. Firm's budget is based

on previous year if there is some issues in past year then it needs to estimate accurate

budget that can give a better output for current year (Granlund, 2011) .

Accounts receivable reports – These reports are used to manage cash flow in a business.

For instance, if Oak cash and Carry sales their goods on credit to their customers. Then,

they manages a report to receive cash against the product but if credit limit exceeds for

30 days , 60 days and 90 day. Manager can find out problems in collection process that

needs improvement to run a business effectively. Accounts receivable reports plays a

crucial report to cater information about the customers dues that needs to be clear on

time. So that firm can conduct its business efficiently and in order to perform well the

business needs to change credit policies. The firm can also analyse these accounts

receivable reports periodically so that it can reduce credit issues that can impact on its

process if it monitored in the end of financial year (Faÿ, Introna and Puyou, 2010) .

Inventory management report – It is valuable for such firms which produces physical

products, it is valuable for especially those which have less manufacturing risk factors.

This is used to support centralize data on inventory costs, labor, and other overheads that

includes production process, raw material to optimize machining. As Oak cash and Carry

is small business that maintains physical inventory to supply products in market then it is

beneficial and efficient for it. It consists of inventory waste, hourly labor cost and per

unit overhead costs. Management accounts officer can compare this with with other

assembly line of the organization so that they can identify areas of improvement.

Performance report – These reports are created to scale performance of company and

employees as well. In the year ending, organizations prepares departmental performance

reports so that owners can analyse performance of each section with respect to company.

These reports will assists in to develop strategic decision that can aid to support for the

future growth. Oak cash and Carry can measure their performance in order to identify

company performance and it can also awards their employees for their working process.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This is also beneficial to know the capabilities of company in details and it also recognize

facts that needs amendments. Hence, it plays a crucial role for firm to accurate measure

of business strategies that needs to attain mission of the organization (Dillard and

Roslender, 2011) .

These management accounting reports plays an important role to run a business in an

effective manner. As it support sin decision making process with analyzing details of each

section within an organization.

5

facts that needs amendments. Hence, it plays a crucial role for firm to accurate measure

of business strategies that needs to attain mission of the organization (Dillard and

Roslender, 2011) .

These management accounting reports plays an important role to run a business in an

effective manner. As it support sin decision making process with analyzing details of each

section within an organization.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M1

Management accounting system processes to prepare and provide timely financial and

statistical information to the management of a company so that their scheduled and short-term

managerial decisions can take place. MAS or management accounting system enables the

management to compare their accounts with original budgets or forecasting, resource

management, trend analysis, as well as highlight the area that requires attention due to variation

in debits and credits. MAS helps in record keeping, planning, control, and decision making. By

implementing MAS, Oak cash and carry can avail benefits of recording business transactions,

measuring results of financial changes, and formulating future expectations. The organisation

can also plan to collect cash, control stocks and expenses, ordinate and monitor performance and

gross margins. MAS provides smooth decision making for evaluation of market and product

profitability as well as efficiency of strategies and plan (Burritt, Schaltegger and Zvezdov, 2011)

.

D1

Management accounting systems is established to provide information, which can be

used by management to make efficient decisions. Manufacturing industries use this system for

costing and managing their manufacturing processes, whereas in hospitals these systems are used

to assist in insurance billing. Similarly management accounting reporting is a comprehensive

depiction of business performance financially. In Oak cash and carry, MAS processes to provide

relevant information of their financial situation to make fruitful decisions. And management

accounting reporting assist them in analysis their business performance. This report also provide

long term goals and objectives to the organisation (Parker, 2012).

TASK 2

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs.

Cost analysis can be define as a method to ascertain the cost of business operations

through fixed and variable assets. This estimated cost is used to analyse the production cost to

attain certain objectives and gaols of the organisation. The managers analyses input cost to gain

maximum production with availability of resources. Costing consists of several kinds of costs

6

Management accounting system processes to prepare and provide timely financial and

statistical information to the management of a company so that their scheduled and short-term

managerial decisions can take place. MAS or management accounting system enables the

management to compare their accounts with original budgets or forecasting, resource

management, trend analysis, as well as highlight the area that requires attention due to variation

in debits and credits. MAS helps in record keeping, planning, control, and decision making. By

implementing MAS, Oak cash and carry can avail benefits of recording business transactions,

measuring results of financial changes, and formulating future expectations. The organisation

can also plan to collect cash, control stocks and expenses, ordinate and monitor performance and

gross margins. MAS provides smooth decision making for evaluation of market and product

profitability as well as efficiency of strategies and plan (Burritt, Schaltegger and Zvezdov, 2011)

.

D1

Management accounting systems is established to provide information, which can be

used by management to make efficient decisions. Manufacturing industries use this system for

costing and managing their manufacturing processes, whereas in hospitals these systems are used

to assist in insurance billing. Similarly management accounting reporting is a comprehensive

depiction of business performance financially. In Oak cash and carry, MAS processes to provide

relevant information of their financial situation to make fruitful decisions. And management

accounting reporting assist them in analysis their business performance. This report also provide

long term goals and objectives to the organisation (Parker, 2012).

TASK 2

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs.

Cost analysis can be define as a method to ascertain the cost of business operations

through fixed and variable assets. This estimated cost is used to analyse the production cost to

attain certain objectives and gaols of the organisation. The managers analyses input cost to gain

maximum production with availability of resources. Costing consists of several kinds of costs

6

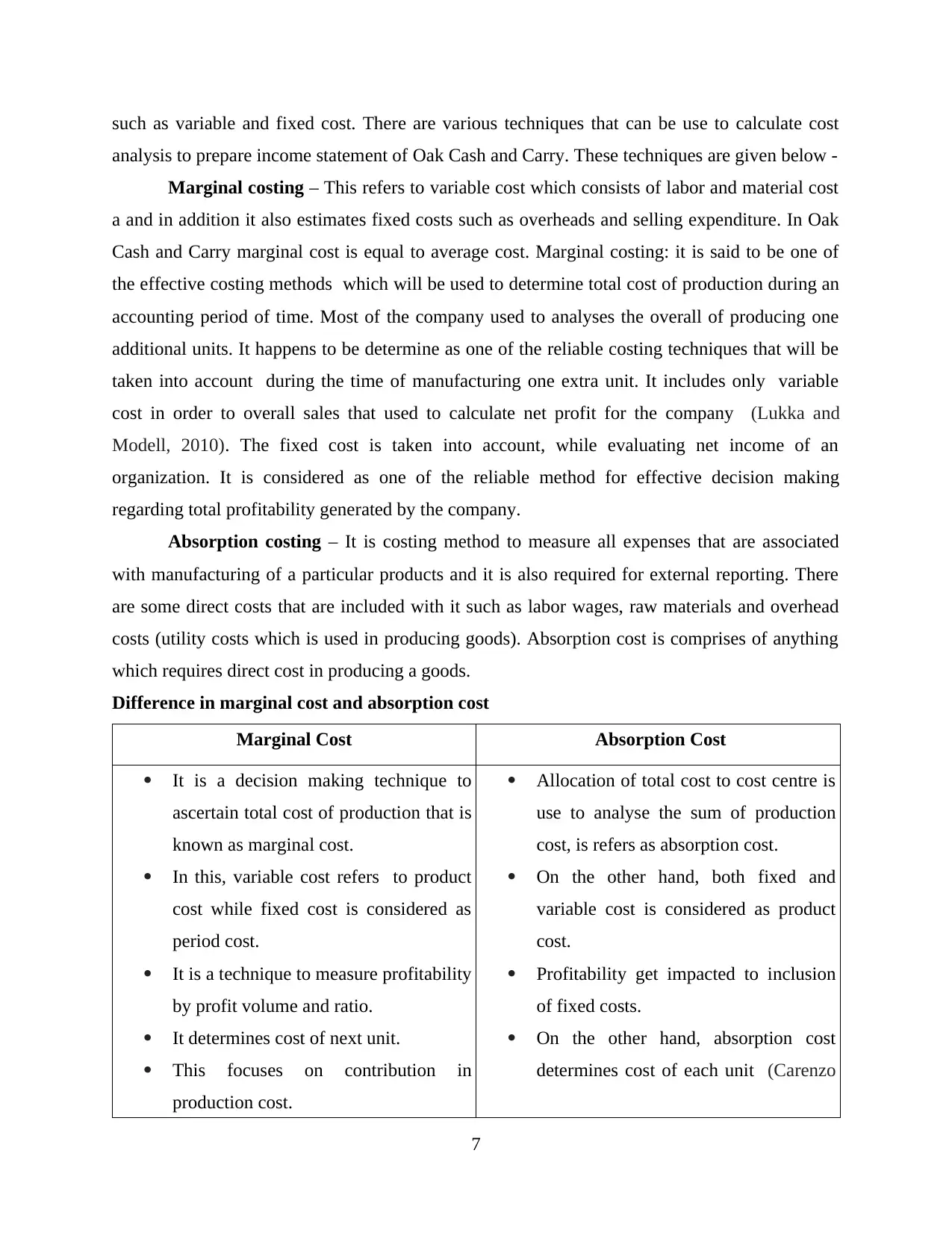

such as variable and fixed cost. There are various techniques that can be use to calculate cost

analysis to prepare income statement of Oak Cash and Carry. These techniques are given below -

Marginal costing – This refers to variable cost which consists of labor and material cost

a and in addition it also estimates fixed costs such as overheads and selling expenditure. In Oak

Cash and Carry marginal cost is equal to average cost. Marginal costing: it is said to be one of

the effective costing methods which will be used to determine total cost of production during an

accounting period of time. Most of the company used to analyses the overall of producing one

additional units. It happens to be determine as one of the reliable costing techniques that will be

taken into account during the time of manufacturing one extra unit. It includes only variable

cost in order to overall sales that used to calculate net profit for the company (Lukka and

Modell, 2010). The fixed cost is taken into account, while evaluating net income of an

organization. It is considered as one of the reliable method for effective decision making

regarding total profitability generated by the company.

Absorption costing – It is costing method to measure all expenses that are associated

with manufacturing of a particular products and it is also required for external reporting. There

are some direct costs that are included with it such as labor wages, raw materials and overhead

costs (utility costs which is used in producing goods). Absorption cost is comprises of anything

which requires direct cost in producing a goods.

Difference in marginal cost and absorption cost

Marginal Cost Absorption Cost

It is a decision making technique to

ascertain total cost of production that is

known as marginal cost.

In this, variable cost refers to product

cost while fixed cost is considered as

period cost.

It is a technique to measure profitability

by profit volume and ratio.

It determines cost of next unit.

This focuses on contribution in

production cost.

Allocation of total cost to cost centre is

use to analyse the sum of production

cost, is refers as absorption cost.

On the other hand, both fixed and

variable cost is considered as product

cost.

Profitability get impacted to inclusion

of fixed costs.

On the other hand, absorption cost

determines cost of each unit (Carenzo

7

analysis to prepare income statement of Oak Cash and Carry. These techniques are given below -

Marginal costing – This refers to variable cost which consists of labor and material cost

a and in addition it also estimates fixed costs such as overheads and selling expenditure. In Oak

Cash and Carry marginal cost is equal to average cost. Marginal costing: it is said to be one of

the effective costing methods which will be used to determine total cost of production during an

accounting period of time. Most of the company used to analyses the overall of producing one

additional units. It happens to be determine as one of the reliable costing techniques that will be

taken into account during the time of manufacturing one extra unit. It includes only variable

cost in order to overall sales that used to calculate net profit for the company (Lukka and

Modell, 2010). The fixed cost is taken into account, while evaluating net income of an

organization. It is considered as one of the reliable method for effective decision making

regarding total profitability generated by the company.

Absorption costing – It is costing method to measure all expenses that are associated

with manufacturing of a particular products and it is also required for external reporting. There

are some direct costs that are included with it such as labor wages, raw materials and overhead

costs (utility costs which is used in producing goods). Absorption cost is comprises of anything

which requires direct cost in producing a goods.

Difference in marginal cost and absorption cost

Marginal Cost Absorption Cost

It is a decision making technique to

ascertain total cost of production that is

known as marginal cost.

In this, variable cost refers to product

cost while fixed cost is considered as

period cost.

It is a technique to measure profitability

by profit volume and ratio.

It determines cost of next unit.

This focuses on contribution in

production cost.

Allocation of total cost to cost centre is

use to analyse the sum of production

cost, is refers as absorption cost.

On the other hand, both fixed and

variable cost is considered as product

cost.

Profitability get impacted to inclusion

of fixed costs.

On the other hand, absorption cost

determines cost of each unit (Carenzo

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and Turolla, 2010) .

Whereas it shows forth and accuracy

and fair treatment of product cost.

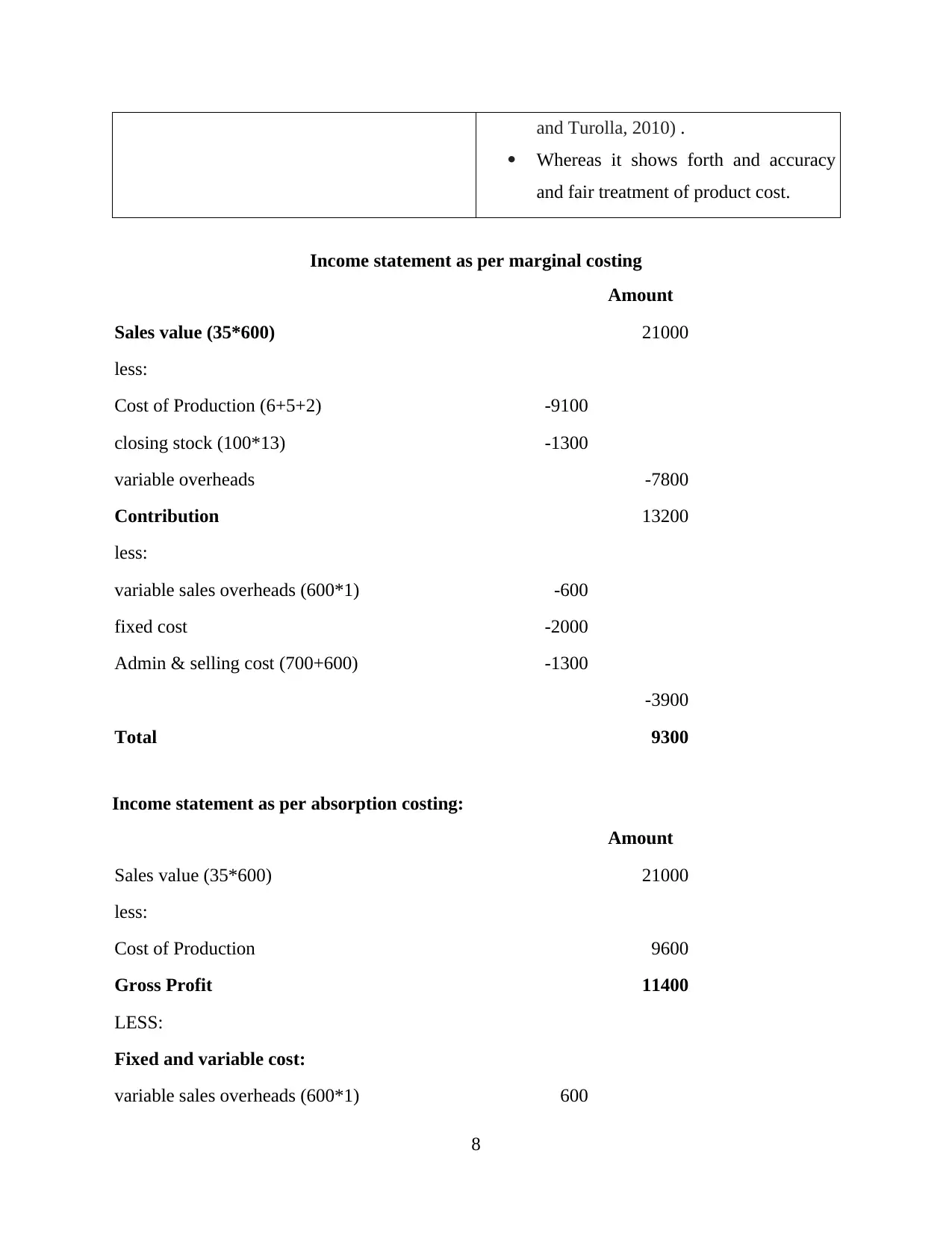

Income statement as per marginal costing

Amount

Sales value (35*600) 21000

less:

Cost of Production (6+5+2) -9100

closing stock (100*13) -1300

variable overheads -7800

Contribution 13200

less:

variable sales overheads (600*1) -600

fixed cost -2000

Admin & selling cost (700+600) -1300

-3900

Total 9300

Income statement as per absorption costing:

Amount

Sales value (35*600) 21000

less:

Cost of Production 9600

Gross Profit 11400

LESS:

Fixed and variable cost:

variable sales overheads (600*1) 600

8

Whereas it shows forth and accuracy

and fair treatment of product cost.

Income statement as per marginal costing

Amount

Sales value (35*600) 21000

less:

Cost of Production (6+5+2) -9100

closing stock (100*13) -1300

variable overheads -7800

Contribution 13200

less:

variable sales overheads (600*1) -600

fixed cost -2000

Admin & selling cost (700+600) -1300

-3900

Total 9300

Income statement as per absorption costing:

Amount

Sales value (35*600) 21000

less:

Cost of Production 9600

Gross Profit 11400

LESS:

Fixed and variable cost:

variable sales overheads (600*1) 600

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Admin & selling cost (700+600) 1300

Less: over absorbed fixed production overheads -100 -1800

Net profit 9600

M2

Management accounting techniques are planning and budgeting, project decision making,

measuring performance and revaluation of accounting. Where planning and budgeting consists of

analysis of weekly and monthly budget to forecast pricing and sell of products. Project decision

making is a step involves decision-making of relevant costing to gain benefits and margin on

products. Measuring performance is used to compare actual results with standard results planned

in budgeting phase.

Sept Oct Nov Dec Jan

Receipts £ £ £ £ £

Cash sales 250 350 255 380 450

Credit sale receipts from

debtors 320 150 100 120 220

Other income received 415 430 320 215 330

Total receipts (a) 985 930 675 715 1000

Payments

Purchases 215 260 290 330 415

Wages- Labour and

overheads 115 90 180 210 150

Fixed costs 200 200 200 200 200

Capital expenditure - Plant 650

Advertising 20 35 55 75 90

Total Payments (b) 1200 585 725 815 855

Surplus/Deficit (a) – (b) -215 345 -50 -100 145

D2

9

Less: over absorbed fixed production overheads -100 -1800

Net profit 9600

M2

Management accounting techniques are planning and budgeting, project decision making,

measuring performance and revaluation of accounting. Where planning and budgeting consists of

analysis of weekly and monthly budget to forecast pricing and sell of products. Project decision

making is a step involves decision-making of relevant costing to gain benefits and margin on

products. Measuring performance is used to compare actual results with standard results planned

in budgeting phase.

Sept Oct Nov Dec Jan

Receipts £ £ £ £ £

Cash sales 250 350 255 380 450

Credit sale receipts from

debtors 320 150 100 120 220

Other income received 415 430 320 215 330

Total receipts (a) 985 930 675 715 1000

Payments

Purchases 215 260 290 330 415

Wages- Labour and

overheads 115 90 180 210 150

Fixed costs 200 200 200 200 200

Capital expenditure - Plant 650

Advertising 20 35 55 75 90

Total Payments (b) 1200 585 725 815 855

Surplus/Deficit (a) – (b) -215 345 -50 -100 145

D2

9

From the above mention income statement it has been identified that , according to the

marginal costing income generated is 9300. whereas on the other hand, income statement as per

the absorption cost generate 9600. Difference between cost of the both is 300 occurring because

in absorption fixed cost is included. This is the main reason of difference in the amount of

income statement.;

TASK 3

P4 Advantages and disadvantages of different types of planning tools for budgetary control

Budget can be described as a financial plan which is build up for a particular period of time. It

basically include sales volume, revenues, resources quantities, costs or expenses, assets,

liabilities and cash flows. Moreover, it is very necessary to make an appropriate budget to

conduct different kinds of operations through spending desired funds to fulfill goals or objectives

of business successfully. In case of Oak & Cash Carry, they should make required budget to

manage overall available funds to various types of operational activities or procedures to

generate better outcomes and earn profits.

Budget control – This can be explained as a system of management control which

provide support to compare actual income and spending with the plan of the same. It helps to

determine differences between real expenses & earnings with planned cost and profits so that

required steps can be taken by selected firm in order to control overall budget of business.

Planning tools – In this part, several planning tools and techniques of budget are include

which can be utilized by give company (Soin and Collier, 2013) . These are described here with

their advantages and disadvantages -

Forecasting – This include to analyze previous data of making budget for particular

company and through following that along with fulfilling present requirements. Moreover, the

past information or trend of establishing budget will be considered as bench mark and to

complete current desires, an appropriate budget will organized. the desired budget will build up. Advantage – It is helpful to follow previous trend of company and support to predict

changes, flexibility & ambiguity.

Disadvantage – This include judgmental approach and risk of false information may

possible which results into inappropriate plan.

10

marginal costing income generated is 9300. whereas on the other hand, income statement as per

the absorption cost generate 9600. Difference between cost of the both is 300 occurring because

in absorption fixed cost is included. This is the main reason of difference in the amount of

income statement.;

TASK 3

P4 Advantages and disadvantages of different types of planning tools for budgetary control

Budget can be described as a financial plan which is build up for a particular period of time. It

basically include sales volume, revenues, resources quantities, costs or expenses, assets,

liabilities and cash flows. Moreover, it is very necessary to make an appropriate budget to

conduct different kinds of operations through spending desired funds to fulfill goals or objectives

of business successfully. In case of Oak & Cash Carry, they should make required budget to

manage overall available funds to various types of operational activities or procedures to

generate better outcomes and earn profits.

Budget control – This can be explained as a system of management control which

provide support to compare actual income and spending with the plan of the same. It helps to

determine differences between real expenses & earnings with planned cost and profits so that

required steps can be taken by selected firm in order to control overall budget of business.

Planning tools – In this part, several planning tools and techniques of budget are include

which can be utilized by give company (Soin and Collier, 2013) . These are described here with

their advantages and disadvantages -

Forecasting – This include to analyze previous data of making budget for particular

company and through following that along with fulfilling present requirements. Moreover, the

past information or trend of establishing budget will be considered as bench mark and to

complete current desires, an appropriate budget will organized. the desired budget will build up. Advantage – It is helpful to follow previous trend of company and support to predict

changes, flexibility & ambiguity.

Disadvantage – This include judgmental approach and risk of false information may

possible which results into inappropriate plan.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.