Financial Analysis of Ocado Group, Budgeting and Investment Appraisal

VerifiedAdded on 2022/02/07

|17

|4453

|42

Report

AI Summary

This report, prepared for a Finance for Decision Making module, conducts a financial analysis of the Ocado Group, a UK-based technology company. It begins with an assessment of the company's financial performance using ratio analysis, evaluating profitability, efficiency, liquidity, and gearing ratios over a five-year period. The analysis highlights the impact of the COVID-19 pandemic on the company's financial standing. The report then explores the advantages and disadvantages of budgeting, emphasizing its role in resource allocation, strategic planning, and performance evaluation. It also examines different approaches to financial planning, including incremental and zero-based budgeting, and underscores the importance of performance management in effective decision-making. Finally, the report critically evaluates investment opportunities using Net Present Value (NPV) and Internal Rate of Return (IRR) techniques, considering the risks and uncertainties associated with investment appraisal. The report concludes with a summary of the key findings and recommendations for the company's financial strategies.

Name of Module:

MOD007667 Finance for Decision Making

SID Number:

Title of Your Course and Year/Stage: Final Submission Date:

Actual word count: Extension Granted to (if any):

Checklist before submission

1. Have you read, understood and acted in accordance with the referencing guidelines set

out in the Harvard Reference Guide?

2. Where you have quoted directly from or where you have paraphrased the work of others,

have you acknowledged and appropriately referenced the source of your quotation in the

body of the text?

3. Have you placed all direct quotations in inverted commas?

4. Have you listed and correctly presented all your sources in the reference list?

Declaration by the candidate

1. I declare that this assignment is my own work (or, in the case of a group assignment, the

work of my group), that it has not been copied from elsewhere and that any extracts from

books, papers or other sources have been properly acknowledged as references or

quotations.

2. The work contains no material drawn from unattributed sources.

Please tick the box to confirm acceptance of the above declaration.

Date ________________________

Signature ________________________

MOD007667 Finance for Decision Making

SID Number:

Title of Your Course and Year/Stage: Final Submission Date:

Actual word count: Extension Granted to (if any):

Checklist before submission

1. Have you read, understood and acted in accordance with the referencing guidelines set

out in the Harvard Reference Guide?

2. Where you have quoted directly from or where you have paraphrased the work of others,

have you acknowledged and appropriately referenced the source of your quotation in the

body of the text?

3. Have you placed all direct quotations in inverted commas?

4. Have you listed and correctly presented all your sources in the reference list?

Declaration by the candidate

1. I declare that this assignment is my own work (or, in the case of a group assignment, the

work of my group), that it has not been copied from elsewhere and that any extracts from

books, papers or other sources have been properly acknowledged as references or

quotations.

2. The work contains no material drawn from unattributed sources.

Please tick the box to confirm acceptance of the above declaration.

Date ________________________

Signature ________________________

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

1. Introduction..............................................................................................................................3

2. Financial Analysis of Ocado group..........................................................................................3

2.1 Problems Associated with Financial Ratios..........................................................................6

3. Advantages and Disadvantages of Budgeting..........................................................................6

3.1 Approaches to Drawing up A Business Financial Plan....................................................8

3.2 Performance Management and Decision Making.............................................................8

4. Evaluating Capital Budgeting Approaches..............................................................................9

4.1 Net Present Value................................................................................................................10

4.2 Internal Rate of Return........................................................................................................11

4.3 Risk and Uncertainty in Investment Appraisal....................................................................12

5. Conclusion..............................................................................................................................12

Reference.......................................................................................................................................14

1. Introduction..............................................................................................................................3

2. Financial Analysis of Ocado group..........................................................................................3

2.1 Problems Associated with Financial Ratios..........................................................................6

3. Advantages and Disadvantages of Budgeting..........................................................................6

3.1 Approaches to Drawing up A Business Financial Plan....................................................8

3.2 Performance Management and Decision Making.............................................................8

4. Evaluating Capital Budgeting Approaches..............................................................................9

4.1 Net Present Value................................................................................................................10

4.2 Internal Rate of Return........................................................................................................11

4.3 Risk and Uncertainty in Investment Appraisal....................................................................12

5. Conclusion..............................................................................................................................12

Reference.......................................................................................................................................14

1. Introduction

Covid-19 poses significant challenges for the economies around the globe. Most of the

businesses are massively affected as they fail to deal with the rapid swings and demand and

supply disruptions (Beninger and Francis, 2021). Covid-19 has significantly impacted the

people’s living patterns. Post Covid-19 will have many consequences on the economies and on

the whole societies. People tend to become more interested in saving their money instead of

investing (Donthu and Gustafsson, 2020). There is a need arises for the businesses to reassess

their financing and investment policies to combat this pandemic situation and able to achieve and

enhance business financial gains (Shen et al., 2020).

Ocado group is a UK based Technology Company and provides innovative and unique end-to-

end online grocery solutions around the globe (Ocado, 2021). As a CFO of this company, I

evaluates the £50 million worth investment for the development of product post Covid-19. In

first section of this report, financial performance of Ocado group is assessed by conducting its

financial ratios analysis. Secondly, this report presents the merits and demerits of budgeting and

importance of performance management in effective decision making of an organization. Third

section critically evaluates the investment opportunity by utilizing two major investment

appraisal techniques (NPV and IRR).

2. Financial Analysis of Ocado group

Ocado group is basically a global technology-led company was founded in April, 2000 and

headquartered in Hatfield, United Kingdom. It provides online retailers with unique and

innovative solutions related to software development, robotics and automation systems

worldwide. Ocado group earn a net income of £ 69.6 million in financial year 2020 (Ocado,

Covid-19 poses significant challenges for the economies around the globe. Most of the

businesses are massively affected as they fail to deal with the rapid swings and demand and

supply disruptions (Beninger and Francis, 2021). Covid-19 has significantly impacted the

people’s living patterns. Post Covid-19 will have many consequences on the economies and on

the whole societies. People tend to become more interested in saving their money instead of

investing (Donthu and Gustafsson, 2020). There is a need arises for the businesses to reassess

their financing and investment policies to combat this pandemic situation and able to achieve and

enhance business financial gains (Shen et al., 2020).

Ocado group is a UK based Technology Company and provides innovative and unique end-to-

end online grocery solutions around the globe (Ocado, 2021). As a CFO of this company, I

evaluates the £50 million worth investment for the development of product post Covid-19. In

first section of this report, financial performance of Ocado group is assessed by conducting its

financial ratios analysis. Secondly, this report presents the merits and demerits of budgeting and

importance of performance management in effective decision making of an organization. Third

section critically evaluates the investment opportunity by utilizing two major investment

appraisal techniques (NPV and IRR).

2. Financial Analysis of Ocado group

Ocado group is basically a global technology-led company was founded in April, 2000 and

headquartered in Hatfield, United Kingdom. It provides online retailers with unique and

innovative solutions related to software development, robotics and automation systems

worldwide. Ocado group earn a net income of £ 69.6 million in financial year 2020 (Ocado,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

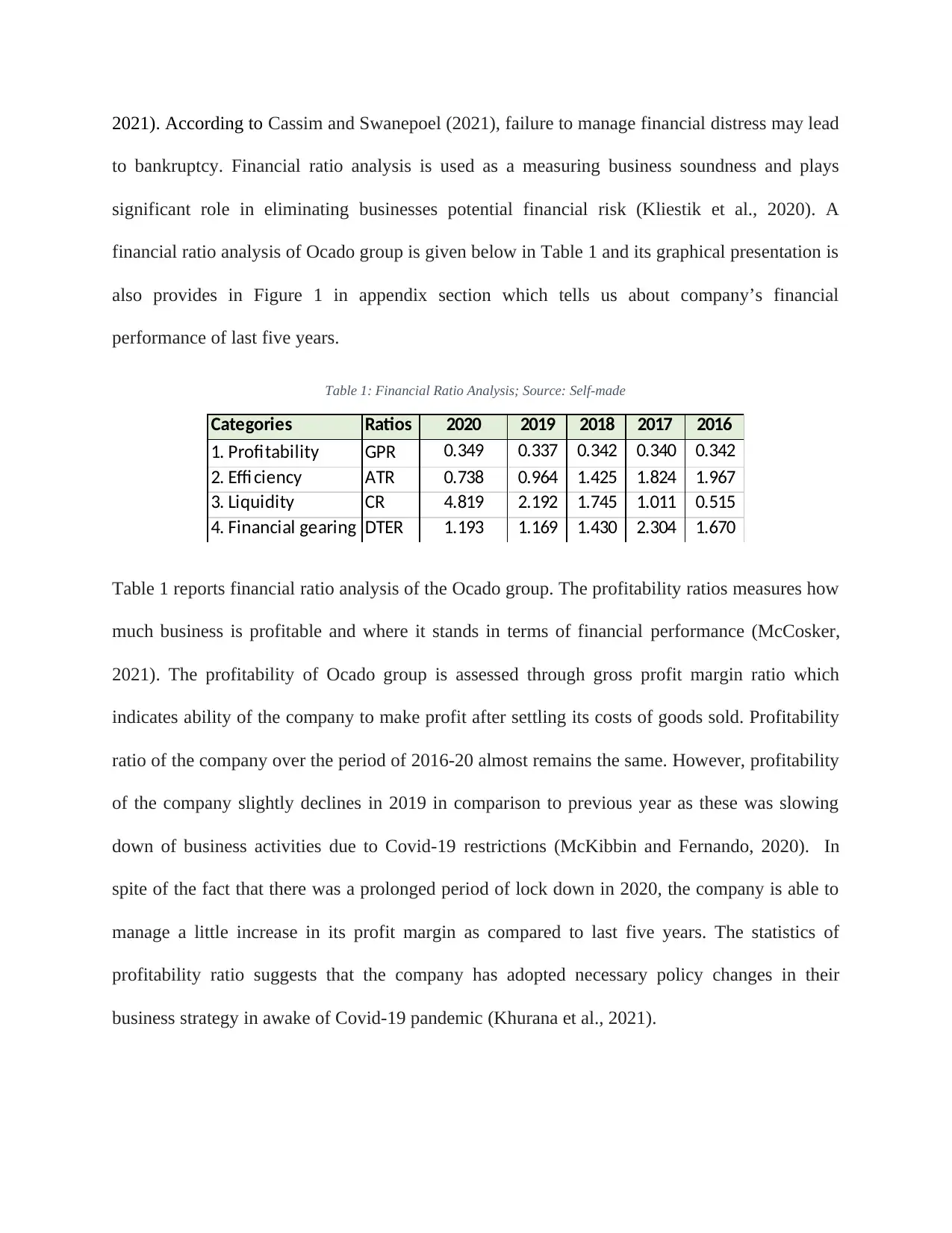

2021). According to Cassim and Swanepoel (2021), failure to manage financial distress may lead

to bankruptcy. Financial ratio analysis is used as a measuring business soundness and plays

significant role in eliminating businesses potential financial risk (Kliestik et al., 2020). A

financial ratio analysis of Ocado group is given below in Table 1 and its graphical presentation is

also provides in Figure 1 in appendix section which tells us about company’s financial

performance of last five years.

Table 1: Financial Ratio Analysis; Source: Self-made

Categories Ratios 2020 2019 2018 2017 2016

1. Profitability GPR 0.349 0.337 0.342 0.340 0.342

2. Effi ciency ATR 0.738 0.964 1.425 1.824 1.967

3. Liquidity CR 4.819 2.192 1.745 1.011 0.515

4. Financial gearing DTER 1.193 1.169 1.430 2.304 1.670

Table 1 reports financial ratio analysis of the Ocado group. The profitability ratios measures how

much business is profitable and where it stands in terms of financial performance (McCosker,

2021). The profitability of Ocado group is assessed through gross profit margin ratio which

indicates ability of the company to make profit after settling its costs of goods sold. Profitability

ratio of the company over the period of 2016-20 almost remains the same. However, profitability

of the company slightly declines in 2019 in comparison to previous year as these was slowing

down of business activities due to Covid-19 restrictions (McKibbin and Fernando, 2020). In

spite of the fact that there was a prolonged period of lock down in 2020, the company is able to

manage a little increase in its profit margin as compared to last five years. The statistics of

profitability ratio suggests that the company has adopted necessary policy changes in their

business strategy in awake of Covid-19 pandemic (Khurana et al., 2021).

to bankruptcy. Financial ratio analysis is used as a measuring business soundness and plays

significant role in eliminating businesses potential financial risk (Kliestik et al., 2020). A

financial ratio analysis of Ocado group is given below in Table 1 and its graphical presentation is

also provides in Figure 1 in appendix section which tells us about company’s financial

performance of last five years.

Table 1: Financial Ratio Analysis; Source: Self-made

Categories Ratios 2020 2019 2018 2017 2016

1. Profitability GPR 0.349 0.337 0.342 0.340 0.342

2. Effi ciency ATR 0.738 0.964 1.425 1.824 1.967

3. Liquidity CR 4.819 2.192 1.745 1.011 0.515

4. Financial gearing DTER 1.193 1.169 1.430 2.304 1.670

Table 1 reports financial ratio analysis of the Ocado group. The profitability ratios measures how

much business is profitable and where it stands in terms of financial performance (McCosker,

2021). The profitability of Ocado group is assessed through gross profit margin ratio which

indicates ability of the company to make profit after settling its costs of goods sold. Profitability

ratio of the company over the period of 2016-20 almost remains the same. However, profitability

of the company slightly declines in 2019 in comparison to previous year as these was slowing

down of business activities due to Covid-19 restrictions (McKibbin and Fernando, 2020). In

spite of the fact that there was a prolonged period of lock down in 2020, the company is able to

manage a little increase in its profit margin as compared to last five years. The statistics of

profitability ratio suggests that the company has adopted necessary policy changes in their

business strategy in awake of Covid-19 pandemic (Khurana et al., 2021).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The second category is of efficiency ratio. Efficiency ratio discusses how well the company is

managing its assets as well as liabilities. Here, asset turnover ratio is employed to compute the

business efficiency. Asset turnover ratio suggests that how much revenue the company earns by

efficiently manage its assets (McCosker, 2021). Statistics reported in Table 1 indicate that the

company asset turnover ratio is quite alarming as shows a decreasing trend over the last five

years which means that the company is inefficiently controlling its assets. As the declining asset

turnover ratio suggests that the business has excess of production but its collection practices and

inventory management is poor which gives bad signal to the investors about the company (Irman

and Purwati, 2020).

After evaluating the efficiency of the company, we analyse its liquidity. Liquidity is measured

with current ratio which indicates that how well the company manages its current assets in

relation to current liabilities and meet its short term loans through sale of its current assets and

higher ratio is mostly preferred and desirable by the companies (McCosker, 2021). It is indicated

that Ocado group performs significantly well in term of managing its short term assets and

liabilities. As the statistics in the Table 1 reflects the increasing trend of the company’s current

ratio. Findings indicate that Ocado group is efficiently repaying its current obligations by

utilizing its current assets even during the pandemic. In 2020, the company reports all time

highest current ratio during the last five years which is 4.819 as compared to previous 2.192

which may be due to the fact that the companies larger in size are more resilient to crisis shocks

(Song et al., 2021).

At last, financial gearing ratio of the company is computed using debt to equity ratio which tells

that how much finance the company has raised through debt and equity. Firms with higher debt

to equity ratio are at higher risk of becoming bankrupt. Debt to equity ratio of Ocado group is

managing its assets as well as liabilities. Here, asset turnover ratio is employed to compute the

business efficiency. Asset turnover ratio suggests that how much revenue the company earns by

efficiently manage its assets (McCosker, 2021). Statistics reported in Table 1 indicate that the

company asset turnover ratio is quite alarming as shows a decreasing trend over the last five

years which means that the company is inefficiently controlling its assets. As the declining asset

turnover ratio suggests that the business has excess of production but its collection practices and

inventory management is poor which gives bad signal to the investors about the company (Irman

and Purwati, 2020).

After evaluating the efficiency of the company, we analyse its liquidity. Liquidity is measured

with current ratio which indicates that how well the company manages its current assets in

relation to current liabilities and meet its short term loans through sale of its current assets and

higher ratio is mostly preferred and desirable by the companies (McCosker, 2021). It is indicated

that Ocado group performs significantly well in term of managing its short term assets and

liabilities. As the statistics in the Table 1 reflects the increasing trend of the company’s current

ratio. Findings indicate that Ocado group is efficiently repaying its current obligations by

utilizing its current assets even during the pandemic. In 2020, the company reports all time

highest current ratio during the last five years which is 4.819 as compared to previous 2.192

which may be due to the fact that the companies larger in size are more resilient to crisis shocks

(Song et al., 2021).

At last, financial gearing ratio of the company is computed using debt to equity ratio which tells

that how much finance the company has raised through debt and equity. Firms with higher debt

to equity ratio are at higher risk of becoming bankrupt. Debt to equity ratio of Ocado group is

keep on changing every year as indicated in the Table 1. Results revealed that the company has

slightly increases the debt financing in 2020 which means that they have taken more debt in 2020

as compared to 2019. Higher debt ratio is the indication of the company’s inability to raise cash

through equity investment in this current scenario of Covid-19 epidemic (Demmou et al., 2021).

2.1 Problems Associated with Financial Ratios

Although, financial ratio analysis is an effective tool to observe and identify issues related to

financial performance of the company by comparing its current performance with the previous

results. It has also some drawbacks as well which are discussed below:

Considers Historical Data: One of the problem associated with the financial ratios is

that the information used in computation of ratios is not current instead the analysis

requires historical information to analyse firm’s current performance and to predict future

decisions of the firms (Faello, 2015).

Avoid External Factors: Another limitation of the ratio analysis is that it doesn’t

consider the external factors effect in the analysis such as inflationary or deflationary

effects. As the data is collected from financial statements of companies which are

periodically released and changes in the prices occurred during the period are not

incorporated in the financial figures.

Financial Statistics Manipulation: According to Zainudin and Hashim (2016), the most

important problem related with financial ratios analysis is that information used in

analysis is based on financial statements statistics which can be manipulated to better

reflect company position.

slightly increases the debt financing in 2020 which means that they have taken more debt in 2020

as compared to 2019. Higher debt ratio is the indication of the company’s inability to raise cash

through equity investment in this current scenario of Covid-19 epidemic (Demmou et al., 2021).

2.1 Problems Associated with Financial Ratios

Although, financial ratio analysis is an effective tool to observe and identify issues related to

financial performance of the company by comparing its current performance with the previous

results. It has also some drawbacks as well which are discussed below:

Considers Historical Data: One of the problem associated with the financial ratios is

that the information used in computation of ratios is not current instead the analysis

requires historical information to analyse firm’s current performance and to predict future

decisions of the firms (Faello, 2015).

Avoid External Factors: Another limitation of the ratio analysis is that it doesn’t

consider the external factors effect in the analysis such as inflationary or deflationary

effects. As the data is collected from financial statements of companies which are

periodically released and changes in the prices occurred during the period are not

incorporated in the financial figures.

Financial Statistics Manipulation: According to Zainudin and Hashim (2016), the most

important problem related with financial ratios analysis is that information used in

analysis is based on financial statements statistics which can be manipulated to better

reflect company position.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. Advantages and Disadvantages of Budgeting

Budgeting is basically a process of estimating company’s income and expenditure over a

particular time period and preparing a proper written plan for its future operations. Businesses

often uses budgeting to assess various operations of the business and helps those in making

effective financial decisions. There are several advantages of preparing budget such as allocation

and reallocation of resources, coordinating business operations across departments and

converting strategic plans into action. Besides, budgeting also helps the company’s management

in planning orientation and urges them to think longer-term instead managing short term

business operations (MJO, 2021). Another merit of budgeting is that it enables the businesses to

look into its financial statistics of the over the period of time to assess which business activities

are helpful in generating revenues and which ones only use it so the management may drop some

unfavourable business activities. Preparing a structured budget guide business in funds planning

such as if little cash amount is in hand to invest in working capital, budgeting help management

in deciding which assets are worth investing (Schuster, Heinemann and Cleary, 2021). It further

helps in evaluating current performance of the business and making estimates for the next year.

On the contrary, there are some demerits of budgeting as well, the major drawback of budgeting

is that this process is very time consuming particularly for the organization that is poorly

governed and if the organization is intended to prepare participative budget. While preparing the

budget, it is possible that manager may deliberately create budgetary slack by changing the

revenue and expenditure estimates over a specific time period to get favourable variances against

the budget which is also a very serious concern. Another limitation of budgeting is rigidity such

as if a company is preparing its budgeting estimates annually and decides to strictly focus on the

outline described in their budgets for the whole next year may not considers the changing market

Budgeting is basically a process of estimating company’s income and expenditure over a

particular time period and preparing a proper written plan for its future operations. Businesses

often uses budgeting to assess various operations of the business and helps those in making

effective financial decisions. There are several advantages of preparing budget such as allocation

and reallocation of resources, coordinating business operations across departments and

converting strategic plans into action. Besides, budgeting also helps the company’s management

in planning orientation and urges them to think longer-term instead managing short term

business operations (MJO, 2021). Another merit of budgeting is that it enables the businesses to

look into its financial statistics of the over the period of time to assess which business activities

are helpful in generating revenues and which ones only use it so the management may drop some

unfavourable business activities. Preparing a structured budget guide business in funds planning

such as if little cash amount is in hand to invest in working capital, budgeting help management

in deciding which assets are worth investing (Schuster, Heinemann and Cleary, 2021). It further

helps in evaluating current performance of the business and making estimates for the next year.

On the contrary, there are some demerits of budgeting as well, the major drawback of budgeting

is that this process is very time consuming particularly for the organization that is poorly

governed and if the organization is intended to prepare participative budget. While preparing the

budget, it is possible that manager may deliberately create budgetary slack by changing the

revenue and expenditure estimates over a specific time period to get favourable variances against

the budget which is also a very serious concern. Another limitation of budgeting is rigidity such

as if a company is preparing its budgeting estimates annually and decides to strictly focus on the

outline described in their budgets for the whole next year may not considers the changing market

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

circumstances which can be a potential problem for the company. In addition, managers of

different departments also blames each other departments if they failed to achieve the expected

outcomes (MJO, 2021).

3.1 Approaches to Drawing up A Business Financial Plan

This report considers two critical approaches to prepare the business financial plans which are

incremental budgeting and zero-based budgeting techniques each having its own pros and cons.

While preparing the budget for next period, these budgets requires either the actual data and

figures or the estimates of the pervious budget. Businesses mostly prefer the preparation of an

incremental budget as this budgeting approach requires only little addition in the existing budget

to make a new budget estimate. On the other hand, zero-based budgeting requires no previous

budgeting estimates as it is prepared from the zero base (Ouassini, 2018). Incremental budget is

widely used by organizations however some businesses makes budgeting estimates using zero-

based budgeting. Zero-based budgets are mostly used to make estimates at the strategic level and

requires more time and resources. In contrast, incremental budgets mostly focuses on short term

day to day activities which usually do not take much time and expertise. Besides, zero-based

budgets are mostly prepared by larger organizations while, small and medium sized companies

prefer the estimation of incremental budget. In short, budgeting estimation either incremental of

zero-based is necessary for the companies to efficiently run their businesses efficiently (TWEN,

2021).

3.2 Performance Management and Decision Making

Management of the organization can make better decisions with the help of performance

management. Performance management is a continuously evolving process of enhancing

performance by setting and aligning individual and team goals with long term goals and

different departments also blames each other departments if they failed to achieve the expected

outcomes (MJO, 2021).

3.1 Approaches to Drawing up A Business Financial Plan

This report considers two critical approaches to prepare the business financial plans which are

incremental budgeting and zero-based budgeting techniques each having its own pros and cons.

While preparing the budget for next period, these budgets requires either the actual data and

figures or the estimates of the pervious budget. Businesses mostly prefer the preparation of an

incremental budget as this budgeting approach requires only little addition in the existing budget

to make a new budget estimate. On the other hand, zero-based budgeting requires no previous

budgeting estimates as it is prepared from the zero base (Ouassini, 2018). Incremental budget is

widely used by organizations however some businesses makes budgeting estimates using zero-

based budgeting. Zero-based budgets are mostly used to make estimates at the strategic level and

requires more time and resources. In contrast, incremental budgets mostly focuses on short term

day to day activities which usually do not take much time and expertise. Besides, zero-based

budgets are mostly prepared by larger organizations while, small and medium sized companies

prefer the estimation of incremental budget. In short, budgeting estimation either incremental of

zero-based is necessary for the companies to efficiently run their businesses efficiently (TWEN,

2021).

3.2 Performance Management and Decision Making

Management of the organization can make better decisions with the help of performance

management. Performance management is a continuously evolving process of enhancing

performance by setting and aligning individual and team goals with long term goals and

objectives of the organizations, planning for the performance to reach the goals, reviewing and

evaluating the progress and empowering people’ knowledge, skills and abilities (Li et al., 2018).

Performance management is linked to the decision making of the firms. If performance

management process is effectively and efficiently designed and implemented, it can lead to better

decision making by firms. Performance management can also be used as a tool to early identify

the potential problems associated with the businesses and helps managers to take necessary

corrective actions timely and keeps the business on tract. Top management may drop some of the

company’s underperformed projects and start investments in profitable and innovative projects

by measuring its performance. Performance management system also helps in prioritizing

employee’s reward and recognition which ultimately motivate employees to perform their duties

well and leading to higher performance of the company (Mello and Thabayapelo, 2021).

4. Evaluating Capital Budgeting Approaches

Capital budgeting techniques are linked to long term capital investment decisions of the

businesses. Businesses uses different capital budgeting approaches to evaluate their various

projects while making important investment decisions. Two widely employed approaches of

investment appraisal by the businesses are NPV and IRR and both have some merits over the

other. Estimation of NPV requires present value of cash inflow and outflow and tells about

profitability of the project (Bosri, 2016). Businesses prefer to invest in projects having non

negative net present values. However, internal rate of returns is basically a return of an

investment underlying the concept of time value of money and Investors usually prefers to invest

in a project with higher internal return. Besides, both approaches involves calculation of future

cash flow estimation based on the historical information. Some companies prefer to use net

present value to evaluate their investments projects as it is easy to calculate. However, according

evaluating the progress and empowering people’ knowledge, skills and abilities (Li et al., 2018).

Performance management is linked to the decision making of the firms. If performance

management process is effectively and efficiently designed and implemented, it can lead to better

decision making by firms. Performance management can also be used as a tool to early identify

the potential problems associated with the businesses and helps managers to take necessary

corrective actions timely and keeps the business on tract. Top management may drop some of the

company’s underperformed projects and start investments in profitable and innovative projects

by measuring its performance. Performance management system also helps in prioritizing

employee’s reward and recognition which ultimately motivate employees to perform their duties

well and leading to higher performance of the company (Mello and Thabayapelo, 2021).

4. Evaluating Capital Budgeting Approaches

Capital budgeting techniques are linked to long term capital investment decisions of the

businesses. Businesses uses different capital budgeting approaches to evaluate their various

projects while making important investment decisions. Two widely employed approaches of

investment appraisal by the businesses are NPV and IRR and both have some merits over the

other. Estimation of NPV requires present value of cash inflow and outflow and tells about

profitability of the project (Bosri, 2016). Businesses prefer to invest in projects having non

negative net present values. However, internal rate of returns is basically a return of an

investment underlying the concept of time value of money and Investors usually prefers to invest

in a project with higher internal return. Besides, both approaches involves calculation of future

cash flow estimation based on the historical information. Some companies prefer to use net

present value to evaluate their investments projects as it is easy to calculate. However, according

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to Mubashar and Tariq (2019), most managers prefer internal rate of return as it makes

comparison with low and high discounting rates.

Considering that vaccination for the Covid-19 epidemic has already started worldwide, it is

expected that the world will be back on the tract as it was before this epidemic. According to

Arjunan (2019), majority of the big business such as Nike, Walmart, etc. are currently working

to develop and produce products and services for post Covid-19 period. In this regard,

management of the Ocado group is also interest in launching new product in the retail business

and the company has an investment of about 50 million pounds. This investment will cover the

expenses for development of new product and expenses for marketing and launching of the

product. I evaluated this investment using both of the above mentioned approaches as a CFO of

the Ocado group.

4.1 Net Present Value

It is the most preferable technique of capital budgeting employed by the company for making

important decision related to investment appraisal. It basically tells about the investments

profitability by calculating the variance in present value of cash inflow and cash outflow.

Projects having positive net present value are most desirable by the company but the projects

with negative net present value are unfavourable ones. Positive net present value implies that the

potential future returns from the project are greater than the present value of its cost (Mubashar

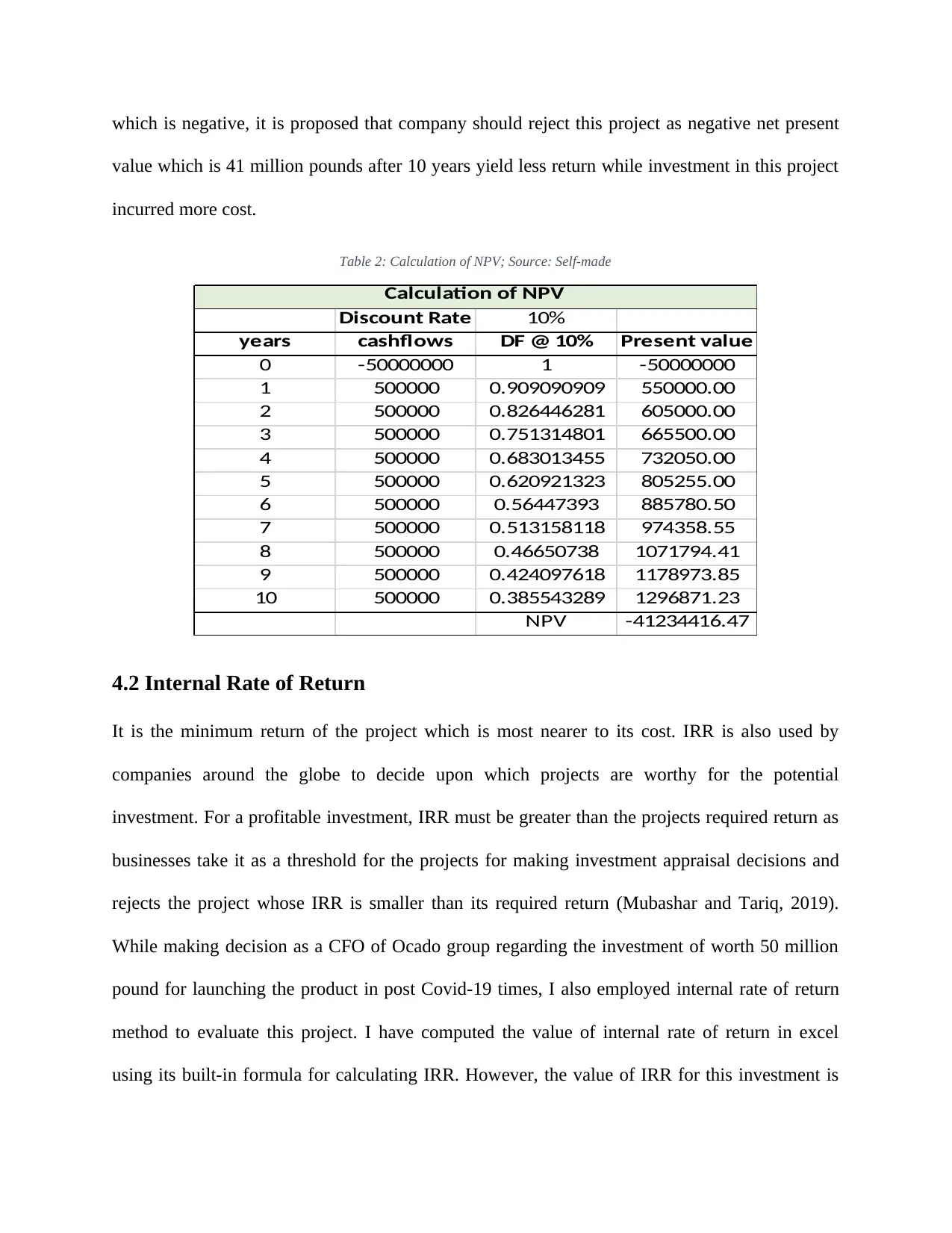

and Tariq, 2019). In this report, I have also used the net present value approach to make crucial

decision regarding the investment of 50 million pounds in the development of new product post

covid-19 and this investment covers the time span of 10 years with 10% discount rate. For the

calculation of net present value, I assume that this project delivers 0.5 million pounds worth

expected constant cash flow. Table 2 reports computation of NPV. Based on the value of NPV

comparison with low and high discounting rates.

Considering that vaccination for the Covid-19 epidemic has already started worldwide, it is

expected that the world will be back on the tract as it was before this epidemic. According to

Arjunan (2019), majority of the big business such as Nike, Walmart, etc. are currently working

to develop and produce products and services for post Covid-19 period. In this regard,

management of the Ocado group is also interest in launching new product in the retail business

and the company has an investment of about 50 million pounds. This investment will cover the

expenses for development of new product and expenses for marketing and launching of the

product. I evaluated this investment using both of the above mentioned approaches as a CFO of

the Ocado group.

4.1 Net Present Value

It is the most preferable technique of capital budgeting employed by the company for making

important decision related to investment appraisal. It basically tells about the investments

profitability by calculating the variance in present value of cash inflow and cash outflow.

Projects having positive net present value are most desirable by the company but the projects

with negative net present value are unfavourable ones. Positive net present value implies that the

potential future returns from the project are greater than the present value of its cost (Mubashar

and Tariq, 2019). In this report, I have also used the net present value approach to make crucial

decision regarding the investment of 50 million pounds in the development of new product post

covid-19 and this investment covers the time span of 10 years with 10% discount rate. For the

calculation of net present value, I assume that this project delivers 0.5 million pounds worth

expected constant cash flow. Table 2 reports computation of NPV. Based on the value of NPV

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which is negative, it is proposed that company should reject this project as negative net present

value which is 41 million pounds after 10 years yield less return while investment in this project

incurred more cost.

Table 2: Calculation of NPV; Source: Self-made

Discount Rate 10%

years cashflows DF @ 10% Present value

0 -50000000 1 -50000000

1 500000 0.909090909 550000.00

2 500000 0.826446281 605000.00

3 500000 0.751314801 665500.00

4 500000 0.683013455 732050.00

5 500000 0.620921323 805255.00

6 500000 0.56447393 885780.50

7 500000 0.513158118 974358.55

8 500000 0.46650738 1071794.41

9 500000 0.424097618 1178973.85

10 500000 0.385543289 1296871.23

NPV -41234416.47

Calculation of NPV

4.2 Internal Rate of Return

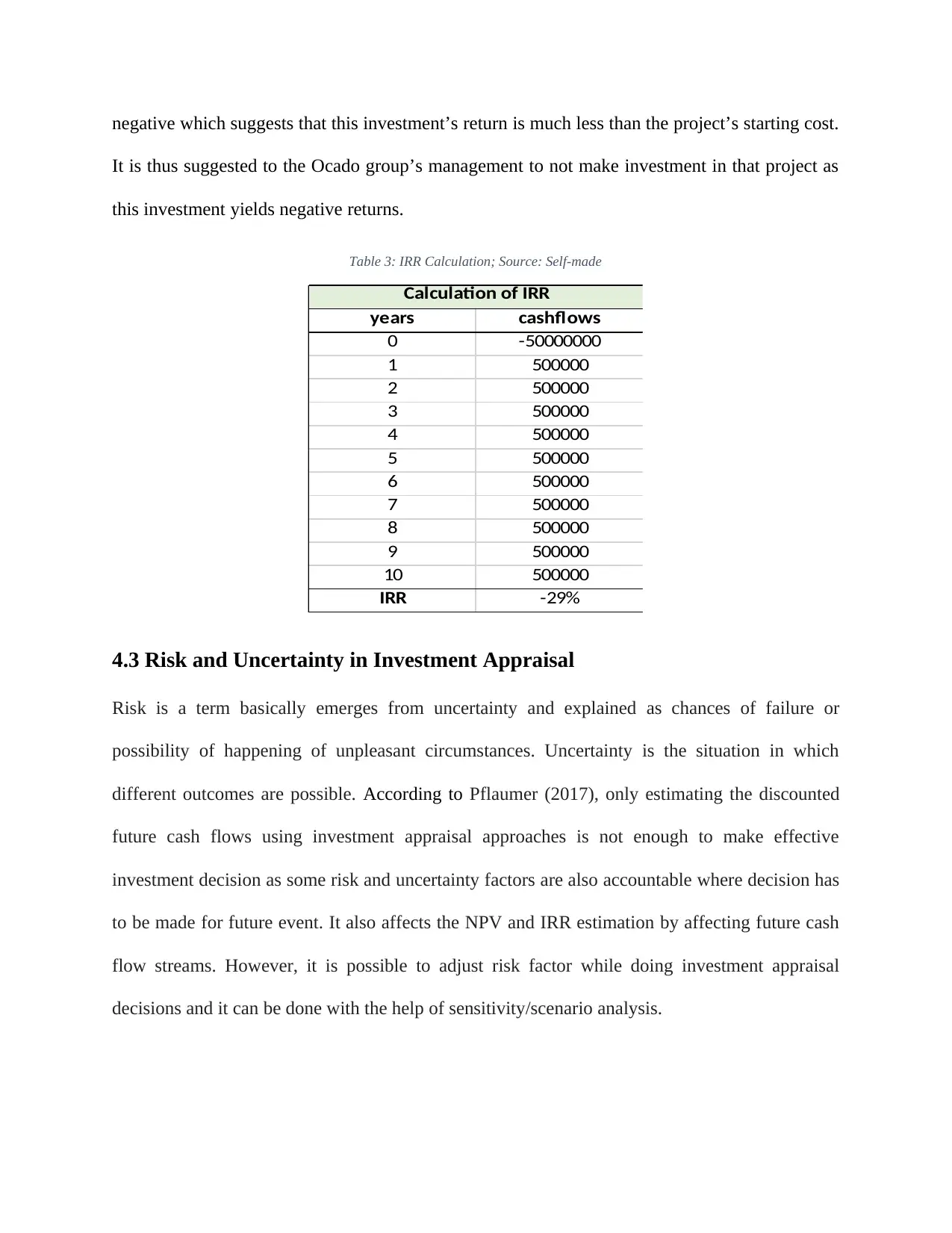

It is the minimum return of the project which is most nearer to its cost. IRR is also used by

companies around the globe to decide upon which projects are worthy for the potential

investment. For a profitable investment, IRR must be greater than the projects required return as

businesses take it as a threshold for the projects for making investment appraisal decisions and

rejects the project whose IRR is smaller than its required return (Mubashar and Tariq, 2019).

While making decision as a CFO of Ocado group regarding the investment of worth 50 million

pound for launching the product in post Covid-19 times, I also employed internal rate of return

method to evaluate this project. I have computed the value of internal rate of return in excel

using its built-in formula for calculating IRR. However, the value of IRR for this investment is

value which is 41 million pounds after 10 years yield less return while investment in this project

incurred more cost.

Table 2: Calculation of NPV; Source: Self-made

Discount Rate 10%

years cashflows DF @ 10% Present value

0 -50000000 1 -50000000

1 500000 0.909090909 550000.00

2 500000 0.826446281 605000.00

3 500000 0.751314801 665500.00

4 500000 0.683013455 732050.00

5 500000 0.620921323 805255.00

6 500000 0.56447393 885780.50

7 500000 0.513158118 974358.55

8 500000 0.46650738 1071794.41

9 500000 0.424097618 1178973.85

10 500000 0.385543289 1296871.23

NPV -41234416.47

Calculation of NPV

4.2 Internal Rate of Return

It is the minimum return of the project which is most nearer to its cost. IRR is also used by

companies around the globe to decide upon which projects are worthy for the potential

investment. For a profitable investment, IRR must be greater than the projects required return as

businesses take it as a threshold for the projects for making investment appraisal decisions and

rejects the project whose IRR is smaller than its required return (Mubashar and Tariq, 2019).

While making decision as a CFO of Ocado group regarding the investment of worth 50 million

pound for launching the product in post Covid-19 times, I also employed internal rate of return

method to evaluate this project. I have computed the value of internal rate of return in excel

using its built-in formula for calculating IRR. However, the value of IRR for this investment is

negative which suggests that this investment’s return is much less than the project’s starting cost.

It is thus suggested to the Ocado group’s management to not make investment in that project as

this investment yields negative returns.

Table 3: IRR Calculation; Source: Self-made

years cashflows

0 -50000000

1 500000

2 500000

3 500000

4 500000

5 500000

6 500000

7 500000

8 500000

9 500000

10 500000

IRR -29%

Calculation of IRR

4.3 Risk and Uncertainty in Investment Appraisal

Risk is a term basically emerges from uncertainty and explained as chances of failure or

possibility of happening of unpleasant circumstances. Uncertainty is the situation in which

different outcomes are possible. According to Pflaumer (2017), only estimating the discounted

future cash flows using investment appraisal approaches is not enough to make effective

investment decision as some risk and uncertainty factors are also accountable where decision has

to be made for future event. It also affects the NPV and IRR estimation by affecting future cash

flow streams. However, it is possible to adjust risk factor while doing investment appraisal

decisions and it can be done with the help of sensitivity/scenario analysis.

It is thus suggested to the Ocado group’s management to not make investment in that project as

this investment yields negative returns.

Table 3: IRR Calculation; Source: Self-made

years cashflows

0 -50000000

1 500000

2 500000

3 500000

4 500000

5 500000

6 500000

7 500000

8 500000

9 500000

10 500000

IRR -29%

Calculation of IRR

4.3 Risk and Uncertainty in Investment Appraisal

Risk is a term basically emerges from uncertainty and explained as chances of failure or

possibility of happening of unpleasant circumstances. Uncertainty is the situation in which

different outcomes are possible. According to Pflaumer (2017), only estimating the discounted

future cash flows using investment appraisal approaches is not enough to make effective

investment decision as some risk and uncertainty factors are also accountable where decision has

to be made for future event. It also affects the NPV and IRR estimation by affecting future cash

flow streams. However, it is possible to adjust risk factor while doing investment appraisal

decisions and it can be done with the help of sensitivity/scenario analysis.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.