OCBC Bank's Credit Card Business: An Integrated Case Study Report

VerifiedAdded on 2023/06/07

|12

|3945

|400

Case Study

AI Summary

This report provides an integrated case study analysis of OCBC Bank, focusing on the challenges faced by its credit card business. It begins with a background of the organization and identifies key problems such as low customer satisfaction, technical difficulties, and intense competition. The analysis employs Porter's Five Forces model to assess the competitive landscape, the STP model to analyze target markets, and customer loyalty frameworks to improve retention. The report also includes a SWOT analysis and PEST analysis to evaluate the internal and external business environment. Finally, the report proposes solutions to address the identified problems, aiming to improve OCBC Bank's performance and competitive advantage in the credit card industry. Desklib provides access to similar case studies and solved assignments for students.

Integrated case study

analysis

analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Executive summary..........................................................................................................................3

INTRODUCTION...........................................................................................................................4

MAIN BODY ..................................................................................................................................4

Case brief: Description of the situation.......................................................................................4

Problem statement, plan of analysis.............................................................................................5

An assessment of the current positions faced by KIA Motors ....................................................8

Proposed solution to problem....................................................................................................10

REFERENCES..............................................................................................................................12

Executive summary..........................................................................................................................3

INTRODUCTION...........................................................................................................................4

MAIN BODY ..................................................................................................................................4

Case brief: Description of the situation.......................................................................................4

Problem statement, plan of analysis.............................................................................................5

An assessment of the current positions faced by KIA Motors ....................................................8

Proposed solution to problem....................................................................................................10

REFERENCES..............................................................................................................................12

Executive summary

This report is based on the integrated case study analysis of an organisation and in order

to demonstrate various prospects of the report, case study of OCBC Banks is taken into account.

For completing several aspects of the respective report, the problems that are faced by this

organisation towards attainment of its set objectives and goals will be discussed. In addition to it,

there will be a background of the organisation for making an analysis on business operations of

the organisation. This report also covers the challenges faced by OCBC Banks in achievement of

its growth as well as different frameworks and theories along with strategic approaches will also

be described to analyse different aspects such as competitors analysis framework, STP model

and many others. Furthermore, current positions faced by OCBC Banks will also be taken into

account and along with this, the solutions that best fit the issues will also be discussed within this

report in the form of recommendations to the respective organisation.

This report is based on the integrated case study analysis of an organisation and in order

to demonstrate various prospects of the report, case study of OCBC Banks is taken into account.

For completing several aspects of the respective report, the problems that are faced by this

organisation towards attainment of its set objectives and goals will be discussed. In addition to it,

there will be a background of the organisation for making an analysis on business operations of

the organisation. This report also covers the challenges faced by OCBC Banks in achievement of

its growth as well as different frameworks and theories along with strategic approaches will also

be described to analyse different aspects such as competitors analysis framework, STP model

and many others. Furthermore, current positions faced by OCBC Banks will also be taken into

account and along with this, the solutions that best fit the issues will also be discussed within this

report in the form of recommendations to the respective organisation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Case study is considered as an approach of research that is used for conducting an in-

depth analysis of the particular cases, multi-faceted understanding of a complicated issue within

the real-life context. An integrated case study analysis provides assessment of the professional

abilities as well as capabilities and skills along with exploring the perceptions of the reporter on

effectiveness of the integrated case study. This kind of case study covers comprehensive cases

which facilitates in throwing a light on the different issues of situations, marketing and

challenges (Anvarovich, 2021). In order to conduct such type of analysis, a reporter is required to

enhance its written and verbal communication skills through making different analysis of the

case. Within this existing report, an analysis of a case study is going to be described and case

study of OCBC Bank is taken into consideration in order to demonstrate multiple prospects of

this report. For accomplishing several aspects of this report, the problems which are faced by the

respective organisation within its path of meeting organisational aspirations will be covered in an

effective manner. Additionally, this report also includes the background of the selected

organisation for the purpose of analysing the performance of the business in a successful way.

Within this current report, the challenges faced by OCBC Bank in attaining its growth will also

be mentioned. Various models, approaches or theories are also going to be used for analysing

different aspects. Beyond all these tasks, the current positions which are faced by the respective

organisation are also going to be discussed as well as the solutions to these positions will also be

taken into account in order to achieve the growth and success of the organisation effectively and

efficiently.

MAIN BODY

Case brief: Description of the situation

Within this report, the case study of OCBC Bank is taken into account for covering

different concepts of this report. According to the given case study, Tammy Ang has been tasked

with the preparation of a business pitch for the respective bank's credit card business (Arifin,

2021). Within March 2020, Institute of Service Excellence had released its 2019 findings on the

credit card industry on the basis of study of Customer Satisfaction of Singapore. OCBC Bank's

credit card business was again ranked last amongst the credit card issuers studied. The bank has

scored 72.1 points on a scale of 0 to 100 and trailed behind market leader Citibank which has

Case study is considered as an approach of research that is used for conducting an in-

depth analysis of the particular cases, multi-faceted understanding of a complicated issue within

the real-life context. An integrated case study analysis provides assessment of the professional

abilities as well as capabilities and skills along with exploring the perceptions of the reporter on

effectiveness of the integrated case study. This kind of case study covers comprehensive cases

which facilitates in throwing a light on the different issues of situations, marketing and

challenges (Anvarovich, 2021). In order to conduct such type of analysis, a reporter is required to

enhance its written and verbal communication skills through making different analysis of the

case. Within this existing report, an analysis of a case study is going to be described and case

study of OCBC Bank is taken into consideration in order to demonstrate multiple prospects of

this report. For accomplishing several aspects of this report, the problems which are faced by the

respective organisation within its path of meeting organisational aspirations will be covered in an

effective manner. Additionally, this report also includes the background of the selected

organisation for the purpose of analysing the performance of the business in a successful way.

Within this current report, the challenges faced by OCBC Bank in attaining its growth will also

be mentioned. Various models, approaches or theories are also going to be used for analysing

different aspects. Beyond all these tasks, the current positions which are faced by the respective

organisation are also going to be discussed as well as the solutions to these positions will also be

taken into account in order to achieve the growth and success of the organisation effectively and

efficiently.

MAIN BODY

Case brief: Description of the situation

Within this report, the case study of OCBC Bank is taken into account for covering

different concepts of this report. According to the given case study, Tammy Ang has been tasked

with the preparation of a business pitch for the respective bank's credit card business (Arifin,

2021). Within March 2020, Institute of Service Excellence had released its 2019 findings on the

credit card industry on the basis of study of Customer Satisfaction of Singapore. OCBC Bank's

credit card business was again ranked last amongst the credit card issuers studied. The bank has

scored 72.1 points on a scale of 0 to 100 and trailed behind market leader Citibank which has

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

scored 73.5 points. Therefore, credit card business of bank has constantly ranked poorly on index

for various years. It has also been mentioned in the given case study that for improving service

sector performance in Singapore, ISE had been conducting CSISG study whose outcomes were

released to both the media as well as industry along with providing consulting services and

research. It has also been stated that through intense competitive credit card market within

Singapore, Ang felt that merchant tie-ups could be critical for helping OCBC Bank in improving

its performance within such area (Bhatia, 2022). As per given case study, personal credit card

industry was dominated by 8 major organisations within the year 2019 and among local issuers

were three key local banks including DBS Bank, UOB and OCBC Bank. Other foreign financial

institutions including American Express, Standard Chartered, Citibank, HSBC and Maybank. In

context to competition, credit card business has been tended to be extreme dynamic with issuers

consistently refreshing as well as reviewing their current portfolio of cards. Organisations also

provided limited time promotions like free gifts for new sign-ups for capturing market-base.

Within the year 2019, OCBC Bank was considered as third-largest issuer by transaction value

and has held 15.9% of customers by transaction value. On other hand, top two issuers including

DBS Bank and UOB held market-base of 26.9% as well as 20.3% respectively.

Problem statement, plan of analysis

Statement of the problems in the case:

The organisation OCBC Bank had faced various problems in the path of its meeting

organisational aspirations as well as attaining growth of the business. The statement of the

problems which are included within the case of the respective organisation are mentioned as

follows:

1. The company had to face lower level of satisfaction as well as loyalty for the credit cards

of the banks which is a major problem for OCBC Bank as the business of credit cards

was ranked last in terms of customer satisfaction (Das, 2020).

2. Another problem faced by OCBC Bank is that the organisation was facing technical

difficulties which are preventing the market share from using its automated teller

machines as well as internet banking network.

3. Problems related to extreme level of competition within the credit card industry in

Singapore has also been faced by OCBC Bank in chasing competitive advantage over its

competitors within the marketplace.

for various years. It has also been mentioned in the given case study that for improving service

sector performance in Singapore, ISE had been conducting CSISG study whose outcomes were

released to both the media as well as industry along with providing consulting services and

research. It has also been stated that through intense competitive credit card market within

Singapore, Ang felt that merchant tie-ups could be critical for helping OCBC Bank in improving

its performance within such area (Bhatia, 2022). As per given case study, personal credit card

industry was dominated by 8 major organisations within the year 2019 and among local issuers

were three key local banks including DBS Bank, UOB and OCBC Bank. Other foreign financial

institutions including American Express, Standard Chartered, Citibank, HSBC and Maybank. In

context to competition, credit card business has been tended to be extreme dynamic with issuers

consistently refreshing as well as reviewing their current portfolio of cards. Organisations also

provided limited time promotions like free gifts for new sign-ups for capturing market-base.

Within the year 2019, OCBC Bank was considered as third-largest issuer by transaction value

and has held 15.9% of customers by transaction value. On other hand, top two issuers including

DBS Bank and UOB held market-base of 26.9% as well as 20.3% respectively.

Problem statement, plan of analysis

Statement of the problems in the case:

The organisation OCBC Bank had faced various problems in the path of its meeting

organisational aspirations as well as attaining growth of the business. The statement of the

problems which are included within the case of the respective organisation are mentioned as

follows:

1. The company had to face lower level of satisfaction as well as loyalty for the credit cards

of the banks which is a major problem for OCBC Bank as the business of credit cards

was ranked last in terms of customer satisfaction (Das, 2020).

2. Another problem faced by OCBC Bank is that the organisation was facing technical

difficulties which are preventing the market share from using its automated teller

machines as well as internet banking network.

3. Problems related to extreme level of competition within the credit card industry in

Singapore has also been faced by OCBC Bank in chasing competitive advantage over its

competitors within the marketplace.

4. The company has also been provided limited time promotions that has created a problem

in capturing more and more customers.

5. There has been relatively less number of market share with OCBC Bank in comparison to

the top issuers within the credit card industry.

These are all the statements of the problems that are faced by OCBC Banks at time of

achieving its success as well as growth effectively.

Proposed plan of analysis

Within this section, there will be description and evaluation of different models or

approaches in relation to OCBC Banks for addressing the problems faced by organisation

(Ibrahim, 2018). Hence, first of all Porter's Five Forces Model will be explained in context to

respective company for analysing market competition and industry.

Porter's Five Forces would assist OCBC Bank to determine competitive scenario within

credit card industry in Singapore. This framework also facilitates in development of effective

business strategies of the organisation. The five forces of this model are discussed as under in

relation to OCBC Bank:

Threat of new entrants: New entrants get entry into the credit card industry can make a

complex problem to OCBC Bank as new entrants may possess more attractable plan for

capturing market-base like interest rate of loan is less expensive, enhance time period of

life insurance policy, etc. For instance, Julybank is new entrant bank from Singapore

having huge monetary expense as well as capital interest within Malaysia (Lai, 2019).

Hence, it is a high threat for OCBC Bank to compete within banking and finance industry

because promotions and offers of company are not attractive enough which may lead to

loss of profitability in long-run.

Threat of bargaining power of buyers: In case if buyers have strong bargaining power

then they generally tend to drive the price down which leads in reduction of potentiality

of OCBC Bank to earn sustainable profit margins.

Threat of bargaining power of suppliers: If suppliers have strong bargaining power

then they will extract greater prices from OCBC Bank which will influence the

potentiality of bank to maintain above average profitability within credit card industry.

Competitive rivalry: This force of Porter's Five Forces Model states that high level of

competition will be difficult for existing players like OCBC Bank in earning sustainable

in capturing more and more customers.

5. There has been relatively less number of market share with OCBC Bank in comparison to

the top issuers within the credit card industry.

These are all the statements of the problems that are faced by OCBC Banks at time of

achieving its success as well as growth effectively.

Proposed plan of analysis

Within this section, there will be description and evaluation of different models or

approaches in relation to OCBC Banks for addressing the problems faced by organisation

(Ibrahim, 2018). Hence, first of all Porter's Five Forces Model will be explained in context to

respective company for analysing market competition and industry.

Porter's Five Forces would assist OCBC Bank to determine competitive scenario within

credit card industry in Singapore. This framework also facilitates in development of effective

business strategies of the organisation. The five forces of this model are discussed as under in

relation to OCBC Bank:

Threat of new entrants: New entrants get entry into the credit card industry can make a

complex problem to OCBC Bank as new entrants may possess more attractable plan for

capturing market-base like interest rate of loan is less expensive, enhance time period of

life insurance policy, etc. For instance, Julybank is new entrant bank from Singapore

having huge monetary expense as well as capital interest within Malaysia (Lai, 2019).

Hence, it is a high threat for OCBC Bank to compete within banking and finance industry

because promotions and offers of company are not attractive enough which may lead to

loss of profitability in long-run.

Threat of bargaining power of buyers: In case if buyers have strong bargaining power

then they generally tend to drive the price down which leads in reduction of potentiality

of OCBC Bank to earn sustainable profit margins.

Threat of bargaining power of suppliers: If suppliers have strong bargaining power

then they will extract greater prices from OCBC Bank which will influence the

potentiality of bank to maintain above average profitability within credit card industry.

Competitive rivalry: This force of Porter's Five Forces Model states that high level of

competition will be difficult for existing players like OCBC Bank in earning sustainable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

profits. Therefore, it is a moderate threat of competitive rivalry to respective organisation

within credit card industry.

Threat of substitute products: In relation to OCBC Bank, Visa holder of organisation

may changes to Public Bank as respective organisation Mastercard requires to charge

RM68 per annum expenses and Maybank without accuse any charge of Debit card and

get similar capacity with credit card (Liu and et.al., 2019). Hence, there is moderate

threat of substitutes for OCBC Bank.

Another model of STP is discussed below for analysing the target market of the OCBC

Bank and effectively positioning its services within the marketplace with the support of better

promotional channels:

STP Model derives from its three steps of segmentation, targeting and positioning and its

use in marketing is to discover profitable marketing segments as well as recognising target

audiences for marketing activities. These three different stages of this model are discussed as

under in relation to OCBC Bank:

Segmentation: It is a process through which OCBC Bank decides to segment its whole

market into smaller groups and segments that are having same buying behaviour,

attributes, socio economic background and many others. This is done for capturing a

large number of customers within the marketplace towards services of organisation and

brand itself in a more effective and efficient way.

Targeting: It is the second stage of STP Model and according to this stage, OCBC Bank

targets its market segments and uses customer-behaviour factor for targeting its potential

market share so that it can identify their preferences and deliver timely, compelling offers

that boost across-sell conversion percentage by doubling digits as well as lifting return on

marketing investment through triple digits. Positioning: This is the last stage of STP model and at this stage, OCBC Bank position

its business services in an effective manner (Long Nguyen and Megargel, 2022). In order

to position its services, the organisation is required to promote its services within

marketplace among its customers for generating awareness. The organisation can make

use of personalised marketing as promotions and offers of the organisation are not

attractive enough. This helps company in attracting a wide number of market-base within

the marketplace.

within credit card industry.

Threat of substitute products: In relation to OCBC Bank, Visa holder of organisation

may changes to Public Bank as respective organisation Mastercard requires to charge

RM68 per annum expenses and Maybank without accuse any charge of Debit card and

get similar capacity with credit card (Liu and et.al., 2019). Hence, there is moderate

threat of substitutes for OCBC Bank.

Another model of STP is discussed below for analysing the target market of the OCBC

Bank and effectively positioning its services within the marketplace with the support of better

promotional channels:

STP Model derives from its three steps of segmentation, targeting and positioning and its

use in marketing is to discover profitable marketing segments as well as recognising target

audiences for marketing activities. These three different stages of this model are discussed as

under in relation to OCBC Bank:

Segmentation: It is a process through which OCBC Bank decides to segment its whole

market into smaller groups and segments that are having same buying behaviour,

attributes, socio economic background and many others. This is done for capturing a

large number of customers within the marketplace towards services of organisation and

brand itself in a more effective and efficient way.

Targeting: It is the second stage of STP Model and according to this stage, OCBC Bank

targets its market segments and uses customer-behaviour factor for targeting its potential

market share so that it can identify their preferences and deliver timely, compelling offers

that boost across-sell conversion percentage by doubling digits as well as lifting return on

marketing investment through triple digits. Positioning: This is the last stage of STP model and at this stage, OCBC Bank position

its business services in an effective manner (Long Nguyen and Megargel, 2022). In order

to position its services, the organisation is required to promote its services within

marketplace among its customers for generating awareness. The organisation can make

use of personalised marketing as promotions and offers of the organisation are not

attractive enough. This helps company in attracting a wide number of market-base within

the marketplace.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Framework for improving customer loyalty

Customer loyalty models are the frameworks that can be used by an organisation like

OCBC Bank for strategising, measuring and improving customer loyalty and retention. Net

Promoter Score is considered as a voice of customer tool which can be used by respective

organisation for collecting feedback from its customers (Lui and et.al., 2021). It provide

assistance to OCBC Bank in maintaining customer loyalty towards organisation and chasing

competitive advantage over competitors within the credit card industry.

An assessment of the current positions faced by KIA Motors

This section includes analysis of the internal as well as external business environment of

the organisation and also analysing the factors that impact the performance of an industry. In

order to analyse the internal and external environment of OCBC Bank, model of SWOT Analysis

and Pest Analysis is used. The SWOT Analysis of OCBC Bank is explained as below for

analysing its internal strengths and weaknesses along with ascertaining external opportunities

and threats to company:

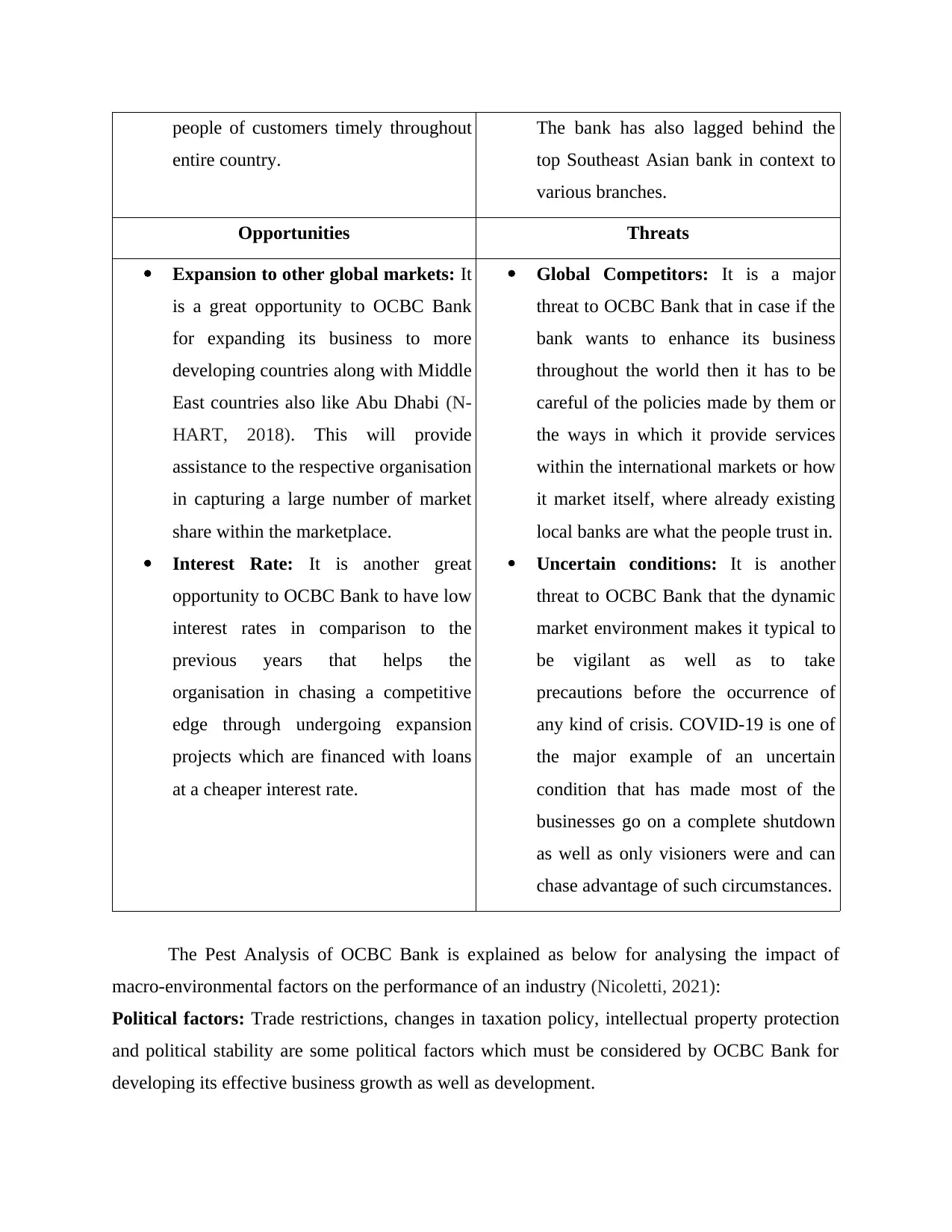

Strengths Weaknesses

Number of Acquisitions: This is a

major strength of OCBC Bank has

acquired various large organisations

within its course of journey such as

Four Seas Communications Banks

within the year 1972, acquisition of

Keppel Capital Holdings in 2001 and

many more.

Range and Speed: It is another

strength of OCBC Bank that the

organisation has a broad distribution

network of 570 branches within over 18

nations including Indonesia, Singapore,

Hong King, etc. which makes sure its

services are easily accessible to wide

Cash Flow Problems: It is the major

weakness of OCBC Bank as there is a

lack of appropriate monetary planning

at bank in relation to the cash flow

which results in certain situations

where there is not suitable cash flow as

required leading to inessential

unplanned borrowing (Mengniyozov,

2021).

Dependency on Singapore and

Southeast Asia: It is another weakness

of OCBC Bank that its global presence

is not up to the mark and respective

organisation is more reliable on

Singapore and Southeast Asia regions.

Customer loyalty models are the frameworks that can be used by an organisation like

OCBC Bank for strategising, measuring and improving customer loyalty and retention. Net

Promoter Score is considered as a voice of customer tool which can be used by respective

organisation for collecting feedback from its customers (Lui and et.al., 2021). It provide

assistance to OCBC Bank in maintaining customer loyalty towards organisation and chasing

competitive advantage over competitors within the credit card industry.

An assessment of the current positions faced by KIA Motors

This section includes analysis of the internal as well as external business environment of

the organisation and also analysing the factors that impact the performance of an industry. In

order to analyse the internal and external environment of OCBC Bank, model of SWOT Analysis

and Pest Analysis is used. The SWOT Analysis of OCBC Bank is explained as below for

analysing its internal strengths and weaknesses along with ascertaining external opportunities

and threats to company:

Strengths Weaknesses

Number of Acquisitions: This is a

major strength of OCBC Bank has

acquired various large organisations

within its course of journey such as

Four Seas Communications Banks

within the year 1972, acquisition of

Keppel Capital Holdings in 2001 and

many more.

Range and Speed: It is another

strength of OCBC Bank that the

organisation has a broad distribution

network of 570 branches within over 18

nations including Indonesia, Singapore,

Hong King, etc. which makes sure its

services are easily accessible to wide

Cash Flow Problems: It is the major

weakness of OCBC Bank as there is a

lack of appropriate monetary planning

at bank in relation to the cash flow

which results in certain situations

where there is not suitable cash flow as

required leading to inessential

unplanned borrowing (Mengniyozov,

2021).

Dependency on Singapore and

Southeast Asia: It is another weakness

of OCBC Bank that its global presence

is not up to the mark and respective

organisation is more reliable on

Singapore and Southeast Asia regions.

people of customers timely throughout

entire country.

The bank has also lagged behind the

top Southeast Asian bank in context to

various branches.

Opportunities Threats

Expansion to other global markets: It

is a great opportunity to OCBC Bank

for expanding its business to more

developing countries along with Middle

East countries also like Abu Dhabi (N-

HART, 2018). This will provide

assistance to the respective organisation

in capturing a large number of market

share within the marketplace.

Interest Rate: It is another great

opportunity to OCBC Bank to have low

interest rates in comparison to the

previous years that helps the

organisation in chasing a competitive

edge through undergoing expansion

projects which are financed with loans

at a cheaper interest rate.

Global Competitors: It is a major

threat to OCBC Bank that in case if the

bank wants to enhance its business

throughout the world then it has to be

careful of the policies made by them or

the ways in which it provide services

within the international markets or how

it market itself, where already existing

local banks are what the people trust in.

Uncertain conditions: It is another

threat to OCBC Bank that the dynamic

market environment makes it typical to

be vigilant as well as to take

precautions before the occurrence of

any kind of crisis. COVID-19 is one of

the major example of an uncertain

condition that has made most of the

businesses go on a complete shutdown

as well as only visioners were and can

chase advantage of such circumstances.

The Pest Analysis of OCBC Bank is explained as below for analysing the impact of

macro-environmental factors on the performance of an industry (Nicoletti, 2021):

Political factors: Trade restrictions, changes in taxation policy, intellectual property protection

and political stability are some political factors which must be considered by OCBC Bank for

developing its effective business growth as well as development.

entire country.

The bank has also lagged behind the

top Southeast Asian bank in context to

various branches.

Opportunities Threats

Expansion to other global markets: It

is a great opportunity to OCBC Bank

for expanding its business to more

developing countries along with Middle

East countries also like Abu Dhabi (N-

HART, 2018). This will provide

assistance to the respective organisation

in capturing a large number of market

share within the marketplace.

Interest Rate: It is another great

opportunity to OCBC Bank to have low

interest rates in comparison to the

previous years that helps the

organisation in chasing a competitive

edge through undergoing expansion

projects which are financed with loans

at a cheaper interest rate.

Global Competitors: It is a major

threat to OCBC Bank that in case if the

bank wants to enhance its business

throughout the world then it has to be

careful of the policies made by them or

the ways in which it provide services

within the international markets or how

it market itself, where already existing

local banks are what the people trust in.

Uncertain conditions: It is another

threat to OCBC Bank that the dynamic

market environment makes it typical to

be vigilant as well as to take

precautions before the occurrence of

any kind of crisis. COVID-19 is one of

the major example of an uncertain

condition that has made most of the

businesses go on a complete shutdown

as well as only visioners were and can

chase advantage of such circumstances.

The Pest Analysis of OCBC Bank is explained as below for analysing the impact of

macro-environmental factors on the performance of an industry (Nicoletti, 2021):

Political factors: Trade restrictions, changes in taxation policy, intellectual property protection

and political stability are some political factors which must be considered by OCBC Bank for

developing its effective business growth as well as development.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Economic factors: These factors include inflation, savings rate, interest rates, exchange rates,

interest rate of loans are critical for OCBC Bank for understanding the impact of such factors

that greatly influence economic environment of the country.

Social factors: Cultural norms, life expectancy, traditions, social values have a great impact on

the culture of organisation. OCBC Bank must have concerns about social values and provide

welfare to them that enhances the reputation of bank within the marketplace and thereby

increases its performance level (PUTRI, 2018). In this way, the company maintain retention of

its customers in a great manner and thereby also maintains customer loyalty effectively and

efficiently.

Technological factors: The relevance of comprehending technological aspects throughout the

strategic process of decision making has risen as a result of progress of fast technology as well as

dissemination around the world. Hence, OCBC Bank is required to adopt advanced technologies

within its business that will help in saving both cost and time of the organisation. In such

manner, the advancements in technology help the company in chasing competitive advantage

over its competitors within the marketplace and also enhances the level of customer satisfaction.

Proposed solution to problem

From the above discussion of the report, the solutions to the above mentioned problem

can be drawn. The major solution to the problem of staying competitive within the competitive

business environment is that OCBC Bank must recognise for its financial stability as well as

strengths. The financial advisor must be strong within the respective bank in Singapore.

Managing risks as well as ensuring that the company is lending in a responsible manner have

always been the major tenets of the approach at OCBC Bank. The Board within the organisation

must oversee the effectiveness in management of all the risks such as ESG risks like climate

change (Vitolla, Marrone and Raimo, 2020). The organisation is also required to consider its

internal strengths in order to overcome the weaknesses that exist within the business as it will

provide assistance to the company in chasing a competitive edge over its competitors within the

marketplace. Through analysing the different forces of Porter's Five Forces Model, it is evaluated

that OCBC bank is provided solution to frame or design effective business strategies that

facilitates the respective organisation in leading the competitive market in a very successful

manner. Another solution that should be given to OCBC Bank is that the company must target

effective market segments so that it can reach up to a large number of market share and offer its

interest rate of loans are critical for OCBC Bank for understanding the impact of such factors

that greatly influence economic environment of the country.

Social factors: Cultural norms, life expectancy, traditions, social values have a great impact on

the culture of organisation. OCBC Bank must have concerns about social values and provide

welfare to them that enhances the reputation of bank within the marketplace and thereby

increases its performance level (PUTRI, 2018). In this way, the company maintain retention of

its customers in a great manner and thereby also maintains customer loyalty effectively and

efficiently.

Technological factors: The relevance of comprehending technological aspects throughout the

strategic process of decision making has risen as a result of progress of fast technology as well as

dissemination around the world. Hence, OCBC Bank is required to adopt advanced technologies

within its business that will help in saving both cost and time of the organisation. In such

manner, the advancements in technology help the company in chasing competitive advantage

over its competitors within the marketplace and also enhances the level of customer satisfaction.

Proposed solution to problem

From the above discussion of the report, the solutions to the above mentioned problem

can be drawn. The major solution to the problem of staying competitive within the competitive

business environment is that OCBC Bank must recognise for its financial stability as well as

strengths. The financial advisor must be strong within the respective bank in Singapore.

Managing risks as well as ensuring that the company is lending in a responsible manner have

always been the major tenets of the approach at OCBC Bank. The Board within the organisation

must oversee the effectiveness in management of all the risks such as ESG risks like climate

change (Vitolla, Marrone and Raimo, 2020). The organisation is also required to consider its

internal strengths in order to overcome the weaknesses that exist within the business as it will

provide assistance to the company in chasing a competitive edge over its competitors within the

marketplace. Through analysing the different forces of Porter's Five Forces Model, it is evaluated

that OCBC bank is provided solution to frame or design effective business strategies that

facilitates the respective organisation in leading the competitive market in a very successful

manner. Another solution that should be given to OCBC Bank is that the company must target

effective market segments so that it can reach up to a large number of market share and offer its

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

services to them through understanding their perceptions towards the services of the company.

The bank is also advised to adopt effective promotional tools and technologies for the purpose of

better positioning of its services among the market-base through generating awareness among

them regarding the features and benefits of the services. In order to effectively promote its

services to its potential customers within the marketplace, OCBC Bank is recommended to make

use of multiple promotional tactics and tools such as social media marketing, digital marketing,

advertising, sales promotion, public relations, offline and online advertising and many others.

Through these promotional channels, the bank can capture a wide number of target market and

enhance the volume of its sales operations within the business and thereby the level of

profitability also got increased within the organisation (Wahyudi and et.al., 2022). When OCBC

Bank will make use of such promotional tools at time of targeting clearly defined groups of the

market share then these will facilitate the organisation in attracting more and more customers

towards the business. OCBC Bank is also required to develop or build its relationships with the

customers which will provide assistance to the organisation in maintaining customer loyalty

towards the business. The Bank must also offer discounts and other offers to its target market so

that the number of market share increases within the organisation. The respective bank is also

needed to consider the feedbacks of its market share regarding the services as well as also

addresses them in an appropriate and effective manner. This will help in maximising the level of

satisfaction of the customers who are connected to business and buy services of the organisation.

In addition to it, there is another solution to the problems of the organisation that OCBC Bank is

required to grab the opportunities which are available to it within the competitive business

environment as it will provide assistance to the company in overcoming the future threats which

may be occur at time of conducting business operations. Moreover, the respective bank is also

needed to consider the impact of those macro-environmental factors which are adversely

influencing overall business performance. After analysing the impact of such factors, OCBC

Bank is required to frame successful business strategies to overcome the adverse impact and

chase competitive edge within credit card industry.

The bank is also advised to adopt effective promotional tools and technologies for the purpose of

better positioning of its services among the market-base through generating awareness among

them regarding the features and benefits of the services. In order to effectively promote its

services to its potential customers within the marketplace, OCBC Bank is recommended to make

use of multiple promotional tactics and tools such as social media marketing, digital marketing,

advertising, sales promotion, public relations, offline and online advertising and many others.

Through these promotional channels, the bank can capture a wide number of target market and

enhance the volume of its sales operations within the business and thereby the level of

profitability also got increased within the organisation (Wahyudi and et.al., 2022). When OCBC

Bank will make use of such promotional tools at time of targeting clearly defined groups of the

market share then these will facilitate the organisation in attracting more and more customers

towards the business. OCBC Bank is also required to develop or build its relationships with the

customers which will provide assistance to the organisation in maintaining customer loyalty

towards the business. The Bank must also offer discounts and other offers to its target market so

that the number of market share increases within the organisation. The respective bank is also

needed to consider the feedbacks of its market share regarding the services as well as also

addresses them in an appropriate and effective manner. This will help in maximising the level of

satisfaction of the customers who are connected to business and buy services of the organisation.

In addition to it, there is another solution to the problems of the organisation that OCBC Bank is

required to grab the opportunities which are available to it within the competitive business

environment as it will provide assistance to the company in overcoming the future threats which

may be occur at time of conducting business operations. Moreover, the respective bank is also

needed to consider the impact of those macro-environmental factors which are adversely

influencing overall business performance. After analysing the impact of such factors, OCBC

Bank is required to frame successful business strategies to overcome the adverse impact and

chase competitive edge within credit card industry.

REFERENCES

Books and Journals

Anvarovich, N. E., 2021. Evolutionary Development of Distance Banking Services in the Digital

Economy. International Journal on Economics, Finance and Sustainable

Development, 3(3), pp.78-84.

Arifin, Z., 2021. STRATEGIC MANAGEMENT PROCESS: BANK NATIONAL IN

IMPROVING PERFORMANCE BEFORE AND DURING COVID-19

PANDEMIC. Academy of Strategic Management Journal, 20(3), pp.1-9.

Bhatia, M., 2022. Platform Banking Business. In Banking 4.0 (pp. 169-196). Springer,

Singapore.

Das, R., 2020. The Blue Elephant: Why India Must Boost its Soft Power. Notion Press.

Ibrahim, I., 2018. The Relationship Between Liquidity Risk and Bank Performance in Bank:

Oversea-Chinese Banking Corporation Limited, Bank in Singapore. Bank in Singapore

(December 16, 2018).

Lai, K., 2019. Opening the gate of China. Int'l Fin. L. Rev., p.41.

Liu and et.al., 2019. Integrated GHG emissions and emission relationships analysis through a

disaggregated ecologically-extended input-output model; A case study for Saskatchewan,

Canada. Renewable and Sustainable Energy Reviews, 106, pp.97-109.

Long Nguyen, H. H. and Megargel, A., 2022. Strategic business models under open banking: A

guideline for incumbent banks. Journal of Digital Banking, 6(4), pp.366-380.

Lui and et.al., 2021. Corporate social responsibility disclosures (CSRDs) in the banking industry:

a study of conventional banks and Islamic banks in Malaysia. International Journal of

Bank Marketing.

Mengniyozov, A. N., 2021. STAGES OF FORMATION OF NON-CASH MONETARY

RELATIONS.

N-HART, L. T., 2018. The Regionalization of SOUtheast Asian BusineSS: TranSnational

NetWOrkS in National COntexts. Remapping East Asia: The Construction of a Region,

p.170.

Nicoletti, B., 2021. Processes in Banking 5.0. In Banking 5.0 (pp. 303-325). Palgrave Macmillan,

Cham.

PUTRI, N. T., 2018. EVALUASI STRATEGI BERSAING BANK OCBC NISP DI SEGMEN

EMERGING BUSINESS (Doctoral dissertation, Universitas Gadjah Mada).

Vitolla, F., Marrone, A. and Raimo, N., 2020. Integrated reporting and integrated thinking: A

case study analysis. Corp. Own. Contr, 18, pp.281-291.

Wahyudi and et.al., 2022. Improving Bank Efficiency and Reducing Asymmetric Information

through Innovation on Extensible Business Reporting Language. In Modeling Economic

Growth in Contemporary Indonesia (pp. 299-317). Emerald Publishing Limited.

Books and Journals

Anvarovich, N. E., 2021. Evolutionary Development of Distance Banking Services in the Digital

Economy. International Journal on Economics, Finance and Sustainable

Development, 3(3), pp.78-84.

Arifin, Z., 2021. STRATEGIC MANAGEMENT PROCESS: BANK NATIONAL IN

IMPROVING PERFORMANCE BEFORE AND DURING COVID-19

PANDEMIC. Academy of Strategic Management Journal, 20(3), pp.1-9.

Bhatia, M., 2022. Platform Banking Business. In Banking 4.0 (pp. 169-196). Springer,

Singapore.

Das, R., 2020. The Blue Elephant: Why India Must Boost its Soft Power. Notion Press.

Ibrahim, I., 2018. The Relationship Between Liquidity Risk and Bank Performance in Bank:

Oversea-Chinese Banking Corporation Limited, Bank in Singapore. Bank in Singapore

(December 16, 2018).

Lai, K., 2019. Opening the gate of China. Int'l Fin. L. Rev., p.41.

Liu and et.al., 2019. Integrated GHG emissions and emission relationships analysis through a

disaggregated ecologically-extended input-output model; A case study for Saskatchewan,

Canada. Renewable and Sustainable Energy Reviews, 106, pp.97-109.

Long Nguyen, H. H. and Megargel, A., 2022. Strategic business models under open banking: A

guideline for incumbent banks. Journal of Digital Banking, 6(4), pp.366-380.

Lui and et.al., 2021. Corporate social responsibility disclosures (CSRDs) in the banking industry:

a study of conventional banks and Islamic banks in Malaysia. International Journal of

Bank Marketing.

Mengniyozov, A. N., 2021. STAGES OF FORMATION OF NON-CASH MONETARY

RELATIONS.

N-HART, L. T., 2018. The Regionalization of SOUtheast Asian BusineSS: TranSnational

NetWOrkS in National COntexts. Remapping East Asia: The Construction of a Region,

p.170.

Nicoletti, B., 2021. Processes in Banking 5.0. In Banking 5.0 (pp. 303-325). Palgrave Macmillan,

Cham.

PUTRI, N. T., 2018. EVALUASI STRATEGI BERSAING BANK OCBC NISP DI SEGMEN

EMERGING BUSINESS (Doctoral dissertation, Universitas Gadjah Mada).

Vitolla, F., Marrone, A. and Raimo, N., 2020. Integrated reporting and integrated thinking: A

case study analysis. Corp. Own. Contr, 18, pp.281-291.

Wahyudi and et.al., 2022. Improving Bank Efficiency and Reducing Asymmetric Information

through Innovation on Extensible Business Reporting Language. In Modeling Economic

Growth in Contemporary Indonesia (pp. 299-317). Emerald Publishing Limited.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.