LSC UoS BA Business Studies: OCBC Bank Credit Card Case Study Analysis

VerifiedAdded on 2023/06/06

|17

|4537

|417

Case Study

AI Summary

This case study examines the customer loyalty and satisfaction challenges faced by OCBC Bank in its credit card business within the highly competitive Singaporean market. The analysis investigates the bank's underperformance relative to competitors, identifying key issues such as declining sales and a last-place ranking in customer satisfaction. The study utilizes the SERVEQUAL model to analyze service quality gaps, including knowledge, standards, delivery, and communications gaps. It also explores the impact of these gaps on customer satisfaction and loyalty. The case study provides a detailed overview of the credit card industry, the bank's position, and the application of the SERVEQUAL model to diagnose problems, with the aim of recommending strategies to improve customer loyalty and market performance. The study also examines the role of customer loyalty programs and communication tools in bridging service gaps and enhancing customer satisfaction.

Integrated Case Study

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The present study is based on issue related to customer loyalty and satisfaction in terms

of credit cards in context of OCBC bank. The respective bank is a well-known financial

institution based on Singapore which offers ample of financial and baking related services such

as loan, investment, credit cards and more. In present study, there is special reference to the

credit cards. It is monitored that credit card industry of Singapore used to dominate by eight

players named as Citibank, American Express, Standard charted bank, HSBC, MayBank, DBS

back, UOB and OCBC bank. Here, the industry is really competitive due to presence of ample

number of players. In 2019, OCBC bank was considered as the third largest issuer of credit cards

in terms of transaction value. However, it is quite complex for the respective bank in surviving

within such a competitive environment. It is found that the respective bank faced complexity in

terms of maintaining loyalty and trust among customers regarding their cards. As a result, they

recorded decline in overall sales of credit cards and the respective bank got last rank amongst the

credit card issuers within the country. It is suggested that OCBC bank needs to adopt suitable

customer loyalty programs, communication tools in order to cover the service gap and attain

higher level of customer satisfaction.

The present study is based on issue related to customer loyalty and satisfaction in terms

of credit cards in context of OCBC bank. The respective bank is a well-known financial

institution based on Singapore which offers ample of financial and baking related services such

as loan, investment, credit cards and more. In present study, there is special reference to the

credit cards. It is monitored that credit card industry of Singapore used to dominate by eight

players named as Citibank, American Express, Standard charted bank, HSBC, MayBank, DBS

back, UOB and OCBC bank. Here, the industry is really competitive due to presence of ample

number of players. In 2019, OCBC bank was considered as the third largest issuer of credit cards

in terms of transaction value. However, it is quite complex for the respective bank in surviving

within such a competitive environment. It is found that the respective bank faced complexity in

terms of maintaining loyalty and trust among customers regarding their cards. As a result, they

recorded decline in overall sales of credit cards and the respective bank got last rank amongst the

credit card issuers within the country. It is suggested that OCBC bank needs to adopt suitable

customer loyalty programs, communication tools in order to cover the service gap and attain

higher level of customer satisfaction.

Table of Contents

Introduction.................................................................................................................................................4

Statement of problem...............................................................................................................................4

Structure of the report..............................................................................................................................4

Case brief: description of the situation:.......................................................................................................5

Problem statement, plan of analysis.............................................................................................................5

Analysis & Findings....................................................................................................................................9

Solution to the problem.............................................................................................................................10

References.................................................................................................................................................12

Introduction.................................................................................................................................................4

Statement of problem...............................................................................................................................4

Structure of the report..............................................................................................................................4

Case brief: description of the situation:.......................................................................................................5

Problem statement, plan of analysis.............................................................................................................5

Analysis & Findings....................................................................................................................................9

Solution to the problem.............................................................................................................................10

References.................................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Statement of problem

Customers are considered as one of the most significant stakeholders of the company as

they purchase the products and drive revenue within the entity. In the present competitive era, it

is highly imperative to keep the customers satisfied to maintain long-term and effective relations

with them (Ming, Chen and Li, 2020). The present study is based on OCBC bank that is a well-

known bank based on Singapore. It is a multinational company that offers financial and banking

services in significant manner. In the current situation, the entity is facing issues related to

customer’s satisfaction regarding credit cards. Due to this, sell of credit cards is significantly

affecting that might create issues for the respective company in future period of time.

Research Aims and objectives

Research Aim: “To increase the customer’s loyalty for credit cards. A study on OCBC bank”.

Research Objectives:

To analyze the credit card industry of Singapore.

To assess challenges faced by OCBC bank in terms of customer loyalty regarding credit

cards.

To identify the ways in order to improve customers loyalty towards credit cards being

offered by OCBC bank.

Structure of the report

The present study is about OCBC bank that is a renowned financial and banking

corportation based on Singapore. They offer different financial services such as credit cards, net

banking, investment, loans and other such services. In the present report, the situation of the

respective company will be analyzed along with the problem statement with the help of suitable

theories, models and more. Further, current situation being faced by the chosen company is also

going to discuss in the following report based on different concepts, theories and models. At end,

it will include suitable suggestions in order to deal with the issues in an efficient manner. Along

with this, limitation of the study will also include in the existing project.

Statement of problem

Customers are considered as one of the most significant stakeholders of the company as

they purchase the products and drive revenue within the entity. In the present competitive era, it

is highly imperative to keep the customers satisfied to maintain long-term and effective relations

with them (Ming, Chen and Li, 2020). The present study is based on OCBC bank that is a well-

known bank based on Singapore. It is a multinational company that offers financial and banking

services in significant manner. In the current situation, the entity is facing issues related to

customer’s satisfaction regarding credit cards. Due to this, sell of credit cards is significantly

affecting that might create issues for the respective company in future period of time.

Research Aims and objectives

Research Aim: “To increase the customer’s loyalty for credit cards. A study on OCBC bank”.

Research Objectives:

To analyze the credit card industry of Singapore.

To assess challenges faced by OCBC bank in terms of customer loyalty regarding credit

cards.

To identify the ways in order to improve customers loyalty towards credit cards being

offered by OCBC bank.

Structure of the report

The present study is about OCBC bank that is a renowned financial and banking

corportation based on Singapore. They offer different financial services such as credit cards, net

banking, investment, loans and other such services. In the present report, the situation of the

respective company will be analyzed along with the problem statement with the help of suitable

theories, models and more. Further, current situation being faced by the chosen company is also

going to discuss in the following report based on different concepts, theories and models. At end,

it will include suitable suggestions in order to deal with the issues in an efficient manner. Along

with this, limitation of the study will also include in the existing project.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Description of the situation:

The present case is based on customer loyalty regarding credit cards with special

reference of OCBC bank. Customer loyalty is about giving preference to a particular brand over

others. When customers are loyal towards a brand, they are likely to purchase the products of

particular brand frequently. In this regard, credit cards are financial products through which a

line of credit is offered to the cardholders by which they can purchase necessary goods or

services. Here, cardholders are likely to borrow money from card issuers which are typically a

bank or financial institution (Yam and Lee, 2021). The present study is based on OCBC bank

that is a popular financial institution based on Singapore. They offer numerous financial services

such as loans, money transfer, investment, credit cards and other such services. To maintain the

high sale of credit cards, it is imperative to maintain trust among the customers. If the customers

are not loyal, they are not likely to avail the services of respective bank for longer duration.

Through the above case study, it is analyzed that credit card industry of Singapore used to

dominate by eight players named as Citibank, American Express, Standard charted bank, HSBC,

MayBank, DBS back, UOB and OCBC bank. In 2019, OCBC bank was considered as the third

largest issuer of credit cards in terms of transaction value. They have nearly 15.9% market share

by transaction value. Here, the credit cards of the respective bank used to target to a specific set

of customers by offering core benefits (Leong, 2020). However, the bank is facing issues related

to increment in market share and transaction value in last five years. Transaction value of the

respective bank has increased from 14.3% in 2015 to 15.9% in 2019. On other side, UOB and

DBS bank, have been recorded increase in transaction value from 26.5% to 26.9% within same

period of time. In terms of customer’s attitude, OCBC bank’s credit card business was ranked

last amongst the credit card issuers. It is because of underperformance of the respective bank in

comparison of its customers (Febrianti, 2017). Therefore, it is important to undertake necessary

improvements in terms of improving overall level of satisfaction of customers significantly.

Problem statement, plan of analysis

S/N Functional Area of Study The

Problem/Issue

The Theory to Use

1 Customer Loyalty Customer loyalty

and satisfaction is

To measure the

respective issues,

The present case is based on customer loyalty regarding credit cards with special

reference of OCBC bank. Customer loyalty is about giving preference to a particular brand over

others. When customers are loyal towards a brand, they are likely to purchase the products of

particular brand frequently. In this regard, credit cards are financial products through which a

line of credit is offered to the cardholders by which they can purchase necessary goods or

services. Here, cardholders are likely to borrow money from card issuers which are typically a

bank or financial institution (Yam and Lee, 2021). The present study is based on OCBC bank

that is a popular financial institution based on Singapore. They offer numerous financial services

such as loans, money transfer, investment, credit cards and other such services. To maintain the

high sale of credit cards, it is imperative to maintain trust among the customers. If the customers

are not loyal, they are not likely to avail the services of respective bank for longer duration.

Through the above case study, it is analyzed that credit card industry of Singapore used to

dominate by eight players named as Citibank, American Express, Standard charted bank, HSBC,

MayBank, DBS back, UOB and OCBC bank. In 2019, OCBC bank was considered as the third

largest issuer of credit cards in terms of transaction value. They have nearly 15.9% market share

by transaction value. Here, the credit cards of the respective bank used to target to a specific set

of customers by offering core benefits (Leong, 2020). However, the bank is facing issues related

to increment in market share and transaction value in last five years. Transaction value of the

respective bank has increased from 14.3% in 2015 to 15.9% in 2019. On other side, UOB and

DBS bank, have been recorded increase in transaction value from 26.5% to 26.9% within same

period of time. In terms of customer’s attitude, OCBC bank’s credit card business was ranked

last amongst the credit card issuers. It is because of underperformance of the respective bank in

comparison of its customers (Febrianti, 2017). Therefore, it is important to undertake necessary

improvements in terms of improving overall level of satisfaction of customers significantly.

Problem statement, plan of analysis

S/N Functional Area of Study The

Problem/Issue

The Theory to Use

1 Customer Loyalty Customer loyalty

and satisfaction is

To measure the

respective issues,

an important to

grow business in

current period of

time. Here,

customer loyalty is

about ongoing

emotional

relationships

between a brand

and its customers.

It describes the

way how willingly

keep a customer

engage with the

brand. In other

words, it is the

measure of

customer’s

likeliness to repeat

buying with the

company.

Basically,

customer loyalty is

the result of

positive

experiences of

customers with the

brad in past along

with the overall

value that buyers

receive from a

theory of customer

satisfaction and loyalty

will be used so that the

respective company

can take suitable steps

to make further

improvements.

grow business in

current period of

time. Here,

customer loyalty is

about ongoing

emotional

relationships

between a brand

and its customers.

It describes the

way how willingly

keep a customer

engage with the

brand. In other

words, it is the

measure of

customer’s

likeliness to repeat

buying with the

company.

Basically,

customer loyalty is

the result of

positive

experiences of

customers with the

brad in past along

with the overall

value that buyers

receive from a

theory of customer

satisfaction and loyalty

will be used so that the

respective company

can take suitable steps

to make further

improvements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

particular business.

2 Service Quality OCBC

bank was

underperforming

comparatively to

its competitors and

in terms of other

loyalty metrics as

well. In context of

OCBC, bank it

faced complexity

in terms of

maintaining

loyalty and trust

among customers

regarding their

cards. As a result,

they recorded

decline in overall

sales of credit

cards and the

respective bank

got last rank

amongst the credit

card issuers within

the country. Based

on the two

important

measures such as

likelihood to use

the credit cards

SERVEQUAL is an

imperative model to

assess and analyze the

expectations and

perception of

customers regarding

the service. This

model is used to

identify the gaps

between expected and

actual services so that

the company can

improve their quality

of services with an aim

to fulfil the level of

expectations of buyers

in significant manner

2 Service Quality OCBC

bank was

underperforming

comparatively to

its competitors and

in terms of other

loyalty metrics as

well. In context of

OCBC, bank it

faced complexity

in terms of

maintaining

loyalty and trust

among customers

regarding their

cards. As a result,

they recorded

decline in overall

sales of credit

cards and the

respective bank

got last rank

amongst the credit

card issuers within

the country. Based

on the two

important

measures such as

likelihood to use

the credit cards

SERVEQUAL is an

imperative model to

assess and analyze the

expectations and

perception of

customers regarding

the service. This

model is used to

identify the gaps

between expected and

actual services so that

the company can

improve their quality

of services with an aim

to fulfil the level of

expectations of buyers

in significant manner

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

again and

likelihood to

recommend its

cards both were

ranked last that

reflects that the

company was

dealing with major

issues of trust and

loyalty among

customer groups.

Customer loyalty and satisfaction are interrelated to each-other (Machado, Karray and de

Sousa, 2019). When customers are satisfied, they are more likely to do repeat shopping from the

brand which further improves their loyalty in an efficient manner. Satisfied customers are the

key asset of the entity as they not only buy products frequently but also suggest such products or

services to others as well which enhances the overall revenue & profit of the brand significantly

(Jamshidi and Kuanova, 2020). In present scenario, the case study is based on analysis of

customer loyalty in terms of credit cards. Here, credit cards are one of the crucial financial

products which allow card holders to buy particular products or avail services when they do not

own sufficient money. In other words, credit cards are financial products through which a line of

credit is offered to the cardholders by which they can purchase necessary goods or services.

In context of present study, OCBC bank is taken into consideration that is one of the

popular banks based on Singapore. But, the credit card industry of the respective country is

highly competitive due to presence of ample of other brand which also offer credit cards to

individuals. There are eight major financial institutions along with OCBC which are also offering

credit cards and other financial products (Bataev, Koroleva and Gorovoy, 2019). By 2019, the

amount of transactions by using personal credit cards was nearly $43 billion which was 18.6%

high than 2015. But, the number of such cards in circulation have declined from 9.2 million to

likelihood to

recommend its

cards both were

ranked last that

reflects that the

company was

dealing with major

issues of trust and

loyalty among

customer groups.

Customer loyalty and satisfaction are interrelated to each-other (Machado, Karray and de

Sousa, 2019). When customers are satisfied, they are more likely to do repeat shopping from the

brand which further improves their loyalty in an efficient manner. Satisfied customers are the

key asset of the entity as they not only buy products frequently but also suggest such products or

services to others as well which enhances the overall revenue & profit of the brand significantly

(Jamshidi and Kuanova, 2020). In present scenario, the case study is based on analysis of

customer loyalty in terms of credit cards. Here, credit cards are one of the crucial financial

products which allow card holders to buy particular products or avail services when they do not

own sufficient money. In other words, credit cards are financial products through which a line of

credit is offered to the cardholders by which they can purchase necessary goods or services.

In context of present study, OCBC bank is taken into consideration that is one of the

popular banks based on Singapore. But, the credit card industry of the respective country is

highly competitive due to presence of ample of other brand which also offer credit cards to

individuals. There are eight major financial institutions along with OCBC which are also offering

credit cards and other financial products (Bataev, Koroleva and Gorovoy, 2019). By 2019, the

amount of transactions by using personal credit cards was nearly $43 billion which was 18.6%

high than 2015. But, the number of such cards in circulation have declined from 9.2 million to

8.9 million from 2015 to 2019. Therefore, the respective brand has to face high competition that

might affect their existing level of revenue and profit as well. The industry of credit cards has

been reached at saturation within the country as the customers are likely to cancel the cards as

they consider these cards are no longer useful (Awanis, 2017).

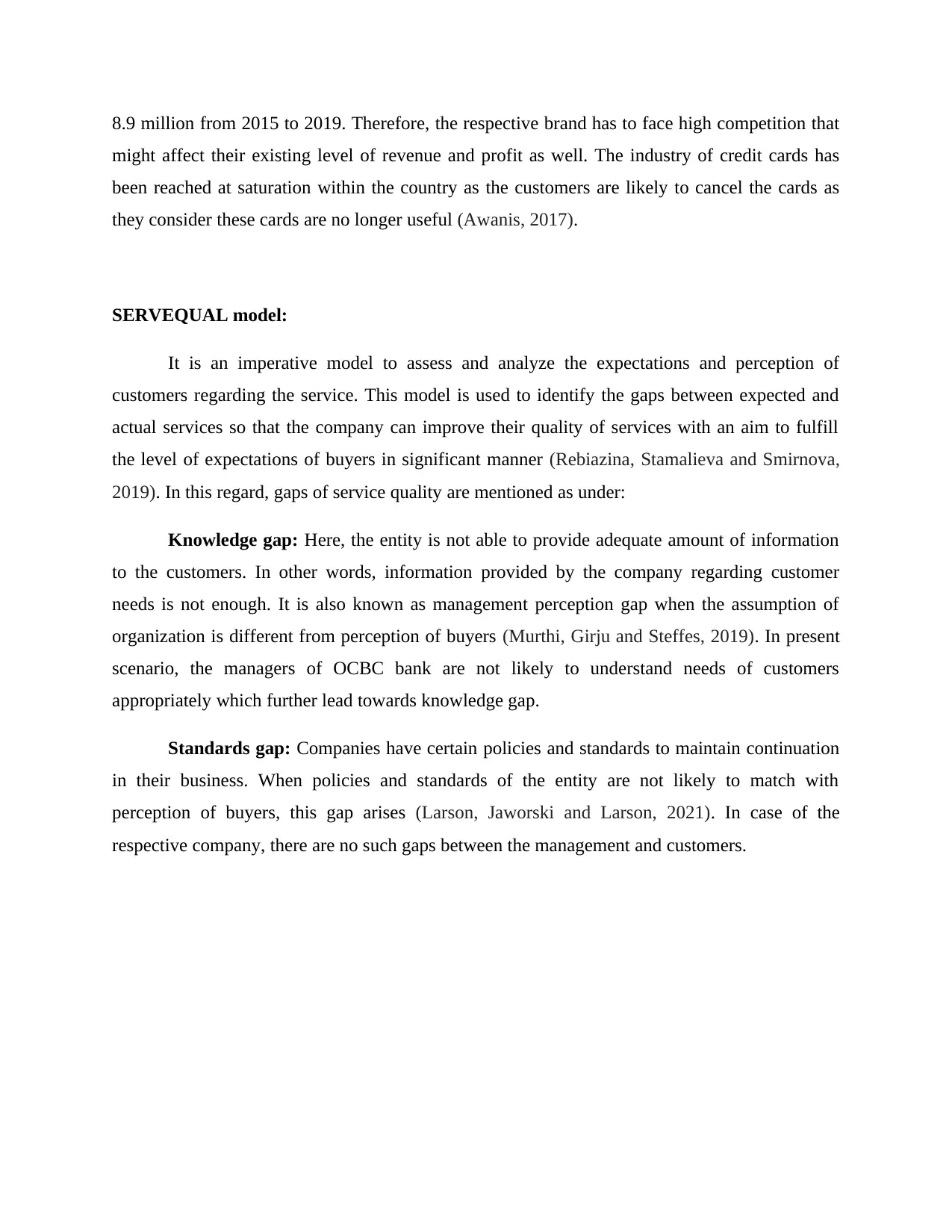

SERVEQUAL model:

It is an imperative model to assess and analyze the expectations and perception of

customers regarding the service. This model is used to identify the gaps between expected and

actual services so that the company can improve their quality of services with an aim to fulfill

the level of expectations of buyers in significant manner (Rebiazina, Stamalieva and Smirnova,

2019). In this regard, gaps of service quality are mentioned as under:

Knowledge gap: Here, the entity is not able to provide adequate amount of information

to the customers. In other words, information provided by the company regarding customer

needs is not enough. It is also known as management perception gap when the assumption of

organization is different from perception of buyers (Murthi, Girju and Steffes, 2019). In present

scenario, the managers of OCBC bank are not likely to understand needs of customers

appropriately which further lead towards knowledge gap.

Standards gap: Companies have certain policies and standards to maintain continuation

in their business. When policies and standards of the entity are not likely to match with

perception of buyers, this gap arises (Larson, Jaworski and Larson, 2021). In case of the

respective company, there are no such gaps between the management and customers.

might affect their existing level of revenue and profit as well. The industry of credit cards has

been reached at saturation within the country as the customers are likely to cancel the cards as

they consider these cards are no longer useful (Awanis, 2017).

SERVEQUAL model:

It is an imperative model to assess and analyze the expectations and perception of

customers regarding the service. This model is used to identify the gaps between expected and

actual services so that the company can improve their quality of services with an aim to fulfill

the level of expectations of buyers in significant manner (Rebiazina, Stamalieva and Smirnova,

2019). In this regard, gaps of service quality are mentioned as under:

Knowledge gap: Here, the entity is not able to provide adequate amount of information

to the customers. In other words, information provided by the company regarding customer

needs is not enough. It is also known as management perception gap when the assumption of

organization is different from perception of buyers (Murthi, Girju and Steffes, 2019). In present

scenario, the managers of OCBC bank are not likely to understand needs of customers

appropriately which further lead towards knowledge gap.

Standards gap: Companies have certain policies and standards to maintain continuation

in their business. When policies and standards of the entity are not likely to match with

perception of buyers, this gap arises (Larson, Jaworski and Larson, 2021). In case of the

respective company, there are no such gaps between the management and customers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

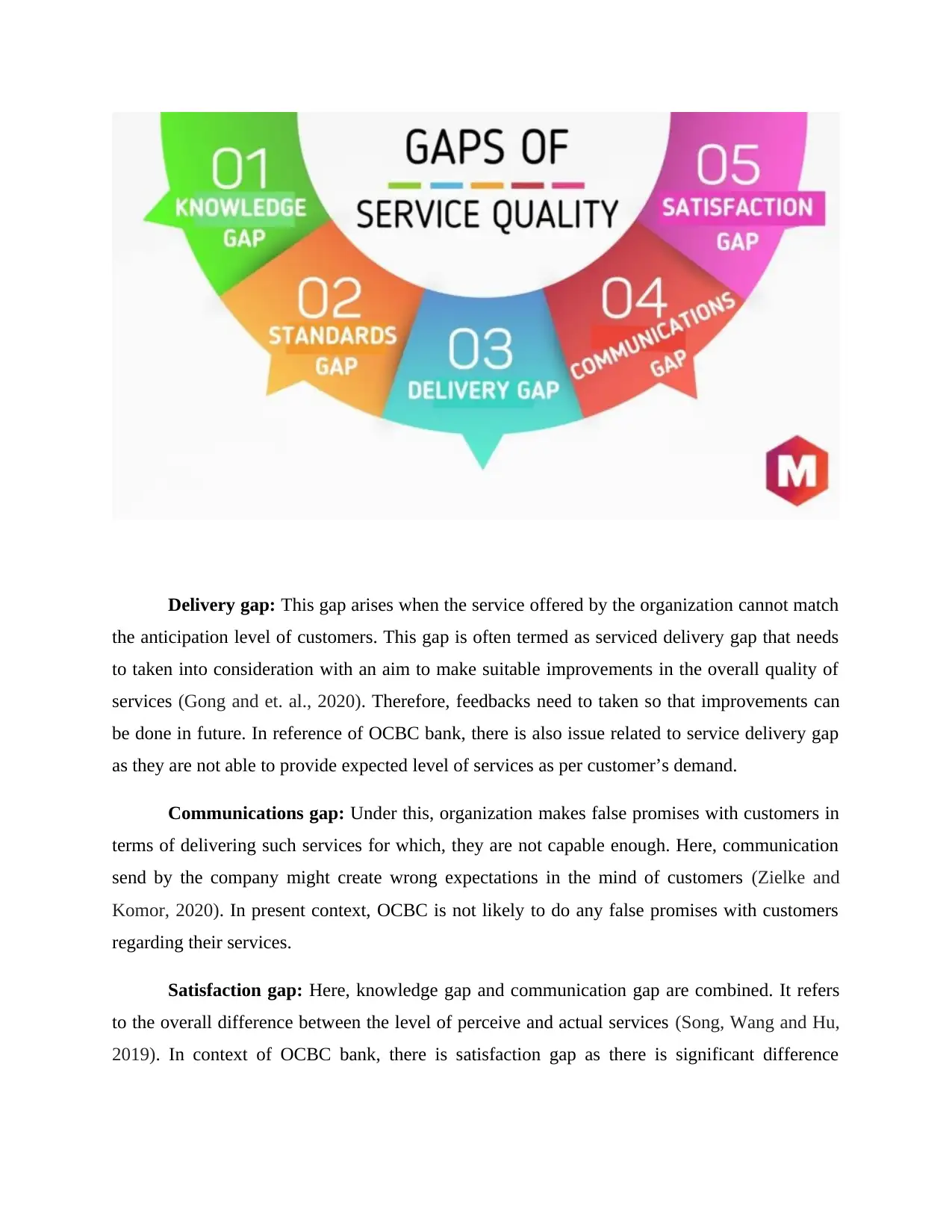

Delivery gap: This gap arises when the service offered by the organization cannot match

the anticipation level of customers. This gap is often termed as serviced delivery gap that needs

to taken into consideration with an aim to make suitable improvements in the overall quality of

services (Gong and et. al., 2020). Therefore, feedbacks need to taken so that improvements can

be done in future. In reference of OCBC bank, there is also issue related to service delivery gap

as they are not able to provide expected level of services as per customer’s demand.

Communications gap: Under this, organization makes false promises with customers in

terms of delivering such services for which, they are not capable enough. Here, communication

send by the company might create wrong expectations in the mind of customers (Zielke and

Komor, 2020). In present context, OCBC is not likely to do any false promises with customers

regarding their services.

Satisfaction gap: Here, knowledge gap and communication gap are combined. It refers

to the overall difference between the level of perceive and actual services (Song, Wang and Hu,

2019). In context of OCBC bank, there is satisfaction gap as there is significant difference

the anticipation level of customers. This gap is often termed as serviced delivery gap that needs

to taken into consideration with an aim to make suitable improvements in the overall quality of

services (Gong and et. al., 2020). Therefore, feedbacks need to taken so that improvements can

be done in future. In reference of OCBC bank, there is also issue related to service delivery gap

as they are not able to provide expected level of services as per customer’s demand.

Communications gap: Under this, organization makes false promises with customers in

terms of delivering such services for which, they are not capable enough. Here, communication

send by the company might create wrong expectations in the mind of customers (Zielke and

Komor, 2020). In present context, OCBC is not likely to do any false promises with customers

regarding their services.

Satisfaction gap: Here, knowledge gap and communication gap are combined. It refers

to the overall difference between the level of perceive and actual services (Song, Wang and Hu,

2019). In context of OCBC bank, there is satisfaction gap as there is significant difference

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

between actual services and perceived service level that will further affect the revenue & growth

of the company as well.

Analysis & Findings

OCBC is a popular bank that is known for offering financial and banking services to its

customers so that they can easily fulfill their financial goals. The main aim of the respective bank

is to offer numerous financial services to buyers such as loans, investment, credit cards, money

transfer and more. In the present time, the entity is facing issues in terms of minimizing the ratio

of credit card holders profoundly. It is analyzed that the customers are losing interest in the

services that are being offered by the respective business entity. Here, the respective bank is

facing complexity in terms of maintaining loyalty and trust among customers regarding their

cards. As a result, they recorded decline in overall sales of credit cards and the respective bank

got last rank amongst the credit card issuers within the country (Mohd Zulkifli and et. al., 2020).

Based on the two important measures such as likelihood to use the credit cards again and

likelihood to recommend its cards both were ranked last that reflects that the company was

dealing with major issues of trust and loyalty among customer groups. In terms of customer

satisfaction, OCBC bank was underperforming comparatively to its competitors and in terms of

other loyalty metrics as well.

Through the above analysis, it is found that OCBC bank is working within highly competitive

industry. There are numerous other banking & financial institutions which are giving intense

competition to the respective bank. Within the credit card industry, there is extensive

competition due to presence of numerous players named as DBC, UOB, Standard charted bank,

American Express and more. In credit card industry, the customers are likely to avail such cards

with an aim to get significant benefits in terms of targeted promotion, discounts and so on.

Cardholders are eligible to receive cashbacks and refunds out of their spending. In this regard,

cashback is provided in different forms in terms of direct offsetting of cardholders, credit card

bills and more. In addition to this, they are also likely to get reward points for their spending.

Here, these points can be further used to redeem vouchers or products and services in significant

manner (OCBC bank, 2022). As per the analysis of case study, it is analyzed that OCBC is used

to be one of the biggest card issuers in terms of transaction value by holding nearly 15.9% of

of the company as well.

Analysis & Findings

OCBC is a popular bank that is known for offering financial and banking services to its

customers so that they can easily fulfill their financial goals. The main aim of the respective bank

is to offer numerous financial services to buyers such as loans, investment, credit cards, money

transfer and more. In the present time, the entity is facing issues in terms of minimizing the ratio

of credit card holders profoundly. It is analyzed that the customers are losing interest in the

services that are being offered by the respective business entity. Here, the respective bank is

facing complexity in terms of maintaining loyalty and trust among customers regarding their

cards. As a result, they recorded decline in overall sales of credit cards and the respective bank

got last rank amongst the credit card issuers within the country (Mohd Zulkifli and et. al., 2020).

Based on the two important measures such as likelihood to use the credit cards again and

likelihood to recommend its cards both were ranked last that reflects that the company was

dealing with major issues of trust and loyalty among customer groups. In terms of customer

satisfaction, OCBC bank was underperforming comparatively to its competitors and in terms of

other loyalty metrics as well.

Through the above analysis, it is found that OCBC bank is working within highly competitive

industry. There are numerous other banking & financial institutions which are giving intense

competition to the respective bank. Within the credit card industry, there is extensive

competition due to presence of numerous players named as DBC, UOB, Standard charted bank,

American Express and more. In credit card industry, the customers are likely to avail such cards

with an aim to get significant benefits in terms of targeted promotion, discounts and so on.

Cardholders are eligible to receive cashbacks and refunds out of their spending. In this regard,

cashback is provided in different forms in terms of direct offsetting of cardholders, credit card

bills and more. In addition to this, they are also likely to get reward points for their spending.

Here, these points can be further used to redeem vouchers or products and services in significant

manner (OCBC bank, 2022). As per the analysis of case study, it is analyzed that OCBC is used

to be one of the biggest card issuers in terms of transaction value by holding nearly 15.9% of

market share whereas the top two issuer’s names as UOB and DBS used to acquire 26.9% and

20.3% market share respectively. In this regard, the respective banking institution is likely to

offer different types of credit cards such as 365 card, NTUC plus credit card, frank credit card,

cashflow master cards, voyage cards and so on. Different cards are offered different benefits like

cashback on travel, food delivery an more (Kessentini and Jeffers, 2018). By using NTUC plus

card, it is easy to get cashback and saving the fuel related expenses. There is also cashflow

master card which provides benefits in terms of auto-installment card where payment can be spilt

and it also offers nearly 1% rebate on all the spending. By offering such benefits, the respective

entity ensures to get attention of more and more number of people to avail the facilities of credit

cards.

After going through with above-analysis, it is found that OCBC bank is facing problems

in terms of customer loyalty and satisfaction that direct affects their sales and revenue. The

respective bank found underperforming comparatively to other competitors such as UOB and

DBS bank. As a result, they start losing trust of customers which minimize their sale of credit

cards. Through application of SERVEQUAL model, it is identified that the respective entity is

facing ample of gaps in terms of knowledge gap, communication gap, satisfaction gap and more.

It is monitored that OCBC bank is offering different types of credit cards for the benefit of its

customers. But they are unable to share this knowledge with customers in proper way. In

addition to this, they are also facing communication gap in terms of exchanging necessary

information with customers in significant manner. Furthermore, the company is encountering

significant issues in terms of maintaining high level of customer’s loyalty and satisfaction. This

will directly affect their current positioning along with existing level of revenue and profit

margin. To maintain strong position in the competitive market place, the respective entity is

required to improve their services so that demand of their products increases in market place in

significant manner.

Proposed solution to the problem

From the above-discussion, it is found that OCBC bank is facing profound issue in terms

of lack of customer loyalty and satisfaction. They are working within finance and banking

industry of Singapore that is really competitive. Here, numerous financial institutions are already

20.3% market share respectively. In this regard, the respective banking institution is likely to

offer different types of credit cards such as 365 card, NTUC plus credit card, frank credit card,

cashflow master cards, voyage cards and so on. Different cards are offered different benefits like

cashback on travel, food delivery an more (Kessentini and Jeffers, 2018). By using NTUC plus

card, it is easy to get cashback and saving the fuel related expenses. There is also cashflow

master card which provides benefits in terms of auto-installment card where payment can be spilt

and it also offers nearly 1% rebate on all the spending. By offering such benefits, the respective

entity ensures to get attention of more and more number of people to avail the facilities of credit

cards.

After going through with above-analysis, it is found that OCBC bank is facing problems

in terms of customer loyalty and satisfaction that direct affects their sales and revenue. The

respective bank found underperforming comparatively to other competitors such as UOB and

DBS bank. As a result, they start losing trust of customers which minimize their sale of credit

cards. Through application of SERVEQUAL model, it is identified that the respective entity is

facing ample of gaps in terms of knowledge gap, communication gap, satisfaction gap and more.

It is monitored that OCBC bank is offering different types of credit cards for the benefit of its

customers. But they are unable to share this knowledge with customers in proper way. In

addition to this, they are also facing communication gap in terms of exchanging necessary

information with customers in significant manner. Furthermore, the company is encountering

significant issues in terms of maintaining high level of customer’s loyalty and satisfaction. This

will directly affect their current positioning along with existing level of revenue and profit

margin. To maintain strong position in the competitive market place, the respective entity is

required to improve their services so that demand of their products increases in market place in

significant manner.

Proposed solution to the problem

From the above-discussion, it is found that OCBC bank is facing profound issue in terms

of lack of customer loyalty and satisfaction. They are working within finance and banking

industry of Singapore that is really competitive. Here, numerous financial institutions are already

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.