A Comprehensive Financial Comparison of OCBC Bank and DBS Bank

VerifiedAdded on 2023/03/23

|9

|2957

|35

Report

AI Summary

This report provides a comparative financial analysis of OCBC Bank and DBS Bank, two prominent banks in Singapore. It begins with an introduction to each bank, detailing their history, services, subsidiaries, and key personnel. The analysis focuses on the service networks of both banks, including branches, ATMs, and online banking platforms, highlighting DBS's digital transformation and OCBC's widespread ATM network. The report then delves into a historical analysis of financial performance, examining growth rates in assets and deposits for both banks over the past three years. Profitability ratios, such as gross margin, return on assets, and return on equity, are calculated and compared. The analysis concludes that while both banks have shown substantial growth, DBS demonstrates more stability in asset growth and deposit rates, making it a potentially more attractive target for a takeover due to its strong asset base and consistent customer trust.

1

BANKING AND FINANCE

By Students Name

Course Name

Professor’s name

Institution

Date

BANKING AND FINANCE

By Students Name

Course Name

Professor’s name

Institution

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Introduction

OCBC Bank

OCBC Bank is a public multinational Chinese bank in Singapore that serves the Asian- Pacific

area with its headquarters in Singapore. The bank was founded in 1932, making its operations

years 32 to date. It operates in the banking industry with financial services as its main product.

The services it renders include;

Investment banking

Corporate banking

Private banking

Retail banking

Treasury management

The bank had an operating revenue of S$5,097 billion with net revenue totaling S$5,89 for the

financial year 2018 and revenue of S$25 billion for the current year. O.C.B.C bank has assets

worth S$469.53 in the current year and equity totaling S$43.3 billion for the financial year

20181. The bank has seven subsidiaries that include; O.C.B.C N.I.S.P Bank, Bank of Singapore,

O.C.B.C Wing Hang Bank, Great Eastern Life, O.C.B.C Al-Amin, Lion Global Investors

O.C.B.C securities, and O.C.B.C Securitas. The bank has a total of 29,000 employees working it

its main branch and subsidiaries. The bank has a credit rating of AA- from Standards and poor

and Aa1 and AA- for Moody’s and Fitch ratings respectively. The key people in O.C.B.C bank

are Ooi Sang Kuang, and Samuel Tsien the chairman and the CEO, respectively. The bank trades

as SGX in the Straits Times Index. The main shareholders include Citibank Nominees Singapore

Pte Ltd who control 17.41%, Selat P.T.E ltd controlling 11.04%, D.B.S nominees controlling

9.26%, H.S.B.C (Singapore) controlling 4.63%, Lee Foundation controlling 4.34% among others

DBS Bank

DBS Bank is a publicly traded bank with its headquarters in Marina Bay, Singapore. It was

founded in 1968 making the current year the 68th year of operation. The main formation aims of

the bank loaned provision and financial aid to processing and manufacturing industries as well as

upgrade as well as establish existing industries2. The bank serves South East Asia and as well as

1 OCBC bank annual reports (2018). Retrieved from https://www.ocbc.com/group/investors/annual-

reports.html

2 DBS bank annual reports (2018). Retrieved from https://www.dbs.com/investor/group-annual-

reports.html

Introduction

OCBC Bank

OCBC Bank is a public multinational Chinese bank in Singapore that serves the Asian- Pacific

area with its headquarters in Singapore. The bank was founded in 1932, making its operations

years 32 to date. It operates in the banking industry with financial services as its main product.

The services it renders include;

Investment banking

Corporate banking

Private banking

Retail banking

Treasury management

The bank had an operating revenue of S$5,097 billion with net revenue totaling S$5,89 for the

financial year 2018 and revenue of S$25 billion for the current year. O.C.B.C bank has assets

worth S$469.53 in the current year and equity totaling S$43.3 billion for the financial year

20181. The bank has seven subsidiaries that include; O.C.B.C N.I.S.P Bank, Bank of Singapore,

O.C.B.C Wing Hang Bank, Great Eastern Life, O.C.B.C Al-Amin, Lion Global Investors

O.C.B.C securities, and O.C.B.C Securitas. The bank has a total of 29,000 employees working it

its main branch and subsidiaries. The bank has a credit rating of AA- from Standards and poor

and Aa1 and AA- for Moody’s and Fitch ratings respectively. The key people in O.C.B.C bank

are Ooi Sang Kuang, and Samuel Tsien the chairman and the CEO, respectively. The bank trades

as SGX in the Straits Times Index. The main shareholders include Citibank Nominees Singapore

Pte Ltd who control 17.41%, Selat P.T.E ltd controlling 11.04%, D.B.S nominees controlling

9.26%, H.S.B.C (Singapore) controlling 4.63%, Lee Foundation controlling 4.34% among others

DBS Bank

DBS Bank is a publicly traded bank with its headquarters in Marina Bay, Singapore. It was

founded in 1968 making the current year the 68th year of operation. The main formation aims of

the bank loaned provision and financial aid to processing and manufacturing industries as well as

upgrade as well as establish existing industries2. The bank serves South East Asia and as well as

1 OCBC bank annual reports (2018). Retrieved from https://www.ocbc.com/group/investors/annual-

reports.html

2 DBS bank annual reports (2018). Retrieved from https://www.dbs.com/investor/group-annual-

reports.html

3

East Asia. The current key people are Peter Seah Huat as chairman and Piyush Gupta as CEO.

The bank's product is financial services but has eight services that include retail banking. DBS

has one subsidiary DBS Bank of India with a total of 24,174 employees (2017). The bank's

revenue totaled S$12,473 in 2018and the total assets totaled S$ 550, 751billion with S$ 500,876

billion liabilities. DBS Bank has a strong market with controlling share in Temasek Holdings.

The credit rating for the bank is good as indicated by AA-ratings from standards and poor, Aa1

from Moody’s and AA- from Fitch Ratings.

Service Networks of DBS and OCBC

The service networks for the banking industry include its branches, ATMs, telephone centers,

mobile banking, and online banking.

DBS

DBS adopted digital transformation in 2009 and has since then witnessed grown in digital

banking3. This included embracing ATMs that existed way before 2009, mobile banking,

telephone centers, internet banking, and branches

ATMs- DBS the bank prides in a number of network services ATMs, online banking as well as

internet banking. The bank has 1,100ATMs spread across fifty cities and operates in seventeen

markets.

Internet Banking-The services have greatly decongested the banking halls. In the wake of

mobile banking, DBS embraced mobile baking through the digibank that enables users to open

savings accounts as well as perform other transaction over the phone. The bank has hit 1.8

million mobile users over a span of two years and the growth is expected to be consistent

Online Banking-On internet banking the DBS iBanking is available, enabling new users to

register and use the service. The service is currently being utilized by 550,000 users and is

expected to grow over the years4. The bank is expanding its networks as well in the sector in

order to expand its operations and ease banking in the halls. The embrace of internet banking is

also meant to provide a convenient solution to personal banking.

Branches- The bank operates more than 2,300 BDS branches and self-service centers in Asia. It

is among the leading in terms of market share serving over 4.6 million clients. In greater China,

3 Auerbach, Alan J., ed. Corporate takeovers: Causes and consequences. University of Chicago Press,

2013. 4 Venardos, Angelo M. Islamic banking & finance in South-East Asia: Its development & future. Vol. 6.

World Scientific, 2012.

East Asia. The current key people are Peter Seah Huat as chairman and Piyush Gupta as CEO.

The bank's product is financial services but has eight services that include retail banking. DBS

has one subsidiary DBS Bank of India with a total of 24,174 employees (2017). The bank's

revenue totaled S$12,473 in 2018and the total assets totaled S$ 550, 751billion with S$ 500,876

billion liabilities. DBS Bank has a strong market with controlling share in Temasek Holdings.

The credit rating for the bank is good as indicated by AA-ratings from standards and poor, Aa1

from Moody’s and AA- from Fitch Ratings.

Service Networks of DBS and OCBC

The service networks for the banking industry include its branches, ATMs, telephone centers,

mobile banking, and online banking.

DBS

DBS adopted digital transformation in 2009 and has since then witnessed grown in digital

banking3. This included embracing ATMs that existed way before 2009, mobile banking,

telephone centers, internet banking, and branches

ATMs- DBS the bank prides in a number of network services ATMs, online banking as well as

internet banking. The bank has 1,100ATMs spread across fifty cities and operates in seventeen

markets.

Internet Banking-The services have greatly decongested the banking halls. In the wake of

mobile banking, DBS embraced mobile baking through the digibank that enables users to open

savings accounts as well as perform other transaction over the phone. The bank has hit 1.8

million mobile users over a span of two years and the growth is expected to be consistent

Online Banking-On internet banking the DBS iBanking is available, enabling new users to

register and use the service. The service is currently being utilized by 550,000 users and is

expected to grow over the years4. The bank is expanding its networks as well in the sector in

order to expand its operations and ease banking in the halls. The embrace of internet banking is

also meant to provide a convenient solution to personal banking.

Branches- The bank operates more than 2,300 BDS branches and self-service centers in Asia. It

is among the leading in terms of market share serving over 4.6 million clients. In greater China,

3 Auerbach, Alan J., ed. Corporate takeovers: Causes and consequences. University of Chicago Press,

2013. 4 Venardos, Angelo M. Islamic banking & finance in South-East Asia: Its development & future. Vol. 6.

World Scientific, 2012.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

the branches are 50 in Hong Kong, 29 in China, and 43 branches in Taiwan5. In South West Asia

there are 12 branches in India, and 39 branches in Indonesia spread over 11 major cities.

OCBC

In service networks, OCBC has a wide range of service networks that decongest the banks as

well as provide a more convenient way for clients to be served. The services and widespread

with products that differ according to the network service utilized.

Branches- OCBC has branches in various regions that include one in Australia, one in Brunei,

four in China, four in Hong Kong, one in Japan, two in Malaysia, one in South Korea, one in

Taiwan, one in Thailand, one in the United Kingdom, two in the USA and one branch in

Vietnam.

ATMs- The bank has over 1,200 ATMs spread across the entire island. With up to five million

ATM transactions recorded over a year, the bank is rich in networks.

Internet banking- For OCBC mobile, the service is available to users registered with velocity.

These users are able to use the mobile app to transact.

Analysis of Previous Performance

This involves the use of historical data on financial performance. The analysis is relevant in

predicting future trends.

Growth Rate in Assets

DBS

The assets of DBS have grown substantially over the three years of 2016, 2017, and2018. In

2017 assets grew by s$ 36,141billion to S$ 517,711billionfrom the previous S$481,570billion in

20166. These assets grew further in 2018 from S$ 517,711billion to S$ 550,751billion this is a

growth of S$33,040billion. The assets of the company have been growing over time although the

growth in 2018 is lower than the previous year

OCBC

The Assets of OCBC have grown substantially basing on the financial statements for the last

three years 2016,2017 and 2018. In 2016 the assets grew from S$ 409,883.560billion to S$

5 Chatterjee, Sris, Kose John, and An Yan. "Takeovers and divergence of investor opinion." The Review of

Financial Studies 25, no. 1 (2012): 227-277.

6 Delen, Dursun, Cemil Kuzey, and Ali Uyar. "Measuring firm performance using financial ratios: A

decision tree approach." Expert Systems with Applications 40, no. 10 (2013): 3970-3983.

the branches are 50 in Hong Kong, 29 in China, and 43 branches in Taiwan5. In South West Asia

there are 12 branches in India, and 39 branches in Indonesia spread over 11 major cities.

OCBC

In service networks, OCBC has a wide range of service networks that decongest the banks as

well as provide a more convenient way for clients to be served. The services and widespread

with products that differ according to the network service utilized.

Branches- OCBC has branches in various regions that include one in Australia, one in Brunei,

four in China, four in Hong Kong, one in Japan, two in Malaysia, one in South Korea, one in

Taiwan, one in Thailand, one in the United Kingdom, two in the USA and one branch in

Vietnam.

ATMs- The bank has over 1,200 ATMs spread across the entire island. With up to five million

ATM transactions recorded over a year, the bank is rich in networks.

Internet banking- For OCBC mobile, the service is available to users registered with velocity.

These users are able to use the mobile app to transact.

Analysis of Previous Performance

This involves the use of historical data on financial performance. The analysis is relevant in

predicting future trends.

Growth Rate in Assets

DBS

The assets of DBS have grown substantially over the three years of 2016, 2017, and2018. In

2017 assets grew by s$ 36,141billion to S$ 517,711billionfrom the previous S$481,570billion in

20166. These assets grew further in 2018 from S$ 517,711billion to S$ 550,751billion this is a

growth of S$33,040billion. The assets of the company have been growing over time although the

growth in 2018 is lower than the previous year

OCBC

The Assets of OCBC have grown substantially basing on the financial statements for the last

three years 2016,2017 and 2018. In 2016 the assets grew from S$ 409,883.560billion to S$

5 Chatterjee, Sris, Kose John, and An Yan. "Takeovers and divergence of investor opinion." The Review of

Financial Studies 25, no. 1 (2012): 227-277.

6 Delen, Dursun, Cemil Kuzey, and Ali Uyar. "Measuring firm performance using financial ratios: A

decision tree approach." Expert Systems with Applications 40, no. 10 (2013): 3970-3983.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

454,938.337 billion in 2017, making a difference in the growth of S$ 45,054.777billion in 2018

the assets grew by S$ 12,604.633 billion to S$467,543.00billion.

Deposit Growth

DBS

The deposit growth has been rising for DBS from percentage growth of 7.8% in 2015 to 8.1%

and 9.4% in 2017 this is an indicator of how the customers are comfortable with depositing funds

in the bank. The growth is an indicator of trust to the bank.

OCBC

The deposit growth rate for OCBC is falling drastically with a sharp increase from 20% in 2015

to 8% in 2016 and 6% in 2016. This is an indicator of negative trust between the customers and

the bank

Profitability Ratios

Gross margin ratio

This ratio basically articulates of the profitability of the company7. It also demonstrates the

amount it cost to produce the product, and it can be calculated by dividing the gross profit and

net sales.

Gross margin ratio DBS OCBC

Net sales 5,656,000 4,492,000

Gross profit 12,537,000 9,413,000

Gross margin ratio 45.11% 53.03%

Return on assets

This ratio measures how the company is efficient in producing revenue from its assets. This can

be calculated by dividing the net revenue for the present period by the value of the total company

assets.

Return on assets DBS OCBC

Net sales 5,656,000 4,492,000

Total Assets 550,738,000 467,543,000

Return on assets 1.03% 0.96%

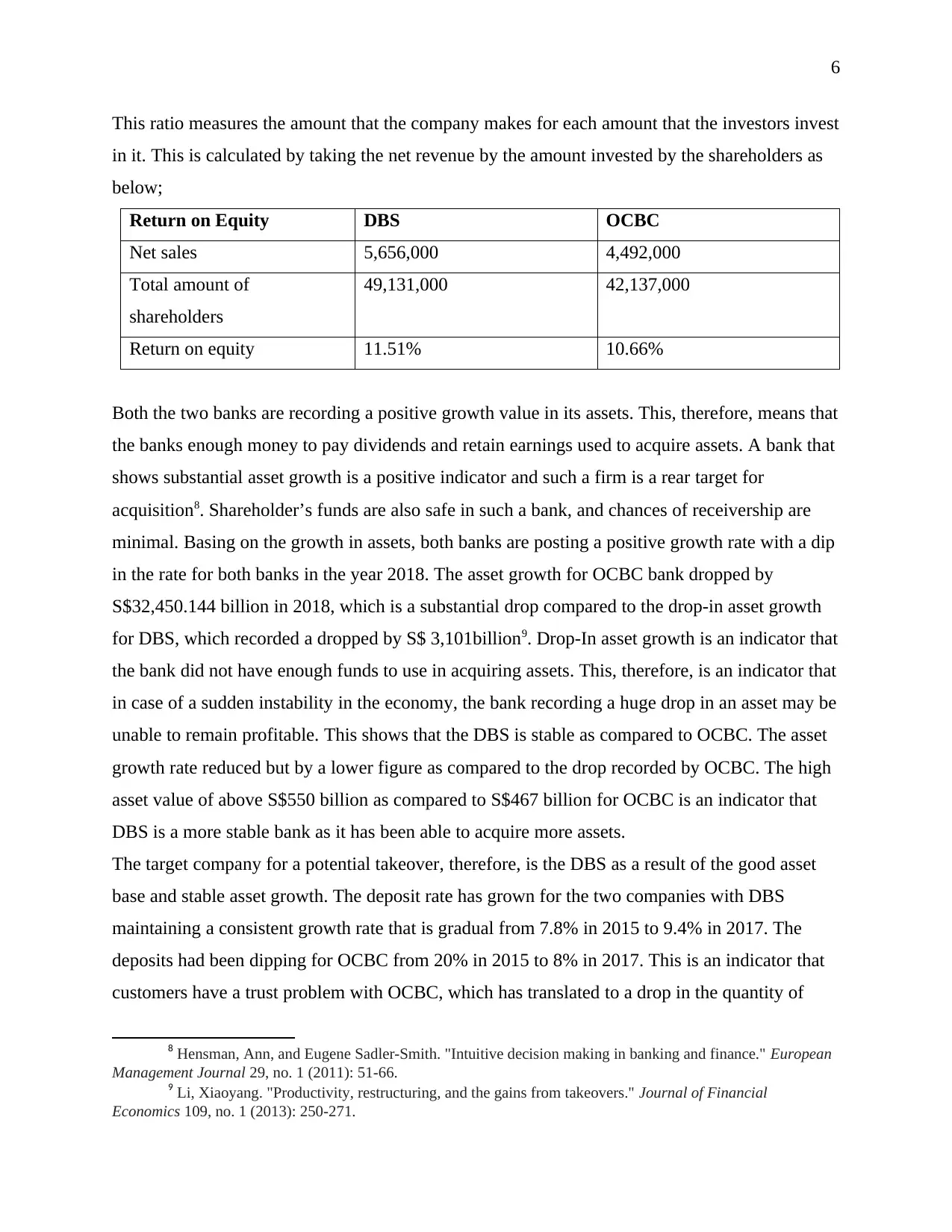

Return on Equity

7 Edmans, Alex, Itay Goldstein, and Wei Jiang. "The real effects of financial markets: The impact of prices

on takeovers." The Journal of Finance 67, no. 3 (2012): 933-971.

454,938.337 billion in 2017, making a difference in the growth of S$ 45,054.777billion in 2018

the assets grew by S$ 12,604.633 billion to S$467,543.00billion.

Deposit Growth

DBS

The deposit growth has been rising for DBS from percentage growth of 7.8% in 2015 to 8.1%

and 9.4% in 2017 this is an indicator of how the customers are comfortable with depositing funds

in the bank. The growth is an indicator of trust to the bank.

OCBC

The deposit growth rate for OCBC is falling drastically with a sharp increase from 20% in 2015

to 8% in 2016 and 6% in 2016. This is an indicator of negative trust between the customers and

the bank

Profitability Ratios

Gross margin ratio

This ratio basically articulates of the profitability of the company7. It also demonstrates the

amount it cost to produce the product, and it can be calculated by dividing the gross profit and

net sales.

Gross margin ratio DBS OCBC

Net sales 5,656,000 4,492,000

Gross profit 12,537,000 9,413,000

Gross margin ratio 45.11% 53.03%

Return on assets

This ratio measures how the company is efficient in producing revenue from its assets. This can

be calculated by dividing the net revenue for the present period by the value of the total company

assets.

Return on assets DBS OCBC

Net sales 5,656,000 4,492,000

Total Assets 550,738,000 467,543,000

Return on assets 1.03% 0.96%

Return on Equity

7 Edmans, Alex, Itay Goldstein, and Wei Jiang. "The real effects of financial markets: The impact of prices

on takeovers." The Journal of Finance 67, no. 3 (2012): 933-971.

6

This ratio measures the amount that the company makes for each amount that the investors invest

in it. This is calculated by taking the net revenue by the amount invested by the shareholders as

below;

Return on Equity DBS OCBC

Net sales 5,656,000 4,492,000

Total amount of

shareholders

49,131,000 42,137,000

Return on equity 11.51% 10.66%

Both the two banks are recording a positive growth value in its assets. This, therefore, means that

the banks enough money to pay dividends and retain earnings used to acquire assets. A bank that

shows substantial asset growth is a positive indicator and such a firm is a rear target for

acquisition8. Shareholder’s funds are also safe in such a bank, and chances of receivership are

minimal. Basing on the growth in assets, both banks are posting a positive growth rate with a dip

in the rate for both banks in the year 2018. The asset growth for OCBC bank dropped by

S$32,450.144 billion in 2018, which is a substantial drop compared to the drop-in asset growth

for DBS, which recorded a dropped by S$ 3,101billion9. Drop-In asset growth is an indicator that

the bank did not have enough funds to use in acquiring assets. This, therefore, is an indicator that

in case of a sudden instability in the economy, the bank recording a huge drop in an asset may be

unable to remain profitable. This shows that the DBS is stable as compared to OCBC. The asset

growth rate reduced but by a lower figure as compared to the drop recorded by OCBC. The high

asset value of above S$550 billion as compared to S$467 billion for OCBC is an indicator that

DBS is a more stable bank as it has been able to acquire more assets.

The target company for a potential takeover, therefore, is the DBS as a result of the good asset

base and stable asset growth. The deposit rate has grown for the two companies with DBS

maintaining a consistent growth rate that is gradual from 7.8% in 2015 to 9.4% in 2017. The

deposits had been dipping for OCBC from 20% in 2015 to 8% in 2017. This is an indicator that

customers have a trust problem with OCBC, which has translated to a drop in the quantity of

8 Hensman, Ann, and Eugene Sadler-Smith. "Intuitive decision making in banking and finance." European

Management Journal 29, no. 1 (2011): 51-66.

9 Li, Xiaoyang. "Productivity, restructuring, and the gains from takeovers." Journal of Financial

Economics 109, no. 1 (2013): 250-271.

This ratio measures the amount that the company makes for each amount that the investors invest

in it. This is calculated by taking the net revenue by the amount invested by the shareholders as

below;

Return on Equity DBS OCBC

Net sales 5,656,000 4,492,000

Total amount of

shareholders

49,131,000 42,137,000

Return on equity 11.51% 10.66%

Both the two banks are recording a positive growth value in its assets. This, therefore, means that

the banks enough money to pay dividends and retain earnings used to acquire assets. A bank that

shows substantial asset growth is a positive indicator and such a firm is a rear target for

acquisition8. Shareholder’s funds are also safe in such a bank, and chances of receivership are

minimal. Basing on the growth in assets, both banks are posting a positive growth rate with a dip

in the rate for both banks in the year 2018. The asset growth for OCBC bank dropped by

S$32,450.144 billion in 2018, which is a substantial drop compared to the drop-in asset growth

for DBS, which recorded a dropped by S$ 3,101billion9. Drop-In asset growth is an indicator that

the bank did not have enough funds to use in acquiring assets. This, therefore, is an indicator that

in case of a sudden instability in the economy, the bank recording a huge drop in an asset may be

unable to remain profitable. This shows that the DBS is stable as compared to OCBC. The asset

growth rate reduced but by a lower figure as compared to the drop recorded by OCBC. The high

asset value of above S$550 billion as compared to S$467 billion for OCBC is an indicator that

DBS is a more stable bank as it has been able to acquire more assets.

The target company for a potential takeover, therefore, is the DBS as a result of the good asset

base and stable asset growth. The deposit rate has grown for the two companies with DBS

maintaining a consistent growth rate that is gradual from 7.8% in 2015 to 9.4% in 2017. The

deposits had been dipping for OCBC from 20% in 2015 to 8% in 2017. This is an indicator that

customers have a trust problem with OCBC, which has translated to a drop in the quantity of

8 Hensman, Ann, and Eugene Sadler-Smith. "Intuitive decision making in banking and finance." European

Management Journal 29, no. 1 (2011): 51-66.

9 Li, Xiaoyang. "Productivity, restructuring, and the gains from takeovers." Journal of Financial

Economics 109, no. 1 (2013): 250-271.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

deposits. On the other hand, DBS is making gradual progress in the percentage of deposits. This

gradual growth means the bank is building a positive reputation in its area of operation. The

customer deposits are funds that will be available for investments, and a positive growth means

that the bank is able to take more investments will result in better growth. The growth in the

deposit is also a sign that the bank will have a higher return to its investors from the interest

earned from savings. Based on this evaluation, the DBS bank is a prime target for a takeover as

the likelihood of growth in the customer savings is higher than as compared to its counterpart

OCBC10.

Based on the evaluation of background and growth, the two banks have grown substantially over

the years with OCBC having recorded higher growth11. However, the low number of employees

in OCBC as compared to DBS could be the reason behind the poor performance recorded by the

company. DBS must be investing in employees, which translate to better quality performance. A

large number of subsidiaries for OCBC could be the reason behind the underperformance12. The

translation of the performance is a great challenge in addition to expansion to areas that proper

research has not been conducted. The two banks, however, have good credit ratings in the

market, but DBS has been ranked the best performing bank in the region while OCBC is among

the best five.

Conclusion

For a takeover, the target company should always have positive growth to ensure that the

takeover is successful. The two banks have positive growth, but DBS is posting better growth as

compared to the counterpart OCBC. Having many subsidiaries, OCBC is not the best target

based on the fact that the bank is already going through financial challenges. Despite the

advantage of expansion to a wider area of coverage, OCBC is not the best candidate.

Recommendation

Basically, based on the above analysis and the ratio analysis, taking over DBS and expanding

gradually could yield better than taking over OCBC. Therefore, taking over OCBC will mean

that the takeover will have to handle matters of restructuring the bank. This will consume a lot of

10 Petersen, Christian Vriborg, and Thomas Plenborg. Financial statement analysis: valuation, credit

analysis and executive compensation. Pearson Longman, 2012.

11 Lin, Fengyi, Deron Liang, and Enchia Chen. Financial ratio selection for business crisis

prediction. Expert Systems with Applications 38, no. 12 (2011): 15094-15102.

12 Morris, Tim. Innovations in Banking (RLE: Banking & Finance): Business Strategies and Employee

Relations. Routledge, 2012.

deposits. On the other hand, DBS is making gradual progress in the percentage of deposits. This

gradual growth means the bank is building a positive reputation in its area of operation. The

customer deposits are funds that will be available for investments, and a positive growth means

that the bank is able to take more investments will result in better growth. The growth in the

deposit is also a sign that the bank will have a higher return to its investors from the interest

earned from savings. Based on this evaluation, the DBS bank is a prime target for a takeover as

the likelihood of growth in the customer savings is higher than as compared to its counterpart

OCBC10.

Based on the evaluation of background and growth, the two banks have grown substantially over

the years with OCBC having recorded higher growth11. However, the low number of employees

in OCBC as compared to DBS could be the reason behind the poor performance recorded by the

company. DBS must be investing in employees, which translate to better quality performance. A

large number of subsidiaries for OCBC could be the reason behind the underperformance12. The

translation of the performance is a great challenge in addition to expansion to areas that proper

research has not been conducted. The two banks, however, have good credit ratings in the

market, but DBS has been ranked the best performing bank in the region while OCBC is among

the best five.

Conclusion

For a takeover, the target company should always have positive growth to ensure that the

takeover is successful. The two banks have positive growth, but DBS is posting better growth as

compared to the counterpart OCBC. Having many subsidiaries, OCBC is not the best target

based on the fact that the bank is already going through financial challenges. Despite the

advantage of expansion to a wider area of coverage, OCBC is not the best candidate.

Recommendation

Basically, based on the above analysis and the ratio analysis, taking over DBS and expanding

gradually could yield better than taking over OCBC. Therefore, taking over OCBC will mean

that the takeover will have to handle matters of restructuring the bank. This will consume a lot of

10 Petersen, Christian Vriborg, and Thomas Plenborg. Financial statement analysis: valuation, credit

analysis and executive compensation. Pearson Longman, 2012.

11 Lin, Fengyi, Deron Liang, and Enchia Chen. Financial ratio selection for business crisis

prediction. Expert Systems with Applications 38, no. 12 (2011): 15094-15102.

12 Morris, Tim. Innovations in Banking (RLE: Banking & Finance): Business Strategies and Employee

Relations. Routledge, 2012.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

money and time, and as a result, the takeover may take too long to yield positive results. The best

target for the takeover is, therefore, DBS, and the chances of success are higher, and this will

basically increase the overall revenue for the company.

money and time, and as a result, the takeover may take too long to yield positive results. The best

target for the takeover is, therefore, DBS, and the chances of success are higher, and this will

basically increase the overall revenue for the company.

9

Bibliography

Auerbach, Alan J., ed. Corporate Takeovers: Causes and consequences. University of Chicago

Press, 2013.

Chatterjee, Sris, Kose John, and An Yan. "Takeovers and divergence of investor opinion." The

Review of Financial Studies 25, no. 1 (2012): 227-277.

Delen, Dursun, Cemil Kuzey, and Ali Uyar. "Measuring firm performance using financial ratios:

A decision tree approach." Expert Systems with Applications 40, no. 10 (2013): 3970-

3983.

DBS bank annual reports (2018). Retrieved from

https://www.dbs.com/investor/group-annual-reports.html

Edmans, Alex, Itay Goldstein, and Wei Jiang. "The real effects of financial markets: The impact

of prices on takeovers." The Journal of Finance 67, no. 3 (2012): 933-971.

Hensman, Ann, and Eugene Sadler-Smith. "Intuitive decision making in banking and

finance." European Management Journal 29, no. 1 (2011): 51-66.

Li, Xiaoyang. "Productivity, restructuring, and the gains from takeovers." Journal of Financial

Economics 109, no. 1 (2013): 250-271.

Lin, Fengyi, Deron Liang, and Enchia Chen. Financial ratio selection for business crisis

prediction. Expert Systems with Applications 38, no. 12 (2011): 15094-15102.

Morris, Tim. Innovations in Banking (RLE: Banking & Finance): Business Strategies and

Employee Relations. Routledge, 2012.

OCBC bank annual reports (2018). Retrieved from

https://www.ocbc.com/group/investors/annual-reports.html

Petersen, Christian Vriborg, and Thomas Plenborg. Financial statement analysis: valuation,

credit analysis, and executive compensation. Pearson Longman, 2012.

Venardos, Angelo M. Islamic banking & finance in South-East Asia: Its development & future.

Vol. 6. World Scientific, 2012.

Bibliography

Auerbach, Alan J., ed. Corporate Takeovers: Causes and consequences. University of Chicago

Press, 2013.

Chatterjee, Sris, Kose John, and An Yan. "Takeovers and divergence of investor opinion." The

Review of Financial Studies 25, no. 1 (2012): 227-277.

Delen, Dursun, Cemil Kuzey, and Ali Uyar. "Measuring firm performance using financial ratios:

A decision tree approach." Expert Systems with Applications 40, no. 10 (2013): 3970-

3983.

DBS bank annual reports (2018). Retrieved from

https://www.dbs.com/investor/group-annual-reports.html

Edmans, Alex, Itay Goldstein, and Wei Jiang. "The real effects of financial markets: The impact

of prices on takeovers." The Journal of Finance 67, no. 3 (2012): 933-971.

Hensman, Ann, and Eugene Sadler-Smith. "Intuitive decision making in banking and

finance." European Management Journal 29, no. 1 (2011): 51-66.

Li, Xiaoyang. "Productivity, restructuring, and the gains from takeovers." Journal of Financial

Economics 109, no. 1 (2013): 250-271.

Lin, Fengyi, Deron Liang, and Enchia Chen. Financial ratio selection for business crisis

prediction. Expert Systems with Applications 38, no. 12 (2011): 15094-15102.

Morris, Tim. Innovations in Banking (RLE: Banking & Finance): Business Strategies and

Employee Relations. Routledge, 2012.

OCBC bank annual reports (2018). Retrieved from

https://www.ocbc.com/group/investors/annual-reports.html

Petersen, Christian Vriborg, and Thomas Plenborg. Financial statement analysis: valuation,

credit analysis, and executive compensation. Pearson Longman, 2012.

Venardos, Angelo M. Islamic banking & finance in South-East Asia: Its development & future.

Vol. 6. World Scientific, 2012.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.