Ogoya Limited: Financial Accounting Report on Debenture Options

VerifiedAdded on 2021/05/30

|13

|2141

|15

Report

AI Summary

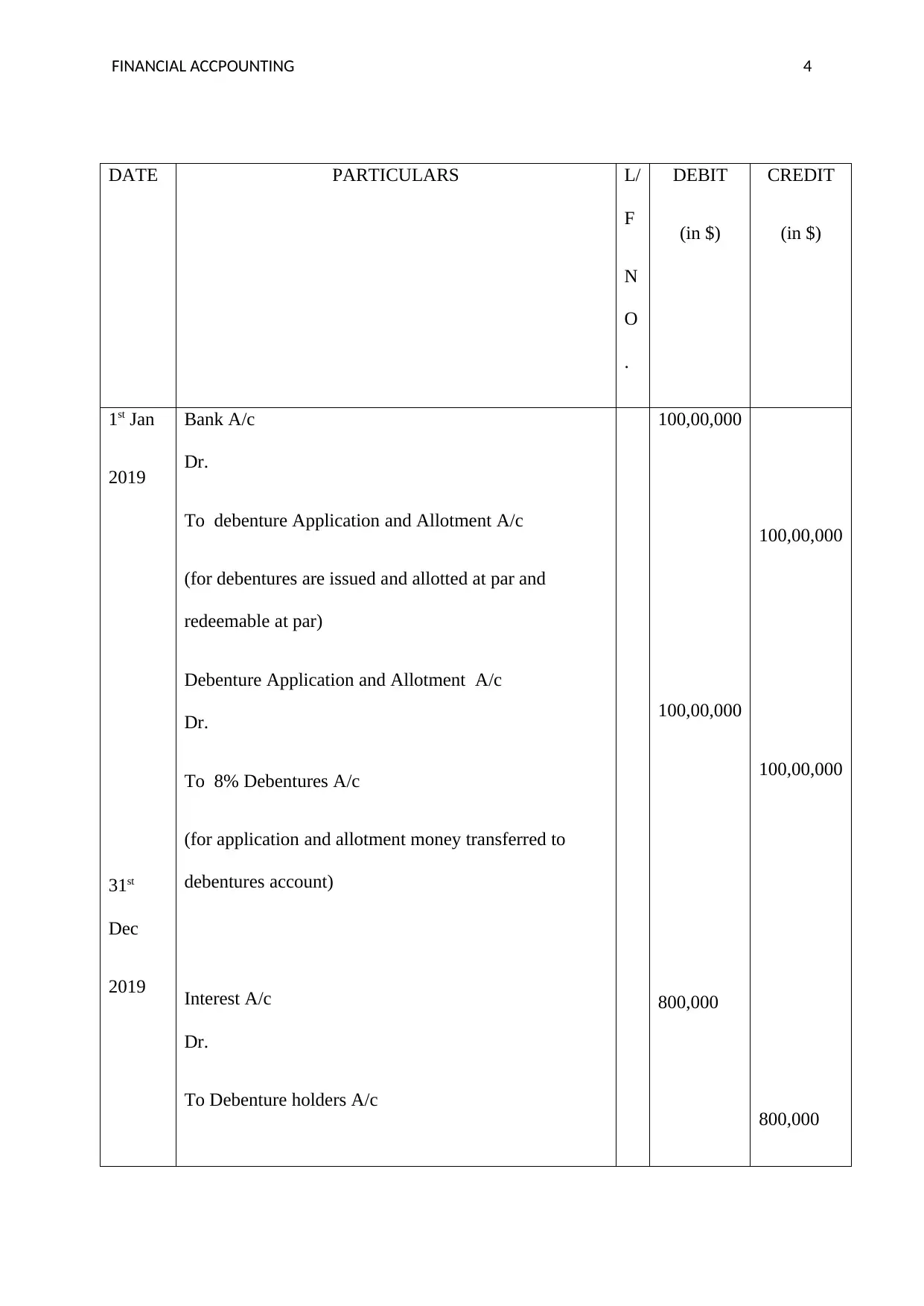

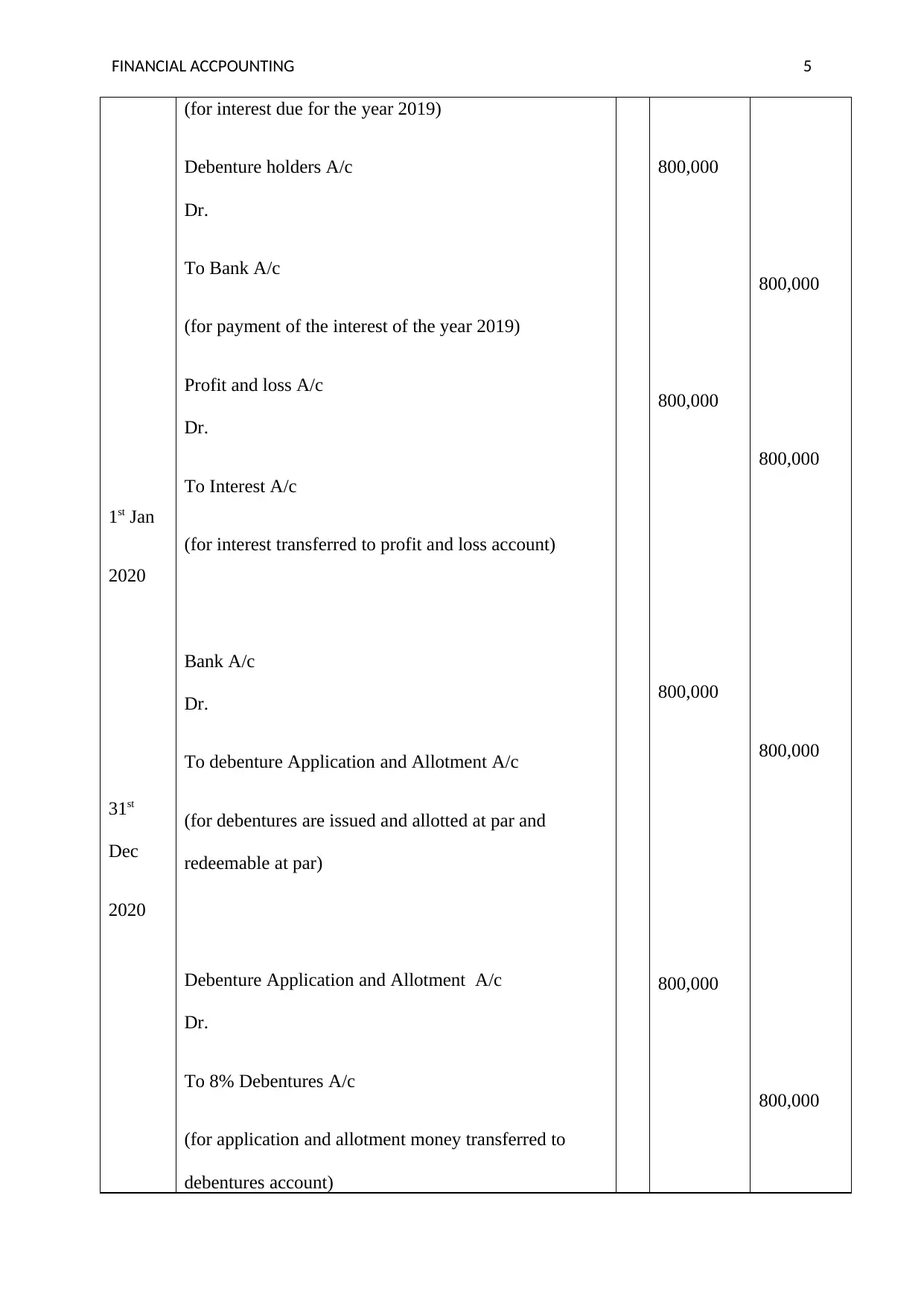

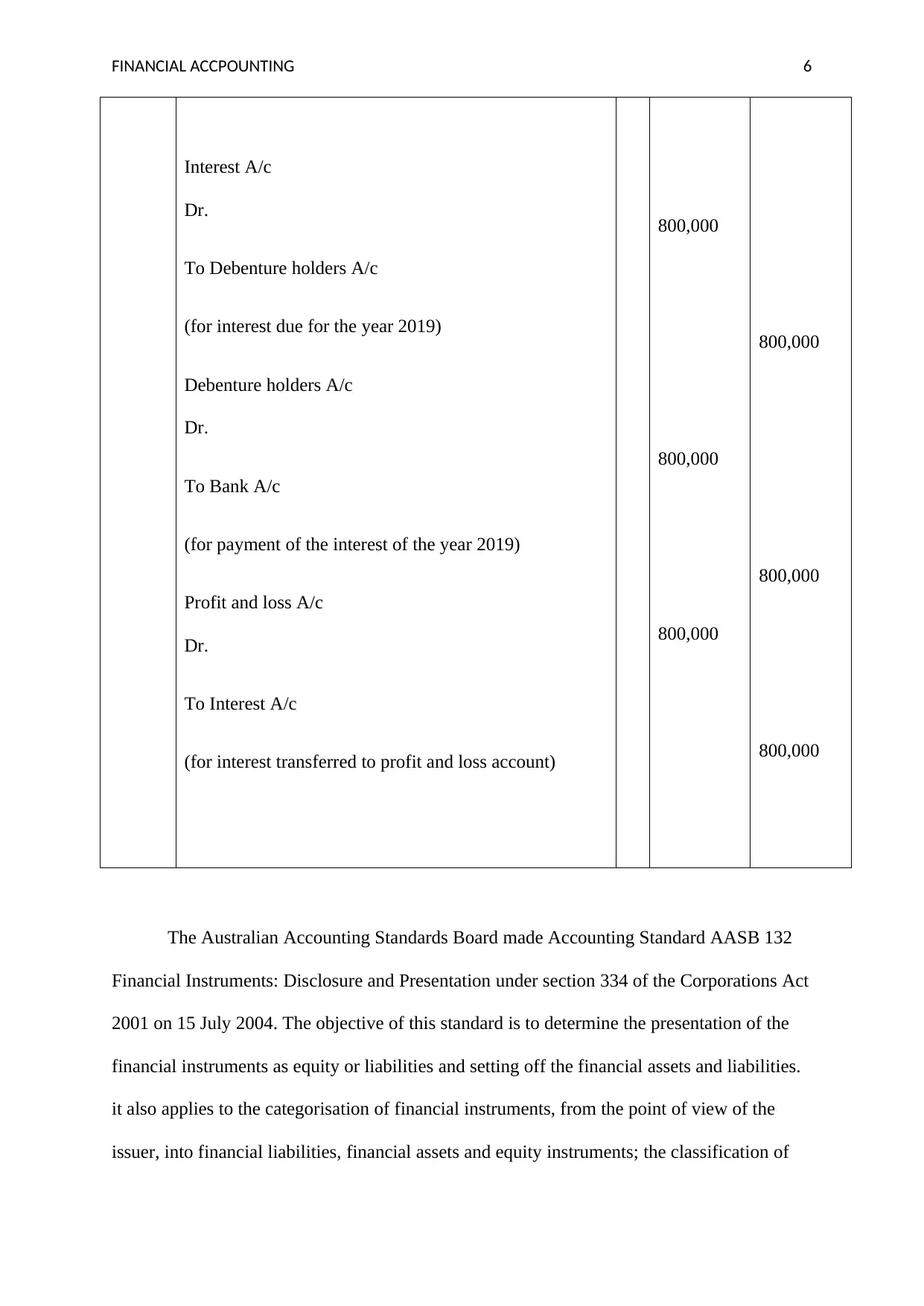

This report provides a financial analysis of debenture financing options for Ogoya Limited, a company seeking to expand its business. The report explores two primary financing methods: issuing debentures at par and issuing convertible debentures. It details the accounting entries for each option, referencing relevant accounting standards like AASB 132. The report evaluates the advantages and disadvantages of each approach, considering factors such as fixed costs, interest rates, investor appeal, and potential for equity conversion. The analysis includes journal entries for both options and discusses the implications for the company's financial statements. Ultimately, the report recommends the most suitable financing option for Ogoya Limited based on a comprehensive evaluation of the available alternatives, concluding that the convertible debenture option is more appropriate, particularly in line with Australian Accounting Standards, due to the potential benefits of protecting the investment and the flexibility of offering conversion into equity shares at a later date, thus reducing the interest liability.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.