Advanced Financial Accounting Report: Australis Oil & Gas and AASB 16

VerifiedAdded on 2022/11/01

|16

|3579

|64

Report

AI Summary

This report provides an in-depth analysis of the impact of the new lease standard, AASB 16, on the operations and financial performance of Australis Oil and Gas Limited. It begins with an executive summary and table of contents, followed by an introduction that outlines the paper's objectives. The report then describes the accounting concepts employed by Australis Oil and Gas, drawing information from the company's financial reports and highlighting significant accounting policies. It identifies the key changes introduced by the new lease standard, AASB 16, and contrasts them with the previous standard, AASB 117. A crucial section summarizes the company's disclosures regarding lease accounting, including transitional provisions and the effects of transitioning from AASB 117 to AASB 16. The analysis considers the company's leasing strategies, the impact of lease acquisitions and renewals, and the industry-specific implications of the new standard. The report concludes with a synthesis of the findings and a reference list. The report leverages the company's annual reports to provide a comprehensive overview of the accounting practices and the anticipated effects of the new lease standard. This analysis helps in understanding the changes and their effect on the company's financial statements.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced financial accounting

Name of the Student

Name of the University

Author Note

Advanced financial accounting

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED FINANCIAL ACCOUNTING

Executive summary:

The paper is developed to assess the impact of the new lease standard on the operation and

performance of the oil and gas limited company. The information and the changes that are

incorporated in the new standard of lease is also accounted by gaining an understating of the

changed lease standard. For this, a thorough analysis of the company named Australis Oil and

gas limited has been done by addressing different concepts of accounting used by the

company and how the adoption of the new standard would impact the process and the

operations. Such analysis has been done by summarizing the key disclosures made by the

company regarding the accounting treatment of leases.

Executive summary:

The paper is developed to assess the impact of the new lease standard on the operation and

performance of the oil and gas limited company. The information and the changes that are

incorporated in the new standard of lease is also accounted by gaining an understating of the

changed lease standard. For this, a thorough analysis of the company named Australis Oil and

gas limited has been done by addressing different concepts of accounting used by the

company and how the adoption of the new standard would impact the process and the

operations. Such analysis has been done by summarizing the key disclosures made by the

company regarding the accounting treatment of leases.

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................3

Description of the accounting concepts used by Australis Oil and Gas limited:.......................3

Identification of the changes incorporated in the new accounting standard for lease AASB 16:

....................................................................................................................................................5

Summarizing the key disclosure made by the company on its accounting for leases including

on the transitional provision and the effect of transition from AASB 117 to AASB 16:..........8

Conclusion:..............................................................................................................................10

Reference list:...........................................................................................................................12

Table of Contents

Introduction:...............................................................................................................................3

Description of the accounting concepts used by Australis Oil and Gas limited:.......................3

Identification of the changes incorporated in the new accounting standard for lease AASB 16:

....................................................................................................................................................5

Summarizing the key disclosure made by the company on its accounting for leases including

on the transitional provision and the effect of transition from AASB 117 to AASB 16:..........8

Conclusion:..............................................................................................................................10

Reference list:...........................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED FINANCIAL ACCOUNTING

Introduction:

In this paper, the accounting concepts used by the organization has been identified

and described. Explanation of the accounting concepts has been done in context of one of the

companies chosen from ASX (Australian stock exchange). With regard to this, the company

chosen is Australis Oil and Gas limited is an oil and gas company owning large gas and oil

licensed area onshore Portugal. Australis is the largest operator and owner of land and it is

also an oil shale basin onshore in United States that has emerged lastly. It has been formed by

the executives and founder of Aurora Oil and Gas limited. In addition to the explanation of

the accounting concepts, a detailed discussion has been made on the lease standard adopted

by the company and how the transition to the new lease standard is accounted. The key

disclosures made by the company in relation to the lease accounting standard and the impact

created by the introduction of the new lease standard on the accounting treatment of lease has

also been evaluated.

Description of the accounting concepts used by Australis Oil and Gas limited:

In this section, different concepts of accounting used by Australis Oil and Gas

Limited is demonstrated. This has been done by retrieving information from the financial

report of the company that highlights the significant accounting policies and the impact of

such policies in the performance of the organization. All the financial statements of the

company has been prepared by adhering to the accounting standards of Australia and all other

applicable standards issued by the International financial reporting standard. The accounting

policies adopted in year 2018 is consistent with what has been adopted in year 2017 and the

accounting policies adopted by the consolidated entity are consistent with the policies of

subsidiaries.

Introduction:

In this paper, the accounting concepts used by the organization has been identified

and described. Explanation of the accounting concepts has been done in context of one of the

companies chosen from ASX (Australian stock exchange). With regard to this, the company

chosen is Australis Oil and Gas limited is an oil and gas company owning large gas and oil

licensed area onshore Portugal. Australis is the largest operator and owner of land and it is

also an oil shale basin onshore in United States that has emerged lastly. It has been formed by

the executives and founder of Aurora Oil and Gas limited. In addition to the explanation of

the accounting concepts, a detailed discussion has been made on the lease standard adopted

by the company and how the transition to the new lease standard is accounted. The key

disclosures made by the company in relation to the lease accounting standard and the impact

created by the introduction of the new lease standard on the accounting treatment of lease has

also been evaluated.

Description of the accounting concepts used by Australis Oil and Gas limited:

In this section, different concepts of accounting used by Australis Oil and Gas

Limited is demonstrated. This has been done by retrieving information from the financial

report of the company that highlights the significant accounting policies and the impact of

such policies in the performance of the organization. All the financial statements of the

company has been prepared by adhering to the accounting standards of Australia and all other

applicable standards issued by the International financial reporting standard. The accounting

policies adopted in year 2018 is consistent with what has been adopted in year 2017 and the

accounting policies adopted by the consolidated entity are consistent with the policies of

subsidiaries.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED FINANCIAL ACCOUNTING

The presentational currency of Australis has been changed to US dollar from

Australian dollar and this has been effective from previous year that us 2017. This has been

done for providing shareholders with a more meaningful and consistent reflection of the

underlying performance of group. However, the change in current to US dollar was done as

the source currency trend concerning the majority of cost of subsidiary and parent companies

was not regarded as temporary. In addition to this, the hedge accounting of the group has

changed due to the adoption of AASB 9 in relation to performance of effectiveness testing of

measurement on the prospective basis. Application of this new accounting standard would be

done on retrospective basis and the policies relating to hedging and financial instruments is

aligned to new accounting standard AASB 9. In addition to this, the acquisition accounting

method is adopted for accounting all the business combination transaction irrespective of the

acquisition of other assets and equity instruments.

It is required by the organization to use certain critical accounting assumptions and

estimates when preparing the financial statements and the process of application of the

accounting policies requires exercising judgment by the management. This involves the

estimates and assumptions that are significant to the preparation of the financial statements

and involves higher degree of complexities or judgment. The costs related to dry hole,

geophysical and geological along with unproved leasehold cost are incurred according to the

successful method of efforts of accounting for evaluation and expenditure related to oil and

gas exploration. Furthermore, the accounting policies of the group has been used to compute

amount of profit and revenue contribution. Another accounting principle is that the report is

prepared assuming the going concern basis and accounting for same.

The presentational currency of Australis has been changed to US dollar from

Australian dollar and this has been effective from previous year that us 2017. This has been

done for providing shareholders with a more meaningful and consistent reflection of the

underlying performance of group. However, the change in current to US dollar was done as

the source currency trend concerning the majority of cost of subsidiary and parent companies

was not regarded as temporary. In addition to this, the hedge accounting of the group has

changed due to the adoption of AASB 9 in relation to performance of effectiveness testing of

measurement on the prospective basis. Application of this new accounting standard would be

done on retrospective basis and the policies relating to hedging and financial instruments is

aligned to new accounting standard AASB 9. In addition to this, the acquisition accounting

method is adopted for accounting all the business combination transaction irrespective of the

acquisition of other assets and equity instruments.

It is required by the organization to use certain critical accounting assumptions and

estimates when preparing the financial statements and the process of application of the

accounting policies requires exercising judgment by the management. This involves the

estimates and assumptions that are significant to the preparation of the financial statements

and involves higher degree of complexities or judgment. The costs related to dry hole,

geophysical and geological along with unproved leasehold cost are incurred according to the

successful method of efforts of accounting for evaluation and expenditure related to oil and

gas exploration. Furthermore, the accounting policies of the group has been used to compute

amount of profit and revenue contribution. Another accounting principle is that the report is

prepared assuming the going concern basis and accounting for same.

ADVANCED FINANCIAL ACCOUNTING

Identification of the changes incorporated in the new accounting standard for lease

AASB 16:

The objective of introducing new lese standard AASB 16 or IFRS 16 is to provide

relevant information to lessors and lessees so that the lease transactions are represented in a

faithful manner in the financial statements. Such information would assist the users in

assessing how the financial position, cash flow and the financial performance of the entity is

impacted by the leases. The new standard has introduced a single accounting model for lessee

and until the underlying assets value is low, it is required by the entity to recognize the

liabilities and assets for the leases with the lease term of more than twelve months (Dakis

2016).

The introduction of new lease standard AASB 16 by the accounting standard board

has replaced the existing or the previous lease standard AASB 117 and a comprehensive

model has been set out by this new standard that helps in identifying the lease arrangements

and the accounting treatment of both lessee and lessors in their financial statements. A

controlled model is applied by the new lease standard for identifying lease and creating a

distinction between service and leased contracts based on identifying the assets which the

customer controls. There is no difference between the classifications of the majority of

contracts under both the standards except for the emergence of divergence when the contract

pricing is considered significant under the previous standard (Aasb.gov.au 2019). The

accounting model of both lessee and lessor are asymmetrical and this is regarded as the most

notable aspect of the new lease standard. Under the AASB 16, the disclosure requirement of

lessor has been expanded and the introduction of additional requirements for the lease and

Identification of the changes incorporated in the new accounting standard for lease

AASB 16:

The objective of introducing new lese standard AASB 16 or IFRS 16 is to provide

relevant information to lessors and lessees so that the lease transactions are represented in a

faithful manner in the financial statements. Such information would assist the users in

assessing how the financial position, cash flow and the financial performance of the entity is

impacted by the leases. The new standard has introduced a single accounting model for lessee

and until the underlying assets value is low, it is required by the entity to recognize the

liabilities and assets for the leases with the lease term of more than twelve months (Dakis

2016).

The introduction of new lease standard AASB 16 by the accounting standard board

has replaced the existing or the previous lease standard AASB 117 and a comprehensive

model has been set out by this new standard that helps in identifying the lease arrangements

and the accounting treatment of both lessee and lessors in their financial statements. A

controlled model is applied by the new lease standard for identifying lease and creating a

distinction between service and leased contracts based on identifying the assets which the

customer controls. There is no difference between the classifications of the majority of

contracts under both the standards except for the emergence of divergence when the contract

pricing is considered significant under the previous standard (Aasb.gov.au 2019). The

accounting model of both lessee and lessor are asymmetrical and this is regarded as the most

notable aspect of the new lease standard. Under the AASB 16, the disclosure requirement of

lessor has been expanded and the introduction of additional requirements for the lease and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED FINANCIAL ACCOUNTING

sub-lease modifications. Apart from subleases, the changes that is introduced for lessor is not

significant.

The new lease standard is expected to create considerable impact on lessees as there

will be fundamental difference in the picture. In addition to this, except for the low value

assets and short term leases, the new standard does not make availability of the accounting

treatment for operating lease. Lessees are required to recognize the related lease liability and

right of use asset by bringing all the other leases on the balance sheet. In addition to this, the

mix of lease arrangements also forms the basis on which the financial statement of lessee

would be affected by the new lease requirements. In respect to the assessment of the lease

term and definition of lease, it is required by the organization to exercise judgment when

accounting some aspects of the application of the standard (Byers 2017).

The implementation of new lease standard AASB 16 requires the essentiality of the

good governance of the project and the scale of challenges faced in the implementation of the

new standard can be gauged by the readiness of the assessment of the standard. The

accounting principles under the new leas standard requires the recognition of leases by lessee

as a lease liability and right of use asset. Measurement of leases by lessee at the date of

commencement should be done at cost. Measurement of the initial value of les at the date of

commencement is done at the lease payment present value and the interest rate that is

implicitly used in leases are used for discounting the lease payments (Brumm and Liu 2019).

Furthermore, the right of use assets is measured subsequently by the application of cost

model and other applicable model of measurement.

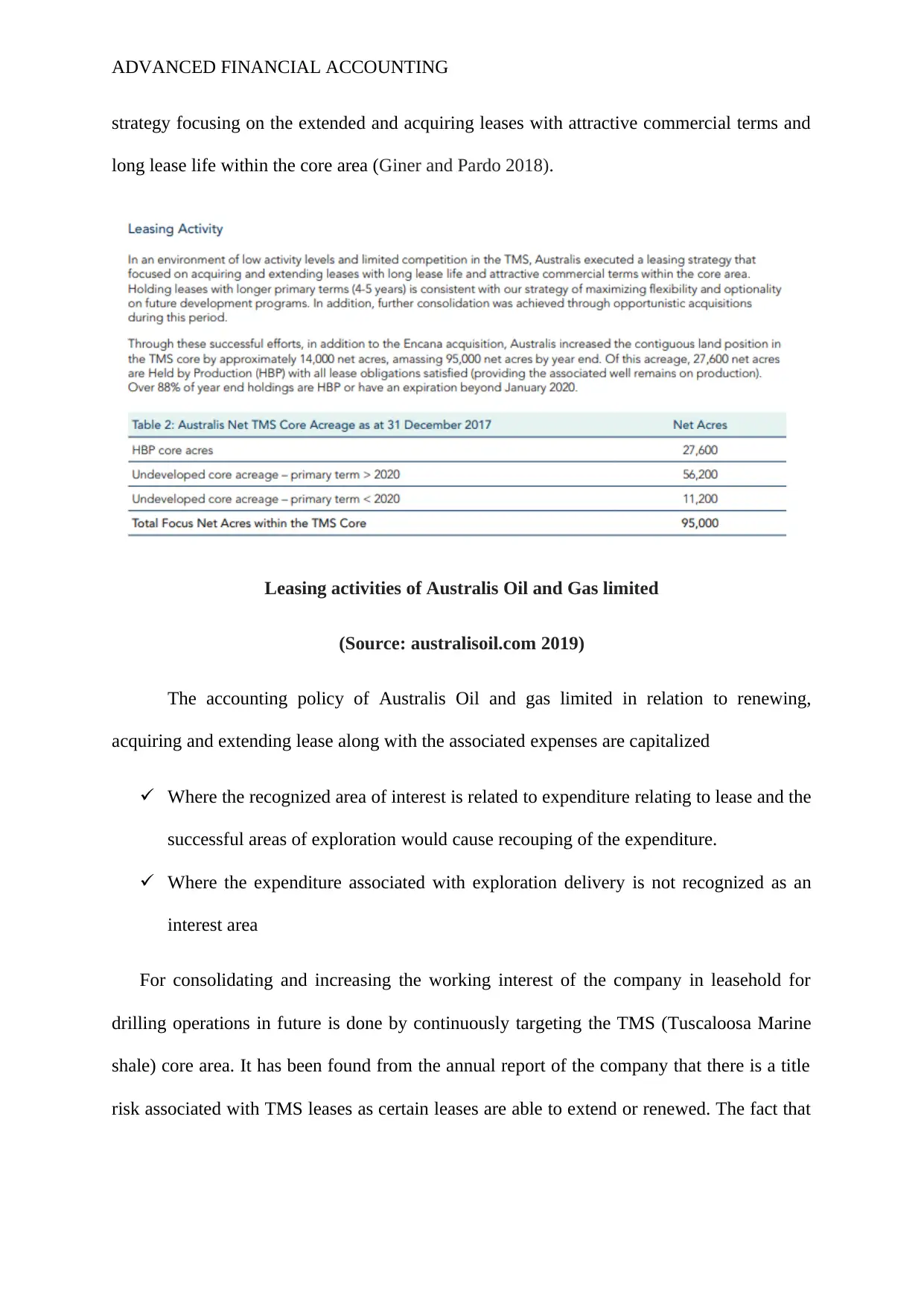

The primary strategy of Australis in year 2017 was to consolidate the vast position of

lease through the extension, renewal and acquisition of leases. The company is virtually

operating all of its assets and have long life time lease on majority of its acreage. A leasing

sub-lease modifications. Apart from subleases, the changes that is introduced for lessor is not

significant.

The new lease standard is expected to create considerable impact on lessees as there

will be fundamental difference in the picture. In addition to this, except for the low value

assets and short term leases, the new standard does not make availability of the accounting

treatment for operating lease. Lessees are required to recognize the related lease liability and

right of use asset by bringing all the other leases on the balance sheet. In addition to this, the

mix of lease arrangements also forms the basis on which the financial statement of lessee

would be affected by the new lease requirements. In respect to the assessment of the lease

term and definition of lease, it is required by the organization to exercise judgment when

accounting some aspects of the application of the standard (Byers 2017).

The implementation of new lease standard AASB 16 requires the essentiality of the

good governance of the project and the scale of challenges faced in the implementation of the

new standard can be gauged by the readiness of the assessment of the standard. The

accounting principles under the new leas standard requires the recognition of leases by lessee

as a lease liability and right of use asset. Measurement of leases by lessee at the date of

commencement should be done at cost. Measurement of the initial value of les at the date of

commencement is done at the lease payment present value and the interest rate that is

implicitly used in leases are used for discounting the lease payments (Brumm and Liu 2019).

Furthermore, the right of use assets is measured subsequently by the application of cost

model and other applicable model of measurement.

The primary strategy of Australis in year 2017 was to consolidate the vast position of

lease through the extension, renewal and acquisition of leases. The company is virtually

operating all of its assets and have long life time lease on majority of its acreage. A leasing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED FINANCIAL ACCOUNTING

strategy focusing on the extended and acquiring leases with attractive commercial terms and

long lease life within the core area (Giner and Pardo 2018).

Leasing activities of Australis Oil and Gas limited

(Source: australisoil.com 2019)

The accounting policy of Australis Oil and gas limited in relation to renewing,

acquiring and extending lease along with the associated expenses are capitalized

Where the recognized area of interest is related to expenditure relating to lease and the

successful areas of exploration would cause recouping of the expenditure.

Where the expenditure associated with exploration delivery is not recognized as an

interest area

For consolidating and increasing the working interest of the company in leasehold for

drilling operations in future is done by continuously targeting the TMS (Tuscaloosa Marine

shale) core area. It has been found from the annual report of the company that there is a title

risk associated with TMS leases as certain leases are able to extend or renewed. The fact that

strategy focusing on the extended and acquiring leases with attractive commercial terms and

long lease life within the core area (Giner and Pardo 2018).

Leasing activities of Australis Oil and Gas limited

(Source: australisoil.com 2019)

The accounting policy of Australis Oil and gas limited in relation to renewing,

acquiring and extending lease along with the associated expenses are capitalized

Where the recognized area of interest is related to expenditure relating to lease and the

successful areas of exploration would cause recouping of the expenditure.

Where the expenditure associated with exploration delivery is not recognized as an

interest area

For consolidating and increasing the working interest of the company in leasehold for

drilling operations in future is done by continuously targeting the TMS (Tuscaloosa Marine

shale) core area. It has been found from the annual report of the company that there is a title

risk associated with TMS leases as certain leases are able to extend or renewed. The fact that

ADVANCED FINANCIAL ACCOUNTING

the existing leases would be extended, renewed and reacquired before the new leases or

before the expiry does not come with guarantee (Ogilvy et al. 2018).

The impact that would be created by the implementation of the new lease standard on

the financial and overall performance of the organisation is being done by the company.

However, the amendment and interpretation of the new standard that is AASB 16 leases are

not yet effective as it is in the process of being assessed (Perera and Chand 2015).

In the current scenario, the cost associated with the new lease acquisition or the

extension or renewal of existing lease is represented by the other capital expenditure. The

budget of TMS is primarily for the extension and renewal of the existing lease and

acquisition of new lease (Ey.com 2019). Therefore, from the analysis of the information

retrieved from the financial report of Australis Oil and Gas limited, it has been ascertained

that the company is following the accounting treatment for lease in accordance with the old

lease standard that is AASB 117 as the assessment of the impact of new lease standard is still

in process.

Summarizing the key disclosure made by the company on its accounting for leases

including on the transitional provision and the effect of transition from AASB 117 to

AASB 16:

This section of report presents the key disclosure that the company has made on its

lease and how the adoption or the transition to new lease standard would impact the business

and its different metrics of measurements. For extending the life term of lease of TSM, a

lease program have been implemented and the optionality and greater flexibility to the future

development activity of the current lease is done by extending the primary term of leases and

focusing on to hold the leases by production. The acquisition cost of TMS including

extensions and leasing is done on the best independent estimate in relation to the net acreage

the existing leases would be extended, renewed and reacquired before the new leases or

before the expiry does not come with guarantee (Ogilvy et al. 2018).

The impact that would be created by the implementation of the new lease standard on

the financial and overall performance of the organisation is being done by the company.

However, the amendment and interpretation of the new standard that is AASB 16 leases are

not yet effective as it is in the process of being assessed (Perera and Chand 2015).

In the current scenario, the cost associated with the new lease acquisition or the

extension or renewal of existing lease is represented by the other capital expenditure. The

budget of TMS is primarily for the extension and renewal of the existing lease and

acquisition of new lease (Ey.com 2019). Therefore, from the analysis of the information

retrieved from the financial report of Australis Oil and Gas limited, it has been ascertained

that the company is following the accounting treatment for lease in accordance with the old

lease standard that is AASB 117 as the assessment of the impact of new lease standard is still

in process.

Summarizing the key disclosure made by the company on its accounting for leases

including on the transitional provision and the effect of transition from AASB 117 to

AASB 16:

This section of report presents the key disclosure that the company has made on its

lease and how the adoption or the transition to new lease standard would impact the business

and its different metrics of measurements. For extending the life term of lease of TSM, a

lease program have been implemented and the optionality and greater flexibility to the future

development activity of the current lease is done by extending the primary term of leases and

focusing on to hold the leases by production. The acquisition cost of TMS including

extensions and leasing is done on the best independent estimate in relation to the net acreage

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED FINANCIAL ACCOUNTING

position of the company. In addition to this, the classification of operating lease or the items

of the operating lease has been shown as they consist of rent that is payable within one year

and not more than five years (Wong and Joshi 2015).

Since Australis Oil and Gas Company limited operates in the Oil and Gas industry,

the assessment of the impact due to the implementation of new lease standard would be

confined to the industry and this helps in deducing the changes due to such standard. The

implementation of AASB 16 requires the company to change certain practice of lease

accounting as it would have far reaching implications on their operation and finance. The

lease accounting currently applied by the company depending upon the nature of assets and

terms of agreements in drilling rigs, transportation contract, equipment, tank and compressor,

office furniture and office space. The key financial metrics and the financial statements is

impacted by the new standard depending upon the importance of such arrangements to the

particular organization (Morales and Zamora 2018).

It would be required by lessee despite of making periodic payments on lease to

recognize a front loaded pattern of expense as the liability is measured using the effective

interest rate at the cost of amortization. The combination of depreciation expense under the

new standard due to recognition of interest expense and right of use assets for making lease

payment is replaced by the operating lease expenses. This has the implication that new

standard would cause EBITDA and operating netbacks to increase and would thereby knock

out the cash flow statement. There would be a reduced impact on cash flow from operating

activities and the principal payment on leases would be represented as a deduction from

financing and operating activities. This would create an impact on the computation of

leverage ratio for oil and gas companies. After the adoption of new standard, it is expected

that there would be an increase in debt equity ratio and an increase in the overall debts. A

position of the company. In addition to this, the classification of operating lease or the items

of the operating lease has been shown as they consist of rent that is payable within one year

and not more than five years (Wong and Joshi 2015).

Since Australis Oil and Gas Company limited operates in the Oil and Gas industry,

the assessment of the impact due to the implementation of new lease standard would be

confined to the industry and this helps in deducing the changes due to such standard. The

implementation of AASB 16 requires the company to change certain practice of lease

accounting as it would have far reaching implications on their operation and finance. The

lease accounting currently applied by the company depending upon the nature of assets and

terms of agreements in drilling rigs, transportation contract, equipment, tank and compressor,

office furniture and office space. The key financial metrics and the financial statements is

impacted by the new standard depending upon the importance of such arrangements to the

particular organization (Morales and Zamora 2018).

It would be required by lessee despite of making periodic payments on lease to

recognize a front loaded pattern of expense as the liability is measured using the effective

interest rate at the cost of amortization. The combination of depreciation expense under the

new standard due to recognition of interest expense and right of use assets for making lease

payment is replaced by the operating lease expenses. This has the implication that new

standard would cause EBITDA and operating netbacks to increase and would thereby knock

out the cash flow statement. There would be a reduced impact on cash flow from operating

activities and the principal payment on leases would be represented as a deduction from

financing and operating activities. This would create an impact on the computation of

leverage ratio for oil and gas companies. After the adoption of new standard, it is expected

that there would be an increase in debt equity ratio and an increase in the overall debts. A

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED FINANCIAL ACCOUNTING

mixed change will be observed in the figures of EBITDA after the implementation of AASB

16 (Ifrs.org 2019).

Some of the efforts that needs to be done by the oil and gas company when

implementing the new lease standard is that they would be required to establish a process for

assessing and identifying all the potential arrangements for lease including transportation and

contracts of drilling. In addition to this, company such as Australis Oil and gas limited would

face some challenges when interacting with the existing standard and separating the lease and

non-lease components. It would be important for the company to determine whether the

contract contains lease or a contract under the new standard as it calls for disclosing all the

leases on the balance sheet (Joubert et al. 2017).

Implementation of the new lease standard would impacts the financial metrics such as

leverage and gearing ratio and this would cause the loan covenants to get breached and such

loan covenants can also be triggered by an increase in the expenses on interest. Moreover, the

covenants based on the interest would also be impacted by an increase in the interest expense.

Accordingly, the credit rating of the company would also be impacted. It is also required by

the entity to evaluate the impact of such changes on staff bonuses and remuneration schemes

(Picker et al. 2019). Entity would also require to revise the arrangements proactively as the

financial ratio are redefined from assessing the arrangement in a timely manner. A substantial

effort would be required on part of the organization adopting the new standard for extracting

all the relevant data concerning lease and identification of lease agreements. In relation to

this, the compliance cost associated with the adoption of AASB 16 can be minimized by

considering the projects front end carefully (Hladika and Valenta 2018). In order to determine

whether certain lease arrangements are in the scope of new standard AASB 16, management

of the entity should apply more judgment as understanding the key financial metrics would be

of a major concern to the investors.

mixed change will be observed in the figures of EBITDA after the implementation of AASB

16 (Ifrs.org 2019).

Some of the efforts that needs to be done by the oil and gas company when

implementing the new lease standard is that they would be required to establish a process for

assessing and identifying all the potential arrangements for lease including transportation and

contracts of drilling. In addition to this, company such as Australis Oil and gas limited would

face some challenges when interacting with the existing standard and separating the lease and

non-lease components. It would be important for the company to determine whether the

contract contains lease or a contract under the new standard as it calls for disclosing all the

leases on the balance sheet (Joubert et al. 2017).

Implementation of the new lease standard would impacts the financial metrics such as

leverage and gearing ratio and this would cause the loan covenants to get breached and such

loan covenants can also be triggered by an increase in the expenses on interest. Moreover, the

covenants based on the interest would also be impacted by an increase in the interest expense.

Accordingly, the credit rating of the company would also be impacted. It is also required by

the entity to evaluate the impact of such changes on staff bonuses and remuneration schemes

(Picker et al. 2019). Entity would also require to revise the arrangements proactively as the

financial ratio are redefined from assessing the arrangement in a timely manner. A substantial

effort would be required on part of the organization adopting the new standard for extracting

all the relevant data concerning lease and identification of lease agreements. In relation to

this, the compliance cost associated with the adoption of AASB 16 can be minimized by

considering the projects front end carefully (Hladika and Valenta 2018). In order to determine

whether certain lease arrangements are in the scope of new standard AASB 16, management

of the entity should apply more judgment as understanding the key financial metrics would be

of a major concern to the investors.

ADVANCED FINANCIAL ACCOUNTING

Conclusion:

The paper discussing about the impact of changes in the accounting lease standard on

Australis Oil and Gas limited have ascertained that the new standard would create far

reaching effects on the operations and performance of the company. In the current scenario,

the accounting treatments for all the leases held by the organization is done in accordance

with the existing leased standard AASB 117 and a distinction is made between the leases. It

is found from the financial report that the company has operating lease that is separately

represented. All the accounting concepts relating to lease has been discussed and for the

implementation of new standard, it is essential for the entity to gain information by enhancing

the current internal control process and system of the organization. The future contracts

should be managed and evaluated by gaining an early understanding of the implications of

the new standard.

Conclusion:

The paper discussing about the impact of changes in the accounting lease standard on

Australis Oil and Gas limited have ascertained that the new standard would create far

reaching effects on the operations and performance of the company. In the current scenario,

the accounting treatments for all the leases held by the organization is done in accordance

with the existing leased standard AASB 117 and a distinction is made between the leases. It

is found from the financial report that the company has operating lease that is separately

represented. All the accounting concepts relating to lease has been discussed and for the

implementation of new standard, it is essential for the entity to gain information by enhancing

the current internal control process and system of the organization. The future contracts

should be managed and evaluated by gaining an early understanding of the implications of

the new standard.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.