Analysis of John Wood Group Plc: Oil and Gas Accounting Management

VerifiedAdded on 2023/06/15

|29

|6588

|348

Report

AI Summary

This report provides a comprehensive analysis of John Wood Group Plc, a multinational company in the energy services industry, focusing on its financial performance over the last five years. It examines the company's growth rate, asset turnover ratio, business and financial risks, and systematic risk, comparing it against competitors like Petrofac Ltd and Schlumberger Ltd. The report evaluates the company's capital structure, cost of capital using Weighted Average Cost of Capital (WACC), and employs various valuation models to assess its share price. Furthermore, it delves into the company's dividend policy, projects, and acquisitions, offering insights into its financial health and strategic decisions. Desklib offers access to similar solved assignments and past papers for students.

RUNNING HEAD: OIL AND GAS ACCOUNTING

John Wood Group Plc. management report

John Wood Group Plc. management report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Oil and gas accounting 1

Contents

Executive Summary...................................................................................................................3

Introduction................................................................................................................................4

Risk Profile.................................................................................................................................4

Growth Rate (Sales)...............................................................................................................4

Asset Turnover Ratio.............................................................................................................6

Business Risk.........................................................................................................................7

Financial Risk.........................................................................................................................8

Systematic Risk....................................................................................................................10

Factors affecting systematic risk..........................................................................................10

Return on Assets..................................................................................................................11

Return on Equity..................................................................................................................12

Actions taken by Management to Manage the Risk.............................................................13

Analysis of company’s value...................................................................................................14

Cost of capital......................................................................................................................14

Net Asset Value Approach...................................................................................................16

The Dividend Valuation Approach......................................................................................16

Price-Earnings Ratio Approach............................................................................................17

Rappaport’s Shareholder Value Model................................................................................17

Projects and acquisitions..........................................................................................................18

Analysis of Company’s Dividend Policy.................................................................................19

References................................................................................................................................21

Bibliography.............................................................................................................................23

Appendices...............................................................................................................................26

Appendix 1...........................................................................................................................26

Appendix 2...........................................................................................................................26

Contents

Executive Summary...................................................................................................................3

Introduction................................................................................................................................4

Risk Profile.................................................................................................................................4

Growth Rate (Sales)...............................................................................................................4

Asset Turnover Ratio.............................................................................................................6

Business Risk.........................................................................................................................7

Financial Risk.........................................................................................................................8

Systematic Risk....................................................................................................................10

Factors affecting systematic risk..........................................................................................10

Return on Assets..................................................................................................................11

Return on Equity..................................................................................................................12

Actions taken by Management to Manage the Risk.............................................................13

Analysis of company’s value...................................................................................................14

Cost of capital......................................................................................................................14

Net Asset Value Approach...................................................................................................16

The Dividend Valuation Approach......................................................................................16

Price-Earnings Ratio Approach............................................................................................17

Rappaport’s Shareholder Value Model................................................................................17

Projects and acquisitions..........................................................................................................18

Analysis of Company’s Dividend Policy.................................................................................19

References................................................................................................................................21

Bibliography.............................................................................................................................23

Appendices...............................................................................................................................26

Appendix 1...........................................................................................................................26

Appendix 2...........................................................................................................................26

Oil and gas accounting 2

Table of Figures

Figure 1: John Wood Revenues..............................................................................................4

Figure 2: John Wood growth rates.........................................................................................5

Figure 3: Asset Turnover.........................................................................................................5

Figure 4: Competitors' revenue..............................................................................................6

Figure 5: Operating Profit.......................................................................................................6

Figure 6: Net Profit..................................................................................................................7

Figure 7: Net Debt....................................................................................................................8

Figure 8: Rappaport Shareholder Value Model.................................................................14

Figure 9: Dividend Yield.......................................................................................................15

Table of Contents

Table 1: Sales by years.............................................................................................................5

Table 2: Financial Leverage....................................................................................................9

Table 3: Return on Assets......................................................................................................10

Table 4: Return on Equity.....................................................................................................10

Table 5: Cost of Equity..........................................................................................................12

Table 6: Cost of Debt.............................................................................................................12

Table 7: Weighted Average Cost of Capital........................................................................12

Table 8: Net Asset Value........................................................................................................13

Table 9: Dividends..................................................................................................................13

Table of Figures

Figure 1: John Wood Revenues..............................................................................................4

Figure 2: John Wood growth rates.........................................................................................5

Figure 3: Asset Turnover.........................................................................................................5

Figure 4: Competitors' revenue..............................................................................................6

Figure 5: Operating Profit.......................................................................................................6

Figure 6: Net Profit..................................................................................................................7

Figure 7: Net Debt....................................................................................................................8

Figure 8: Rappaport Shareholder Value Model.................................................................14

Figure 9: Dividend Yield.......................................................................................................15

Table of Contents

Table 1: Sales by years.............................................................................................................5

Table 2: Financial Leverage....................................................................................................9

Table 3: Return on Assets......................................................................................................10

Table 4: Return on Equity.....................................................................................................10

Table 5: Cost of Equity..........................................................................................................12

Table 6: Cost of Debt.............................................................................................................12

Table 7: Weighted Average Cost of Capital........................................................................12

Table 8: Net Asset Value........................................................................................................13

Table 9: Dividends..................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Oil and gas accounting 3

Executive Summary

John Wood Group Plc was established in the year 1961 (Yahoo Finance, 2016) and is

listed on FTSE 250 Index. This report examines the performance of the company over the last

five years to bring out with a conclusion after identifying and evaluating various risks against

its competitors. The various competitors compared in this report are (Energy Business

Review, 2018) are:

Petrofac Ltd.

Schlumberger Ltd.

National Oilwell Varco

Halliburton Co.

The growth rate and how sales have been affected by various factors of the company has

been analysed. In addition, the operating profit, degree of operating leverage (DOL) and

degree of financial leverage (DFL) are assessed to know the business and financial risk of the

company. Further, the report also emphasizes on the capital structure of John Wood Group

PLC and evaluates its cost of capital through Weighted Average Cost of Capital (WACC).

Moreover, the significant models of valuations are used to compute the company’s share

price in the market.

Executive Summary

John Wood Group Plc was established in the year 1961 (Yahoo Finance, 2016) and is

listed on FTSE 250 Index. This report examines the performance of the company over the last

five years to bring out with a conclusion after identifying and evaluating various risks against

its competitors. The various competitors compared in this report are (Energy Business

Review, 2018) are:

Petrofac Ltd.

Schlumberger Ltd.

National Oilwell Varco

Halliburton Co.

The growth rate and how sales have been affected by various factors of the company has

been analysed. In addition, the operating profit, degree of operating leverage (DOL) and

degree of financial leverage (DFL) are assessed to know the business and financial risk of the

company. Further, the report also emphasizes on the capital structure of John Wood Group

PLC and evaluates its cost of capital through Weighted Average Cost of Capital (WACC).

Moreover, the significant models of valuations are used to compute the company’s share

price in the market.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Oil and gas accounting 4

Introduction

John Wood Group is a multinational company and operates in the energy services

Industry. Primarily, the company is headquartered in the Aberdeen, United Kingdom, but the

operations are spread in various countries across the globe. The company make available a

range of activities to oil and gas and energy sectors worldwide like engineering, maintaining

management services, and supporting production. The company has grown year by year

significantly to function in more than 60 countries and employed more than 25000 employees

(John Wood Group PLC, 2018).

Risk Profile

Growth Rate (Sales)

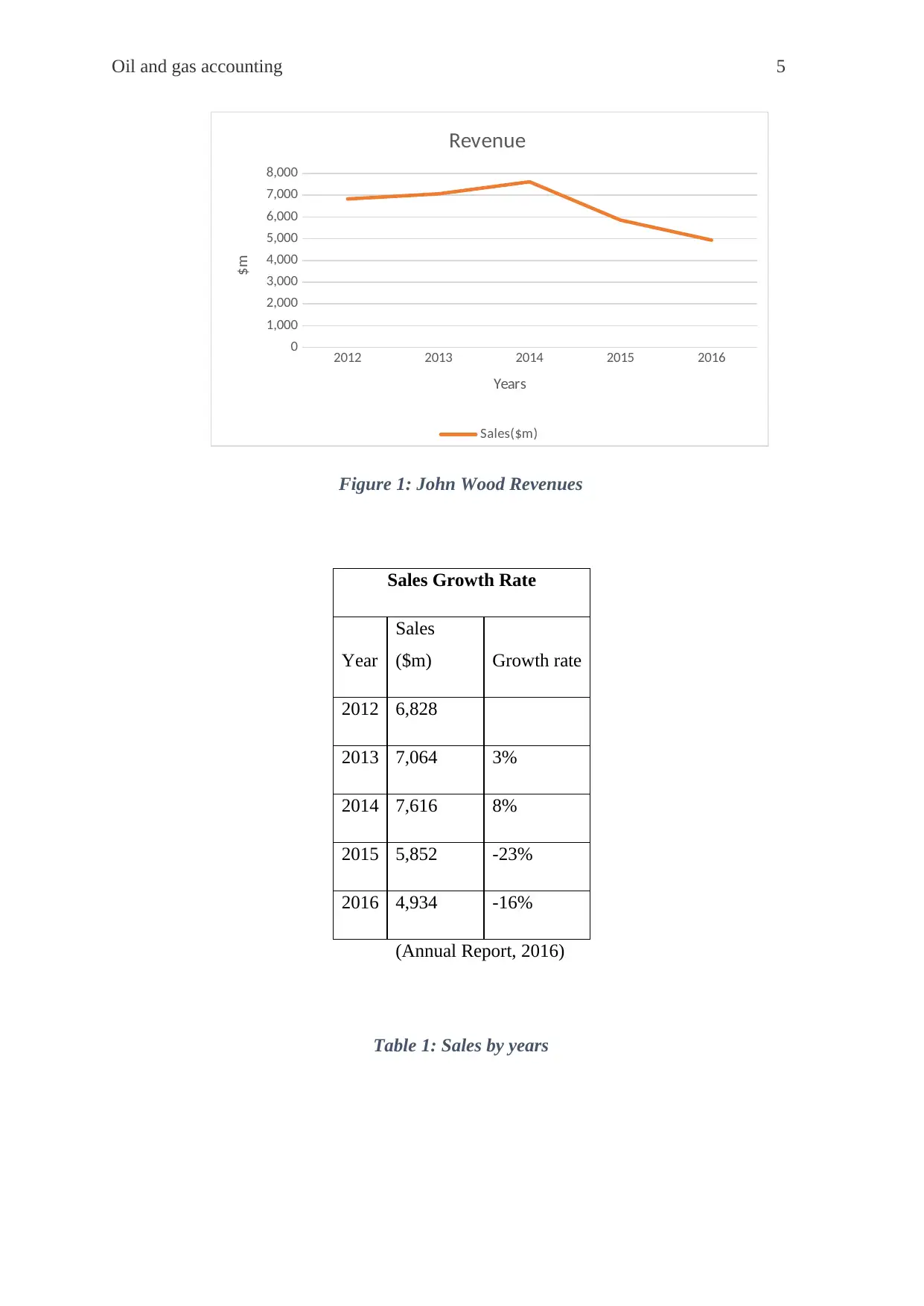

Sales growth rate analyses the volume of average sales grown from year to year

(Henriques and Sadorsky, 2011).The growth rate of John Wood Group PLC has shown a

significant fluctuation over the past years. The reasons for this fluctuation were related to the

fluctuation in the industry as well. From the above table of sales growth rate, it is seen that in

the year 2012, the revenue of the company was nearly USD 6,828 million. Than in 2014, the

growth rate increased because there was an economic growth in the oil industry and

unemployment was also decreased. (Pettinger, 2017). In the year 2015, the sales decreased

and there was substantial decline in the growth rate from 8% to -23%. It was seen that this

was due to the impact of the prices of oil dropped leading to decline of short term

investments in the oil industry.

Introduction

John Wood Group is a multinational company and operates in the energy services

Industry. Primarily, the company is headquartered in the Aberdeen, United Kingdom, but the

operations are spread in various countries across the globe. The company make available a

range of activities to oil and gas and energy sectors worldwide like engineering, maintaining

management services, and supporting production. The company has grown year by year

significantly to function in more than 60 countries and employed more than 25000 employees

(John Wood Group PLC, 2018).

Risk Profile

Growth Rate (Sales)

Sales growth rate analyses the volume of average sales grown from year to year

(Henriques and Sadorsky, 2011).The growth rate of John Wood Group PLC has shown a

significant fluctuation over the past years. The reasons for this fluctuation were related to the

fluctuation in the industry as well. From the above table of sales growth rate, it is seen that in

the year 2012, the revenue of the company was nearly USD 6,828 million. Than in 2014, the

growth rate increased because there was an economic growth in the oil industry and

unemployment was also decreased. (Pettinger, 2017). In the year 2015, the sales decreased

and there was substantial decline in the growth rate from 8% to -23%. It was seen that this

was due to the impact of the prices of oil dropped leading to decline of short term

investments in the oil industry.

Oil and gas accounting 5

2012 2013 2014 2015 2016

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Revenue

Sales($m)

Years

$m

Figure 1: John Wood Revenues

Sales Growth Rate

Year

Sales

($m) Growth rate

2012 6,828

2013 7,064 3%

2014 7,616 8%

2015 5,852 -23%

2016 4,934 -16%

(Annual Report, 2016)

Table 1: Sales by years

2012 2013 2014 2015 2016

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Revenue

Sales($m)

Years

$m

Figure 1: John Wood Revenues

Sales Growth Rate

Year

Sales

($m) Growth rate

2012 6,828

2013 7,064 3%

2014 7,616 8%

2015 5,852 -23%

2016 4,934 -16%

(Annual Report, 2016)

Table 1: Sales by years

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Oil and gas accounting 6

2012 2013 2014 2015 2016

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

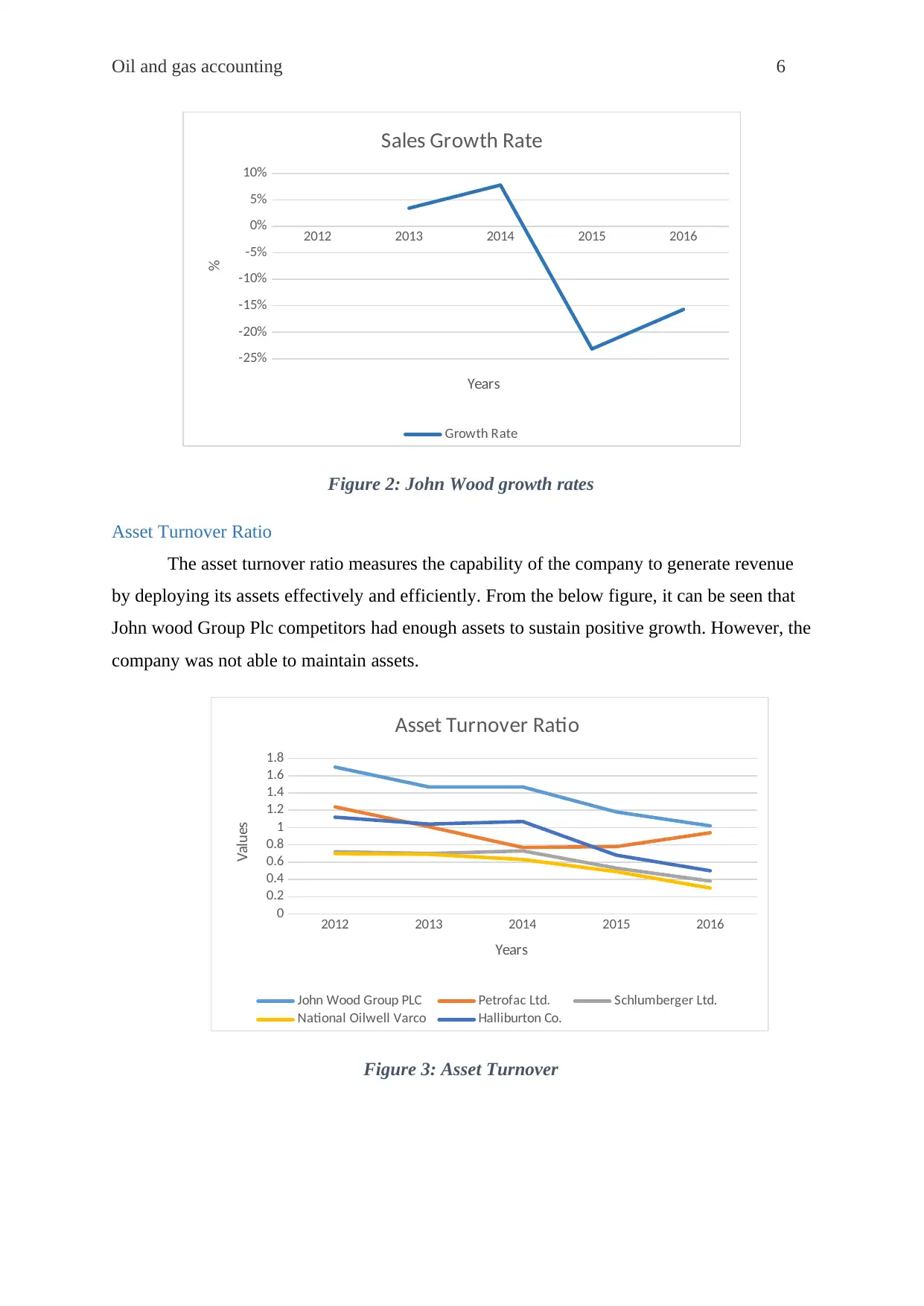

Sales Growth Rate

Growth Rate

Years

%

Figure 2: John Wood growth rates

Asset Turnover Ratio

The asset turnover ratio measures the capability of the company to generate revenue

by deploying its assets effectively and efficiently. From the below figure, it can be seen that

John wood Group Plc competitors had enough assets to sustain positive growth. However, the

company was not able to maintain assets.

2012 2013 2014 2015 2016

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

Asset Turnover Ratio

John Wood Group PLC Petrofac Ltd. Schlumberger Ltd.

National Oilwell Varco Halliburton Co.

Years

Values

Figure 3: Asset Turnover

2012 2013 2014 2015 2016

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

Sales Growth Rate

Growth Rate

Years

%

Figure 2: John Wood growth rates

Asset Turnover Ratio

The asset turnover ratio measures the capability of the company to generate revenue

by deploying its assets effectively and efficiently. From the below figure, it can be seen that

John wood Group Plc competitors had enough assets to sustain positive growth. However, the

company was not able to maintain assets.

2012 2013 2014 2015 2016

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

Asset Turnover Ratio

John Wood Group PLC Petrofac Ltd. Schlumberger Ltd.

National Oilwell Varco Halliburton Co.

Years

Values

Figure 3: Asset Turnover

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Oil and gas accounting 7

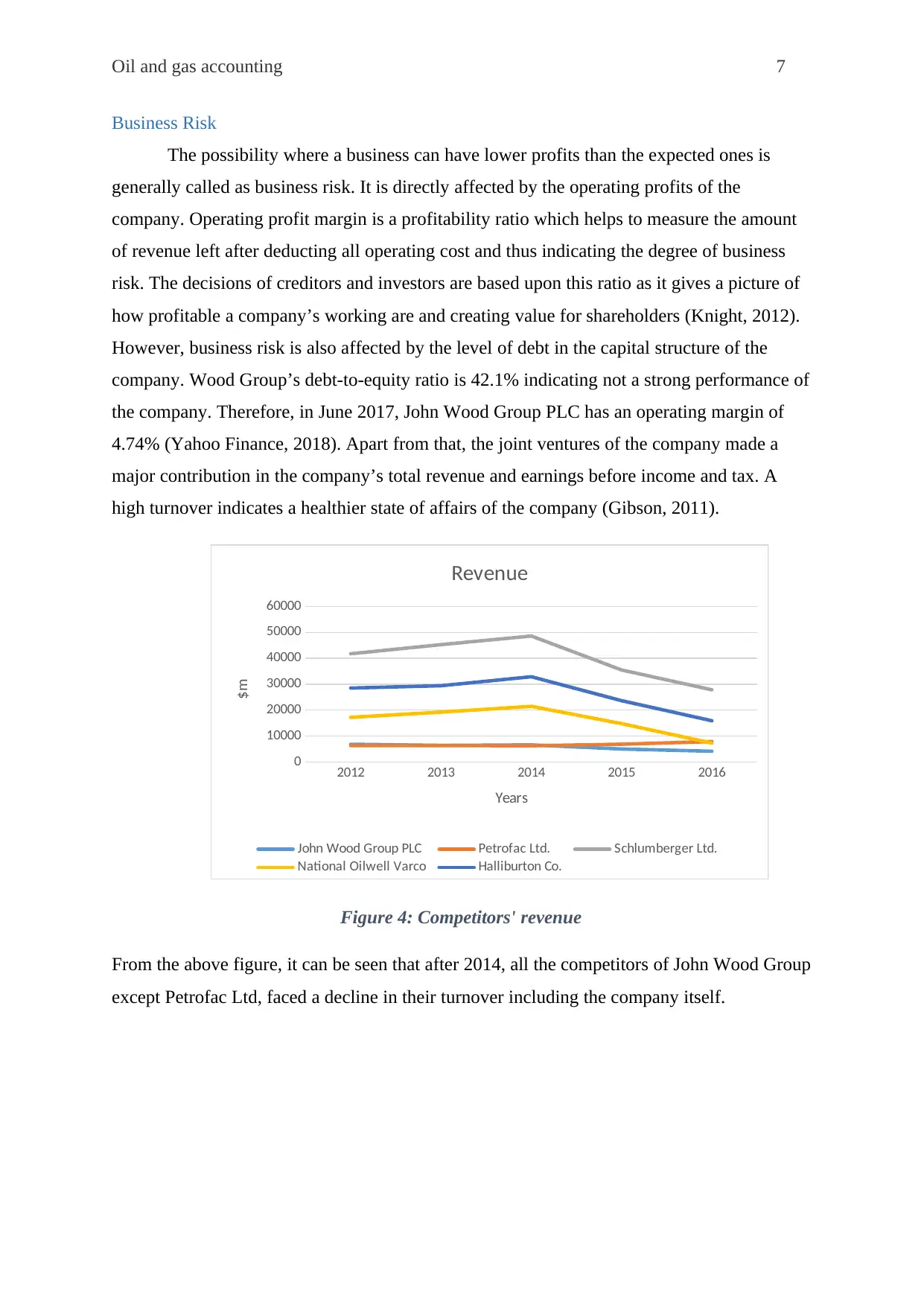

Business Risk

The possibility where a business can have lower profits than the expected ones is

generally called as business risk. It is directly affected by the operating profits of the

company. Operating profit margin is a profitability ratio which helps to measure the amount

of revenue left after deducting all operating cost and thus indicating the degree of business

risk. The decisions of creditors and investors are based upon this ratio as it gives a picture of

how profitable a company’s working are and creating value for shareholders (Knight, 2012).

However, business risk is also affected by the level of debt in the capital structure of the

company. Wood Group’s debt-to-equity ratio is 42.1% indicating not a strong performance of

the company. Therefore, in June 2017, John Wood Group PLC has an operating margin of

4.74% (Yahoo Finance, 2018). Apart from that, the joint ventures of the company made a

major contribution in the company’s total revenue and earnings before income and tax. A

high turnover indicates a healthier state of affairs of the company (Gibson, 2011).

2012 2013 2014 2015 2016

0

10000

20000

30000

40000

50000

60000

Revenue

John Wood Group PLC Petrofac Ltd. Schlumberger Ltd.

National Oilwell Varco Halliburton Co.

Years

$m

Figure 4: Competitors' revenue

From the above figure, it can be seen that after 2014, all the competitors of John Wood Group

except Petrofac Ltd, faced a decline in their turnover including the company itself.

Business Risk

The possibility where a business can have lower profits than the expected ones is

generally called as business risk. It is directly affected by the operating profits of the

company. Operating profit margin is a profitability ratio which helps to measure the amount

of revenue left after deducting all operating cost and thus indicating the degree of business

risk. The decisions of creditors and investors are based upon this ratio as it gives a picture of

how profitable a company’s working are and creating value for shareholders (Knight, 2012).

However, business risk is also affected by the level of debt in the capital structure of the

company. Wood Group’s debt-to-equity ratio is 42.1% indicating not a strong performance of

the company. Therefore, in June 2017, John Wood Group PLC has an operating margin of

4.74% (Yahoo Finance, 2018). Apart from that, the joint ventures of the company made a

major contribution in the company’s total revenue and earnings before income and tax. A

high turnover indicates a healthier state of affairs of the company (Gibson, 2011).

2012 2013 2014 2015 2016

0

10000

20000

30000

40000

50000

60000

Revenue

John Wood Group PLC Petrofac Ltd. Schlumberger Ltd.

National Oilwell Varco Halliburton Co.

Years

$m

Figure 4: Competitors' revenue

From the above figure, it can be seen that after 2014, all the competitors of John Wood Group

except Petrofac Ltd, faced a decline in their turnover including the company itself.

Oil and gas accounting 8

2012 2013 2014 2015 2016

-8000

-6000

-4000

-2000

0

2000

4000

6000

8000

10000

12000

Operating Profit

John Wood Group PLC Petrofac Ltd. Schlumberger Ltd.

National Oilwell Varco Halliburton Co.

Years

$m

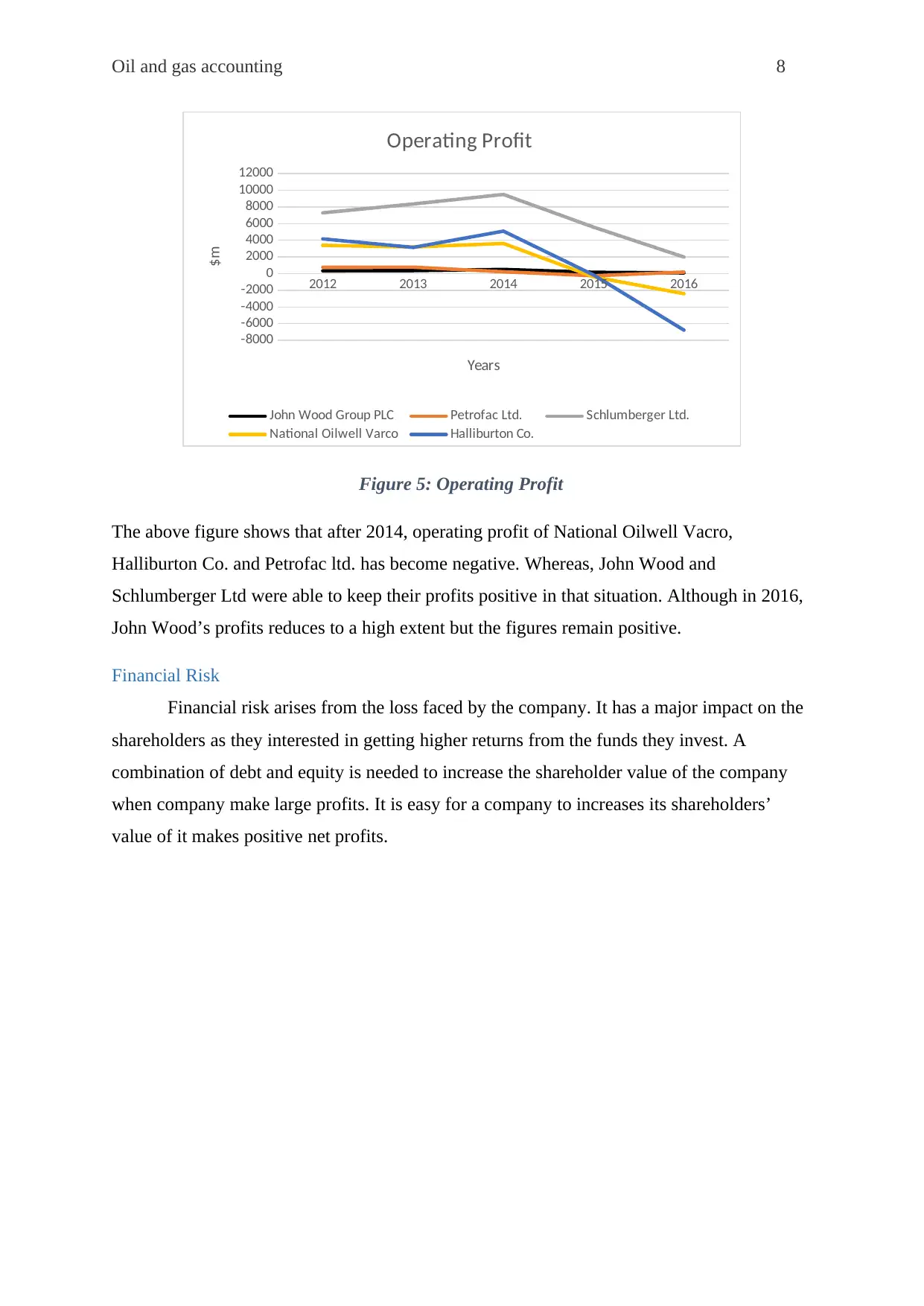

Figure 5: Operating Profit

The above figure shows that after 2014, operating profit of National Oilwell Vacro,

Halliburton Co. and Petrofac ltd. has become negative. Whereas, John Wood and

Schlumberger Ltd were able to keep their profits positive in that situation. Although in 2016,

John Wood’s profits reduces to a high extent but the figures remain positive.

Financial Risk

Financial risk arises from the loss faced by the company. It has a major impact on the

shareholders as they interested in getting higher returns from the funds they invest. A

combination of debt and equity is needed to increase the shareholder value of the company

when company make large profits. It is easy for a company to increases its shareholders’

value of it makes positive net profits.

2012 2013 2014 2015 2016

-8000

-6000

-4000

-2000

0

2000

4000

6000

8000

10000

12000

Operating Profit

John Wood Group PLC Petrofac Ltd. Schlumberger Ltd.

National Oilwell Varco Halliburton Co.

Years

$m

Figure 5: Operating Profit

The above figure shows that after 2014, operating profit of National Oilwell Vacro,

Halliburton Co. and Petrofac ltd. has become negative. Whereas, John Wood and

Schlumberger Ltd were able to keep their profits positive in that situation. Although in 2016,

John Wood’s profits reduces to a high extent but the figures remain positive.

Financial Risk

Financial risk arises from the loss faced by the company. It has a major impact on the

shareholders as they interested in getting higher returns from the funds they invest. A

combination of debt and equity is needed to increase the shareholder value of the company

when company make large profits. It is easy for a company to increases its shareholders’

value of it makes positive net profits.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Oil and gas accounting 9

2012 2013 2014 2015 2016

-8000

-6000

-4000

-2000

0

2000

4000

6000

8000

Net Profit

John Wood Group PLC Petrofac Ltd. Schlumberger Ltd.

National Oilwell Varco Halliburton Co.

Years

$m

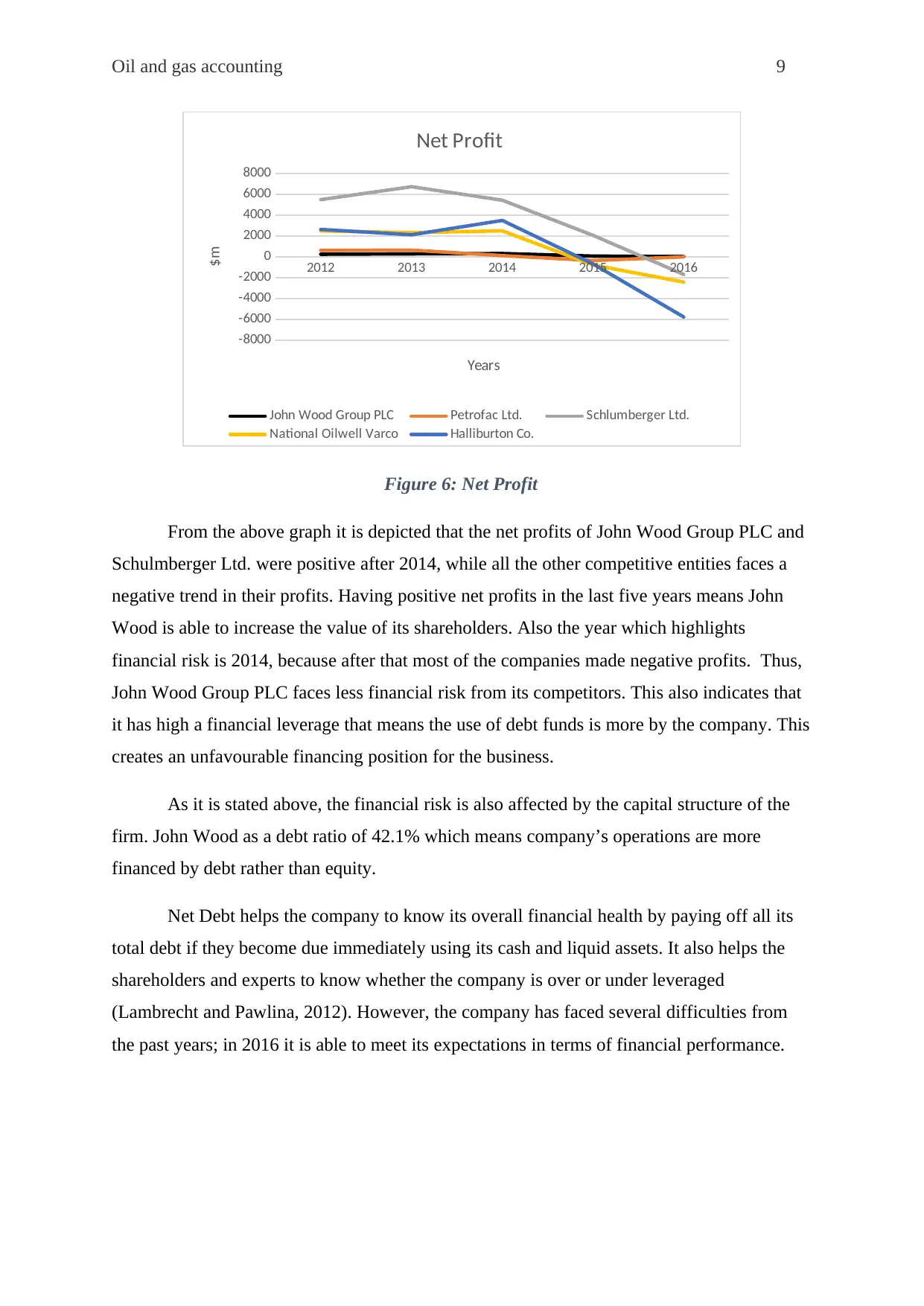

Figure 6: Net Profit

From the above graph it is depicted that the net profits of John Wood Group PLC and

Schulmberger Ltd. were positive after 2014, while all the other competitive entities faces a

negative trend in their profits. Having positive net profits in the last five years means John

Wood is able to increase the value of its shareholders. Also the year which highlights

financial risk is 2014, because after that most of the companies made negative profits. Thus,

John Wood Group PLC faces less financial risk from its competitors. This also indicates that

it has high a financial leverage that means the use of debt funds is more by the company. This

creates an unfavourable financing position for the business.

As it is stated above, the financial risk is also affected by the capital structure of the

firm. John Wood as a debt ratio of 42.1% which means company’s operations are more

financed by debt rather than equity.

Net Debt helps the company to know its overall financial health by paying off all its

total debt if they become due immediately using its cash and liquid assets. It also helps the

shareholders and experts to know whether the company is over or under leveraged

(Lambrecht and Pawlina, 2012). However, the company has faced several difficulties from

the past years; in 2016 it is able to meet its expectations in terms of financial performance.

2012 2013 2014 2015 2016

-8000

-6000

-4000

-2000

0

2000

4000

6000

8000

Net Profit

John Wood Group PLC Petrofac Ltd. Schlumberger Ltd.

National Oilwell Varco Halliburton Co.

Years

$m

Figure 6: Net Profit

From the above graph it is depicted that the net profits of John Wood Group PLC and

Schulmberger Ltd. were positive after 2014, while all the other competitive entities faces a

negative trend in their profits. Having positive net profits in the last five years means John

Wood is able to increase the value of its shareholders. Also the year which highlights

financial risk is 2014, because after that most of the companies made negative profits. Thus,

John Wood Group PLC faces less financial risk from its competitors. This also indicates that

it has high a financial leverage that means the use of debt funds is more by the company. This

creates an unfavourable financing position for the business.

As it is stated above, the financial risk is also affected by the capital structure of the

firm. John Wood as a debt ratio of 42.1% which means company’s operations are more

financed by debt rather than equity.

Net Debt helps the company to know its overall financial health by paying off all its

total debt if they become due immediately using its cash and liquid assets. It also helps the

shareholders and experts to know whether the company is over or under leveraged

(Lambrecht and Pawlina, 2012). However, the company has faced several difficulties from

the past years; in 2016 it is able to meet its expectations in terms of financial performance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Oil and gas accounting 10

2012 2013 2014 2015 2016

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

Net Debt

John Wood Group PLC

Petrofac Ltd

Schlumberger Ltd.

National Oilwell Varco

Halliburton Co.

Years

$m

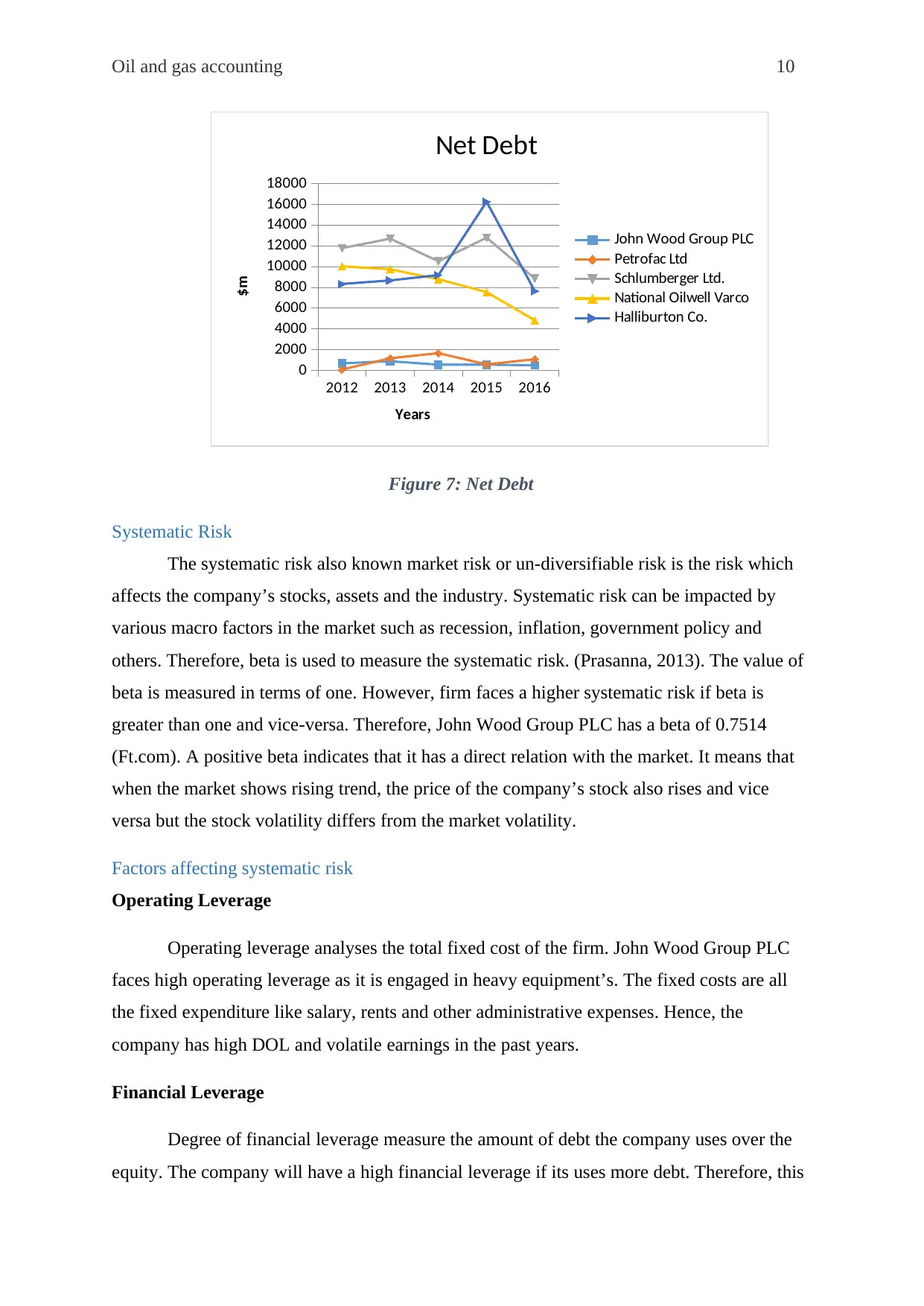

Figure 7: Net Debt

Systematic Risk

The systematic risk also known market risk or un-diversifiable risk is the risk which

affects the company’s stocks, assets and the industry. Systematic risk can be impacted by

various macro factors in the market such as recession, inflation, government policy and

others. Therefore, beta is used to measure the systematic risk. (Prasanna, 2013). The value of

beta is measured in terms of one. However, firm faces a higher systematic risk if beta is

greater than one and vice-versa. Therefore, John Wood Group PLC has a beta of 0.7514

(Ft.com). A positive beta indicates that it has a direct relation with the market. It means that

when the market shows rising trend, the price of the company’s stock also rises and vice

versa but the stock volatility differs from the market volatility.

Factors affecting systematic risk

Operating Leverage

Operating leverage analyses the total fixed cost of the firm. John Wood Group PLC

faces high operating leverage as it is engaged in heavy equipment’s. The fixed costs are all

the fixed expenditure like salary, rents and other administrative expenses. Hence, the

company has high DOL and volatile earnings in the past years.

Financial Leverage

Degree of financial leverage measure the amount of debt the company uses over the

equity. The company will have a high financial leverage if its uses more debt. Therefore, this

2012 2013 2014 2015 2016

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

Net Debt

John Wood Group PLC

Petrofac Ltd

Schlumberger Ltd.

National Oilwell Varco

Halliburton Co.

Years

$m

Figure 7: Net Debt

Systematic Risk

The systematic risk also known market risk or un-diversifiable risk is the risk which

affects the company’s stocks, assets and the industry. Systematic risk can be impacted by

various macro factors in the market such as recession, inflation, government policy and

others. Therefore, beta is used to measure the systematic risk. (Prasanna, 2013). The value of

beta is measured in terms of one. However, firm faces a higher systematic risk if beta is

greater than one and vice-versa. Therefore, John Wood Group PLC has a beta of 0.7514

(Ft.com). A positive beta indicates that it has a direct relation with the market. It means that

when the market shows rising trend, the price of the company’s stock also rises and vice

versa but the stock volatility differs from the market volatility.

Factors affecting systematic risk

Operating Leverage

Operating leverage analyses the total fixed cost of the firm. John Wood Group PLC

faces high operating leverage as it is engaged in heavy equipment’s. The fixed costs are all

the fixed expenditure like salary, rents and other administrative expenses. Hence, the

company has high DOL and volatile earnings in the past years.

Financial Leverage

Degree of financial leverage measure the amount of debt the company uses over the

equity. The company will have a high financial leverage if its uses more debt. Therefore, this

Oil and gas accounting 11

also increases the burden of repayment of debts along with their interest on the maturity date

affecting the company’s EPS.

Financial Leverage (%)

Year Financial Leverage

201

2 1.87

201

3 1.89

201

4 1.72

201

5 1.7

201

6 1.84

(Morningstar, 2018)

Table 2: Financial Leverage

The above table shows the financial leverage of John Wood Group PLC over the last

five years. In the year 2012, the company had a leverage of 1.87. In the year 2016, it

decreased to 1.84 thus, reducing the financial risk of the company.

Performance Visibility

Visibility of company’s performance is another factor that indicates its systematic risk. The

beta of the company is directly influenced by the level of transparency kept by the firm in its

financial reports, management process and performance. John Wood Group has make its

shareholders aware about its strategies and performance in the last five years. This increases

the reliability as well as kept the beta of the company lower than its competitors.

also increases the burden of repayment of debts along with their interest on the maturity date

affecting the company’s EPS.

Financial Leverage (%)

Year Financial Leverage

201

2 1.87

201

3 1.89

201

4 1.72

201

5 1.7

201

6 1.84

(Morningstar, 2018)

Table 2: Financial Leverage

The above table shows the financial leverage of John Wood Group PLC over the last

five years. In the year 2012, the company had a leverage of 1.87. In the year 2016, it

decreased to 1.84 thus, reducing the financial risk of the company.

Performance Visibility

Visibility of company’s performance is another factor that indicates its systematic risk. The

beta of the company is directly influenced by the level of transparency kept by the firm in its

financial reports, management process and performance. John Wood Group has make its

shareholders aware about its strategies and performance in the last five years. This increases

the reliability as well as kept the beta of the company lower than its competitors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.