Detailed Management Accounting Report: O'Keefe Construction Analysis

VerifiedAdded on 2023/01/20

|21

|4736

|79

Report

AI Summary

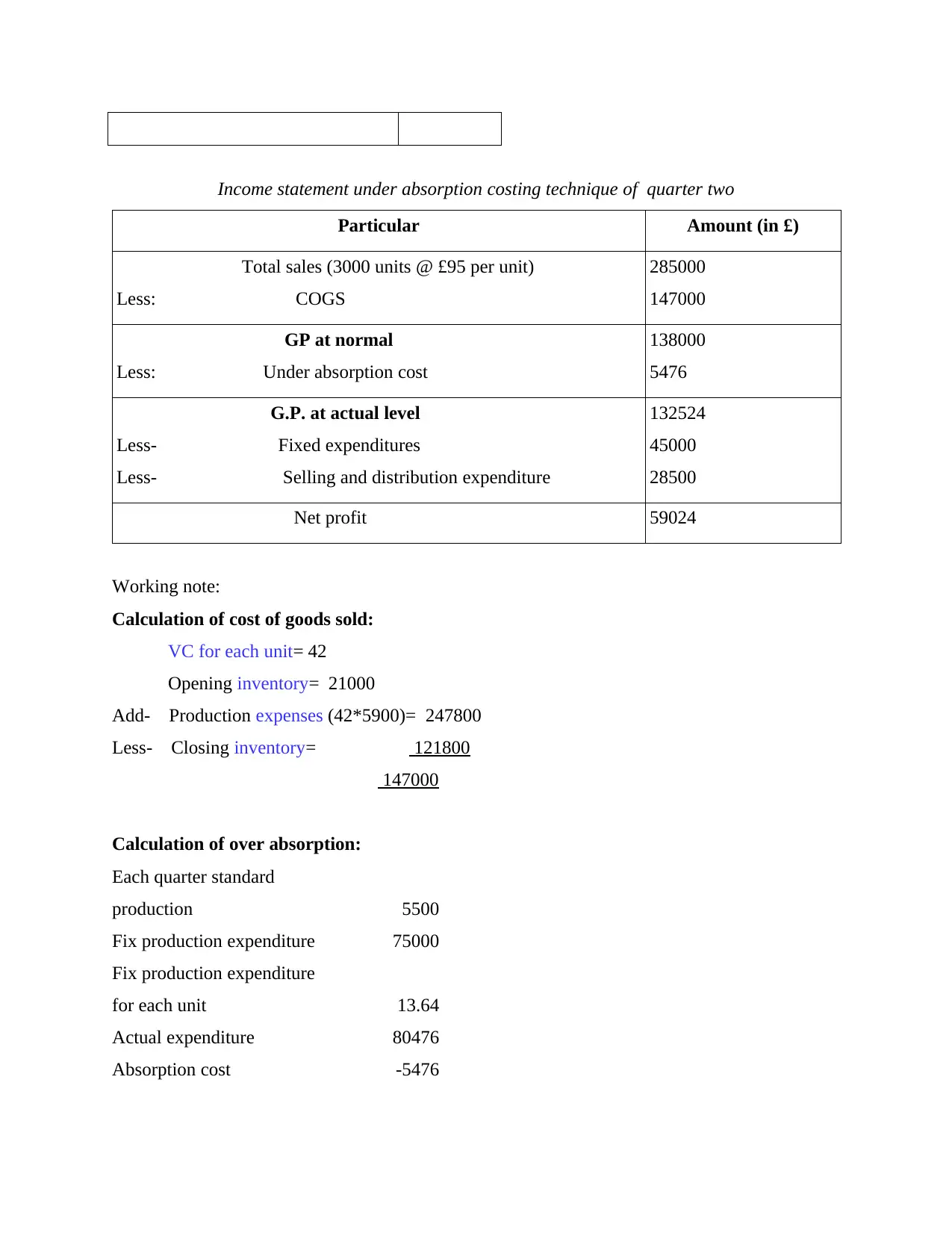

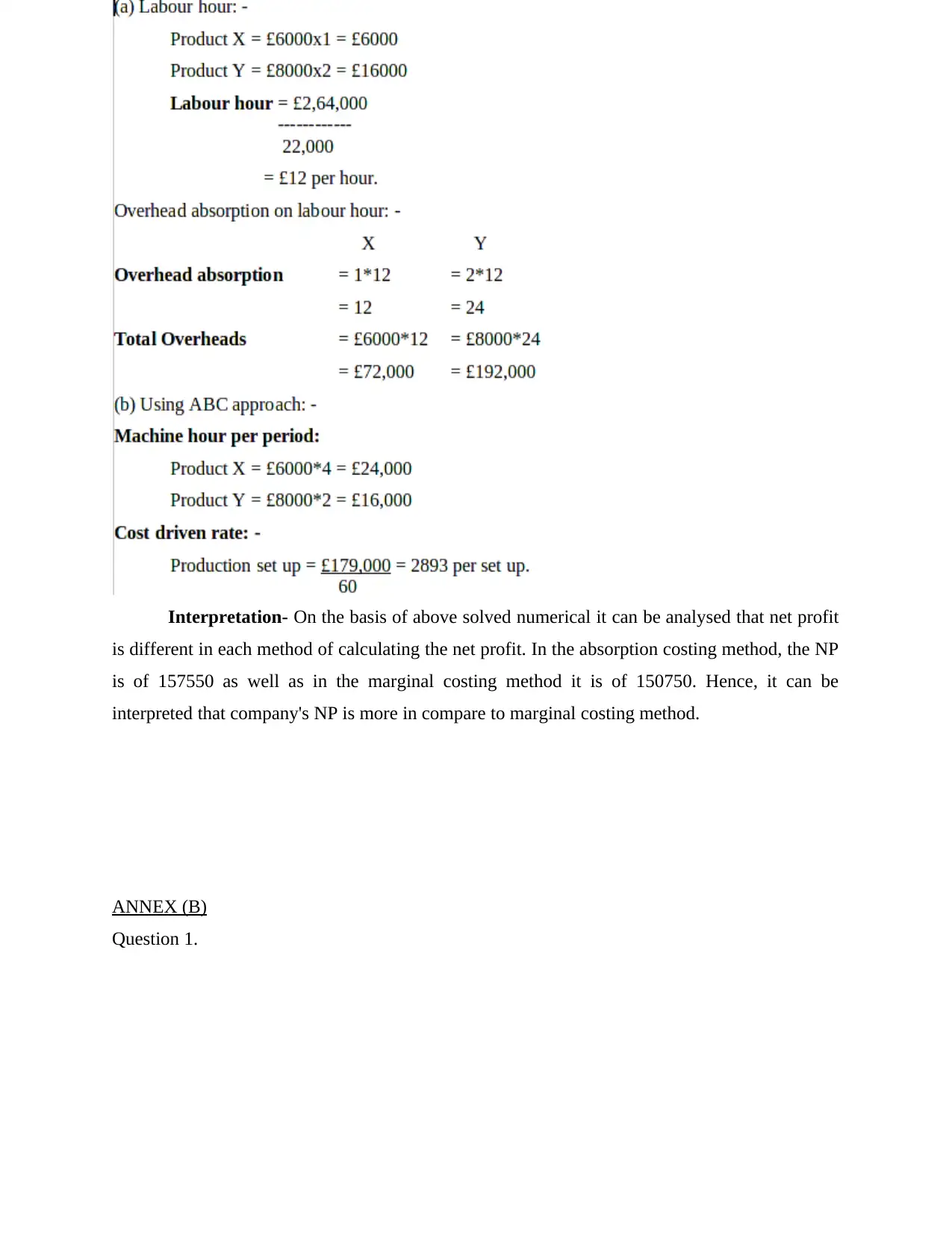

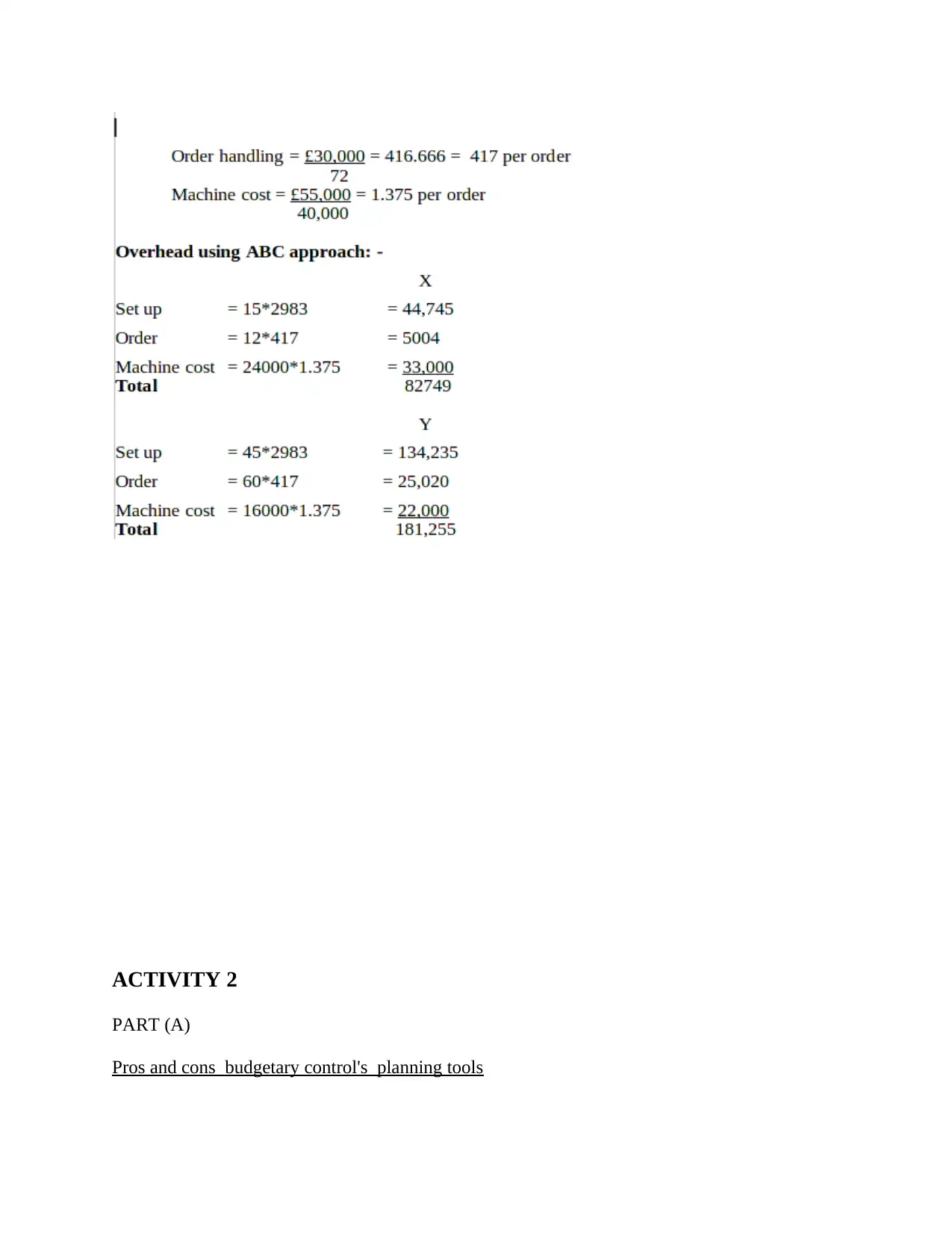

This report provides a comprehensive analysis of management accounting principles applied to O'Keefe Construction Limited, a civil engineering company based in London, UK. It explores the role of management accounting in decision-making, planning, and control, highlighting its importance in contrast to financial accounting. The report details various management accounting systems, including price optimization, inventory management, cost accounting, and job costing, and explains how these systems are utilized to generate crucial financial and non-financial reports such as inventory management reports, cost accounting reports, accounts receivable aging reports, and performance reports. It also compares and contrasts absorption costing and marginal costing techniques, demonstrating their impact on profit calculation through income statements for both methods, and evaluates the advantages and disadvantages of budgetary control planning tools, such as fixed budgets, for effective financial management. The analysis includes detailed calculations and interpretations, showcasing the practical application of management accounting in a real-world business context.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.