Financial & Asset Management: Budgeting, Costing, Oman Cement Analysis

VerifiedAdded on 2023/06/14

|12

|3041

|385

Report

AI Summary

This report conducts a financial and asset management analysis, applying accounting and financial management principles to Oman Cement Company. It examines budgetary control techniques such as variance analysis, zero-based budgeting, and responsibility accounting, evaluating their impact on business performance. The report also covers cost-volume-profit analysis, assessing how changes in cost and volume affect operating income. Furthermore, cost control and earned value techniques are applied to evaluate the performance of Oman Cement, focusing on cost reduction and project efficiency within the construction business.

Financial and Asset Management 1

Financial and Asset Management

Financial and Asset Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial and Asset Management 2

Table of Contents

Introduction......................................................................................................................................3

Principles of construction project management...............................................................................4

Analysis of budgetary control techniques for business performance examination.........................4

Evaluation of Cost, value, profit techniques....................................................................................7

Cost control and earned value techniques for analyzing the performance of Oman Cement..........9

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Table of Contents

Introduction......................................................................................................................................3

Principles of construction project management...............................................................................4

Analysis of budgetary control techniques for business performance examination.........................4

Evaluation of Cost, value, profit techniques....................................................................................7

Cost control and earned value techniques for analyzing the performance of Oman Cement..........9

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Financial and Asset Management 3

Introduction

The main aim of this report is to carry out the financial and asset management with including the

theories, principles and methodologies of accounting and the financial management. With

reference to this financial analysis, Oman Cement Company has been elected. The budgetary

techniques such as variance analysis, zero base budgeting and responsibility accounting have

been examined. This report also covers the cost volume profit analysis techniques through which

the changes in cost and volume, the impact can be overseen on the operating income. Moreover,

cost control and earned value techniques have also been applied over the chosen business in

order to assessing the performance of construction business.

Introduction

The main aim of this report is to carry out the financial and asset management with including the

theories, principles and methodologies of accounting and the financial management. With

reference to this financial analysis, Oman Cement Company has been elected. The budgetary

techniques such as variance analysis, zero base budgeting and responsibility accounting have

been examined. This report also covers the cost volume profit analysis techniques through which

the changes in cost and volume, the impact can be overseen on the operating income. Moreover,

cost control and earned value techniques have also been applied over the chosen business in

order to assessing the performance of construction business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial and Asset Management 4

Principles of construction project management

The construction industry is one of the most growing industries and it also contributes

significantly in relation to boosting the performance of nation. The OMAN cement business is

also a construction company which is also engaged into the construction project development

and it manufacture the cement for developing the project in this industry. The construction

industry follows the core principles that may be valuable to avail the significant return of project

management which is as

Project completion with the available resource management

Reliable scheduling

Managing the risk in project

Creation of real –time budget accountability (Otim, et al., 2012)

Development of great project plan

Analysis of budgetary control techniques for business performance examination

The main purpose of budgetary control is to carry out the comparison in between the real

revenue and spending in accordance with the planned aspects so that this budgetary comparison

can be resulted into meeting the gap and attempted to get out of profit (Shim, et al., 2011). On

the other hand, it becomes typical to prepare the budget under the inflationary conditions. In

addition to this, budget is geared up for the future period but the future is uncertain so that the

uncertainties might diminish the convenience of budgetary control mechanism (Eastman, 2018).

The positive impact and implementation of effective budgetary control is concerned to the

assistance of top management but if the support is not provided than it might not be successful.

In addition to this, the budgetary control is decisive for the Oman Cement business as it helps

business to increase efficiency, financial planning and quick reporting of information so that the

business operations can be planned, controlled and monitored in a significant coordination

manner.

Variance analysis: The variance analysis is very important for the Oman Cement company as it

allows the business to allocate the budgeted figures to the different department of Oman Cement

business and these figures are compared with the actual at the last time of financial year. With

this help of this technique, variation in the actual and budgeted figures and the variance may be

favorable and unfavorable for the business which assists the business to identify the cause behind

Principles of construction project management

The construction industry is one of the most growing industries and it also contributes

significantly in relation to boosting the performance of nation. The OMAN cement business is

also a construction company which is also engaged into the construction project development

and it manufacture the cement for developing the project in this industry. The construction

industry follows the core principles that may be valuable to avail the significant return of project

management which is as

Project completion with the available resource management

Reliable scheduling

Managing the risk in project

Creation of real –time budget accountability (Otim, et al., 2012)

Development of great project plan

Analysis of budgetary control techniques for business performance examination

The main purpose of budgetary control is to carry out the comparison in between the real

revenue and spending in accordance with the planned aspects so that this budgetary comparison

can be resulted into meeting the gap and attempted to get out of profit (Shim, et al., 2011). On

the other hand, it becomes typical to prepare the budget under the inflationary conditions. In

addition to this, budget is geared up for the future period but the future is uncertain so that the

uncertainties might diminish the convenience of budgetary control mechanism (Eastman, 2018).

The positive impact and implementation of effective budgetary control is concerned to the

assistance of top management but if the support is not provided than it might not be successful.

In addition to this, the budgetary control is decisive for the Oman Cement business as it helps

business to increase efficiency, financial planning and quick reporting of information so that the

business operations can be planned, controlled and monitored in a significant coordination

manner.

Variance analysis: The variance analysis is very important for the Oman Cement company as it

allows the business to allocate the budgeted figures to the different department of Oman Cement

business and these figures are compared with the actual at the last time of financial year. With

this help of this technique, variation in the actual and budgeted figures and the variance may be

favorable and unfavorable for the business which assists the business to identify the cause behind

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial and Asset Management 5

the variations in its budgeting and attempt to rectify the same (Wu, 2017). For instance, the

actual quantity of raw material for cement is recorded with the cost and quantity and this quantity

and cost is compared with the budgeted figures and it resulted into the determination of changes

in the amount and the variance analysis will be helpful for the Oman Cement business to reduce

the cost. On the other hand, it is very time –consuming process to find the results for business

performance which might also be resulted into the facilitation of effective control.

Zero base budgeting: The zero based budgeting is a technique of budgeting which helps the

business to plan the strategy in order to maintain the financials for business. It is a transparent

and open way for the Oman Cement business which is used by the business to create the budget

and identify the insights from the results. In comparison of traditional and zero-based budgeting,

the traditional method follows the previous year budget but the ZBB includes re-evaluation each

activity and start from the initial level for better planning (Dykstra, 2018). The Oman Cement

business uses the zero based budgeting for the purpose of decision making strategy. In relation to

this, the zero based budgeting can be used by the Oman business in order to allocating the

resources over the different departments and construction project activities in proper manner so

that the efficiency can be drawn in reliable manner. In addition to this, this technique is also

reliable for the cement company to identify the items of cash flow and cost of operations can

easily be determined that directly supports the business to reduce the cost for the business over

the desired performance of business (Kamali and Hewage, 2017). On the other hand, zero based

budgeting might also be critical for the Oman cement as it will require high man-power turnover

to plan and adequate and reasonable resource management which might influence the cost –

effectiveness assurance. In addition to this, this method might also be expensive for the Oman

Cement business if the accounting managers are lacking in the expertise to prepare the budget in

efficient manner.

Responsibility accounting: The responsibility accounting is also effective method for the

budgetary control strategy which is used by the business to measure the cost and revenue for the

different responsibility centre and measure the performance in reliable manner (Neal and

Harpham, 2017). In context to this, the major responsibility centers re as profit center, cost center

and revenue center which are attributed towards the determination of performance of assigned

each responsibility center that can empower the accounting system.

the variations in its budgeting and attempt to rectify the same (Wu, 2017). For instance, the

actual quantity of raw material for cement is recorded with the cost and quantity and this quantity

and cost is compared with the budgeted figures and it resulted into the determination of changes

in the amount and the variance analysis will be helpful for the Oman Cement business to reduce

the cost. On the other hand, it is very time –consuming process to find the results for business

performance which might also be resulted into the facilitation of effective control.

Zero base budgeting: The zero based budgeting is a technique of budgeting which helps the

business to plan the strategy in order to maintain the financials for business. It is a transparent

and open way for the Oman Cement business which is used by the business to create the budget

and identify the insights from the results. In comparison of traditional and zero-based budgeting,

the traditional method follows the previous year budget but the ZBB includes re-evaluation each

activity and start from the initial level for better planning (Dykstra, 2018). The Oman Cement

business uses the zero based budgeting for the purpose of decision making strategy. In relation to

this, the zero based budgeting can be used by the Oman business in order to allocating the

resources over the different departments and construction project activities in proper manner so

that the efficiency can be drawn in reliable manner. In addition to this, this technique is also

reliable for the cement company to identify the items of cash flow and cost of operations can

easily be determined that directly supports the business to reduce the cost for the business over

the desired performance of business (Kamali and Hewage, 2017). On the other hand, zero based

budgeting might also be critical for the Oman cement as it will require high man-power turnover

to plan and adequate and reasonable resource management which might influence the cost –

effectiveness assurance. In addition to this, this method might also be expensive for the Oman

Cement business if the accounting managers are lacking in the expertise to prepare the budget in

efficient manner.

Responsibility accounting: The responsibility accounting is also effective method for the

budgetary control strategy which is used by the business to measure the cost and revenue for the

different responsibility centre and measure the performance in reliable manner (Neal and

Harpham, 2017). In context to this, the major responsibility centers re as profit center, cost center

and revenue center which are attributed towards the determination of performance of assigned

each responsibility center that can empower the accounting system.

Financial and Asset Management 6

Cost center: The cost center segment is an important aspect for the business for which the

managers of organization are responsible in order to measure the cost which incurred in the

business operations. The cost center is valuable for the Oman Cement business in order to plan

out the business cost and it is a comparison in between the actual and budgeted and it is also

supportive for business to take decisions effectively. As the Oman Cement manufacturing

business is a manufacturing business for which the production and service departments are the

cost center. Along with this, the marketing department is also a cost center for the Oman Cement

business to determine the cost for business.

Revenue center: The revenue center is also an important center for the cost determination and

this center is responsible for the measurement of business revenue in a particular time period. On

the other hand, the assigned people is not engaged into the control of cost, assets investment but

the responsible people focused on the reducing expenses for the marketing service to promoting

the products to enhance the awareness about the business products (Neal and Harpham, 2017). In

addition to this, the revenue center is concerned towards the comparison of actual and budgeted

revenue for the business and decisions are taken accordingly. For the revenue center for business,

product line manager and sales representative are the revenue center which helps the business to

generate the higher revenue.

Profit center: The profit center is a crucial center for the business which can be affected from the

revenue and cost centers for business. The main objective of this center is to gain the profit for

business. In addition to this, it can also be stated that the profit centers are reliable for the Oman

cement business in which it leads to encourage the center’s manager to increase the production

and distribution of product so that business can generate higher revenue.

Evaluation of Cost, value, profit techniques

The cost value profit analysis is significant for the Oman Cement company to measure the

contribution margin from deducting the variable expenses out of total sales revenue (Dykstra,

2018). It is also significant to review the performance of business and the remaining amount can

also be used by the business for covering the fixed cost. The Cost value profit analysis is

important for the Oman Cement company in relation to measure the future sales, profit and cost

for the business which will directly resulted into the amendment of decisions for gaining higher

profits. On the other hand, it is also critical for the business to determine the targeted income for

which how much sales is required is also forecasted (Harrison and Lock, 2017). In context to

Cost center: The cost center segment is an important aspect for the business for which the

managers of organization are responsible in order to measure the cost which incurred in the

business operations. The cost center is valuable for the Oman Cement business in order to plan

out the business cost and it is a comparison in between the actual and budgeted and it is also

supportive for business to take decisions effectively. As the Oman Cement manufacturing

business is a manufacturing business for which the production and service departments are the

cost center. Along with this, the marketing department is also a cost center for the Oman Cement

business to determine the cost for business.

Revenue center: The revenue center is also an important center for the cost determination and

this center is responsible for the measurement of business revenue in a particular time period. On

the other hand, the assigned people is not engaged into the control of cost, assets investment but

the responsible people focused on the reducing expenses for the marketing service to promoting

the products to enhance the awareness about the business products (Neal and Harpham, 2017). In

addition to this, the revenue center is concerned towards the comparison of actual and budgeted

revenue for the business and decisions are taken accordingly. For the revenue center for business,

product line manager and sales representative are the revenue center which helps the business to

generate the higher revenue.

Profit center: The profit center is a crucial center for the business which can be affected from the

revenue and cost centers for business. The main objective of this center is to gain the profit for

business. In addition to this, it can also be stated that the profit centers are reliable for the Oman

cement business in which it leads to encourage the center’s manager to increase the production

and distribution of product so that business can generate higher revenue.

Evaluation of Cost, value, profit techniques

The cost value profit analysis is significant for the Oman Cement company to measure the

contribution margin from deducting the variable expenses out of total sales revenue (Dykstra,

2018). It is also significant to review the performance of business and the remaining amount can

also be used by the business for covering the fixed cost. The Cost value profit analysis is

important for the Oman Cement company in relation to measure the future sales, profit and cost

for the business which will directly resulted into the amendment of decisions for gaining higher

profits. On the other hand, it is also critical for the business to determine the targeted income for

which how much sales is required is also forecasted (Harrison and Lock, 2017). In context to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial and Asset Management 7

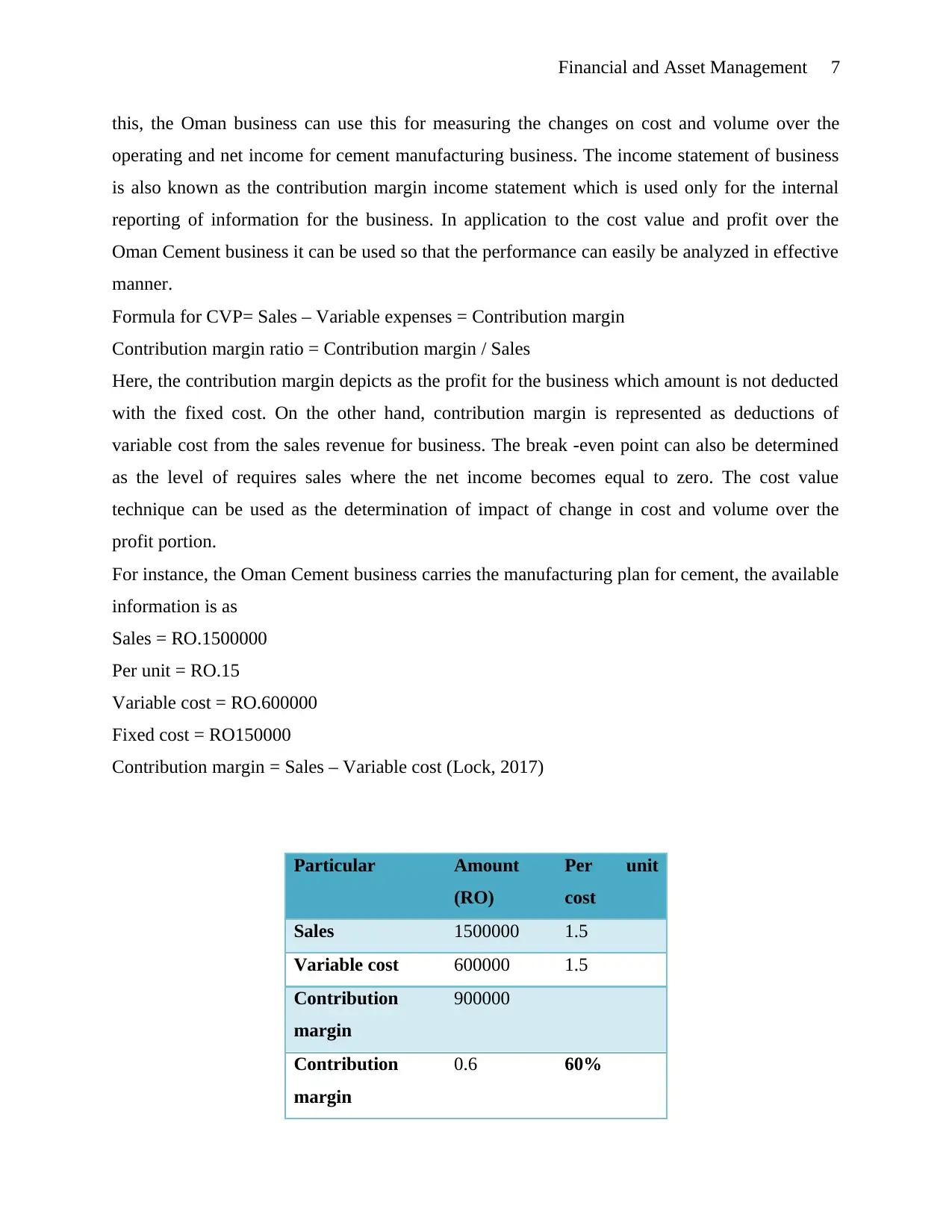

this, the Oman business can use this for measuring the changes on cost and volume over the

operating and net income for cement manufacturing business. The income statement of business

is also known as the contribution margin income statement which is used only for the internal

reporting of information for the business. In application to the cost value and profit over the

Oman Cement business it can be used so that the performance can easily be analyzed in effective

manner.

Formula for CVP= Sales – Variable expenses = Contribution margin

Contribution margin ratio = Contribution margin / Sales

Here, the contribution margin depicts as the profit for the business which amount is not deducted

with the fixed cost. On the other hand, contribution margin is represented as deductions of

variable cost from the sales revenue for business. The break -even point can also be determined

as the level of requires sales where the net income becomes equal to zero. The cost value

technique can be used as the determination of impact of change in cost and volume over the

profit portion.

For instance, the Oman Cement business carries the manufacturing plan for cement, the available

information is as

Sales = RO.1500000

Per unit = RO.15

Variable cost = RO.600000

Fixed cost = RO150000

Contribution margin = Sales – Variable cost (Lock, 2017)

Particular Amount

(RO)

Per unit

cost

Sales 1500000 1.5

Variable cost 600000 1.5

Contribution

margin

900000

Contribution

margin

0.6 60%

this, the Oman business can use this for measuring the changes on cost and volume over the

operating and net income for cement manufacturing business. The income statement of business

is also known as the contribution margin income statement which is used only for the internal

reporting of information for the business. In application to the cost value and profit over the

Oman Cement business it can be used so that the performance can easily be analyzed in effective

manner.

Formula for CVP= Sales – Variable expenses = Contribution margin

Contribution margin ratio = Contribution margin / Sales

Here, the contribution margin depicts as the profit for the business which amount is not deducted

with the fixed cost. On the other hand, contribution margin is represented as deductions of

variable cost from the sales revenue for business. The break -even point can also be determined

as the level of requires sales where the net income becomes equal to zero. The cost value

technique can be used as the determination of impact of change in cost and volume over the

profit portion.

For instance, the Oman Cement business carries the manufacturing plan for cement, the available

information is as

Sales = RO.1500000

Per unit = RO.15

Variable cost = RO.600000

Fixed cost = RO150000

Contribution margin = Sales – Variable cost (Lock, 2017)

Particular Amount

(RO)

Per unit

cost

Sales 1500000 1.5

Variable cost 600000 1.5

Contribution

margin

900000

Contribution

margin

0.6 60%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial and Asset Management 8

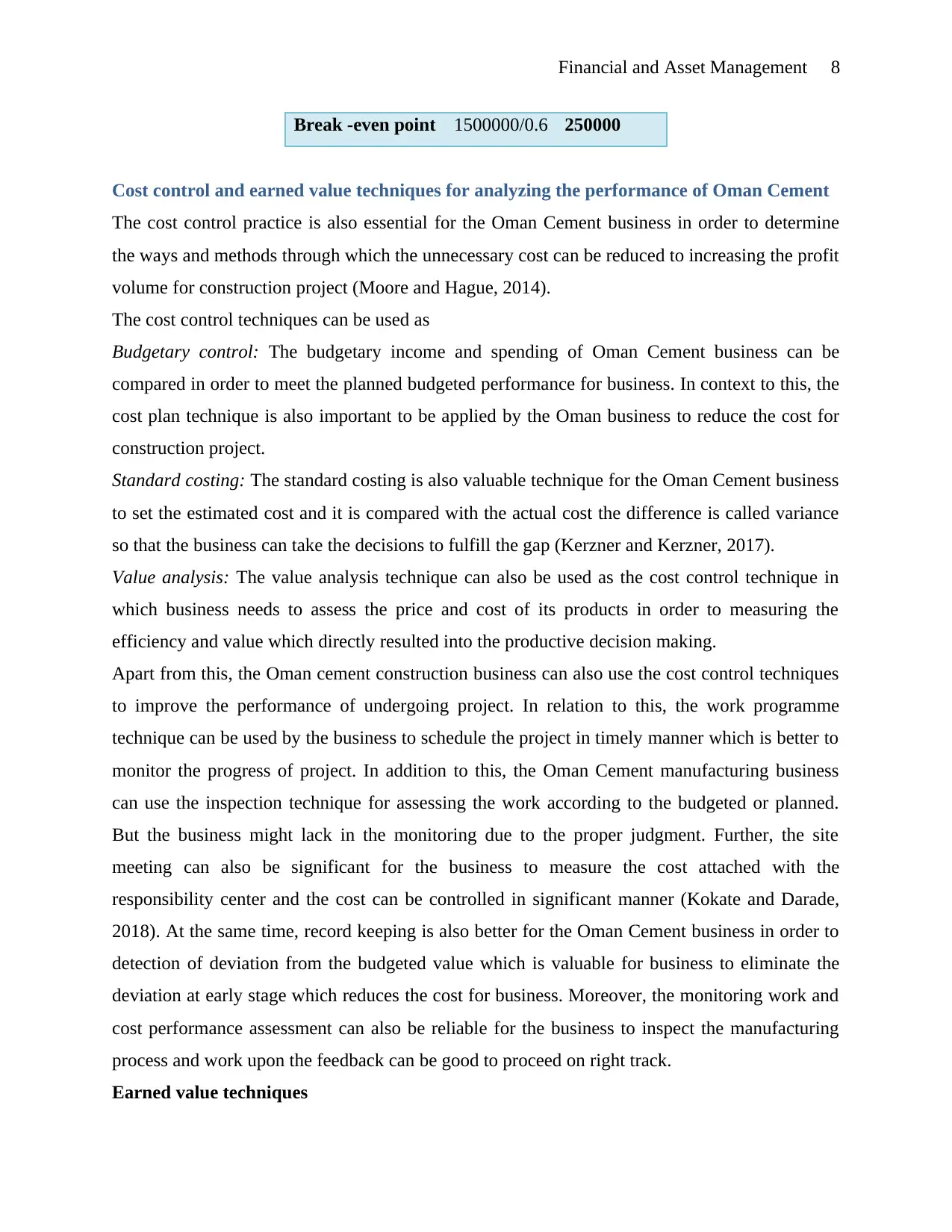

Break -even point 1500000/0.6 250000

Cost control and earned value techniques for analyzing the performance of Oman Cement

The cost control practice is also essential for the Oman Cement business in order to determine

the ways and methods through which the unnecessary cost can be reduced to increasing the profit

volume for construction project (Moore and Hague, 2014).

The cost control techniques can be used as

Budgetary control: The budgetary income and spending of Oman Cement business can be

compared in order to meet the planned budgeted performance for business. In context to this, the

cost plan technique is also important to be applied by the Oman business to reduce the cost for

construction project.

Standard costing: The standard costing is also valuable technique for the Oman Cement business

to set the estimated cost and it is compared with the actual cost the difference is called variance

so that the business can take the decisions to fulfill the gap (Kerzner and Kerzner, 2017).

Value analysis: The value analysis technique can also be used as the cost control technique in

which business needs to assess the price and cost of its products in order to measuring the

efficiency and value which directly resulted into the productive decision making.

Apart from this, the Oman cement construction business can also use the cost control techniques

to improve the performance of undergoing project. In relation to this, the work programme

technique can be used by the business to schedule the project in timely manner which is better to

monitor the progress of project. In addition to this, the Oman Cement manufacturing business

can use the inspection technique for assessing the work according to the budgeted or planned.

But the business might lack in the monitoring due to the proper judgment. Further, the site

meeting can also be significant for the business to measure the cost attached with the

responsibility center and the cost can be controlled in significant manner (Kokate and Darade,

2018). At the same time, record keeping is also better for the Oman Cement business in order to

detection of deviation from the budgeted value which is valuable for business to eliminate the

deviation at early stage which reduces the cost for business. Moreover, the monitoring work and

cost performance assessment can also be reliable for the business to inspect the manufacturing

process and work upon the feedback can be good to proceed on right track.

Earned value techniques

Break -even point 1500000/0.6 250000

Cost control and earned value techniques for analyzing the performance of Oman Cement

The cost control practice is also essential for the Oman Cement business in order to determine

the ways and methods through which the unnecessary cost can be reduced to increasing the profit

volume for construction project (Moore and Hague, 2014).

The cost control techniques can be used as

Budgetary control: The budgetary income and spending of Oman Cement business can be

compared in order to meet the planned budgeted performance for business. In context to this, the

cost plan technique is also important to be applied by the Oman business to reduce the cost for

construction project.

Standard costing: The standard costing is also valuable technique for the Oman Cement business

to set the estimated cost and it is compared with the actual cost the difference is called variance

so that the business can take the decisions to fulfill the gap (Kerzner and Kerzner, 2017).

Value analysis: The value analysis technique can also be used as the cost control technique in

which business needs to assess the price and cost of its products in order to measuring the

efficiency and value which directly resulted into the productive decision making.

Apart from this, the Oman cement construction business can also use the cost control techniques

to improve the performance of undergoing project. In relation to this, the work programme

technique can be used by the business to schedule the project in timely manner which is better to

monitor the progress of project. In addition to this, the Oman Cement manufacturing business

can use the inspection technique for assessing the work according to the budgeted or planned.

But the business might lack in the monitoring due to the proper judgment. Further, the site

meeting can also be significant for the business to measure the cost attached with the

responsibility center and the cost can be controlled in significant manner (Kokate and Darade,

2018). At the same time, record keeping is also better for the Oman Cement business in order to

detection of deviation from the budgeted value which is valuable for business to eliminate the

deviation at early stage which reduces the cost for business. Moreover, the monitoring work and

cost performance assessment can also be reliable for the business to inspect the manufacturing

process and work upon the feedback can be good to proceed on right track.

Earned value techniques

Financial and Asset Management 9

The earned value technique is termed as the technique through which the performance of project

can be measured in relation to objective manner. The earned value techniques are supportive to

track the performance of Oman Cement business in against to the project baseline. The output

from the earned value techniques are also helpful for business to measure the deviation of project

from the schedule and cost as well. The earned value technique is convenient for the Oman

Cement business to schedule construction activities, controlling account and project process in

planned manner so that the desired outcome of project can be measured in efficient manner.

The earned value technique is termed as the technique through which the performance of project

can be measured in relation to objective manner. The earned value techniques are supportive to

track the performance of Oman Cement business in against to the project baseline. The output

from the earned value techniques are also helpful for business to measure the deviation of project

from the schedule and cost as well. The earned value technique is convenient for the Oman

Cement business to schedule construction activities, controlling account and project process in

planned manner so that the desired outcome of project can be measured in efficient manner.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial and Asset Management 10

Conclusion

On the basis of above analysis, it can be concluded that the finance and asset management is

valuable for the business to manage its performance. It can also be concluded that the principles

are the constraints for the project as to finish the project under projected budget and time with

the scope. It can also be summarized that the variance analysis is supportive fort Oman Cement

business to measure the difference in its actual and budgeted income and expenses which

indicates towards better decisions. The zero –based budgeting is also reliable for business to

allocate the resource from new scratch not following the previous budget. On the other hand,

responsibility center as profit, revenue and cost are good to gauge the performance of business in

effective manner. It can also be said that the cost value profit analysis method is also good to

measure the contribution of business in accounting manner. Apart from this, it can also be stated

that the business can use the cost control techniques such as budgeting control, value analysis,

standard accounting, work programming and scheduling, site meetings, record keeping and

monitoring the work and cost performance against the planned criteria so that the Oman business

can control over the cost and positive value can be earned for construction project.

Conclusion

On the basis of above analysis, it can be concluded that the finance and asset management is

valuable for the business to manage its performance. It can also be concluded that the principles

are the constraints for the project as to finish the project under projected budget and time with

the scope. It can also be summarized that the variance analysis is supportive fort Oman Cement

business to measure the difference in its actual and budgeted income and expenses which

indicates towards better decisions. The zero –based budgeting is also reliable for business to

allocate the resource from new scratch not following the previous budget. On the other hand,

responsibility center as profit, revenue and cost are good to gauge the performance of business in

effective manner. It can also be said that the cost value profit analysis method is also good to

measure the contribution of business in accounting manner. Apart from this, it can also be stated

that the business can use the cost control techniques such as budgeting control, value analysis,

standard accounting, work programming and scheduling, site meetings, record keeping and

monitoring the work and cost performance against the planned criteria so that the Oman business

can control over the cost and positive value can be earned for construction project.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial and Asset Management 11

References

Dykstra, A., (2018) Construction project management: A complete introduction. USA: Kirshner

Publishing Company.

Eastman, C.M., (2018) Building product models: computer environments, supporting design and

construction. USA: CRC press.

Harrison, F. and Lock, D., (2017) Advanced project management: a structured approach. UK:

Routledge.

Kamali, M. and Hewage, K., (2017) Development of performance criteria for sustainability

evaluation of modular versus conventional construction methods. Journal of cleaner production,

142, pp.3592-3606.

Kerzner, H. and Kerzner, H.R., (2017) Project management: a systems approach to planning,

scheduling, and controlling. USA: John Wiley & Sons.

Kokate, P., and Darade, M. (2018) Cost Control Techniques for Construction Project.

International Research Journal of Engineering and Technology (IRJET), 5(6), pp. 1-4.

Lock, D., (2017) The essentials of project management. UK: Routledge.

Moore,D. andHague, D. (2014) Building Production Management Techniques: An Introduction

through a Systems Approach. UK: Routledge.

Neal, J. and Harpham, A., (2017) The Spirit of Project Management. UK: Routledge.

OCC (2017) Annual Report 2017. [Online]. Available from: https://occ.om/images/OCC-

2017.pdf (Accessed: November 16, 2018).

OCC (2018) About Us. [Online]. Available from: https://occ.om/about-us.html (Accessed:

November 16, 2018).

Otim, G., Nakacwa, F. and Kyakula, M., (2012) Cost control techniques used on building

construction sites in Uganda. In Second International Conference on Advances in Engineering

and Technology pp. 367-373.

Shim,J. Siegel, J. and Shim, A. (2011) Budgeting Basics and Beyond. USA: John Wiley and

Sons.

Wu, G., Zhao, X. and Zuo, J., (2017) Relationship between project’s added value and the trust–

conflict interaction among project teams. Journal of Management in Engineering, 33(4).

References

Dykstra, A., (2018) Construction project management: A complete introduction. USA: Kirshner

Publishing Company.

Eastman, C.M., (2018) Building product models: computer environments, supporting design and

construction. USA: CRC press.

Harrison, F. and Lock, D., (2017) Advanced project management: a structured approach. UK:

Routledge.

Kamali, M. and Hewage, K., (2017) Development of performance criteria for sustainability

evaluation of modular versus conventional construction methods. Journal of cleaner production,

142, pp.3592-3606.

Kerzner, H. and Kerzner, H.R., (2017) Project management: a systems approach to planning,

scheduling, and controlling. USA: John Wiley & Sons.

Kokate, P., and Darade, M. (2018) Cost Control Techniques for Construction Project.

International Research Journal of Engineering and Technology (IRJET), 5(6), pp. 1-4.

Lock, D., (2017) The essentials of project management. UK: Routledge.

Moore,D. andHague, D. (2014) Building Production Management Techniques: An Introduction

through a Systems Approach. UK: Routledge.

Neal, J. and Harpham, A., (2017) The Spirit of Project Management. UK: Routledge.

OCC (2017) Annual Report 2017. [Online]. Available from: https://occ.om/images/OCC-

2017.pdf (Accessed: November 16, 2018).

OCC (2018) About Us. [Online]. Available from: https://occ.om/about-us.html (Accessed:

November 16, 2018).

Otim, G., Nakacwa, F. and Kyakula, M., (2012) Cost control techniques used on building

construction sites in Uganda. In Second International Conference on Advances in Engineering

and Technology pp. 367-373.

Shim,J. Siegel, J. and Shim, A. (2011) Budgeting Basics and Beyond. USA: John Wiley and

Sons.

Wu, G., Zhao, X. and Zuo, J., (2017) Relationship between project’s added value and the trust–

conflict interaction among project teams. Journal of Management in Engineering, 33(4).

Financial and Asset Management 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.