SAPM Report: Fundamental Analysis of Oman Stock Market

VerifiedAdded on 2021/06/16

|17

|3981

|293

Report

AI Summary

This report presents a fundamental analysis of the Oman stock market, evaluating investment opportunities. It begins with an introduction to the Muscat Securities Market and the significance of fundamental analysis. The methodology section details the data collection process, focusing on secondary data from the Muscat Securities Market and company annual reports, with a study period from 2017 to 2018. The core of the report applies fundamental analysis, examining the Omani economy through GDP, interest rates, and oil prices, followed by industry analysis of the financial, industrial, and service sectors. Company analysis is performed on selected firms, including EPS, DPS, ROI, and P/E ratios. The report concludes by summarizing investment viability based on the analysis, including risk and return assessments of selected companies and the MSM Index.

Running head: SAPM

SAPM

Name of the Student:

Name of the University:

Authors Note:

SAPM

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SAPM

1

Table of Contents

1. Introduction:...........................................................................................................................2

2. Methodology:.........................................................................................................................3

3. Application of Fundamental Analysis:...................................................................................4

Country Analysis:.......................................................................................................................4

Industry Analysis:......................................................................................................................7

Company Analysis:..................................................................................................................10

4. Conclusion:..........................................................................................................................14

Reference and Bibliography:....................................................................................................15

1

Table of Contents

1. Introduction:...........................................................................................................................2

2. Methodology:.........................................................................................................................3

3. Application of Fundamental Analysis:...................................................................................4

Country Analysis:.......................................................................................................................4

Industry Analysis:......................................................................................................................7

Company Analysis:..................................................................................................................10

4. Conclusion:..........................................................................................................................14

Reference and Bibliography:....................................................................................................15

SAPM

2

1. Introduction:

The overall assessment mainly focuses on identifying the significance of fundamental

analysis and how out could allow investors to detect investment opportunity, which could

increase return from investment. In addition, the assessment structure mainly comprises of

methodology, fundamental analysis, and conclusion, which could help in detecting the overall

stock that could be used for investment. The overall date collection process and period of the

study is also depicted to identify viability of the research, which is conducted on the stock for

deriving its financial viability in the long-run. Moreover, financial performance of the

company is identified, which could help in understanding the level of returns that might be

provided from investment. Furthermore, the overall fundamental valuation also helps in

understanding the level of progress that could be generated form investment.

The main objective of the report is to identify the investment opportunity based on

fundamental analysis, which could help in understanding the level of return that could be

generated the investment. In addition, the risk and return concept of investors are also

conducted to identify investment opportunity, which could be generated from investment.

Furthermore, the investment scope detected with the help of fundamental analysis mainly

helps in understanding the level of profits that could be generated form investment.

Moreover, relevant country, company and industry analysis is conducted to identify the level

of returns, which could be generated form investment.

There is only one stock exchange market in Oman, known as the Muscat Securities

Market, which was established in 1988 for developing the financial sector of the country

(Msm.gov.om 2018). The overall security exchange market in Oman allowed the

international organisation to set up their operations in Oman and participate effectively to

strengthen the sultanate. In addition, the creation of the market allowed companies in Oman

2

1. Introduction:

The overall assessment mainly focuses on identifying the significance of fundamental

analysis and how out could allow investors to detect investment opportunity, which could

increase return from investment. In addition, the assessment structure mainly comprises of

methodology, fundamental analysis, and conclusion, which could help in detecting the overall

stock that could be used for investment. The overall date collection process and period of the

study is also depicted to identify viability of the research, which is conducted on the stock for

deriving its financial viability in the long-run. Moreover, financial performance of the

company is identified, which could help in understanding the level of returns that might be

provided from investment. Furthermore, the overall fundamental valuation also helps in

understanding the level of progress that could be generated form investment.

The main objective of the report is to identify the investment opportunity based on

fundamental analysis, which could help in understanding the level of return that could be

generated the investment. In addition, the risk and return concept of investors are also

conducted to identify investment opportunity, which could be generated from investment.

Furthermore, the investment scope detected with the help of fundamental analysis mainly

helps in understanding the level of profits that could be generated form investment.

Moreover, relevant country, company and industry analysis is conducted to identify the level

of returns, which could be generated form investment.

There is only one stock exchange market in Oman, known as the Muscat Securities

Market, which was established in 1988 for developing the financial sector of the country

(Msm.gov.om 2018). The overall security exchange market in Oman allowed the

international organisation to set up their operations in Oman and participate effectively to

strengthen the sultanate. In addition, the creation of the market allowed companies in Oman

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

SAPM

3

to participate in the capital market growth, while obtaining the level of funds to conduct their

operations. The MSM-Index was relatively formed in 1992 with the 30 most highly traded

stock in the market. The combination of the stocks relevantly helped in understanding the

level of returns, which could be generated from investment in the Omani security market. The

MSM index comprises of companies who are old and are not government controlled, while

their shares are most liquid in the market. Moreover, the Muscat Securities Market has been

awarded ISO 9001:2008 certificate for trading securities and ISO 27001:2005 certificate for

information security management system.

2. Methodology:

Data Collection:

The data collection conducted for the assessment is secondary in nature, as the data is

collected from the website of Muscat Securities Market. The data was collected it the excel

sheet, which helped in completing the overall requirement of the calculation conducted on the

assessment. In addition, the data for the ratios was collected from the annual report of the

companies used in the assessment for calculation purposes. Lastly, the data used in the

assessment for analysis performance of the organisation is from the annual report of the

company, which is presented in both the website of the company and in Muscat Securities

Market welfare (Tradingeconomics.com 2018).

Period of the study:

The overall period that was taken for the calculation purposes is one year, which

could help in understanding the level of return, which could improve the investment. In

addition, the data from 2017 to 2018 is relevantly taken into consideration for completing the

assessment and analyse the performance of selected companies. Furthermore, the share price

3

to participate in the capital market growth, while obtaining the level of funds to conduct their

operations. The MSM-Index was relatively formed in 1992 with the 30 most highly traded

stock in the market. The combination of the stocks relevantly helped in understanding the

level of returns, which could be generated from investment in the Omani security market. The

MSM index comprises of companies who are old and are not government controlled, while

their shares are most liquid in the market. Moreover, the Muscat Securities Market has been

awarded ISO 9001:2008 certificate for trading securities and ISO 27001:2005 certificate for

information security management system.

2. Methodology:

Data Collection:

The data collection conducted for the assessment is secondary in nature, as the data is

collected from the website of Muscat Securities Market. The data was collected it the excel

sheet, which helped in completing the overall requirement of the calculation conducted on the

assessment. In addition, the data for the ratios was collected from the annual report of the

companies used in the assessment for calculation purposes. Lastly, the data used in the

assessment for analysis performance of the organisation is from the annual report of the

company, which is presented in both the website of the company and in Muscat Securities

Market welfare (Tradingeconomics.com 2018).

Period of the study:

The overall period that was taken for the calculation purposes is one year, which

could help in understanding the level of return, which could improve the investment. In

addition, the data from 2017 to 2018 is relevantly taken into consideration for completing the

assessment and analyse the performance of selected companies. Furthermore, the share price

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SAPM

4

movement of the companies are also taken from historical price movement between April

2017 to April 2018. This helped in detecting the level of returns, which could be generated

from investment (Tradingeconomics.com 2018).

3. Application of Fundamental Analysis:

Country Analysis:

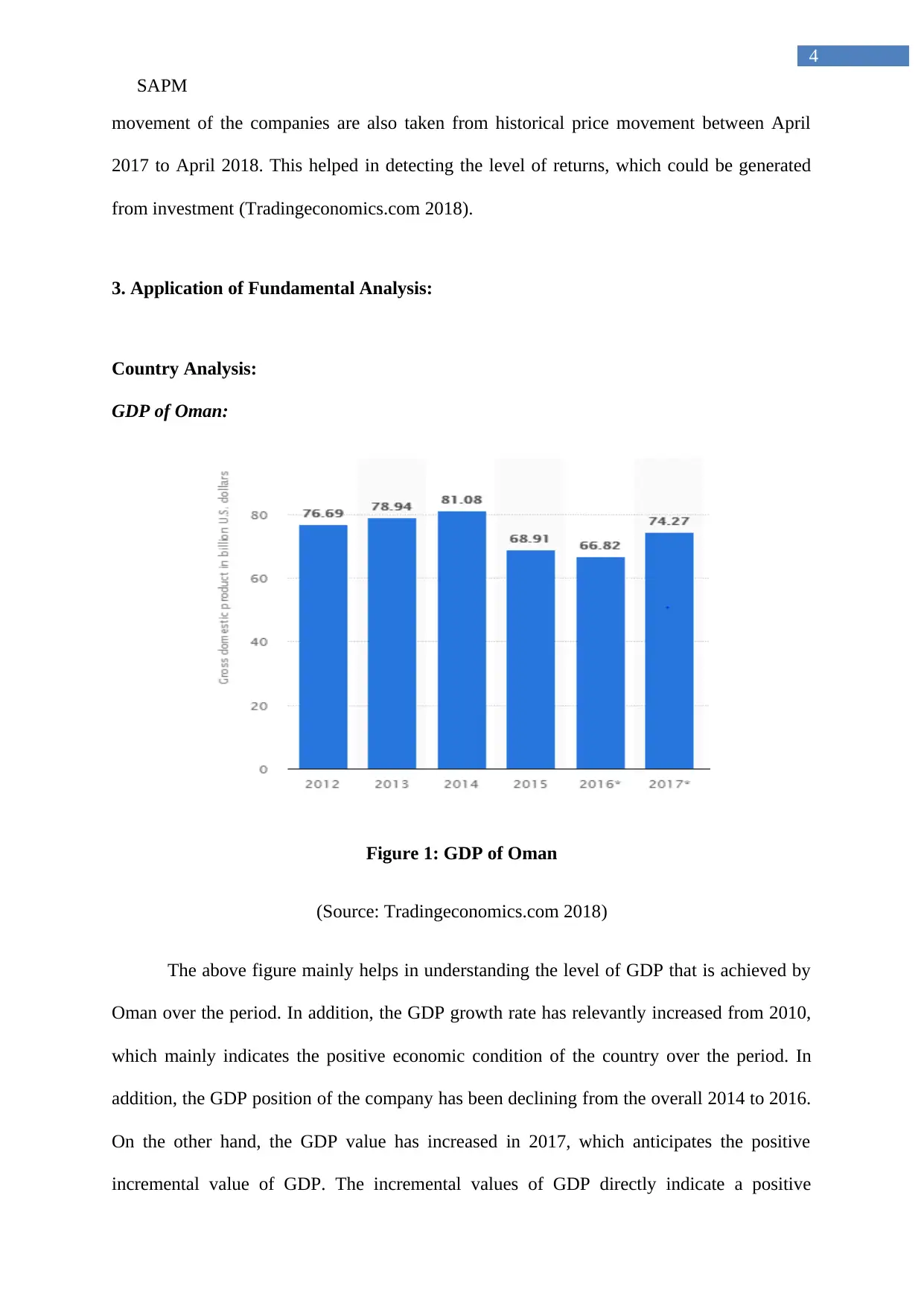

GDP of Oman:

Figure 1: GDP of Oman

(Source: Tradingeconomics.com 2018)

The above figure mainly helps in understanding the level of GDP that is achieved by

Oman over the period. In addition, the GDP growth rate has relevantly increased from 2010,

which mainly indicates the positive economic condition of the country over the period. In

addition, the GDP position of the company has been declining from the overall 2014 to 2016.

On the other hand, the GDP value has increased in 2017, which anticipates the positive

incremental value of GDP. The incremental values of GDP directly indicate a positive

4

movement of the companies are also taken from historical price movement between April

2017 to April 2018. This helped in detecting the level of returns, which could be generated

from investment (Tradingeconomics.com 2018).

3. Application of Fundamental Analysis:

Country Analysis:

GDP of Oman:

Figure 1: GDP of Oman

(Source: Tradingeconomics.com 2018)

The above figure mainly helps in understanding the level of GDP that is achieved by

Oman over the period. In addition, the GDP growth rate has relevantly increased from 2010,

which mainly indicates the positive economic condition of the country over the period. In

addition, the GDP position of the company has been declining from the overall 2014 to 2016.

On the other hand, the GDP value has increased in 2017, which anticipates the positive

incremental value of GDP. The incremental values of GDP directly indicate a positive

SAPM

5

attribute of the Omani economic condition, which could be feasible for the investor to

generate high rate of returns from investment. The GDP directly states the positive increment

in the overall economic position of the country and the incremental value of Omani GDP

indicates the high probability of positive economic position of the country. In this context,

Akimova, Stein and Prokhorova (2015) stated that with the measurement of GDP the

investment opportunity in the country is anticipated by the investors.

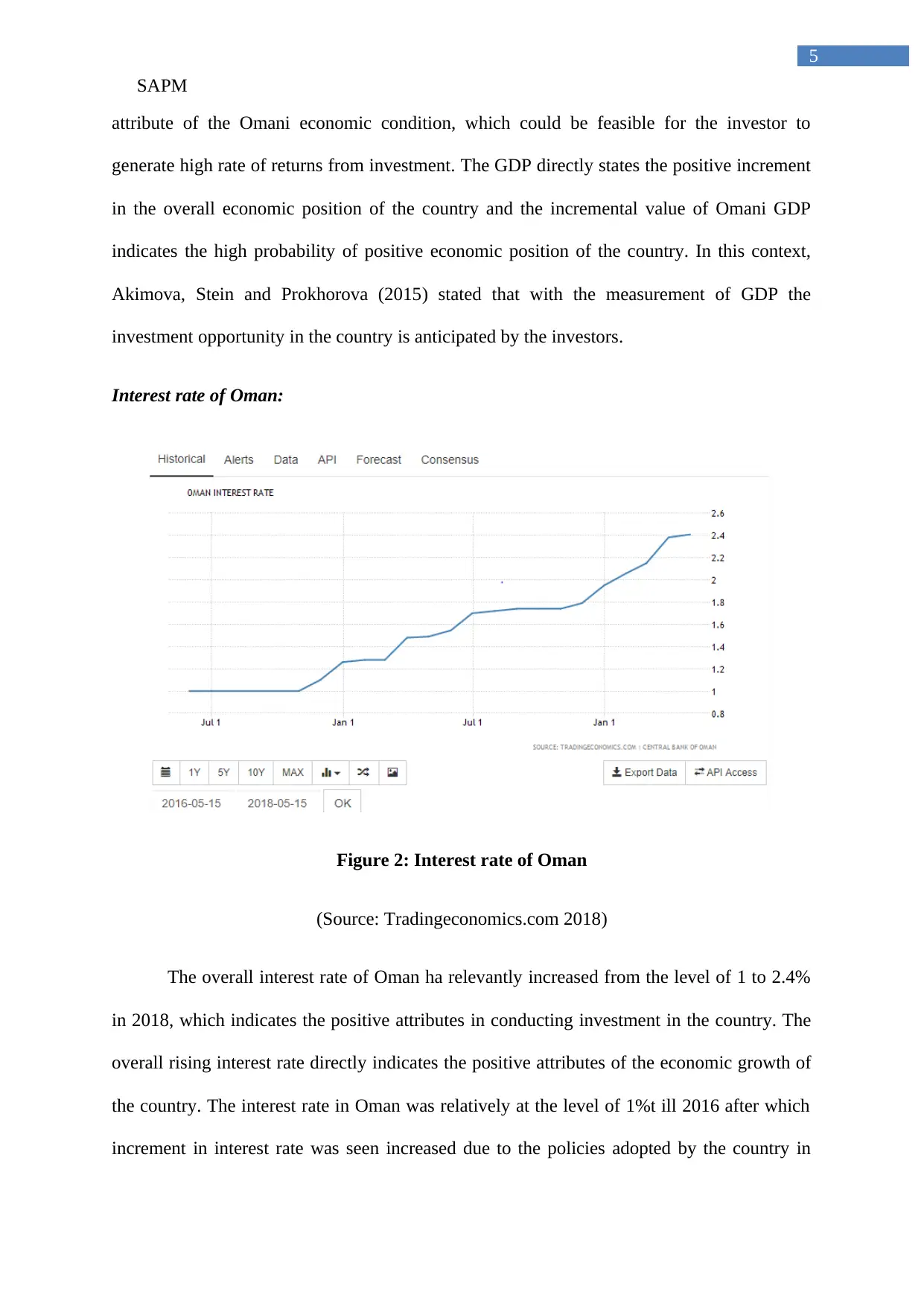

Interest rate of Oman:

Figure 2: Interest rate of Oman

(Source: Tradingeconomics.com 2018)

The overall interest rate of Oman ha relevantly increased from the level of 1 to 2.4%

in 2018, which indicates the positive attributes in conducting investment in the country. The

overall rising interest rate directly indicates the positive attributes of the economic growth of

the country. The interest rate in Oman was relatively at the level of 1%t ill 2016 after which

increment in interest rate was seen increased due to the policies adopted by the country in

5

attribute of the Omani economic condition, which could be feasible for the investor to

generate high rate of returns from investment. The GDP directly states the positive increment

in the overall economic position of the country and the incremental value of Omani GDP

indicates the high probability of positive economic position of the country. In this context,

Akimova, Stein and Prokhorova (2015) stated that with the measurement of GDP the

investment opportunity in the country is anticipated by the investors.

Interest rate of Oman:

Figure 2: Interest rate of Oman

(Source: Tradingeconomics.com 2018)

The overall interest rate of Oman ha relevantly increased from the level of 1 to 2.4%

in 2018, which indicates the positive attributes in conducting investment in the country. The

overall rising interest rate directly indicates the positive attributes of the economic growth of

the country. The interest rate in Oman was relatively at the level of 1%t ill 2016 after which

increment in interest rate was seen increased due to the policies adopted by the country in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

SAPM

6

easing their currency and creating demand for their product in the intentional market. In this

context, Krupa (2016) stated that with the investment in overall interest rates citizens are

interested in depositing more into the bank, which is used for other economy development

process by the government. However, the condition of financial sector will deteriorate, as

more interest payment will be provided to the depositors reducing their interest income.

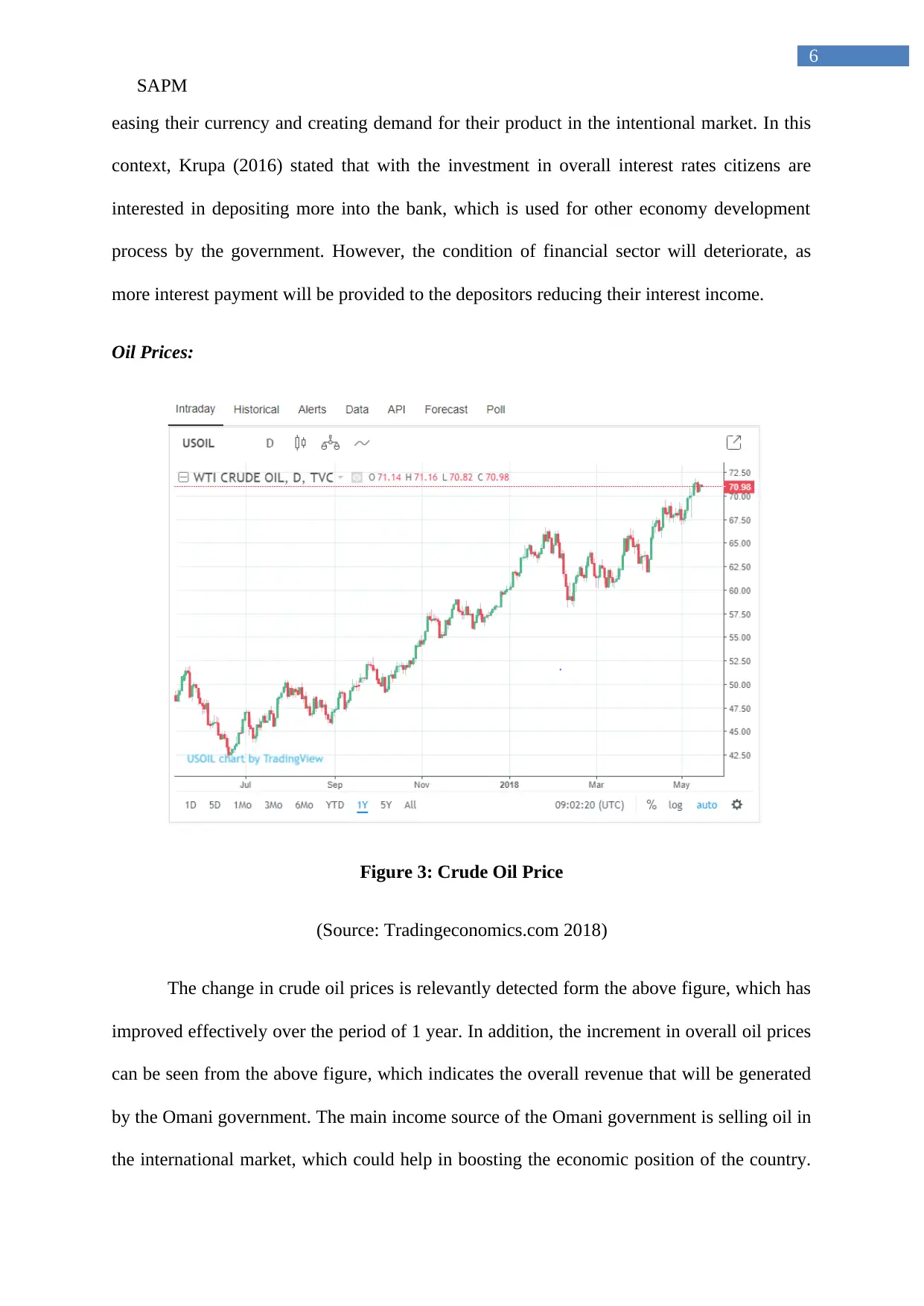

Oil Prices:

Figure 3: Crude Oil Price

(Source: Tradingeconomics.com 2018)

The change in crude oil prices is relevantly detected form the above figure, which has

improved effectively over the period of 1 year. In addition, the increment in overall oil prices

can be seen from the above figure, which indicates the overall revenue that will be generated

by the Omani government. The main income source of the Omani government is selling oil in

the international market, which could help in boosting the economic position of the country.

6

easing their currency and creating demand for their product in the intentional market. In this

context, Krupa (2016) stated that with the investment in overall interest rates citizens are

interested in depositing more into the bank, which is used for other economy development

process by the government. However, the condition of financial sector will deteriorate, as

more interest payment will be provided to the depositors reducing their interest income.

Oil Prices:

Figure 3: Crude Oil Price

(Source: Tradingeconomics.com 2018)

The change in crude oil prices is relevantly detected form the above figure, which has

improved effectively over the period of 1 year. In addition, the increment in overall oil prices

can be seen from the above figure, which indicates the overall revenue that will be generated

by the Omani government. The main income source of the Omani government is selling oil in

the international market, which could help in boosting the economic position of the country.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SAPM

7

The crude oil price in the international market has relevantly increased over time, which

indicates the high level of income generated by the government. This could be used in

infrastructure and capital expenditure, which is being conducted by the country. This positive

trend in the oil market relevantly indicates the uptrend in the oil market, which could allow

the Omani government to maximise their profit from operations. Therefore, the positive

attributes of the Omani economy can be anticipated from the overall evaluation of the oil

prices, interest rates and GDP of the country (Sullivan and Mackenzie 2017).

Industry Analysis:

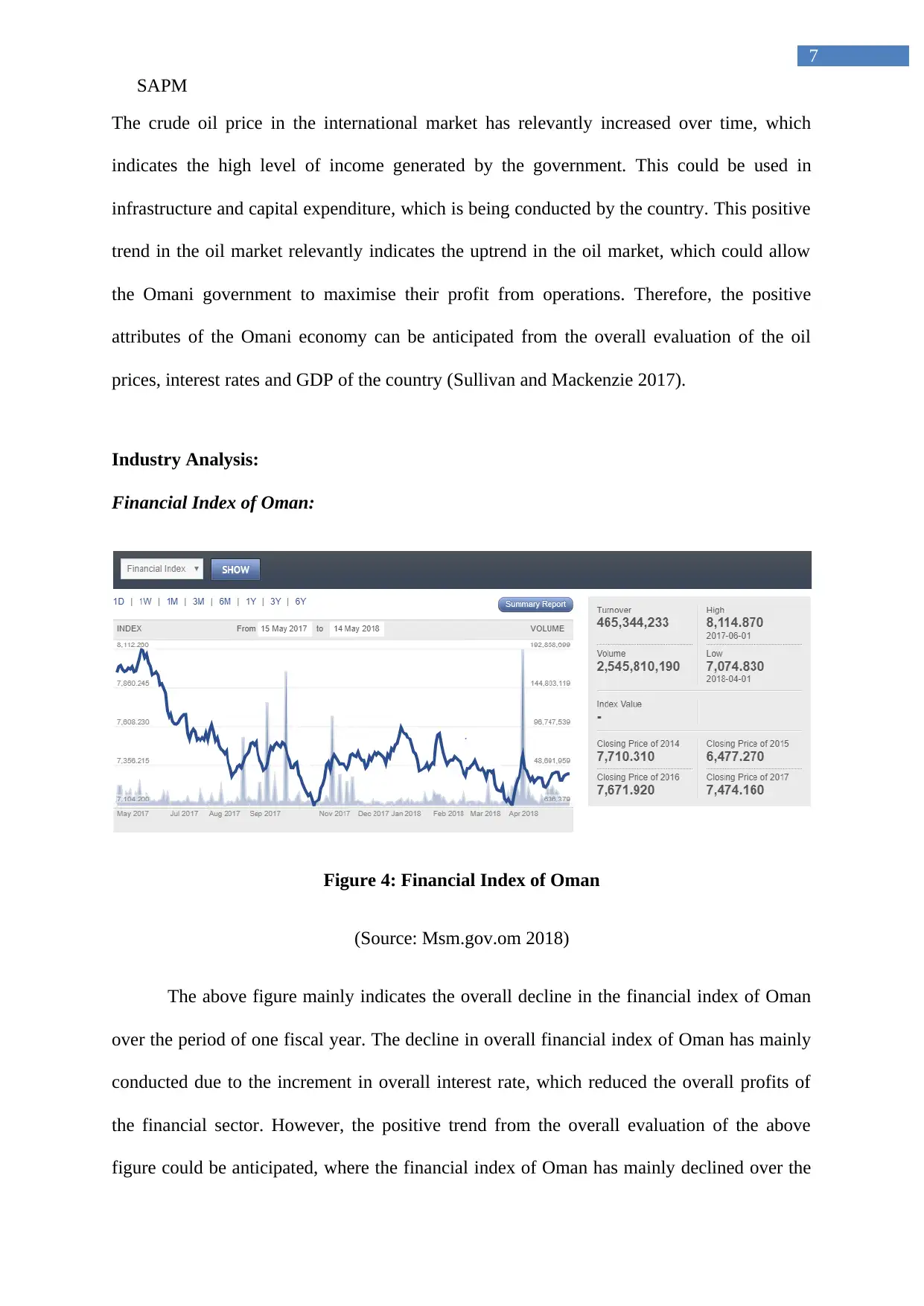

Financial Index of Oman:

Figure 4: Financial Index of Oman

(Source: Msm.gov.om 2018)

The above figure mainly indicates the overall decline in the financial index of Oman

over the period of one fiscal year. The decline in overall financial index of Oman has mainly

conducted due to the increment in overall interest rate, which reduced the overall profits of

the financial sector. However, the positive trend from the overall evaluation of the above

figure could be anticipated, where the financial index of Oman has mainly declined over the

7

The crude oil price in the international market has relevantly increased over time, which

indicates the high level of income generated by the government. This could be used in

infrastructure and capital expenditure, which is being conducted by the country. This positive

trend in the oil market relevantly indicates the uptrend in the oil market, which could allow

the Omani government to maximise their profit from operations. Therefore, the positive

attributes of the Omani economy can be anticipated from the overall evaluation of the oil

prices, interest rates and GDP of the country (Sullivan and Mackenzie 2017).

Industry Analysis:

Financial Index of Oman:

Figure 4: Financial Index of Oman

(Source: Msm.gov.om 2018)

The above figure mainly indicates the overall decline in the financial index of Oman

over the period of one fiscal year. The decline in overall financial index of Oman has mainly

conducted due to the increment in overall interest rate, which reduced the overall profits of

the financial sector. However, the positive trend from the overall evaluation of the above

figure could be anticipated, where the financial index of Oman has mainly declined over the

SAPM

8

period. Koo (2017) stated the continuous decline in share price of the organisation mainly

indicates a downtrend in the market, which will have negative impact on financial revenue

generation capability of the investors. Moreover, the financial sector index of the country has

directly shown the possibility of stagnation in the market, while no further decline in prices is

seen. This indicates the positive attribute of the financial sector, which could allow investor

in maximining profits from investment.

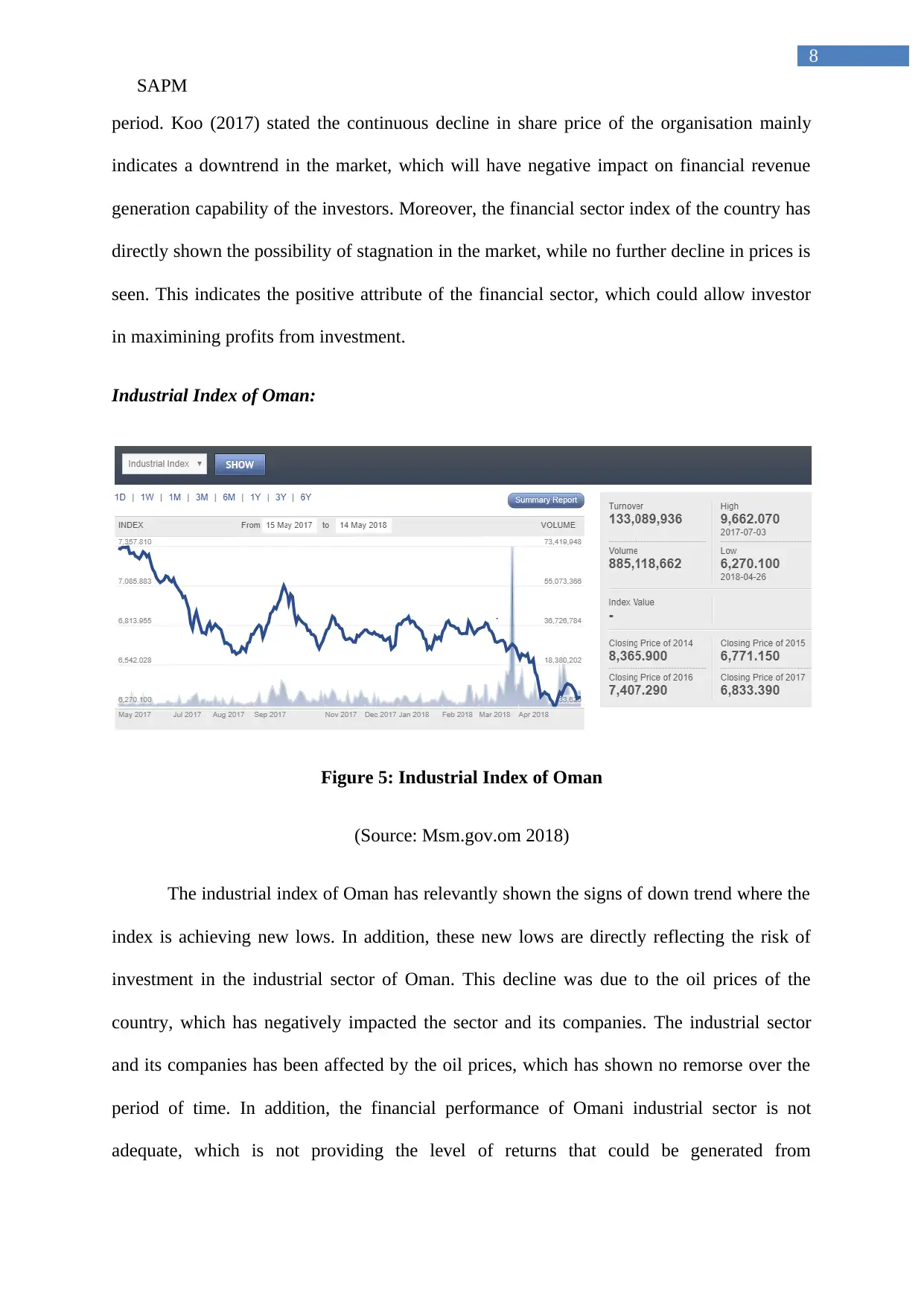

Industrial Index of Oman:

Figure 5: Industrial Index of Oman

(Source: Msm.gov.om 2018)

The industrial index of Oman has relevantly shown the signs of down trend where the

index is achieving new lows. In addition, these new lows are directly reflecting the risk of

investment in the industrial sector of Oman. This decline was due to the oil prices of the

country, which has negatively impacted the sector and its companies. The industrial sector

and its companies has been affected by the oil prices, which has shown no remorse over the

period of time. In addition, the financial performance of Omani industrial sector is not

adequate, which is not providing the level of returns that could be generated from

8

period. Koo (2017) stated the continuous decline in share price of the organisation mainly

indicates a downtrend in the market, which will have negative impact on financial revenue

generation capability of the investors. Moreover, the financial sector index of the country has

directly shown the possibility of stagnation in the market, while no further decline in prices is

seen. This indicates the positive attribute of the financial sector, which could allow investor

in maximining profits from investment.

Industrial Index of Oman:

Figure 5: Industrial Index of Oman

(Source: Msm.gov.om 2018)

The industrial index of Oman has relevantly shown the signs of down trend where the

index is achieving new lows. In addition, these new lows are directly reflecting the risk of

investment in the industrial sector of Oman. This decline was due to the oil prices of the

country, which has negatively impacted the sector and its companies. The industrial sector

and its companies has been affected by the oil prices, which has shown no remorse over the

period of time. In addition, the financial performance of Omani industrial sector is not

adequate, which is not providing the level of returns that could be generated from

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

SAPM

9

investments, due to the continuous decline in the share price. Therefore, the investors should

ignore the investment scope in companies that are listed in the industrial sector of Oman.

Altuntas and Dereli (2015) stated that investor by using trend analysis is able to identify the

viability of the sector and estimate its overall progress in future.

Service Index of Oman:

Figure 6: Service Index of Oman

(Source: Msm.gov.om 2018)

The overall Service sector of Oman has relevantly shown progress, where the service

index has obtained new highs over the period of the analysis. This relevantly indicates the

overall progress, which has been obtained by the service sector. In addition, this also

indicates the positive attributes of investing in the service sector, which could help in

improving the level of profits that could be generated form investment. The slight upward

movement from Aug 2017 is seen in the above figure, which indicates a positive attribute for

the investors aims to maximise profits from their investments (Najeeb Bacha and Masih

2015).

9

investments, due to the continuous decline in the share price. Therefore, the investors should

ignore the investment scope in companies that are listed in the industrial sector of Oman.

Altuntas and Dereli (2015) stated that investor by using trend analysis is able to identify the

viability of the sector and estimate its overall progress in future.

Service Index of Oman:

Figure 6: Service Index of Oman

(Source: Msm.gov.om 2018)

The overall Service sector of Oman has relevantly shown progress, where the service

index has obtained new highs over the period of the analysis. This relevantly indicates the

overall progress, which has been obtained by the service sector. In addition, this also

indicates the positive attributes of investing in the service sector, which could help in

improving the level of profits that could be generated form investment. The slight upward

movement from Aug 2017 is seen in the above figure, which indicates a positive attribute for

the investors aims to maximise profits from their investments (Najeeb Bacha and Masih

2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SAPM

10

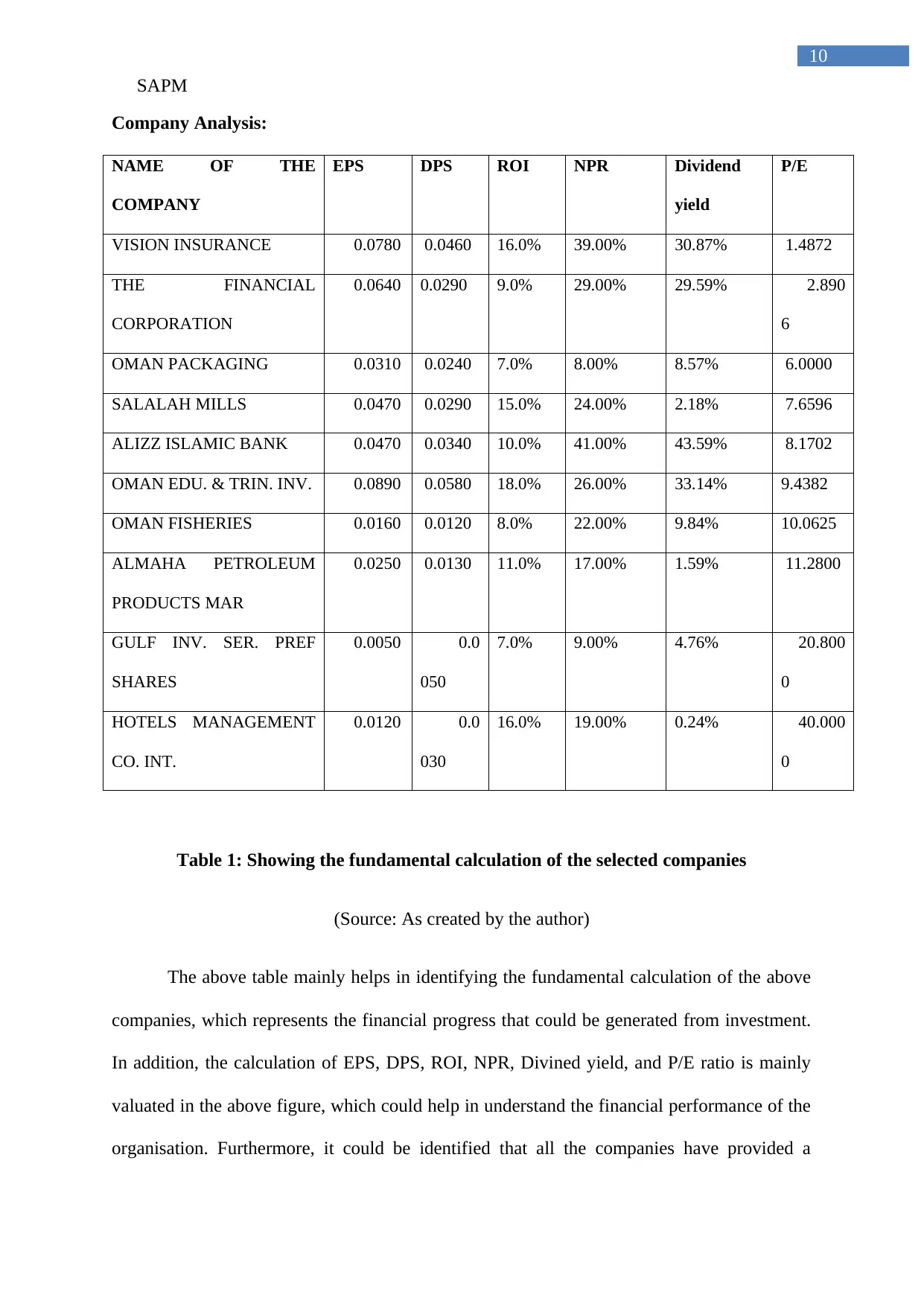

Company Analysis:

NAME OF THE

COMPANY

EPS DPS ROI NPR Dividend

yield

P/E

VISION INSURANCE 0.0780 0.0460 16.0% 39.00% 30.87% 1.4872

THE FINANCIAL

CORPORATION

0.0640 0.0290 9.0% 29.00% 29.59% 2.890

6

OMAN PACKAGING 0.0310 0.0240 7.0% 8.00% 8.57% 6.0000

SALALAH MILLS 0.0470 0.0290 15.0% 24.00% 2.18% 7.6596

ALIZZ ISLAMIC BANK 0.0470 0.0340 10.0% 41.00% 43.59% 8.1702

OMAN EDU. & TRIN. INV. 0.0890 0.0580 18.0% 26.00% 33.14% 9.4382

OMAN FISHERIES 0.0160 0.0120 8.0% 22.00% 9.84% 10.0625

ALMAHA PETROLEUM

PRODUCTS MAR

0.0250 0.0130 11.0% 17.00% 1.59% 11.2800

GULF INV. SER. PREF

SHARES

0.0050 0.0

050

7.0% 9.00% 4.76% 20.800

0

HOTELS MANAGEMENT

CO. INT.

0.0120 0.0

030

16.0% 19.00% 0.24% 40.000

0

Table 1: Showing the fundamental calculation of the selected companies

(Source: As created by the author)

The above table mainly helps in identifying the fundamental calculation of the above

companies, which represents the financial progress that could be generated from investment.

In addition, the calculation of EPS, DPS, ROI, NPR, Divined yield, and P/E ratio is mainly

valuated in the above figure, which could help in understand the financial performance of the

organisation. Furthermore, it could be identified that all the companies have provided a

10

Company Analysis:

NAME OF THE

COMPANY

EPS DPS ROI NPR Dividend

yield

P/E

VISION INSURANCE 0.0780 0.0460 16.0% 39.00% 30.87% 1.4872

THE FINANCIAL

CORPORATION

0.0640 0.0290 9.0% 29.00% 29.59% 2.890

6

OMAN PACKAGING 0.0310 0.0240 7.0% 8.00% 8.57% 6.0000

SALALAH MILLS 0.0470 0.0290 15.0% 24.00% 2.18% 7.6596

ALIZZ ISLAMIC BANK 0.0470 0.0340 10.0% 41.00% 43.59% 8.1702

OMAN EDU. & TRIN. INV. 0.0890 0.0580 18.0% 26.00% 33.14% 9.4382

OMAN FISHERIES 0.0160 0.0120 8.0% 22.00% 9.84% 10.0625

ALMAHA PETROLEUM

PRODUCTS MAR

0.0250 0.0130 11.0% 17.00% 1.59% 11.2800

GULF INV. SER. PREF

SHARES

0.0050 0.0

050

7.0% 9.00% 4.76% 20.800

0

HOTELS MANAGEMENT

CO. INT.

0.0120 0.0

030

16.0% 19.00% 0.24% 40.000

0

Table 1: Showing the fundamental calculation of the selected companies

(Source: As created by the author)

The above table mainly helps in identifying the fundamental calculation of the above

companies, which represents the financial progress that could be generated from investment.

In addition, the calculation of EPS, DPS, ROI, NPR, Divined yield, and P/E ratio is mainly

valuated in the above figure, which could help in understand the financial performance of the

organisation. Furthermore, it could be identified that all the companies have provided a

SAPM

11

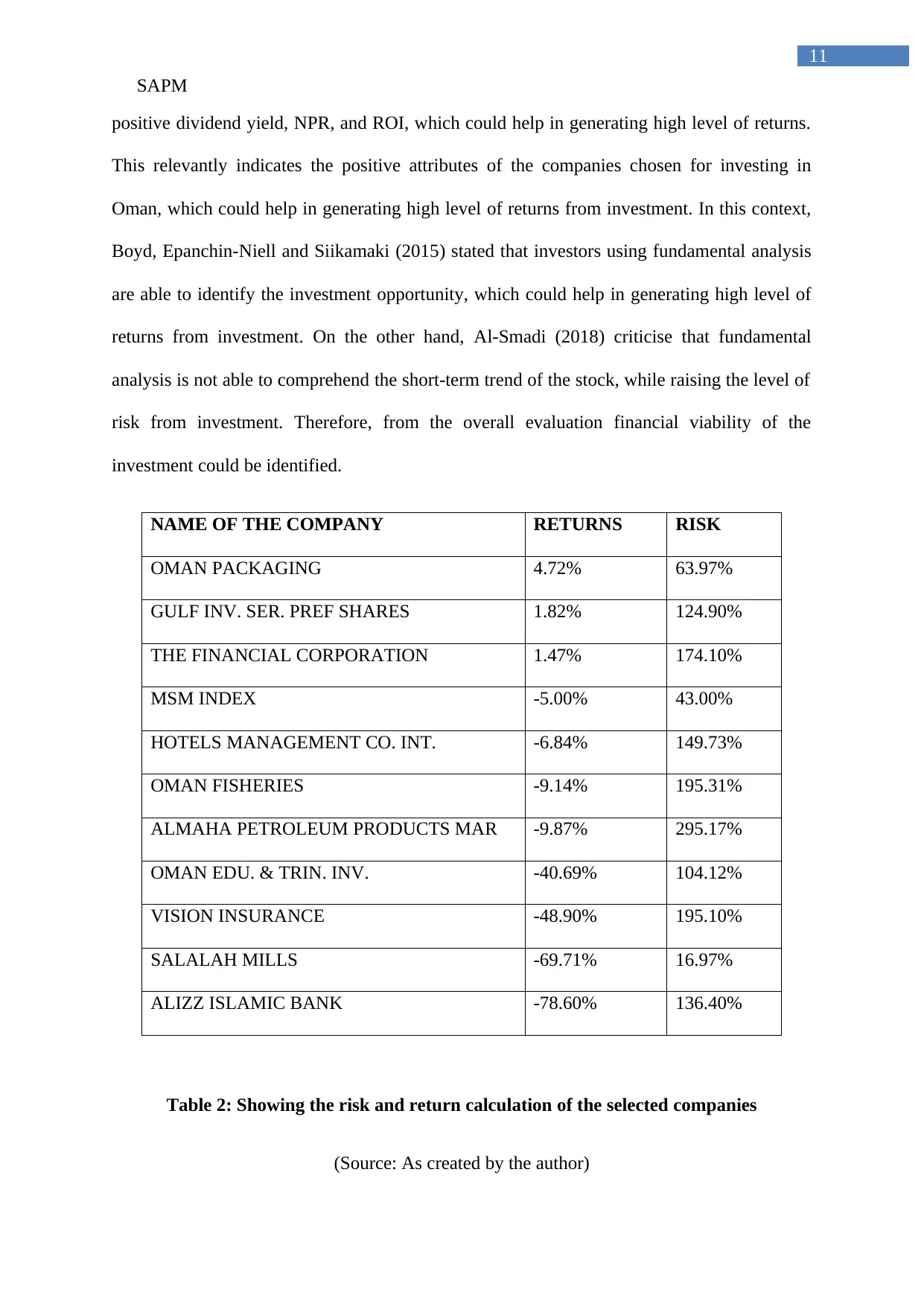

positive dividend yield, NPR, and ROI, which could help in generating high level of returns.

This relevantly indicates the positive attributes of the companies chosen for investing in

Oman, which could help in generating high level of returns from investment. In this context,

Boyd, Epanchin-Niell and Siikamaki (2015) stated that investors using fundamental analysis

are able to identify the investment opportunity, which could help in generating high level of

returns from investment. On the other hand, Al-Smadi (2018) criticise that fundamental

analysis is not able to comprehend the short-term trend of the stock, while raising the level of

risk from investment. Therefore, from the overall evaluation financial viability of the

investment could be identified.

NAME OF THE COMPANY RETURNS RISK

OMAN PACKAGING 4.72% 63.97%

GULF INV. SER. PREF SHARES 1.82% 124.90%

THE FINANCIAL CORPORATION 1.47% 174.10%

MSM INDEX -5.00% 43.00%

HOTELS MANAGEMENT CO. INT. -6.84% 149.73%

OMAN FISHERIES -9.14% 195.31%

ALMAHA PETROLEUM PRODUCTS MAR -9.87% 295.17%

OMAN EDU. & TRIN. INV. -40.69% 104.12%

VISION INSURANCE -48.90% 195.10%

SALALAH MILLS -69.71% 16.97%

ALIZZ ISLAMIC BANK -78.60% 136.40%

Table 2: Showing the risk and return calculation of the selected companies

(Source: As created by the author)

11

positive dividend yield, NPR, and ROI, which could help in generating high level of returns.

This relevantly indicates the positive attributes of the companies chosen for investing in

Oman, which could help in generating high level of returns from investment. In this context,

Boyd, Epanchin-Niell and Siikamaki (2015) stated that investors using fundamental analysis

are able to identify the investment opportunity, which could help in generating high level of

returns from investment. On the other hand, Al-Smadi (2018) criticise that fundamental

analysis is not able to comprehend the short-term trend of the stock, while raising the level of

risk from investment. Therefore, from the overall evaluation financial viability of the

investment could be identified.

NAME OF THE COMPANY RETURNS RISK

OMAN PACKAGING 4.72% 63.97%

GULF INV. SER. PREF SHARES 1.82% 124.90%

THE FINANCIAL CORPORATION 1.47% 174.10%

MSM INDEX -5.00% 43.00%

HOTELS MANAGEMENT CO. INT. -6.84% 149.73%

OMAN FISHERIES -9.14% 195.31%

ALMAHA PETROLEUM PRODUCTS MAR -9.87% 295.17%

OMAN EDU. & TRIN. INV. -40.69% 104.12%

VISION INSURANCE -48.90% 195.10%

SALALAH MILLS -69.71% 16.97%

ALIZZ ISLAMIC BANK -78.60% 136.40%

Table 2: Showing the risk and return calculation of the selected companies

(Source: As created by the author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.